- Performance management. Target costing. (Topic 1)

Содержание

- 2. Exam guide Target costing may be examined in Section A multiple choice questions or it may

- 3. 1. What is target costing? Target costing involves setting a target cost for a product, having

- 4. 1. What is target costing? Target costing is most effective at the DESIGN stage and less

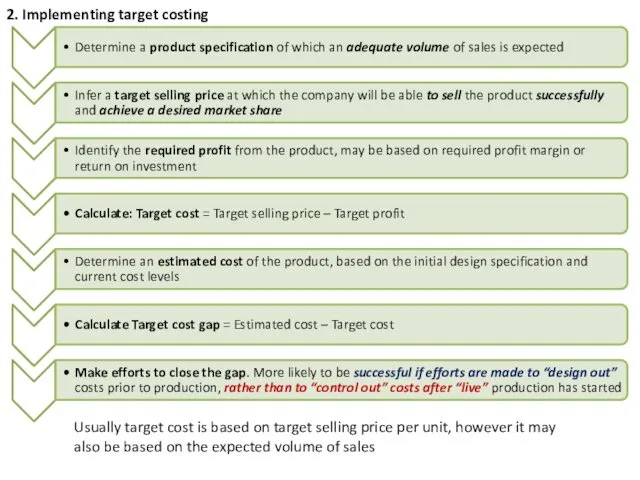

- 5. 2. Implementing target costing Usually target cost is based on target selling price per unit, however

- 6. 2. Implementing target costing – Case study Swedish retailer IKEA dominates the home furniture market in

- 7. 3. Deriving a target cost Example 1: A car manufacturer wants to calculate a target cost

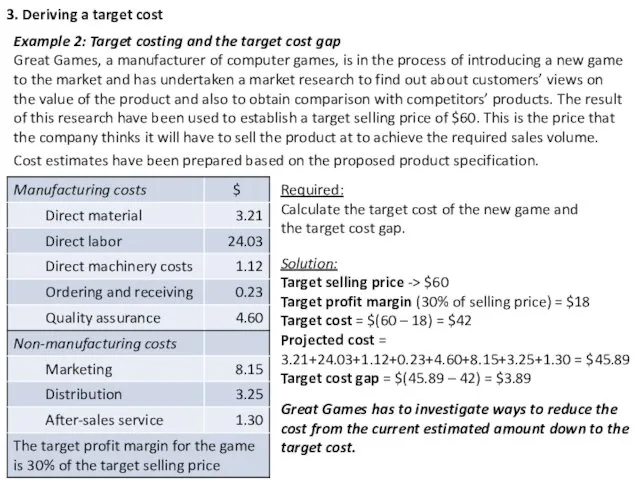

- 8. 3. Deriving a target cost Example 2: Target costing and the target cost gap Great Games,

- 9. 4. Closing a target cost gap Increasing the price will not close the cost gap. What

- 10. 4. Closing a target cost gap After you split the costs -> set benchmarks for improvement

- 11. 5. Target costing in service industries Examples of service businesses: Mass service eg banking, transportation (rail,

- 12. 5. Target costing in service industries Remind that: a target cost for a product is a

- 14. Скачать презентацию

Exam guide

Target costing may be examined in Section A multiple choice

Exam guide

Target costing may be examined in Section A multiple choice

1. What is target costing?

Target costing involves setting a target cost

1. What is target costing?

Target costing involves setting a target cost

1. What is target costing?

Target costing is most effective at the

1. What is target costing?

Target costing is most effective at the

2. Implementing target costing

Usually target cost is based on target selling

2. Implementing target costing

Usually target cost is based on target selling

2. Implementing target costing – Case study

Swedish retailer IKEA dominates the

2. Implementing target costing – Case study

Swedish retailer IKEA dominates the

3. Deriving a target cost

Example 1:

A car manufacturer wants to calculate

3. Deriving a target cost

Example 1:

A car manufacturer wants to calculate

3. Deriving a target cost

Example 2: Target costing and the target

3. Deriving a target cost

Example 2: Target costing and the target

4. Closing a target cost gap

Increasing the price will not close

4. Closing a target cost gap

Increasing the price will not close

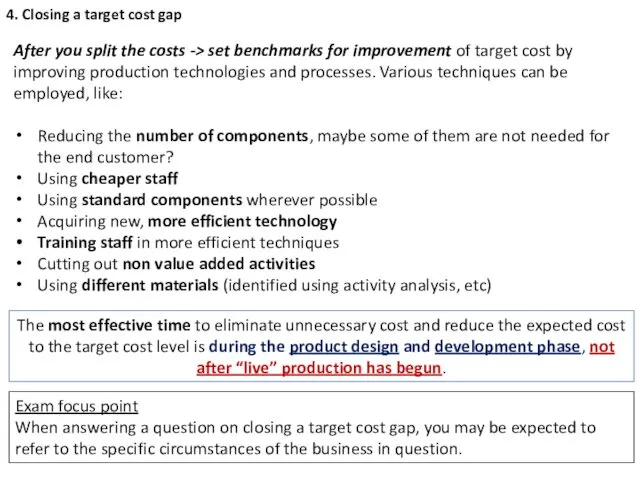

4. Closing a target cost gap

After you split the costs ->

4. Closing a target cost gap

After you split the costs ->

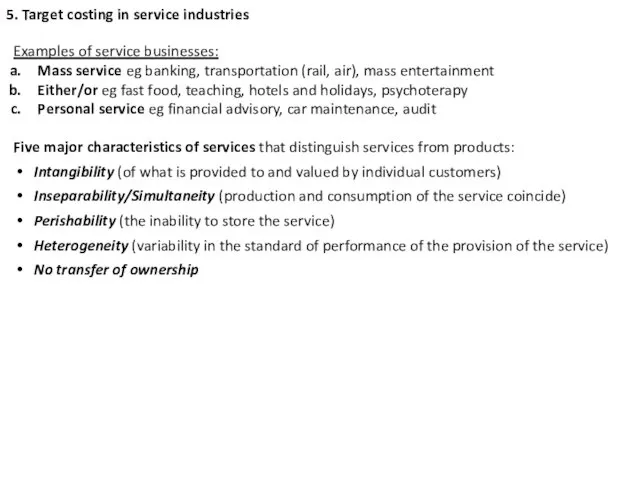

5. Target costing in service industries

Examples of service businesses:

Mass service eg

5. Target costing in service industries

Examples of service businesses:

Mass service eg

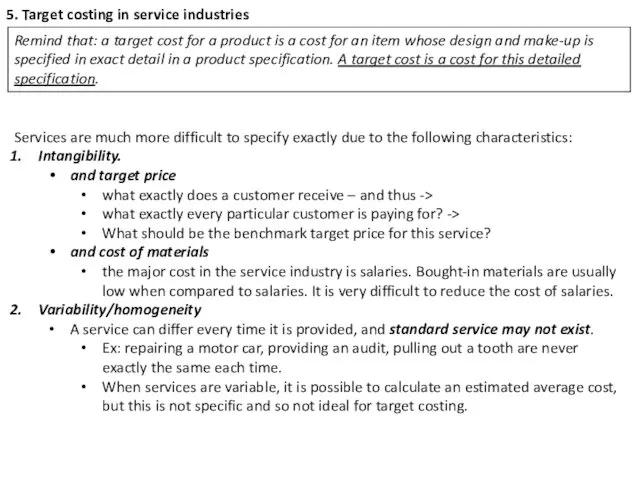

5. Target costing in service industries

Remind that: a target cost for

5. Target costing in service industries

Remind that: a target cost for

Деловое общение

Деловое общение Мониторинг рынка труда и позиционирование организации на рынке труда

Мониторинг рынка труда и позиционирование организации на рынке труда Бұйрық және оның түрлері

Бұйрық және оның түрлері Оценка эффективности управленческих решений. Ответственность за принятие управленческих решений

Оценка эффективности управленческих решений. Ответственность за принятие управленческих решений Мотивация в менеджменте. (Тема 8)

Мотивация в менеджменте. (Тема 8) Кеңсе меңгерушісі

Кеңсе меңгерушісі Контейнерная транспортная система

Контейнерная транспортная система Материальные ресурсы

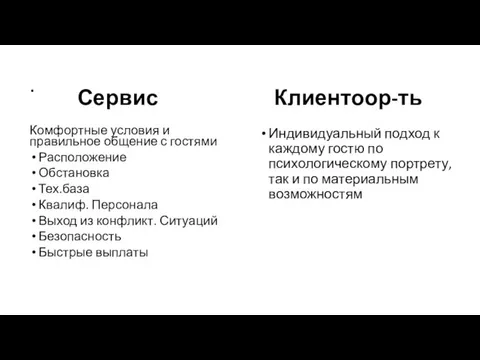

Материальные ресурсы Сервис клиентоор-ть. Правильное общение с гостями

Сервис клиентоор-ть. Правильное общение с гостями Закон синергии

Закон синергии Экономическая оценка трудового потенциала организации

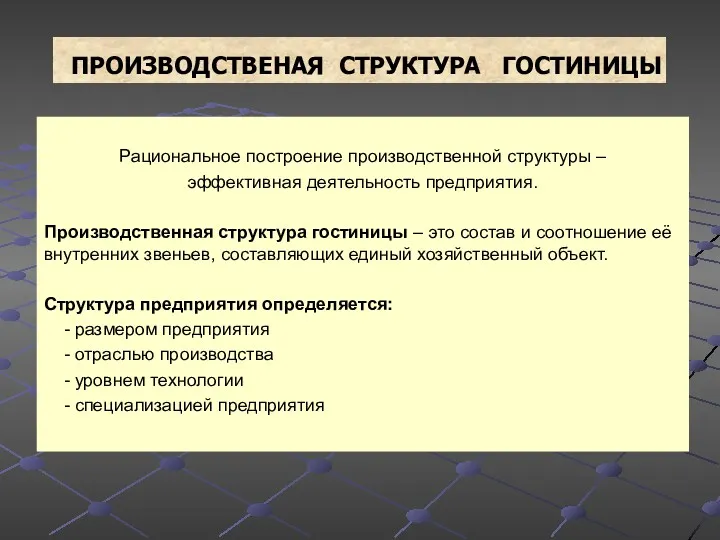

Экономическая оценка трудового потенциала организации Производственная структура гостиницы. (Лекция 5.3)

Производственная структура гостиницы. (Лекция 5.3) How can you become a better recruiter and get even paid for it?

How can you become a better recruiter and get even paid for it? Avon. Новая долгосрочная Программа поощрения для представителей

Avon. Новая долгосрочная Программа поощрения для представителей Корпоративная культура

Корпоративная культура Уникальный шанс. Лидер

Уникальный шанс. Лидер Organizacja i zarządzanie

Organizacja i zarządzanie Классификация управленческих решений

Классификация управленческих решений Профессия Менеджер по персоналу на рынке труда Самары

Профессия Менеджер по персоналу на рынке труда Самары Успешный руководитель

Успешный руководитель Отбор, наем и адаптация персонала

Отбор, наем и адаптация персонала Теоретические аспекты формирования системы управленческой отчетности

Теоретические аспекты формирования системы управленческой отчетности Совершенствование организации труда персонала (на примере ОАО Белгородские молочные продукты г. Белгород)

Совершенствование организации труда персонала (на примере ОАО Белгородские молочные продукты г. Белгород) Управление группой и формирование команды

Управление группой и формирование команды Рівні стратегічних рішень, типологія стратегій підприємства

Рівні стратегічних рішень, типологія стратегій підприємства Инновационный процесс и сущность управления инновационной деятельностью

Инновационный процесс и сущность управления инновационной деятельностью Основная цель компании

Основная цель компании Procesy informacyjne zarządzania w przedsiębiorstwie

Procesy informacyjne zarządzania w przedsiębiorstwie