- Fundamental legal principles

Содержание

- 2. Agenda Principle of Indemnity Principle of Insurable Interest Principle of Subrogation Principle of Utmost Good Faith

- 3. Principle of Indemnity The insurer agrees to pay no more than the actual amount of the

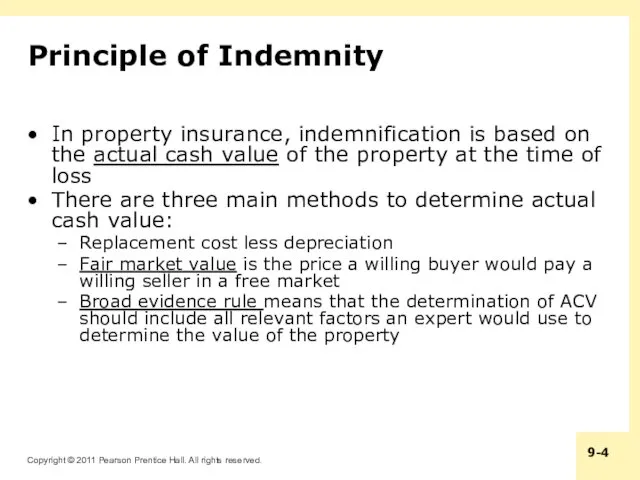

- 4. Principle of Indemnity In property insurance, indemnification is based on the actual cash value of the

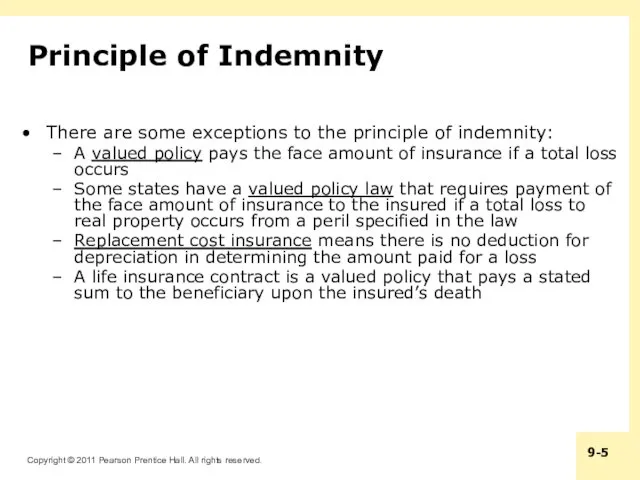

- 5. Principle of Indemnity There are some exceptions to the principle of indemnity: A valued policy pays

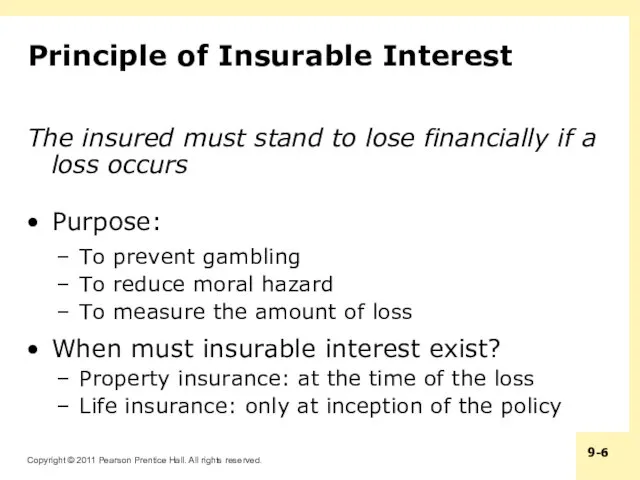

- 6. Principle of Insurable Interest The insured must stand to lose financially if a loss occurs Purpose:

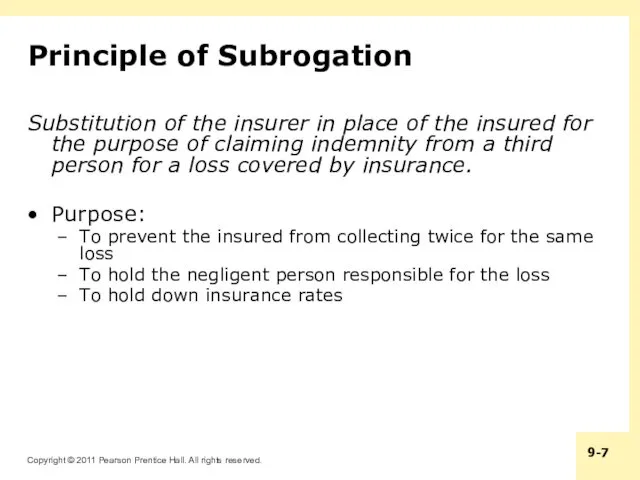

- 7. Principle of Subrogation Substitution of the insurer in place of the insured for the purpose of

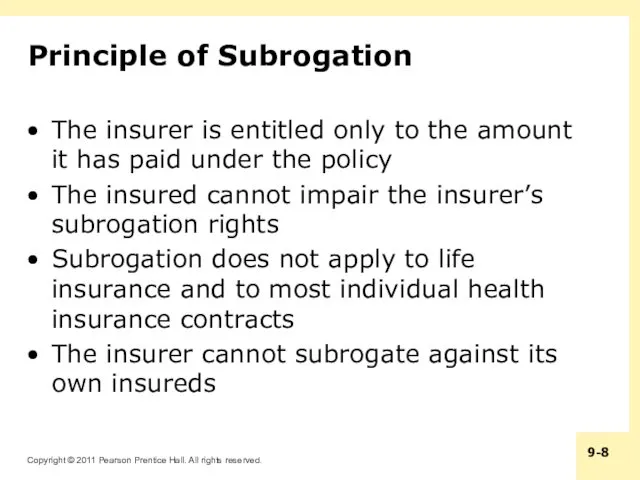

- 8. Principle of Subrogation The insurer is entitled only to the amount it has paid under the

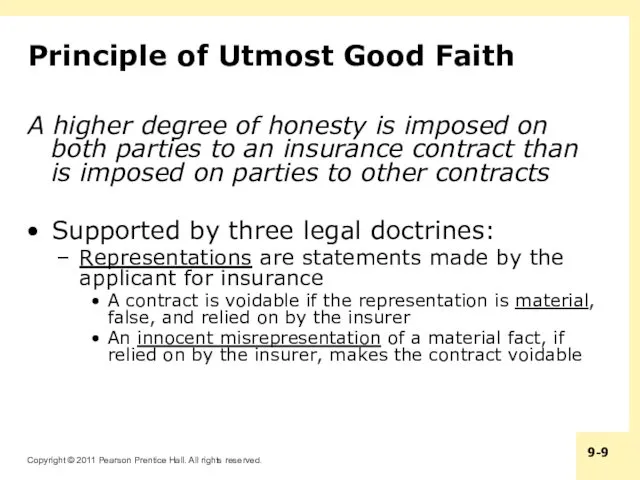

- 9. Principle of Utmost Good Faith A higher degree of honesty is imposed on both parties to

- 10. Principle of Utmost Good Faith A concealment is intentional failure of the applicant for insurance to

- 11. Requirements of an Insurance Contract To be legally enforceable, an insurance contract must meet four requirements:

- 12. Distinct Legal Characteristics of Insurance Contracts Aleatory: values exchanged are not equal Unilateral: only the insurer

- 13. Law and the Insurance Agent An agent is someone who has the authority to act on

- 15. Скачать презентацию

Agenda

Principle of Indemnity

Principle of Insurable Interest

Principle of Subrogation

Principle of Utmost Good

Agenda

Principle of Indemnity

Principle of Insurable Interest

Principle of Subrogation

Principle of Utmost Good

Principle of Indemnity

The insurer agrees to pay no more than the

Principle of Indemnity

The insurer agrees to pay no more than the

Principle of Indemnity

In property insurance, indemnification is based on the actual

Principle of Indemnity

In property insurance, indemnification is based on the actual

Principle of Indemnity

There are some exceptions to the principle of indemnity:

A

Principle of Indemnity

There are some exceptions to the principle of indemnity:

A

Principle of Insurable Interest

The insured must stand to lose financially if

Principle of Insurable Interest

The insured must stand to lose financially if

Principle of Subrogation

Substitution of the insurer in place of the insured

Principle of Subrogation

Substitution of the insurer in place of the insured

Principle of Subrogation

The insurer is entitled only to the amount it

Principle of Subrogation

The insurer is entitled only to the amount it

Principle of Utmost Good Faith

A higher degree of honesty is imposed

Principle of Utmost Good Faith

A higher degree of honesty is imposed

Principle of Utmost Good Faith

A concealment is intentional failure of the

Principle of Utmost Good Faith

A concealment is intentional failure of the

Requirements of an Insurance Contract

To be legally enforceable, an insurance contract

Requirements of an Insurance Contract

To be legally enforceable, an insurance contract

Distinct Legal Characteristics of Insurance Contracts

Aleatory: values exchanged are not equal

Unilateral:

Distinct Legal Characteristics of Insurance Contracts

Aleatory: values exchanged are not equal

Unilateral:

Law and the Insurance Agent

An agent is someone who has the

Law and the Insurance Agent

An agent is someone who has the

Семейный бюджет

Семейный бюджет Бухгалтерлік Баланс

Бухгалтерлік Баланс Стальфонд. Работа финансового консультанта

Стальфонд. Работа финансового консультанта Экономическая оценка инвестиций

Экономическая оценка инвестиций Валюты мира

Валюты мира SME – Small &Medium Enterprise

SME – Small &Medium Enterprise Подготовка к взрослой жизни. Повышение финансовой грамотности

Подготовка к взрослой жизни. Повышение финансовой грамотности Порядок формирования цен в общественном питании

Порядок формирования цен в общественном питании Управление основными элементами оборотных активов

Управление основными элементами оборотных активов Правовое регулирование личного страхования

Правовое регулирование личного страхования Процедуры в деле о банкротстве. (Лекция №1)

Процедуры в деле о банкротстве. (Лекция №1) Оценка недвижимости. Задачник для подготовки к экзамену

Оценка недвижимости. Задачник для подготовки к экзамену Отбор социальных некоммерческих организаций для предоставления субсидий из бюджета республики Карелия

Отбор социальных некоммерческих организаций для предоставления субсидий из бюджета республики Карелия Формы и виды лизинга

Формы и виды лизинга Финансовая устойчивость коммерческого банка

Финансовая устойчивость коммерческого банка Термины страхования

Термины страхования Самые важные и срочные изменения в работе бухгалтера. Отчетность по новым правилам 2023

Самые важные и срочные изменения в работе бухгалтера. Отчетность по новым правилам 2023 Деньги Кыргызстана

Деньги Кыргызстана Бюджет государства и семьи

Бюджет государства и семьи Analiza 10 kriptomenjalnic

Analiza 10 kriptomenjalnic Законодательное и нормативное регулирование бухгалтерского учета и отчетности в РФ

Законодательное и нормативное регулирование бухгалтерского учета и отчетности в РФ Оплата труда, гарантийные и компенсационные выплаты

Оплата труда, гарантийные и компенсационные выплаты Социальная помощь. Распределение доходов

Социальная помощь. Распределение доходов Рынок ценных бумаг

Рынок ценных бумаг Методы определения рыночной стоимости земельных угодий

Методы определения рыночной стоимости земельных угодий Практическое занятие Лизинг. Расчет лизинговых платежей

Практическое занятие Лизинг. Расчет лизинговых платежей Анализ и оценка финансовых результатов деятельности предприятия

Анализ и оценка финансовых результатов деятельности предприятия Фінансові посередники. Сутність фінансових посередників та їх функції. Суб'єкти банківської системи. (Тема 3)

Фінансові посередники. Сутність фінансових посередників та їх функції. Суб'єкти банківської системи. (Тема 3)