- System of mortgage lending of the Republic of Kazakhstan

Содержание

- 2. The downturn in investment activity in the construction industry repeatedly increases the importance of the actual

- 3. Kazakhstan has real prerequisites for positive development of the legal framework of implementation of mortgage lending

- 4. The main forms of housing finance are loans, including mortgages, direct investment, budgetary financing, equity investors,

- 5. The term "mortgage" first appeared in Greece in the beginning of the VI. BC (it has

- 6. In November 2005, the maximum interest rate on mortgage loans issued by market program, the Company

- 7. To sign the agreement on housing construction savings, the following documents: identity card, a copy of

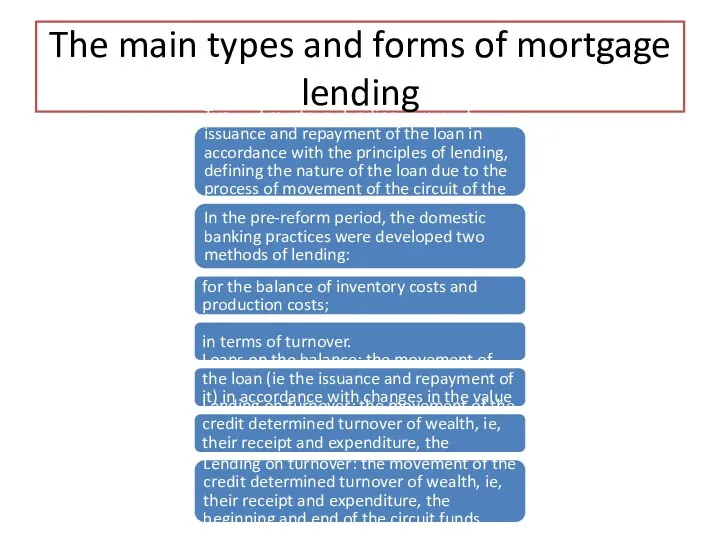

- 8. The main types and forms of mortgage lending Types of mortgage lending - a way of

- 9. The experience of the credit market of the United States says that although over time in

- 10. Foreign experience of mortgage lending In developed countries, the mortgage loan is very widespread and is

- 11. In each country, the institutional structure of the system of mortgage lending institutions significantly differentiated. Referring

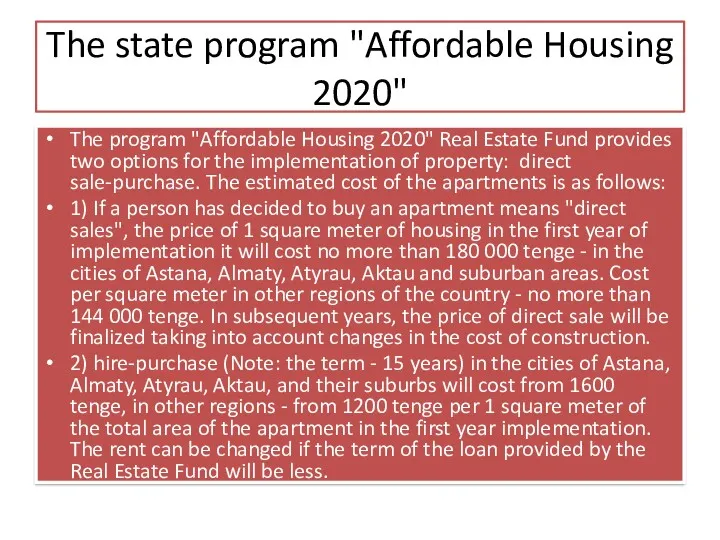

- 12. The state program "Affordable Housing 2020" The program "Affordable Housing 2020" Real Estate Fund provides two

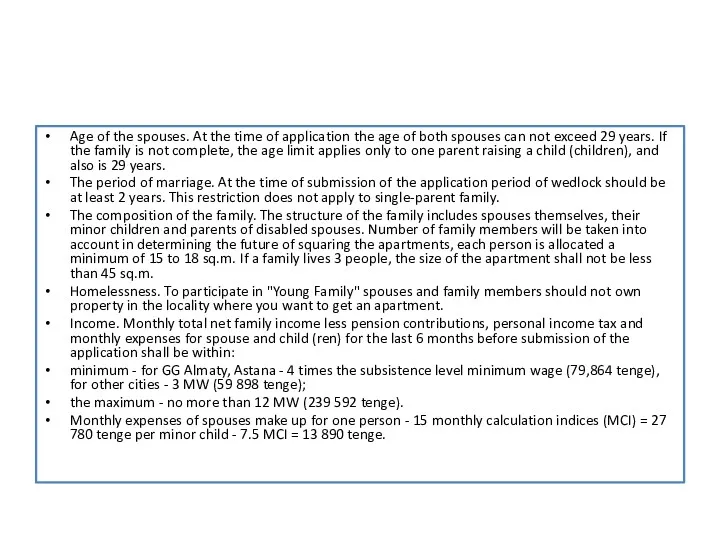

- 13. Age of the spouses. At the time of application the age of both spouses can not

- 14. For example, it looks like this If the loan term advance loan is 8 years, the

- 15. As international experience shows, the methods of economic policy in the field of formation and development

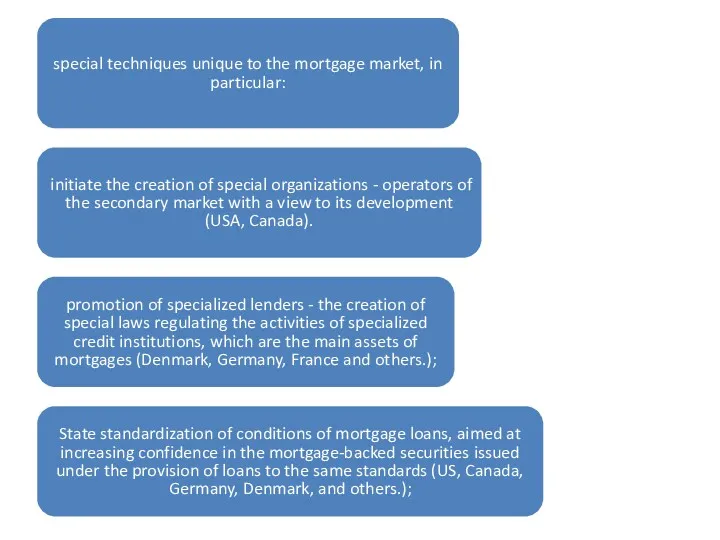

- 16. special techniques unique to the mortgage market, in particular: initiate the creation of special organizations -

- 17. Thus, we can conclude that the country mortgage lending is gaining momentum, proof of this is

- 18. In 2014 begin to show positive trends in the development of mortgage lending. In 2011, an

- 20. Скачать презентацию

The downturn in investment activity in the construction industry repeatedly increases

The downturn in investment activity in the construction industry repeatedly increases

Kazakhstan has real prerequisites for positive development of the legal framework

Kazakhstan has real prerequisites for positive development of the legal framework

The main forms of housing finance are loans, including mortgages, direct

The main forms of housing finance are loans, including mortgages, direct

The term "mortgage" first appeared in Greece in the beginning of

The term "mortgage" first appeared in Greece in the beginning of

In November 2005, the maximum interest rate on mortgage loans issued

In November 2005, the maximum interest rate on mortgage loans issued

To sign the agreement on housing construction savings, the following documents:

To sign the agreement on housing construction savings, the following documents:

The main types and forms of mortgage lending

Types of mortgage lending

The main types and forms of mortgage lending

Types of mortgage lending

The experience of the credit market of the United States says

The experience of the credit market of the United States says

Foreign experience of mortgage lending

In developed countries, the mortgage loan is

Foreign experience of mortgage lending

In developed countries, the mortgage loan is

In each country, the institutional structure of the system of mortgage

In each country, the institutional structure of the system of mortgage

The state program "Affordable Housing 2020"

The program "Affordable Housing 2020" Real

The state program "Affordable Housing 2020"

The program "Affordable Housing 2020" Real

Age of the spouses. At the time of application the age

Age of the spouses. At the time of application the age

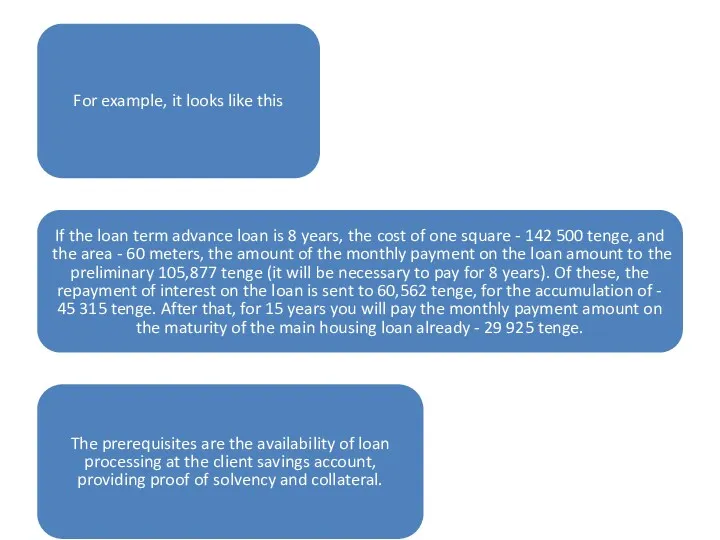

For example, it looks like this

If the loan term advance loan

For example, it looks like this

If the loan term advance loan

As international experience shows, the methods of economic policy in the

As international experience shows, the methods of economic policy in the

special techniques unique to the mortgage market, in particular:

initiate the creation

special techniques unique to the mortgage market, in particular:

initiate the creation

Thus, we can conclude that the country mortgage lending is gaining

Thus, we can conclude that the country mortgage lending is gaining

In 2014 begin to show positive trends in the development of

In 2014 begin to show positive trends in the development of

Государственные услуги ФСС

Государственные услуги ФСС Финансовая пирамида

Финансовая пирамида Форвардные и фьючерсные контракты

Форвардные и фьючерсные контракты Формирование и использование оборотного капитала

Формирование и использование оборотного капитала О мерах социальной поддержки семей с детьми

О мерах социальной поддержки семей с детьми Світовий ринок робочої сили. Міжнародна міграція робочої сили (Тема 7, Тема 8)

Світовий ринок робочої сили. Міжнародна міграція робочої сили (Тема 7, Тема 8) 1С:Управление небольшой фирмой 8 + 1С:Бухгалтерия 8 = создаем гармонию управленческого и бухгалтерского учета

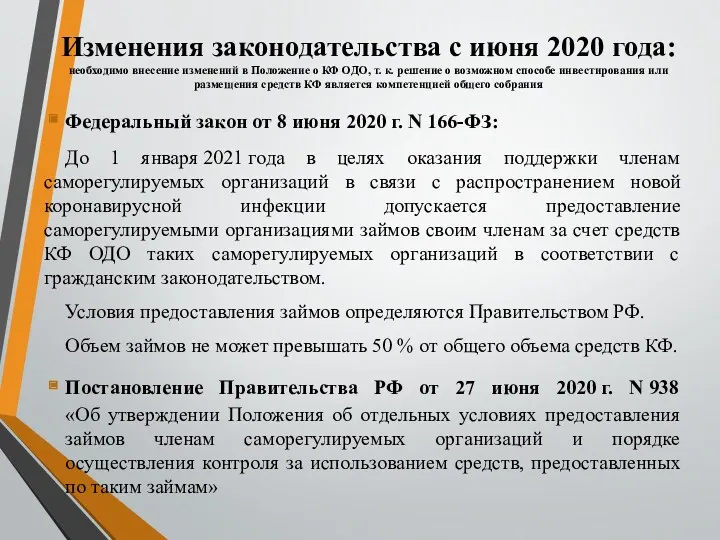

1С:Управление небольшой фирмой 8 + 1С:Бухгалтерия 8 = создаем гармонию управленческого и бухгалтерского учета Предоставление саморегулируемыми организациями займов своим членам за счет средств КФ ОДО в связи с распространением COVID-19

Предоставление саморегулируемыми организациями займов своим членам за счет средств КФ ОДО в связи с распространением COVID-19 Модели и методы оценки облигаций

Модели и методы оценки облигаций Учет материально-производственных запасов в ПАО Магнит

Учет материально-производственных запасов в ПАО Магнит Банктік клиенттерге несие беру қызметін басқарудағы ақпараттық жүйені зерттеу

Банктік клиенттерге несие беру қызметін басқарудағы ақпараттық жүйені зерттеу Государственные внебюджетные фонды РФ

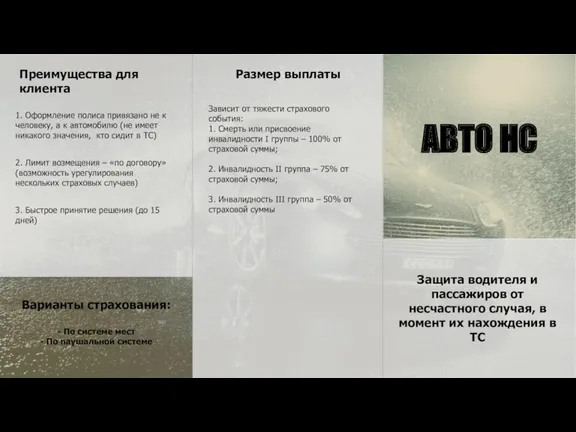

Государственные внебюджетные фонды РФ Страхование. Преимущества для клиента. Размер выплаты

Страхование. Преимущества для клиента. Размер выплаты Денежный рынок и денежно-кредитная политика. (Тема 12)

Денежный рынок и денежно-кредитная политика. (Тема 12) Анализ размещения капитала и оценка имущественного состояния предприятия

Анализ размещения капитала и оценка имущественного состояния предприятия Тәуекелділік және табыстылық

Тәуекелділік және табыстылық Презентация Манаников

Презентация Манаников Фінансова стратегія підприємства

Фінансова стратегія підприємства Денежная система государства

Денежная система государства Технология блокчейн. Криптовалюты. Биткойн. Цифровая (виртуальная) валюта

Технология блокчейн. Криптовалюты. Биткойн. Цифровая (виртуальная) валюта Особенности бюджетной системы Швейцарии

Особенности бюджетной системы Швейцарии Инвестиционная деятельность. Факторы стоимости. Лекция 5 (1)

Инвестиционная деятельность. Факторы стоимости. Лекция 5 (1) Персонифицированное финансирование дополнительного образования. Московская область

Персонифицированное финансирование дополнительного образования. Московская область Комерческое предложение по БВД

Комерческое предложение по БВД Страхование квартир и загородных строений

Страхование квартир и загородных строений Страховые взносы

Страховые взносы Инвентаризация: назначение и порядок её проведения, учета и оформления результатов

Инвентаризация: назначение и порядок её проведения, учета и оформления результатов Президентские гранты для ННО

Президентские гранты для ННО