- Performance management. Throughput accounting. (Topic 3)

Содержание

- 2. ACCA exam references HW: Read the following articles before you proceed with the chapter: http://www.accaglobal.com/in/en/student/exam-support-resources/fundamentals-exams-study-resources/f5/technical-articles/throughput-constraints1.html http://www.accaglobal.com/in/en/student/exam-support-resources/fundamentals-exams-study-resources/f5/technical-articles/throughput-constraints2.html

- 3. Theory of constraints – approach to production management and optimizing production performance Was developed by Goldratt

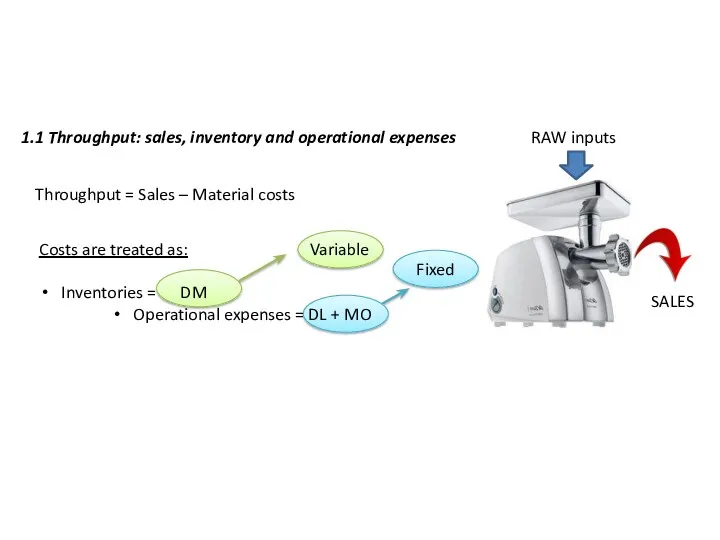

- 4. 1.1 Throughput: sales, inventory and operational expenses RAW inputs SALES Throughput = Sales – Material costs

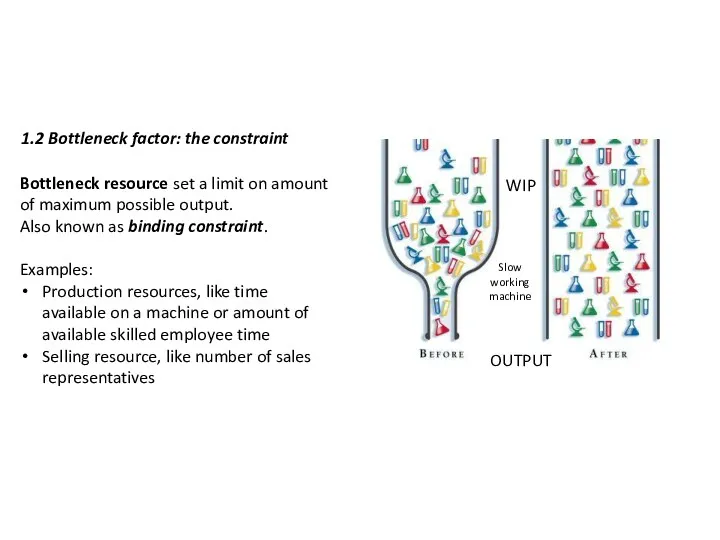

- 5. 1.2 Bottleneck factor: the constraint WIP OUTPUT Bottleneck resource set a limit on amount of maximum

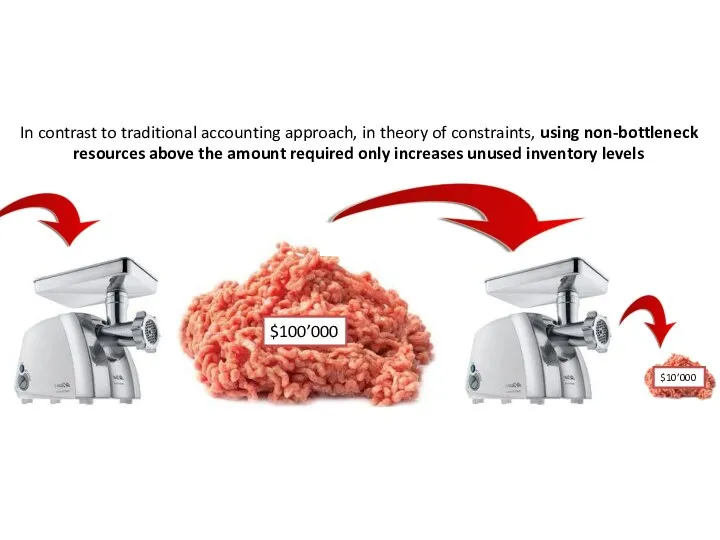

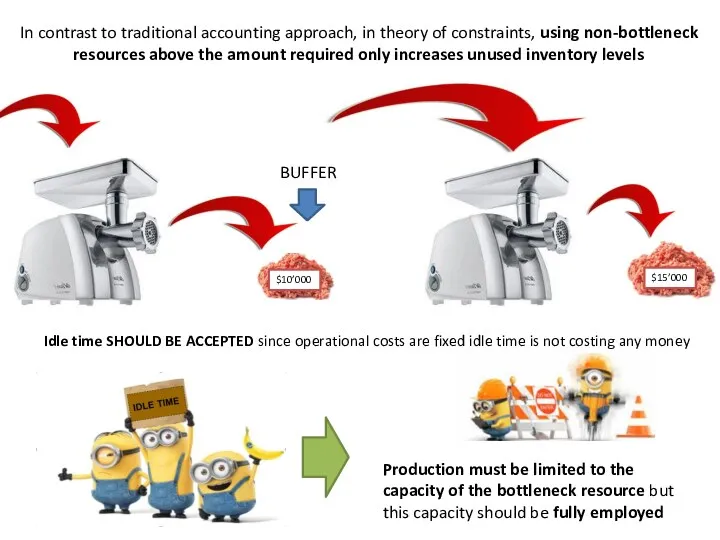

- 6. In contrast to traditional accounting approach, in theory of constraints, using non-bottleneck resources above the amount

- 7. Idle time SHOULD BE ACCEPTED since operational costs are fixed idle time is not costing any

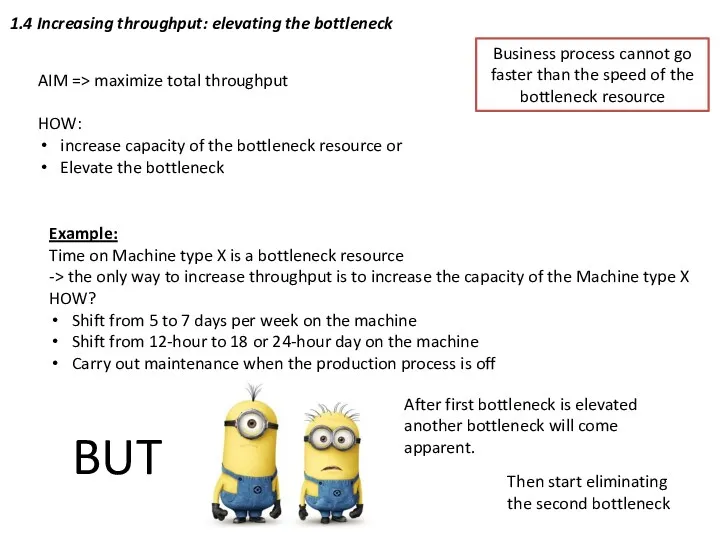

- 8. 1.4 Increasing throughput: elevating the bottleneck AIM => maximize total throughput HOW: increase capacity of the

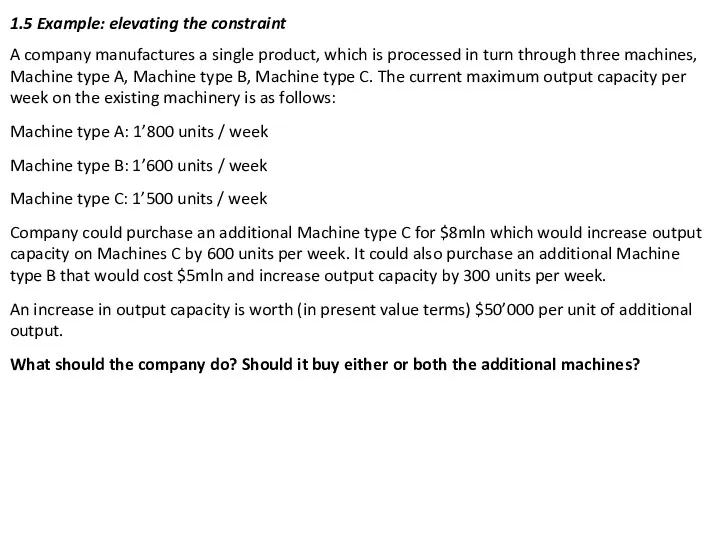

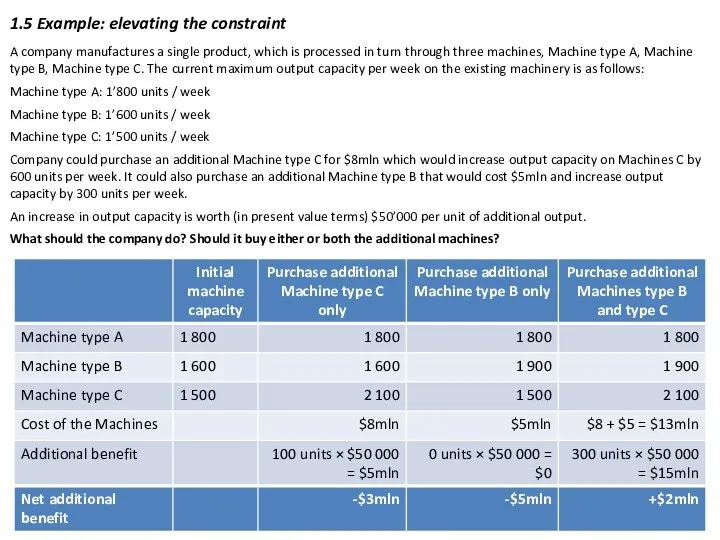

- 9. 1.5 Example: elevating the constraint A company manufactures a single product, which is processed in turn

- 10. 1.5 Example: elevating the constraint A company manufactures a single product, which is processed in turn

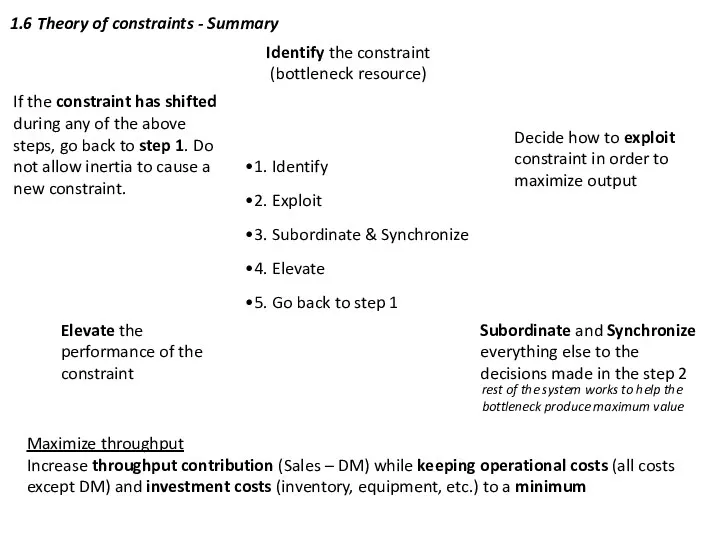

- 11. 1. Identify 2. Exploit 3. Subordinate & Synchronize 4. Elevate 5. Go back to step 1

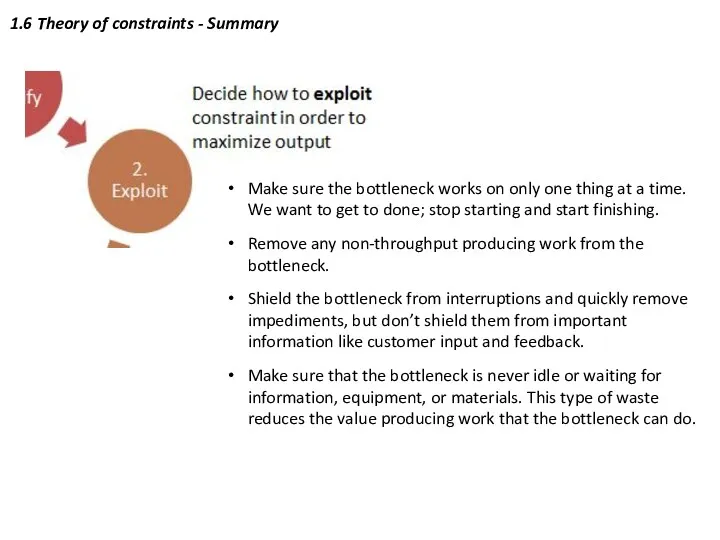

- 12. 1.6 Theory of constraints - Summary Make sure the bottleneck works on only one thing at

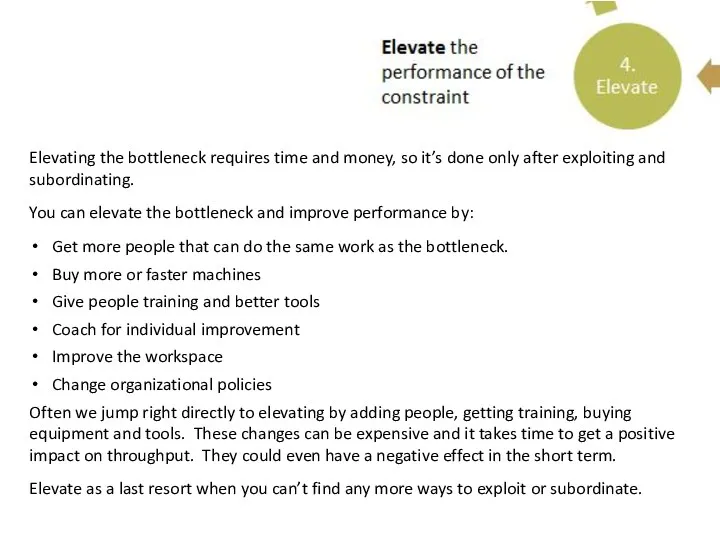

- 13. Elevating the bottleneck requires time and money, so it’s done only after exploiting and subordinating. You

- 14. 1.7 Example: an illustration of the theory of constraints Machine X can process 1’000 kg of

- 15. 2 THROUGHPUT ACCOUNTING Throughput accounting (TA) is an approach to production management which aims to maximize

- 16. 2 THROUGHPUT ACCOUNTING

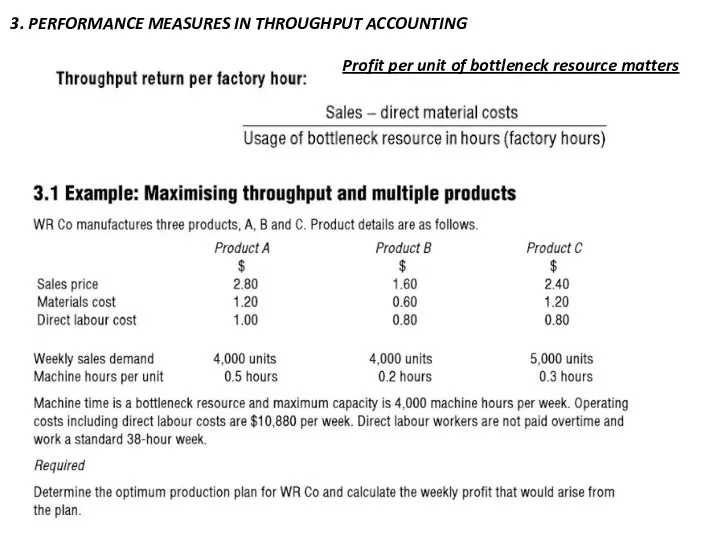

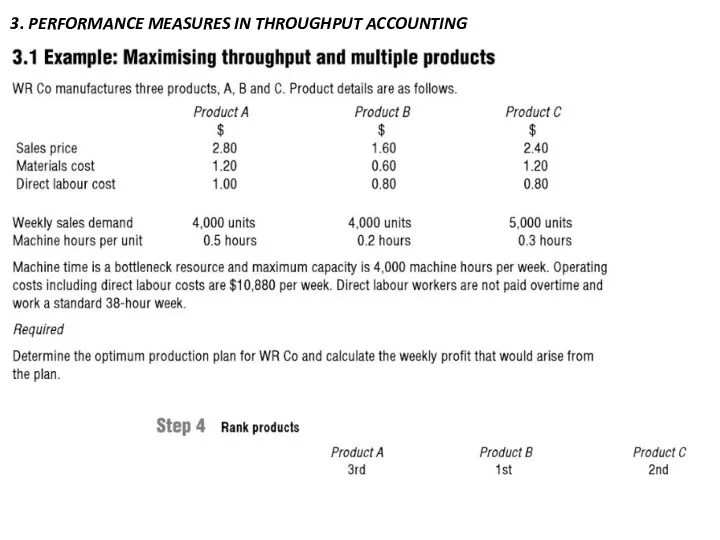

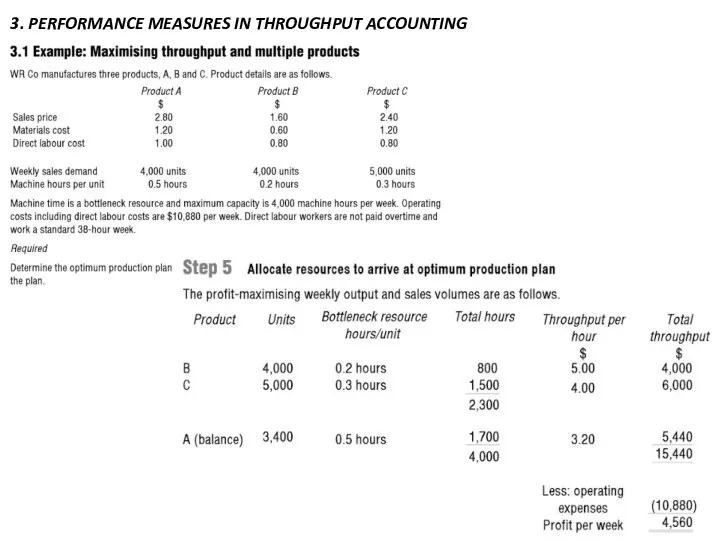

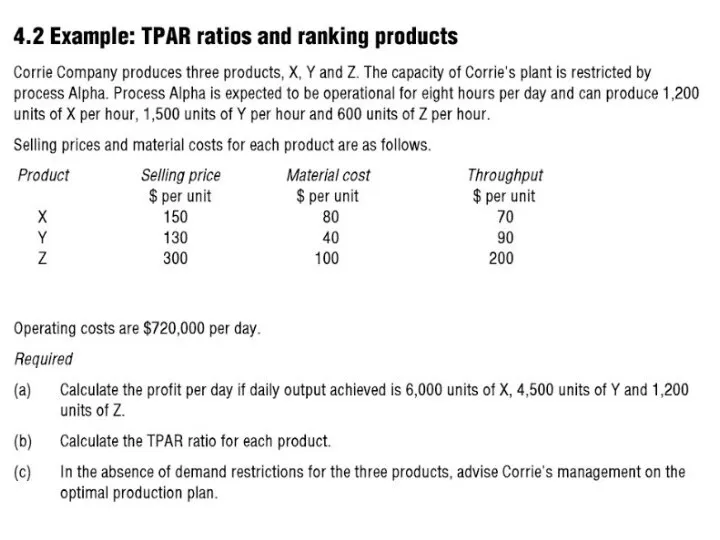

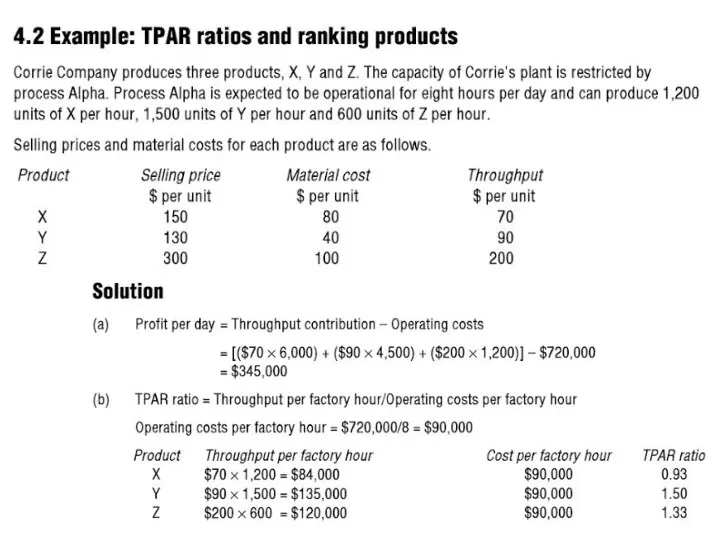

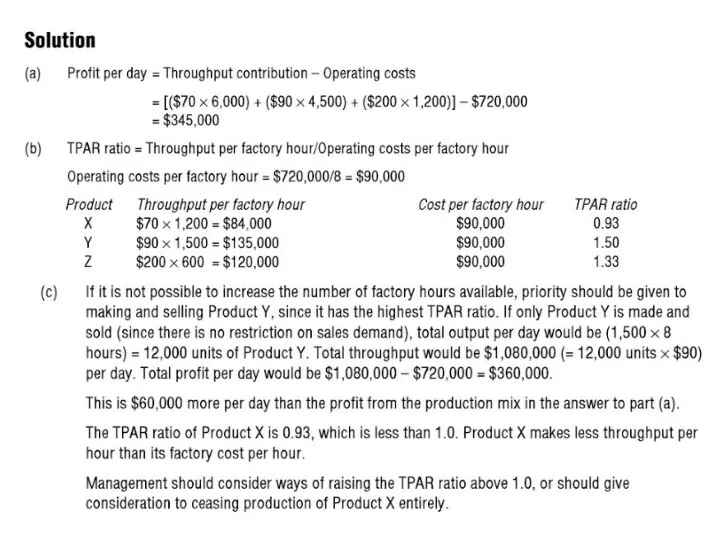

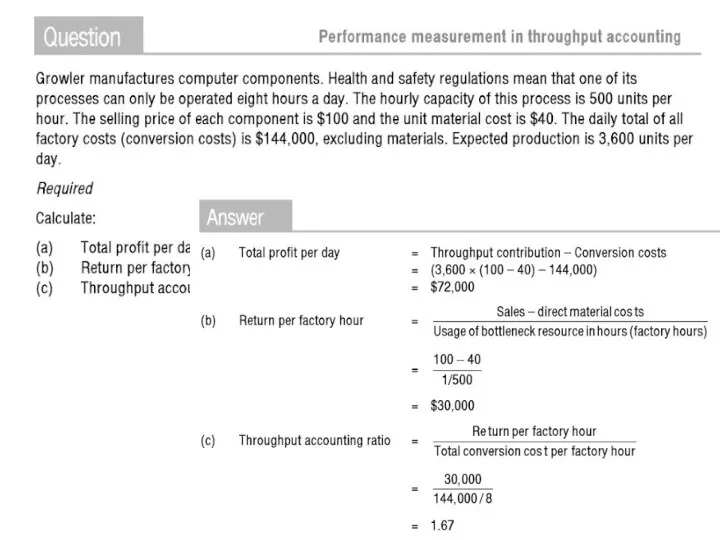

- 18. 3. PERFORMANCE MEASURES IN THROUGHPUT ACCOUNTING Profit per unit of bottleneck resource matters

- 19. 3. PERFORMANCE MEASURES IN THROUGHPUT ACCOUNTING

- 20. 3. PERFORMANCE MEASURES IN THROUGHPUT ACCOUNTING

- 21. 3. PERFORMANCE MEASURES IN THROUGHPUT ACCOUNTING

- 22. 3. PERFORMANCE MEASURES IN THROUGHPUT ACCOUNTING

- 23. 3. PERFORMANCE MEASURES IN THROUGHPUT ACCOUNTING

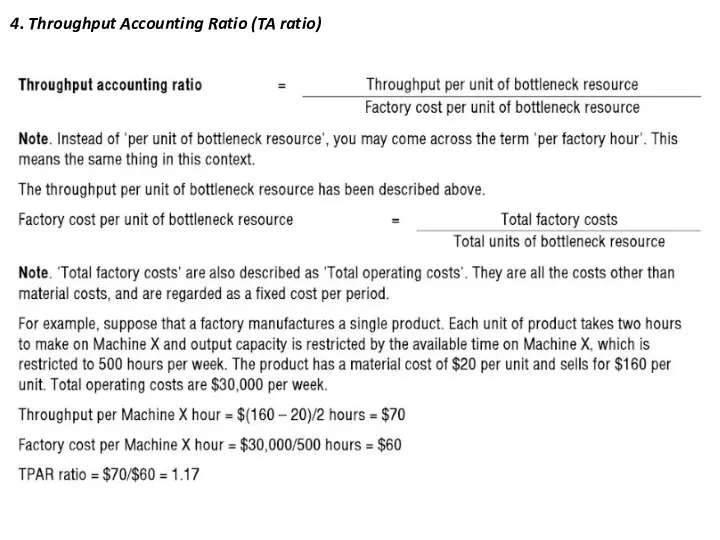

- 24. 4. Throughput Accounting Ratio (TA ratio)

- 32. Скачать презентацию

ACCA exam references

HW: Read the following articles before you proceed with

ACCA exam references

HW: Read the following articles before you proceed with

Theory of constraints – approach to production management and optimizing production

Theory of constraints – approach to production management and optimizing production

1.1 Throughput: sales, inventory and operational expenses

RAW inputs

SALES

Throughput = Sales –

1.1 Throughput: sales, inventory and operational expenses

RAW inputs

SALES

Throughput = Sales –

1.2 Bottleneck factor: the constraint

WIP

OUTPUT

Bottleneck resource set a limit on amount

1.2 Bottleneck factor: the constraint

WIP

OUTPUT

Bottleneck resource set a limit on amount

In contrast to traditional accounting approach, in theory of constraints, using

In contrast to traditional accounting approach, in theory of constraints, using

Idle time SHOULD BE ACCEPTED since operational costs are fixed idle

Idle time SHOULD BE ACCEPTED since operational costs are fixed idle

1.4 Increasing throughput: elevating the bottleneck

AIM => maximize total throughput

HOW:

increase

1.4 Increasing throughput: elevating the bottleneck

AIM => maximize total throughput

HOW:

increase

1.5 Example: elevating the constraint

A company manufactures a single product, which

1.5 Example: elevating the constraint

A company manufactures a single product, which

1.5 Example: elevating the constraint

A company manufactures a single product, which

1.5 Example: elevating the constraint

A company manufactures a single product, which

1. Identify

2. Exploit

3. Subordinate & Synchronize

4. Elevate

5. Go back to step

1. Identify

2. Exploit

3. Subordinate & Synchronize

4. Elevate

5. Go back to step

1.6 Theory of constraints - Summary

Make sure the bottleneck works on

1.6 Theory of constraints - Summary

Make sure the bottleneck works on

Elevating the bottleneck requires time and money, so it’s done only

Elevating the bottleneck requires time and money, so it’s done only

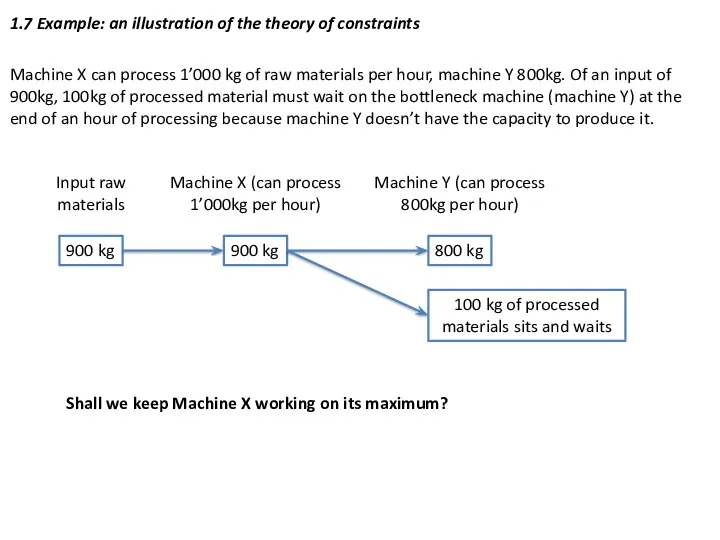

1.7 Example: an illustration of the theory of constraints

Machine X can

1.7 Example: an illustration of the theory of constraints

Machine X can

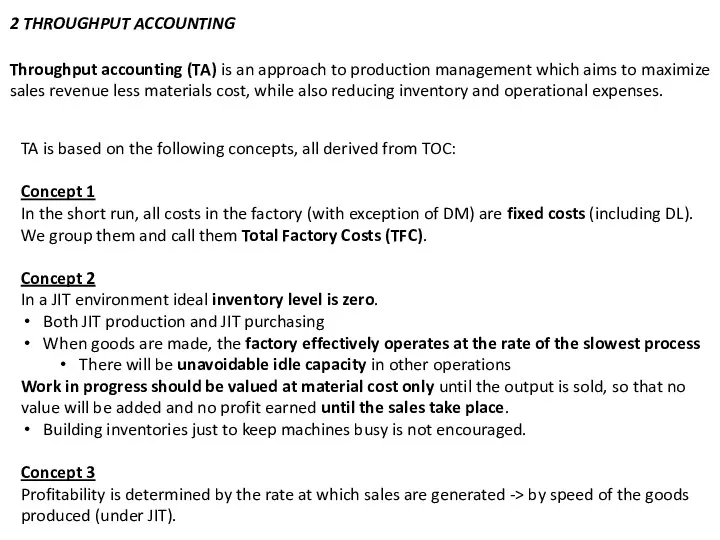

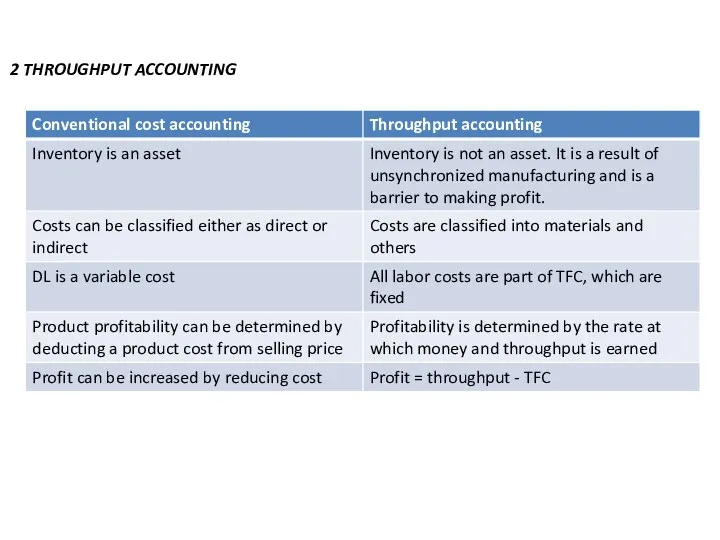

2 THROUGHPUT ACCOUNTING

Throughput accounting (TA) is an approach to production management

2 THROUGHPUT ACCOUNTING

Throughput accounting (TA) is an approach to production management

2 THROUGHPUT ACCOUNTING

2 THROUGHPUT ACCOUNTING

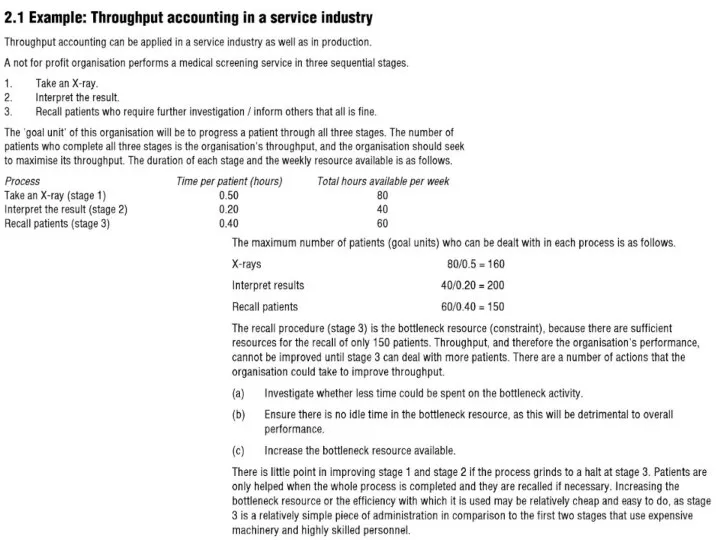

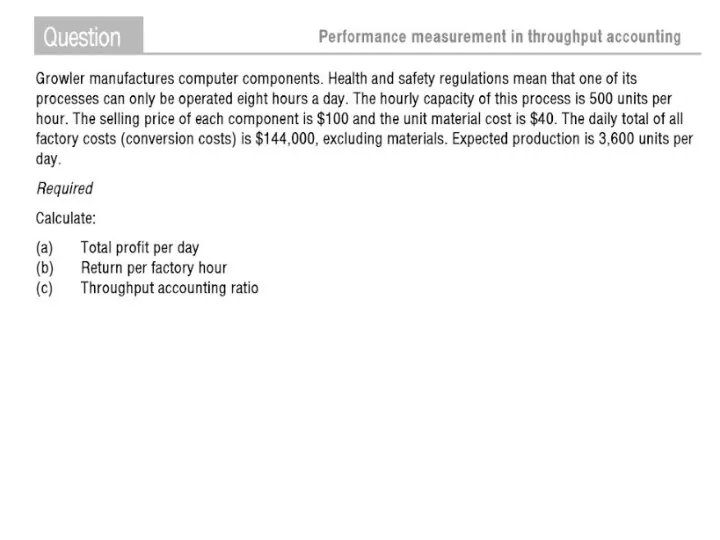

3. PERFORMANCE MEASURES IN THROUGHPUT ACCOUNTING

Profit per unit of bottleneck resource

3. PERFORMANCE MEASURES IN THROUGHPUT ACCOUNTING

Profit per unit of bottleneck resource

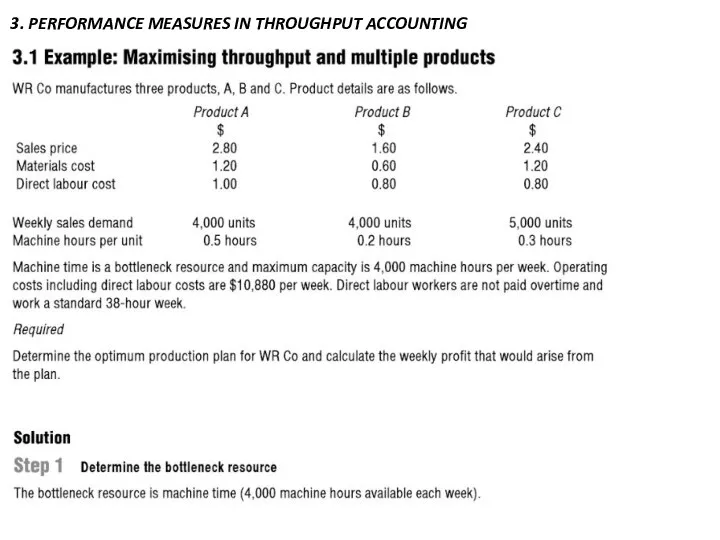

3. PERFORMANCE MEASURES IN THROUGHPUT ACCOUNTING

3. PERFORMANCE MEASURES IN THROUGHPUT ACCOUNTING

3. PERFORMANCE MEASURES IN THROUGHPUT ACCOUNTING

3. PERFORMANCE MEASURES IN THROUGHPUT ACCOUNTING

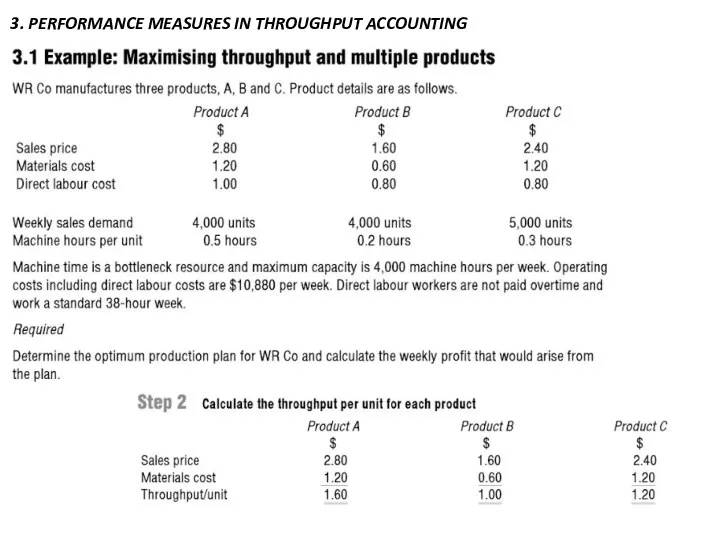

3. PERFORMANCE MEASURES IN THROUGHPUT ACCOUNTING

3. PERFORMANCE MEASURES IN THROUGHPUT ACCOUNTING

3. PERFORMANCE MEASURES IN THROUGHPUT ACCOUNTING

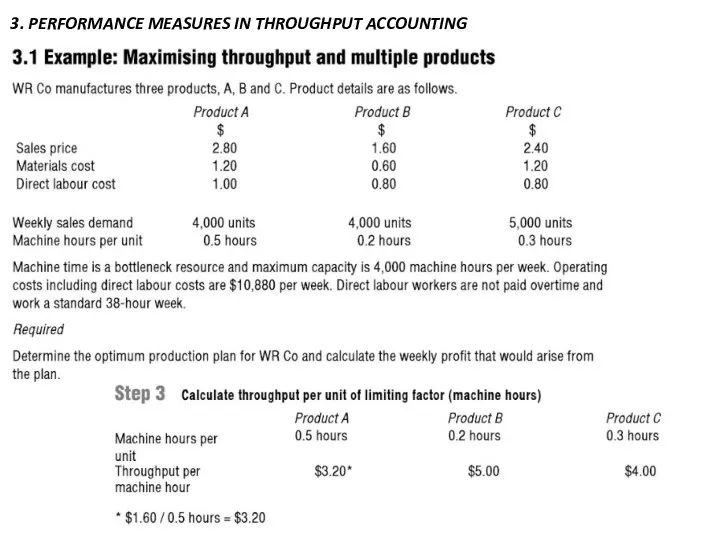

3. PERFORMANCE MEASURES IN THROUGHPUT ACCOUNTING

3. PERFORMANCE MEASURES IN THROUGHPUT ACCOUNTING

3. PERFORMANCE MEASURES IN THROUGHPUT ACCOUNTING

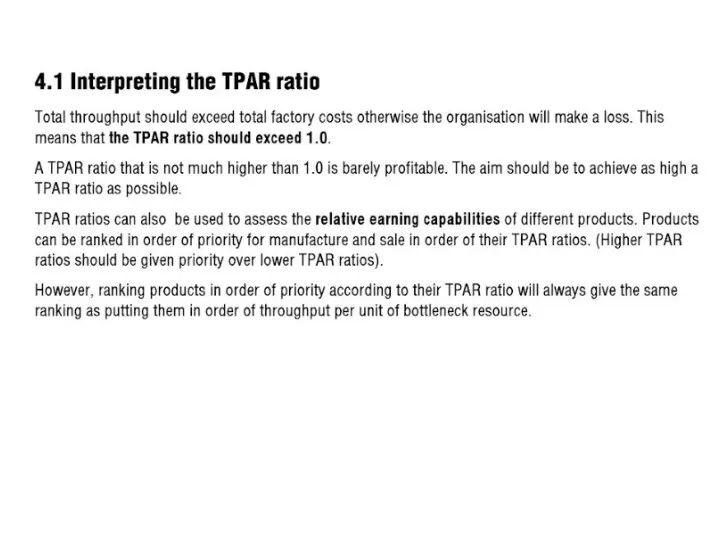

4. Throughput Accounting Ratio (TA ratio)

4. Throughput Accounting Ratio (TA ratio)

Поняття і визначення у сфері підтвердження відповідності. Сертифікація продукції. Акредитація. (Лекція 4-6)

Поняття і визначення у сфері підтвердження відповідності. Сертифікація продукції. Акредитація. (Лекція 4-6) История и сущность делового этикета, его специфика, основные функции

История и сущность делового этикета, его специфика, основные функции ВКР: Повышение эффективности использования основных средств в системе антикризисного управления

ВКР: Повышение эффективности использования основных средств в системе антикризисного управления Управление качеством

Управление качеством Закони, принципи, правила спілкування. (Лекція 1-2)

Закони, принципи, правила спілкування. (Лекція 1-2) Руководитель как организатор системы управления персоналом государственной службы

Руководитель как организатор системы управления персоналом государственной службы Shopping Live. Прием на работу

Shopping Live. Прием на работу Өнімді сертификаттау және оның негізгі бағыттары

Өнімді сертификаттау және оның негізгі бағыттары Анализ дерева неисправностей

Анализ дерева неисправностей Ораторское искусство – залог успешного лидера

Ораторское искусство – залог успешного лидера Основы управления проектами. Лекция 1

Основы управления проектами. Лекция 1 Основные понятия управления проектами. Современные практики и подходы к управлению IT-проектами

Основные понятия управления проектами. Современные практики и подходы к управлению IT-проектами Удовлетворенность, вовлеченность персонала Нижегородского ИВЦ

Удовлетворенность, вовлеченность персонала Нижегородского ИВЦ Управление организационными изменениями

Управление организационными изменениями Лекция 6. Инновационное управление человеческими ресурсами

Лекция 6. Инновационное управление человеческими ресурсами Сказка о том, как выработать решение в условиях риска и неопределенности

Сказка о том, как выработать решение в условиях риска и неопределенности Экспертные области в управлении проектами

Экспертные области в управлении проектами Мониторинг качества проектного управления в колледже

Мониторинг качества проектного управления в колледже Организационное стимулирование труда. Мотивация персонала

Организационное стимулирование труда. Мотивация персонала Ethical decision-making in everyday work situations. (Part 2)

Ethical decision-making in everyday work situations. (Part 2) Государственные стандарты Российской Федерации в сфере туристской деятельности

Государственные стандарты Российской Федерации в сфере туристской деятельности Проекты, которые изменили мир (тема 1)

Проекты, которые изменили мир (тема 1) Мотивация персонала

Мотивация персонала Принятие решений

Принятие решений Школы и теории управления

Школы и теории управления Подходы управления проектами. (Тема 3)

Подходы управления проектами. (Тема 3) Формирование и управление организационной культурой

Формирование и управление организационной культурой Теоретические основы тайм-менеджмента. Лекция 1

Теоретические основы тайм-менеджмента. Лекция 1