- Hall ARCH and GARCH

Содержание

- 2. REFS A thorough introduction ‘ARCH Models’ Bollerslev T, Engle R F and Nelson D B Handbook

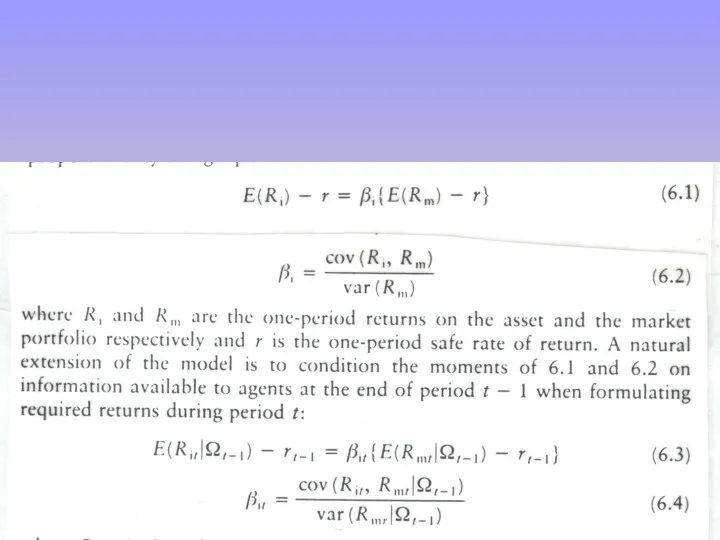

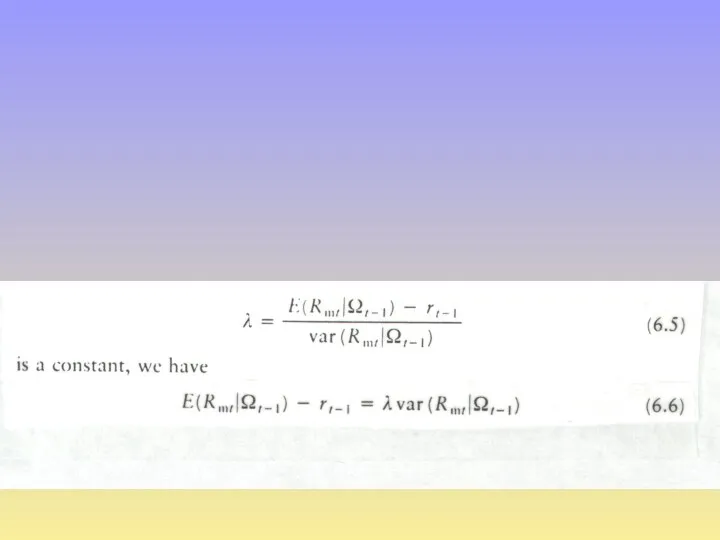

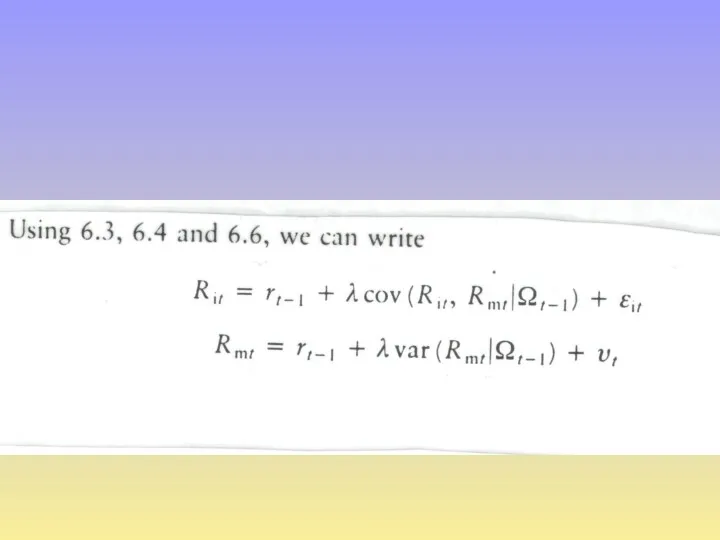

- 3. Until the early 80s econometrics had focused almost solely on modelling the means of series, ie

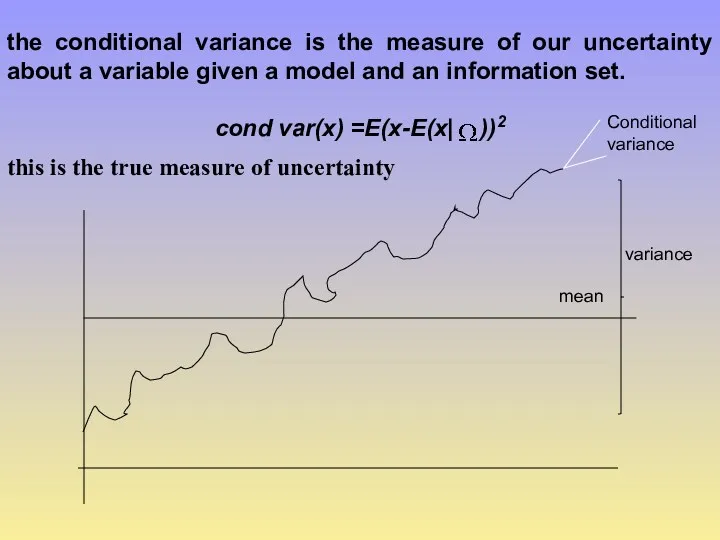

- 4. the conditional variance is the measure of our uncertainty about a variable given a model and

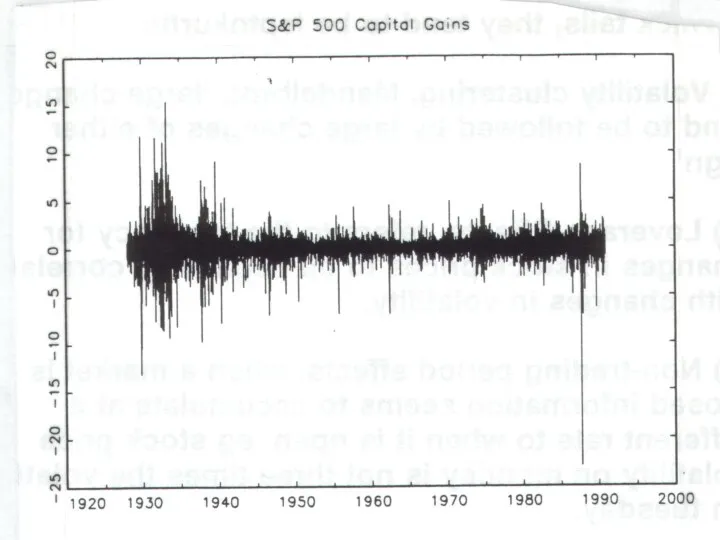

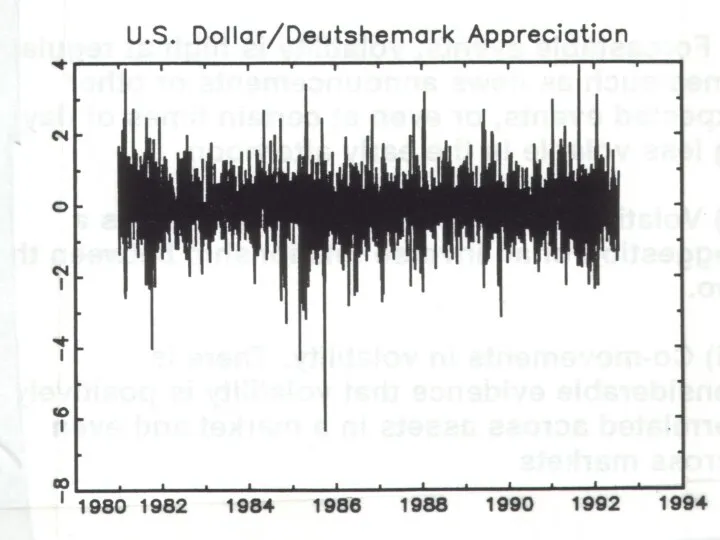

- 5. Stylised Facts of asset returns i) Thick tails, they tend to be leptokurtic ii)Volatility clustering, Mandelbrot,

- 6. vi)Volatility and serial correlation. There is a suggestion of an inverse relationship between the two. vii)

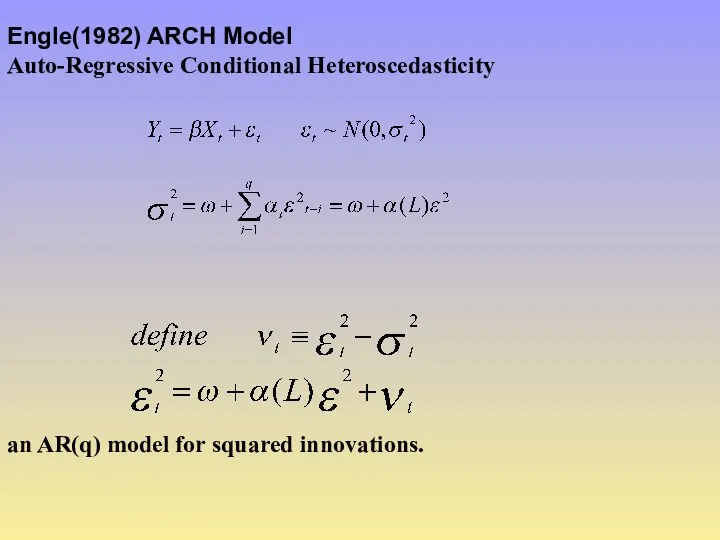

- 9. Engle(1982) ARCH Model Auto-Regressive Conditional Heteroscedasticity an AR(q) model for squared innovations.

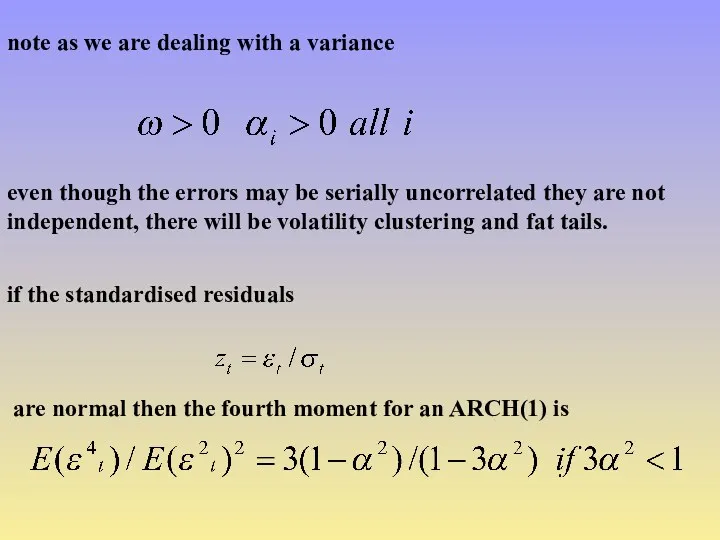

- 10. note as we are dealing with a variance even though the errors may be serially uncorrelated

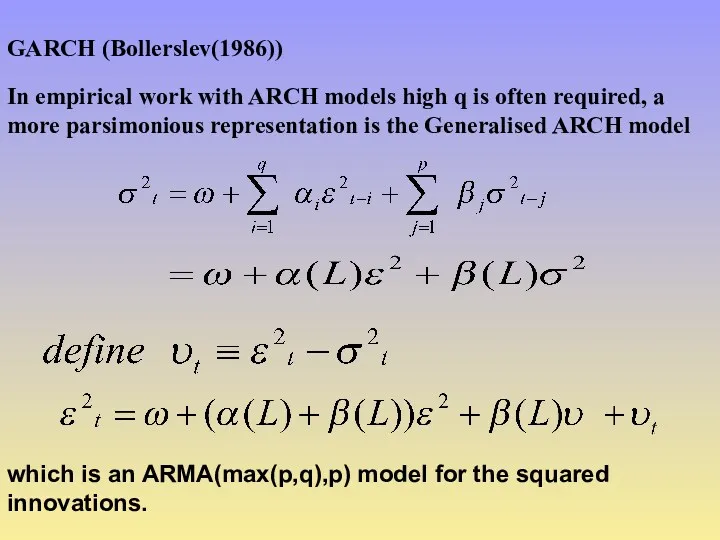

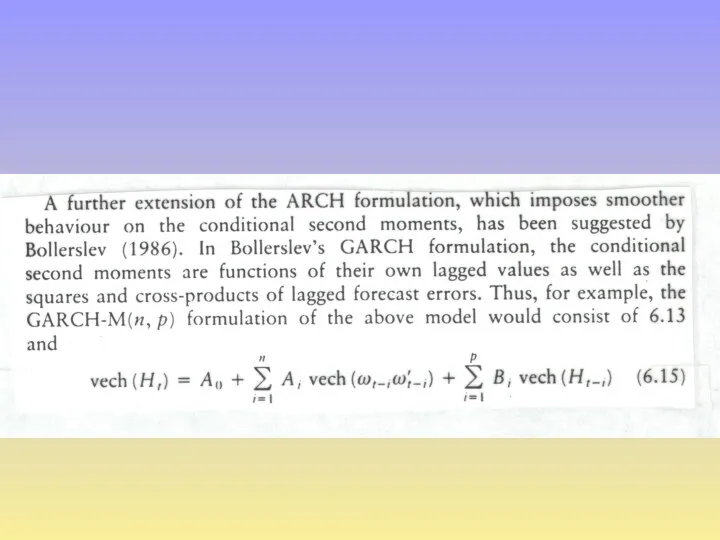

- 11. GARCH (Bollerslev(1986)) In empirical work with ARCH models high q is often required, a more parsimonious

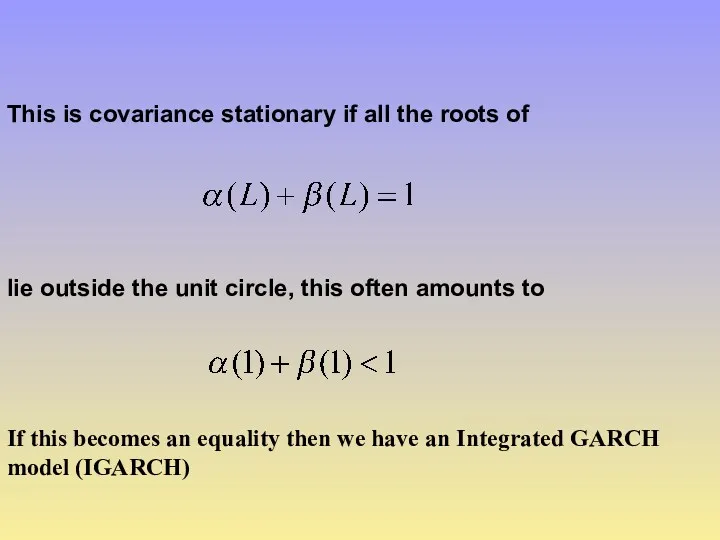

- 12. This is covariance stationary if all the roots of lie outside the unit circle, this often

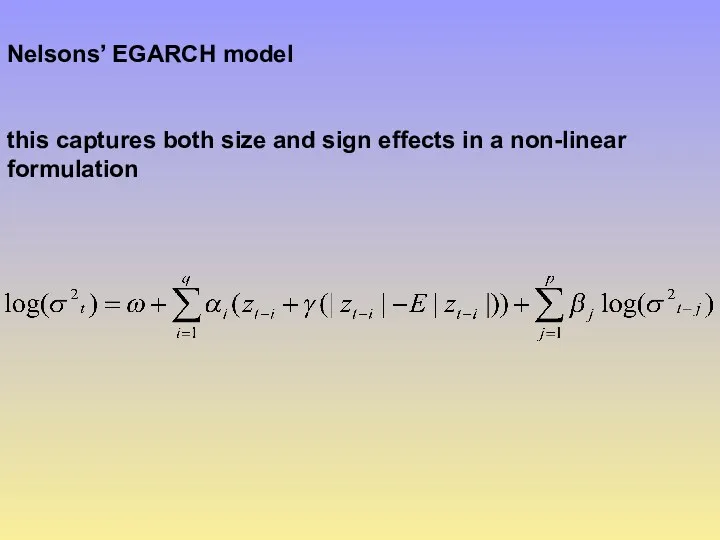

- 13. Nelsons’ EGARCH model this captures both size and sign effects in a non-linear formulation

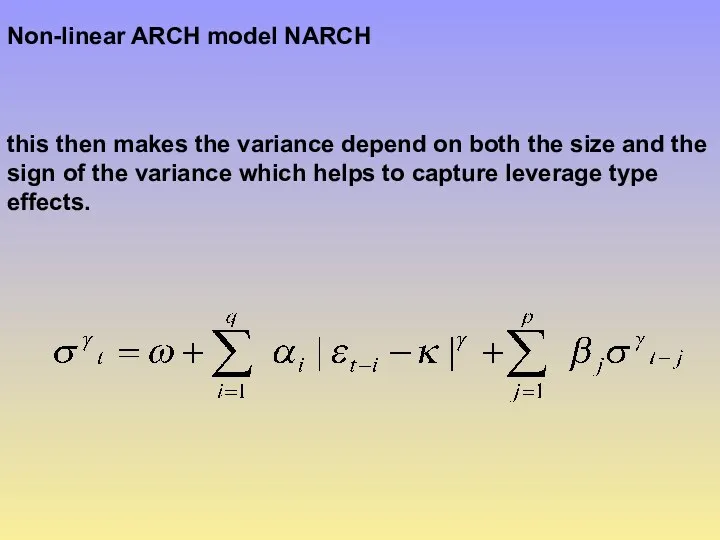

- 14. Non-linear ARCH model NARCH this then makes the variance depend on both the size and the

- 15. Threshold ARCH (TARCH) Many other versions are possible by adding minor asymmetries or non-linearities in a

- 16. All of these are simply estimated by maximum likelihood using the same basic likelihood function, assuming

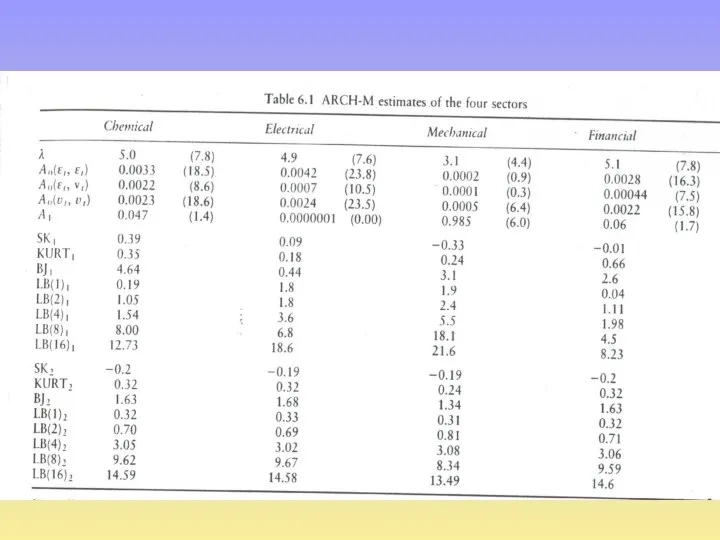

- 17. ARCH in MEAN (G)ARCH-M Many classic areas of finance suggest that the mean of a relationship

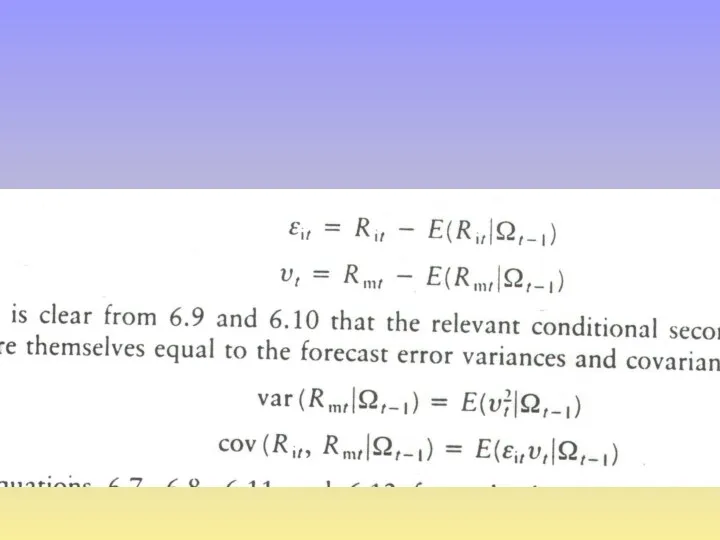

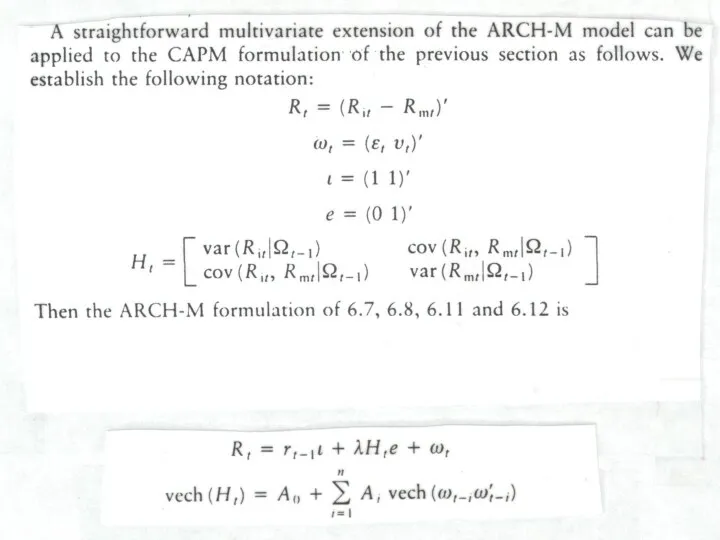

- 18. often finance stresses the importance of covariance terms. The above model can handle this if y

- 19. Non normality assumptions While the basic GARCH model allows a certain amount of leptokurtic behaviour this

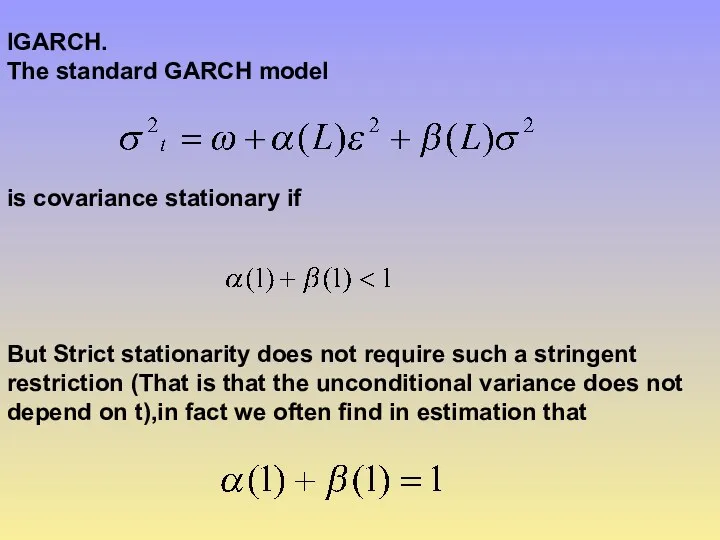

- 20. IGARCH. The standard GARCH model is covariance stationary if But Strict stationarity does not require such

- 21. this is then termed an Integrated GARCH model (IGARCH), Nelson has established that as this satisfies

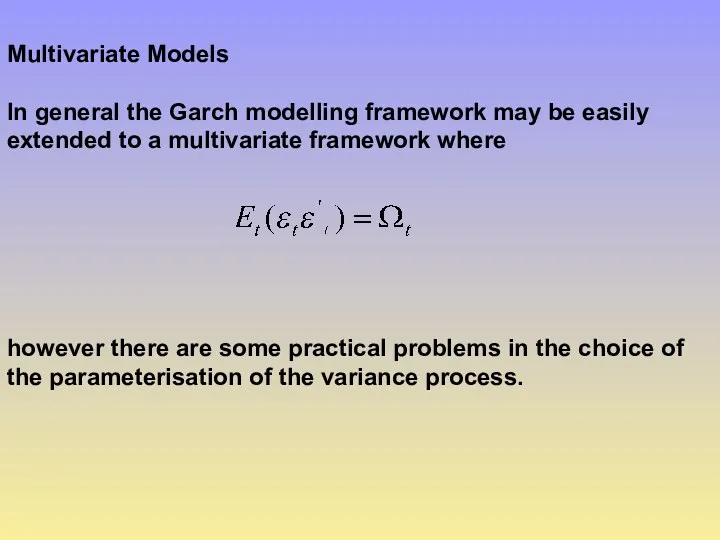

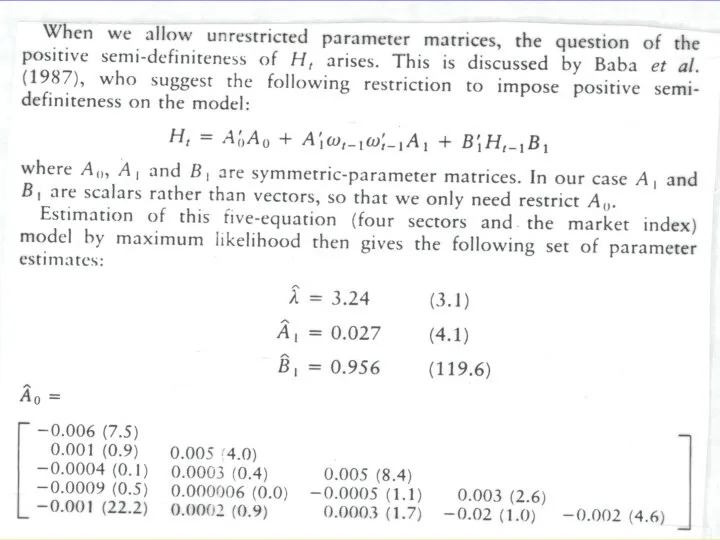

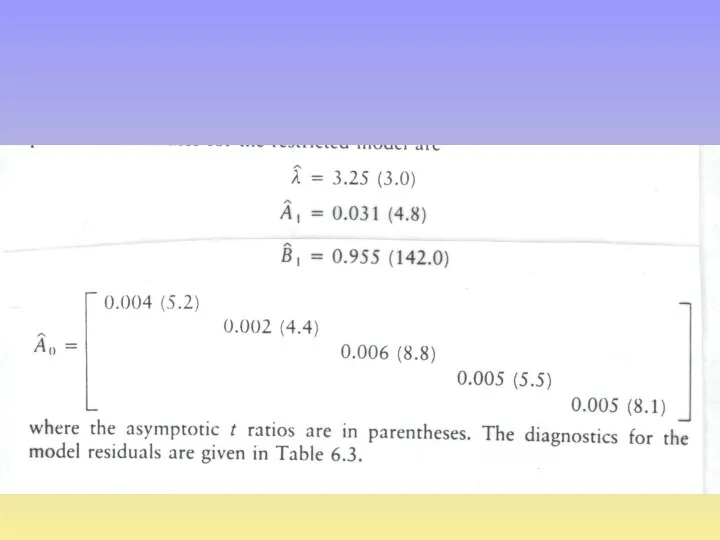

- 22. Multivariate Models In general the Garch modelling framework may be easily extended to a multivariate framework

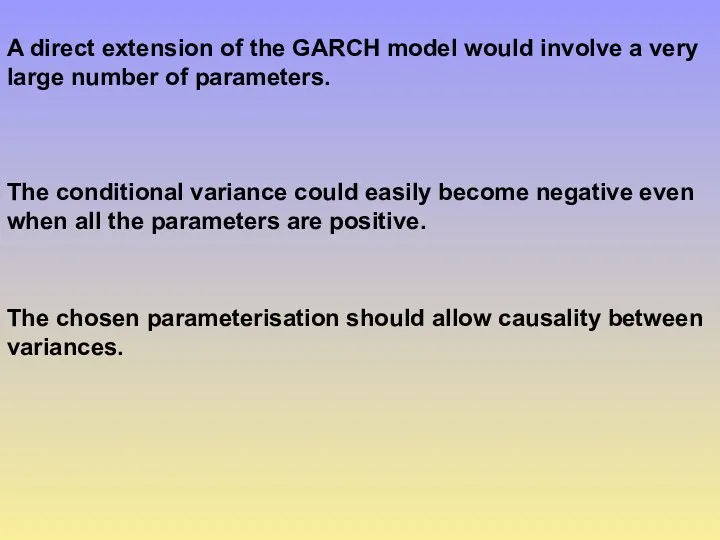

- 23. The conditional variance could easily become negative even when all the parameters are positive. A direct

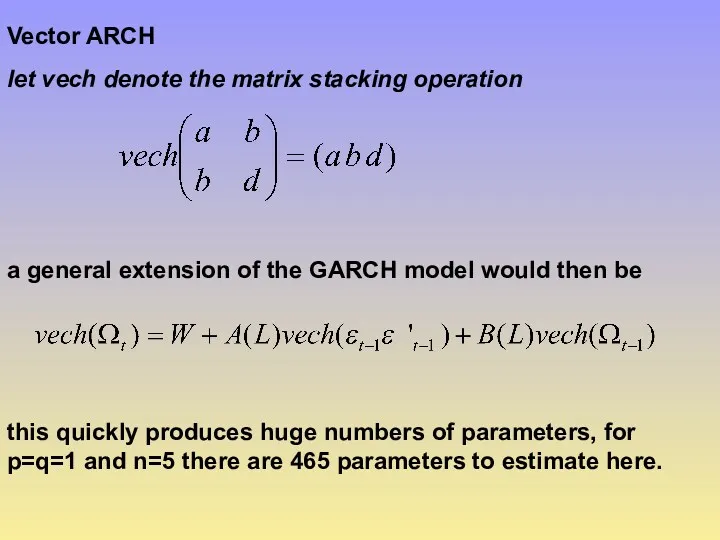

- 24. Vector ARCH let vech denote the matrix stacking operation a general extension of the GARCH model

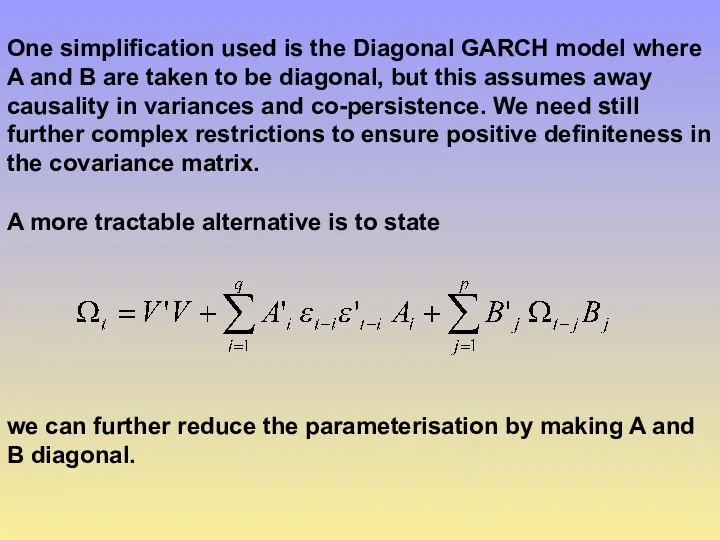

- 25. One simplification used is the Diagonal GARCH model where A and B are taken to be

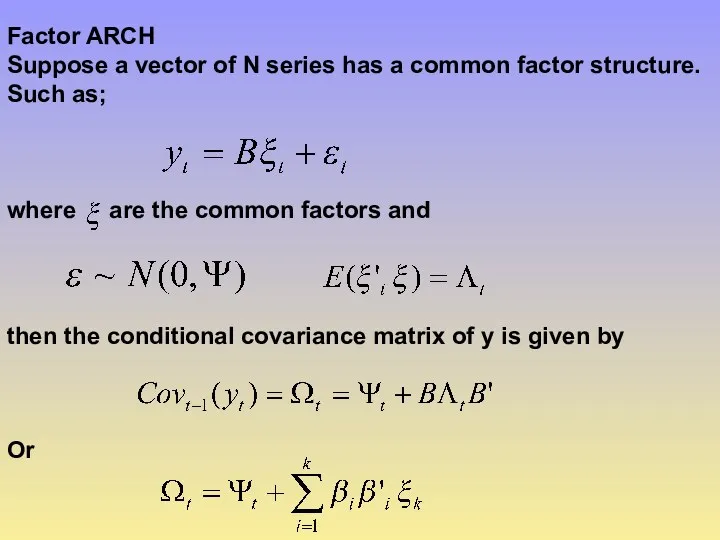

- 26. Factor ARCH Suppose a vector of N series has a common factor structure. Such as; where

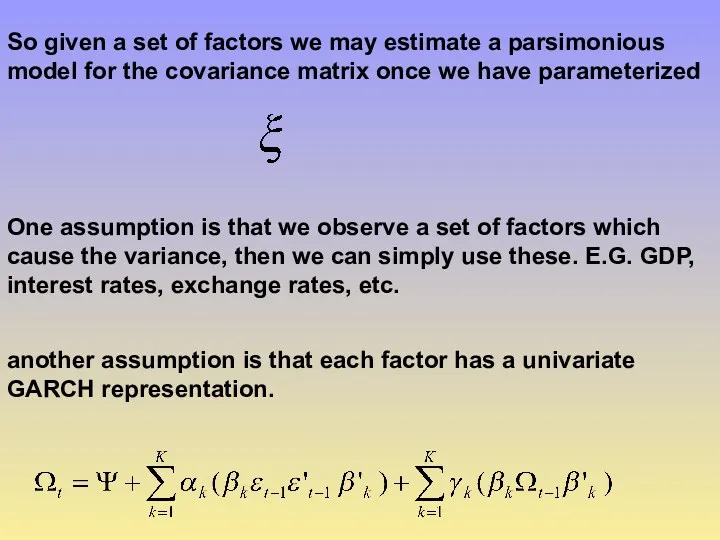

- 27. So given a set of factors we may estimate a parsimonious model for the covariance matrix

- 40. Скачать презентацию

REFS

A thorough introduction

‘ARCH Models’ Bollerslev T, Engle R F and Nelson

REFS

A thorough introduction

‘ARCH Models’ Bollerslev T, Engle R F and Nelson

Until the early 80s econometrics had focused almost solely on modelling

Until the early 80s econometrics had focused almost solely on modelling

the conditional variance is the measure of our uncertainty about a

the conditional variance is the measure of our uncertainty about a

Stylised Facts of asset returns

i) Thick tails, they tend to be

Stylised Facts of asset returns

i) Thick tails, they tend to be

vi)Volatility and serial correlation. There is a suggestion of an inverse

vi)Volatility and serial correlation. There is a suggestion of an inverse

Engle(1982) ARCH Model

Auto-Regressive Conditional Heteroscedasticity

an AR(q) model for squared innovations.

Engle(1982) ARCH Model

Auto-Regressive Conditional Heteroscedasticity

an AR(q) model for squared innovations.

note as we are dealing with a variance

even though the

note as we are dealing with a variance

even though the

GARCH (Bollerslev(1986))

In empirical work with ARCH models high q is

GARCH (Bollerslev(1986))

In empirical work with ARCH models high q is

This is covariance stationary if all the roots of

lie outside

This is covariance stationary if all the roots of

lie outside

Nelsons’ EGARCH model

this captures both size and sign effects in a

Nelsons’ EGARCH model

this captures both size and sign effects in a

Non-linear ARCH model NARCH

this then makes the variance depend on

Non-linear ARCH model NARCH

this then makes the variance depend on

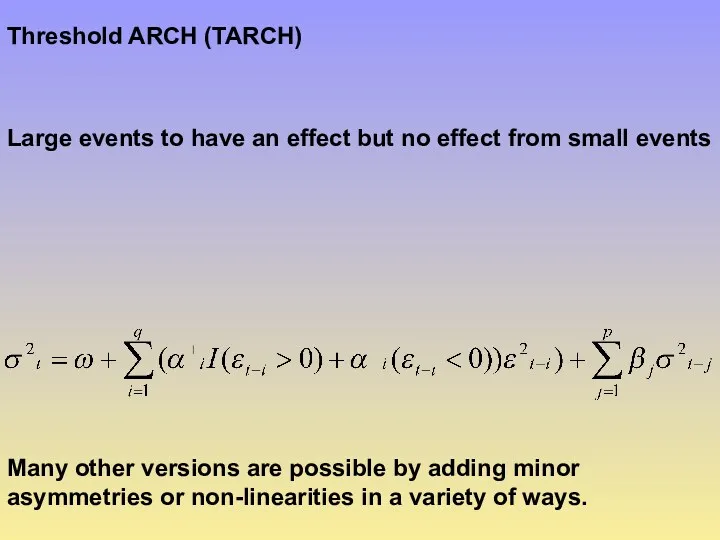

Threshold ARCH (TARCH)

Many other versions are possible by adding minor

Threshold ARCH (TARCH)

Many other versions are possible by adding minor

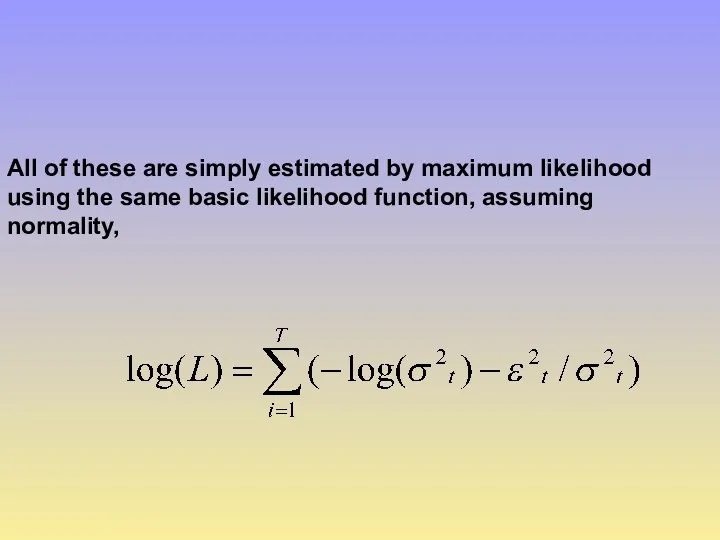

All of these are simply estimated by maximum likelihood using the

All of these are simply estimated by maximum likelihood using the

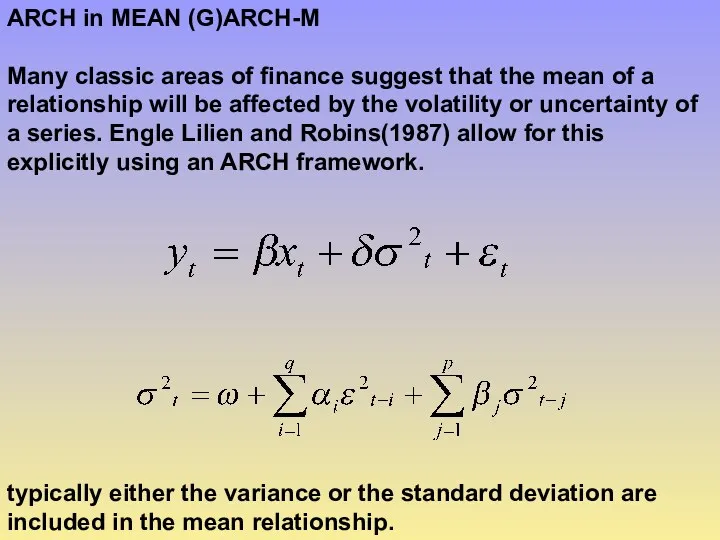

ARCH in MEAN (G)ARCH-M

Many classic areas of finance suggest that the

ARCH in MEAN (G)ARCH-M

Many classic areas of finance suggest that the

often finance stresses the importance of covariance terms. The above model

often finance stresses the importance of covariance terms. The above model

Non normality assumptions

While the basic GARCH model allows a certain amount

Non normality assumptions

While the basic GARCH model allows a certain amount

IGARCH.

The standard GARCH model

is covariance stationary if

But Strict stationarity

IGARCH.

The standard GARCH model

is covariance stationary if

But Strict stationarity

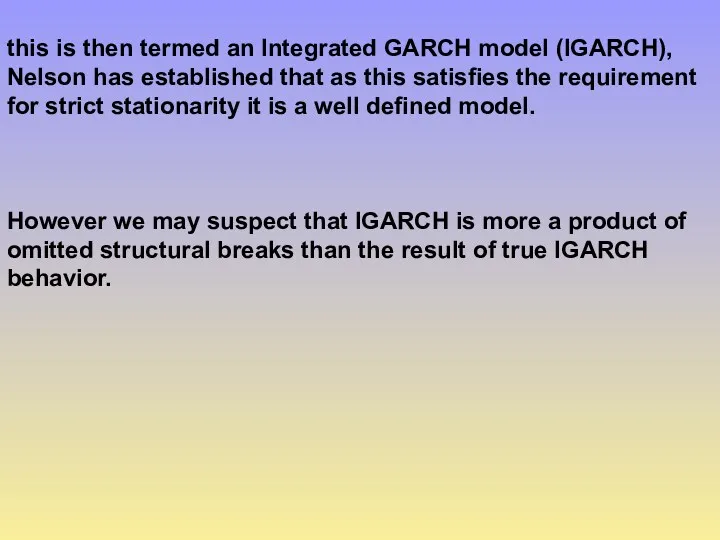

this is then termed an Integrated GARCH model (IGARCH), Nelson has

this is then termed an Integrated GARCH model (IGARCH), Nelson has

Multivariate Models

In general the Garch modelling framework may be easily extended

Multivariate Models

In general the Garch modelling framework may be easily extended

The conditional variance could easily become negative even when all the

The conditional variance could easily become negative even when all the

Vector ARCH

let vech denote the matrix stacking operation

a general extension

Vector ARCH

let vech denote the matrix stacking operation

a general extension

One simplification used is the Diagonal GARCH model where A and

One simplification used is the Diagonal GARCH model where A and

Factor ARCH

Suppose a vector of N series has a common factor

Factor ARCH

Suppose a vector of N series has a common factor

So given a set of factors we may estimate a parsimonious

So given a set of factors we may estimate a parsimonious

Підприємство в соціально-орієнтованій ринковій економіці

Підприємство в соціально-орієнтованій ринковій економіці The pros and cons of migration

The pros and cons of migration Региональная политика в основе управления экономикой региона

Региональная политика в основе управления экономикой региона Економічна теорія: предмет, метод, функції. Людина у світі економіки. Історичний погляд на економічний розвиток країни

Економічна теорія: предмет, метод, функції. Людина у світі економіки. Історичний погляд на економічний розвиток країни Финансовая система США

Финансовая система США Открытая экономика и платежный баланс

Открытая экономика и платежный баланс Ожидаемый уровень качества марочного товара

Ожидаемый уровень качества марочного товара Теория производства: издержки и прибыль

Теория производства: издержки и прибыль Внутренняя и внешняя среда предприятия

Внутренняя и внешняя среда предприятия Государственная поддержка малого и среднего бизнеса

Государственная поддержка малого и среднего бизнеса Демографическая проблема

Демографическая проблема Россия в современном мире. Основные направления социально-экономического, политического и военно-технического развития страны

Россия в современном мире. Основные направления социально-экономического, политического и военно-технического развития страны Роль государства в экономике

Роль государства в экономике Ekonomia behawioralna. Ograniczenia poznawcze jednostki i heurystyki w analizie behawioralnej

Ekonomia behawioralna. Ograniczenia poznawcze jednostki i heurystyki w analizie behawioralnej Человек и экономика. Экономика и ее основные участники. (7 класс)

Человек и экономика. Экономика и ее основные участники. (7 класс) Бережливое производство

Бережливое производство Формування нових форм організації праці в умовах співробітництва України з ЄС

Формування нових форм організації праці в умовах співробітництва України з ЄС Экономическая теория: предмет, цели и задачи

Экономическая теория: предмет, цели и задачи Экономический потенциал Приморского края и его место в развитии экономики России

Экономический потенциал Приморского края и его место в развитии экономики России Государственная поддержка малого и среднего предпринимательства в Саратовской области

Государственная поддержка малого и среднего предпринимательства в Саратовской области Национальный инновационный фонд

Национальный инновационный фонд Макроэкономика. Модель IS-LM

Макроэкономика. Модель IS-LM Транснационализация и социализация международного бизнеса

Транснационализация и социализация международного бизнеса Экономикалық теорияның пәні және зерттеу әдістері

Экономикалық теорияның пәні және зерттеу әдістері Конкурентоспособность продукции ООО ЭКОМ и факторы ее определяющие

Конкурентоспособность продукции ООО ЭКОМ и факторы ее определяющие Экономика, как наука

Экономика, как наука Россия в системе международного (мирового) разделения труда

Россия в системе международного (мирового) разделения труда Основной капитал предприятия

Основной капитал предприятия