- Introduction to Financial Statement Analysis. Chapter 2

Содержание

- 2. Introduction to this Chapter We will learn some bases of a firm’s financial statements We’ll then

- 3. Motivation: Why This Chapter? Some of you may find this chapter a bit ‘dry’ or ‘too

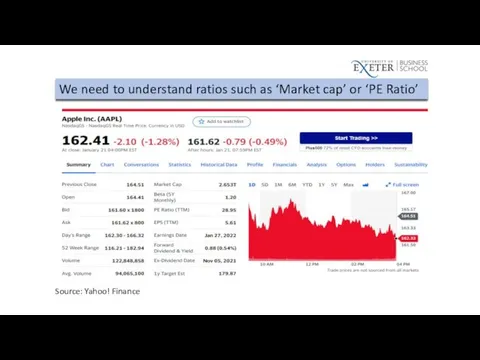

- 4. We need to understand ratios such as ‘Market cap’ or ‘PE Ratio’ Source: Yahoo! Finance

- 5. Why This Chapter? Another Reason: good for your CFA exam Contents discussed in this chapter are

- 6. Chapter Outline 2.1 Firms’ Disclosure of Financial Information 2.2 The Balance Sheet 2.3 The Income Statement

- 7. Learning Objectives List the four major financial statements required by the SEC for publicly traded firms,

- 8. Learning Objectives Discuss the uses of the DuPont identity in disaggregating ROE, and assess the impact

- 9. 2.1 Firms’ Disclosure of Financial Information

- 10. Financial Statements Firm-issued accounting reports with past performance information Filed with the SEC (U.S. Securities and

- 11. Apple Inc. Financial Statements Link: https://investor.apple.com/investor-relations/default.aspx

- 12. Preparation of Financial Statements Generally Accepted Accounting Principles (GAAP) A common set of rules and standard

- 13. Preparation of Financial Statements Auditor Neutral third party that checks a firm’s financial statements Four leading

- 14. Optional Reading on Auditing Market and Regulation https://www.ft.com/content/96d4b090-f973-11e9-a354-36acbbb0d9b6 https://www.ft.com/content/7ad4d113-0c33-44b2-b4e4-ede47f334505 https://www.ft.com/content/d5103236-2799-4eab-bb71-afad7b703ae4 https://www.ft.com/content/4219750e-612a-11e9-a27a-fdd51850994c https://www.theguardian.com/business/2004/dec/17/europeanunion

- 15. Types of Financial Statements Balance Sheet Income Statement Statement of Cash Flows Statement of Stockholders’ Equity

- 16. Stock vs Flow A stock is measured at a specific time, and represents a quantity existing

- 17. 2.2 Balance Sheet

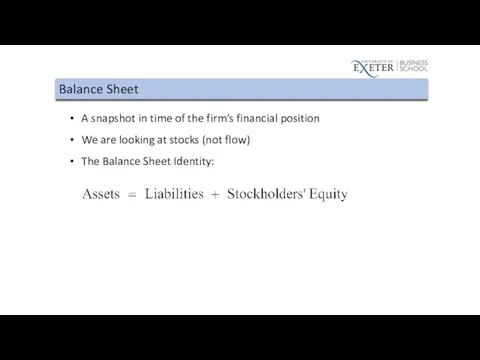

- 18. Balance Sheet A snapshot in time of the firm’s financial position We are looking at stocks

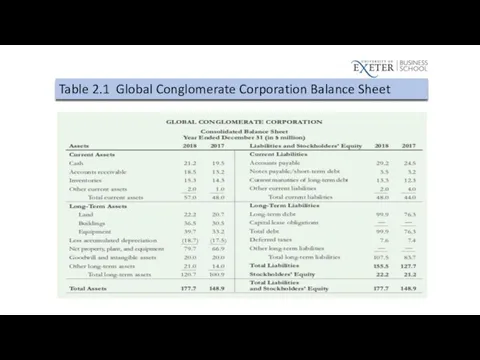

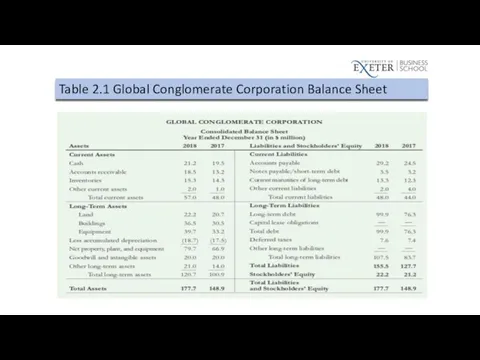

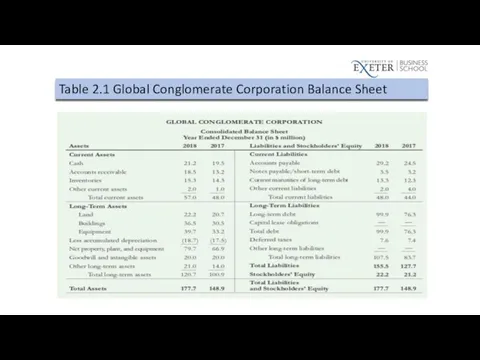

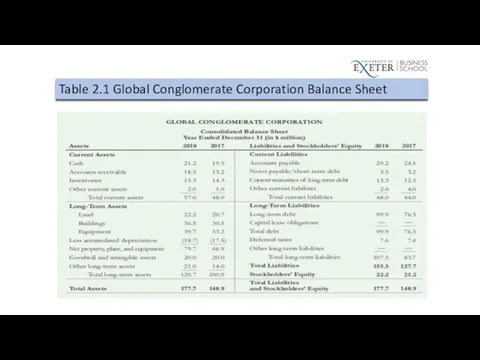

- 19. Table 2.1 Global Conglomerate Corporation Balance Sheet

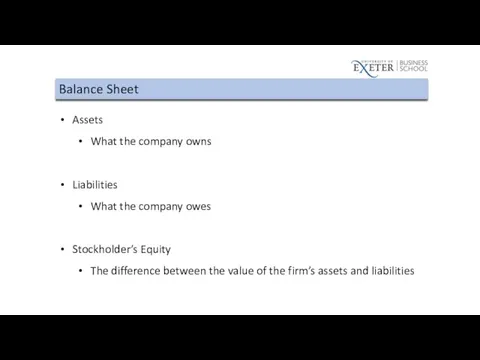

- 20. Balance Sheet Assets What the company owns Liabilities What the company owes Stockholder’s Equity The difference

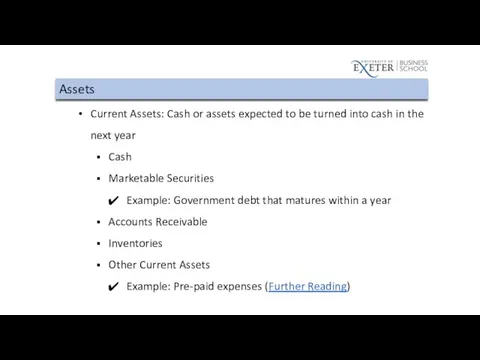

- 21. Assets Current Assets: Cash or assets expected to be turned into cash in the next year

- 22. Assets Long-Term Assets Net Property, Plant, & Equipment Depreciation (and Accumulated Depreciation) Notice that you don’t

- 23. Liabilities Current Liabilities: Due to be paid within the next year Accounts Payable Short-Term Debt/Notes Payable

- 24. Liabilities Long-Term Liabilities Long-Term Debt Capital Leases Deferred Taxes

- 25. Table 2.1 Global Conglomerate Corporation Balance Sheet

- 26. Stockholder’s Equity: Market Value Versus Book Value

- 27. Market-to-Book Ratio Also called Price-to-Book Ratio Value Stocks Low M/B ratios Growth Stocks High M/B ratios

- 28. Enterprise Value Market Capitalization measures the market value of equity What is the market value of

- 29. Textbook Example 2.1

- 30. Textbook Example 2.1

- 31. 2.3 Income Statement

- 32. Income Statement Income statement lists the firm’s revenues and expenses over a period of time So

- 33. Income Statement Reminder: net income is accounting profit (not change of cash) Net income is generally

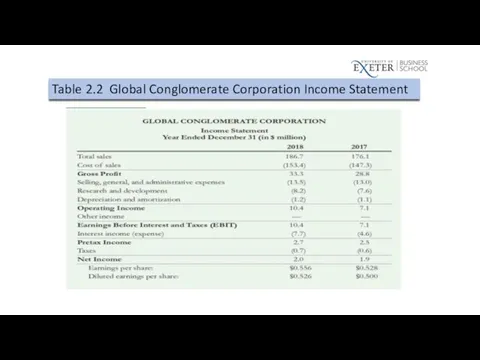

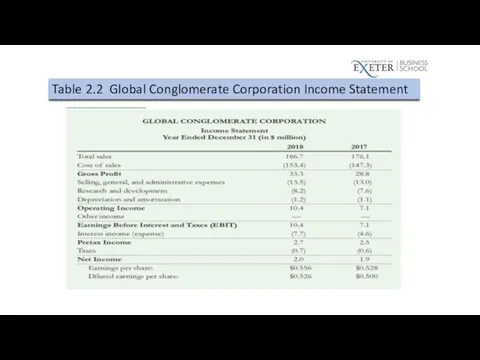

- 34. Table 2.2 Global Conglomerate Corporation Income Statement

- 35. Example: Apple Inc. Apple’s 2021 Income Statement From its 2021 10-K Annual Report (Page 32) Link:

- 36. Income Statement

- 37. Complete Formula

- 38. Complete Formula of Net Income

- 39. What can Net Income be used for?

- 40. Income Statement

- 41. 2.4 Statement of Cash Flows

- 42. Statement of Cash Flows Net Income typically does NOT equal the amount of cash the firm

- 43. Statement of Cash Flows The difference between net income and cash flow may also come from:

- 44. Statement of Cash Flows: Three Sections Operating Activity Investment Activity Financing Activity

- 45. Operating Activity Adjusts net income by all non-cash items related to operating activities and changes in

- 46. Cash from Operating Activities

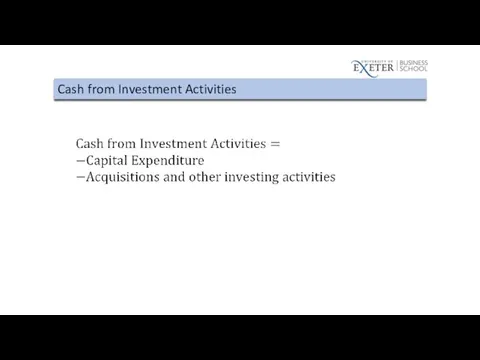

- 47. Investment Activity and Financing Activity Investment Activity Capital Expenditures Buying or Selling Marketable Securities Financing Activity

- 48. Cash from Investment Activities

- 49. Cash from Financing Activities

- 50. Change in cash and cash equivalents

- 51. Another way to calculate change in cash

- 52. Change in cash and cash equivalents

- 53. Table 2.3 Global Conglomerate Corporation Statement of Cash Flows

- 54. Table 2.1 Global Conglomerate Corporation Balance Sheet

- 55. 2.5 Other Financial Statement Information

- 56. Statement of Stockholders’ Equity

- 57. Other Financial Statement Information Management Discussion and Analysis Off-Balance Sheet Transactions Notes to the Financial Statements

- 58. Textbook Example 2.3

- 59. Textbook Example 2.3

- 60. 2.6 Financial Statement Analysis

- 61. Financial Statement Analysis Financial Statement Analysis can be used Compare the firm with itself over time

- 62. Types of Ratios Profitability Ratios Liquidity Ratios Working Capital Ratios Interest Coverage Ratios Leverage Ratios Valuation

- 63. Profitability Ratios

- 64. Figure 2.1 EBIT Margins for Five U.S. Airlines Source: Capital IQ

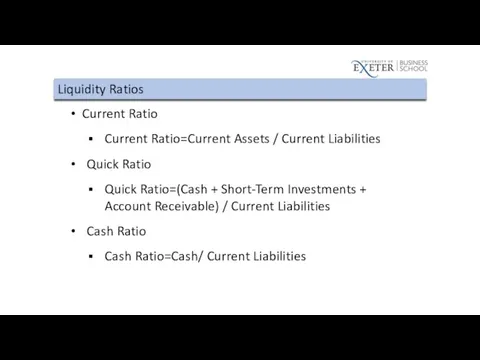

- 65. Liquidity Ratios Current Ratio Current Ratio=Current Assets / Current Liabilities Quick Ratio Quick Ratio=(Cash + Short-Term

- 66. Textbook Example 2.4

- 67. Table 2.1 Global Conglomerate Corporation Balance Sheet

- 68. Textbook Example 2.4

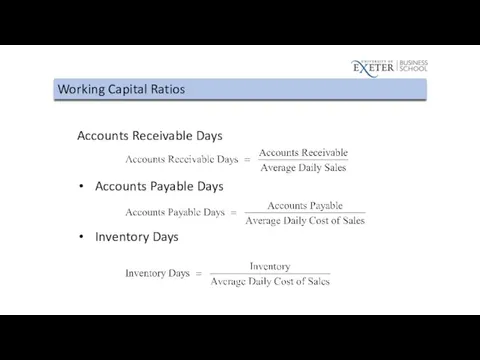

- 69. Working Capital Ratios Accounts Receivable Days Accounts Payable Days Inventory Days

- 70. Working Capital Ratios Accounts Receivable Turnover Accounts Payable Turnover Inventory Turnover

- 71. Interest Coverage Ratios EBIT/Interest EBITDA/Interest EBITDA = EBIT + Depreciation and Amortization

- 72. Textbook Example 2.5

- 73. Table 2.1 Global Conglomerate Corporation Balance Sheet

- 74. Table 2.2 Global Conglomerate Corporation Income Statement

- 75. Textbook Example 2.5

- 76. Leverage Ratios Debt-Equity Ratio Debt-to-Capital Ratio

- 77. Table 2.1 Global Conglomerate Corporation Balance Sheet

- 78. Leverage Ratios Net Debt Total Debt - Excess Cash & Short-Term Investments Debt-to-Enterprise Value Equity Multiplier

- 79. Valuation Ratios P/E Ratio Enterprise Value to EBIT Enterprise Value to Sales

- 80. Valuation Ratios

- 81. Textbook Example 2.6

- 82. Textbook Example 2.6

- 83. Operating Returns Return on Equity Return on Assets Return on Invested Capital

- 84. Textbook Example 2.7

- 85. Table 2.2 Global Conglomerate Corporation Income Statement

- 86. Textbook Example 2.7

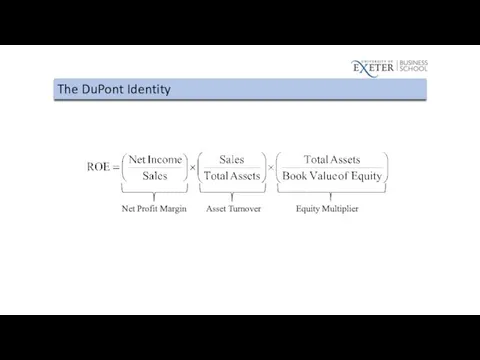

- 87. The DuPont Identity

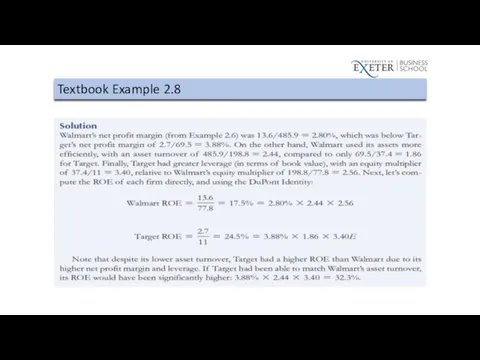

- 88. Textbook Example 2.8

- 89. Textbook Example 2.8

- 90. Table 2.4 Key Financial Ratios for Large U.S. Firms, Spring 2018

- 91. 2.7 (Optional) Financial Reporting in Practice

- 92. (Optional) Financial Reporting in Practice Even with safeguards, reporting abuses still happen: Enron WorldCom Sarbanes-Oxley Act

- 94. Скачать презентацию

Introduction to this Chapter

We will learn some bases of a firm’s

Introduction to this Chapter

We will learn some bases of a firm’s

Motivation: Why This Chapter?

Some of you may find this chapter a

Motivation: Why This Chapter?

Some of you may find this chapter a

We need to understand ratios such as ‘Market cap’ or ‘PE

We need to understand ratios such as ‘Market cap’ or ‘PE

Why This Chapter?

Another Reason: good for your CFA exam

Contents discussed in

Why This Chapter?

Another Reason: good for your CFA exam

Contents discussed in

Chapter Outline

2.1 Firms’ Disclosure of Financial Information

2.2 The Balance Sheet

Chapter Outline

2.1 Firms’ Disclosure of Financial Information

2.2 The Balance Sheet

Learning Objectives

List the four major financial statements required by the SEC

Learning Objectives

List the four major financial statements required by the SEC

Learning Objectives

Discuss the uses of the DuPont identity in disaggregating ROE,

Learning Objectives

Discuss the uses of the DuPont identity in disaggregating ROE,

2.1

Firms’ Disclosure of Financial Information

2.1

Firms’ Disclosure of Financial Information

Financial Statements

Firm-issued accounting reports with past performance information

Filed with the SEC

Financial Statements

Firm-issued accounting reports with past performance information

Filed with the SEC

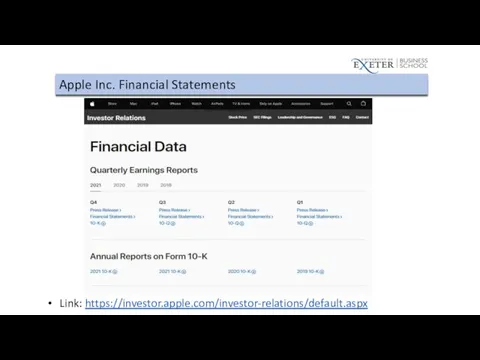

Apple Inc. Financial Statements

Link: https://investor.apple.com/investor-relations/default.aspx

Apple Inc. Financial Statements

Link: https://investor.apple.com/investor-relations/default.aspx

Preparation of Financial Statements

Generally Accepted Accounting Principles (GAAP)

A common set of

Preparation of Financial Statements

Generally Accepted Accounting Principles (GAAP)

A common set of

Preparation of Financial Statements

Auditor

Neutral third party that checks a firm’s financial

Preparation of Financial Statements

Auditor

Neutral third party that checks a firm’s financial

Optional Reading on Auditing Market and Regulation

https://www.ft.com/content/96d4b090-f973-11e9-a354-36acbbb0d9b6

https://www.ft.com/content/7ad4d113-0c33-44b2-b4e4-ede47f334505

https://www.ft.com/content/d5103236-2799-4eab-bb71-afad7b703ae4

https://www.ft.com/content/4219750e-612a-11e9-a27a-fdd51850994c

https://www.theguardian.com/business/2004/dec/17/europeanunion

Optional Reading on Auditing Market and Regulation

https://www.ft.com/content/96d4b090-f973-11e9-a354-36acbbb0d9b6

https://www.ft.com/content/7ad4d113-0c33-44b2-b4e4-ede47f334505

https://www.ft.com/content/d5103236-2799-4eab-bb71-afad7b703ae4

https://www.ft.com/content/4219750e-612a-11e9-a27a-fdd51850994c

https://www.theguardian.com/business/2004/dec/17/europeanunion

Types of Financial Statements

Balance Sheet

Income Statement

Statement of Cash Flows

Statement of Stockholders’

Types of Financial Statements

Balance Sheet

Income Statement

Statement of Cash Flows

Statement of Stockholders’

Stock vs Flow

A stock is measured at a specific time, and

Stock vs Flow

A stock is measured at a specific time, and

2.2

Balance Sheet

2.2

Balance Sheet

Balance Sheet

A snapshot in time of the firm’s financial position

We are

Balance Sheet

A snapshot in time of the firm’s financial position

We are

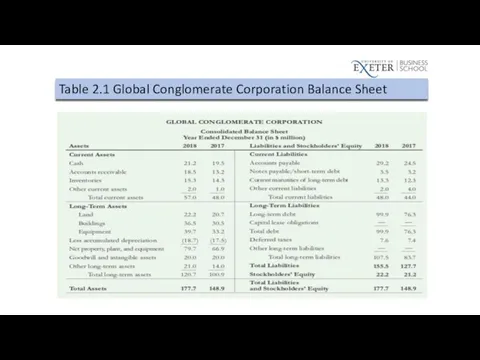

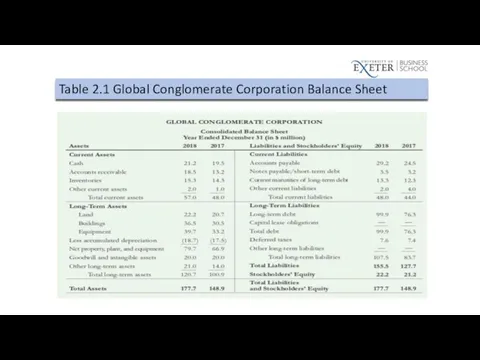

Table 2.1 Global Conglomerate Corporation Balance Sheet

Table 2.1 Global Conglomerate Corporation Balance Sheet

Balance Sheet

Assets

What the company owns

Liabilities

What the company owes

Stockholder’s Equity

The difference between

Balance Sheet

Assets

What the company owns

Liabilities

What the company owes

Stockholder’s Equity

The difference between

Assets

Current Assets: Cash or assets expected to be turned into cash

Assets

Current Assets: Cash or assets expected to be turned into cash

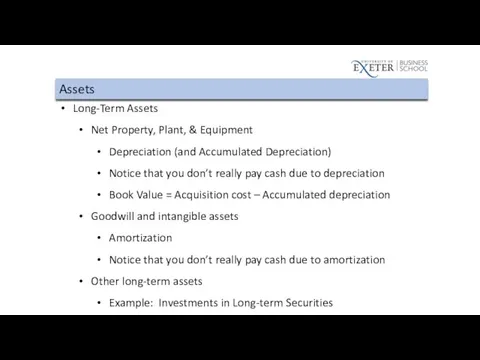

Assets

Long-Term Assets

Net Property, Plant, & Equipment

Depreciation (and Accumulated Depreciation)

Notice that you

Assets

Long-Term Assets

Net Property, Plant, & Equipment

Depreciation (and Accumulated Depreciation)

Notice that you

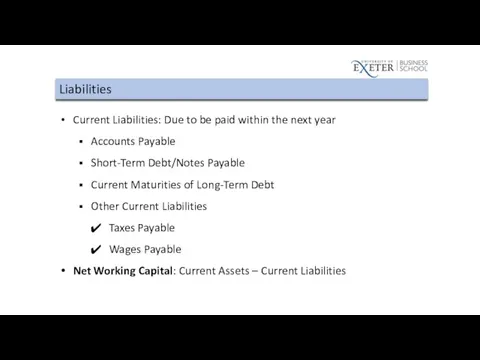

Liabilities

Current Liabilities: Due to be paid within the next year

Accounts Payable

Short-Term

Liabilities

Current Liabilities: Due to be paid within the next year

Accounts Payable

Short-Term

Liabilities

Long-Term Liabilities

Long-Term Debt

Capital Leases

Deferred Taxes

Liabilities

Long-Term Liabilities

Long-Term Debt

Capital Leases

Deferred Taxes

Table 2.1 Global Conglomerate Corporation Balance Sheet

Table 2.1 Global Conglomerate Corporation Balance Sheet

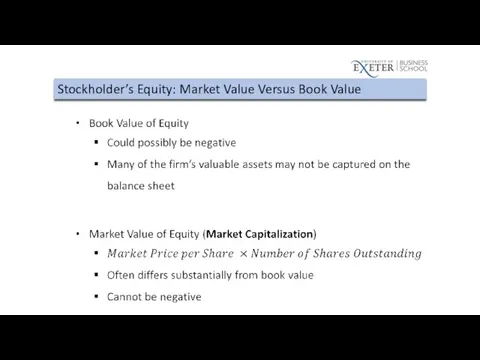

Stockholder’s Equity: Market Value Versus Book Value

Stockholder’s Equity: Market Value Versus Book Value

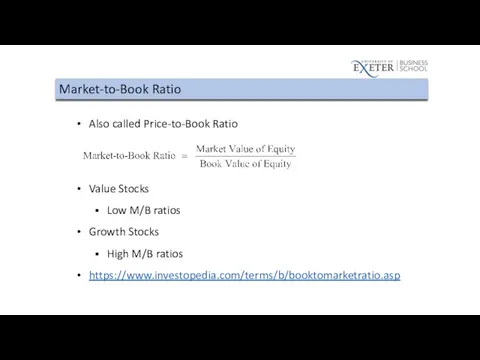

Market-to-Book Ratio

Also called Price-to-Book Ratio

Value Stocks

Low M/B ratios

Growth Stocks

High M/B

Market-to-Book Ratio

Also called Price-to-Book Ratio

Value Stocks

Low M/B ratios

Growth Stocks

High M/B

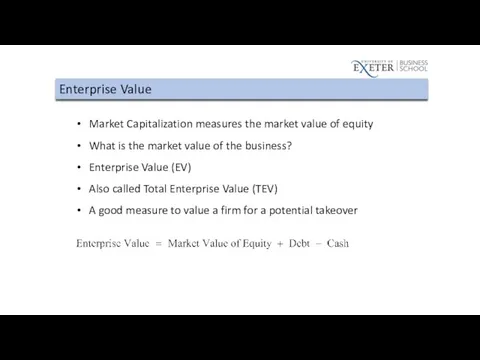

Enterprise Value

Market Capitalization measures the market value of equity

What is the

Enterprise Value

Market Capitalization measures the market value of equity

What is the

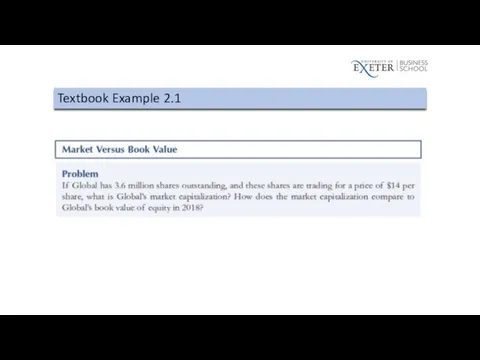

Textbook Example 2.1

Textbook Example 2.1

Textbook Example 2.1

Textbook Example 2.1

2.3

Income Statement

2.3

Income Statement

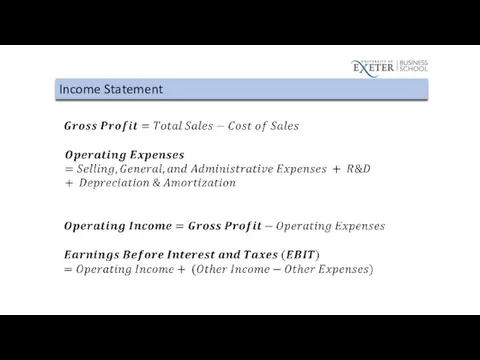

Income Statement

Income statement lists the firm’s revenues and expenses over a

Income Statement

Income statement lists the firm’s revenues and expenses over a

Income Statement

Reminder: net income is accounting profit (not change of cash)

Net

Income Statement

Reminder: net income is accounting profit (not change of cash)

Net

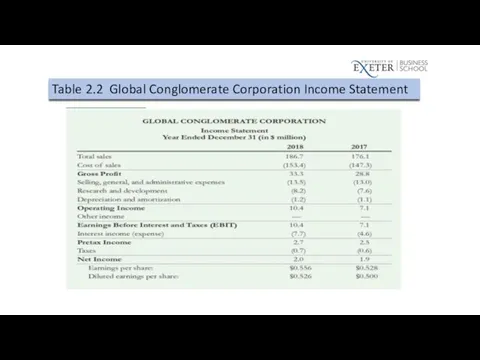

Table 2.2 Global Conglomerate Corporation Income Statement

Table 2.2 Global Conglomerate Corporation Income Statement

Example: Apple Inc.

Apple’s 2021 Income Statement

From its 2021 10-K Annual Report

Example: Apple Inc.

Apple’s 2021 Income Statement

From its 2021 10-K Annual Report

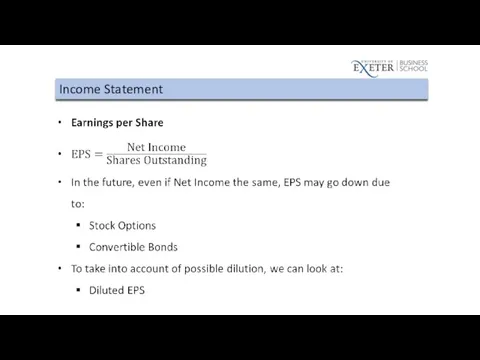

Income Statement

Income Statement

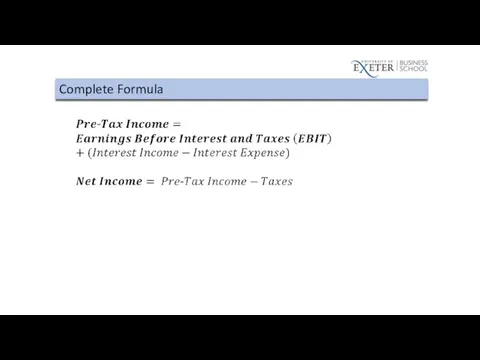

Complete Formula

Complete Formula

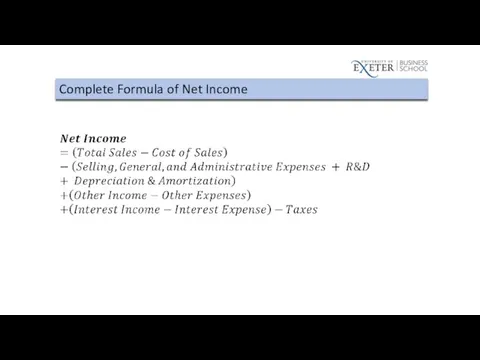

Complete Formula of Net Income

Complete Formula of Net Income

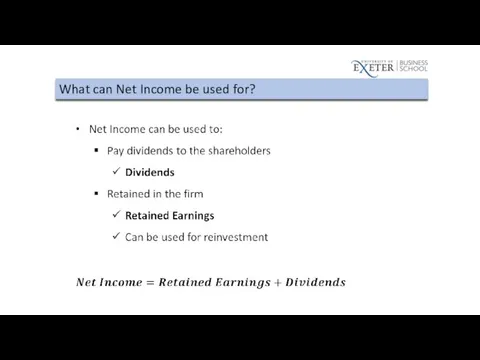

What can Net Income be used for?

What can Net Income be used for?

Income Statement

Income Statement

2.4

Statement of Cash Flows

2.4

Statement of Cash Flows

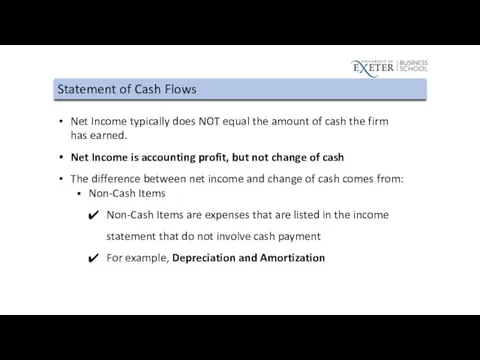

Statement of Cash Flows

Net Income typically does NOT equal the amount

Statement of Cash Flows

Net Income typically does NOT equal the amount

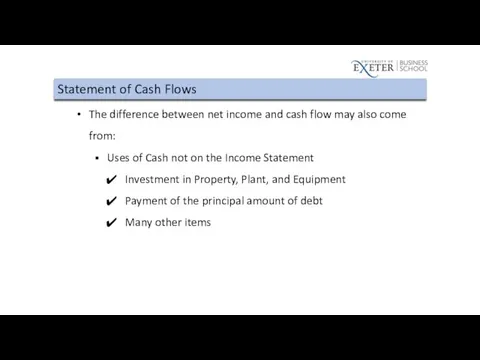

Statement of Cash Flows

The difference between net income and cash flow

Statement of Cash Flows

The difference between net income and cash flow

Statement of Cash Flows: Three Sections

Operating Activity

Investment Activity

Financing Activity

Statement of Cash Flows: Three Sections

Operating Activity

Investment Activity

Financing Activity

Operating Activity

Adjusts net income by all non-cash items related to operating

Operating Activity

Adjusts net income by all non-cash items related to operating

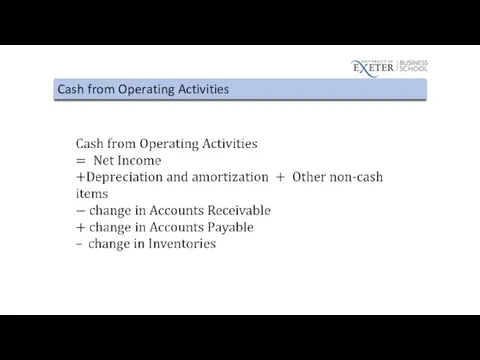

Cash from Operating Activities

Cash from Operating Activities

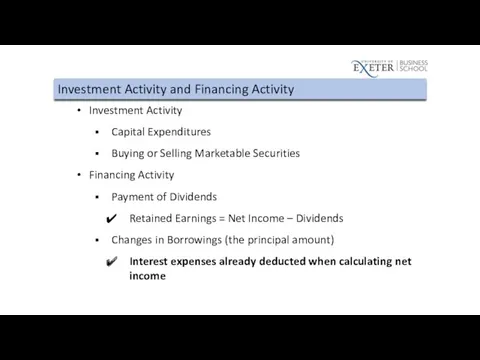

Investment Activity and Financing Activity

Investment Activity

Capital Expenditures

Buying or Selling Marketable

Investment Activity and Financing Activity

Investment Activity

Capital Expenditures

Buying or Selling Marketable

Cash from Investment Activities

Cash from Investment Activities

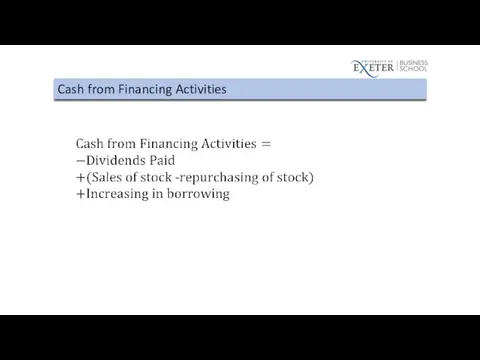

Cash from Financing Activities

Cash from Financing Activities

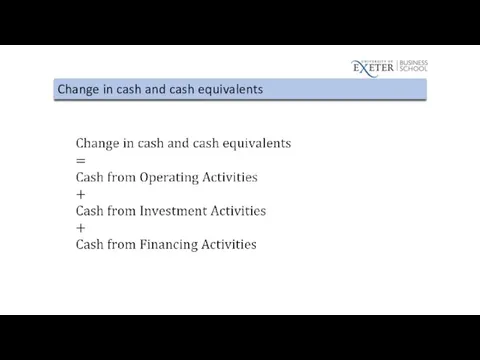

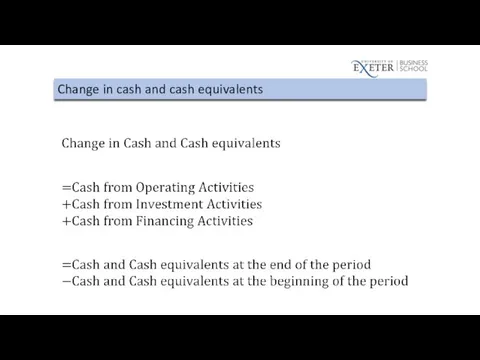

Change in cash and cash equivalents

Change in cash and cash equivalents

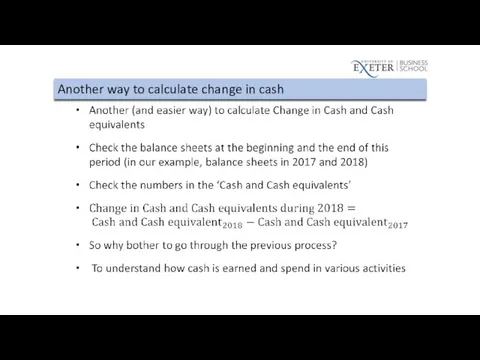

Another way to calculate change in cash

Another way to calculate change in cash

Change in cash and cash equivalents

Change in cash and cash equivalents

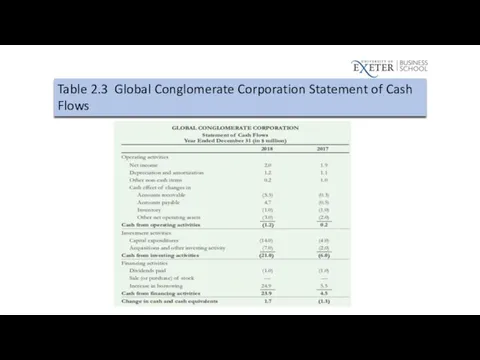

Table 2.3 Global Conglomerate Corporation Statement of Cash Flows

Table 2.3 Global Conglomerate Corporation Statement of Cash Flows

Table 2.1 Global Conglomerate Corporation Balance Sheet

Table 2.1 Global Conglomerate Corporation Balance Sheet

2.5 Other Financial Statement Information

2.5 Other Financial Statement Information

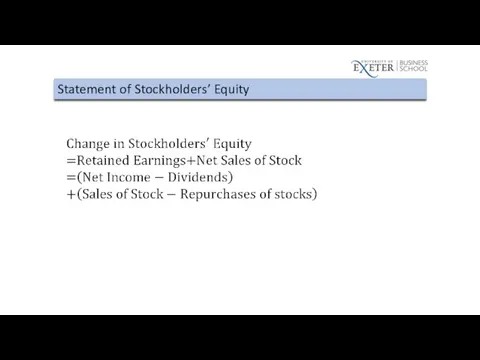

Statement of Stockholders’ Equity

Statement of Stockholders’ Equity

Other Financial Statement Information

Management Discussion and Analysis

Off-Balance Sheet Transactions

Notes to the

Other Financial Statement Information

Management Discussion and Analysis

Off-Balance Sheet Transactions

Notes to the

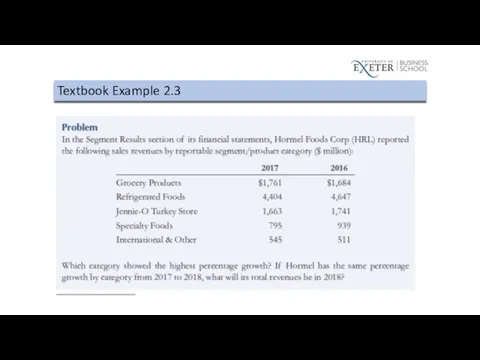

Textbook Example 2.3

Textbook Example 2.3

Textbook Example 2.3

Textbook Example 2.3

2.6

Financial Statement Analysis

2.6

Financial Statement Analysis

Financial Statement Analysis

Financial Statement Analysis can be used

Compare the firm

Financial Statement Analysis

Financial Statement Analysis can be used

Compare the firm

Types of Ratios

Profitability Ratios

Liquidity Ratios

Working Capital Ratios

Interest Coverage Ratios

Leverage Ratios

Valuation Ratios

Operating

Types of Ratios

Profitability Ratios

Liquidity Ratios

Working Capital Ratios

Interest Coverage Ratios

Leverage Ratios

Valuation Ratios

Operating

Profitability Ratios

Profitability Ratios

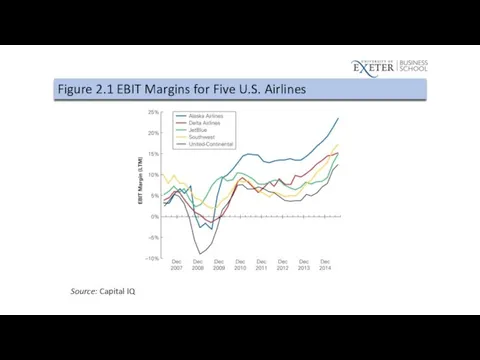

Figure 2.1 EBIT Margins for Five U.S. Airlines

Source: Capital IQ

Figure 2.1 EBIT Margins for Five U.S. Airlines

Source: Capital IQ

Liquidity Ratios

Current Ratio

Current Ratio=Current Assets / Current Liabilities

Quick Ratio

Quick Ratio=(Cash +

Liquidity Ratios

Current Ratio

Current Ratio=Current Assets / Current Liabilities

Quick Ratio

Quick Ratio=(Cash +

Textbook Example 2.4

Textbook Example 2.4

Table 2.1 Global Conglomerate Corporation Balance Sheet

Table 2.1 Global Conglomerate Corporation Balance Sheet

Textbook Example 2.4

Textbook Example 2.4

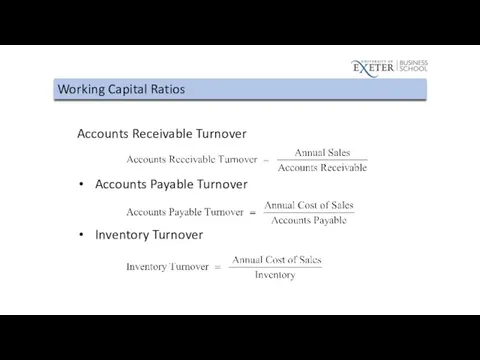

Working Capital Ratios

Accounts Receivable Days

Accounts Payable Days

Inventory Days

Working Capital Ratios

Accounts Receivable Days

Accounts Payable Days

Inventory Days

Working Capital Ratios

Accounts Receivable Turnover

Accounts Payable Turnover

Inventory Turnover

Working Capital Ratios

Accounts Receivable Turnover

Accounts Payable Turnover

Inventory Turnover

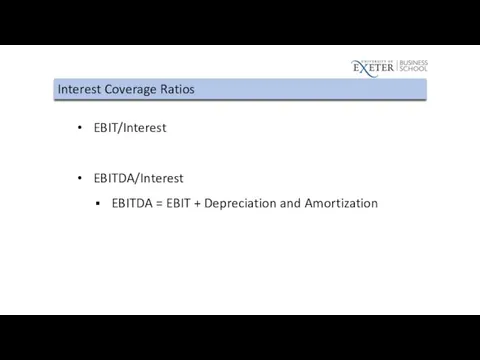

Interest Coverage Ratios

EBIT/Interest

EBITDA/Interest

EBITDA = EBIT + Depreciation and Amortization

Interest Coverage Ratios

EBIT/Interest

EBITDA/Interest

EBITDA = EBIT + Depreciation and Amortization

Textbook Example 2.5

Textbook Example 2.5

Table 2.1 Global Conglomerate Corporation Balance Sheet

Table 2.1 Global Conglomerate Corporation Balance Sheet

Table 2.2 Global Conglomerate Corporation Income Statement

Table 2.2 Global Conglomerate Corporation Income Statement

Textbook Example 2.5

Textbook Example 2.5

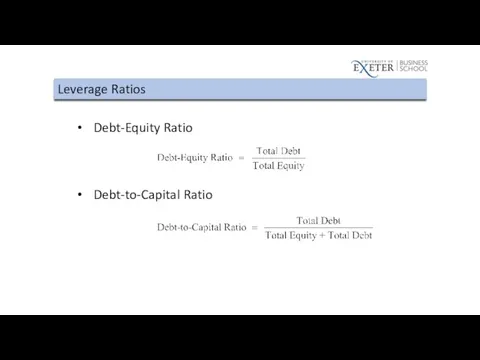

Leverage Ratios

Debt-Equity Ratio

Debt-to-Capital Ratio

Leverage Ratios

Debt-Equity Ratio

Debt-to-Capital Ratio

Table 2.1 Global Conglomerate Corporation Balance Sheet

Table 2.1 Global Conglomerate Corporation Balance Sheet

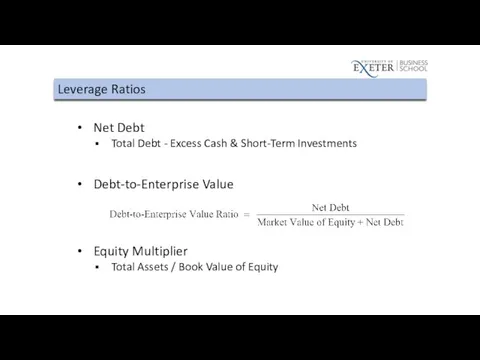

Leverage Ratios

Net Debt

Total Debt - Excess Cash & Short-Term Investments

Debt-to-Enterprise Value

Equity

Leverage Ratios

Net Debt

Total Debt - Excess Cash & Short-Term Investments

Debt-to-Enterprise Value

Equity

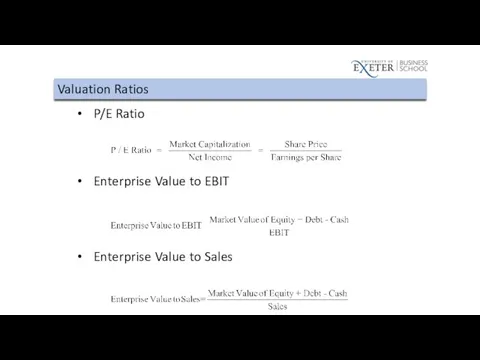

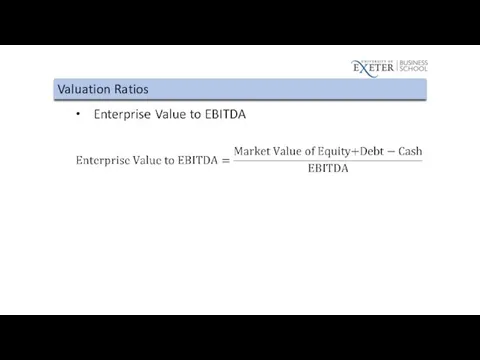

Valuation Ratios

P/E Ratio

Enterprise Value to EBIT

Enterprise Value to Sales

Valuation Ratios

P/E Ratio

Enterprise Value to EBIT

Enterprise Value to Sales

Valuation Ratios

Valuation Ratios

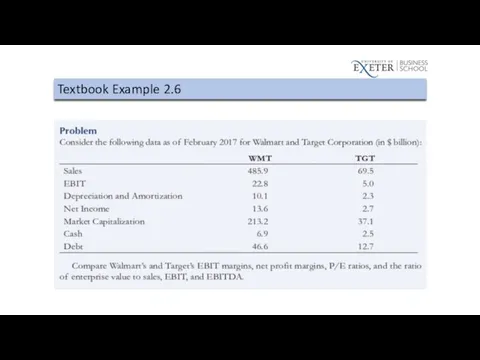

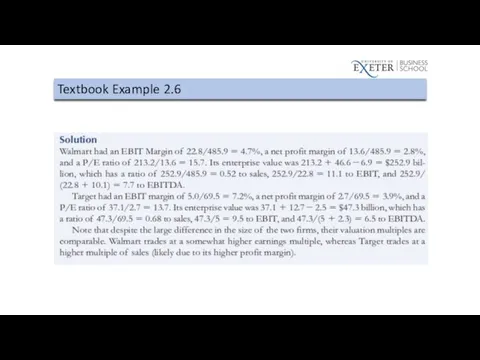

Textbook Example 2.6

Textbook Example 2.6

Textbook Example 2.6

Textbook Example 2.6

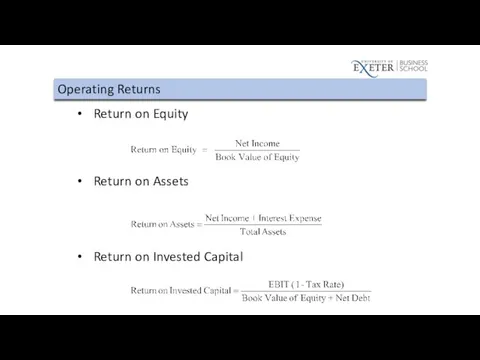

Operating Returns

Return on Equity

Return on Assets

Return on Invested Capital

Operating Returns

Return on Equity

Return on Assets

Return on Invested Capital

Textbook Example 2.7

Textbook Example 2.7

Table 2.2 Global Conglomerate Corporation Income Statement

Table 2.2 Global Conglomerate Corporation Income Statement

Textbook Example 2.7

Textbook Example 2.7

The DuPont Identity

The DuPont Identity

Textbook Example 2.8

Textbook Example 2.8

Textbook Example 2.8

Textbook Example 2.8

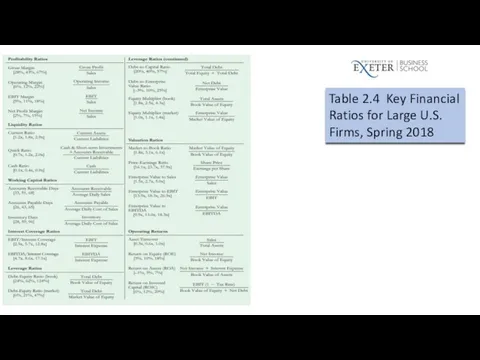

Table 2.4 Key Financial Ratios for Large U.S. Firms, Spring 2018

Table 2.4 Key Financial Ratios for Large U.S. Firms, Spring 2018

2.7 (Optional)

Financial Reporting in Practice

2.7 (Optional)

Financial Reporting in Practice

(Optional) Financial Reporting in Practice

Even with safeguards, reporting abuses still happen:

Enron

WorldCom

Sarbanes-Oxley

(Optional) Financial Reporting in Practice

Even with safeguards, reporting abuses still happen:

Enron

WorldCom

Sarbanes-Oxley

Похожие презентации

Основной капитал компании. Инвестиции

Основной капитал компании. Инвестиции Роль НБУ у регулюванні грошової маси

Роль НБУ у регулюванні грошової маси Приложение к аудиторскому заключению

Приложение к аудиторскому заключению Сектор доставки банковских продуктов проект. Система мотивации специалистов по доставке

Сектор доставки банковских продуктов проект. Система мотивации специалистов по доставке Бухгалтерский учет

Бухгалтерский учет Инвестиционный климат России и инвестиционная привлекательность

Инвестиционный климат России и инвестиционная привлекательность Роль и границы кредита. Роль кредита и его функции

Роль и границы кредита. Роль кредита и его функции Теоретичні засади ринку фінансових послуг. Його роль в економіці України

Теоретичні засади ринку фінансових послуг. Його роль в економіці України Финансовая составляющая социально значимого проекта. Типичные ошибки при составлении сметы проекта

Финансовая составляющая социально значимого проекта. Типичные ошибки при составлении сметы проекта Оценка стоимости земли и природных ресурсов

Оценка стоимости земли и природных ресурсов

Анализ финансового состояния коммерческого банка (на примере ОАО КБ Пойдем)

Анализ финансового состояния коммерческого банка (на примере ОАО КБ Пойдем) Семинар для потенциальных предпринимателей Повышение уровня финансовой грамотности населения Ставропольского края

Семинар для потенциальных предпринимателей Повышение уровня финансовой грамотности населения Ставропольского края Страхование

Страхование Финансовая система Нидерландов

Финансовая система Нидерландов Організація процесу аудиторської перевірки фінансової звітності та її інформаційного забезпечення

Організація процесу аудиторської перевірки фінансової звітності та її інформаційного забезпечення Долевые ценные бумаги. (Тема 3)

Долевые ценные бумаги. (Тема 3) Инструменты поддержки малого и среднего предпринимательства

Инструменты поддержки малого и среднего предпринимательства Анализ рынка жилой недвижимости

Анализ рынка жилой недвижимости Деньги, их функции

Деньги, их функции Продажа программы Идеальный заемщик

Продажа программы Идеальный заемщик Распределение бумаг по группам

Распределение бумаг по группам Понятие стоимости жизненного цикла. Тема 2

Понятие стоимости жизненного цикла. Тема 2 Об основных направлениях бюджетной политики и налоговой политики Ефремово-Степановского сельского поселения на 2018-2020

Об основных направлениях бюджетной политики и налоговой политики Ефремово-Степановского сельского поселения на 2018-2020 Инструменты поддержки стартапов

Инструменты поддержки стартапов Эффективность деятельности компании

Эффективность деятельности компании Range market. Торговля в боковом тренде

Range market. Торговля в боковом тренде Учет, аудит и анализ товарных операций в торговле

Учет, аудит и анализ товарных операций в торговле