- Auditing & assurance. Introduction to course

Содержание

- 2. Introduction to Course What is an Audit? What is the purpose of an audit? Why study

- 3. Examples of ‘Audits’ Financial Statement Audit Environmental Audit Medical Audit Forensic Audit Technology audits Teaching audits

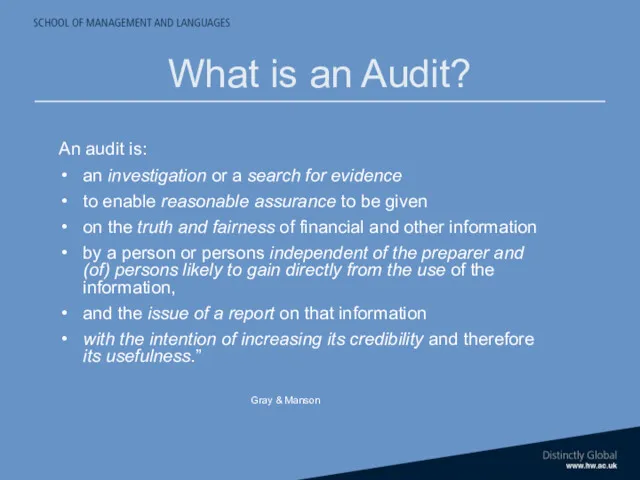

- 4. What is an Audit? An audit is: an investigation or a search for evidence to enable

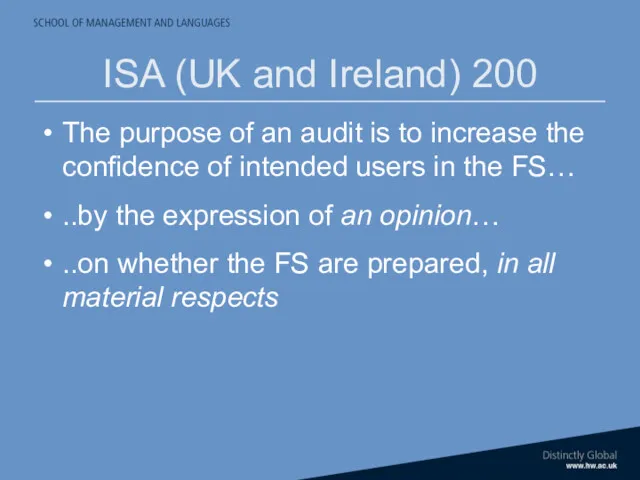

- 5. ISA (UK and Ireland) 200 The purpose of an audit is to increase the confidence of

- 6. ISA 200 para 7 The ISAs require that the auditor exercise professional judgment and maintain professional

- 7. Justifications for Audit Agency Theory Information Hypothesis Insurance Hypothesis

- 8. Agency theory basic ideas Both the owners (principals) of organisation and the managers (agents) employed to

- 9. Information & Insurance Hypotheses An insurance policy over the accuracy of the accounts

- 10. Reasonable Assurance The auditor does not guarantee that the accounts are 100% correct. The auditor provides

- 11. Truth & Fairness Stated in the auditor’s opinion that the financial statements are ‘true and fair’.

- 12. Audit Process Preliminary Stages (Client acceptance & Planning) Systems work and transaction testing Preparation for final

- 13. Why Study Auditing?

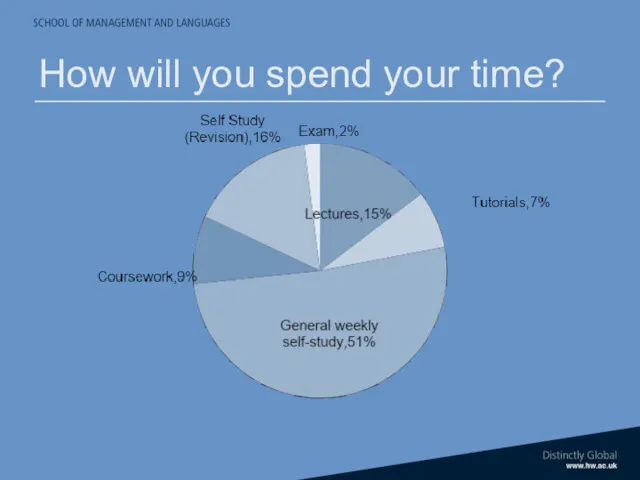

- 16. How will you spend your time?

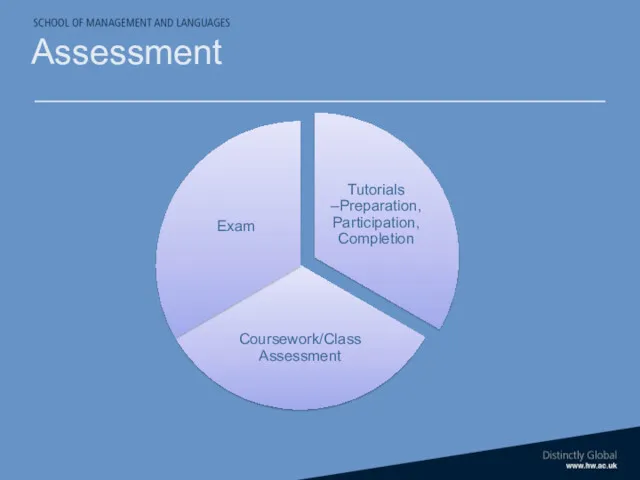

- 17. Assessment

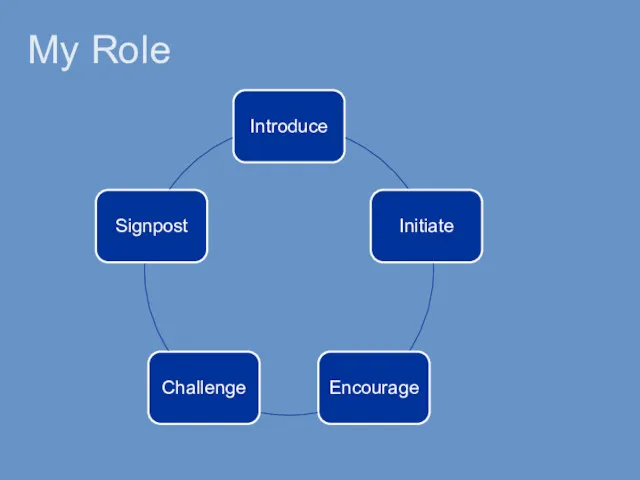

- 18. My Role

- 19. Practical Issues Sign up for tutorial groups Start thinking about Coursework

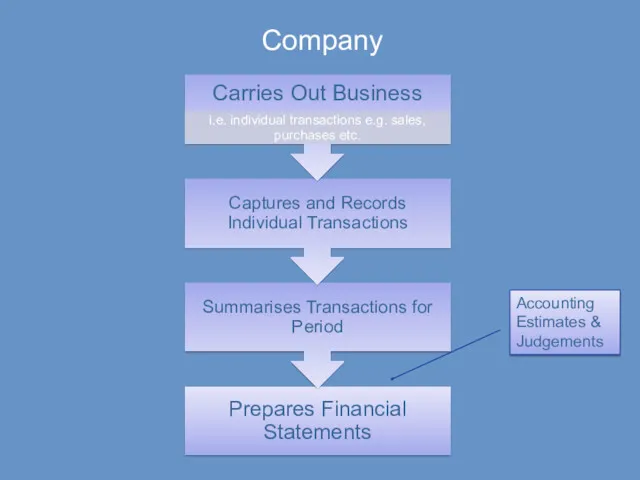

- 20. Company Accounting Estimates & Judgements

- 21. Assertions in Financial Statements Financial Statements issued by management contain explicit and implicit assertions e.g. Inventory

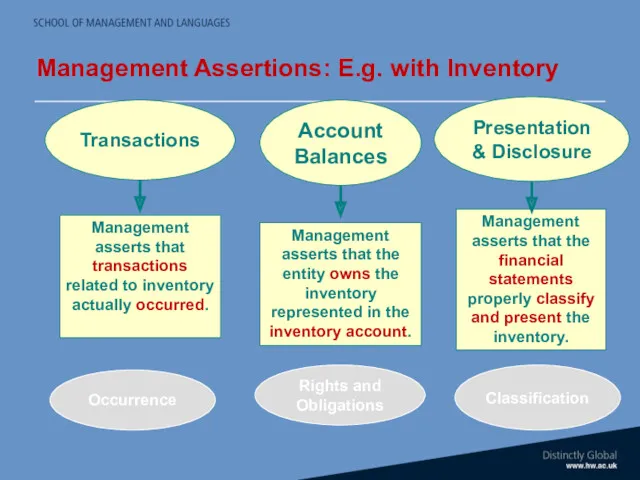

- 22. Management Assertions: E.g. with Inventory Occurrence Rights and Obligations Classification

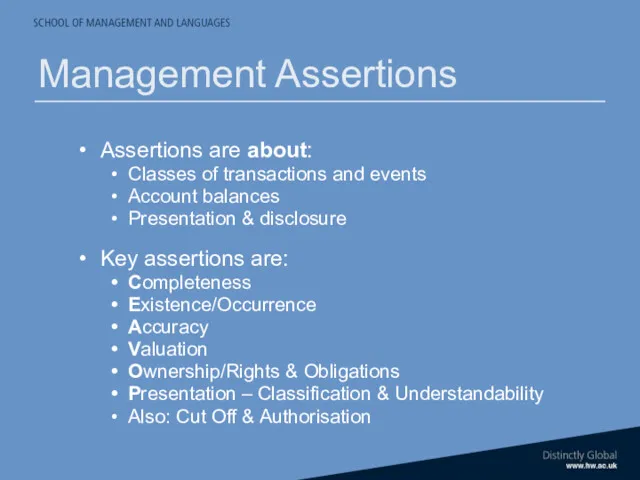

- 23. Assertions are about: Classes of transactions and events Account balances Presentation & disclosure Key assertions are:

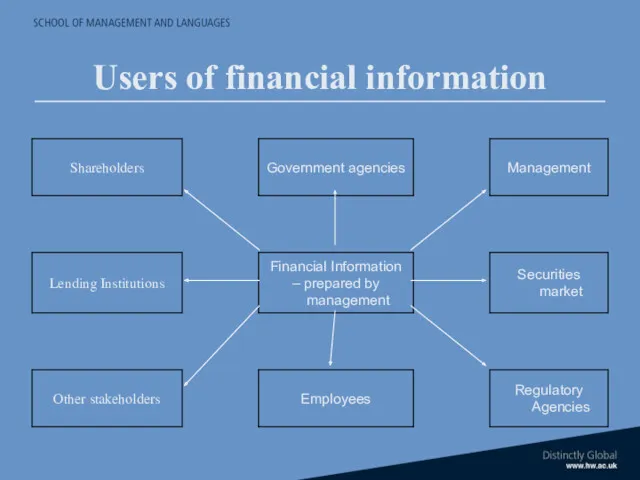

- 24. Users of financial information

- 25. Why need audit? Conflict of Interest Remoteness Complexity Public Interest Public Trust

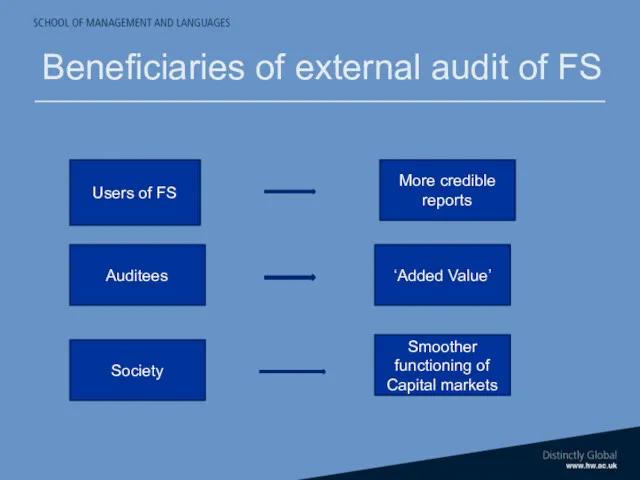

- 26. Beneficiaries of external audit of FS Users of FS More credible reports ‘Added Value’ Auditees Smoother

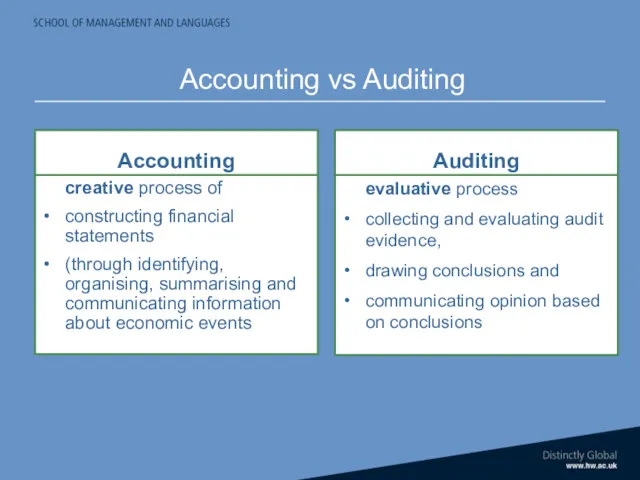

- 27. Accounting creative process of constructing financial statements (through identifying, organising, summarising and communicating information about economic

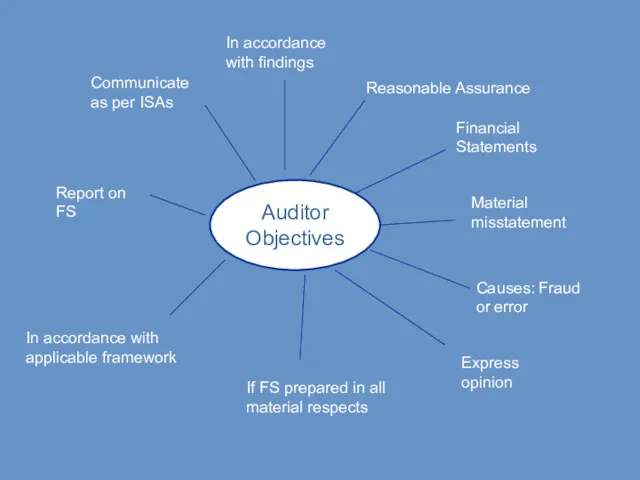

- 28. Auditor Objectives Reasonable Assurance Financial Statements Material misstatement Causes: Fraud or error Express opinion If FS

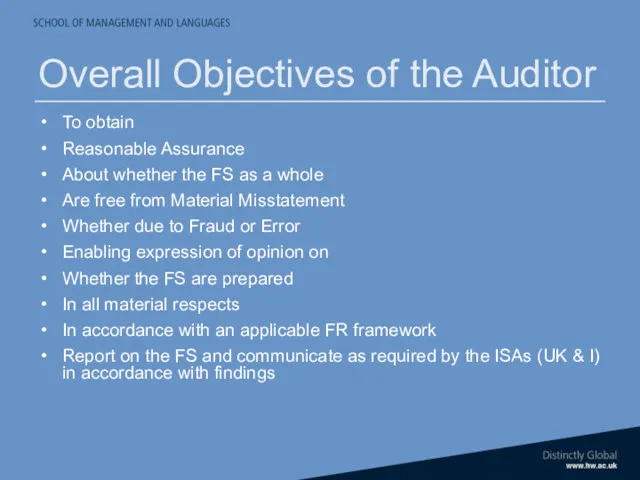

- 29. Overall Objectives of the Auditor To obtain Reasonable Assurance About whether the FS as a whole

- 30. Key Audit Terms Fill in the Blanks Ask for explanations of any words you don’t understand

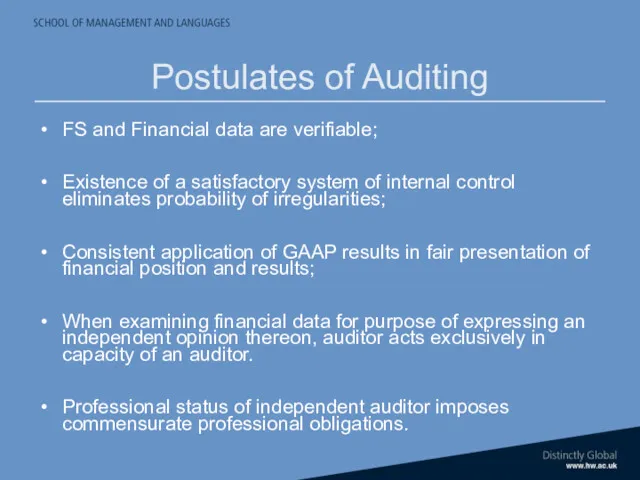

- 31. Postulates of Auditing FS and Financial data are verifiable; Existence of a satisfactory system of internal

- 33. Скачать презентацию

Introduction to Course

What is an Audit?

What is the purpose of an

Introduction to Course

What is an Audit?

What is the purpose of an

Examples of ‘Audits’

Financial Statement Audit

Environmental Audit

Medical Audit

Forensic Audit

Technology audits

Teaching

Examples of ‘Audits’

Financial Statement Audit

Environmental Audit

Medical Audit

Forensic Audit

Technology audits

Teaching

What is an Audit?

An audit is:

an investigation or a search for

What is an Audit?

An audit is:

an investigation or a search for

ISA (UK and Ireland) 200

The purpose of an audit is to

ISA (UK and Ireland) 200

The purpose of an audit is to

ISA 200 para 7

The ISAs require that the auditor exercise professional

ISA 200 para 7

The ISAs require that the auditor exercise professional

Justifications for Audit

Agency Theory

Information Hypothesis

Insurance Hypothesis

Justifications for Audit

Agency Theory

Information Hypothesis

Insurance Hypothesis

Agency theory basic ideas

Both the owners (principals) of organisation and the

Agency theory basic ideas

Both the owners (principals) of organisation and the

Information & Insurance Hypotheses

An insurance policy over the accuracy of the

Information & Insurance Hypotheses

An insurance policy over the accuracy of the

Reasonable Assurance

The auditor does not guarantee that the accounts are 100%

Reasonable Assurance

The auditor does not guarantee that the accounts are 100%

Truth & Fairness

Stated in the auditor’s opinion that the financial statements

Truth & Fairness

Stated in the auditor’s opinion that the financial statements

Audit Process

Preliminary Stages (Client acceptance & Planning)

Systems work and transaction testing

Preparation

Audit Process

Preliminary Stages (Client acceptance & Planning)

Systems work and transaction testing

Preparation

Why Study Auditing?

Why Study Auditing?

How will you spend your time?

How will you spend your time?

Assessment

Assessment

My Role

My Role

Practical Issues

Sign up for tutorial groups

Start thinking about Coursework

Practical Issues

Sign up for tutorial groups

Start thinking about Coursework

Company

Accounting Estimates & Judgements

Company

Accounting Estimates & Judgements

Assertions in Financial Statements

Financial Statements issued by management contain explicit and

Assertions in Financial Statements

Financial Statements issued by management contain explicit and

Management Assertions: E.g. with Inventory

Occurrence

Rights and Obligations

Classification

Management Assertions: E.g. with Inventory

Occurrence

Rights and Obligations

Classification

Assertions are about:

Classes of transactions and events

Account balances

Presentation & disclosure

Key assertions

Classes of transactions and events

Account balances

Presentation & disclosure

Key assertions

Users of financial information

Users of financial information

Why need audit?

Conflict of Interest

Remoteness

Complexity

Public Interest

Public Trust

Why need audit?

Conflict of Interest

Remoteness

Complexity

Public Interest

Public Trust

Beneficiaries of external audit of FS

Users of FS

More credible reports

‘Added Value’

Auditees

Smoother

Beneficiaries of external audit of FS

Users of FS

More credible reports

‘Added Value’

Auditees

Smoother

Accounting

creative process of

constructing financial statements

(through identifying, organising, summarising and

Accounting

creative process of

constructing financial statements

(through identifying, organising, summarising and

Auditor

Objectives

Reasonable Assurance

Financial Statements

Material misstatement

Causes: Fraud or error

Express opinion

If FS prepared in

Auditor

Objectives

Reasonable Assurance

Financial Statements

Material misstatement

Causes: Fraud or error

Express opinion

If FS prepared in

Overall Objectives of the Auditor

To obtain

Reasonable Assurance

About whether the FS

Overall Objectives of the Auditor

To obtain

Reasonable Assurance

About whether the FS

Key Audit Terms

Fill in the Blanks

Ask for explanations of any words

Key Audit Terms

Fill in the Blanks

Ask for explanations of any words

Postulates of Auditing

FS and Financial data are verifiable;

Existence of a satisfactory

Postulates of Auditing

FS and Financial data are verifiable;

Existence of a satisfactory

Тайм-менеджмент

Тайм-менеджмент Logistika letecké dopravy

Logistika letecké dopravy Управление людьми. Управление человеческим капиталом. (Раздел 1.2)

Управление людьми. Управление человеческим капиталом. (Раздел 1.2) SWOT-анализ

SWOT-анализ Теории управления персоналом

Теории управления персоналом Восемь принципов менеджмента качества

Восемь принципов менеджмента качества Поиск работы

Поиск работы Объекты и субъекты сферы услуг

Объекты и субъекты сферы услуг Корпоративный имидж и репутация фирмы

Корпоративный имидж и репутация фирмы Закупочная логистика. Планирование закупок

Закупочная логистика. Планирование закупок Кадровое делопроизводство. (Лекция 1)

Кадровое делопроизводство. (Лекция 1) Стратегия управления репутацией компании

Стратегия управления репутацией компании Операционный сервис-менеджмент во фронт-офисах государственной корпорации Правительство для граждан

Операционный сервис-менеджмент во фронт-офисах государственной корпорации Правительство для граждан Мотивация розницы. Торговая сеть Перекресток

Мотивация розницы. Торговая сеть Перекресток Организация как функция управления

Организация как функция управления Ұйымның сыртқы ортасын бағалау және талдау. Ұйым қызымет атқаратын саладағы бәсекелестік күштер және олардың ұйымға әсері

Ұйымның сыртқы ортасын бағалау және талдау. Ұйым қызымет атқаратын саладағы бәсекелестік күштер және олардың ұйымға әсері Көшбасшылық

Көшбасшылық Инструменты и методы бережливого производства

Инструменты и методы бережливого производства Принципы управления

Принципы управления Понятие и сущность логистики. (Раздел 1.1)

Понятие и сущность логистики. (Раздел 1.1) Основные принципы современных систем менеджмента

Основные принципы современных систем менеджмента Управління інноваційною діяльністю

Управління інноваційною діяльністю Сутність планування та особливості його здійснення на підприємстві

Сутність планування та особливості його здійснення на підприємстві Функциональное моделирование систем. Методики: SADT - IDEF0, DFD, IDEF3

Функциональное моделирование систем. Методики: SADT - IDEF0, DFD, IDEF3 DHL – международная логистическая компания

DHL – международная логистическая компания HSJ Chapter 5. Business-Level Strategy

HSJ Chapter 5. Business-Level Strategy Начала менеджмента. Менеджмент и менеджеры

Начала менеджмента. Менеджмент и менеджеры Функции менеджмента

Функции менеджмента