- Using Consumer Loans: The Role of Planned Borrowing

Содержание

- 2. Learning Objectives Understand the various consumer loans. Calculate the cost of a consumer loan. Pick an

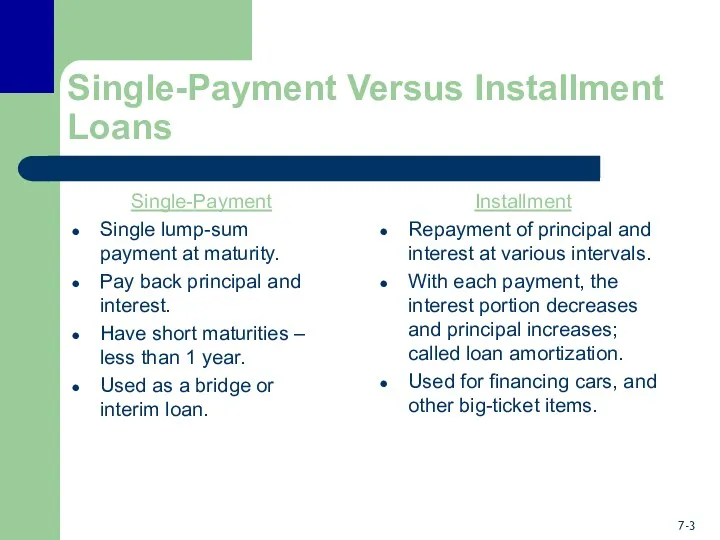

- 3. Single-Payment Versus Installment Loans Single-Payment Single lump-sum payment at maturity. Pay back principal and interest. Have

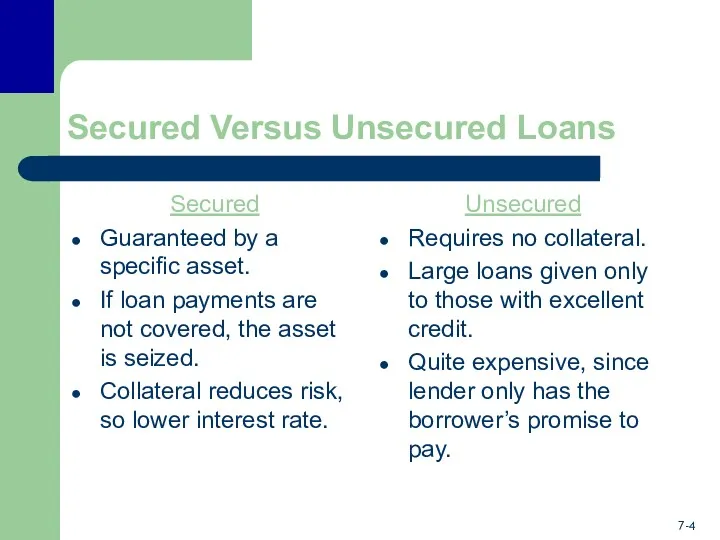

- 4. Secured Versus Unsecured Loans Secured Guaranteed by a specific asset. If loan payments are not covered,

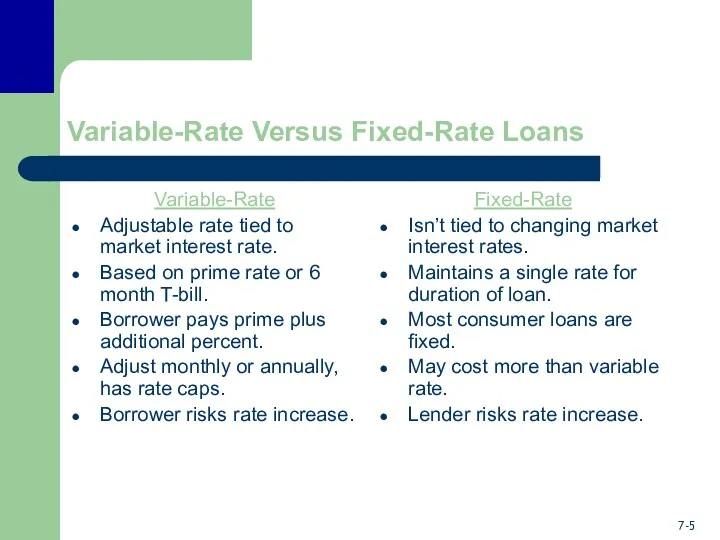

- 5. Variable-Rate Versus Fixed-Rate Loans Variable-Rate Adjustable rate tied to market interest rate. Based on prime rate

- 6. The Loan Contract Security agreement states if purchased item will be used as collateral. Note states

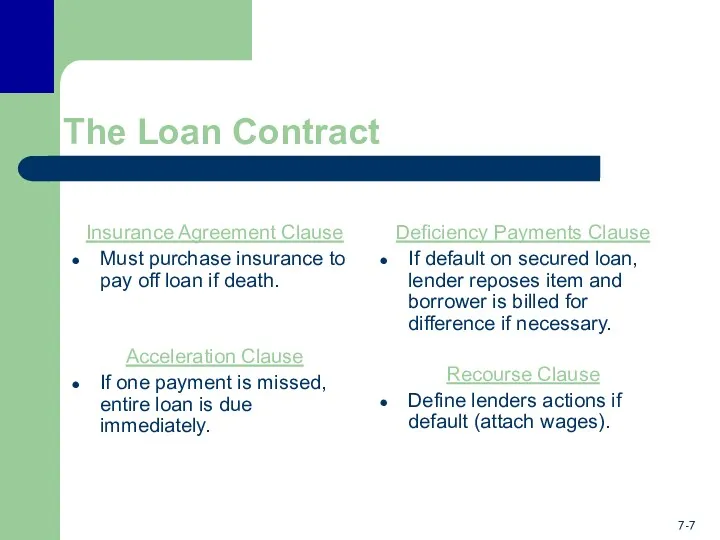

- 7. The Loan Contract Insurance Agreement Clause Must purchase insurance to pay off loan if death. Acceleration

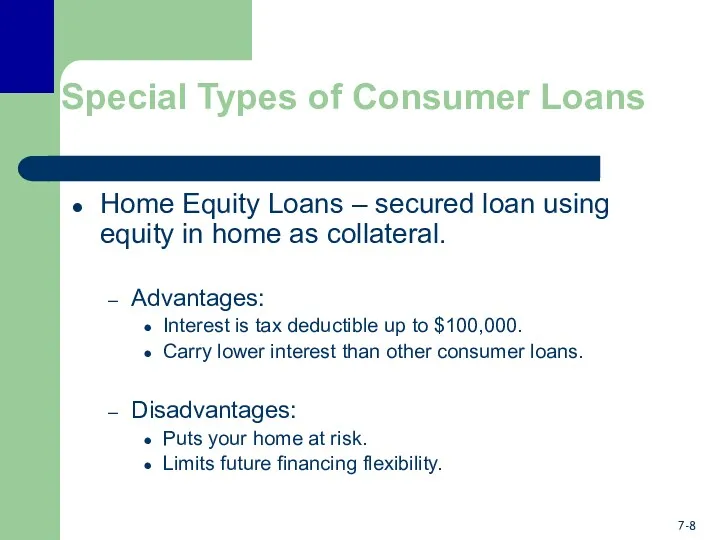

- 8. Special Types of Consumer Loans Home Equity Loans – secured loan using equity in home as

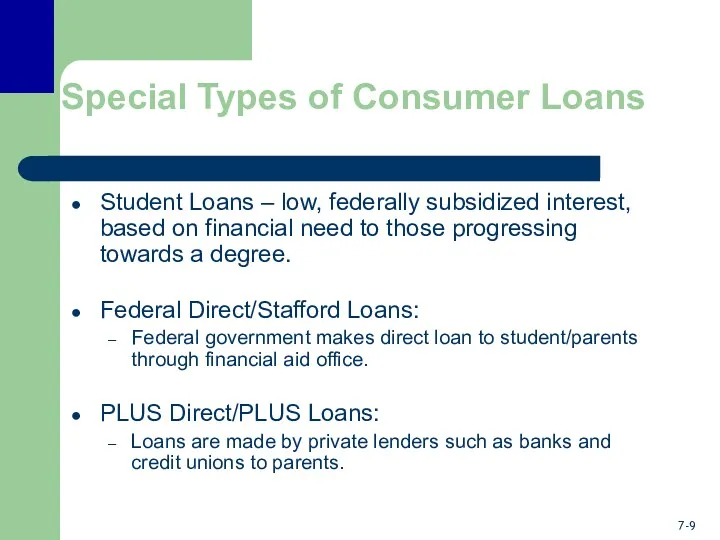

- 9. Special Types of Consumer Loans Student Loans – low, federally subsidized interest, based on financial need

- 10. Special Types of Consumer Loans Automobile Loans – loan secured by auto. Duration usually for 24,

- 11. Cost and Early Payment of Consumer Loans Truth in Lending Act requires written notification of total

- 12. Cost and Early Payment of Consumer Loans Finance charges include all costs associated with the loan:

- 13. Payday Loans Payday loans: Given by check cashing companies. Aimed at those who need money until

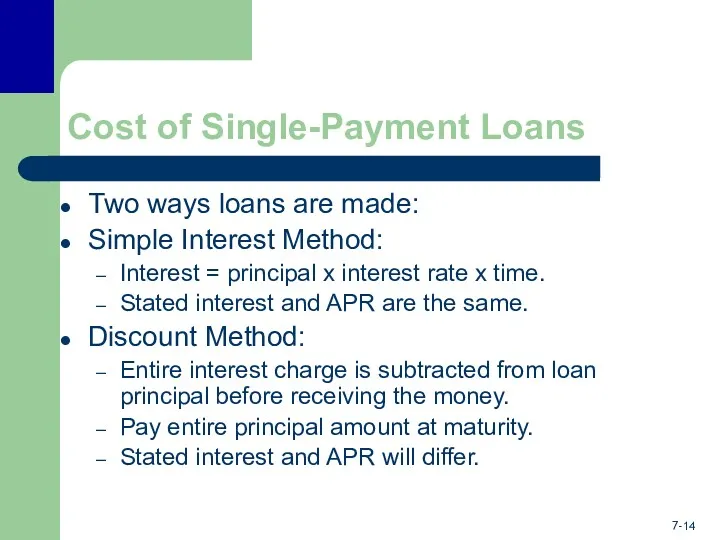

- 14. Cost of Single-Payment Loans Two ways loans are made: Simple Interest Method: Interest = principal x

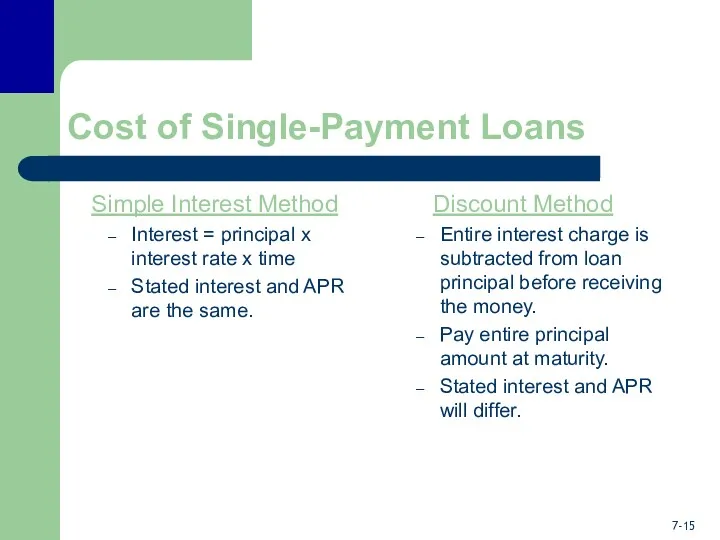

- 15. Cost of Single-Payment Loans Simple Interest Method Interest = principal x interest rate x time Stated

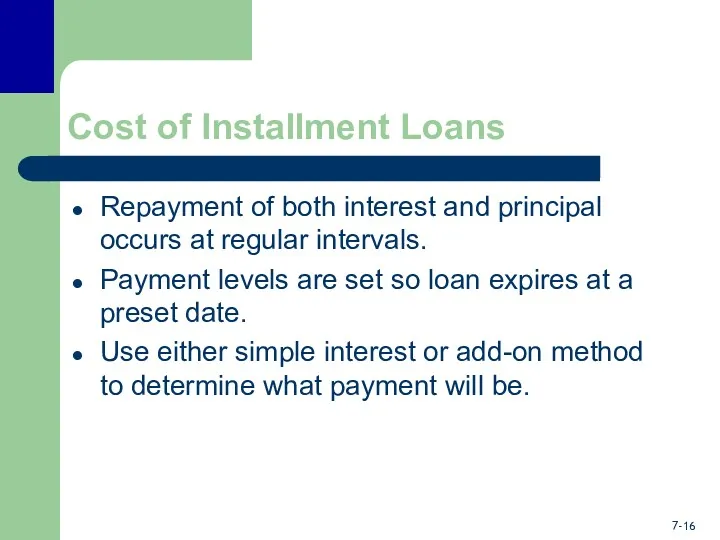

- 16. Cost of Installment Loans Repayment of both interest and principal occurs at regular intervals. Payment levels

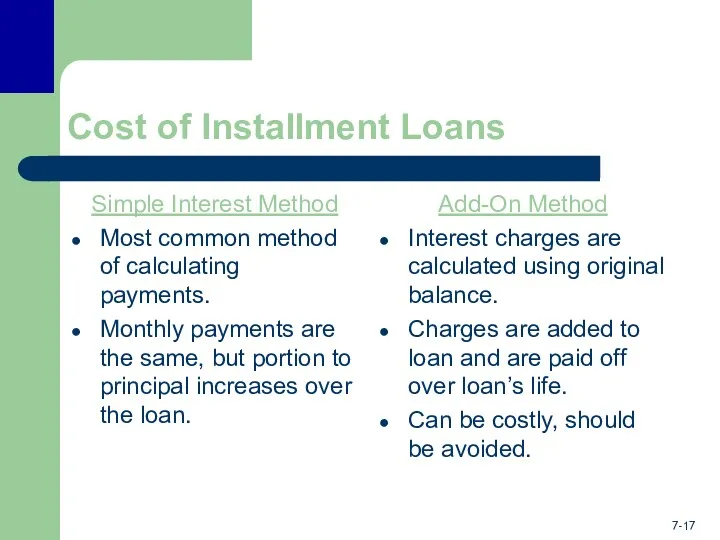

- 17. Cost of Installment Loans Simple Interest Method Most common method of calculating payments. Monthly payments are

- 18. Early Payment If installment loan is repaid early, determine amount of principal still owed. Most common

- 19. Relationship of Payment, Interest Rate, and Term of the Loan How does the duration of loan

- 20. Sources of Consumer Loans Inexpensive sources: The least expensive source of funds is your family. Home

- 21. Sources of Consumer Loans More Expensive Sources: Credit unions, S&L’s, and commercial banks. Exact cost depends

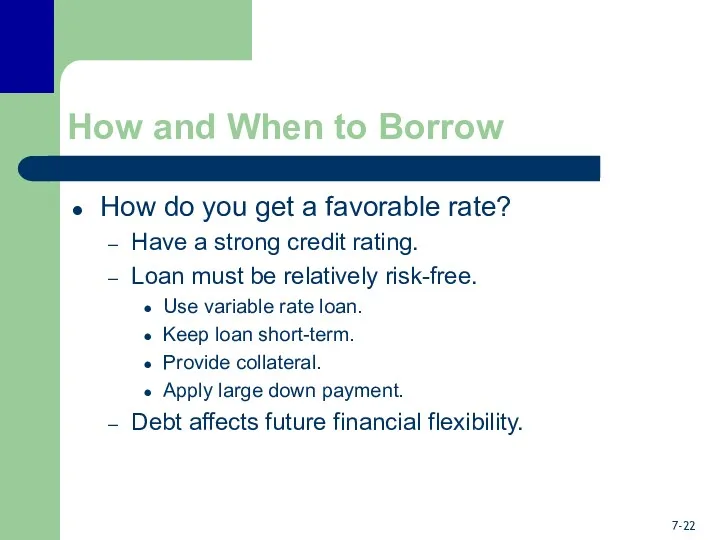

- 22. How and When to Borrow How do you get a favorable rate? Have a strong credit

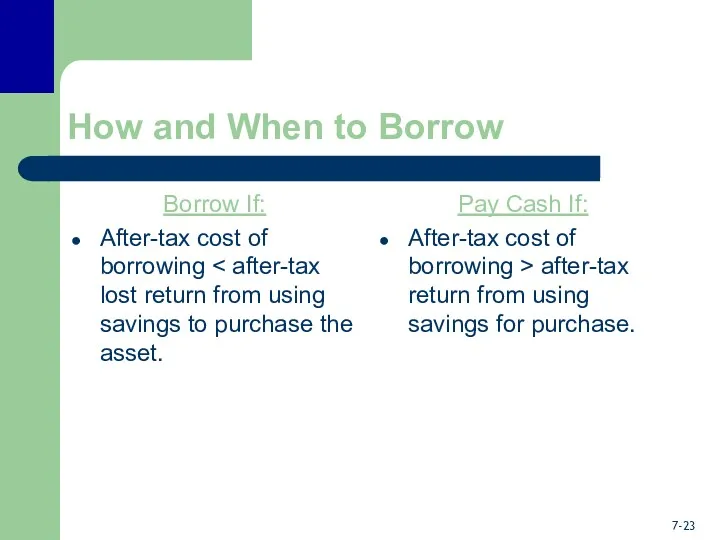

- 23. How and When to Borrow Borrow If: After-tax cost of borrowing Pay Cash If: After-tax cost

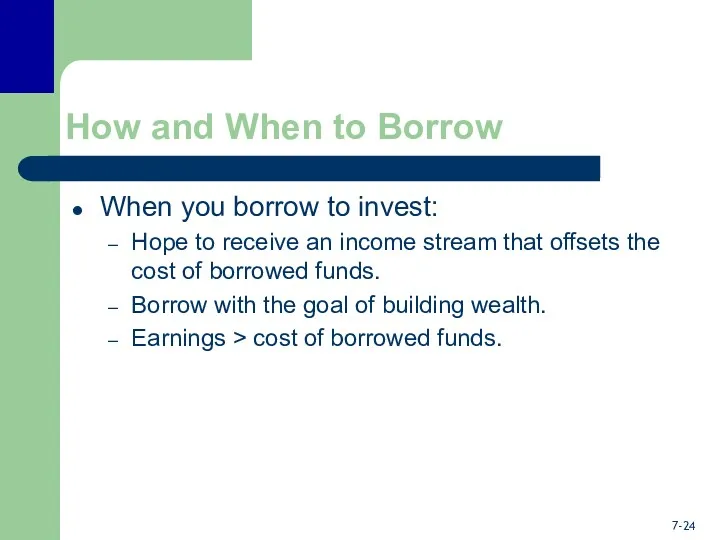

- 24. How and When to Borrow When you borrow to invest: Hope to receive an income stream

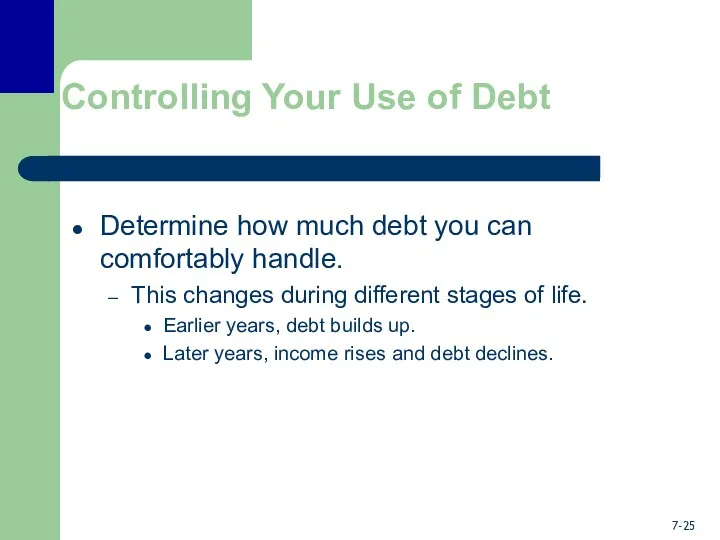

- 25. Controlling Your Use of Debt Determine how much debt you can comfortably handle. This changes during

- 26. Controlling Your Use of Debt Debt Limit Ratio measures the percentage of take-home pay committed to

- 27. Controlling Your Use of Debt 28/36 Rule A good credit risk when mortgage payments are below

- 28. Debt Resolution Rule Debt resolution rule helps control debt obligation, excluding borrowing for education and home

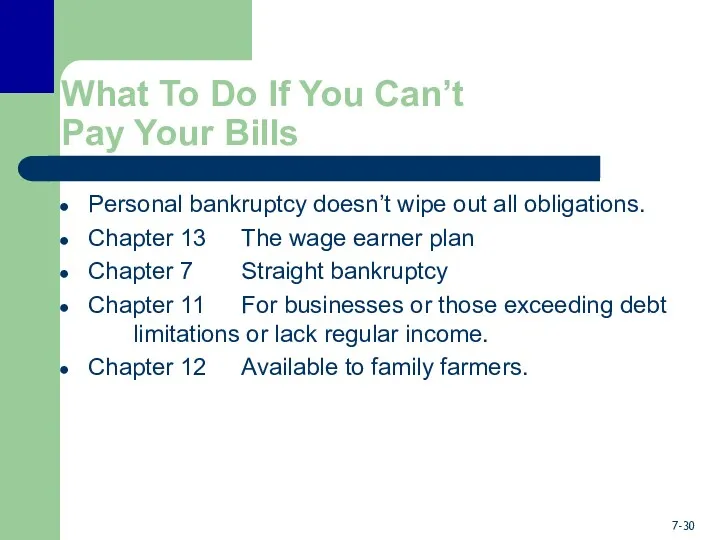

- 29. What To Do If You Can’t Pay Your Bills Go to creditors to get help resolving

- 30. What To Do If You Can’t Pay Your Bills Personal bankruptcy doesn’t wipe out all obligations.

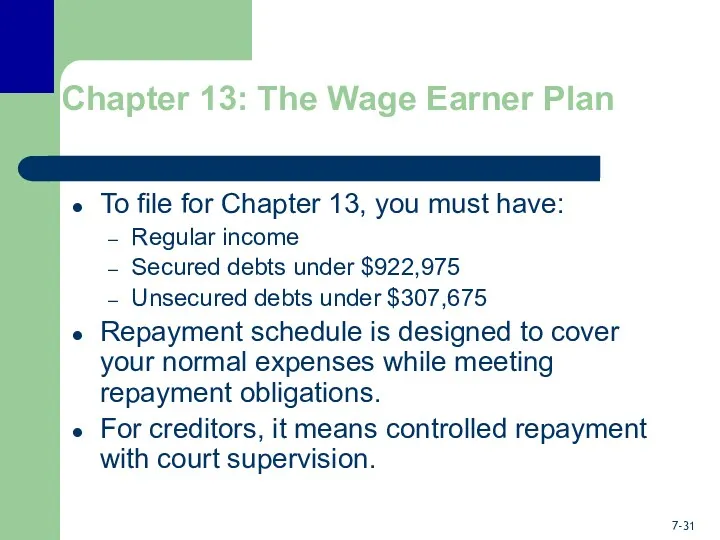

- 31. Chapter 13: The Wage Earner Plan To file for Chapter 13, you must have: Regular income

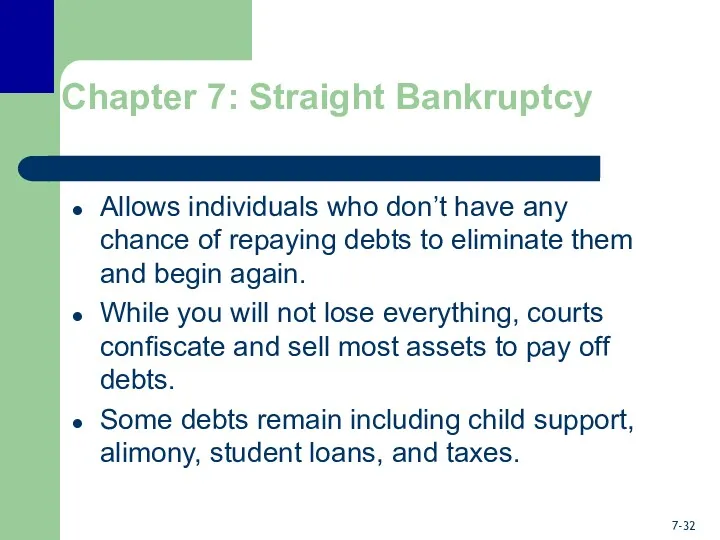

- 32. Chapter 7: Straight Bankruptcy Allows individuals who don’t have any chance of repaying debts to eliminate

- 34. Скачать презентацию

Learning Objectives

Understand the various consumer loans.

Calculate the cost of a consumer

Learning Objectives

Understand the various consumer loans.

Calculate the cost of a consumer

Single-Payment Versus Installment Loans

Single-Payment

Single lump-sum payment at maturity.

Pay back principal and

Single-Payment Versus Installment Loans

Single-Payment

Single lump-sum payment at maturity.

Pay back principal and

Secured Versus Unsecured Loans

Secured

Guaranteed by a specific asset.

If loan payments

Secured Versus Unsecured Loans

Secured

Guaranteed by a specific asset.

If loan payments

Variable-Rate Versus Fixed-Rate Loans

Variable-Rate

Adjustable rate tied to market interest rate.

Based on

Variable-Rate Versus Fixed-Rate Loans

Variable-Rate

Adjustable rate tied to market interest rate.

Based on

The Loan Contract

Security agreement states if purchased item will be used

The Loan Contract

Security agreement states if purchased item will be used

The Loan Contract

Insurance Agreement Clause

Must purchase insurance to pay off

The Loan Contract

Insurance Agreement Clause

Must purchase insurance to pay off

Special Types of Consumer Loans

Home Equity Loans – secured loan using

Special Types of Consumer Loans

Home Equity Loans – secured loan using

Special Types of Consumer Loans

Student Loans – low, federally subsidized interest,

Special Types of Consumer Loans

Student Loans – low, federally subsidized interest,

Special Types of Consumer Loans

Automobile Loans – loan secured by auto.

Special Types of Consumer Loans

Automobile Loans – loan secured by auto.

Cost and Early Payment of

Consumer Loans

Truth in Lending Act requires written

Cost and Early Payment of

Consumer Loans

Truth in Lending Act requires written

Cost and Early Payment of

Consumer Loans

Finance charges include all costs associated

Cost and Early Payment of

Consumer Loans

Finance charges include all costs associated

Payday Loans

Payday loans:

Given by check cashing companies.

Aimed at those who need

Payday Loans

Payday loans:

Given by check cashing companies.

Aimed at those who need

Cost of Single-Payment Loans

Two ways loans are made:

Simple Interest Method:

Interest =

Cost of Single-Payment Loans

Two ways loans are made:

Simple Interest Method:

Interest =

Cost of Single-Payment Loans

Simple Interest Method

Interest = principal x interest rate

Cost of Single-Payment Loans

Simple Interest Method

Interest = principal x interest rate

Cost of Installment Loans

Repayment of both interest and principal occurs at

Cost of Installment Loans

Repayment of both interest and principal occurs at

Cost of Installment Loans

Simple Interest Method

Most common method of calculating payments.

Monthly

Cost of Installment Loans

Simple Interest Method

Most common method of calculating payments.

Monthly

Early Payment

If installment loan is repaid early, determine amount of principal

Early Payment

If installment loan is repaid early, determine amount of principal

Relationship of Payment, Interest Rate, and Term of the Loan

How does

Relationship of Payment, Interest Rate, and Term of the Loan

How does

Sources of Consumer Loans

Inexpensive sources:

The least expensive source of funds is

Sources of Consumer Loans

Inexpensive sources:

The least expensive source of funds is

Sources of Consumer Loans

More Expensive Sources:

Credit unions, S&L’s, and commercial banks.

Exact

Sources of Consumer Loans

More Expensive Sources:

Credit unions, S&L’s, and commercial banks.

Exact

How and When to Borrow

How do you get a favorable rate?

Have

How and When to Borrow

How do you get a favorable rate?

Have

How and When to Borrow

Borrow If:

After-tax cost of borrowing < after-tax

How and When to Borrow

Borrow If:

After-tax cost of borrowing < after-tax

How and When to Borrow

When you borrow to invest:

Hope to receive

How and When to Borrow

When you borrow to invest:

Hope to receive

Controlling Your Use of Debt

Determine how much debt you can comfortably

Controlling Your Use of Debt

Determine how much debt you can comfortably

Controlling Your Use of Debt

Debt Limit Ratio measures the percentage of

Controlling Your Use of Debt

Debt Limit Ratio measures the percentage of

Controlling Your Use of Debt

28/36 Rule

A good credit risk when

Controlling Your Use of Debt

28/36 Rule

A good credit risk when

Debt Resolution Rule

Debt resolution rule helps control debt obligation, excluding borrowing

Debt Resolution Rule

Debt resolution rule helps control debt obligation, excluding borrowing

What To Do If You Can’t

Pay Your Bills

Go to creditors to

What To Do If You Can’t

Pay Your Bills

Go to creditors to

What To Do If You Can’t

Pay Your Bills

Personal bankruptcy doesn’t wipe

What To Do If You Can’t

Pay Your Bills

Personal bankruptcy doesn’t wipe

Chapter 13: The Wage Earner Plan

To file for Chapter 13, you

Chapter 13: The Wage Earner Plan

To file for Chapter 13, you

Chapter 7: Straight Bankruptcy

Allows individuals who don’t have any chance

Chapter 7: Straight Bankruptcy

Allows individuals who don’t have any chance

Основы бизнес-аналитики. Лекция 11. Сбалансированная система показателей

Основы бизнес-аналитики. Лекция 11. Сбалансированная система показателей Финансы, денежное обращение и кредит

Финансы, денежное обращение и кредит Бюджет для граждан города Курска

Бюджет для граждан города Курска Бизнес-планирование

Бизнес-планирование Місце фінансового ринку в фінансовій системі

Місце фінансового ринку в фінансовій системі Что такое банковская карта? Чем отличается дебетовая карта от кредитной?

Что такое банковская карта? Чем отличается дебетовая карта от кредитной? Единая форма Сведения для ведения индивидуального (персонифицированного) учета и сведения о начисленных страховых взносах

Единая форма Сведения для ведения индивидуального (персонифицированного) учета и сведения о начисленных страховых взносах Финансы и финансовая деятельность государства

Финансы и финансовая деятельность государства Самозанятость

Самозанятость Финансовая система Германии

Финансовая система Германии Финансовый анализ: анализ состояния предприятия; анализ доходов и финансовых результатов деятельности предприятия

Финансовый анализ: анализ состояния предприятия; анализ доходов и финансовых результатов деятельности предприятия 1С Документооборот 8

1С Документооборот 8 Понятие, предмет, метод, источники и система финансового права

Понятие, предмет, метод, источники и система финансового права Налоги как экономико-правовая категория

Налоги как экономико-правовая категория Довірчі (трастові) операції комерційних банків

Довірчі (трастові) операції комерційних банків Технология и специфика организации и проведения государственного и муниципального финансового контроля

Технология и специфика организации и проведения государственного и муниципального финансового контроля Зачем и как заниматься коммерциализацией результатов НИОКР в ВУЗе

Зачем и как заниматься коммерциализацией результатов НИОКР в ВУЗе Банки. Банковская система

Банки. Банковская система Международные валютно-финансовые отношения

Международные валютно-финансовые отношения Тема: Податки і податкове право в Україні

Тема: Податки і податкове право в Україні Методы калькулирования себестоимости в управленческом учете

Методы калькулирования себестоимости в управленческом учете Общие положения денежного содержания сотрудников МЧС России

Общие положения денежного содержания сотрудников МЧС России Особенности развития аудита в Великобритании

Особенности развития аудита в Великобритании Облигации. Сущность, классификация, инвестиционные характеристики

Облигации. Сущность, классификация, инвестиционные характеристики Физический износ: сущность, виды, особенности расчета

Физический износ: сущность, виды, особенности расчета Порядок составления, рассмотрения и утверждения проектов бюджетов

Порядок составления, рассмотрения и утверждения проектов бюджетов Materiālā atbildība

Materiālā atbildība Краудфандинг - система финансирования ваших проектов

Краудфандинг - система финансирования ваших проектов