- Internal control and deontology - Chapter 8 Fraud

Содержание

- 2. 1. What is fraud? No ‘clear’ definition: it can be manipulation, deception, corruption or just monkey

- 3. 2. Types of fraud Examples: Exam fraud Diploma fraud ,CV fraud Tax fraud VAT fraud Money

- 4. 2. Types of fraud Abuse of assets: Most frequent type of fraude Thefts, abusing corporate assets,

- 5. Fraude Red flags for fraud BRON: The ACFE's 2010 Report to the Nations on Occupational Fraud

- 6. 3.Forensic audit Specialization in the audit domain dealing with fraud detection and controlling. Forensic auditors need

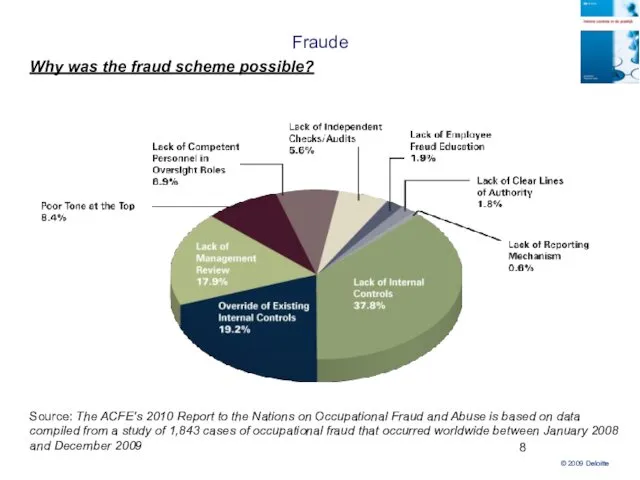

- 8. Fraude Why was the fraud scheme possible? Source: The ACFE's 2010 Report to the Nations on

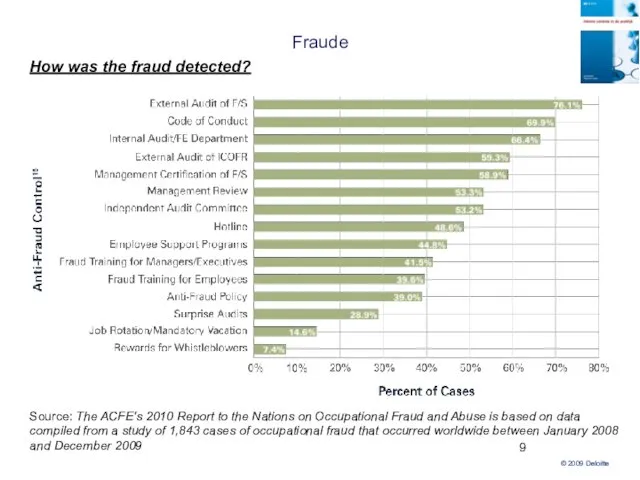

- 9. Fraude How was the fraud detected? Source: The ACFE's 2010 Report to the Nations on Occupational

- 10. Fraud Some figures Fraud with the hightest occurance rate ≠ highest financial impact American research: abuse

- 11. Fraud: some facts Source: The ACFE's 2010 Report to the Nations on Occupational Fraud and Abuse

- 12. Fraud: some facts More fraud is perpetrated by men Why? Source: The ACFE's 2010 Report to

- 13. Fraud: some facts Impact by gender Source: The ACFE's 2010 Report to the Nations on Occupational

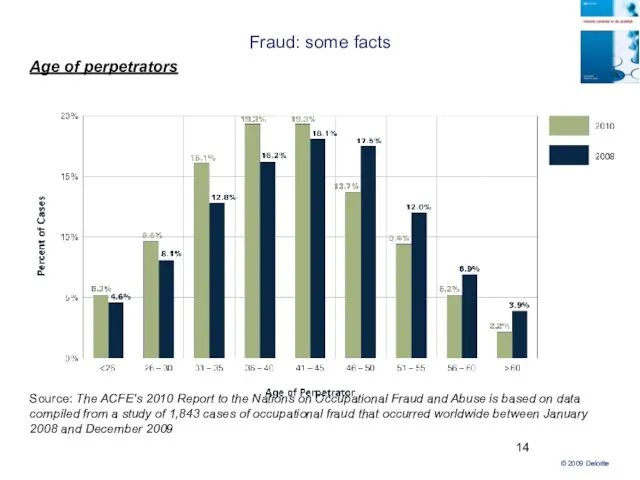

- 14. Fraud: some facts Age of perpetrators Source: The ACFE's 2010 Report to the Nations on Occupational

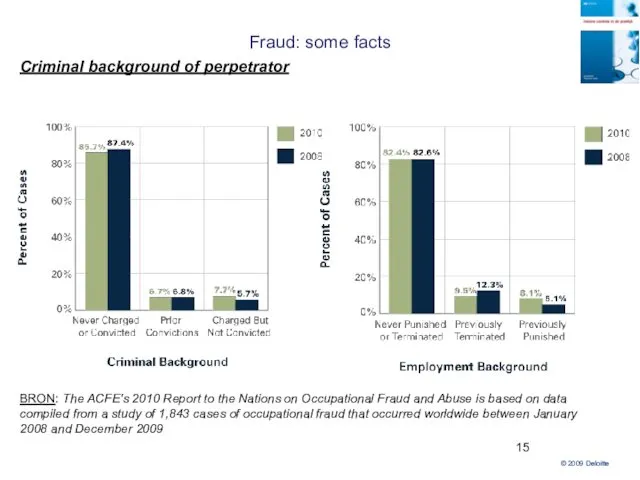

- 15. Fraud: some facts Criminal background of perpetrator BRON: The ACFE's 2010 Report to the Nations on

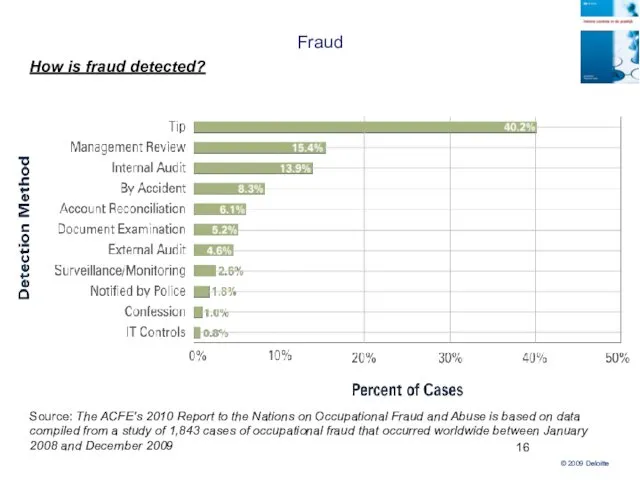

- 16. Fraud How is fraud detected? Source: The ACFE's 2010 Report to the Nations on Occupational Fraud

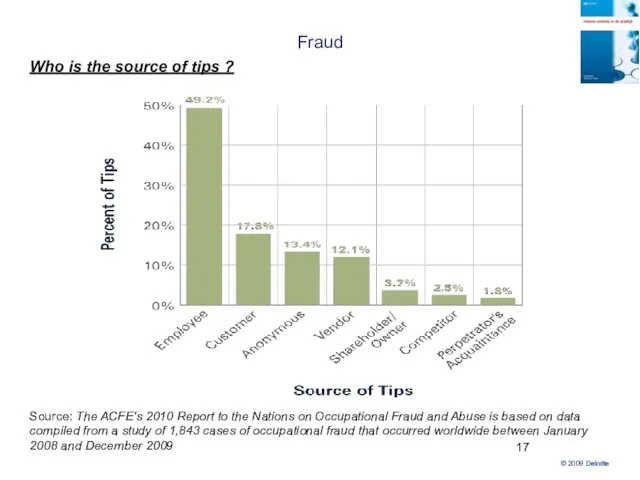

- 17. Fraud Who is the source of tips ? Source: The ACFE's 2010 Report to the Nations

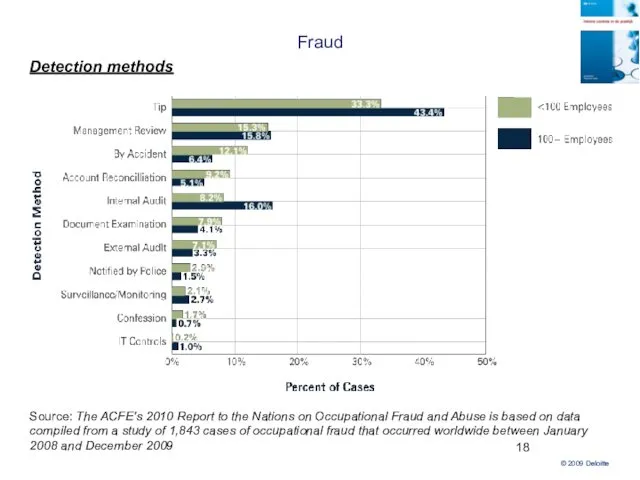

- 18. Fraud Detection methods Source: The ACFE's 2010 Report to the Nations on Occupational Fraud and Abuse

- 19. Fraud Occurance of fraude in SME’s Source: The ACFE's 2010 Report to the Nations on Occupational

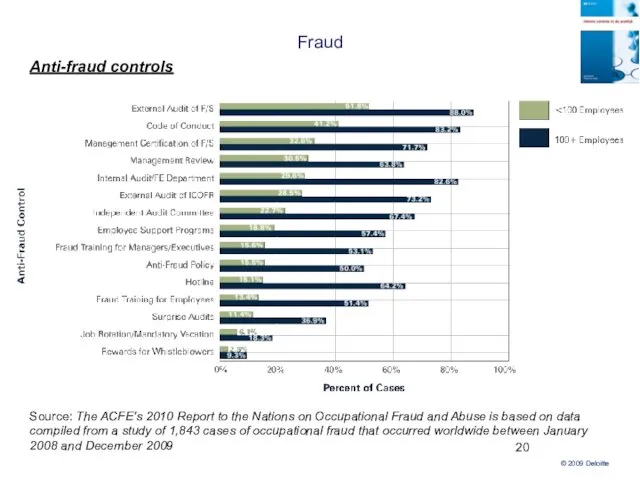

- 20. Fraud Anti-fraud controls Source: The ACFE's 2010 Report to the Nations on Occupational Fraud and Abuse

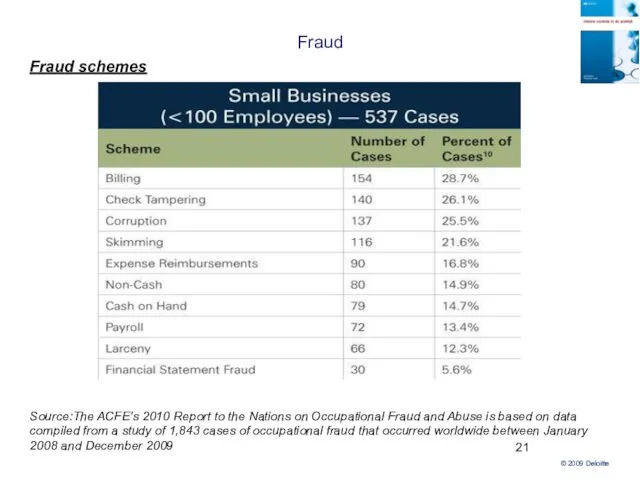

- 21. Fraud Fraud schemes Source:The ACFE's 2010 Report to the Nations on Occupational Fraud and Abuse is

- 23. Скачать презентацию

1. What is fraud?

No ‘clear’ definition: it can be manipulation, deception,

1. What is fraud?

No ‘clear’ definition: it can be manipulation, deception,

2. Types of fraud

Examples:

Exam fraud

Diploma fraud ,CV fraud

2. Types of fraud

Examples:

Exam fraud

Diploma fraud ,CV fraud

2. Types of fraud

Abuse of assets:

Most frequent type of fraude

Thefts, abusing

2. Types of fraud

Abuse of assets:

Most frequent type of fraude

Thefts, abusing

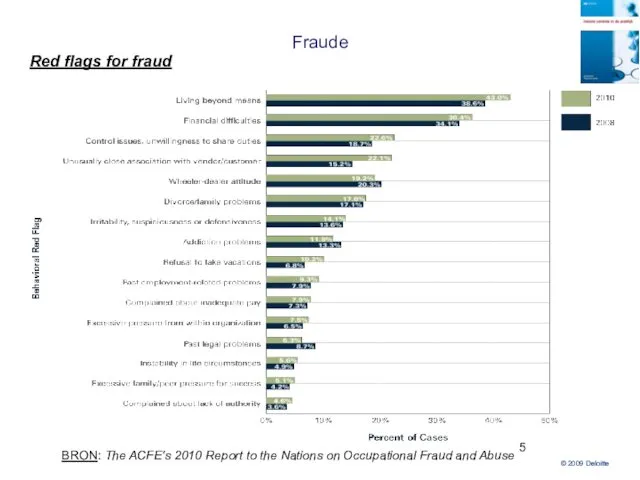

Fraude

Red flags for fraud

BRON: The ACFE's 2010 Report to the Nations

Fraude

Red flags for fraud

BRON: The ACFE's 2010 Report to the Nations

3.Forensic audit

Specialization in the audit domain dealing with fraud detection and

3.Forensic audit

Specialization in the audit domain dealing with fraud detection and

Fraude

Why was the fraud scheme possible?

Source: The ACFE's 2010 Report to

Fraude

Why was the fraud scheme possible?

Source: The ACFE's 2010 Report to

Fraude

How was the fraud detected?

Source: The ACFE's 2010 Report to the

Fraude

How was the fraud detected?

Source: The ACFE's 2010 Report to the

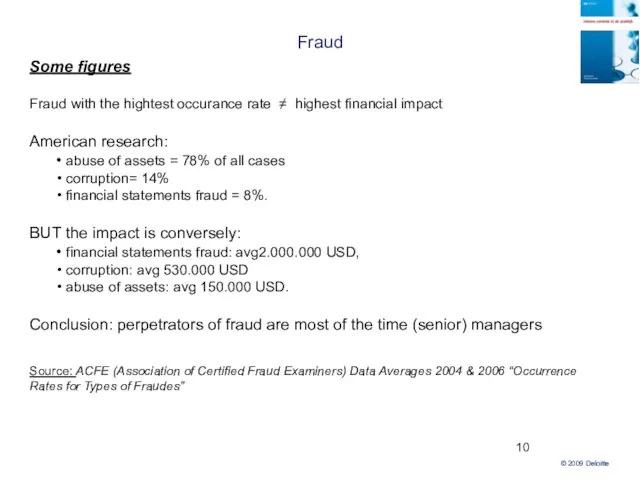

Fraud

Some figures

Fraud with the hightest occurance rate ≠ highest financial impact

American

Fraud

Some figures

Fraud with the hightest occurance rate ≠ highest financial impact

American

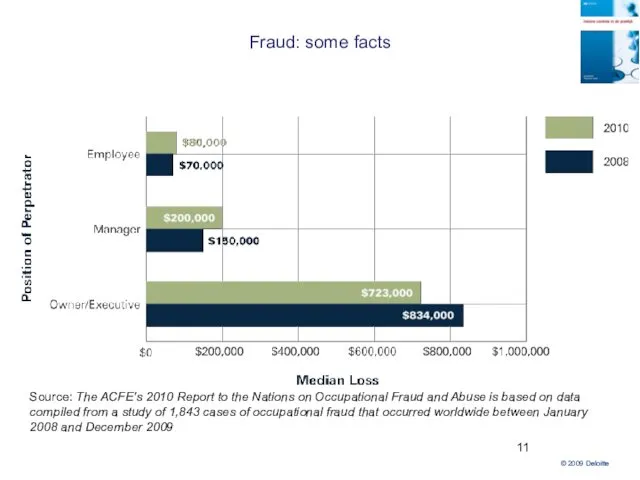

Fraud: some facts

Source: The ACFE's 2010 Report to the Nations on

Fraud: some facts

Source: The ACFE's 2010 Report to the Nations on

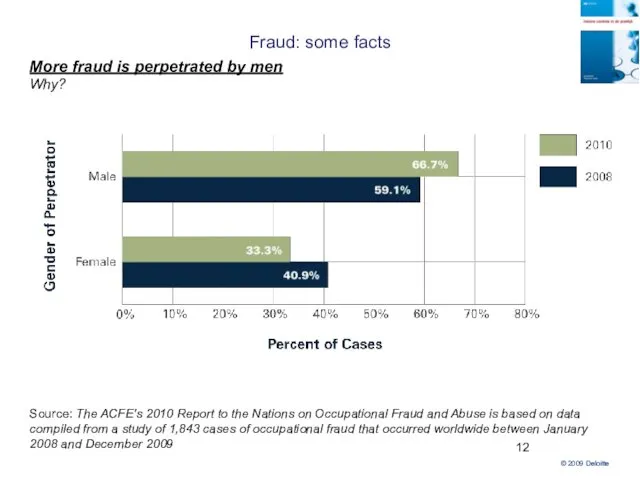

Fraud: some facts

More fraud is perpetrated by men

Why?

Source: The ACFE's 2010

Fraud: some facts

More fraud is perpetrated by men

Why?

Source: The ACFE's 2010

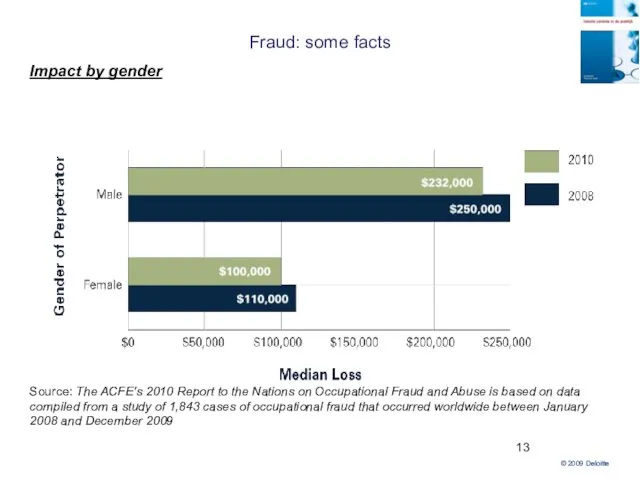

Fraud: some facts

Impact by gender

Source: The ACFE's 2010 Report to the

Fraud: some facts

Impact by gender

Source: The ACFE's 2010 Report to the

Fraud: some facts

Age of perpetrators

Source: The ACFE's 2010 Report to the

Fraud: some facts

Age of perpetrators

Source: The ACFE's 2010 Report to the

Fraud: some facts

Criminal background of perpetrator

BRON: The ACFE's 2010 Report to

Fraud: some facts

Criminal background of perpetrator

BRON: The ACFE's 2010 Report to

Fraud

How is fraud detected?

Source: The ACFE's 2010 Report to the Nations

Fraud

How is fraud detected?

Source: The ACFE's 2010 Report to the Nations

Fraud

Who is the source of tips ?

Source: The ACFE's 2010 Report

Fraud

Who is the source of tips ?

Source: The ACFE's 2010 Report

Fraud

Detection methods

Source: The ACFE's 2010 Report to the Nations on Occupational

Fraud

Detection methods

Source: The ACFE's 2010 Report to the Nations on Occupational

Fraud

Occurance of fraude in SME’s

Source: The ACFE's 2010 Report to the

Fraud

Occurance of fraude in SME’s

Source: The ACFE's 2010 Report to the

Fraud

Anti-fraud controls

Source: The ACFE's 2010 Report to the Nations on Occupational

Fraud

Anti-fraud controls

Source: The ACFE's 2010 Report to the Nations on Occupational

Fraud

Fraud schemes

Source:The ACFE's 2010 Report to the Nations on Occupational Fraud

Fraud

Fraud schemes

Source:The ACFE's 2010 Report to the Nations on Occupational Fraud

Формирование группового поведения в организации

Формирование группового поведения в организации Прикладные методы в управлении

Прикладные методы в управлении Таможенный менеджмент. Развитие организационного поведения и управление персоналом в таможенных органах. Тема 4

Таможенный менеджмент. Развитие организационного поведения и управление персоналом в таможенных органах. Тема 4 Диаграмма Парето

Диаграмма Парето Интеграция: автоматизация логистики

Интеграция: автоматизация логистики Содержание и психологические факторы эффективной управленческой деятельности

Содержание и психологические факторы эффективной управленческой деятельности Управление стоимостью проекта

Управление стоимостью проекта Принятие решений в условиях неопределенности и риска

Принятие решений в условиях неопределенности и риска Морской транспорт. Преимущества морского транспорта

Морской транспорт. Преимущества морского транспорта Ұйымда жеке тұлғалық мінез-құлықтың ерекшелігі, когнитивті диссонанс

Ұйымда жеке тұлғалық мінез-құлықтың ерекшелігі, когнитивті диссонанс Филиал Сервисный Центр Новосибирск

Филиал Сервисный Центр Новосибирск Аудит качества

Аудит качества Понятие качества в современной экономике. 14 принципов Деминга

Понятие качества в современной экономике. 14 принципов Деминга Управление и менеджмент в сфере культуры

Управление и менеджмент в сфере культуры Организации и управление ими (практика)

Организации и управление ими (практика) Қытайлық басқару моделі

Қытайлық басқару моделі Методика разработки стандартов государственных и муниципальных услуг

Методика разработки стандартов государственных и муниципальных услуг Логистика. Обязанности логиста

Логистика. Обязанности логиста Основные навыки менеджмента. Тренинг

Основные навыки менеджмента. Тренинг Управление качеством продукции

Управление качеством продукции Концепция организационных изменений

Концепция организационных изменений Мировые тенденции развития различных видов транспорта

Мировые тенденции развития различных видов транспорта Корпоративный кодекс. Формула корпоративной культуры

Корпоративный кодекс. Формула корпоративной культуры Japanese Manufacturing Systems - JIT (Just In Time), known also by names: Stockless Production (HP), Zero Inventories, Kanban

Japanese Manufacturing Systems - JIT (Just In Time), known also by names: Stockless Production (HP), Zero Inventories, Kanban Лекции по управлению ИТ проектами

Лекции по управлению ИТ проектами Методы исследования в менеджменте

Методы исследования в менеджменте Организационная культура в системе управления. Лекция 2

Организационная культура в системе управления. Лекция 2 Инструкторский тренинг. Специфика роста в Active Sale Group

Инструкторский тренинг. Специфика роста в Active Sale Group