- An overview of financial system

Содержание

- 2. Function of Financial Markets ` To bring lenders and borrowers together to make both of them

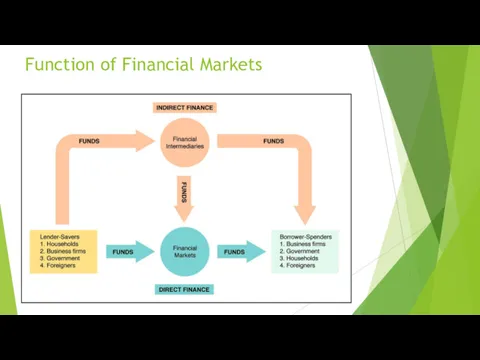

- 3. Function of Financial Markets

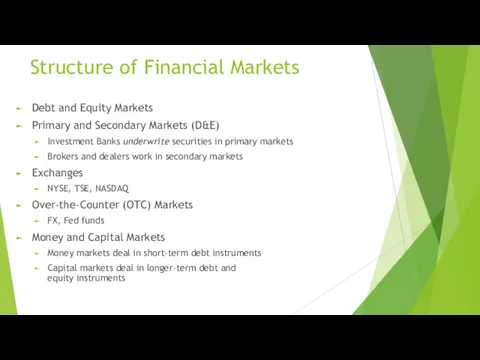

- 4. Structure of Financial Markets Debt and Equity Markets Primary and Secondary Markets (D&E) Investment Banks underwrite

- 5. Financial Intermediaries Financial Intermediation is the process of transforming certain financial assets into more widely preferred

- 6. Functions of Intermediation : Indirect Finance Lower transaction costs (time and money spent in carrying out

- 7. Functions of Intermediation : Indirect Finance Deal with asymmetric information problems (before the transaction) Adverse Selection:

- 8. Financial Intermediaries A closer look at Financial Institutions Types Banks – Commercial, Investment, Credit Unions, Savings

- 9. Financial intermediaries There are other services that financial intermediaries can provide: Facilitating the trading of financial

- 10. Types of financial intermediaries Brokers help their clients buy/sell securities by finding counterparties to trade in

- 12. Regulation of the Financial System To increase the information available to investors: Reduce adverse selection and

- 13. Commercial Banks Most prominent financial institution Range in size from huge to small Major sources of

- 14. INVESTMENT BANKS Help corporations sell securities to investors (underwriting services) Provide advice to firms about merger&

- 15. CREDIT UNIONS Credit unions are similar to traditional banks in the sense that both institutions offer

- 16. Insurance Companies Insurance companies play an important role in an economy in that they are risk

- 17. Life Insurance Companies Insure against death Receive funds in form of premiums Use of funds is

- 18. Property and Casualty Insurance Companies Insure homeowners and businesses against losses Receive premiums Need to be

- 19. Investment Companies Investment Companies, also known as asset management companies, manage the funds of individuals, businesses

- 20. Investment Companies: Pension Funds Concerned with long run Receive funds from working individuals building “nest-egg” Accurate

- 21. Finance companies Finance companies raise funds by selling commercial paper and by issuing stocks and bonds

- 22. Investment Companies : Mutual Funds A mutual fund accepts funds from investors who in exchange receive

- 24. Скачать презентацию

Function of Financial Markets

`

To bring lenders and borrowers together to make

Function of Financial Markets

`

To bring lenders and borrowers together to make

Function of Financial Markets

Function of Financial Markets

Structure of Financial Markets

Debt and Equity Markets

Primary and Secondary Markets (D&E)

Investment

Structure of Financial Markets

Debt and Equity Markets

Primary and Secondary Markets (D&E)

Investment

Financial Intermediaries

Financial Intermediation is the process of transforming certain financial assets

Financial Intermediaries

Financial Intermediation is the process of transforming certain financial assets

Functions of Intermediation : Indirect Finance

Lower transaction costs (time and money

Functions of Intermediation : Indirect Finance

Lower transaction costs (time and money

Functions of Intermediation : Indirect Finance

Deal with asymmetric information problems

(before the

Functions of Intermediation : Indirect Finance

Deal with asymmetric information problems

(before the

Financial Intermediaries

A closer look at Financial Institutions

Types

Banks – Commercial, Investment, Credit

Financial Intermediaries

A closer look at Financial Institutions

Types

Banks – Commercial, Investment, Credit

Financial intermediaries

There are other services that financial intermediaries can provide:

Facilitating the

Financial intermediaries

There are other services that financial intermediaries can provide:

Facilitating the

Types of financial intermediaries

Brokers help their clients buy/sell securities by

Types of financial intermediaries

Brokers help their clients buy/sell securities by

Regulation of the Financial System

To increase the information available to investors:

Reduce

Regulation of the Financial System

To increase the information available to investors:

Reduce

Commercial Banks

Most prominent financial institution

Range in size from huge to small

Commercial Banks

Most prominent financial institution

Range in size from huge to small

INVESTMENT BANKS

Help corporations sell securities to investors (underwriting services)

Provide advice to

INVESTMENT BANKS

Help corporations sell securities to investors (underwriting services)

Provide advice to

CREDIT UNIONS

Credit unions are similar to traditional banks in the sense

CREDIT UNIONS

Credit unions are similar to traditional banks in the sense

Insurance Companies

Insurance companies play an important role in an economy in

Insurance Companies

Insurance companies play an important role in an economy in

Life Insurance Companies

Insure against death

Receive funds in form of premiums

Use of

Life Insurance Companies

Insure against death

Receive funds in form of premiums

Use of

Property and Casualty Insurance Companies

Insure homeowners and businesses against losses

Receive premiums

Need

Property and Casualty Insurance Companies

Insure homeowners and businesses against losses

Receive premiums

Need

Investment Companies

Investment Companies, also known as asset management companies, manage

Investment Companies

Investment Companies, also known as asset management companies, manage

Investment Companies: Pension Funds

Concerned with long run

Receive funds from working individuals

Investment Companies: Pension Funds

Concerned with long run

Receive funds from working individuals

Finance companies

Finance companies raise funds by selling commercial paper and by

Finance companies

Finance companies raise funds by selling commercial paper and by

Investment Companies : Mutual Funds

A mutual fund accepts funds from investors

Investment Companies : Mutual Funds

A mutual fund accepts funds from investors

Страхование в банковском секторе. Проблемы и меры по усовершенствованию

Страхование в банковском секторе. Проблемы и меры по усовершенствованию Учет неопределенности и риска. Тема 10

Учет неопределенности и риска. Тема 10 Рынок акций

Рынок акций Финансовое право

Финансовое право Using Consumer Loans: The Role of Planned Borrowing

Using Consumer Loans: The Role of Planned Borrowing Анализ и оценка платежеспособности и финансовой устойчивости коммерческой организации

Анализ и оценка платежеспособности и финансовой устойчивости коммерческой организации Страховое публичное акционерное общество Ингосстрах

Страховое публичное акционерное общество Ингосстрах ЖСК - как способ реализации проекта строительства 3-х многоквартирных домов

ЖСК - как способ реализации проекта строительства 3-х многоквартирных домов Защита покупки. Группа АльфаСтрахование. АО ОТП Банк

Защита покупки. Группа АльфаСтрахование. АО ОТП Банк Суб’єкти та об’єкти біржової торгівлі. Біржові угоди

Суб’єкти та об’єкти біржової торгівлі. Біржові угоди Финансовая стратегия и тактика корпораций

Финансовая стратегия и тактика корпораций Оптимизация денежных потоков организации на примере ООО Вент-Сервис Гарант

Оптимизация денежных потоков организации на примере ООО Вент-Сервис Гарант Внедрение персонифицированного финансирования дополнительного образования детей в Вологодской области

Внедрение персонифицированного финансирования дополнительного образования детей в Вологодской области Основы девелопмента недвижимости

Основы девелопмента недвижимости Юридические вопросы, налоги и финансы. Субъекты малого предпринимательства: кто к ним относится в 2018 году

Юридические вопросы, налоги и финансы. Субъекты малого предпринимательства: кто к ним относится в 2018 году Прогнозирование денежных потоков предприятия по инвестиционной деятельности

Прогнозирование денежных потоков предприятия по инвестиционной деятельности Компьютеризация ведения бухгалтерского учета: проблемы и преимущества на примере ООО Управляющая Компания Уралгрит

Компьютеризация ведения бухгалтерского учета: проблемы и преимущества на примере ООО Управляющая Компания Уралгрит StockChain Business Case

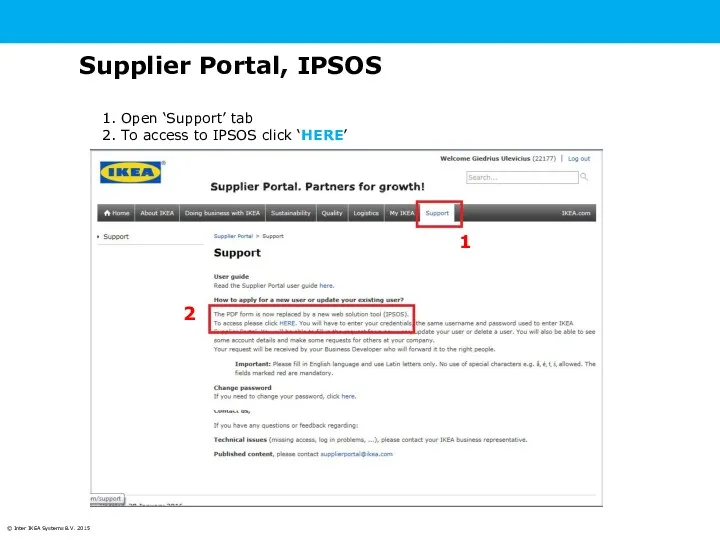

StockChain Business Case Ipsos for non-ru suppliers

Ipsos for non-ru suppliers Лизинг как метод финансирования инвестиционных проектов

Лизинг как метод финансирования инвестиционных проектов 20230320_modul_1.3._banki_i_zoloto_kak_sohranit_sberezheniya_v_dragotsennyh_metallah

20230320_modul_1.3._banki_i_zoloto_kak_sohranit_sberezheniya_v_dragotsennyh_metallah Анализ финансового состояния предприятия

Анализ финансового состояния предприятия Анализ роли криптовалют в современной экономике

Анализ роли криптовалют в современной экономике Зачем нужна страховка

Зачем нужна страховка Предложение способов пополнения счета

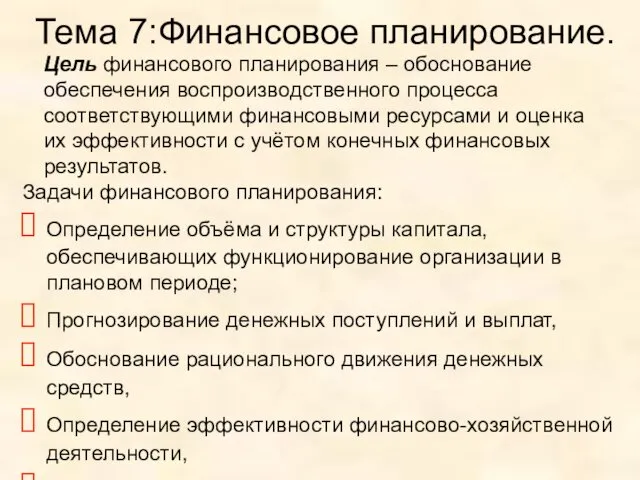

Предложение способов пополнения счета Финансовое планирование

Финансовое планирование Оффшорные зоны

Оффшорные зоны Облік, аналіз і аудит товарів на підприємстві роздрібної торгівлі

Облік, аналіз і аудит товарів на підприємстві роздрібної торгівлі