- Risky business. Making decisions under uncertainty

Содержание

- 2. Overview Next unit up - Insurers Insurance theory & concepts Risk & uncertainty Insurance premiums Evolution

- 3. Risky Business: Making Decisions Under Uncertainty Uncertainty: A situation when more than one event may occur

- 4. Risk Defined Risk: The probability of incurring a loss (or some other misfortune). More precisely, risk

- 5. The Cost of Risk Some people are willing to bear more risk than others. In economics,

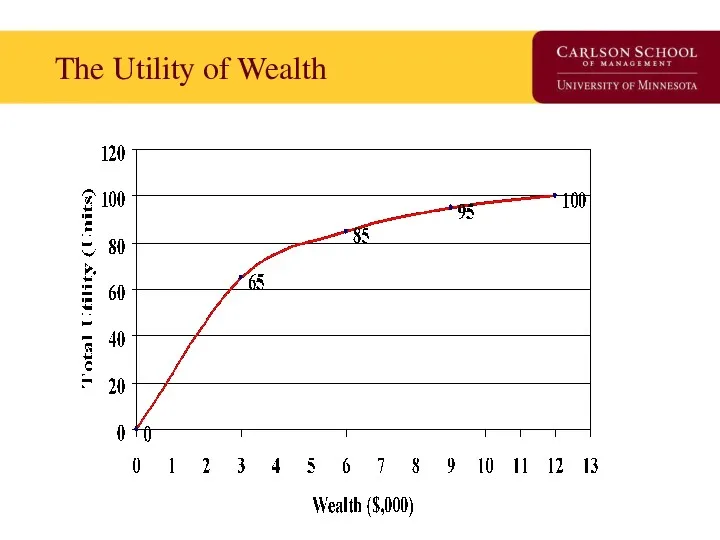

- 6. The Utility of Wealth

- 7. What can we observe from the Utility of Wealth Schedule? Utility increases as wealth increases. Change

- 8. Translate Utility of Wealth into Expected Utility Due to uncertainty, people do not know the actual

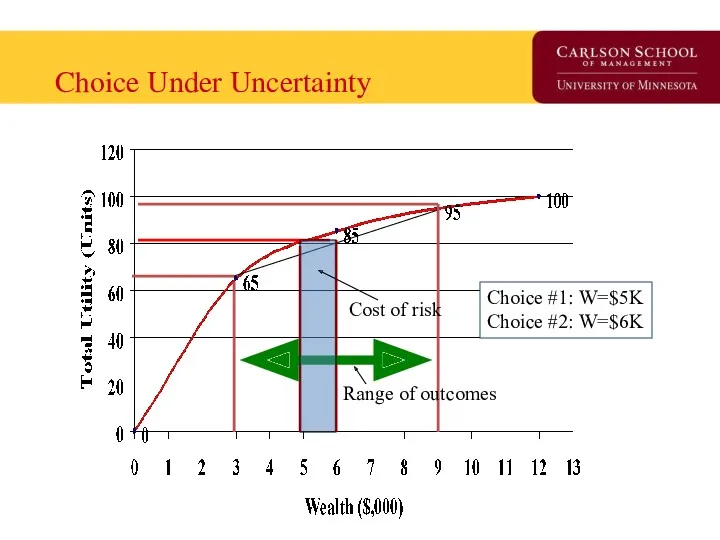

- 9. Choice Under Uncertainty Range of outcomes Cost of risk Choice #1: W=$5K Choice #2: W=$6K

- 10. Interpretation of Choice under Uncertainty At Choice #1, Tania’s wealth is $5K, U=80, no risk, At

- 11. Risk Aversion and Risk Neutrality Risk Averse: Someone who sees risk as not cost-less. The degree

- 12. Choice Under Uncertainty for Risk Neutral Person For Risk Neutral Person, Uncertainty is not an issue.

- 13. How do we reduce risk? Buy the ‘the cost of risk’ off. (similar to getting protection

- 14. How does Insurance work? Insurance works by ‘pooling’ risks. Insurance is possible and profitable because people

- 15. The Gains from Insurance Maximum value of Insurance Minimum cost of insurance Total Utility Wealth Range

- 16. Understanding the Graph At $10K, utility is 100. If one loses health (or a another valued

- 17. Understanding the Graph - 2 Up to what price will you buy insurance? What will insurance

- 18. Moral Hazard & Adverse Selection Private information is information that is available to one person but

- 19. Moral Hazard Defined: When one of two or more parities with an agreement has an incentive

- 20. Adverse Selection Defined: The tendency for people to enter into agreements in which they use private

- 21. Understanding the difference between the two People who face greater risks are more likely to purchase

- 22. How do insurance companies overcome these problems? Find a signal to convey information from outside the

- 23. Examine Evolution of a Market Using the “Time Machine” from Davey & Goliath

- 24. Slow Day? Starr got you down? Consider…. http://www.awn.com/heaven_and_hell/DG/DG4.htm

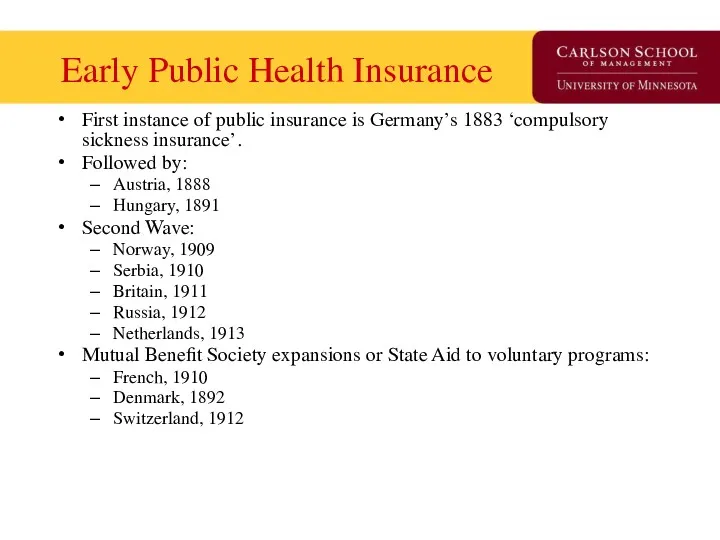

- 25. Early Public Health Insurance First instance of public insurance is Germany’s 1883 ‘compulsory sickness insurance’. Followed

- 26. U.S. Public Health Insurance Failed proposals made in Congress for National Health Insurance: 1918-19 1935-36 1948

- 27. Private Insurance – Two early models Fee-for-service insurance Epitomized by Blue Cross plan started for Baylor

- 28. Four characteristics of Blue Cross/Blue Shield fundamentally shaped American health care. Hospitals were reimbursed on a

- 29. Points of Inflection in Insurance Market -1 1930s – Great Depression reduces physician’s opposition to third

- 30. Points of Inflection in Insurance Market - 2 1983 – Medicare institutes prospective payment for hospital

- 31. State of Health Insurance Today Insurance models Demand side control programs Supply side control programs Market

- 32. Insurance Models in 2007 9% Conventional Fee for Service/Managed Indemnity Payment is based on a fee-schedule

- 33. 2013: ACA Accelerated HDHP - Distribution of Health Plan Enrollment for Covered Workers, by Plan Type,

- 34. Insurance Tower of Babel PPO: Preferred Provider Organization (Medica) IDS: Integrated Delivery System (Fairview) HMO: Health

- 35. CDHP Business Enablers ‘Ready to Lease’ Components of Health Insurance: Electronic claims processing National panel of

- 36. CDHP Component Details Health Tools and Resources Care management program Extensive easy-to-use information and services Health

- 37. …The HSA Model Health Coverage Purchased by ‘Qualified’ Plans Annual deductible Expenses beyond the HSA No

- 38. Demand Side Controls ‘Affect the consumer to mitigate moral hazard’ Coinsurance, Copayments, Deductibles Specialist access through

- 39. Supply Side Controls ‘Reduce the probability of provider induced demand’ Fee schedules Diagnosis Related Groups RBRVS

- 40. Insurance ‘Market Success’ Primary funding source of medical innovation in the United States. Consumers have more

- 41. Insurance ‘Market Failures’ 50+ million uninsured (at any point in time) prior to ACA 120% health

- 42. Average Annual Premiums for Single and Family Coverage, 1999-2013 * Estimate is statistically different from estimate

- 43. Question for Reflection How uniquely American is evolution of the insurance market in the 20th century?

- 44. The Uninsured Problem Who are the uninsured? Why is this a ‘market failure’? If government were

- 45. Who Are the Uninsured?

- 46. Types of Uninsured (Over 4 Years) From Pamela Farley Short and Deborah R. Graefe, 2003, Health

- 47. Geo-variation in the Uninsured

- 48. Does theory square with health insurance today? What is the purpose of insurance? How is modern

- 49. Insurance: In Theory Maximum value of Insurance Minimum cost of insurance Total Utility Wealth Range of

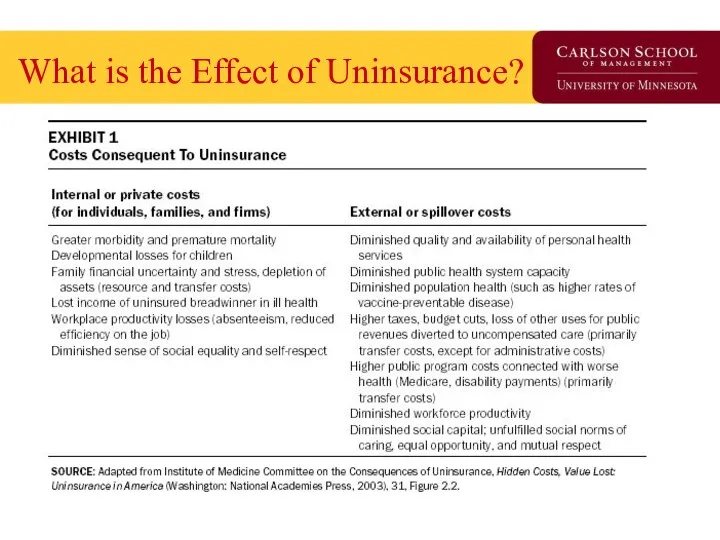

- 50. What is the Effect of Uninsurance?

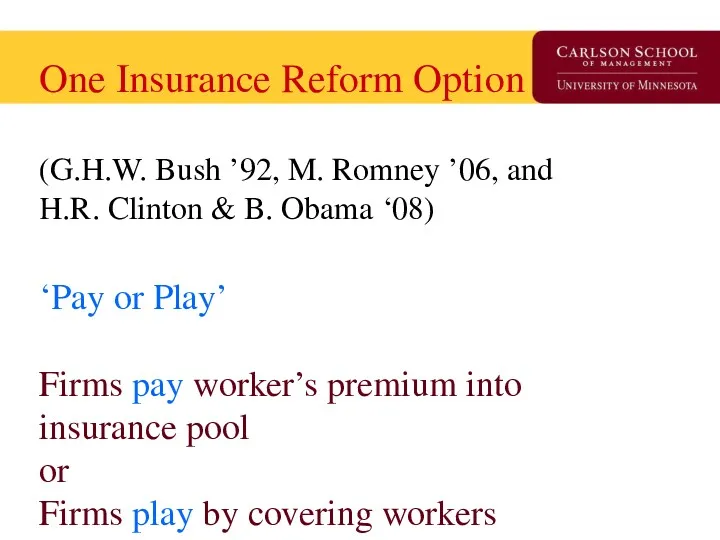

- 51. One Insurance Reform Option (G.H.W. Bush ’92, M. Romney ’06, and H.R. Clinton & B. Obama

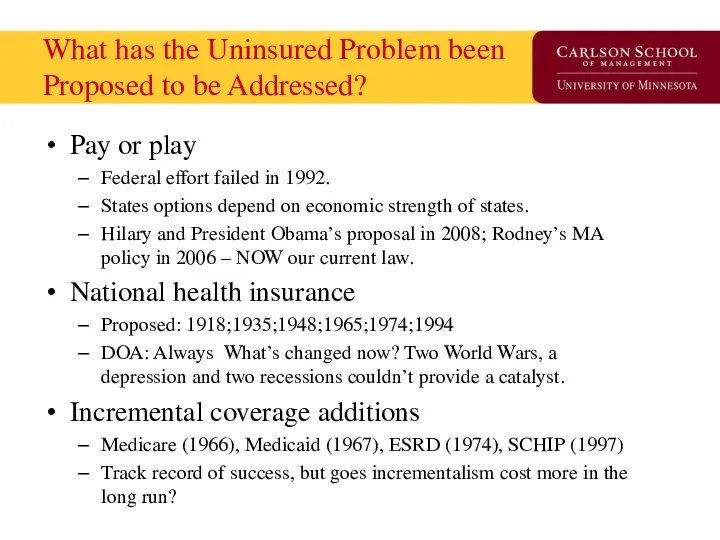

- 52. What has the Uninsured Problem been Proposed to be Addressed? Pay or play Federal effort failed

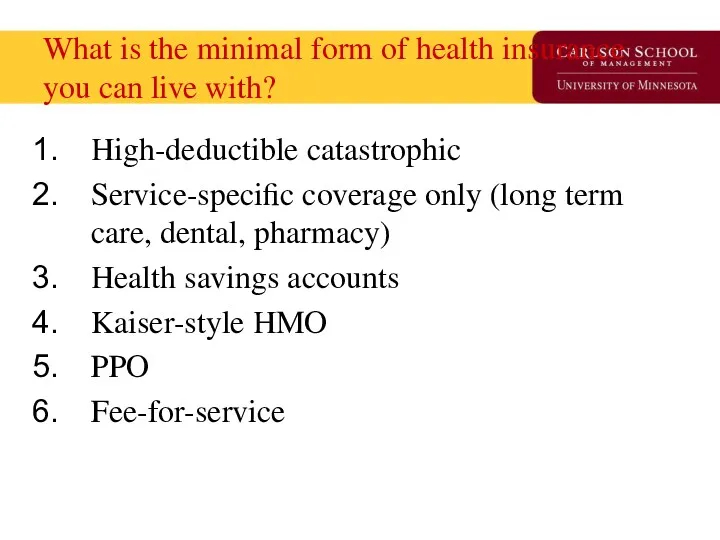

- 53. What is the minimal form of health insurance you can live with? High-deductible catastrophic Service-specific coverage

- 54. The Free-Rider Problem Free-rider is a person who consumes a good without paying for it. The

- 55. Break

- 56. Health Insurance Market Today Health Economist Health Reform Priors Current Law Overview Coverage and Financing Insurance

- 57. Priors as a Health Economist Health economists find that technology is both good for society and

- 58. Coverage and Financing Coverage: 32 of 54 million uninsured covered 24 million in Exchange 16 million

- 59. Insurance Market: 2010 Effective Immediately: Annual process set by HHS and States for premium rate review.

- 60. NAIC Health Reform Committees HHS is required to consult with the National Association of Insurance Commissioners

- 61. Insurance Market: 2011 Effective January 2011: 80% MLR for individual and small group, 85% MLR for

- 62. New Federal Health Reform Structure -2010 New “Office of Consumer Information and Insurance Oversight” established within

- 63. Exchanges: 2010 Effective July 2010: HHS with States to establish internet portal to identify coverage options.

- 64. Exchanges: 2014 Effective 2014: States to establish Exchange to facilitate comparison shopping, enrollment, and subsidy administration

- 65. Payment Reform & Care Coordination CMS Innovation Center: Created in 2011 to test and expand Medicare

- 66. National Impact of Health Reform Uninsured status is reduced by 59.8% (81% if base is US

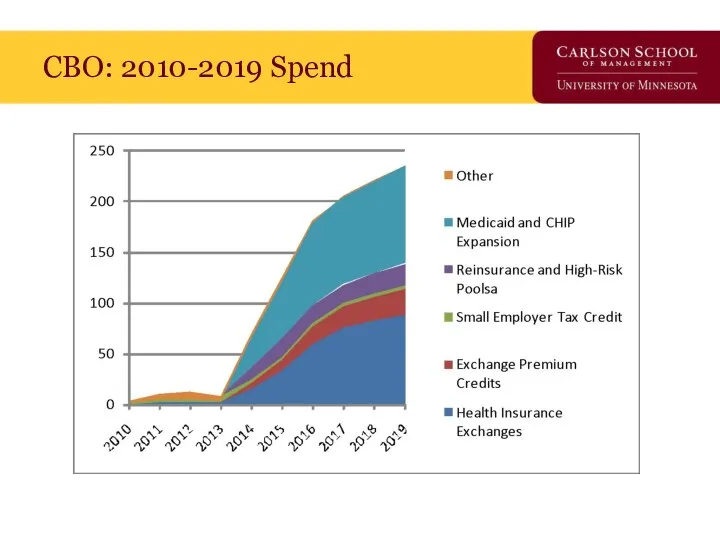

- 67. CBO: 2010-2019 Spend

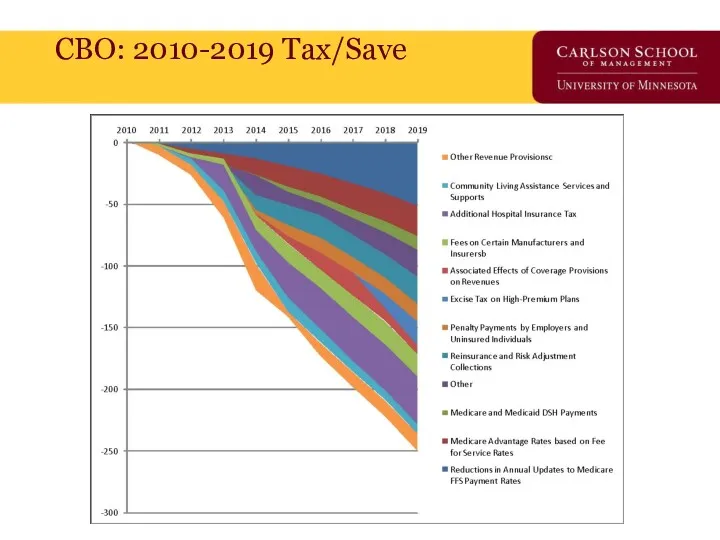

- 68. CBO: 2010-2019 Tax/Save

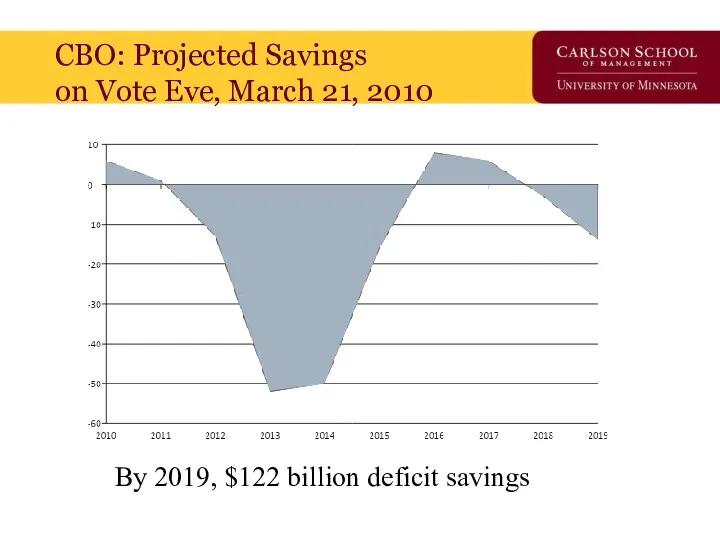

- 69. CBO: Projected Savings on Vote Eve, March 21, 2010 By 2019, $122 billion deficit savings

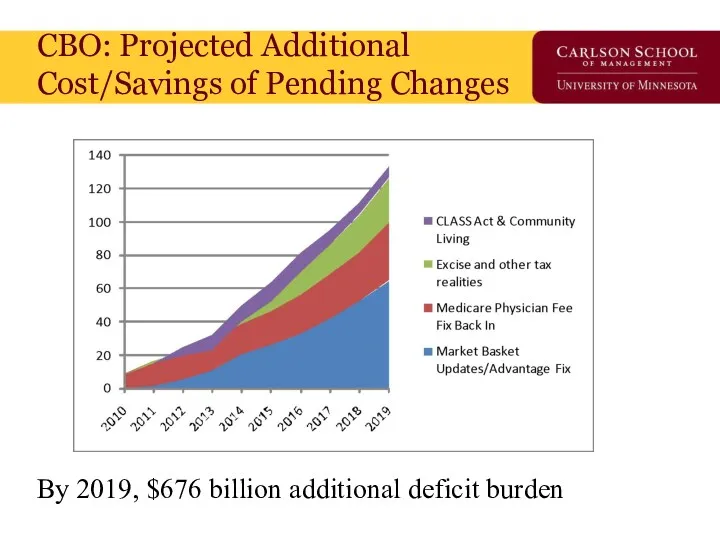

- 70. CBO: Projected Additional Cost/Savings of Pending Changes By 2019, $676 billion additional deficit burden

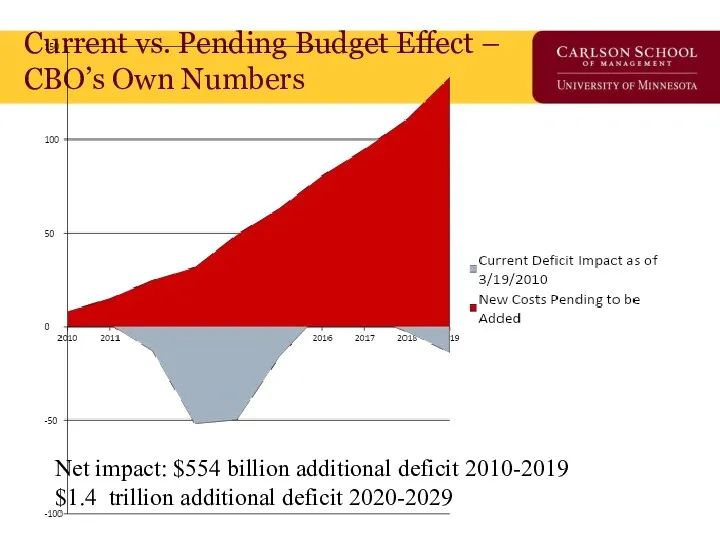

- 71. Current vs. Pending Budget Effect – CBO’s Own Numbers Net impact: $554 billion additional deficit 2010-2019

- 72. Train Wrecks Do Happen In DC But, to be fair, who’s train wreck is it?

- 73. Does this Look Familiar?

- 74. Or This?

- 75. Guess the Year? Guess the Authors?

- 76. Guess the Year? Guess the Authors?

- 77. Implementation Iceberg Cometh?

- 79. Even Friends can Wound if Implementation Poor

- 80. ACA Privacy Nightmare?

- 81. Not all data hacked – just the parts that let you create a fake credit card

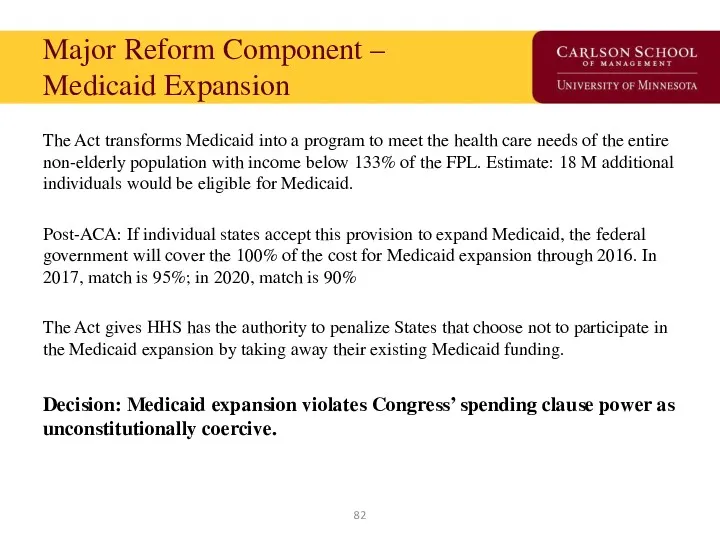

- 82. Major Reform Component – Medicaid Expansion The Act transforms Medicaid into a program to meet the

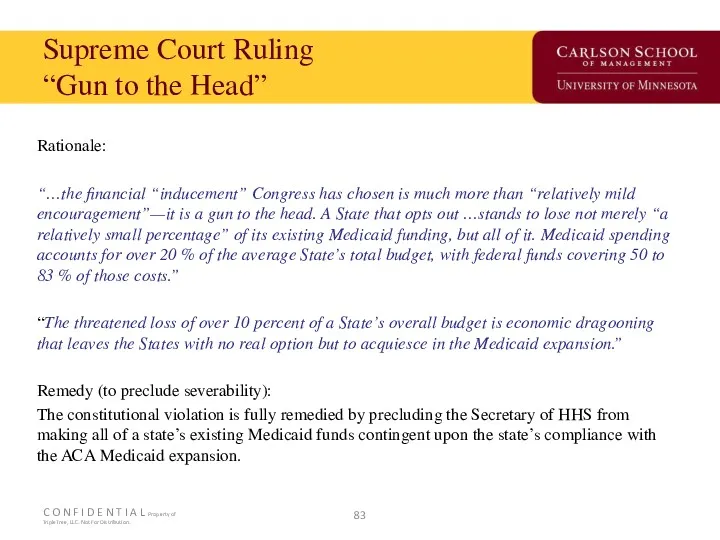

- 83. Supreme Court Ruling “Gun to the Head” Rationale: “…the financial “inducement” Congress has chosen is much

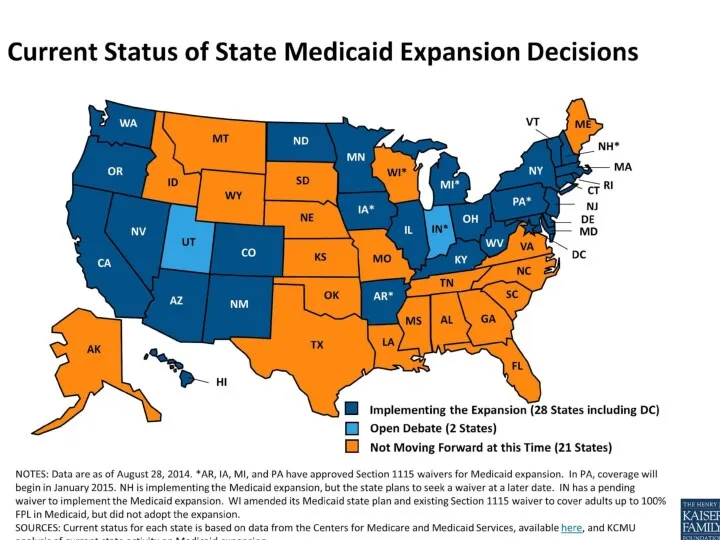

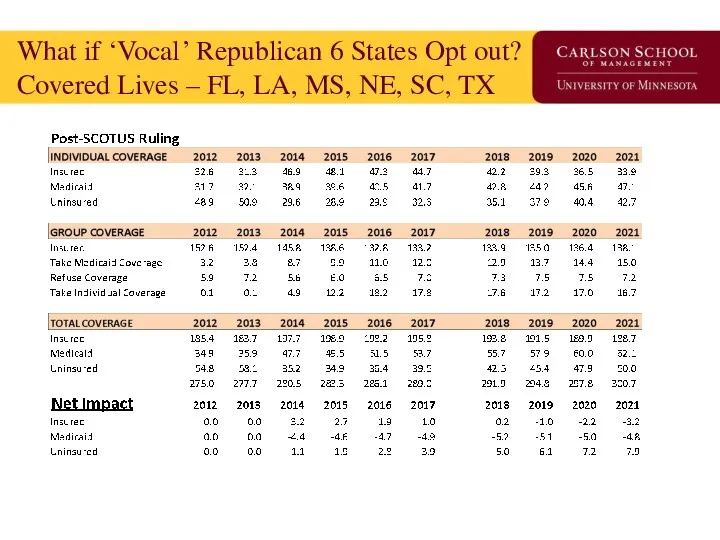

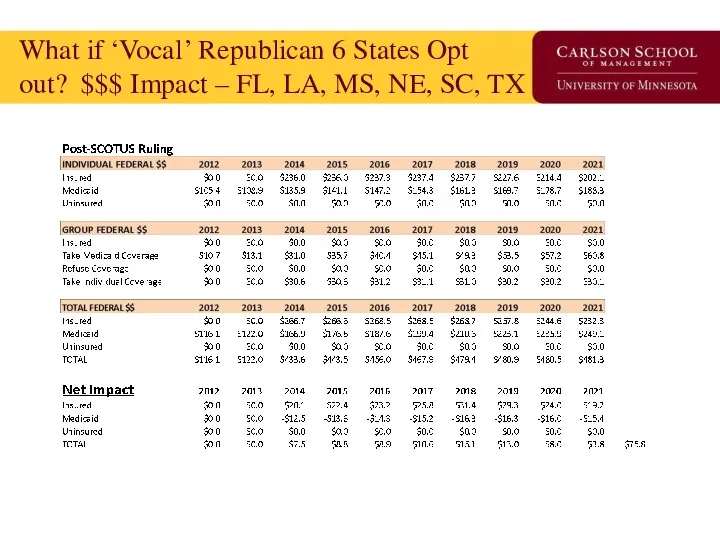

- 85. What if ‘Vocal’ Republican 6 States Opt out? Covered Lives – FL, LA, MS, NE, SC,

- 86. What if ‘Vocal’ Republican 6 States Opt out? $$$ Impact – FL, LA, MS, NE, SC,

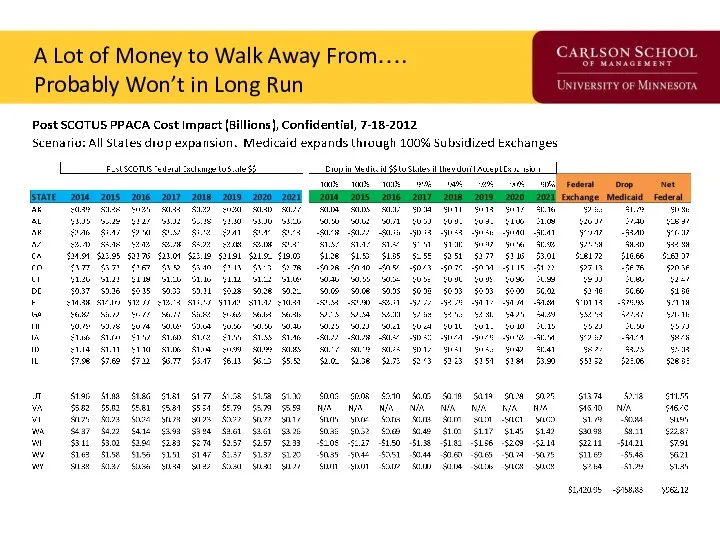

- 87. A Lot of Money to Walk Away From…. Probably Won’t in Long Run

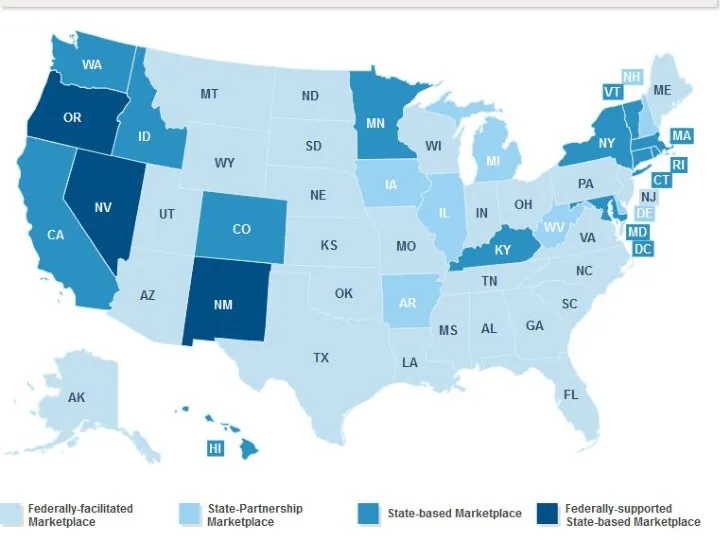

- 88. Next Supreme Court Ruling, June 2015 Are Insurance Subsidies Legal in 34 States using Federal Exchange?

- 90. Some Insights from themorningconsult.com (2/11/2015)

- 91. If Asked: A 21st Century Version of Health Insurance Reform Get actuarially certified risk profiles for

- 92. Supreme Court Decision in June, 2015 on State Exchanges The GOP Unicorn / Replace Plan Trojan

- 93. Closing Thoughts We are going to get a great natural experiment in economics, political science and

- 95. Скачать презентацию

Overview

Next unit up - Insurers

Insurance theory & concepts

Risk & uncertainty

Insurance premiums

Evolution of modern

Overview

Next unit up - Insurers

Insurance theory & concepts

Risk & uncertainty

Insurance premiums

Evolution of modern

Risky Business:

Making Decisions Under Uncertainty

Uncertainty: A situation when more than one event may

Risky Business:

Making Decisions Under Uncertainty

Uncertainty: A situation when more than one event may

Risk Defined

Risk: The probability of incurring a loss (or some other misfortune).

More precisely,

Risk Defined

Risk: The probability of incurring a loss (or some other misfortune).

More precisely,

The Cost of Risk

Some people are willing to bear more risk than others.

In

The Cost of Risk

Some people are willing to bear more risk than others.

In

The Utility of Wealth

The Utility of Wealth

What can we observe from the Utility

of Wealth Schedule?

Utility increases as wealth

What can we observe from the Utility

of Wealth Schedule?

Utility increases as wealth

Translate Utility of Wealth into

Expected Utility

Due to uncertainty, people do not know

Translate Utility of Wealth into

Expected Utility

Due to uncertainty, people do not know

Choice Under Uncertainty

Range of outcomes

Cost of risk

Choice #1: W=$5K

Choice #2: W=$6K

Choice Under Uncertainty

Range of outcomes

Cost of risk

Choice #1: W=$5K

Choice #2: W=$6K

Interpretation of Choice under Uncertainty

At Choice #1, Tania’s wealth is $5K, U=80, no

Interpretation of Choice under Uncertainty

At Choice #1, Tania’s wealth is $5K, U=80, no

Risk Aversion and Risk Neutrality

Risk Averse: Someone who sees risk as not cost-less.

The

Risk Aversion and Risk Neutrality

Risk Averse: Someone who sees risk as not cost-less.

The

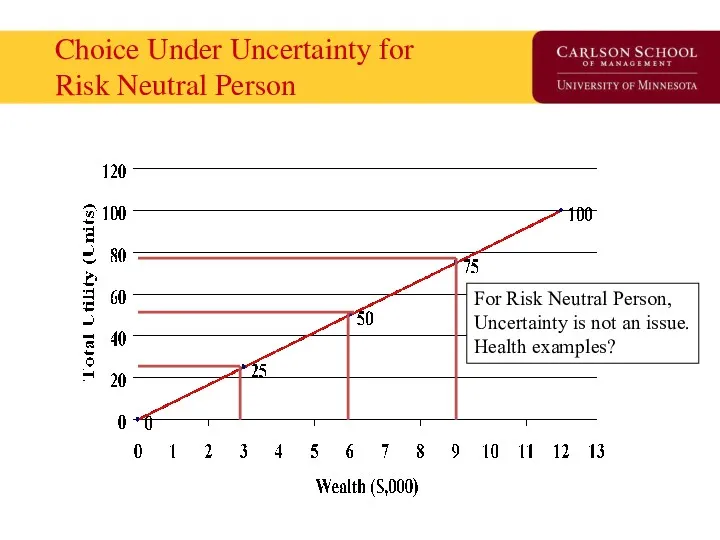

Choice Under Uncertainty for

Risk Neutral Person

For Risk Neutral Person,

Uncertainty is not an

Choice Under Uncertainty for

Risk Neutral Person

For Risk Neutral Person,

Uncertainty is not an

How do we reduce risk?

Buy the ‘the cost of risk’ off. (similar to

How do we reduce risk?

Buy the ‘the cost of risk’ off. (similar to

How does Insurance work?

Insurance works by ‘pooling’ risks.

Insurance is possible and profitable because

How does Insurance work?

Insurance works by ‘pooling’ risks.

Insurance is possible and profitable because

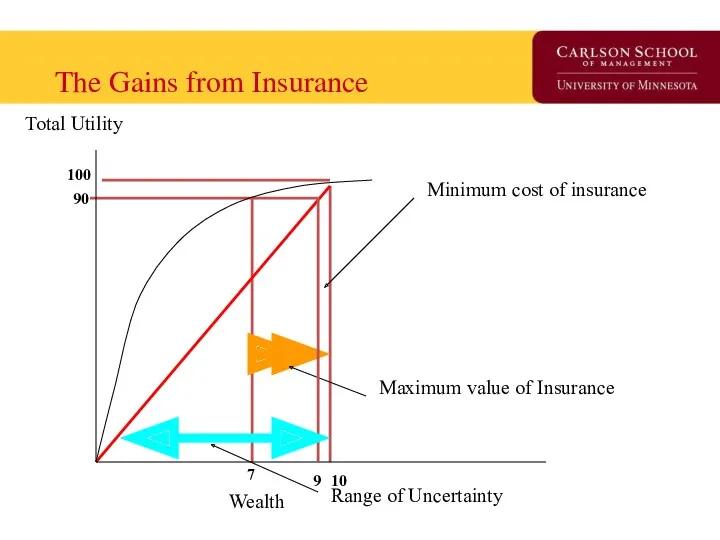

The Gains from Insurance

Maximum value of Insurance

Minimum cost of insurance

Total Utility

Wealth

Range of Uncertainty

100

90

10

7

9

The Gains from Insurance

Maximum value of Insurance

Minimum cost of insurance

Total Utility

Wealth

Range of Uncertainty

100

90

10

7

9

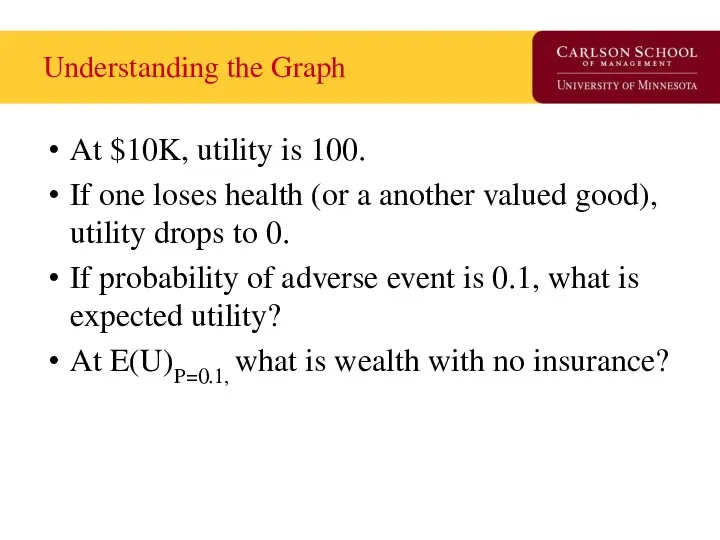

Understanding the Graph

At $10K, utility is 100.

If one loses health (or a another

Understanding the Graph

At $10K, utility is 100.

If one loses health (or a another

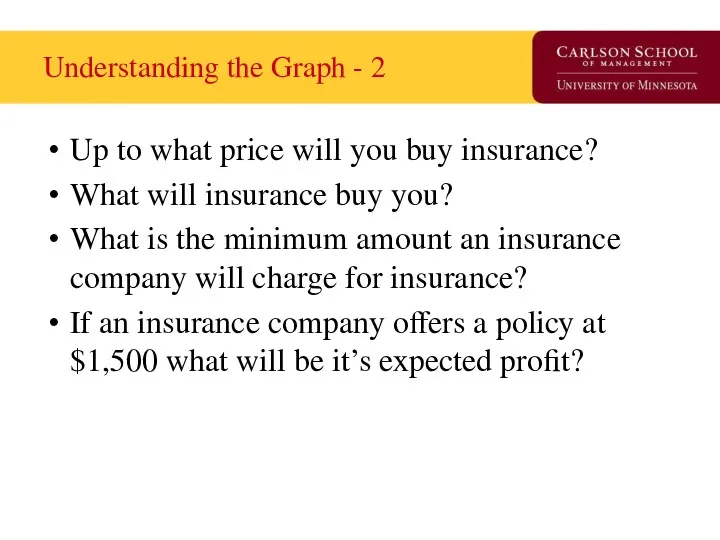

Understanding the Graph - 2

Up to what price will you buy insurance?

What will

Understanding the Graph - 2

Up to what price will you buy insurance?

What will

Moral Hazard & Adverse Selection

Private information is information that is available to one

Moral Hazard & Adverse Selection

Private information is information that is available to one

Moral Hazard

Defined: When one of two or more parities with an agreement has

Moral Hazard

Defined: When one of two or more parities with an agreement has

Adverse Selection

Defined: The tendency for people to enter into agreements in which they

Adverse Selection

Defined: The tendency for people to enter into agreements in which they

Understanding the difference between the two

People who face greater risks are more likely

Understanding the difference between the two

People who face greater risks are more likely

How do insurance companies overcome these problems?

Find a signal to convey information from

How do insurance companies overcome these problems?

Find a signal to convey information from

Examine Evolution of a Market

Using the “Time Machine” from Davey & Goliath

Examine Evolution of a Market

Using the “Time Machine” from Davey & Goliath

Slow Day? Starr got you down?

Consider….

http://www.awn.com/heaven_and_hell/DG/DG4.htm

Slow Day? Starr got you down?

Consider….

http://www.awn.com/heaven_and_hell/DG/DG4.htm

Early Public Health Insurance

First instance of public insurance is Germany’s 1883 ‘compulsory

Early Public Health Insurance

First instance of public insurance is Germany’s 1883 ‘compulsory

U.S. Public Health Insurance

Failed proposals made in Congress for National Health Insurance:

1918-19

1935-36

1948

1974

1993-94

Successful

U.S. Public Health Insurance

Failed proposals made in Congress for National Health Insurance:

1918-19

1935-36

1948

1974

1993-94

Successful

Private Insurance – Two early models

Fee-for-service insurance

Epitomized by Blue Cross plan started for

Private Insurance – Two early models

Fee-for-service insurance

Epitomized by Blue Cross plan started for

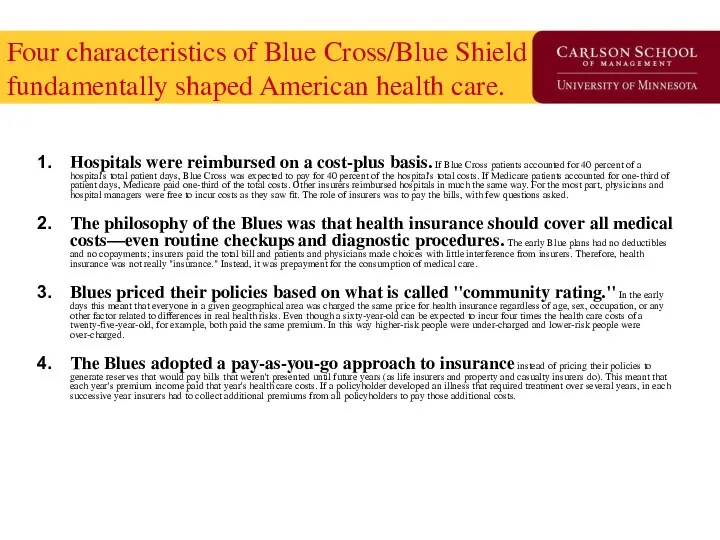

Four characteristics of Blue Cross/Blue Shield fundamentally shaped American health care.

Hospitals were

Four characteristics of Blue Cross/Blue Shield fundamentally shaped American health care.

Hospitals were

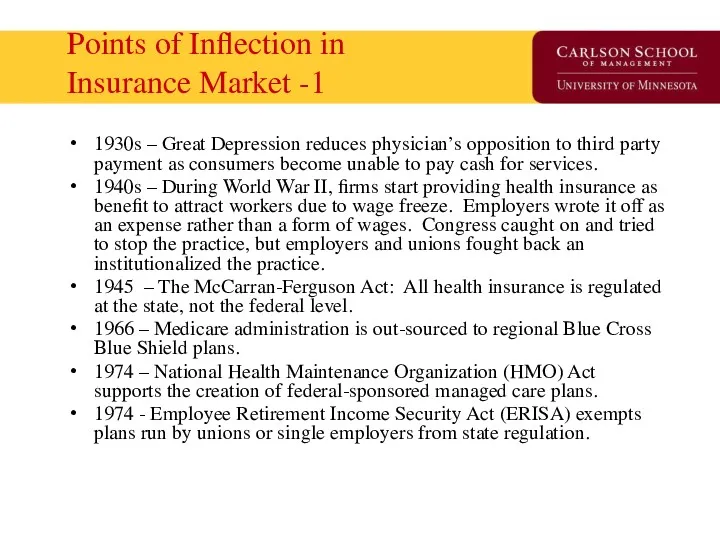

Points of Inflection in

Insurance Market -1

1930s – Great Depression reduces physician’s opposition

Points of Inflection in

Insurance Market -1

1930s – Great Depression reduces physician’s opposition

Points of Inflection in

Insurance Market - 2

1983 – Medicare institutes prospective payment

Points of Inflection in

Insurance Market - 2

1983 – Medicare institutes prospective payment

State of Health Insurance Today

Insurance models

Demand side control programs

Supply side control programs

Market

State of Health Insurance Today

Insurance models

Demand side control programs

Supply side control programs

Market

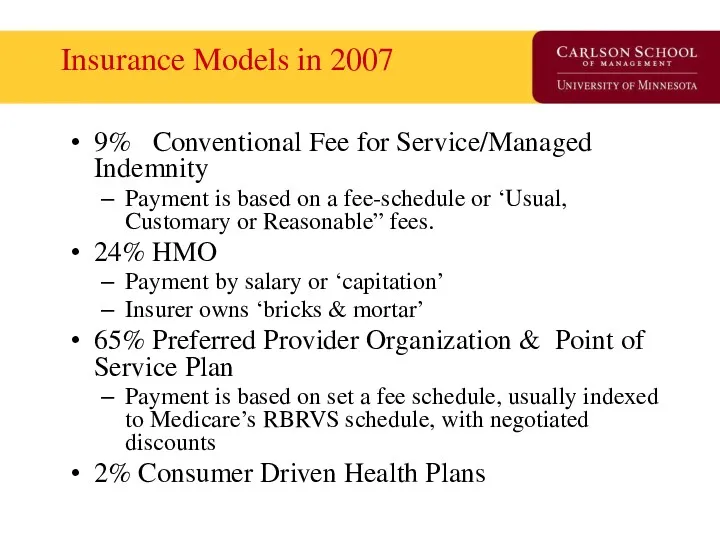

Insurance Models in 2007

9% Conventional Fee for Service/Managed Indemnity

Payment is based on a

Insurance Models in 2007

9% Conventional Fee for Service/Managed Indemnity

Payment is based on a

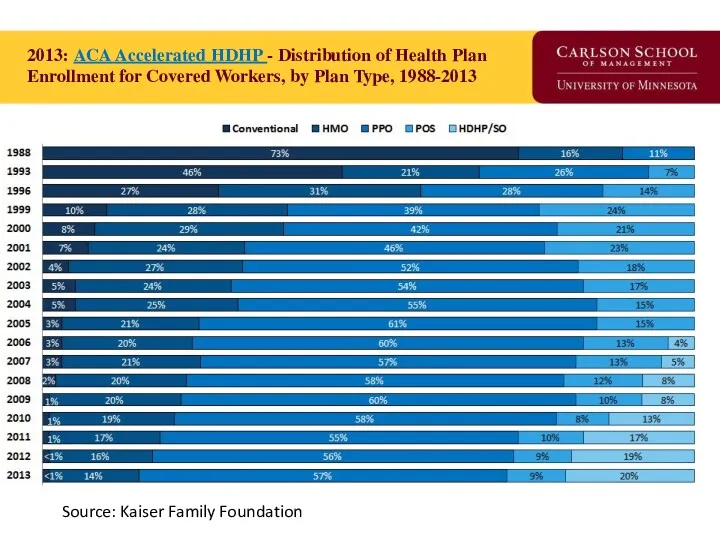

2013: ACA Accelerated HDHP - Distribution of Health Plan

Enrollment for Covered Workers,

2013: ACA Accelerated HDHP - Distribution of Health Plan Enrollment for Covered Workers,

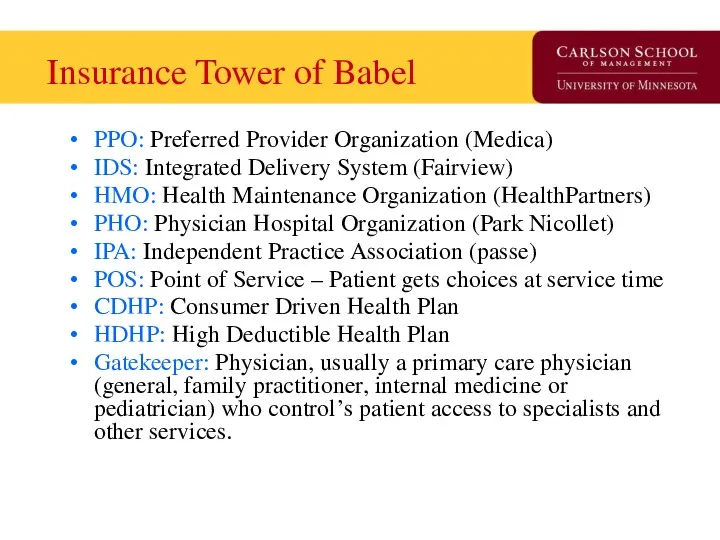

Insurance Tower of Babel

PPO: Preferred Provider Organization (Medica)

IDS: Integrated Delivery System (Fairview)

HMO:

Insurance Tower of Babel

PPO: Preferred Provider Organization (Medica)

IDS: Integrated Delivery System (Fairview)

HMO:

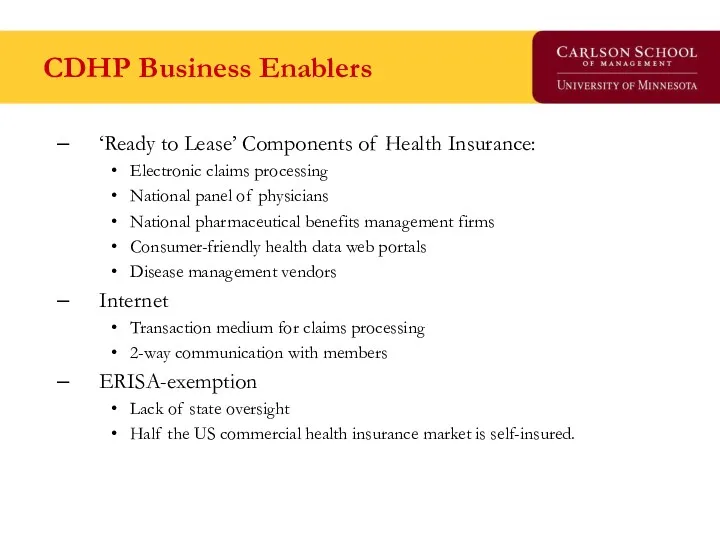

CDHP Business Enablers

‘Ready to Lease’ Components of Health Insurance:

Electronic claims processing

National panel

CDHP Business Enablers

‘Ready to Lease’ Components of Health Insurance:

Electronic claims processing

National panel

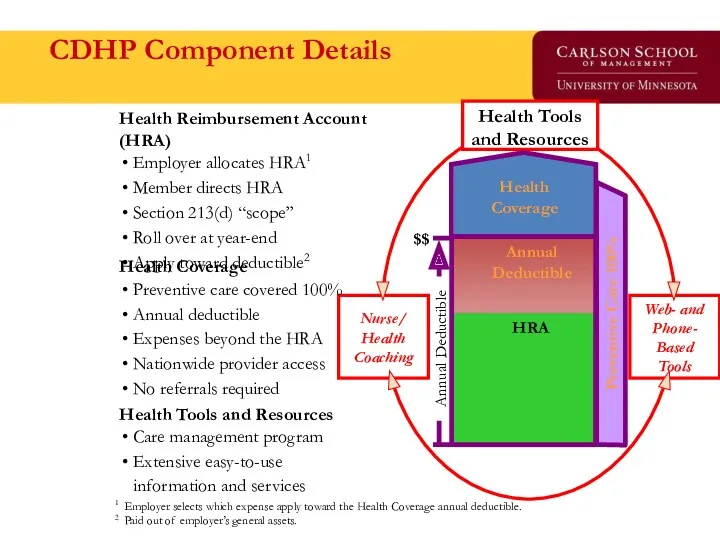

CDHP Component Details

Health Tools and Resources

Care management program

Extensive easy-to-use

information and services

Health Coverage

Preventive

CDHP Component Details

Health Tools and Resources

Care management program

Extensive easy-to-use

information and services

Health Coverage

Preventive

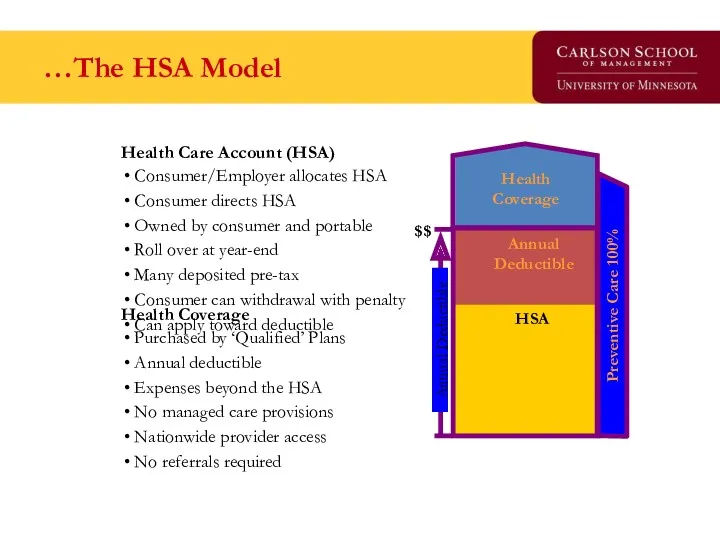

…The HSA Model

Health Coverage

Purchased by ‘Qualified’ Plans

Annual deductible

Expenses beyond the HSA

No managed care

…The HSA Model

Health Coverage

Purchased by ‘Qualified’ Plans

Annual deductible

Expenses beyond the HSA

No managed care

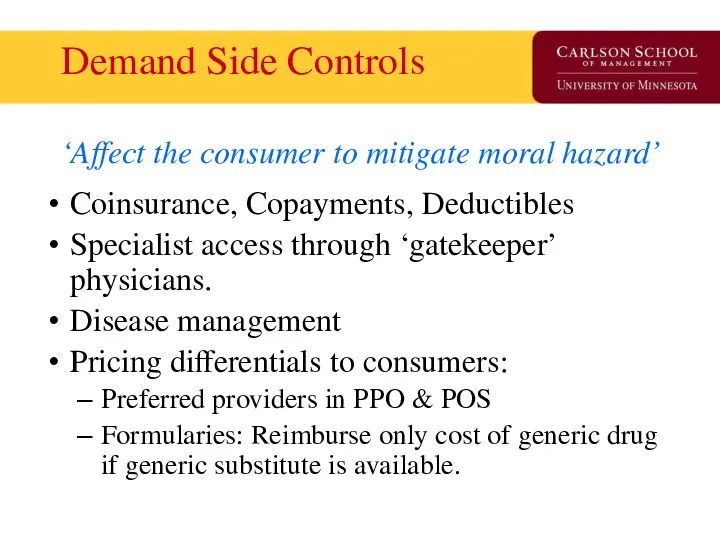

Demand Side Controls

‘Affect the consumer to mitigate moral hazard’

Coinsurance, Copayments, Deductibles

Specialist access through

Demand Side Controls

‘Affect the consumer to mitigate moral hazard’

Coinsurance, Copayments, Deductibles

Specialist access through

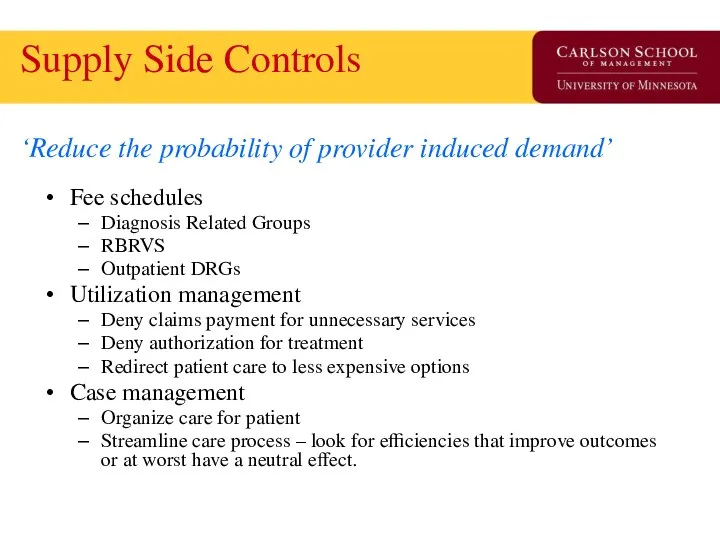

Supply Side Controls

‘Reduce the probability of provider induced demand’

Fee schedules

Diagnosis Related Groups

RBRVS

Outpatient

Supply Side Controls

‘Reduce the probability of provider induced demand’

Fee schedules

Diagnosis Related Groups

RBRVS

Outpatient

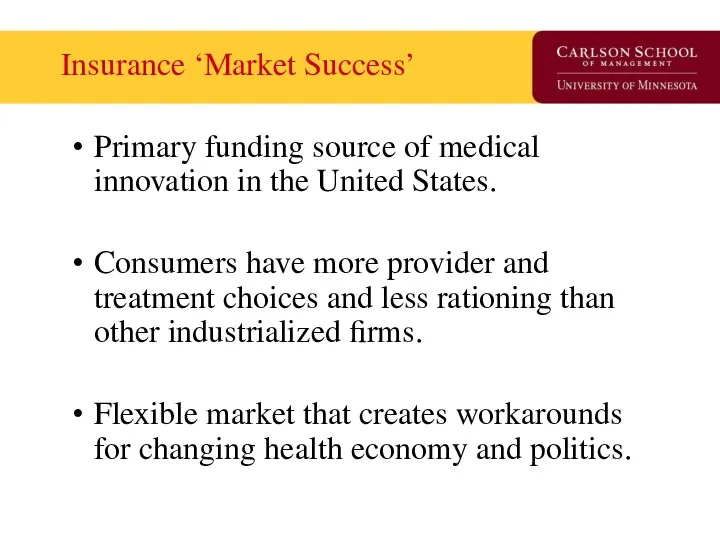

Insurance ‘Market Success’

Primary funding source of medical innovation in the United States.

Consumers have

Insurance ‘Market Success’

Primary funding source of medical innovation in the United States.

Consumers have

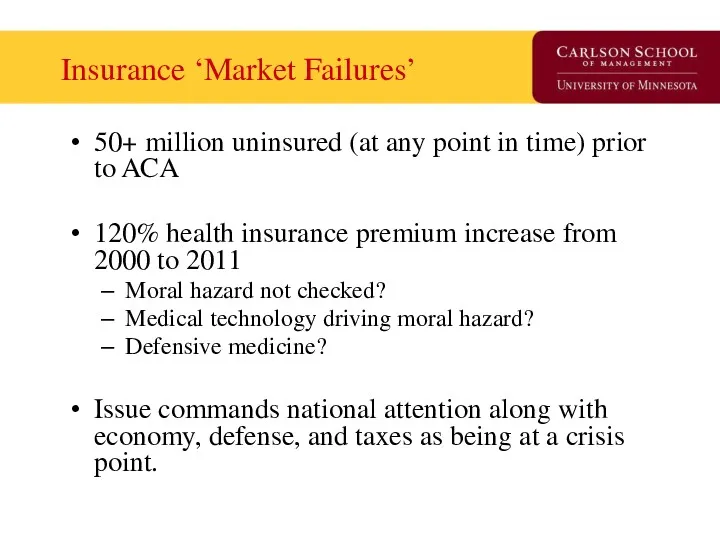

Insurance ‘Market Failures’

50+ million uninsured (at any point in time) prior to ACA

120%

Insurance ‘Market Failures’

50+ million uninsured (at any point in time) prior to ACA

120%

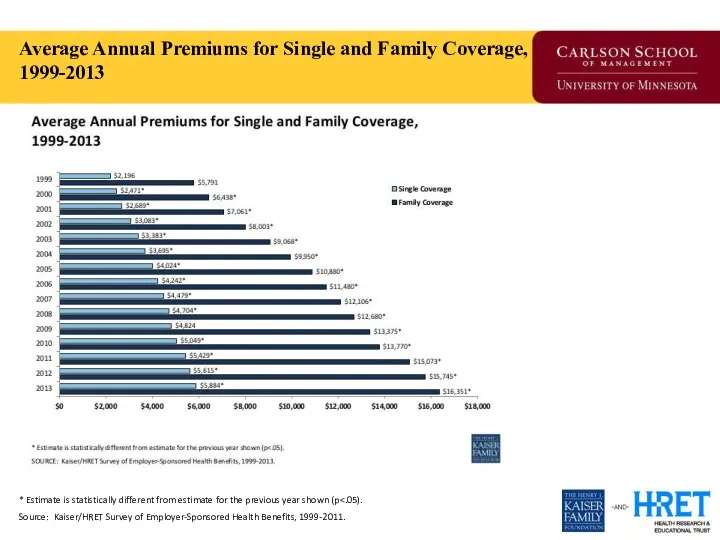

Average Annual Premiums for Single and Family Coverage, 1999-2013

* Estimate is statistically different

Average Annual Premiums for Single and Family Coverage, 1999-2013

* Estimate is statistically different

Question for Reflection

How uniquely American is evolution of the insurance market in the

Question for Reflection

How uniquely American is evolution of the insurance market in the

The Uninsured Problem

Who are the uninsured?

Why is this a ‘market failure’?

If government were

The Uninsured Problem

Who are the uninsured?

Why is this a ‘market failure’?

If government were

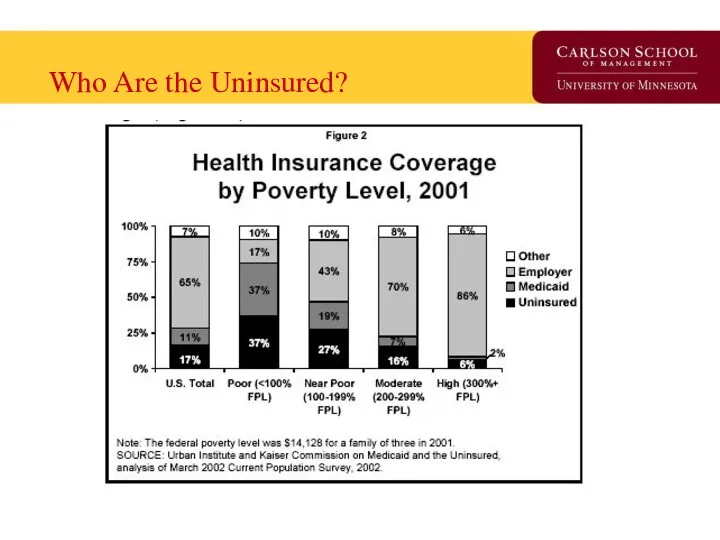

Who Are the Uninsured?

Who Are the Uninsured?

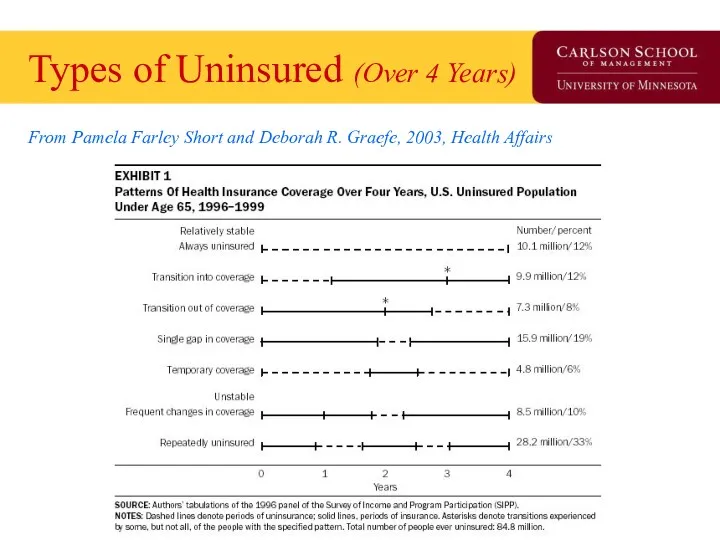

Types of Uninsured (Over 4 Years)

From Pamela Farley Short and Deborah R. Graefe,

Types of Uninsured (Over 4 Years)

From Pamela Farley Short and Deborah R. Graefe,

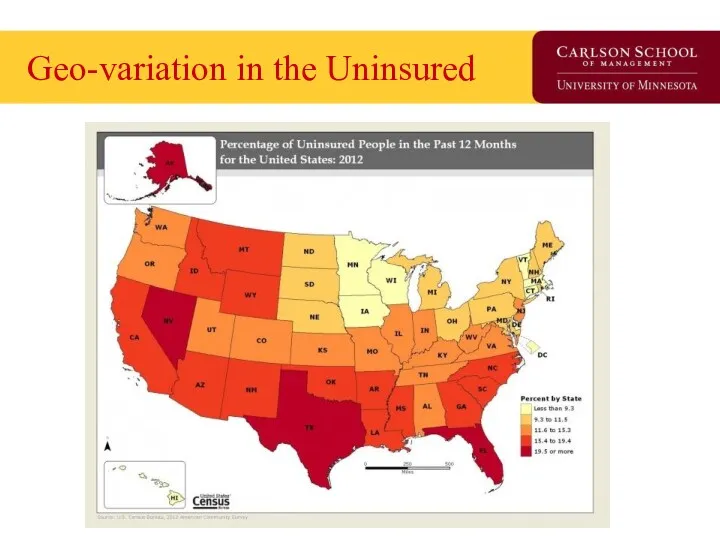

Geo-variation in the Uninsured

Geo-variation in the Uninsured

Does theory square with

health insurance today?

What is the purpose of insurance?

How is

Does theory square with

health insurance today?

What is the purpose of insurance?

How is

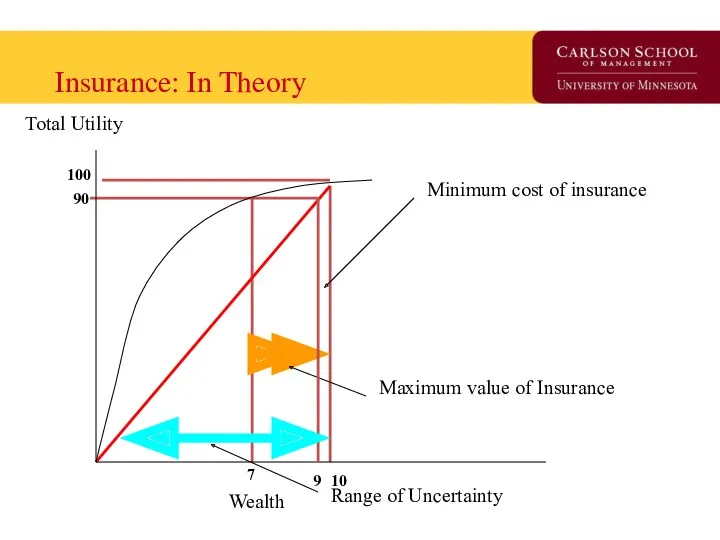

Insurance: In Theory

Maximum value of Insurance

Minimum cost of insurance

Total Utility

Wealth

Range of Uncertainty

100

90

10

7

9

Insurance: In Theory

Maximum value of Insurance

Minimum cost of insurance

Total Utility

Wealth

Range of Uncertainty

100

90

10

7

9

What is the Effect of Uninsurance?

What is the Effect of Uninsurance?

One Insurance Reform Option

(G.H.W. Bush ’92, M. Romney ’06, and

H.R. Clinton & B.

One Insurance Reform Option (G.H.W. Bush ’92, M. Romney ’06, and H.R. Clinton & B.

What has the Uninsured Problem been

Proposed to be Addressed?

Pay or play

Federal

What has the Uninsured Problem been

Proposed to be Addressed?

Pay or play

Federal

What is the minimal form of health insurance you can live with?

High-deductible catastrophic

Service-specific

What is the minimal form of health insurance you can live with?

High-deductible catastrophic

Service-specific

The Free-Rider Problem

Free-rider is a person who consumes a good without paying for

The Free-Rider Problem

Free-rider is a person who consumes a good without paying for

Break

Break

Health Insurance Market Today

Health Economist Health Reform Priors

Current Law Overview

Coverage and Financing

Insurance Markets

Exchanges

Payment

Health Insurance Market Today

Health Economist Health Reform Priors

Current Law Overview

Coverage and Financing

Insurance Markets

Exchanges

Payment

Priors as a Health Economist

Health economists find that technology is both good for

Priors as a Health Economist

Health economists find that technology is both good for

Coverage and Financing

Coverage: 32 of 54 million uninsured covered

24 million in Exchange

16

Coverage and Financing

Coverage: 32 of 54 million uninsured covered

24 million in Exchange

16

Insurance Market: 2010

Effective Immediately: Annual process set by HHS and States for premium

Insurance Market: 2010

Effective Immediately: Annual process set by HHS and States for premium

NAIC Health Reform Committees

HHS is required to consult with the National Association

NAIC Health Reform Committees

HHS is required to consult with the National Association

Insurance Market: 2011

Effective January 2011: 80% MLR for individual and small group, 85%

Insurance Market: 2011

Effective January 2011: 80% MLR for individual and small group, 85%

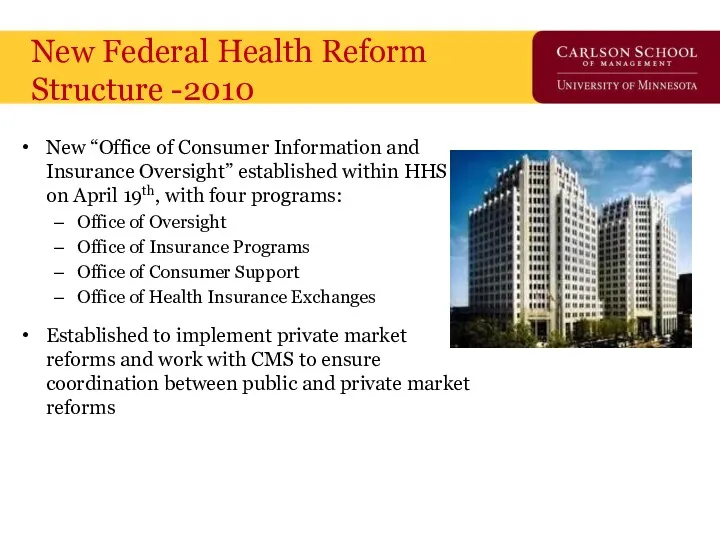

New Federal Health Reform

Structure -2010

New “Office of Consumer Information and Insurance Oversight” established

New Federal Health Reform

Structure -2010

New “Office of Consumer Information and Insurance Oversight” established

Exchanges: 2010

Effective July 2010: HHS with States to establish internet portal to identify

Exchanges: 2010

Effective July 2010: HHS with States to establish internet portal to identify

Exchanges: 2014

Effective 2014: States to establish Exchange to facilitate comparison shopping, enrollment, and

Exchanges: 2014

Effective 2014: States to establish Exchange to facilitate comparison shopping, enrollment, and

Payment Reform &

Care Coordination

CMS Innovation Center: Created in 2011 to test and

Payment Reform &

Care Coordination

CMS Innovation Center: Created in 2011 to test and

National Impact of Health Reform

Uninsured status is reduced by 59.8% (81% if base

National Impact of Health Reform

Uninsured status is reduced by 59.8% (81% if base

CBO: 2010-2019 Spend

CBO: 2010-2019 Spend

CBO: 2010-2019 Tax/Save

CBO: 2010-2019 Tax/Save

CBO: Projected Savings

on Vote Eve, March 21, 2010

By 2019, $122 billion deficit

CBO: Projected Savings

on Vote Eve, March 21, 2010

By 2019, $122 billion deficit

CBO: Projected Additional

Cost/Savings of Pending Changes

By 2019, $676 billion additional deficit burden

CBO: Projected Additional

Cost/Savings of Pending Changes

By 2019, $676 billion additional deficit burden

Current vs. Pending Budget Effect –

CBO’s Own Numbers

Net impact: $554 billion additional

Current vs. Pending Budget Effect –

CBO’s Own Numbers

Net impact: $554 billion additional

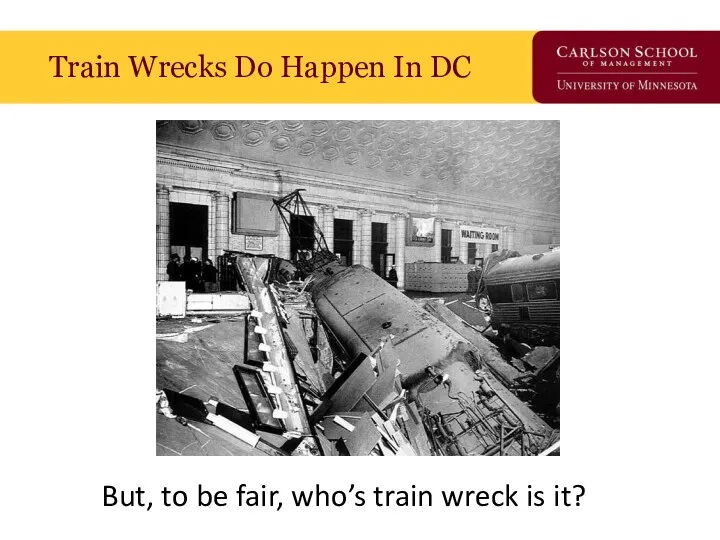

Train Wrecks Do Happen In DC

But, to be fair, who’s train wreck is

Train Wrecks Do Happen In DC

But, to be fair, who’s train wreck is

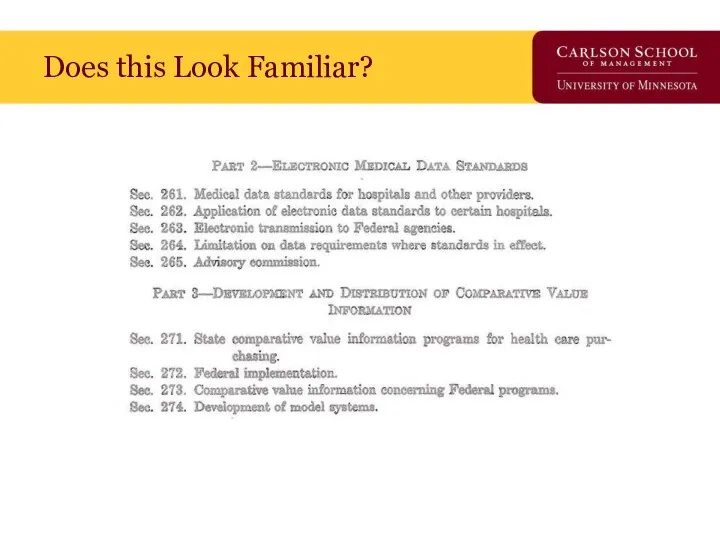

Does this Look Familiar?

Does this Look Familiar?

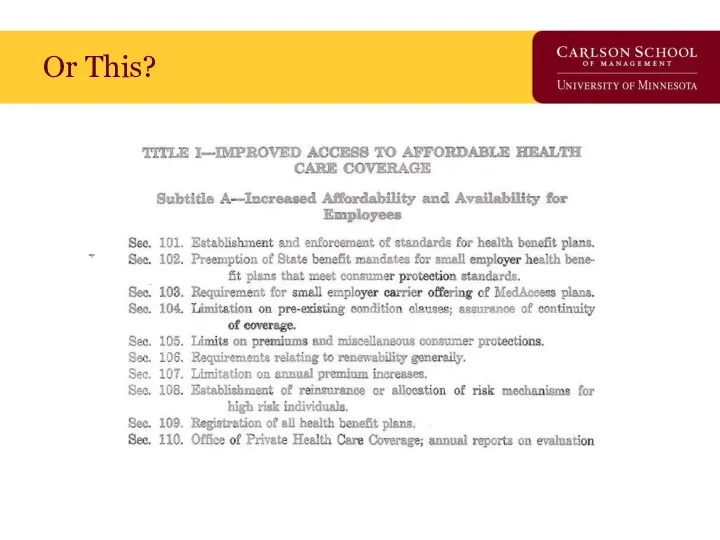

Or This?

Or This?

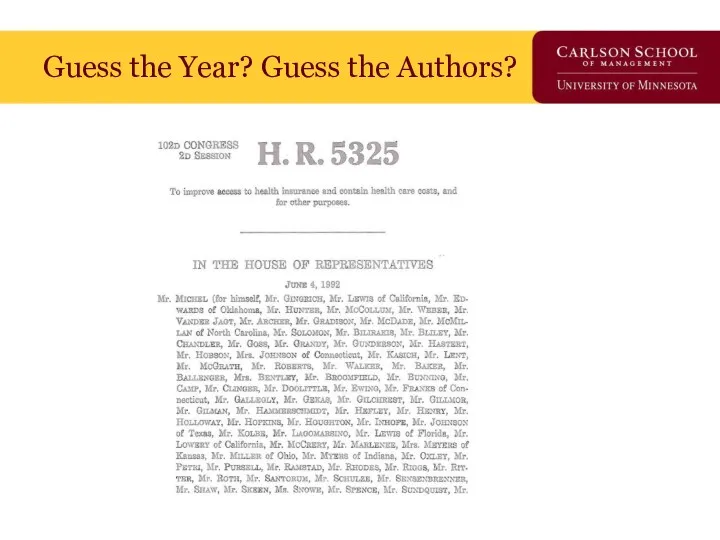

Guess the Year? Guess the Authors?

Guess the Year? Guess the Authors?

Guess the Year? Guess the Authors?

Guess the Year? Guess the Authors?

Implementation Iceberg Cometh?

Implementation Iceberg Cometh?

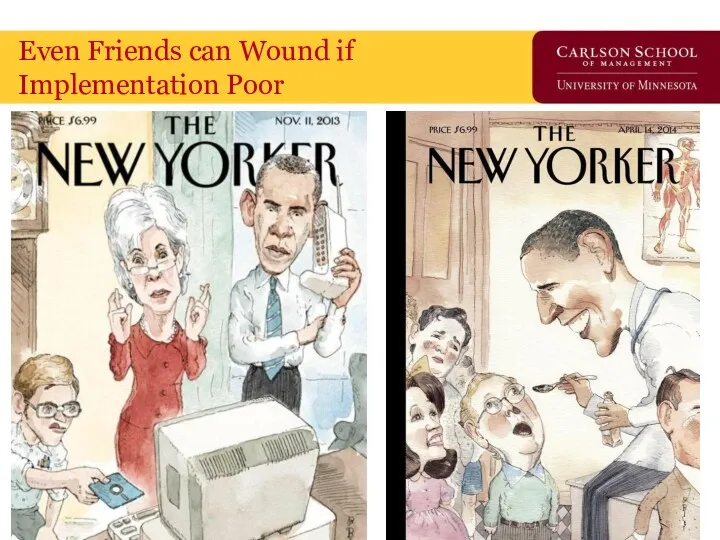

Even Friends can Wound if

Implementation Poor

Even Friends can Wound if

Implementation Poor

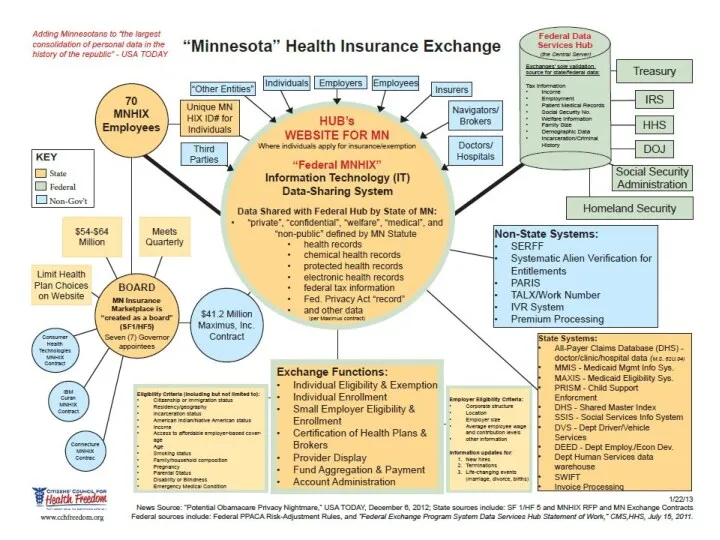

ACA Privacy Nightmare?

ACA Privacy Nightmare?

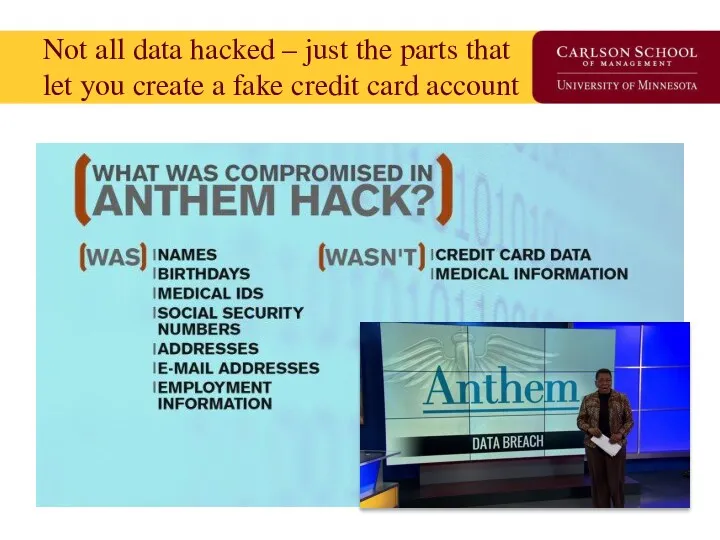

Not all data hacked – just the parts that

let you create a

Not all data hacked – just the parts that let you create a

Major Reform Component –

Medicaid Expansion

The Act transforms Medicaid into a program to meet

Major Reform Component –

Medicaid Expansion

The Act transforms Medicaid into a program to meet

Supreme Court Ruling

“Gun to the Head”

Rationale:

“…the financial “inducement” Congress has chosen is much

Supreme Court Ruling

“Gun to the Head”

Rationale:

“…the financial “inducement” Congress has chosen is much

What if ‘Vocal’ Republican 6 States Opt out?

Covered Lives – FL, LA,

What if ‘Vocal’ Republican 6 States Opt out? Covered Lives – FL, LA,

What if ‘Vocal’ Republican 6 States Opt

out? $$$ Impact – FL, LA,

What if ‘Vocal’ Republican 6 States Opt out? $$$ Impact – FL, LA,

A Lot of Money to Walk Away From….

Probably Won’t in Long Run

A Lot of Money to Walk Away From….

Probably Won’t in Long Run

Next Supreme Court Ruling, June 2015

Are Insurance Subsidies Legal in 34 States using

Next Supreme Court Ruling, June 2015 Are Insurance Subsidies Legal in 34 States using

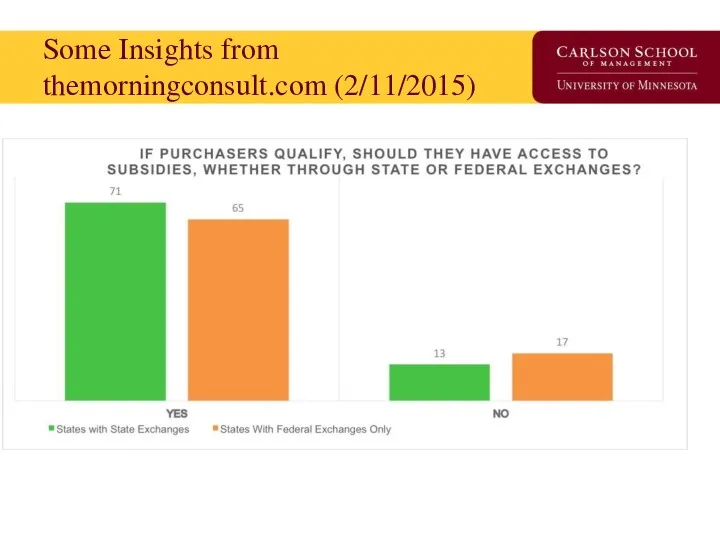

Some Insights from

themorningconsult.com (2/11/2015)

Some Insights from

themorningconsult.com (2/11/2015)

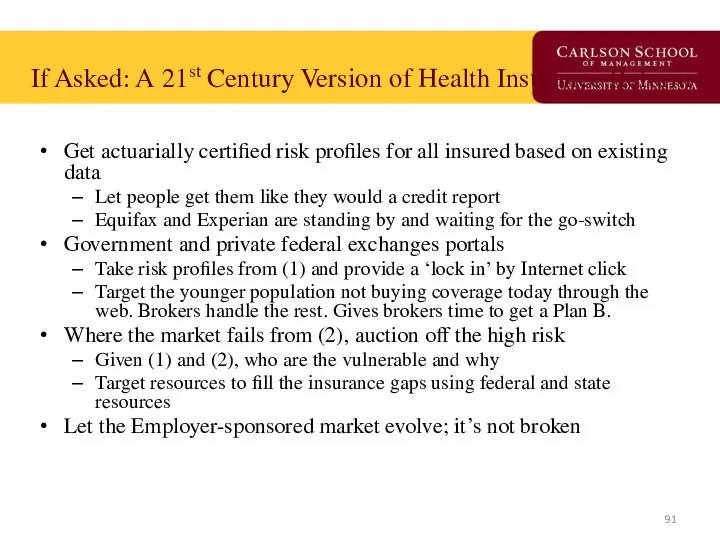

If Asked: A 21st Century Version of Health Insurance Reform

Get actuarially certified risk

If Asked: A 21st Century Version of Health Insurance Reform

Get actuarially certified risk

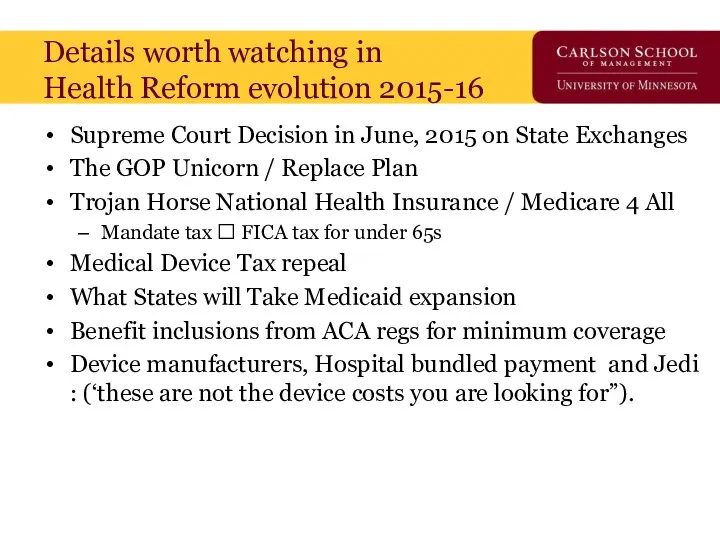

Supreme Court Decision in June, 2015 on State Exchanges

The GOP Unicorn / Replace

Supreme Court Decision in June, 2015 on State Exchanges

The GOP Unicorn / Replace

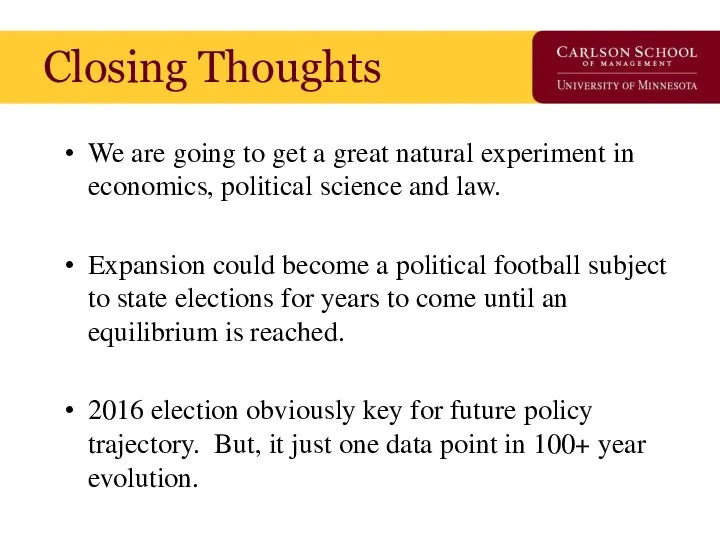

Closing Thoughts

We are going to get a great natural experiment in economics, political

Closing Thoughts

We are going to get a great natural experiment in economics, political

Индивид в организации

Индивид в организации Структура и основной сортамент продукции ОАО ММК. Численность кадрового состава

Структура и основной сортамент продукции ОАО ММК. Численность кадрового состава Управление и моделирование бизнес-процессами

Управление и моделирование бизнес-процессами История развития менеджмента в России

История развития менеджмента в России Стратегии масштабирования бизнеса

Стратегии масштабирования бизнеса Научный менеджмент в России в первой половине XX века

Научный менеджмент в России в первой половине XX века Первые научные теории управления

Первые научные теории управления КБ Ренессанс кредит. ООО Поиск клининговой компании для офиса в г. Москва

КБ Ренессанс кредит. ООО Поиск клининговой компании для офиса в г. Москва Методы отбора персонала в организации

Методы отбора персонала в организации Основы коммуникации

Основы коммуникации Сущность организационного поведения

Сущность организационного поведения Nonverbal intercultural communication

Nonverbal intercultural communication Көлік логистикасы слайд-дәрісі мамандығы үшін тасымалды ұйымдастыру, қозғалысты басқару

Көлік логистикасы слайд-дәрісі мамандығы үшін тасымалды ұйымдастыру, қозғалысты басқару Действия бортпроводников. Вопросы брифинга и инструктажи

Действия бортпроводников. Вопросы брифинга и инструктажи Этапы рационального решения проблем

Этапы рационального решения проблем Мотивация сотрудников. Сектора обслуживания дебетовых карт

Мотивация сотрудников. Сектора обслуживания дебетовых карт Диаграмма Исикавы и Парето

Диаграмма Исикавы и Парето Onboarding сотрудников в ГК СНЕГ

Onboarding сотрудников в ГК СНЕГ Дерево решений

Дерево решений Концепція менеджменту заінтересованих сторін

Концепція менеджменту заінтересованих сторін Инструменты для ведения открытого диалога с клиентом

Инструменты для ведения открытого диалога с клиентом Стратегическое управление: необходимость, сущность, этапы. Лекция 1

Стратегическое управление: необходимость, сущность, этапы. Лекция 1 Эффективное трудоустройство. Программа тренинга

Эффективное трудоустройство. Программа тренинга Инструкция по навигации и оформлению офиса

Инструкция по навигации и оформлению офиса Цель и задачи современной службы управления персоналом

Цель и задачи современной службы управления персоналом Система государственного управления. Лекция 3

Система государственного управления. Лекция 3 Major building systems

Major building systems Создать стандарт

Создать стандарт