- Accounting and Financial Reporting

Содержание

- 2. Course objectives preparing and understanding companies’ financial statements

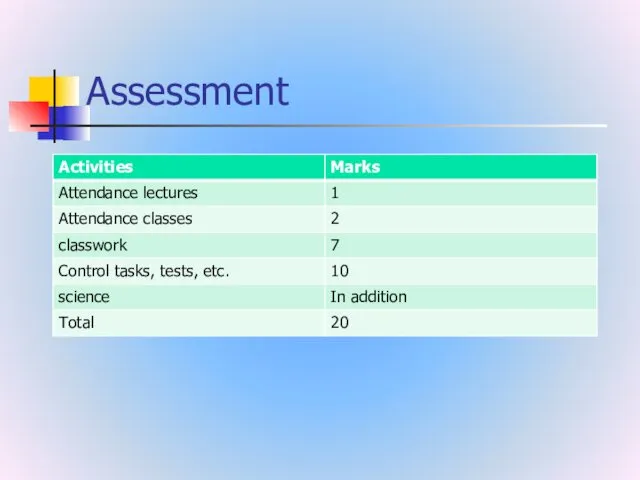

- 3. Assessment

- 4. Science International Scientific Students’ Congress (МНСК) – Fin. University +3 (+3-1 for 1-3 places) Prizes in

- 5. Essential reading Belverd E. Needles, Marian Powers, Susan V. Crosson Accounting principles David Alexander, Christopher Nobes

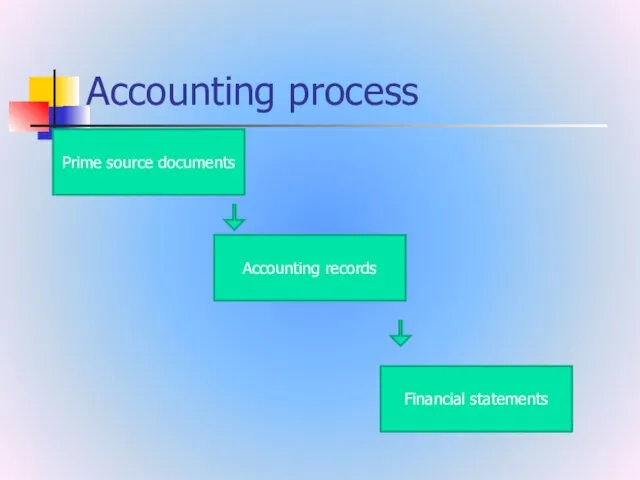

- 6. Accounting process Prime source documents Accounting records Financial statements

- 7. 1– Communications Through Financial Statements Identify the four financial statements

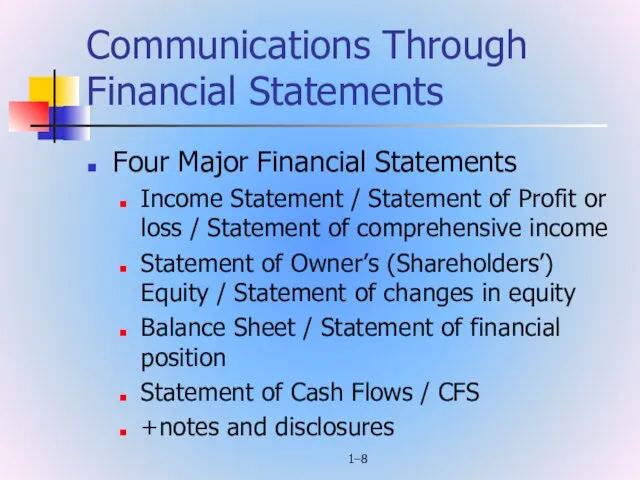

- 8. 1– Communications Through Financial Statements Four Major Financial Statements Income Statement / Statement of Profit or

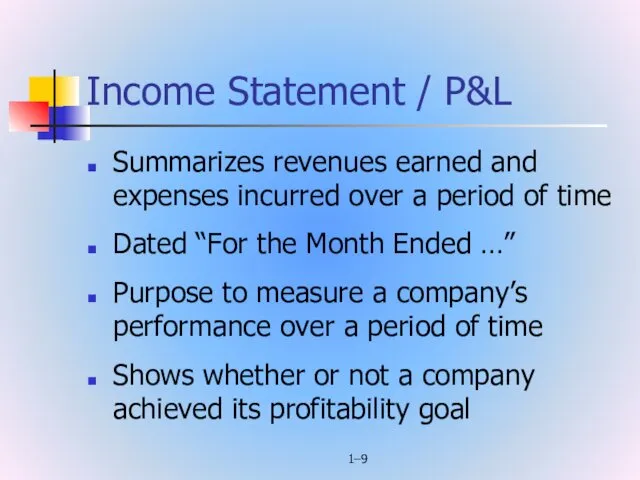

- 9. 1– Income Statement / P&L Summarizes revenues earned and expenses incurred over a period of time

- 10. 1– Income Statement (cont’d) Considered by many to be most important financial statement First financial statement

- 11. 1– Income Statement

- 12. 1– Statement of Owner’s Equity Shows changes in owner’s equity over a period of time Dated

- 13. 1– Statement of Owner’s Equity

- 14. 1– Balance Sheet Shows the financial position of a company on a certain date Dated as

- 15. 1– Balance Sheet

- 16. 1– Statement of Cash Flows Shows cash flows into and out of a business over a

- 17. 1– Statement of Cash Flows

- 18. 1– Discussion The balance sheet is often referred to as the statement of financial position. What

- 19. Towards a definition Accounting is a science as well as an art Accounting is concerned with

- 20. The American Institute of Certified Public Accountants: Accounting is the art of recording, classifying and summarizing

- 21. Accounting is the language of business (i) What he owns? (ii) What he owes? (iii) Whether

- 22. Decisions that users of accounting information make Economic (allocation of resources) Legal (management/stewardship)

- 23. A brief history stewardship function regular reports (financial reporting) accounting information is used to help make

- 24. The changing role of accounting Many businesses operate globally (different regulators, need for common set of

- 25. The functions of accounting Information for decisions Classification Measurement Stewardship Recording Monitoring and control Performance evaluation

- 26. Users of accounting information external internal

- 27. Common needs of most users (a) to decide when to buy, hold or sell an equity

- 28. Investors information to help them determine whether they should buy, hold or sell assess the ability

- 29. Employees stability and profitability of their employers ability of the entity to provide remuneration, retirement benefits

- 30. Lenders whether their loans, and the interest attaching to them, will be paid when due

- 31. Suppliers and other trade creditors determine whether amounts owing to them will be paid when due

- 32. Customers continuance of an entity, especially when they have a long-term involvement with, or are dependent

- 33. Governments and their agencies allocation of resources and, therefore, the activities of entities information in order

- 34. Public substantial contribution to the local economy trends and recent developments in the prosperity of the

- 35. Management interested in every aspect of accounting as their uses are diverse for different purposes interested

- 36. BOOK-KEEPING AND ACCOUNTANCY Book-keeping is the art of recording business transactions in a set of books

- 37. The functions of an accountant (i) Examination of entries made in the books of accounts (ii)

- 38. Accounting Financial Management Tax Cost Environmental Sustainability …

- 39. A comparison of financial accounting and management accounting

- 40. Accounting principles the rules based on assumptions, customs, usages and traditions for recording transactions Accounting principles

- 41. Need for Regulation Relevant&reliable information Comparability Fair information

- 42. Sources of Regulation Accounting Standards Company Law *Listing Rules

- 43. GAAP International National IAS IFRS UK GAAP US GAAP

- 44. IASB IFRS IAS Conceptual Framework for Financial Reporting IFRIC SIC issued before 2001

- 45. IASB www.ifrs.org The mission To develop IFRS Standards that bring transparency, accountability and efficiency to financial

- 46. IFRS Standards Strengthen accountability Bring transparency Contribute to economic efficiency

- 47. The Need for a Conceptual Framework To develop a coherent set of standards and rules To

- 48. Purpose of the Conceptual Framework (a) to assist the Board in the development of future IFRSs

- 49. The Conceptual Framework deals with: (a) the objective of financial reporting; (b) the qualitative characteristics of

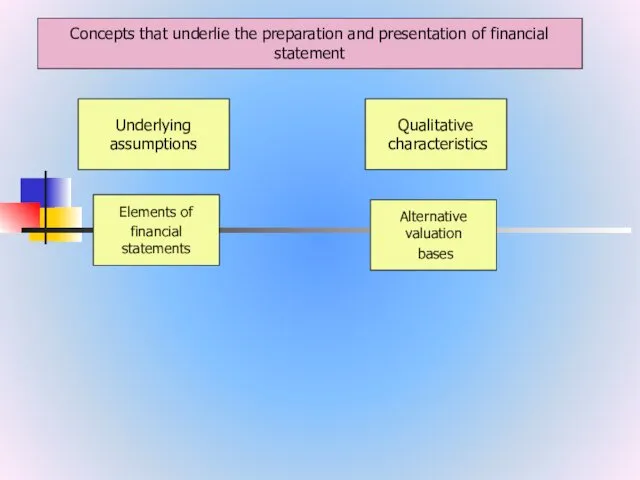

- 50. Concepts that underlie the preparation and presentation of financial statement Underlying assumptions Qualitative characteristics Elements of

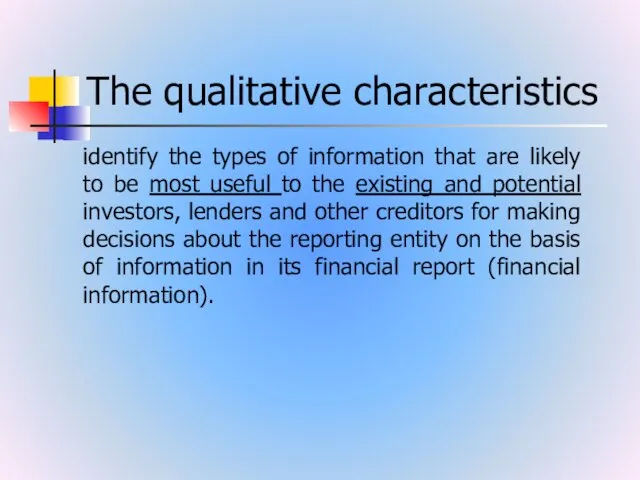

- 51. The qualitative characteristics identify the types of information that are likely to be most useful to

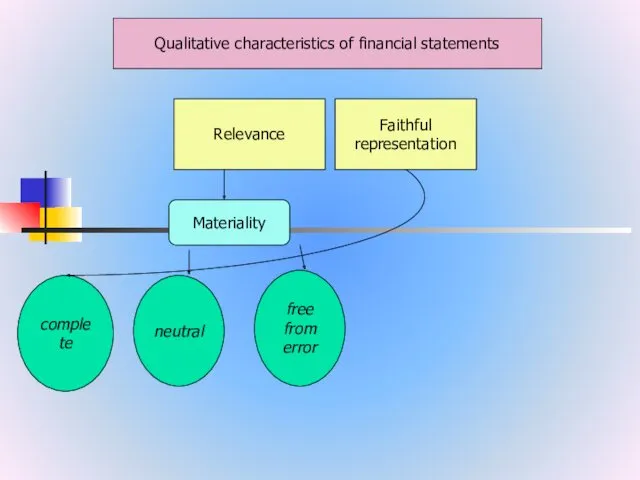

- 52. Qualitative characteristics of financial statements Relevance Faithful representation Materiality complete neutral free from error

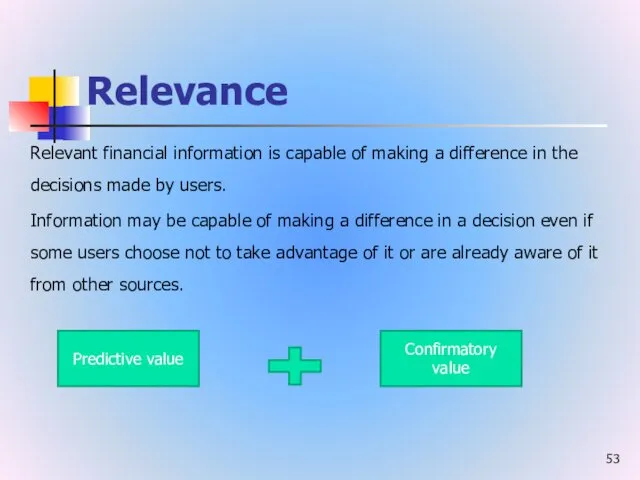

- 53. Relevance Relevant financial information is capable of making a difference in the decisions made by users.

- 54. Faithful representation financial information must faithfully represent the phenomena that it purports to represent

- 55. complete A complete depiction includes all information necessary for a user to understand the phenomenon being

- 56. neutral A neutral depiction is without bias in the selection or presentation of financial information

- 57. free from error there are no errors or omissions in the description of the phenomenon, and

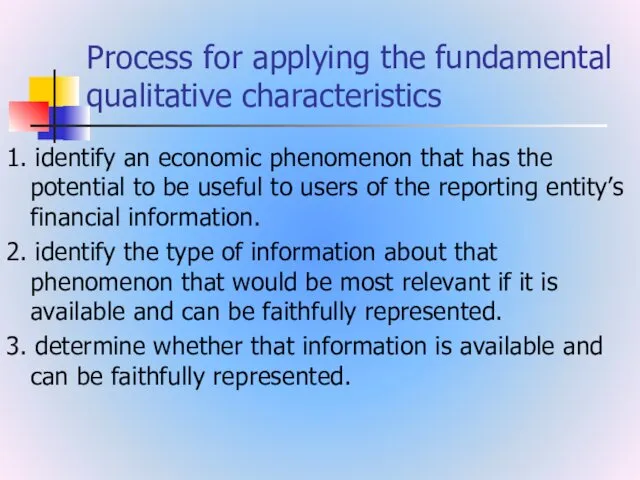

- 58. Process for applying the fundamental qualitative characteristics 1. identify an economic phenomenon that has the potential

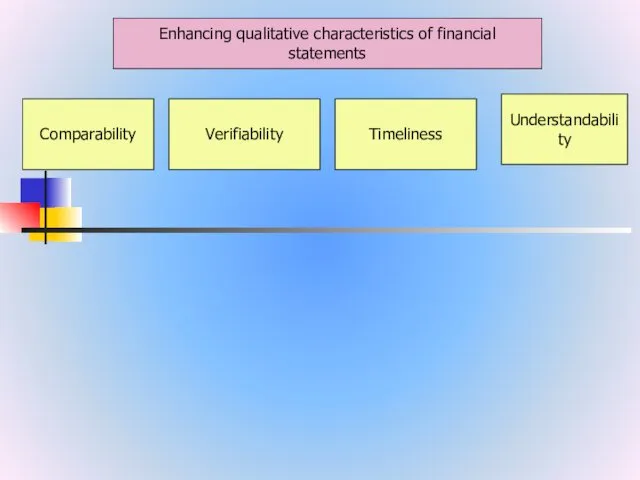

- 59. Enhancing qualitative characteristics of financial statements Understandability Verifiability Timeliness Comparability

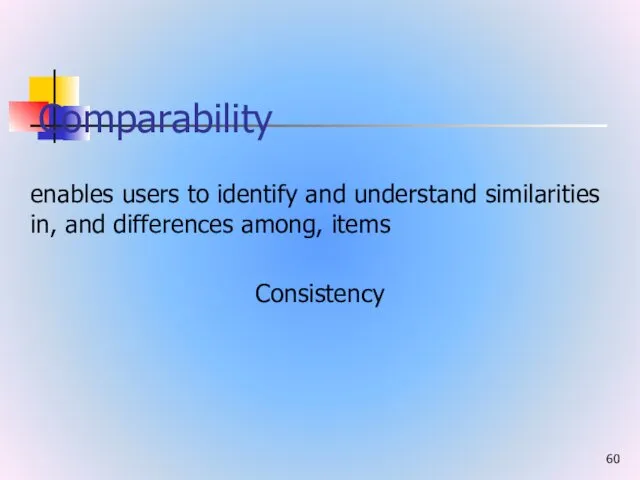

- 60. Comparability enables users to identify and understand similarities in, and differences among, items Consistency

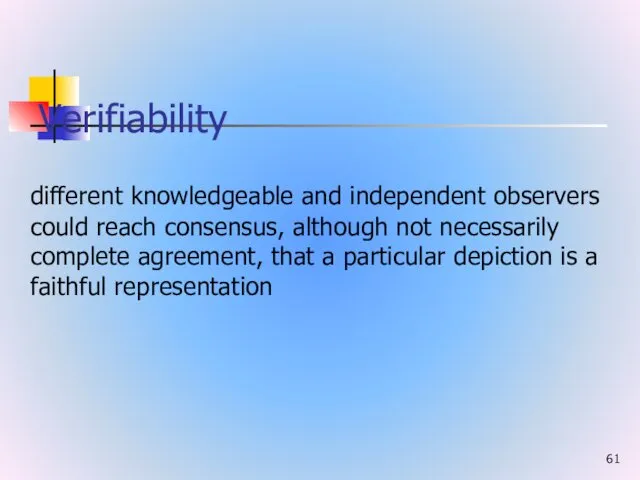

- 61. Verifiability different knowledgeable and independent observers could reach consensus, although not necessarily complete agreement, that a

- 62. Timeliness having information available to decision-makers in time to be capable of influencing their decisions

- 63. Understandability Classifying, characterising and presenting information clearly and concisely makes it understandable

- 64. The cost constraint on useful financial reporting Providers of financial information - collecting, processing, verifying and

- 65. Underlying assumption The financial statements are normally prepared on the assumption that an entity is a

- 66. Accrual basis Effects of transactions and other events are recognised when they occur (and not as

- 67. 1– Money Measurement Recording of all business transactions in terms of money Money is the only

- 68. 1– Money Measure (cont’d) Exchange Rate The value of one currency in terms of another Changes

- 69. 1– Separate Entity A business is distinct from its Owner(s) Creditors Customers Its financial records and

- 70. The elements of financial statements Assets Liabilities Equity financial position

- 71. Profit Income Expenses Performance

- 72. Recognition of the elements of financial statements The probability of future economic benefit Reliability of measurement

- 73. Measurement of the elements of financial statements Historical cost Current cost Realisable (settlement) value Present value

- 74. Concepts of capital financial concept physical concept

- 76. Скачать презентацию

Course objectives

preparing and understanding companies’ financial statements

Course objectives

preparing and understanding companies’ financial statements

Assessment

Assessment

Science

International Scientific Students’ Congress (МНСК) – Fin. University +3 (+3-1 for

Science

International Scientific Students’ Congress (МНСК) – Fin. University +3 (+3-1 for

Essential reading

Belverd E. Needles, Marian Powers, Susan V. Crosson Accounting

Essential reading

Belverd E. Needles, Marian Powers, Susan V. Crosson Accounting

Accounting process

Prime source documents

Accounting records

Financial statements

Accounting process

Prime source documents

Accounting records

Financial statements

1–

Communications Through

Financial Statements

Identify the four financial statements

1–

Communications Through

Financial Statements

Identify the four financial statements

1–

Communications Through Financial Statements

Four Major Financial Statements

Income Statement / Statement of

1–

Communications Through Financial Statements

Four Major Financial Statements

Income Statement / Statement of

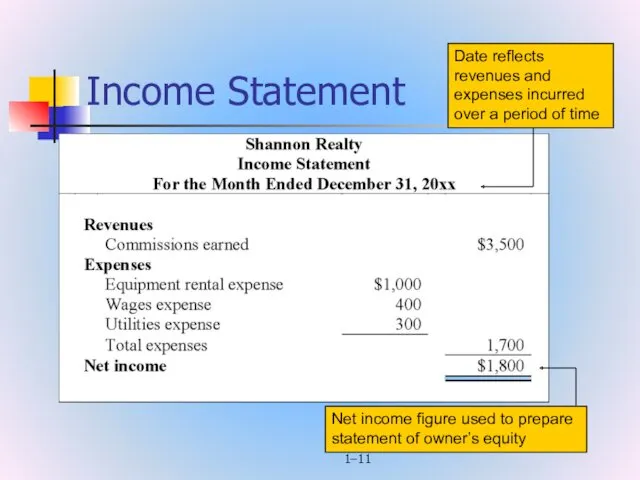

1–

Income Statement / P&L

Summarizes revenues earned and expenses incurred over a

1–

Income Statement / P&L

Summarizes revenues earned and expenses incurred over a

1–

Income Statement (cont’d)

Considered by many to be most important financial statement

1–

Income Statement (cont’d)

Considered by many to be most important financial statement

1–

Income Statement

1–

Income Statement

1–

Statement of Owner’s Equity

Shows changes in owner’s equity over a period

1–

Statement of Owner’s Equity

Shows changes in owner’s equity over a period

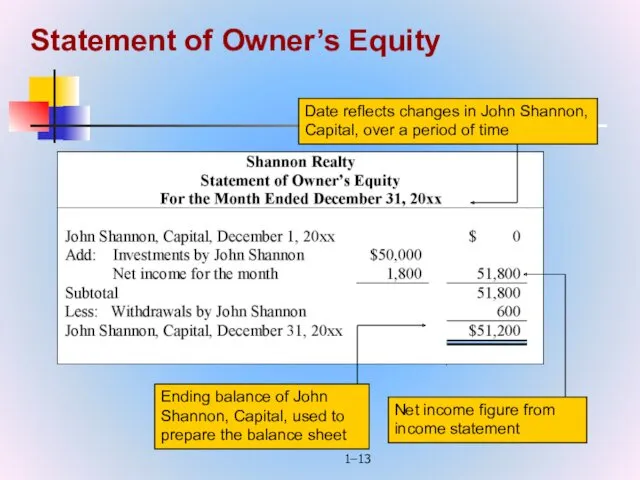

1–

Statement of Owner’s Equity

1–

Statement of Owner’s Equity

1–

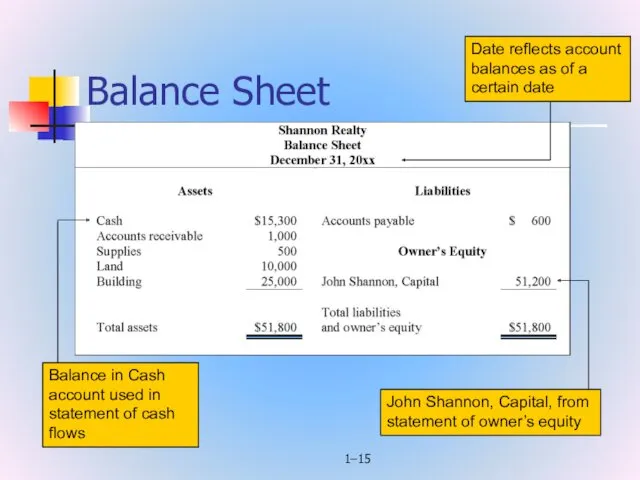

Balance Sheet

Shows the financial position of a company on a certain

1–

Balance Sheet

Shows the financial position of a company on a certain

1–

Balance Sheet

1–

Balance Sheet

1–

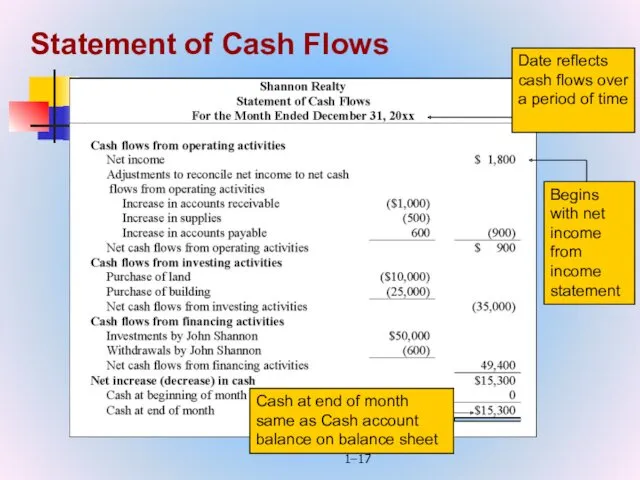

Statement of Cash Flows

Shows cash flows into and out of a

1–

Statement of Cash Flows

Shows cash flows into and out of a

1–

Statement of Cash Flows

1–

Statement of Cash Flows

1–

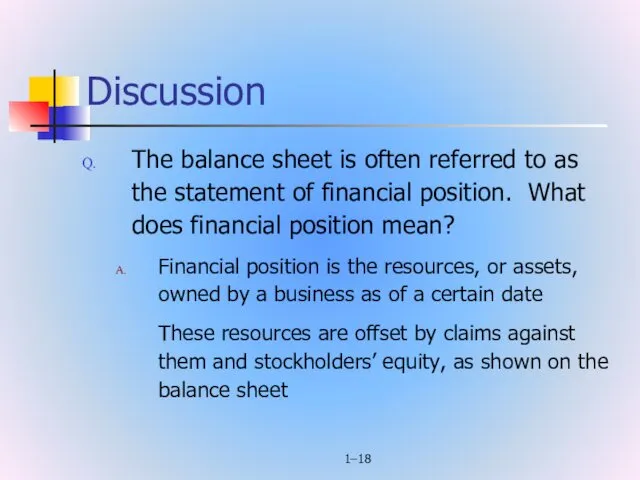

Discussion

The balance sheet is often referred to as the statement of

1–

Discussion

The balance sheet is often referred to as the statement of

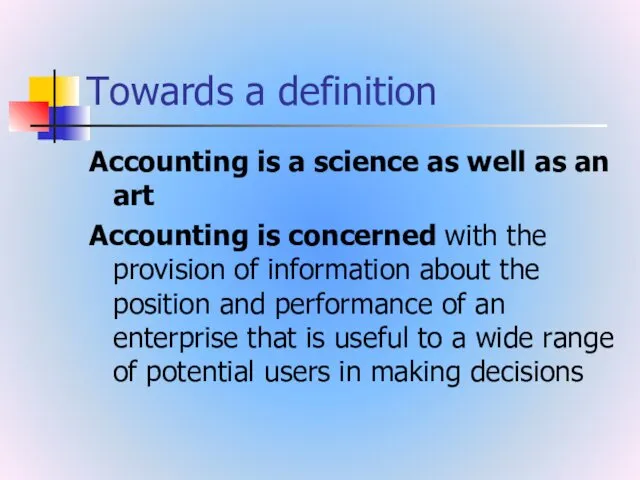

Towards a definition

Accounting is a science as well as an art

Accounting

Towards a definition

Accounting is a science as well as an art

Accounting

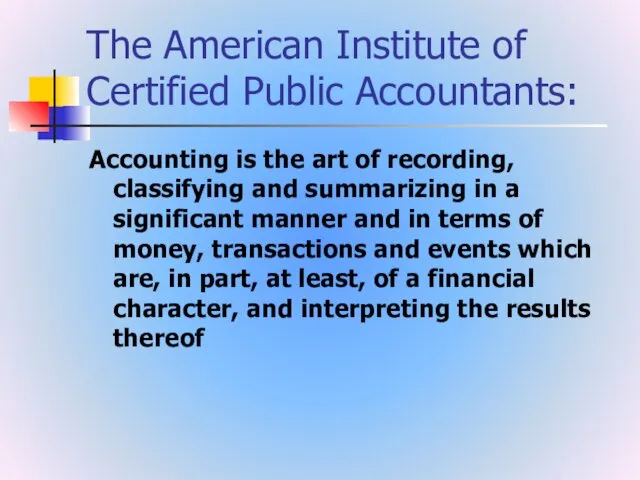

The American Institute of Certified Public Accountants:

Accounting is the art of

The American Institute of Certified Public Accountants:

Accounting is the art of

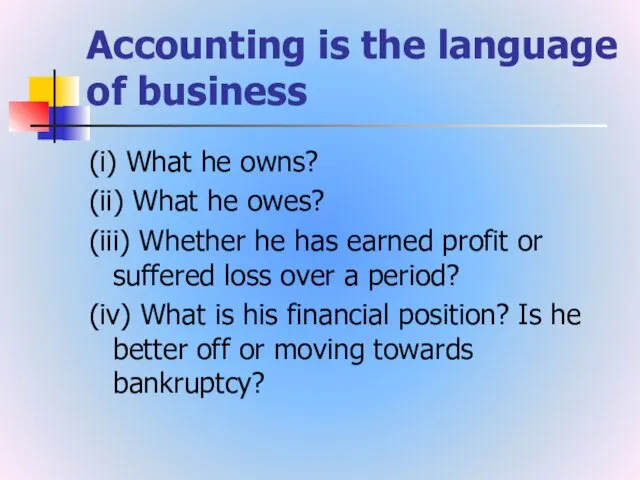

Accounting is the language of business

(i) What he owns?

(ii) What he

Accounting is the language of business

(i) What he owns?

(ii) What he

Decisions that users of accounting information make

Economic

(allocation of resources)

Legal

(management/stewardship)

Decisions that users of accounting information make

Economic

(allocation of resources)

Legal

(management/stewardship)

A brief history

stewardship function

regular reports (financial reporting)

accounting information is used to

A brief history

stewardship function

regular reports (financial reporting)

accounting information is used to

The changing role of accounting

Many businesses operate globally (different regulators, need

The changing role of accounting

Many businesses operate globally (different regulators, need

The functions of accounting

Information for decisions

Classification

Measurement

Stewardship

Recording

Monitoring and control

Performance evaluation and compensation

Communication

The functions of accounting

Information for decisions

Classification

Measurement

Stewardship

Recording

Monitoring and control

Performance evaluation and compensation

Communication

Users of accounting information

external

internal

Users of accounting information

external

internal

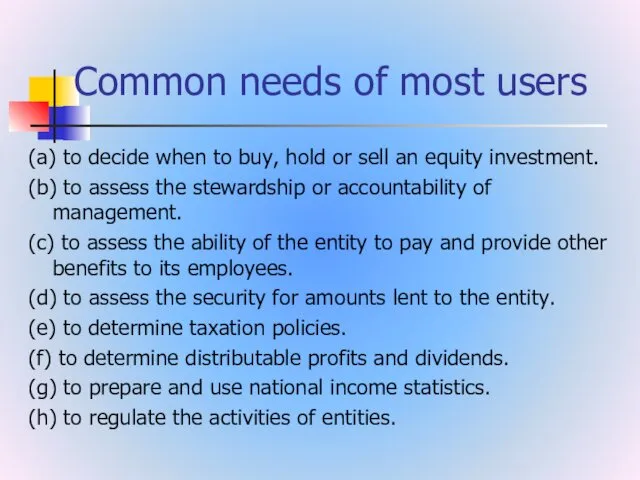

Common needs of most users

(a) to decide when to buy, hold

Common needs of most users

(a) to decide when to buy, hold

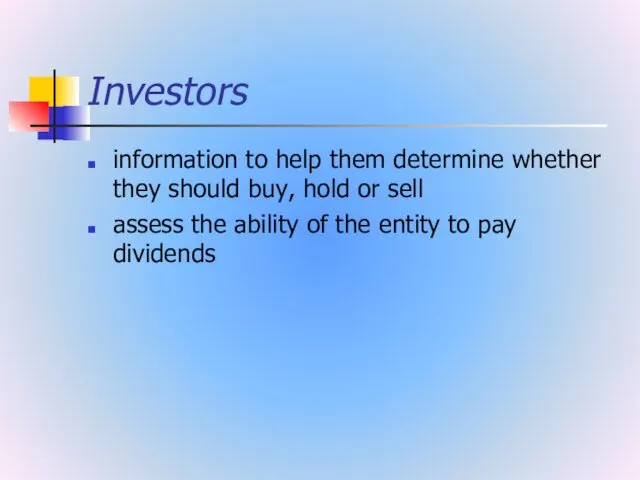

Investors

information to help them determine whether they should buy, hold or

Investors

information to help them determine whether they should buy, hold or

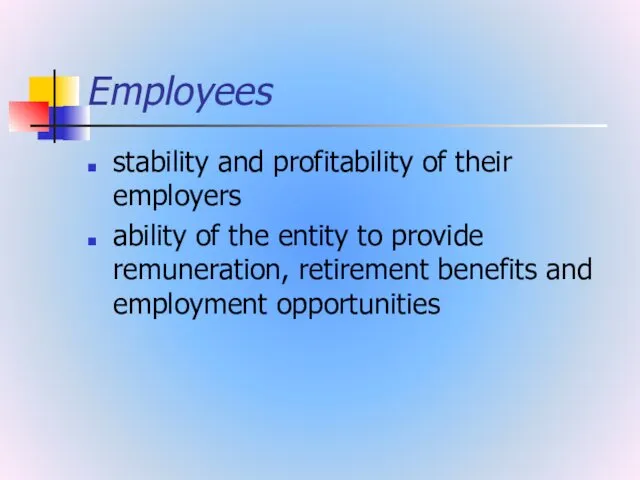

Employees

stability and profitability of their employers

ability of the entity to provide

Employees

stability and profitability of their employers

ability of the entity to provide

Lenders

whether their loans, and the interest attaching to them, will be

Lenders

whether their loans, and the interest attaching to them, will be

Suppliers and other trade creditors

determine whether amounts owing to them will

Suppliers and other trade creditors

determine whether amounts owing to them will

Customers

continuance of an entity, especially when they have a long-term involvement

Customers

continuance of an entity, especially when they have a long-term involvement

Governments and their agencies

allocation of resources and, therefore, the activities of

Governments and their agencies

allocation of resources and, therefore, the activities of

Public

substantial contribution to the local economy

trends and recent developments in the

Public

substantial contribution to the local economy

trends and recent developments in the

Management

interested in every aspect of accounting as their uses are diverse

Management

interested in every aspect of accounting as their uses are diverse

BOOK-KEEPING AND ACCOUNTANCY

Book-keeping is the art of recording business transactions in

BOOK-KEEPING AND ACCOUNTANCY

Book-keeping is the art of recording business transactions in

The functions of an accountant

(i) Examination of entries made in the

The functions of an accountant

(i) Examination of entries made in the

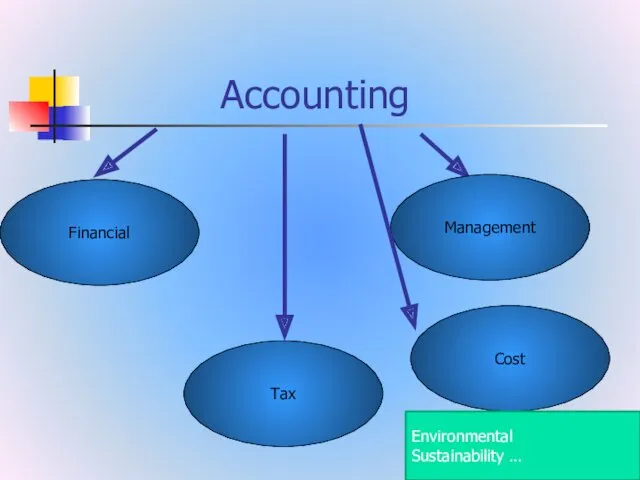

Accounting

Financial

Management

Tax

Cost

Environmental

Sustainability …

Accounting

Financial

Management

Tax

Cost

Environmental

Sustainability …

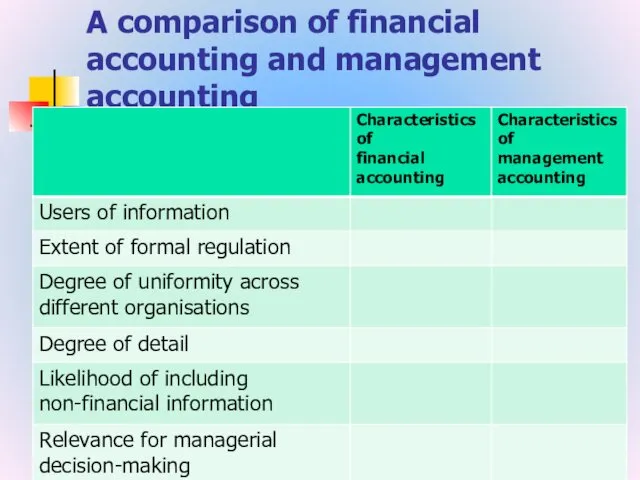

A comparison of financial accounting and management accounting

A comparison of financial accounting and management accounting

Accounting principles

the rules based on assumptions, customs, usages and traditions

Accounting principles

the rules based on assumptions, customs, usages and traditions

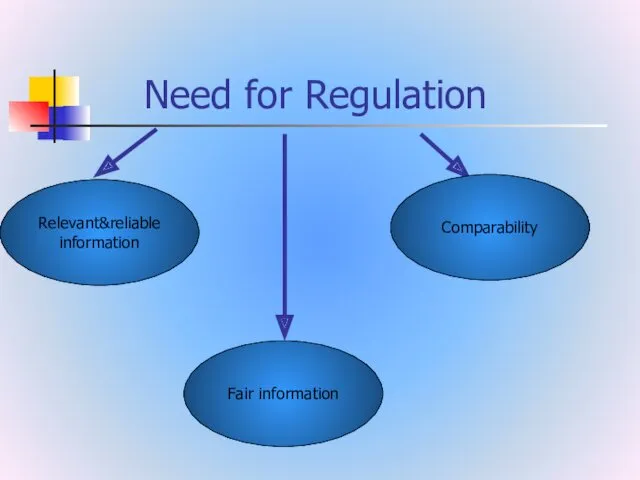

Need for Regulation

Relevant&reliable

information

Comparability

Fair information

Need for Regulation

Relevant&reliable

information

Comparability

Fair information

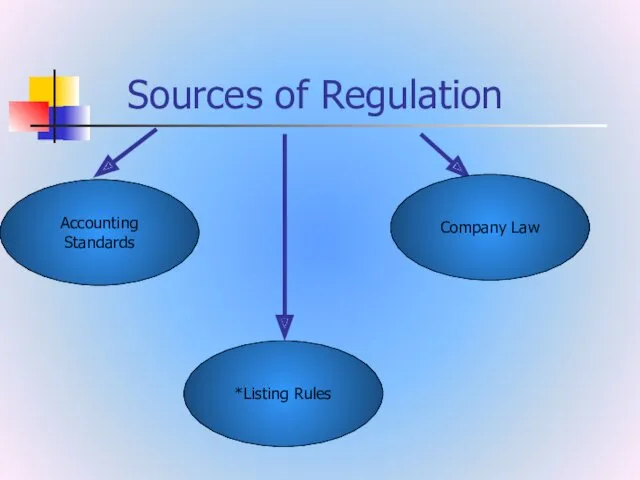

Sources of Regulation

Accounting Standards

Company Law

*Listing Rules

Sources of Regulation

Accounting Standards

Company Law

*Listing Rules

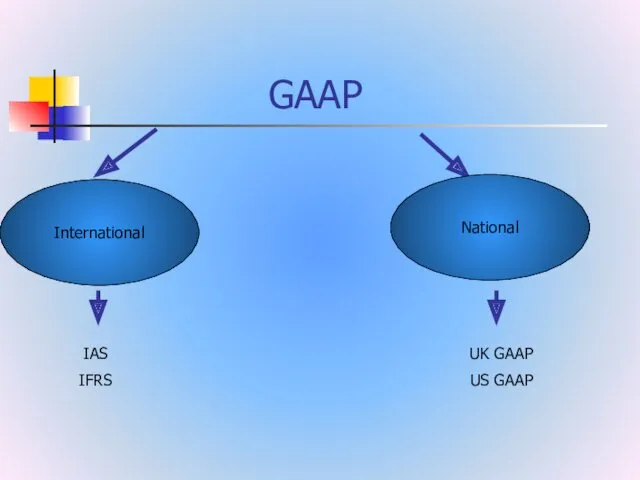

GAAP

International

National

IAS

IFRS

UK GAAP

US GAAP

GAAP

International

National

IAS

IFRS

UK GAAP

US GAAP

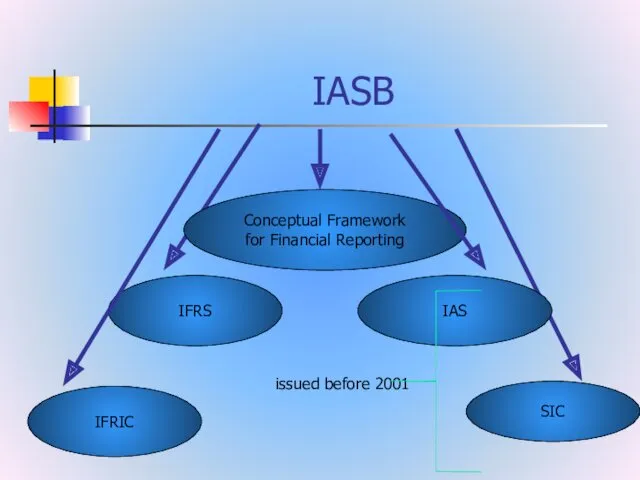

IASB

IFRS

IAS

Conceptual Framework

for Financial Reporting

IFRIC

SIC

issued before 2001

IASB

IFRS

IAS

Conceptual Framework

for Financial Reporting

IFRIC

SIC

issued before 2001

IASB

www.ifrs.org

The mission

To develop IFRS Standards that bring transparency, accountability and

IASB

www.ifrs.org

The mission

To develop IFRS Standards that bring transparency, accountability and

IFRS Standards

Strengthen accountability

Bring transparency

Contribute to economic efficiency

IFRS Standards

Strengthen accountability

Bring transparency

Contribute to economic efficiency

The Need for a Conceptual Framework

To develop a coherent set of

The Need for a Conceptual Framework

To develop a coherent set of

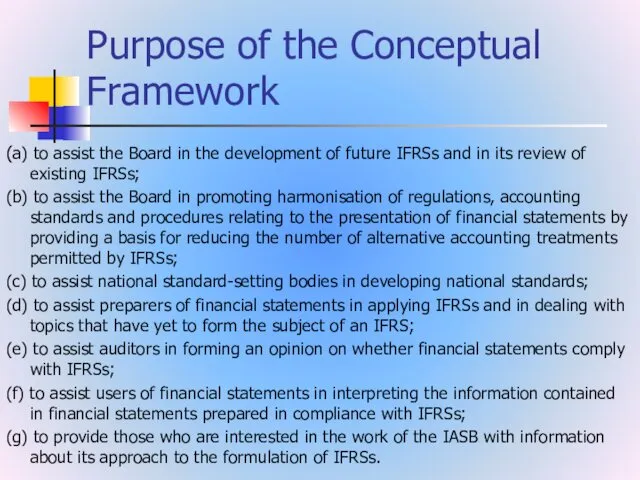

Purpose of the Conceptual

Framework

(a) to assist the Board in the development

Purpose of the Conceptual

Framework

(a) to assist the Board in the development

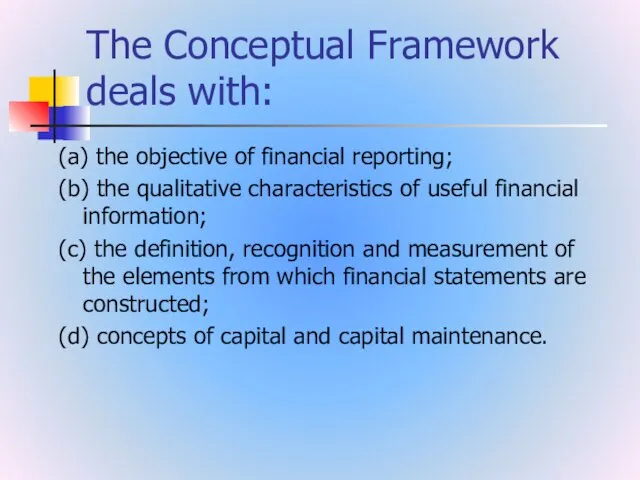

The Conceptual Framework deals with:

(a) the objective of financial reporting;

(b) the

The Conceptual Framework deals with:

(a) the objective of financial reporting;

(b) the

Concepts that underlie the preparation and presentation of financial statement

Underlying

assumptions

Qualitative

Concepts that underlie the preparation and presentation of financial statement

Underlying

assumptions

Qualitative

The qualitative characteristics

identify the types of information that are likely

The qualitative characteristics

identify the types of information that are likely

Qualitative characteristics of financial statements

Relevance

Faithful

representation

Materiality

complete

neutral

free

from

error

Qualitative characteristics of financial statements

Relevance

Faithful

representation

Materiality

complete

neutral

free

from

error

Relevance

Relevant financial information is capable of making a difference in the

Relevance

Relevant financial information is capable of making a difference in the

Faithful representation

financial information must faithfully represent the phenomena that it purports

Faithful representation

financial information must faithfully represent the phenomena that it purports

complete

A complete depiction includes all information necessary for a user to

complete

A complete depiction includes all information necessary for a user to

neutral

A neutral depiction is without bias in the selection or presentation

neutral

A neutral depiction is without bias in the selection or presentation

free

from

error

there are no errors or omissions in the description

free

from

error

there are no errors or omissions in the description

Process for applying the fundamental qualitative characteristics

1. identify an economic phenomenon

Process for applying the fundamental qualitative characteristics

1. identify an economic phenomenon

Enhancing qualitative characteristics of financial statements

Understandability

Verifiability

Timeliness

Comparability

Enhancing qualitative characteristics of financial statements

Understandability

Verifiability

Timeliness

Comparability

Comparability

enables users to identify and understand similarities in, and differences among,

Comparability

enables users to identify and understand similarities in, and differences among,

Verifiability

different knowledgeable and independent observers could reach consensus, although not necessarily

Verifiability

different knowledgeable and independent observers could reach consensus, although not necessarily

Timeliness

having information available to decision-makers in time to be capable of

Timeliness

having information available to decision-makers in time to be capable of

Understandability

Classifying, characterising and presenting information clearly and concisely makes it understandable

Understandability

Classifying, characterising and presenting information clearly and concisely makes it understandable

The cost constraint on useful financial reporting

Providers of financial information -

The cost constraint on useful financial reporting

Providers of financial information -

Underlying assumption

The financial statements are normally prepared on the assumption that

Underlying assumption

The financial statements are normally prepared on the assumption that

Accrual basis

Effects of transactions and other events are

recognised when they occur

Accrual basis

Effects of transactions and other events are

recognised when they occur

1–

Money Measurement

Recording of all business transactions in terms of money

Money is

1–

Money Measurement

Recording of all business transactions in terms of money

Money is

1–

Money Measure (cont’d)

Exchange Rate

The value of one currency in terms of

1–

Money Measure (cont’d)

Exchange Rate

The value of one currency in terms of

1–

Separate Entity

A business is distinct from its

Owner(s)

Creditors

Customers

Its financial records and reports

1–

Separate Entity

A business is distinct from its

Owner(s)

Creditors

Customers

Its financial records and reports

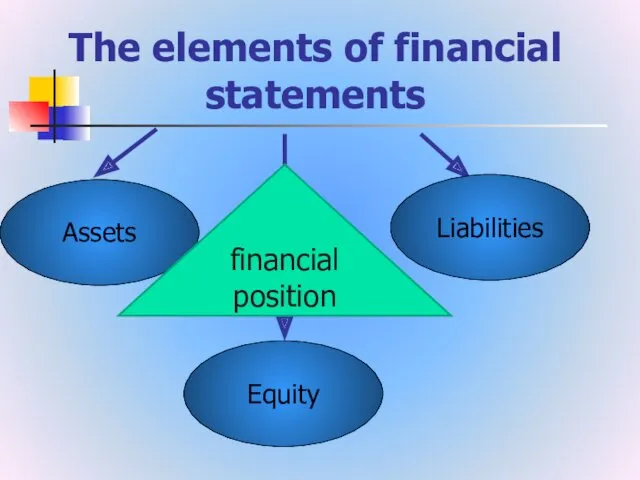

The elements of financial statements

Assets

Liabilities

Equity

financial

position

The elements of financial statements

Assets

Liabilities

Equity

financial

position

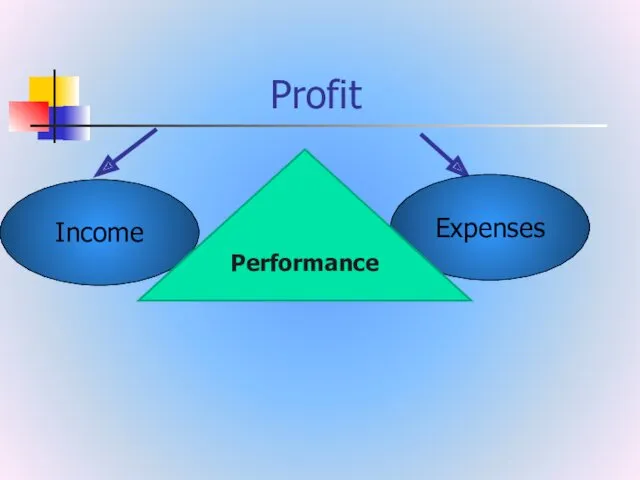

Profit

Income

Expenses

Performance

Profit

Income

Expenses

Performance

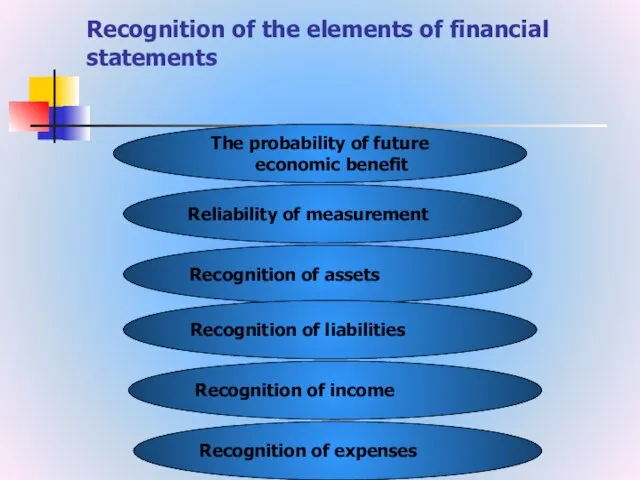

Recognition of the elements of financial statements

The probability of future economic

Recognition of the elements of financial statements

The probability of future economic

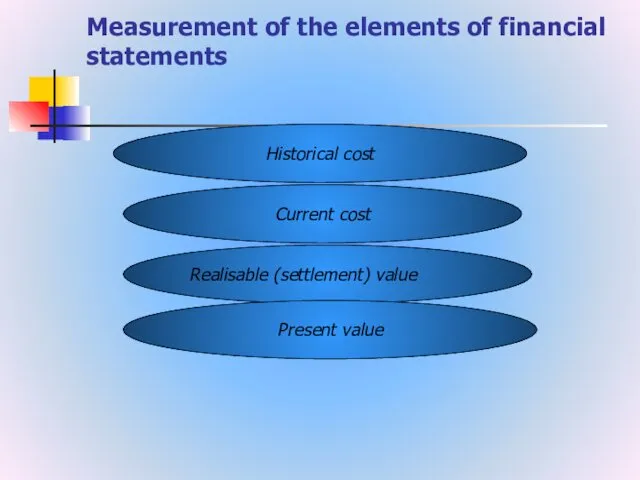

Measurement of the elements of financial statements

Historical cost

Current cost

Realisable (settlement) value

Present

Measurement of the elements of financial statements

Historical cost

Current cost

Realisable (settlement) value

Present

Concepts of capital

financial concept

physical concept

Concepts of capital

financial concept

physical concept

Тәуекелділік және табыстылық

Тәуекелділік және табыстылық ВКР: Финансовое состояние как фактор обеспечения экономической безопасности организации

ВКР: Финансовое состояние как фактор обеспечения экономической безопасности организации Учет основных средств в 2023 году

Учет основных средств в 2023 году История возникновения денег

История возникновения денег Світовий ринок робочої сили. Міжнародна міграція робочої сили (Тема 7, Тема 8)

Світовий ринок робочої сили. Міжнародна міграція робочої сили (Тема 7, Тема 8) Фінансовий аналіз діяльності комерційних банків

Фінансовий аналіз діяльності комерційних банків Деньги и денежный оборот

Деньги и денежный оборот Лизинг как форма финансирования капитальных вложений (на примере ООО Мир у дачи)

Лизинг как форма финансирования капитальных вложений (на примере ООО Мир у дачи) Содействие повышению уровня финансовой грамотности населения и развитию финансового образования в РФ в Республике Татарстан

Содействие повышению уровня финансовой грамотности населения и развитию финансового образования в РФ в Республике Татарстан Анализ финансового состояния компании. (Лекция 3)

Анализ финансового состояния компании. (Лекция 3) Налог на доходы физических лиц

Налог на доходы физических лиц Совершенствование системы оплаты труда персонала на примере ООО Промтехэнерго

Совершенствование системы оплаты труда персонала на примере ООО Промтехэнерго Финансовый контроль

Финансовый контроль Прием подраздела 1.2. Сведения о страховом стаже формы ЕФС-1

Прием подраздела 1.2. Сведения о страховом стаже формы ЕФС-1 Деятельность Фонда социального страхования

Деятельность Фонда социального страхования Формирование финансовой грамотности

Формирование финансовой грамотности Анализ финансового состояния предприятия

Анализ финансового состояния предприятия Деятельность администрации города Апатиты для создания благоприятных условий для развития малого и среднего предпринимательства

Деятельность администрации города Апатиты для создания благоприятных условий для развития малого и среднего предпринимательства Отчет о работе фонда социальной поддержки населения города Урень (РАСТЕМ ВМЕСТЕ)

Отчет о работе фонда социальной поддержки населения города Урень (РАСТЕМ ВМЕСТЕ) Система MyAdvertisingPays

Система MyAdvertisingPays The equity. Implications of taxation. Tax incidence. (Lecture 11-19)

The equity. Implications of taxation. Tax incidence. (Lecture 11-19) Учет и анализ денежных средств в ООО НПК Механика Сервис

Учет и анализ денежных средств в ООО НПК Механика Сервис Франшиза. Франшайзиинг. Патент. Сертификация. Ноу хау. Лицензия

Франшиза. Франшайзиинг. Патент. Сертификация. Ноу хау. Лицензия Еңбекақы бойынша жұмысшылармен және бюджетпен есеп айырысу есебін ұйымдастыру

Еңбекақы бойынша жұмысшылармен және бюджетпен есеп айырысу есебін ұйымдастыру Технологія складання бізнес-плану

Технологія складання бізнес-плану Доходность и риск финансовой операции

Доходность и риск финансовой операции Правове регулювання валютних операцій

Правове регулювання валютних операцій О мерах социальной поддержки семей с детьми

О мерах социальной поддержки семей с детьми