Demand is the economic term for the cumulative wants and desires of consumers as they relate to a particular good or service презентация

- Demand is the economic term for the cumulative wants and desires of consumers as they relate to a particular good or service

Содержание

- 2. Plan Demand. What is demand? The Law of Demand Determinants of (Factors affecting) demand Excess demand

- 3. Demand is the economic term for the cumulative wants and desires of consumers as they relate

- 4. The figure above depicts the most basic relationship between the price of a good and its

- 5. For purposes of our discussion, let's assume that the product in question is television sets. If

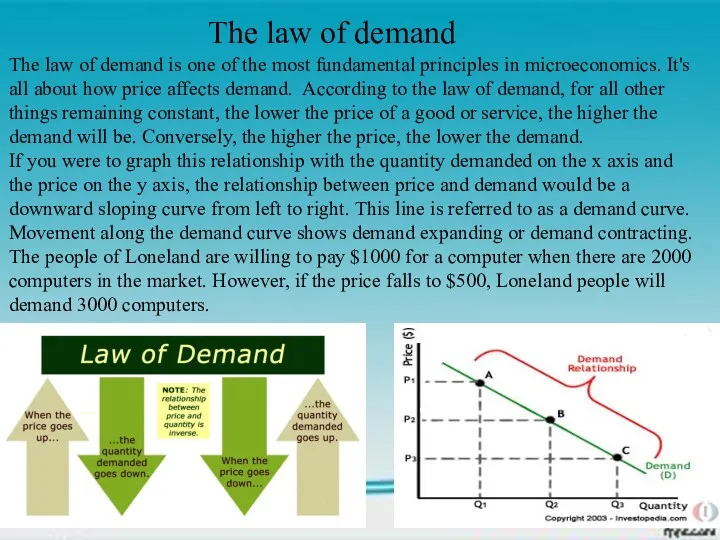

- 6. The law of demand is one of the most fundamental principles in microeconomics. It's all about

- 7. This is an example of a change in the demand curve where price is the only

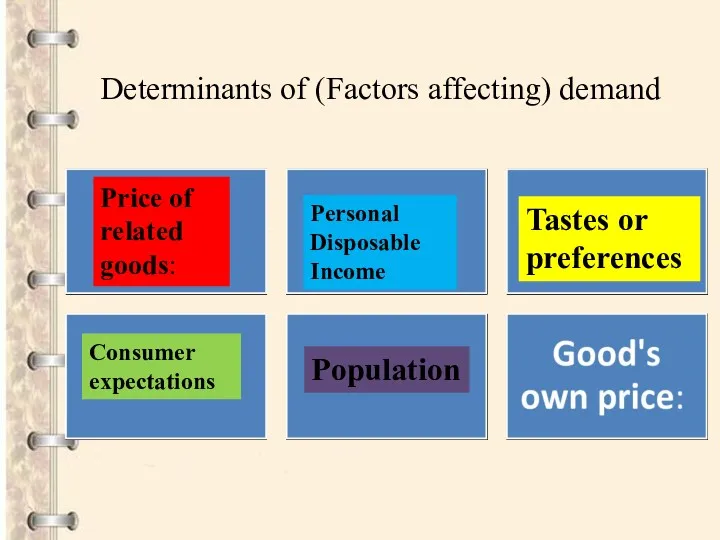

- 8. Determinants of (Factors affecting) demand Price of related goods: Personal Disposable Income Tastes or preferences Consumer

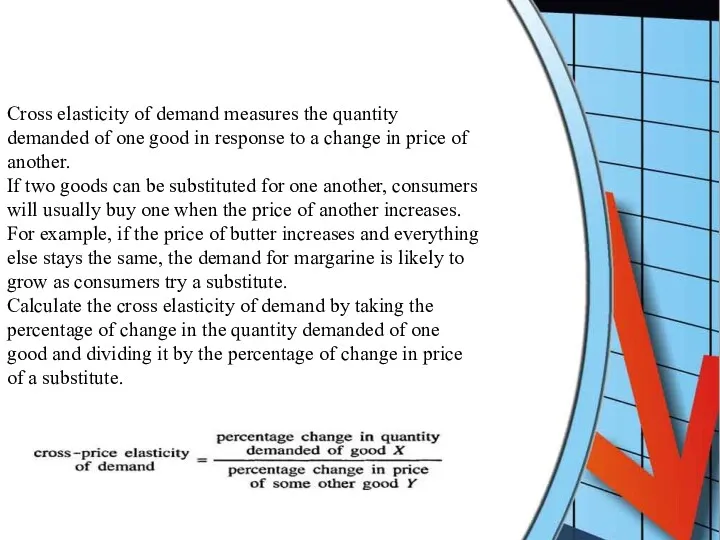

- 9. Cross elasticity of demand measures the quantity demanded of one good in response to a change

- 10. Income elasticity of demand is a measure of how consumer demand changes when income changes. The

- 11. Excess Demand Excess demand is created when price is set below the equilibrium price. Because the

- 12. 1.Marshall, Alfred and Mary Paley Marshall (1879). The Economics of Industry. 2.The Concise Encyclopedia of Economics.'.'

- 15. Скачать презентацию

Plan

Demand. What is demand?

The Law of Demand

Determinants of (Factors affecting) demand

Excess

Plan

Demand. What is demand?

The Law of Demand

Determinants of (Factors affecting) demand

Excess

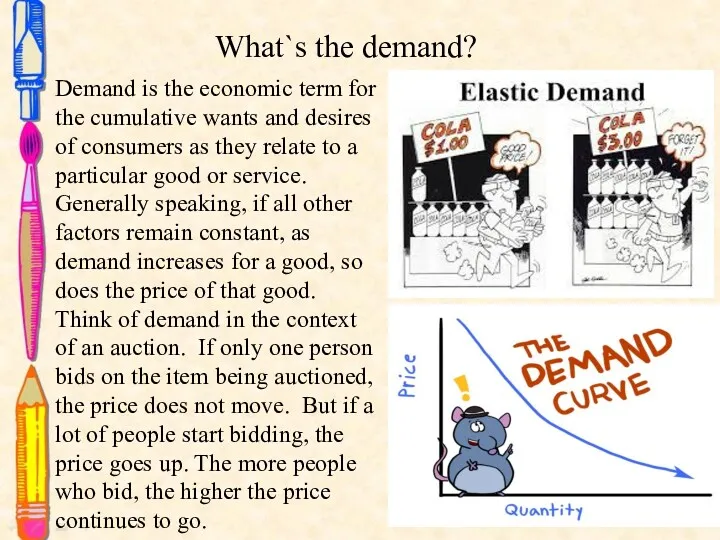

Demand is the economic term for the cumulative wants and desires

Demand is the economic term for the cumulative wants and desires

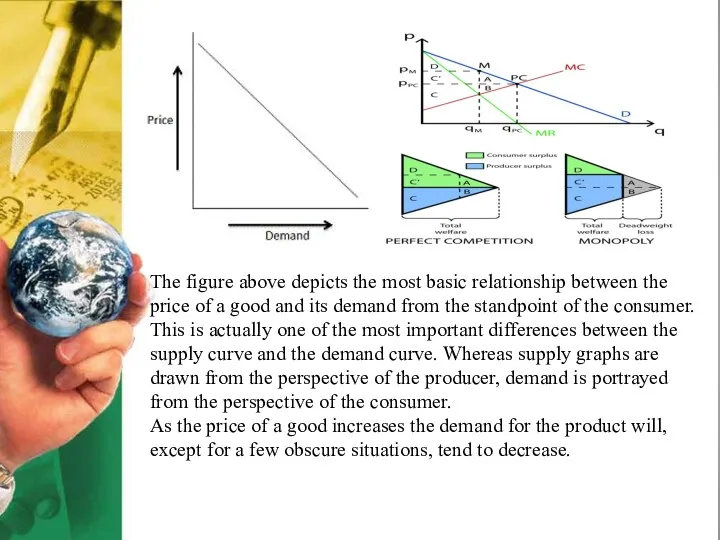

The figure above depicts the most basic relationship between the price

The figure above depicts the most basic relationship between the price

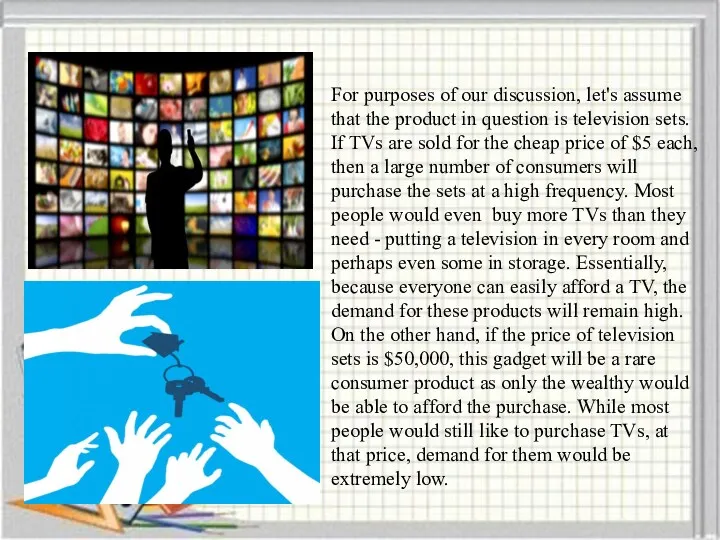

For purposes of our discussion, let's assume that the product in

For purposes of our discussion, let's assume that the product in

The law of demand is one of the most fundamental principles

The law of demand is one of the most fundamental principles

This is an example of a change in the demand curve

This is an example of a change in the demand curve

Determinants of (Factors affecting) demand

Price of related goods:

Personal Disposable Income

Tastes or

Determinants of (Factors affecting) demand

Price of related goods:

Personal Disposable Income

Tastes or

Cross elasticity of demand measures the quantity demanded of one good in

Cross elasticity of demand measures the quantity demanded of one good in

Income elasticity of demand is a measure of how consumer demand changes

Income elasticity of demand is a measure of how consumer demand changes

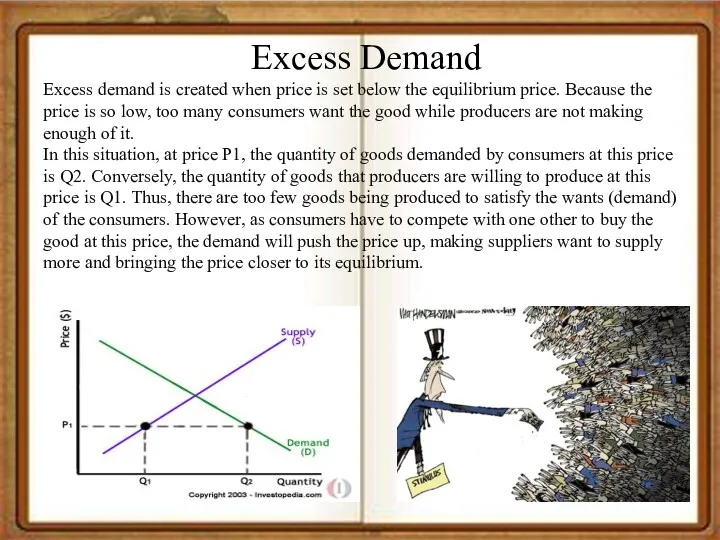

Excess Demand

Excess demand is created when price is set below

Excess Demand

Excess demand is created when price is set below

1.Marshall, Alfred and Mary Paley Marshall (1879). The Economics of Industry.

2.The Concise Encyclopedia of

1.Marshall, Alfred and Mary Paley Marshall (1879). The Economics of Industry.

2.The Concise Encyclopedia of

Современная международная торговая система (СМТС) и ВТО

Современная международная торговая система (СМТС) и ВТО Роль воды в жизни человека

Роль воды в жизни человека Государственное регулирование экономики США

Государственное регулирование экономики США Анализ основных показателей НТП

Анализ основных показателей НТП Макроэкономическое планирование и прогнозирование. Тема 4

Макроэкономическое планирование и прогнозирование. Тема 4 Какое будущее создадите вы

Какое будущее создадите вы Макроэкономическая политика реиндустриализации и импортозамещения

Макроэкономическая политика реиндустриализации и импортозамещения Торгово-экономические отношения России и Чехии

Торгово-экономические отношения России и Чехии Особенности участия субъектов МСП в закупках крупнейших заказчиков в моногородах

Особенности участия субъектов МСП в закупках крупнейших заказчиков в моногородах Международные экономические отношения

Международные экономические отношения Постсоветское пространство. Укрепление влияния России и его кризис

Постсоветское пространство. Укрепление влияния России и его кризис Человеческий капитал города. Активация

Человеческий капитал города. Активация Человеческий капитал как фактор развития национальной экономики

Человеческий капитал как фактор развития национальной экономики Бизнес-модель, бюджет проекта и его экономические показатели

Бизнес-модель, бюджет проекта и его экономические показатели Моделирование потребления населения

Моделирование потребления населения Капитал: сущность, формы

Капитал: сущность, формы Монополистическая конкуренция и олигополия. Тема 15

Монополистическая конкуренция и олигополия. Тема 15 Экономические системы

Экономические системы Экономическая теория образования

Экономическая теория образования Учетная политика для целей налогообложения

Учетная политика для целей налогообложения Коммерциялық банктің қызметін талдаудың мазмұны, түрлері мен әдістері

Коммерциялық банктің қызметін талдаудың мазмұны, түрлері мен әдістері Диагностика социально-экономического развития Южного Федерального округа

Диагностика социально-экономического развития Южного Федерального округа Theoretical framework, objectives and principles of competition

Theoretical framework, objectives and principles of competition Экономический кризис 1929-1933 год

Экономический кризис 1929-1933 год Экономиканың төрт секторы. Географиялық ақпараттық жүйе (ГАЖ), технополис

Экономиканың төрт секторы. Географиялық ақпараттық жүйе (ГАЖ), технополис презентация Богатство страны

презентация Богатство страны Экономика, как наука

Экономика, как наука Предмет экономики

Предмет экономики