- Introduction au management (financier) des entreprises

Содержание

- 2. Practical 3 days – 25 hours Interactive and case-based Evaluation: 50% case (last course) 50% end

- 3. module :Stratégies et financement des entreprises en Europe

- 4. Content Basis concepts Financial Management Investment analysis Credits Value of a company Venture capital Business angels

- 5. Definitions Financial Management: “Increase the value of the company for the shareholders” “Shareholders value approach” Corporate

- 6. Importance of financial management Two main reasons for bankrupcy: Management Financing Major obstacle growth: Lack of

- 7. Comments Managerial revolution Maximising versus satisfying behaviour Agency theory (Jensen & Meckling): solution Options/tantièmes Shares Cooperatives

- 8. What type of company?

- 9. “Not all companies are the same”

- 10. Not all the money is the same

- 11. I. Financial management (narrow) How to finance my company? Own funds Capital Reserves Reported results Mezzanine

- 12. Balance sheet

- 13. Entreprise cycle sales INVOICE TURNOVER RECIEVABLES

- 14. P&L

- 15. II. Financieel management (broad) Management working capital: How big is it? How influence level Hoe inlfuence

- 16. WC = OF + DLT – FIXED WK = FLOATING - DST Working capital

- 17. Financial plan Means are bigger than needs Objective: determine financing modalities Case: CVBA Lakatos (p. 62)

- 18. Bankrupcy prediction Models DEFAULT RATE Alarm levels Altman Multiple regression-analysis

- 19. Summary

- 20. II. Financieel management (broad) Management working capital: How big is it? How influence level Hoe inlfuence

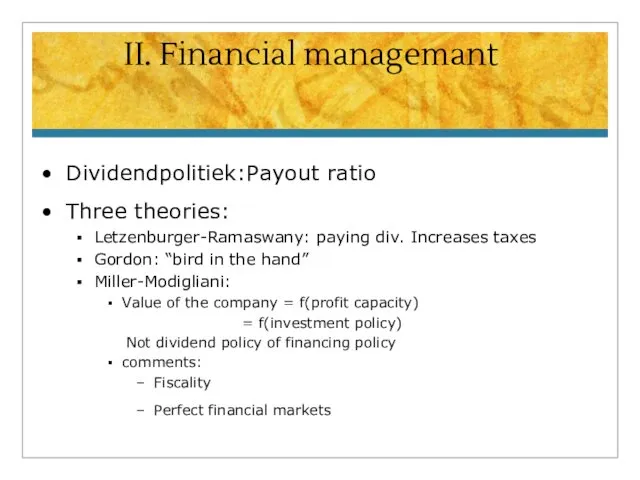

- 21. II. Financial managemant Dividendpolitiek:Payout ratio Three theories: Letzenburger-Ramaswany: paying div. Increases taxes Gordon: “bird in the

- 23. Скачать презентацию

Practical

3 days – 25 hours

Interactive and case-based

Evaluation:

50% case (last course)

50%

Practical

3 days – 25 hours

Interactive and case-based

Evaluation:

50% case (last course)

50%

module :Stratégies et financement

des entreprises en Europe

module :Stratégies et financement

des entreprises en Europe

Content

Basis concepts Financial Management

Investment analysis

Credits

Value of a company

Venture capital

Business angels (crowdfunding,

Content

Basis concepts Financial Management

Investment analysis

Credits

Value of a company

Venture capital

Business angels (crowdfunding,

Definitions

Financial Management:

“Increase the value of the company for the shareholders”

“Shareholders

Definitions

Financial Management:

“Increase the value of the company for the shareholders”

“Shareholders

Importance of financial management

Two main reasons for bankrupcy:

Management

Financing

Major obstacle growth:

Lack

Importance of financial management

Two main reasons for bankrupcy:

Management

Financing

Major obstacle growth:

Lack

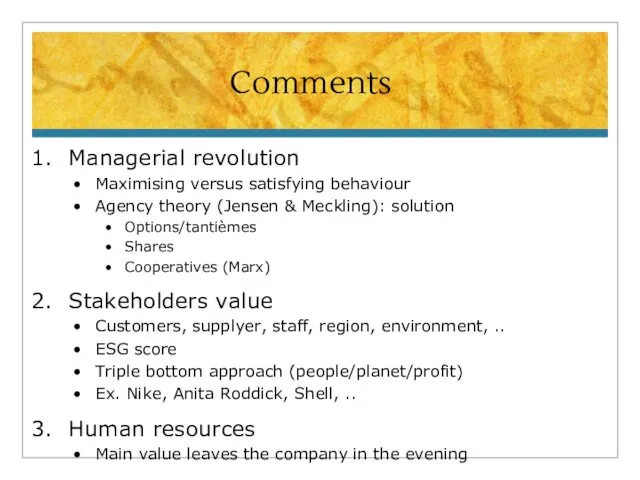

Comments

Managerial revolution

Maximising versus satisfying behaviour

Agency theory (Jensen & Meckling): solution

Options/tantièmes

Shares

Cooperatives (Marx)

Stakeholders

Comments

Managerial revolution

Maximising versus satisfying behaviour

Agency theory (Jensen & Meckling): solution

Options/tantièmes

Shares

Cooperatives (Marx)

Stakeholders

What type of company?

What type of company?

“Not all companies are the same”

“Not all companies are the same”

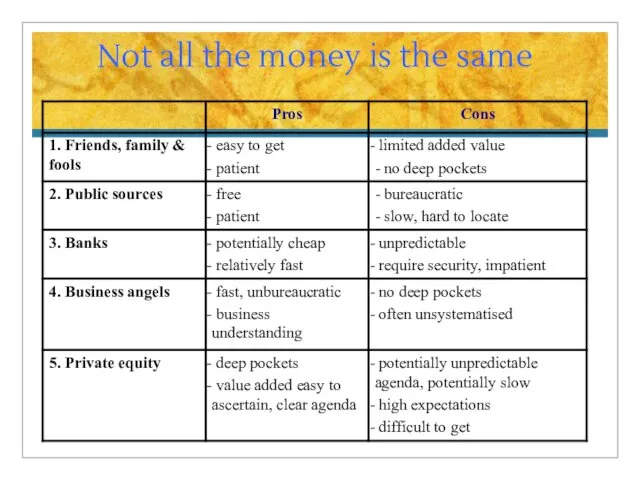

Not all the money is the same

Not all the money is the same

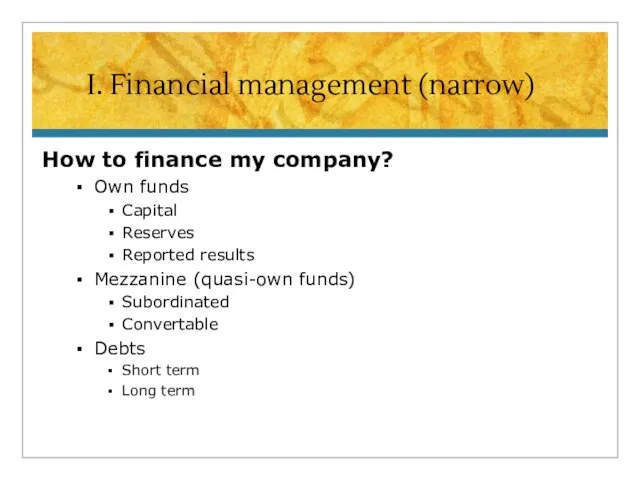

I. Financial management (narrow)

How to finance my company?

Own funds

Capital

Reserves

Reported results

Mezzanine (quasi-own

I. Financial management (narrow)

How to finance my company?

Own funds

Capital

Reserves

Reported results

Mezzanine (quasi-own

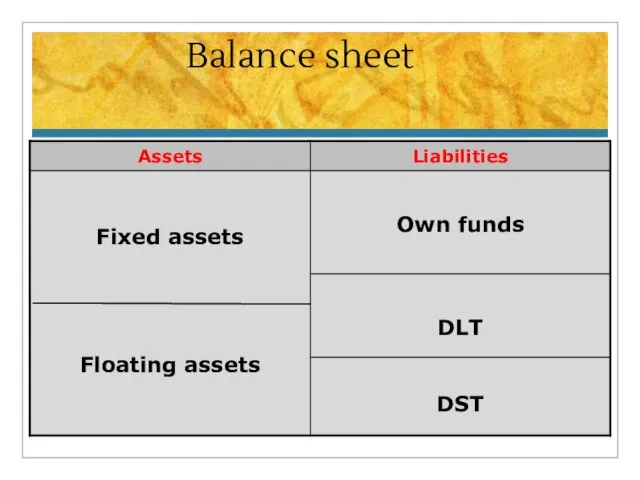

Balance sheet

Balance sheet

Entreprise cycle

sales

INVOICE

TURNOVER

RECIEVABLES

Entreprise cycle

sales

INVOICE

TURNOVER

RECIEVABLES

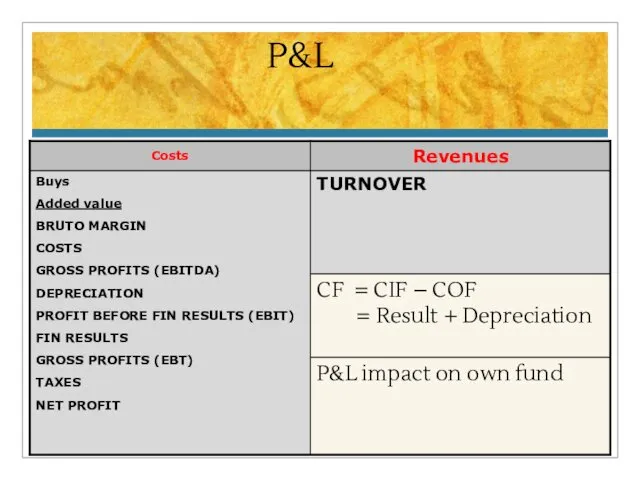

P&L

P&L

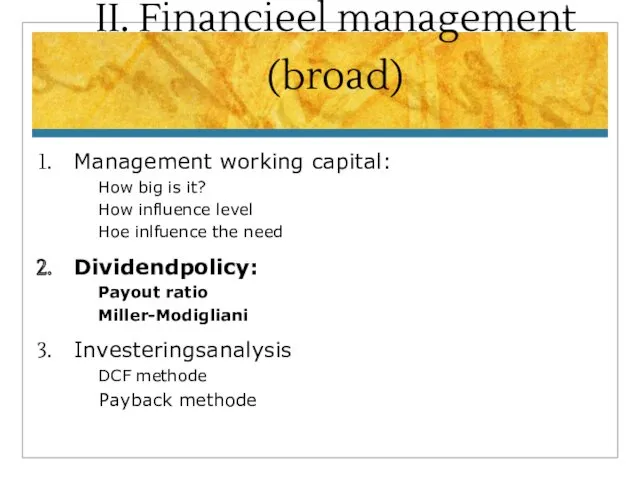

II. Financieel management (broad)

Management working capital:

How big is it?

How influence level

Hoe

II. Financieel management (broad)

Management working capital:

How big is it?

How influence level

Hoe

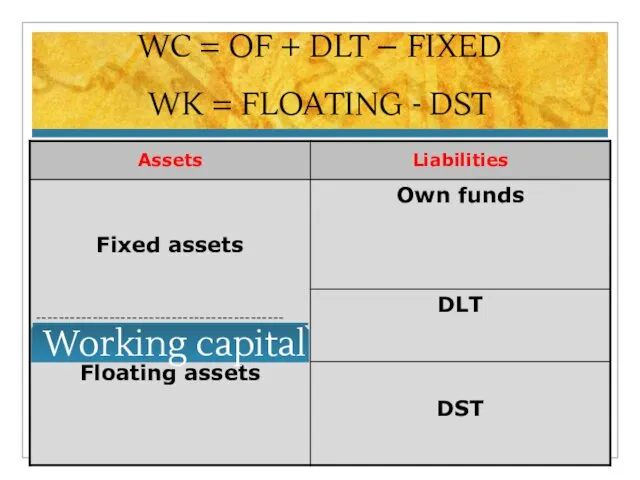

WC = OF + DLT – FIXED

WK = FLOATING - DST

WC = OF + DLT – FIXED

WK = FLOATING - DST

Financial plan

Means are bigger than needs

Objective: determine financing modalities

Case: CVBA

Financial plan

Means are bigger than needs

Objective: determine financing modalities

Case: CVBA

Bankrupcy prediction Models

DEFAULT RATE

Alarm levels

Altman

Multiple regression-analysis

Bankrupcy prediction Models

DEFAULT RATE

Alarm levels

Altman

Multiple regression-analysis

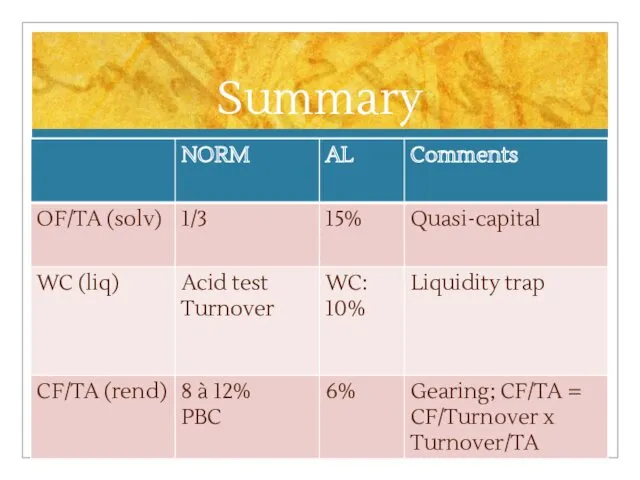

Summary

Summary

II. Financieel management (broad)

Management working capital:

How big is it?

How influence level

Hoe

II. Financieel management (broad)

Management working capital:

How big is it?

How influence level

Hoe

II. Financial managemant

Dividendpolitiek:Payout ratio

Three theories:

Letzenburger-Ramaswany: paying div. Increases taxes

Gordon: “bird

II. Financial managemant

Dividendpolitiek:Payout ratio

Three theories:

Letzenburger-Ramaswany: paying div. Increases taxes

Gordon: “bird

Инструменты предпринимателя

Инструменты предпринимателя Методология и методы исследования в менеджменте

Методология и методы исследования в менеджменте Ситуационные факторы проектирования организации

Ситуационные факторы проектирования организации Результативность государственного управления, подходы к определению

Результативность государственного управления, подходы к определению Значение управления персоналом в управлении современным предприятием. Факторы, обусловившие возрастание роли человека

Значение управления персоналом в управлении современным предприятием. Факторы, обусловившие возрастание роли человека Сущность управленческого труда

Сущность управленческого труда 3 еркіндік дәрежелі дельта-роботты жобалау және басқару

3 еркіндік дәрежелі дельта-роботты жобалау және басқару ВКР: Анализ и оценка конкурентных преимуществ фирмы

ВКР: Анализ и оценка конкурентных преимуществ фирмы Руководитель как организатор системы управления персоналом государственной службы

Руководитель как организатор системы управления персоналом государственной службы Правила ведения беседы

Правила ведения беседы Команда лидера. Мотивация других

Команда лидера. Мотивация других Технология метода проектов

Технология метода проектов Основные понятия в области научно-исследовательских работ. Лекция 1

Основные понятия в области научно-исследовательских работ. Лекция 1 Диаграммы деятельности

Диаграммы деятельности Бизнес-планирование в ИС Project Expert

Бизнес-планирование в ИС Project Expert Управление временем. Тайм-менеджмент. Основы

Управление временем. Тайм-менеджмент. Основы Система менеджмента безопасности. Анализ опасностей

Система менеджмента безопасности. Анализ опасностей Процесс управленческого консультирования

Процесс управленческого консультирования Управление качеством в проекте

Управление качеством в проекте Евент-менеджмент

Евент-менеджмент Проектное управление

Проектное управление Управление конфликтом в организации. Содержание, уровни, стратегии и стили

Управление конфликтом в организации. Содержание, уровни, стратегии и стили Формирование и развитие системы мотивации и стимулирования трудовой деятельности

Формирование и развитие системы мотивации и стимулирования трудовой деятельности Метод мозгового штурма

Метод мозгового штурма Основы профессиональной этики

Основы профессиональной этики Эффективность использования всех ресурсов агропромышленного предприятия

Эффективность использования всех ресурсов агропромышленного предприятия Corporate Governance. State Owned Enterprises

Corporate Governance. State Owned Enterprises Организационные структуры управления

Организационные структуры управления