- Operating and Financial Leverage

Содержание

- 2. After studying Chapter 16, you should be able to: Define operating and financial leverage and identify

- 3. Operating and Financial Leverage Operating Leverage Financial Leverage Total Leverage Cash-Flow Ability to Service Debt Other

- 4. Operating Leverage One potential “effect” caused by the presence of operating leverage is that a change

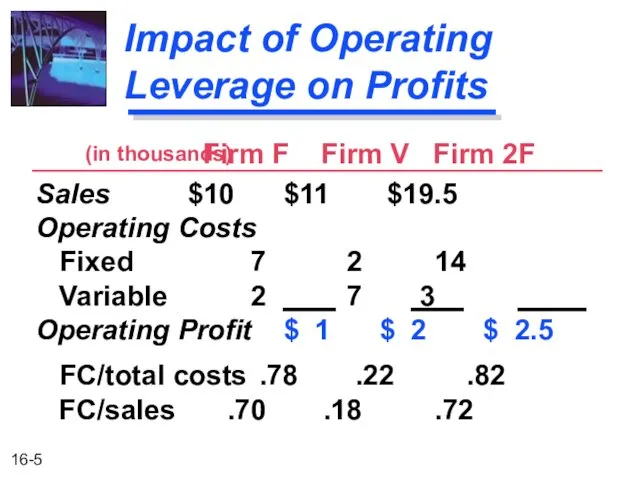

- 5. Impact of Operating Leverage on Profits Firm F Firm V Firm 2F Sales $10 $11 $19.5

- 6. Impact of Operating Leverage on Profits Now, subject each firm to a 50% increase in sales

- 7. Impact of Operating Leverage on Profits Firm F Firm V Firm 2F Sales $15 $16.5 $29.25

- 8. Impact of Operating Leverage on Profits Firm F is the most “sensitive” firm -- for it,

- 9. Break-Even Analysis When studying operating leverage, “profits” refers to operating profits before taxes (i.e., EBIT) and

- 10. Break-Even Chart QUANTITY PRODUCED AND SOLD 0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 Total Revenues

- 11. Break-Even (Quantity) Point How to find the quantity break-even point: EBIT = P(Q) - V(Q) -

- 12. Break-Even (Quantity) Point Breakeven occurs when EBIT = 0 Q (P - V) - FC =

- 13. Break-Even (Sales) Point How to find the sales break-even point: SBE = FC + (VCBE) SBE

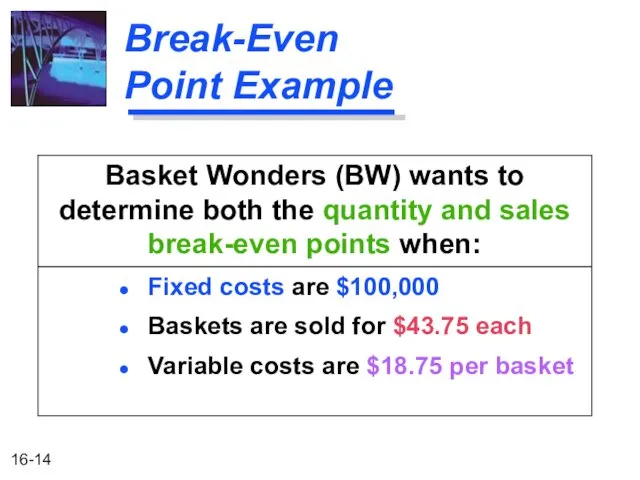

- 14. Break-Even Point Example Basket Wonders (BW) wants to determine both the quantity and sales break-even points

- 15. Break-Even Point (s) Breakeven occurs when: QBE = FC / (P - V) QBE = $100,000

- 16. Break-Even Chart QUANTITY PRODUCED AND SOLD 0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 Total Revenues

- 17. Degree of Operating Leverage (DOL) DOL at Q units of output (or sales) Degree of Operating

- 18. Computing the DOL DOLQ units Calculating the DOL for a single product or a single-product firm.

- 19. Computing the DOL DOLS dollars of sales Calculating the DOL for a multiproduct firm. = S

- 20. Break-Even Point Example Lisa Miller wants to determine the degree of operating leverage at sales levels

- 21. Computing BW’s DOL DOL6,000 units Computation based on the previously calculated break-even point of 4,000 units

- 22. Interpretation of the DOL A 1% increase in sales above the 8,000 unit level increases EBIT

- 23. Interpretation of the DOL 2,000 4,000 6,000 8,000 1 2 3 4 5 QUANTITY PRODUCED AND

- 24. Interpretation of the DOL DOL is a quantitative measure of the “sensitivity” of a firm’s operating

- 25. DOL and Business Risk DOL is only one component of business risk and becomes “active” only

- 26. Application of DOL for Our Three Firm Example Use the data in Slide 16-5 and the

- 27. Application of DOL for Our Three Firm Example Use the data in Slide 16-5 and the

- 28. Application of DOL for Our Three-Firm Example Use the data in Slide 16-5 and the following

- 29. Application of DOL for Our Three-Firm Example The ranked results indicate that the firm most sensitive

- 30. Financial Leverage Financial leverage is acquired by choice. Used as a means of increasing the return

- 31. EBIT-EPS Break-Even, or Indifference, Analysis Calculate EPS for a given level of EBIT at a given

- 32. EBIT-EPS Chart Current common equity shares = 50,000 $1 million in new financing of either: All

- 33. EBIT-EPS Calculation with New Equity Financing EBIT $500,000 $150,000* Interest 0 0 EBT $500,000 $150,000 Taxes

- 34. EBIT-EPS Chart 0 100 200 300 400 500 600 700 EBIT ($ thousands) Earnings per Share

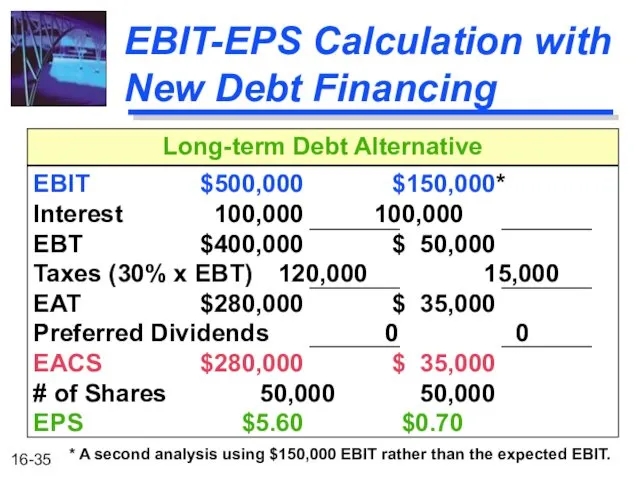

- 35. EBIT-EPS Calculation with New Debt Financing EBIT $500,000 $150,000* Interest 100,000 100,000 EBT $400,000 $ 50,000

- 36. EBIT-EPS Chart 0 100 200 300 400 500 600 700 EBIT ($ thousands) Earnings per Share

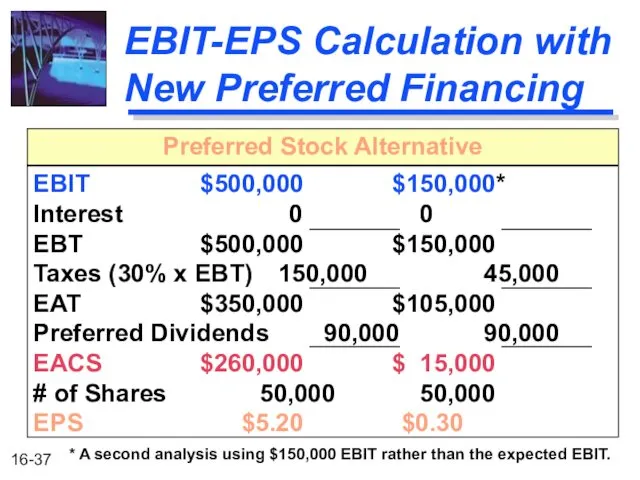

- 37. EBIT-EPS Calculation with New Preferred Financing EBIT $500,000 $150,000* Interest 0 0 EBT $500,000 $150,000 Taxes

- 38. 0 100 200 300 400 500 600 700 EBIT-EPS Chart EBIT ($ thousands) Earnings per Share

- 39. What About Risk? 0 100 200 300 400 500 600 700 EBIT ($ thousands) Earnings per

- 40. What About Risk? 0 100 200 300 400 500 600 700 EBIT ($ thousands) Earnings per

- 41. Degree of Financial Leverage (DFL) DFL at EBIT of X dollars Degree of Financial Leverage --

- 42. Computing the DFL DFL EBIT of $X Calculating the DFL = EBIT EBIT - I -

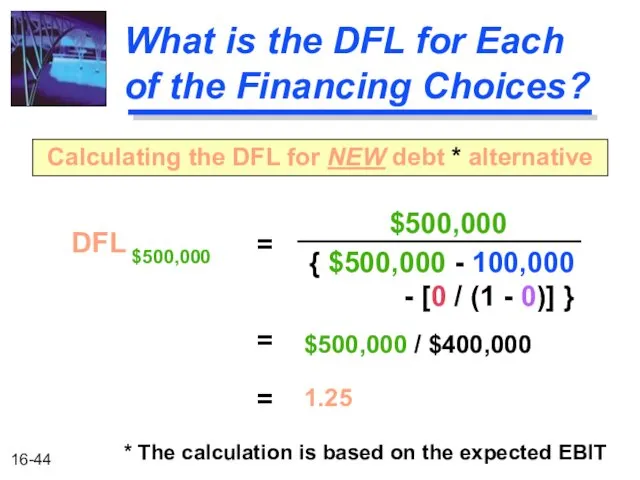

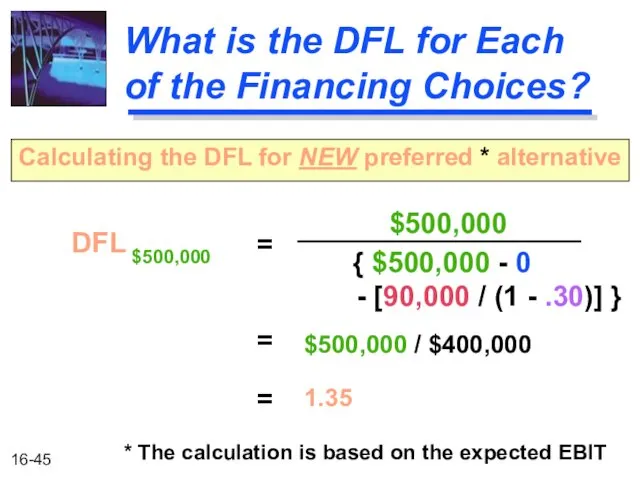

- 43. What is the DFL for Each of the Financing Choices? DFL $500,000 Calculating the DFL for

- 44. What is the DFL for Each of the Financing Choices? DFL $500,000 Calculating the DFL for

- 45. What is the DFL for Each of the Financing Choices? DFL $500,000 Calculating the DFL for

- 46. Variability of EPS Preferred stock financing will lead to the greatest variability in earnings per share

- 47. Financial Risk Debt increases the probability of cash insolvency over an all-equity-financed firm. For example, our

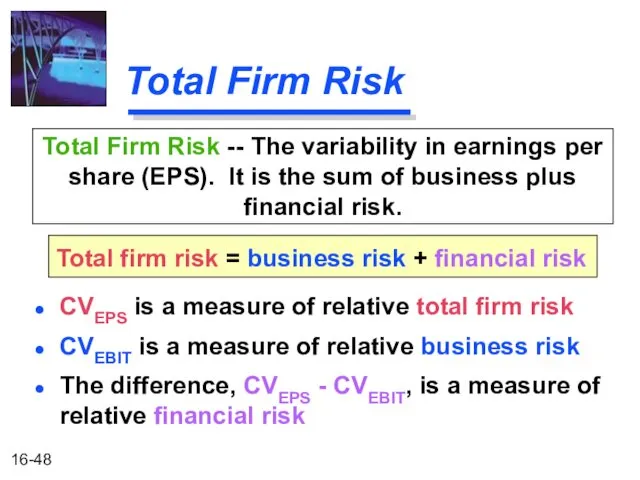

- 48. Total Firm Risk CVEPS is a measure of relative total firm risk CVEBIT is a measure

- 49. Degree of Total Leverage (DTL) DTL at Q units (or S dollars) of output (or sales)

- 50. Computing the DTL DTL S dollars of sales DTL Q units (or S dollars) = (

- 51. DTL Example Lisa Miller wants to determine the Degree of Total Leverage at EBIT=$500,000. As we

- 52. Computing the DTL for All-Equity Financing DTL S dollars of sales = $500,000 + $100,000 $500,000

- 53. Computing the DTL for Debt Financing DTL S dollars of sales = $500,000 + $100,000 {

- 54. Risk versus Return Compare the expected EPS to the DTL for the common stock equity financing

- 55. What is an Appropriate Amount of Financial Leverage? Firms must first analyze their expected future cash

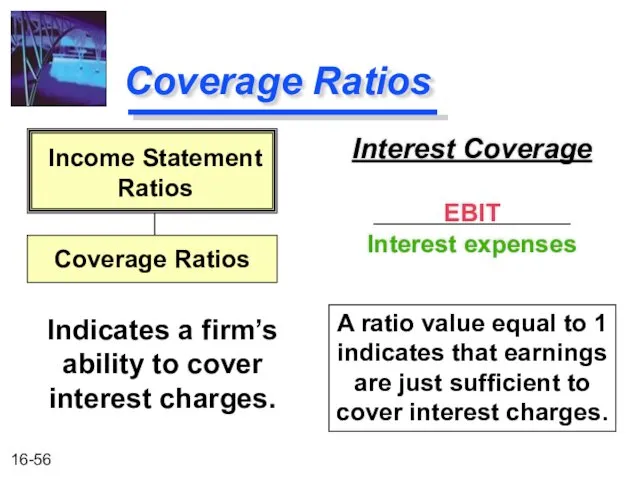

- 56. Coverage Ratios Interest Coverage EBIT Interest expenses Indicates a firm’s ability to cover interest charges. Income

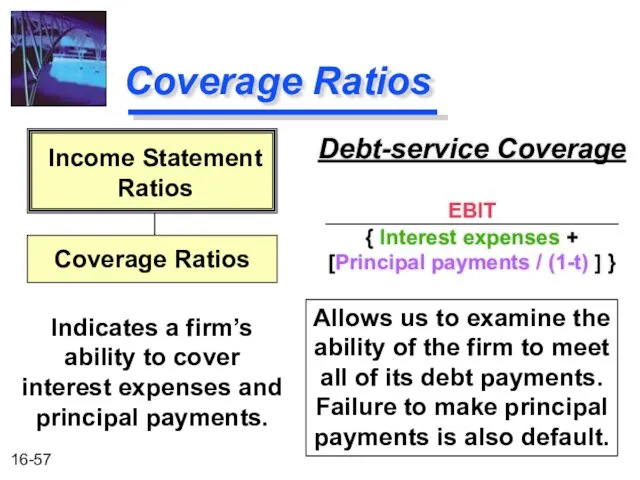

- 57. Coverage Ratios Debt-service Coverage EBIT { Interest expenses + [Principal payments / (1-t) ] } Indicates

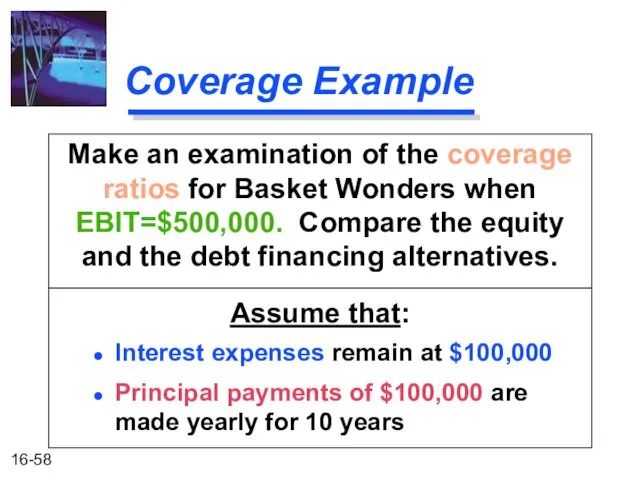

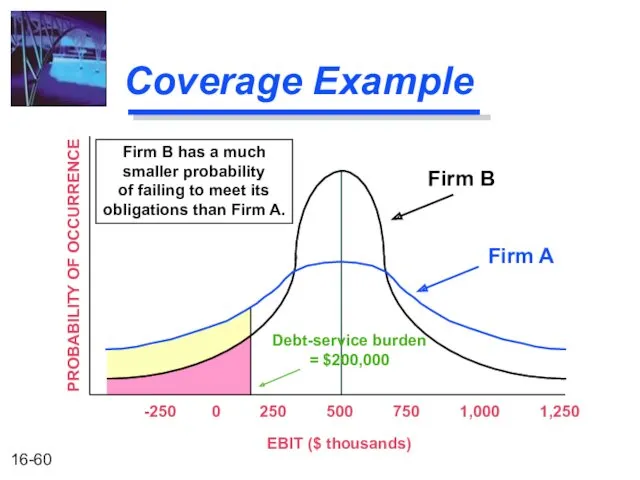

- 58. Coverage Example Make an examination of the coverage ratios for Basket Wonders when EBIT=$500,000. Compare the

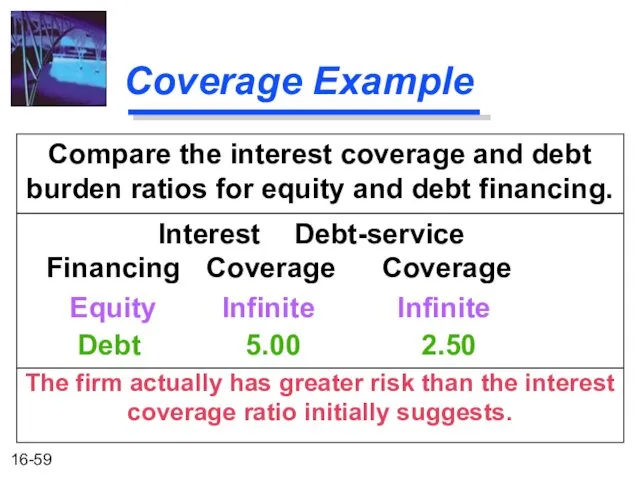

- 59. Coverage Example Compare the interest coverage and debt burden ratios for equity and debt financing. Interest

- 60. Coverage Example -250 0 250 500 750 1,000 1,250 EBIT ($ thousands) Firm B has a

- 61. Summary of the Coverage Ratio Discussion A single ratio value cannot be interpreted identically for all

- 62. Other Methods of Analysis Often, firms are compared to peer institutions in the same industry. Large

- 63. Other Methods of Analysis Firms may gain insight into the financial markets’ evaluation of their firm

- 65. Скачать презентацию

After studying Chapter 16, you should be able to:

Define operating and

After studying Chapter 16, you should be able to:

Define operating and

Operating and Financial Leverage

Operating Leverage

Financial Leverage

Total Leverage

Cash-Flow Ability to Service Debt

Other

Operating and Financial Leverage

Operating Leverage

Financial Leverage

Total Leverage

Cash-Flow Ability to Service Debt

Other

Operating Leverage

One potential “effect” caused by the presence of operating leverage

Operating Leverage

One potential “effect” caused by the presence of operating leverage

Impact of Operating Leverage on Profits

Firm F Firm V Firm

Impact of Operating Leverage on Profits

Firm F Firm V Firm

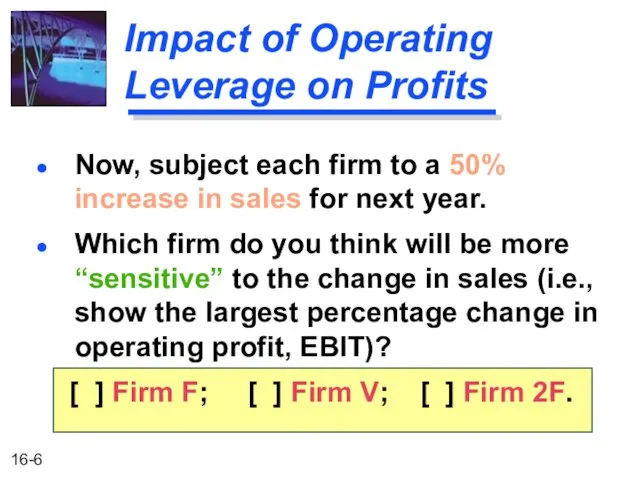

Impact of Operating Leverage on Profits

Now, subject each firm to a

Impact of Operating Leverage on Profits

Now, subject each firm to a

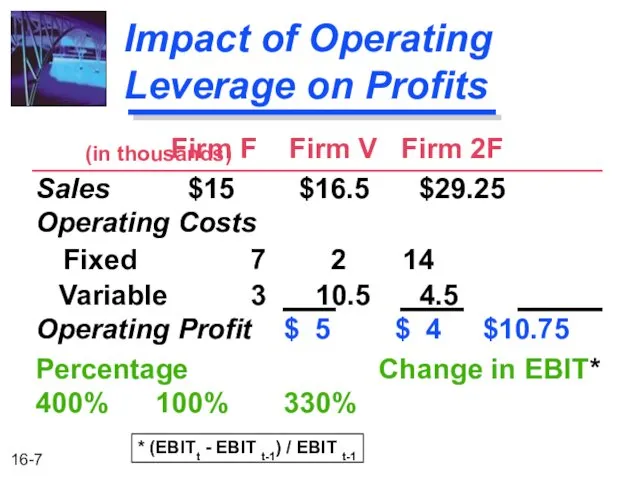

Impact of Operating Leverage on Profits

Firm F Firm V Firm

Impact of Operating Leverage on Profits

Firm F Firm V Firm

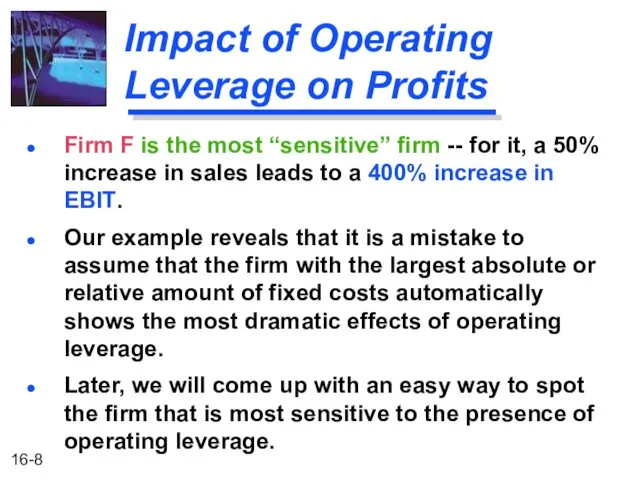

Impact of Operating Leverage on Profits

Firm F is the most “sensitive”

Impact of Operating Leverage on Profits

Firm F is the most “sensitive”

Break-Even Analysis

When studying operating leverage, “profits” refers to operating profits before

Break-Even Analysis

When studying operating leverage, “profits” refers to operating profits before

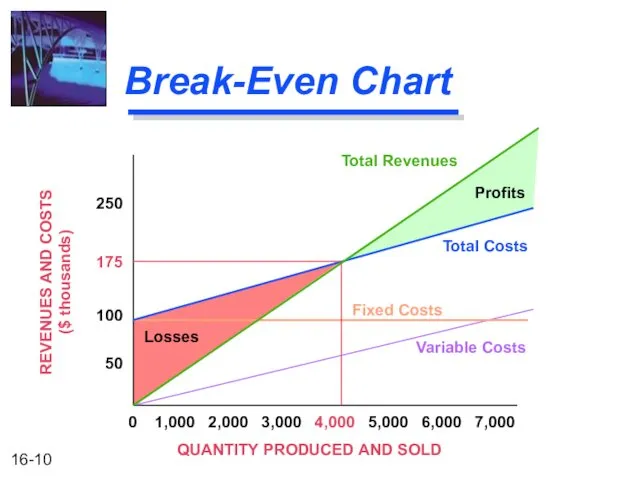

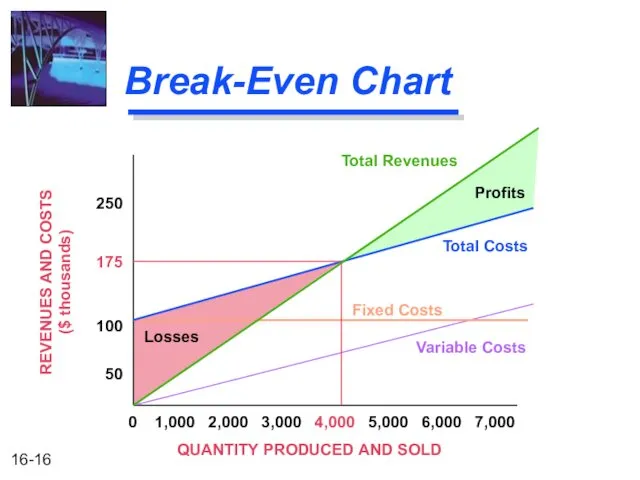

Break-Even Chart

QUANTITY PRODUCED AND SOLD

0 1,000 2,000 3,000 4,000 5,000 6,000

Break-Even Chart

QUANTITY PRODUCED AND SOLD

0 1,000 2,000 3,000 4,000 5,000 6,000

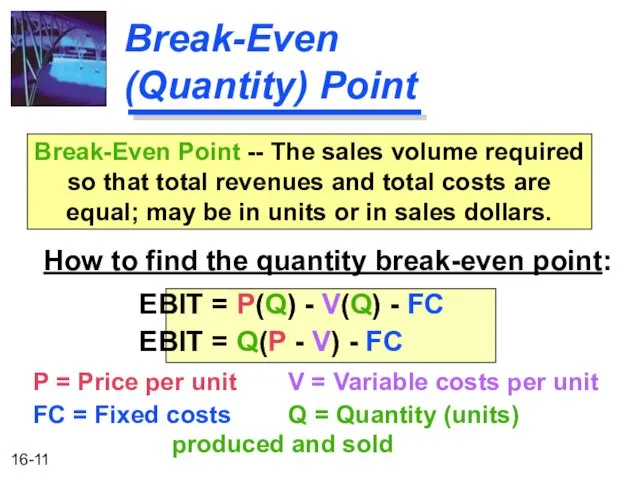

Break-Even (Quantity) Point

How to find the quantity break-even point:

EBIT =

Break-Even (Quantity) Point

How to find the quantity break-even point:

EBIT =

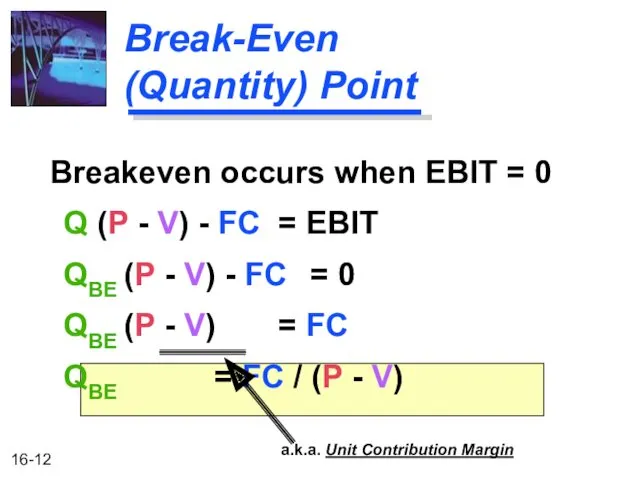

Break-Even (Quantity) Point

Breakeven occurs when EBIT = 0

Q (P -

Break-Even (Quantity) Point

Breakeven occurs when EBIT = 0

Q (P -

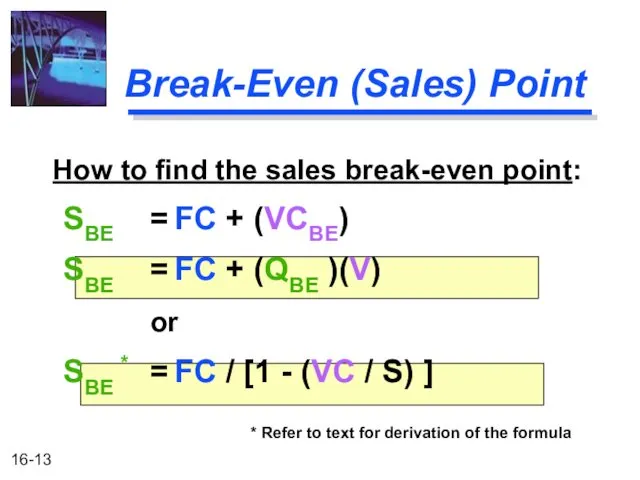

Break-Even (Sales) Point

How to find the sales break-even point:

SBE =

Break-Even (Sales) Point

How to find the sales break-even point:

SBE =

Break-Even Point Example

Basket Wonders (BW) wants to determine both the quantity

Break-Even Point Example

Basket Wonders (BW) wants to determine both the quantity

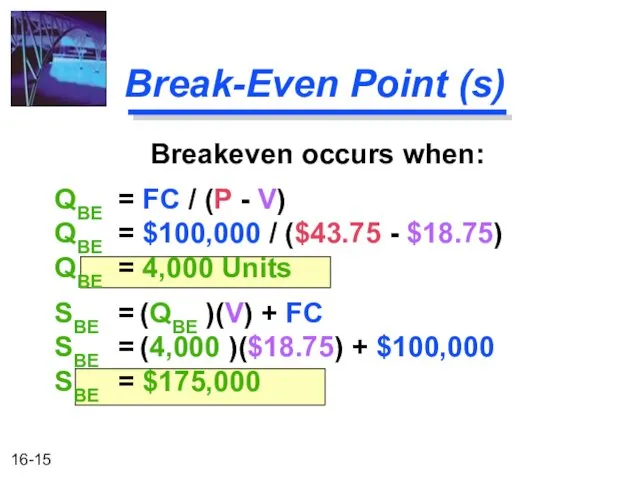

Break-Even Point (s)

Breakeven occurs when:

QBE = FC / (P - V)

Break-Even Point (s)

Breakeven occurs when:

QBE = FC / (P - V)

Break-Even Chart

QUANTITY PRODUCED AND SOLD

0 1,000 2,000 3,000 4,000 5,000 6,000

Break-Even Chart

QUANTITY PRODUCED AND SOLD

0 1,000 2,000 3,000 4,000 5,000 6,000

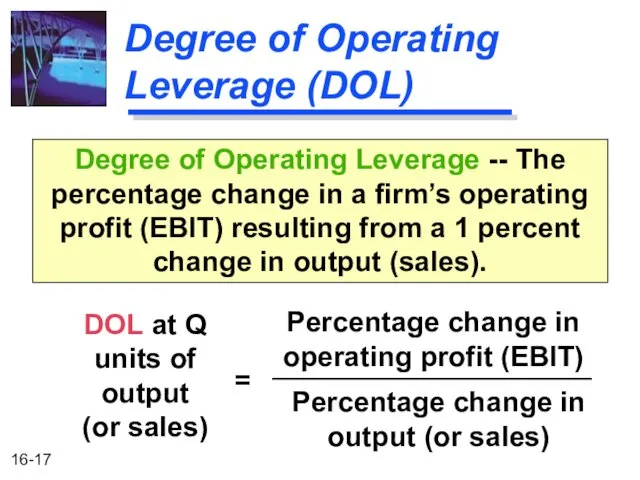

Degree of Operating Leverage (DOL)

DOL at Q units of output

(or

Degree of Operating Leverage (DOL)

DOL at Q units of output

(or

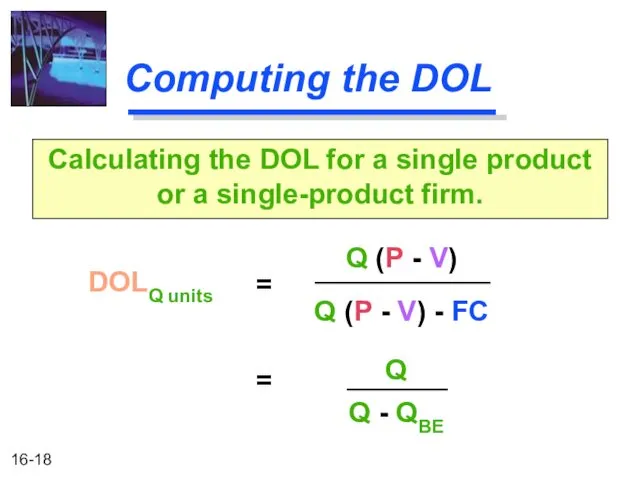

Computing the DOL

DOLQ units

Calculating the DOL for a single product or

Computing the DOL

DOLQ units

Calculating the DOL for a single product or

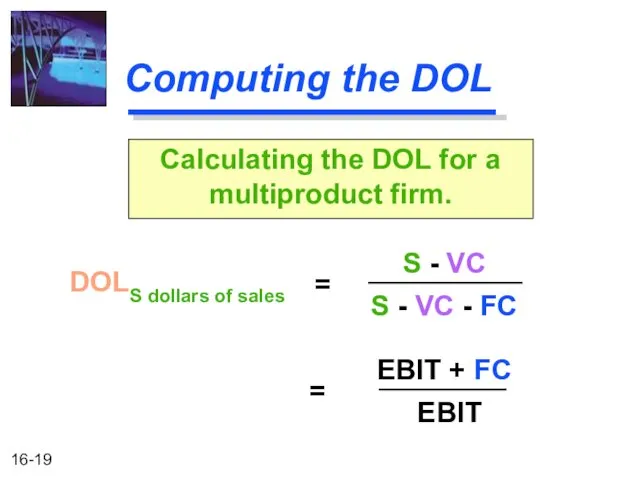

Computing the DOL

DOLS dollars of sales

Calculating the DOL for a multiproduct

Computing the DOL

DOLS dollars of sales

Calculating the DOL for a multiproduct

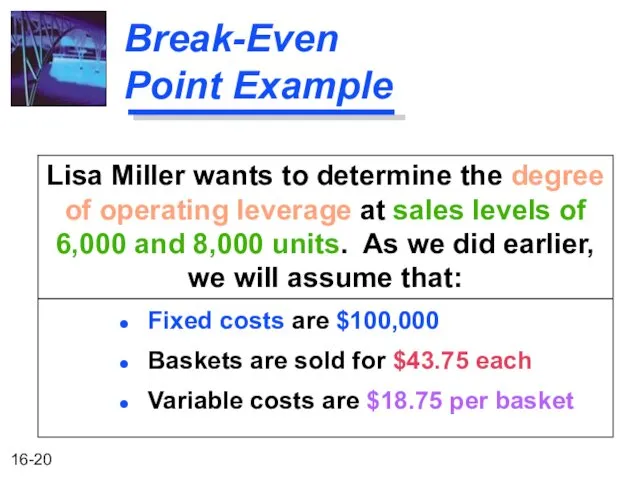

Break-Even Point Example

Lisa Miller wants to determine the degree of operating

Break-Even Point Example

Lisa Miller wants to determine the degree of operating

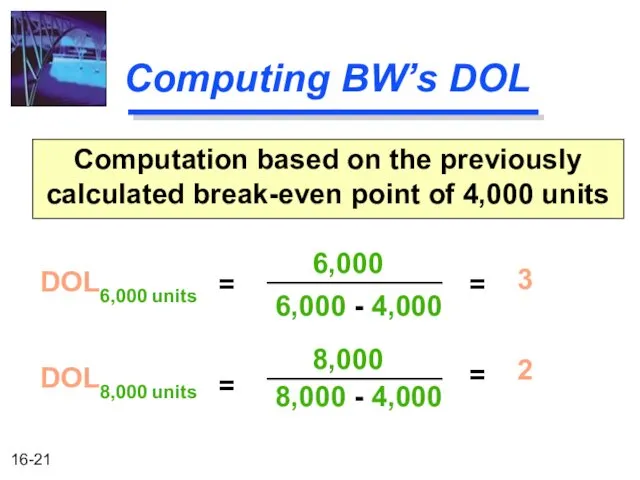

Computing BW’s DOL

DOL6,000 units

Computation based on the previously calculated break-even point

Computing BW’s DOL

DOL6,000 units

Computation based on the previously calculated break-even point

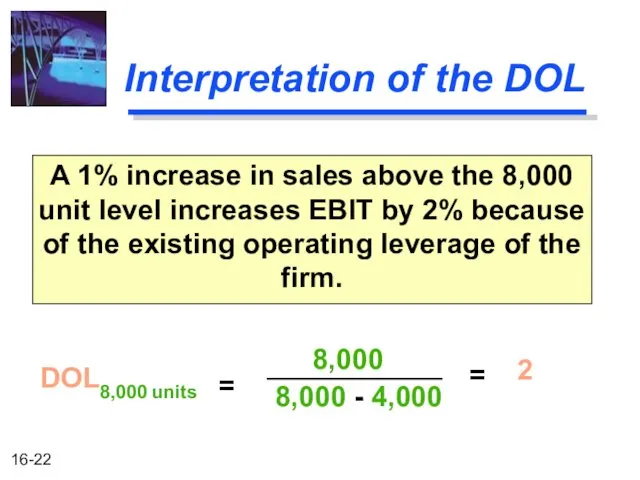

Interpretation of the DOL

A 1% increase in sales above the 8,000

Interpretation of the DOL

A 1% increase in sales above the 8,000

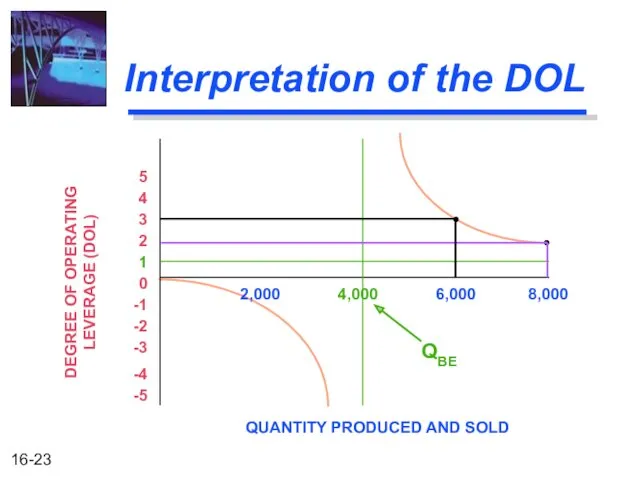

Interpretation of the DOL

2,000 4,000 6,000 8,000

1

2

3

4

5

QUANTITY PRODUCED AND SOLD

0

-1

-2

-3

-4

-5

DEGREE OF

Interpretation of the DOL

2,000 4,000 6,000 8,000

1

2

3

4

5

QUANTITY PRODUCED AND SOLD

0

-1

-2

-3

-4

-5

DEGREE OF

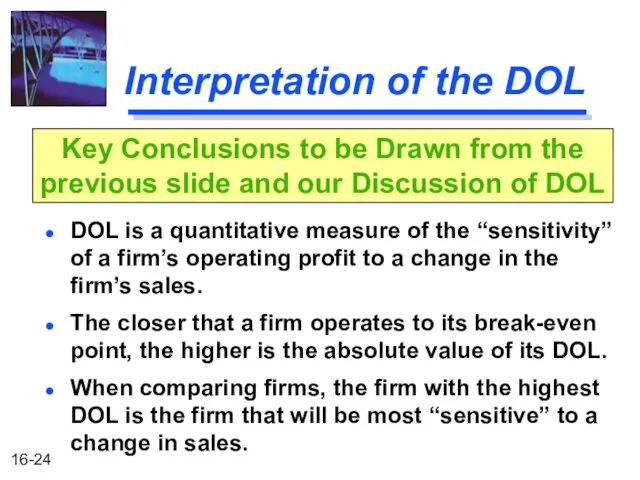

Interpretation of the DOL

DOL is a quantitative measure of the “sensitivity”

Interpretation of the DOL

DOL is a quantitative measure of the “sensitivity”

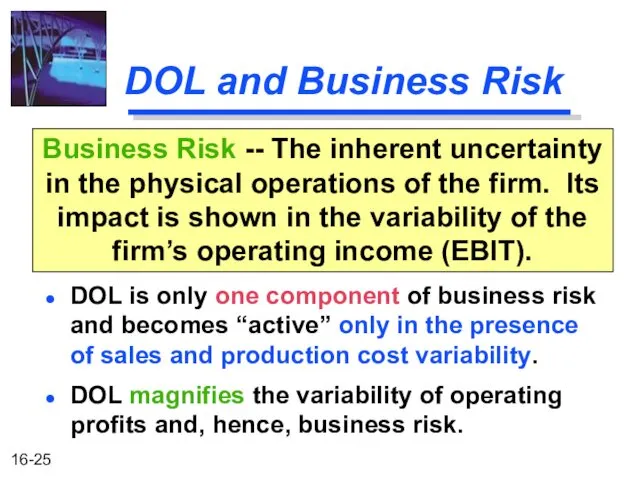

DOL and Business Risk

DOL is only one component of business risk

DOL and Business Risk

DOL is only one component of business risk

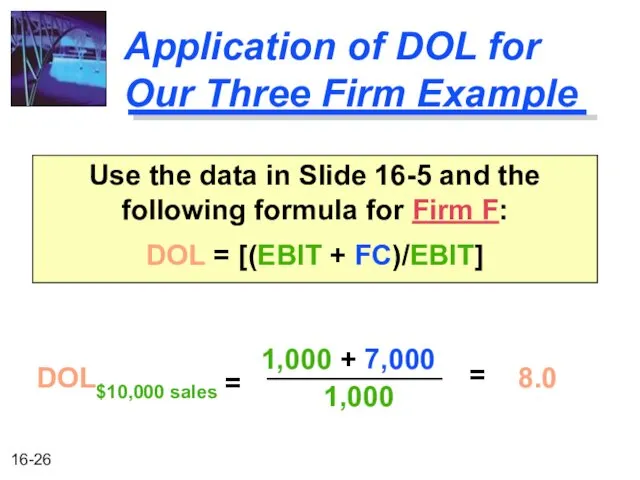

Application of DOL for Our Three Firm Example

Use the data in

Application of DOL for Our Three Firm Example

Use the data in

Application of DOL for Our Three Firm Example

Use the data in

Application of DOL for Our Three Firm Example

Use the data in

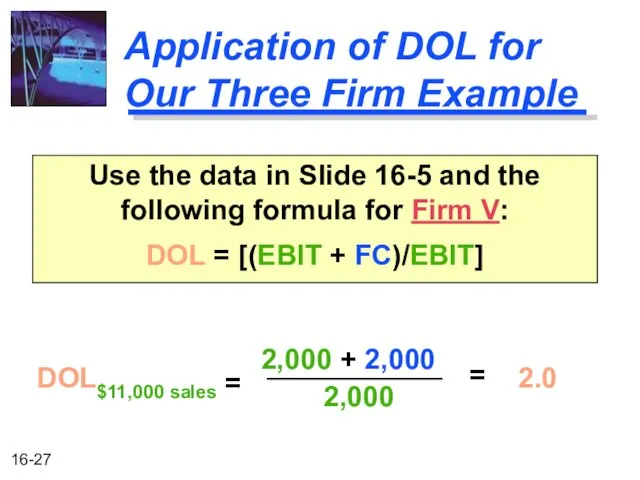

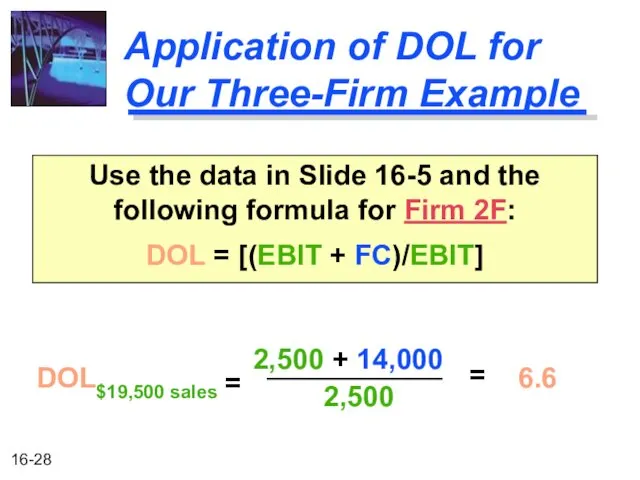

Application of DOL for Our Three-Firm Example

Use the data in Slide

Application of DOL for Our Three-Firm Example

Use the data in Slide

Application of DOL for Our Three-Firm Example

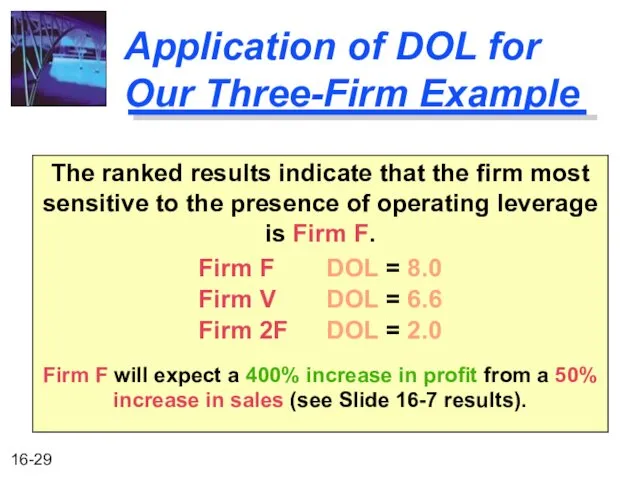

The ranked results indicate that

Application of DOL for Our Three-Firm Example

The ranked results indicate that

Financial Leverage

Financial leverage is acquired by choice.

Used as a means of

Financial Leverage

Financial leverage is acquired by choice.

Used as a means of

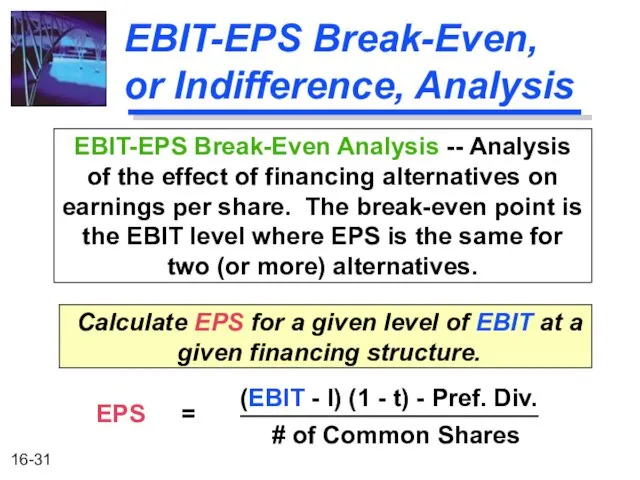

EBIT-EPS Break-Even, or Indifference, Analysis

Calculate EPS for a given level of

EBIT-EPS Break-Even, or Indifference, Analysis

Calculate EPS for a given level of

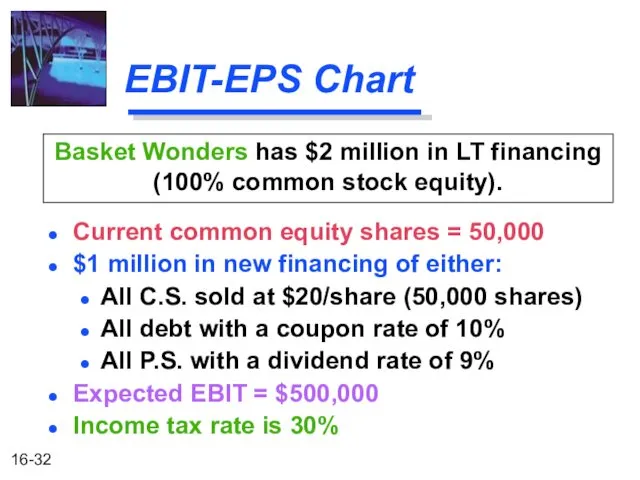

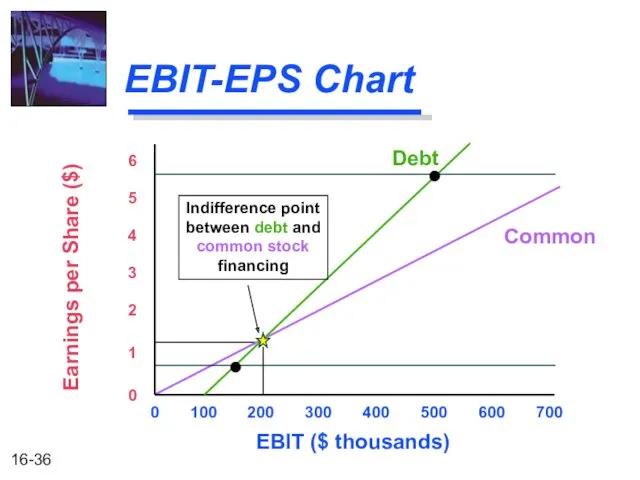

EBIT-EPS Chart

Current common equity shares = 50,000

$1 million in new financing

EBIT-EPS Chart

Current common equity shares = 50,000

$1 million in new financing

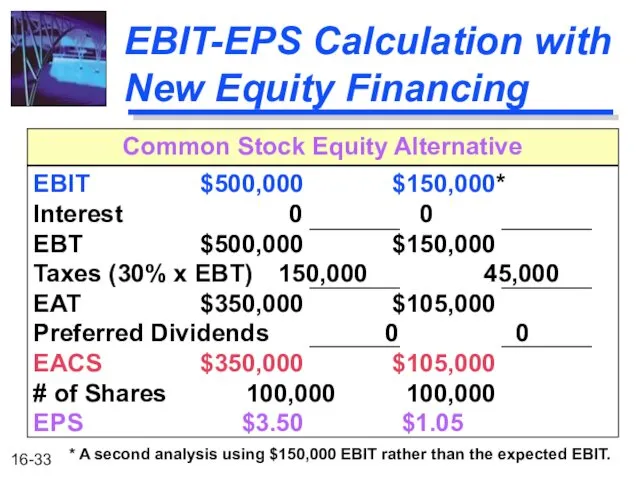

EBIT-EPS Calculation with New Equity Financing

EBIT $500,000 $150,000*

Interest 0 0

EBT $500,000

EBIT-EPS Calculation with New Equity Financing

EBIT $500,000 $150,000*

Interest 0 0

EBT $500,000

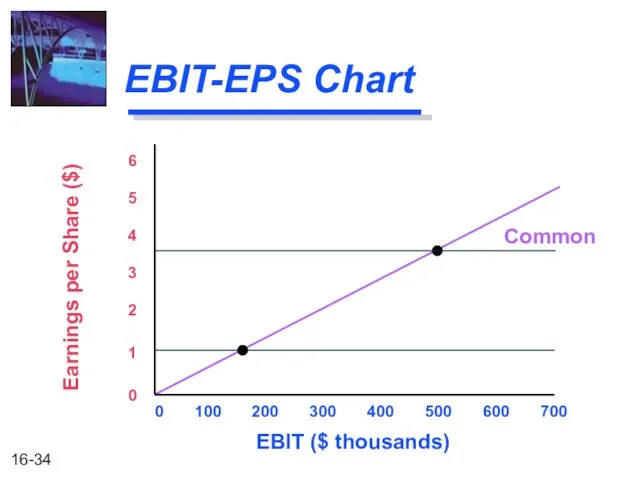

EBIT-EPS Chart

0 100 200 300 400 500 600 700

EBIT ($ thousands)

Earnings

EBIT-EPS Chart

0 100 200 300 400 500 600 700

EBIT ($ thousands)

Earnings

EBIT-EPS Calculation with New Debt Financing

EBIT $500,000 $150,000*

Interest 100,000 100,000

EBT $400,000

EBIT-EPS Calculation with New Debt Financing

EBIT $500,000 $150,000*

Interest 100,000 100,000

EBT $400,000

EBIT-EPS Chart

0 100 200 300 400 500 600 700

EBIT ($ thousands)

Earnings

EBIT-EPS Chart

0 100 200 300 400 500 600 700

EBIT ($ thousands)

Earnings

EBIT-EPS Calculation with New Preferred Financing

EBIT $500,000 $150,000*

Interest 0 0

EBT $500,000

EBIT-EPS Calculation with New Preferred Financing

EBIT $500,000 $150,000*

Interest 0 0

EBT $500,000

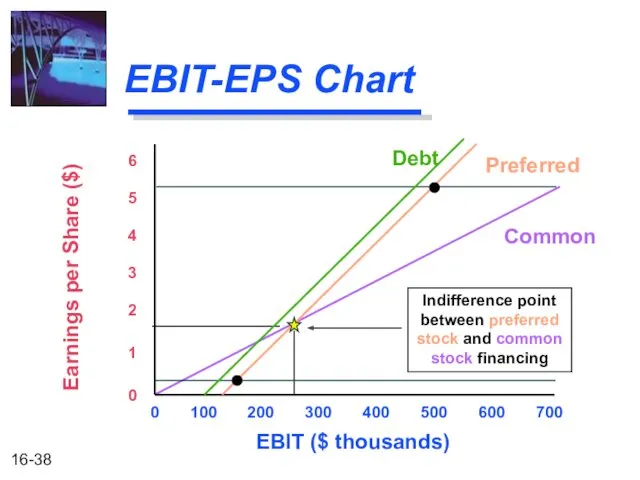

0 100 200 300 400 500 600 700

EBIT-EPS Chart

EBIT ($ thousands)

Earnings

0 100 200 300 400 500 600 700

EBIT-EPS Chart

EBIT ($ thousands)

Earnings

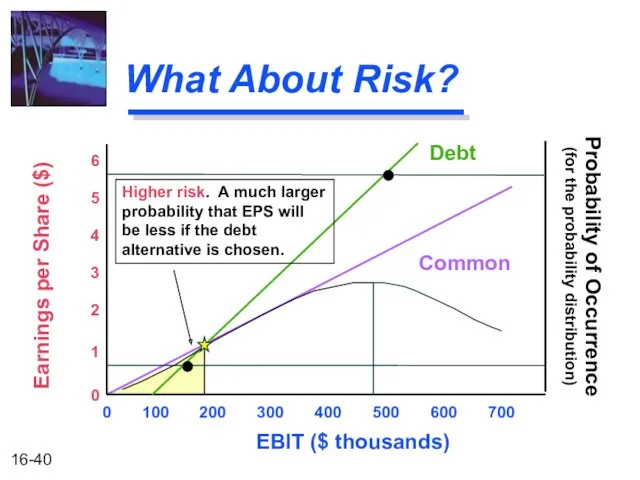

What About Risk?

0 100 200 300 400 500 600 700

EBIT ($

What About Risk?

0 100 200 300 400 500 600 700

EBIT ($

What About Risk?

0 100 200 300 400 500 600 700

EBIT ($

What About Risk?

0 100 200 300 400 500 600 700

EBIT ($

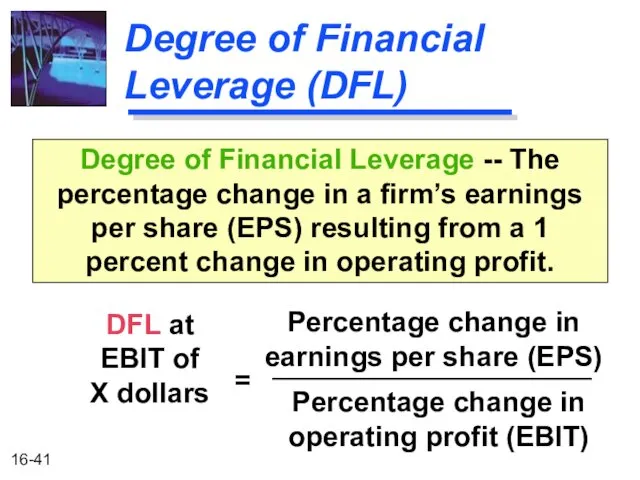

Degree of Financial Leverage (DFL)

DFL at EBIT of X dollars

Degree of

Degree of Financial Leverage (DFL)

DFL at EBIT of X dollars

Degree of

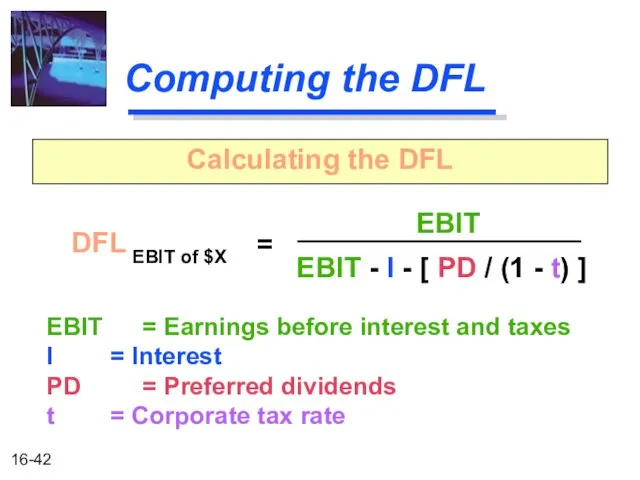

Computing the DFL

DFL EBIT of $X

Calculating the DFL

=

EBIT

EBIT - I -

Computing the DFL

DFL EBIT of $X

Calculating the DFL

=

EBIT

EBIT - I -

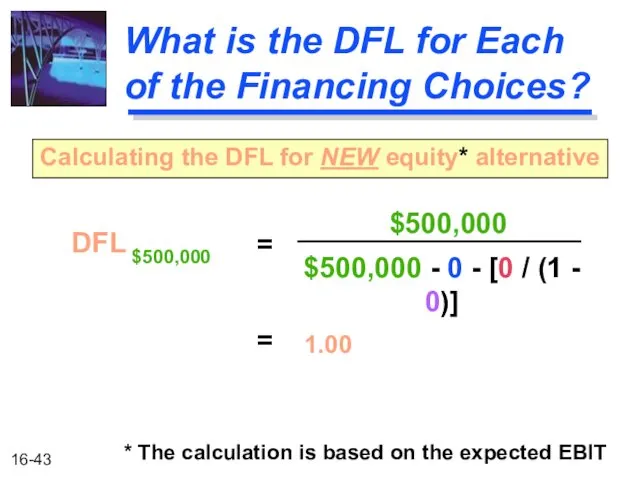

What is the DFL for Each of the Financing Choices?

DFL $500,000

Calculating

What is the DFL for Each of the Financing Choices?

DFL $500,000

Calculating

What is the DFL for Each of the Financing Choices?

DFL $500,000

Calculating

What is the DFL for Each of the Financing Choices?

DFL $500,000

Calculating

What is the DFL for Each of the Financing Choices?

DFL $500,000

Calculating

What is the DFL for Each of the Financing Choices?

DFL $500,000

Calculating

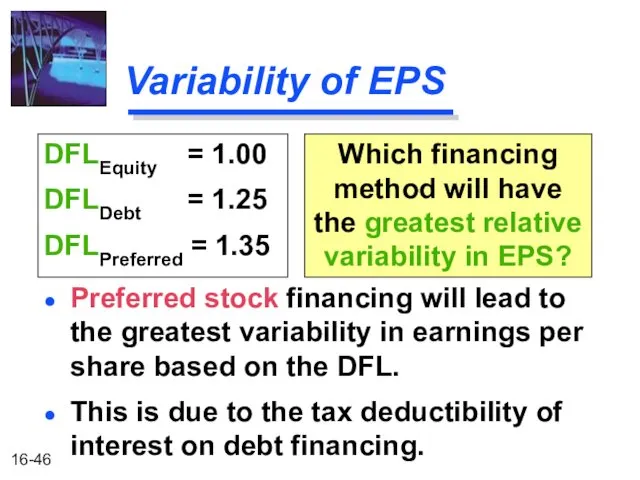

Variability of EPS

Preferred stock financing will lead to the greatest variability

Variability of EPS

Preferred stock financing will lead to the greatest variability

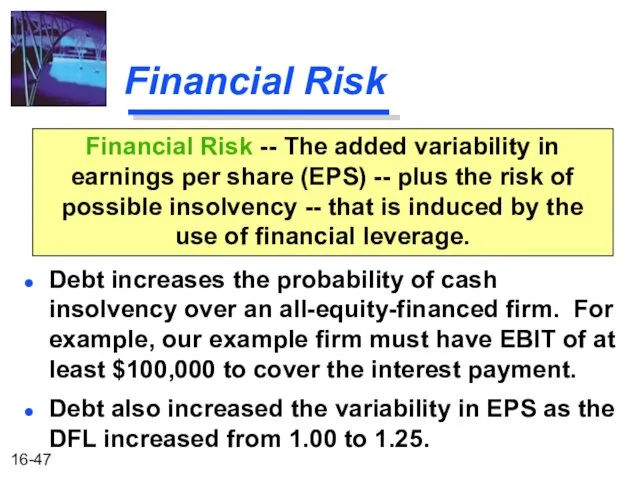

Financial Risk

Debt increases the probability of cash insolvency over an all-equity-financed

Financial Risk

Debt increases the probability of cash insolvency over an all-equity-financed

Total Firm Risk

CVEPS is a measure of relative total firm risk

CVEBIT

Total Firm Risk

CVEPS is a measure of relative total firm risk

CVEBIT

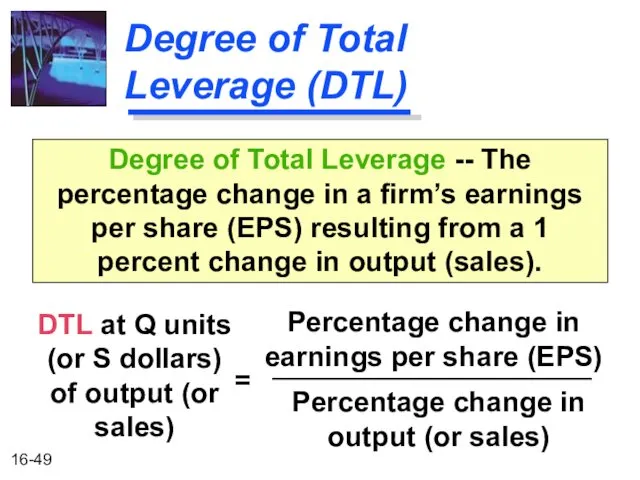

Degree of Total Leverage (DTL)

DTL at Q units (or S dollars)

Degree of Total Leverage (DTL)

DTL at Q units (or S dollars)

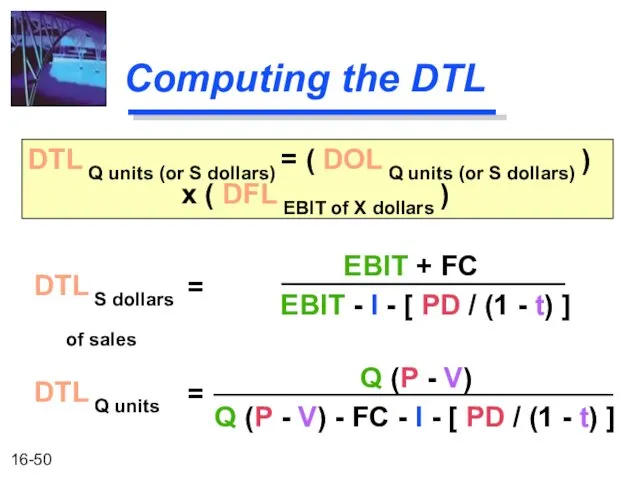

Computing the DTL

DTL S dollars

of sales

DTL Q units (or S dollars)

Computing the DTL

DTL S dollars

of sales

DTL Q units (or S dollars)

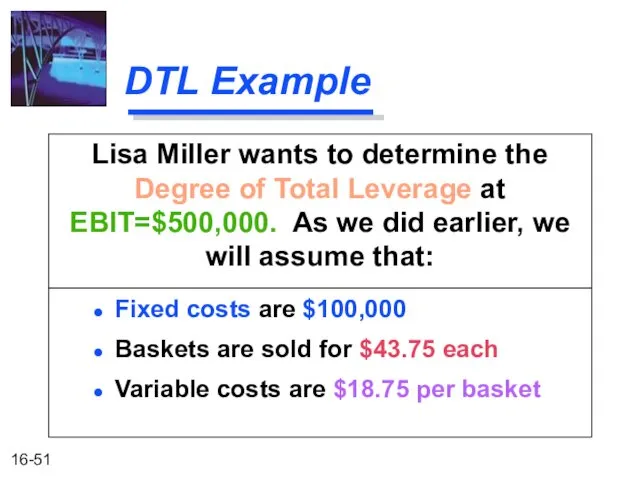

DTL Example

Lisa Miller wants to determine the Degree of Total Leverage

DTL Example

Lisa Miller wants to determine the Degree of Total Leverage

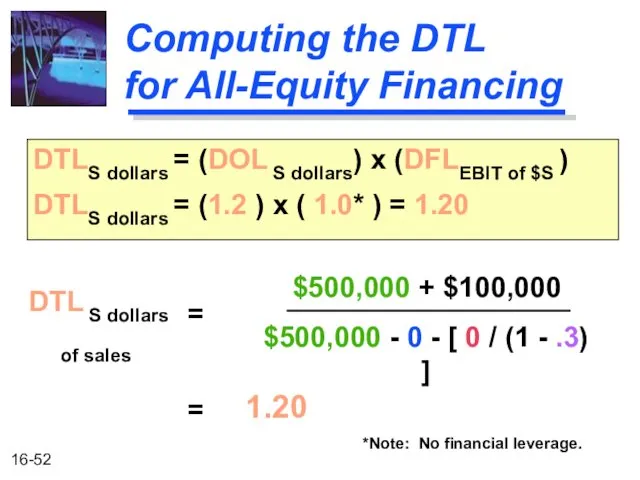

Computing the DTL

for All-Equity Financing

DTL S dollars

of sales

=

$500,000 + $100,000

$500,000

Computing the DTL

for All-Equity Financing

DTL S dollars

of sales

=

$500,000 + $100,000

$500,000

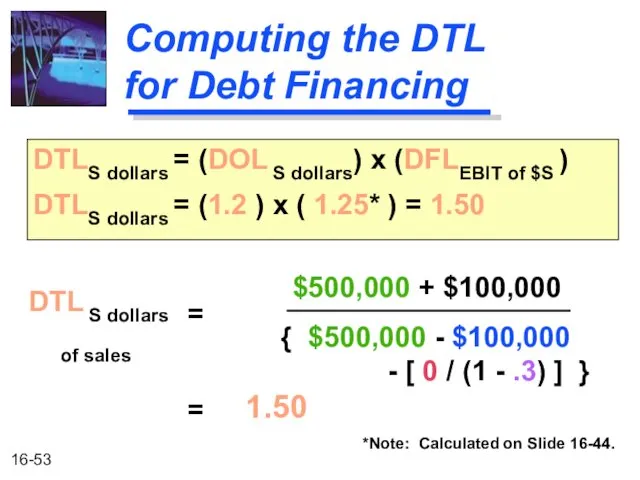

Computing the DTL

for Debt Financing

DTL S dollars

of sales

=

$500,000 + $100,000

{

Computing the DTL

for Debt Financing

DTL S dollars

of sales

=

$500,000 + $100,000

{

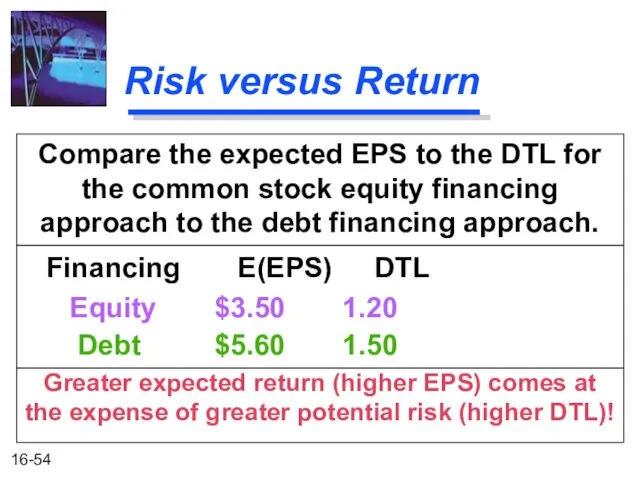

Risk versus Return

Compare the expected EPS to the DTL for the

Risk versus Return

Compare the expected EPS to the DTL for the

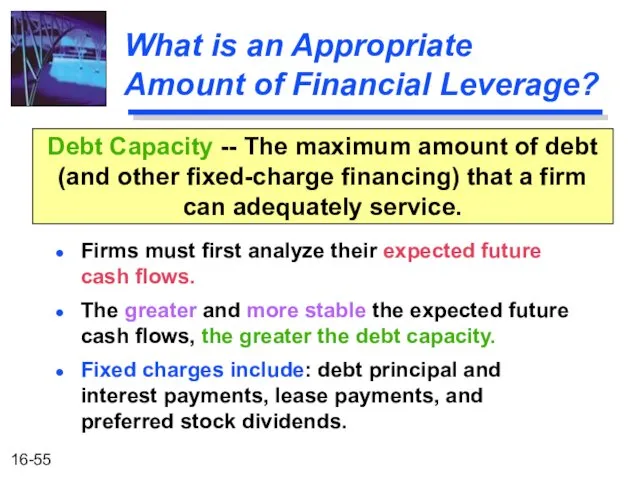

What is an Appropriate

Amount of Financial Leverage?

Firms must first analyze

What is an Appropriate

Amount of Financial Leverage?

Firms must first analyze

Coverage Ratios

Interest Coverage

EBIT

Interest expenses

Indicates a firm’s ability to cover interest charges.

Income

Coverage Ratios

Interest Coverage

EBIT

Interest expenses

Indicates a firm’s ability to cover interest charges.

Income

Coverage Ratios

Debt-service Coverage

EBIT

{ Interest expenses + [Principal payments / (1-t) ]

Coverage Ratios

Debt-service Coverage

EBIT

{ Interest expenses + [Principal payments / (1-t) ]

Coverage Example

Make an examination of the coverage ratios for Basket Wonders

Coverage Example

Make an examination of the coverage ratios for Basket Wonders

Coverage Example

Compare the interest coverage and debt burden ratios for equity

Coverage Example

Compare the interest coverage and debt burden ratios for equity

Coverage Example

-250 0 250 500 750 1,000 1,250

EBIT ($ thousands)

Firm B

Coverage Example

-250 0 250 500 750 1,000 1,250

EBIT ($ thousands)

Firm B

Summary of the Coverage Ratio Discussion

A single ratio value cannot be

Summary of the Coverage Ratio Discussion

A single ratio value cannot be

Other Methods of Analysis

Often, firms are compared to peer institutions in

Other Methods of Analysis

Often, firms are compared to peer institutions in

Other Methods of Analysis

Firms may gain insight into the financial markets’

Other Methods of Analysis

Firms may gain insight into the financial markets’

Презентация о моей работе

Презентация о моей работе Оценка качества зданий. Показатели качества зданий. Обследование зданий

Оценка качества зданий. Показатели качества зданий. Обследование зданий Вокальная музыка. (5 класс)

Вокальная музыка. (5 класс) Заповедники и славянофилы

Заповедники и славянофилы Основные понятия и определения делопроизводства

Основные понятия и определения делопроизводства Тайна имени

Тайна имени Пивоварня Anchor

Пивоварня Anchor Математическое моделирование и численные методы в инженерных задачах

Математическое моделирование и численные методы в инженерных задачах Основы генетики

Основы генетики Контроль, как функция менеджмента. (Тема 12)

Контроль, как функция менеджмента. (Тема 12) Омонимы разработка урока по татарскому языку.

Омонимы разработка урока по татарскому языку. Сдай макулатуру спаси дерево Сережкина (1)

Сдай макулатуру спаси дерево Сережкина (1) Прощай Букварь! Сау бул Әлифба!

Прощай Букварь! Сау бул Әлифба! 17424-ulitsy-goroda-tambova-vosstanovlen.pptx

17424-ulitsy-goroda-tambova-vosstanovlen.pptx Континент Антарктида

Континент Антарктида Мастер - класс для родителей Народная кукла - как источник развития ребёнка

Мастер - класс для родителей Народная кукла - как источник развития ребёнка Презентация по татарскому языку 2 класс. Тема Шәхси гигиена.

Презентация по татарскому языку 2 класс. Тема Шәхси гигиена. Витамины - общая характеристика.

Витамины - общая характеристика. Ислам діні.Суннит

Ислам діні.Суннит Презентация Путешествие Лунтика по планете Земля

Презентация Путешествие Лунтика по планете Земля Ферменты (10 класс)

Ферменты (10 класс) Технология нанесения антикоррозионных покрытий

Технология нанесения антикоррозионных покрытий Нефтяная и газовая промышленность

Нефтяная и газовая промышленность проектная работа Знакомьтесь - ёжик!

проектная работа Знакомьтесь - ёжик! Мифы о поколении Z

Мифы о поколении Z Циклы поршневых двигателей внутреннего сгорания

Циклы поршневых двигателей внутреннего сгорания Обзор технологий заканчивания скважин для многостадийного ГРП

Обзор технологий заканчивания скважин для многостадийного ГРП Изготовление бахил

Изготовление бахил