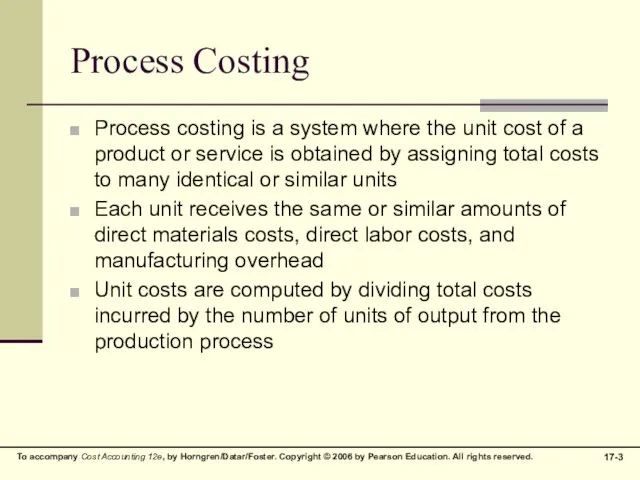

- Process Costing

Содержание

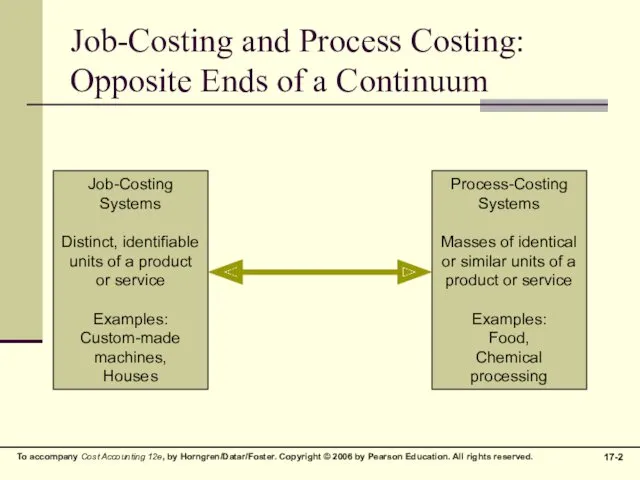

- 2. Job-Costing and Process Costing: Opposite Ends of a Continuum Job-Costing Systems Distinct, identifiable units of a

- 3. Process Costing Process costing is a system where the unit cost of a product or service

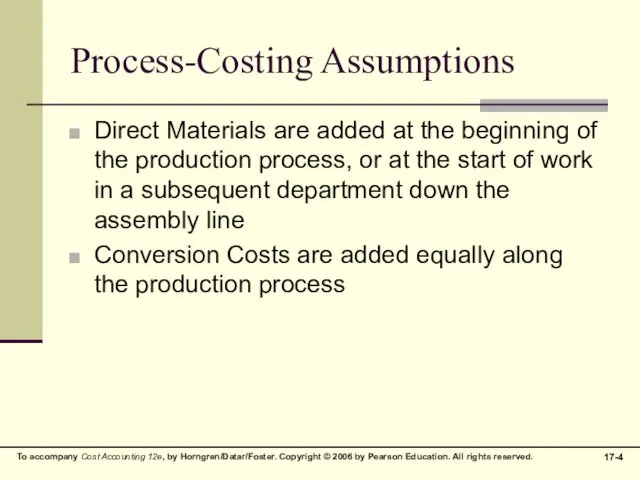

- 4. Process-Costing Assumptions Direct Materials are added at the beginning of the production process, or at the

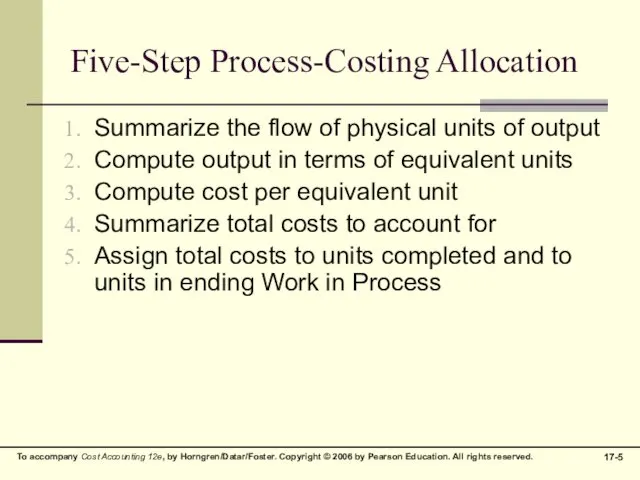

- 5. Five-Step Process-Costing Allocation Summarize the flow of physical units of output Compute output in terms of

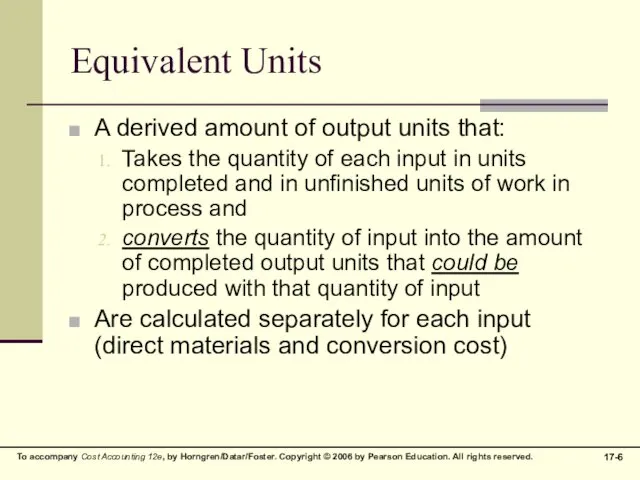

- 6. Equivalent Units A derived amount of output units that: Takes the quantity of each input in

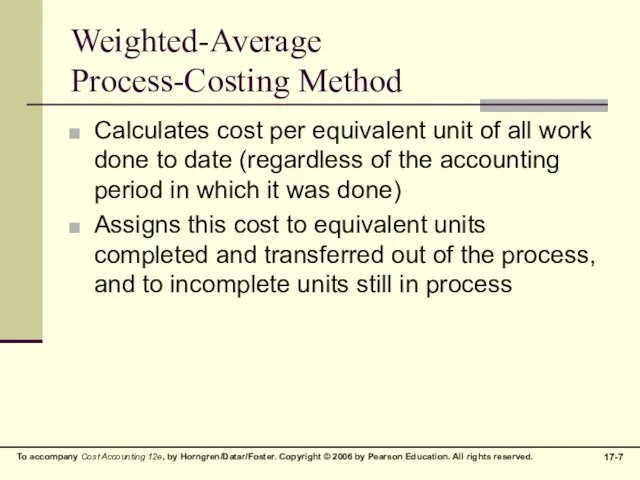

- 7. Weighted-Average Process-Costing Method Calculates cost per equivalent unit of all work done to date (regardless of

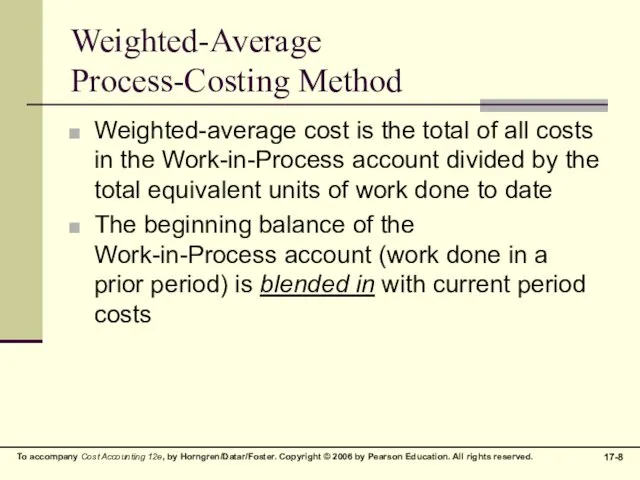

- 8. Weighted-Average Process-Costing Method Weighted-average cost is the total of all costs in the Work-in-Process account divided

- 9. Steps 1 - 5 Weighted-Average Method

- 10. Step 1: Summarize Output Step 2: Compute Equivalent Units

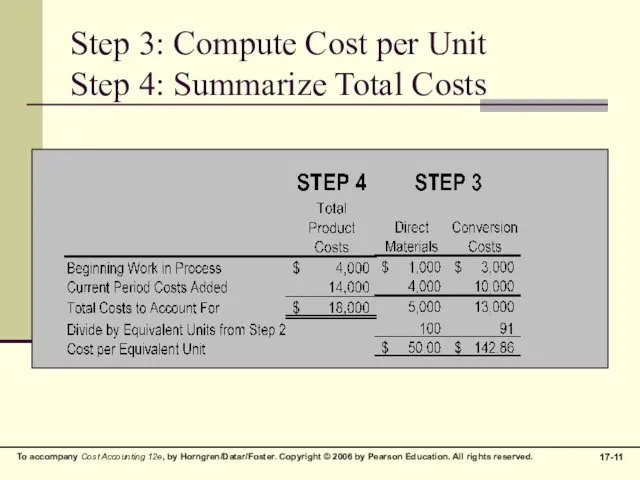

- 11. Step 3: Compute Cost per Unit Step 4: Summarize Total Costs

- 12. Step 5: Assign Costs to Units Completed and Ending Work in Process

- 13. Result of the Process (as before) Two critical figures arise out of Step Five of the

- 14. Standard Costing and Process Costing Teams of design and process engineers, operations personnel, and management accountants

- 16. Скачать презентацию

Job-Costing and Process Costing: Opposite Ends of a Continuum

Job-Costing Systems

Distinct, identifiable

units

Job-Costing and Process Costing: Opposite Ends of a Continuum

Job-Costing Systems

Distinct, identifiable

units

Process Costing

Process costing is a system where the unit cost of

Process Costing

Process costing is a system where the unit cost of

Process-Costing Assumptions

Direct Materials are added at the beginning of the production

Process-Costing Assumptions

Direct Materials are added at the beginning of the production

Five-Step Process-Costing Allocation

Summarize the flow of physical units of output

Compute output

Five-Step Process-Costing Allocation

Summarize the flow of physical units of output

Compute output

Equivalent Units

A derived amount of output units that:

Takes the quantity of

Equivalent Units

A derived amount of output units that:

Takes the quantity of

Weighted-Average

Process-Costing Method

Calculates cost per equivalent unit of all work done

Weighted-Average

Process-Costing Method

Calculates cost per equivalent unit of all work done

Weighted-Average

Process-Costing Method

Weighted-average cost is the total of all costs in

Weighted-Average

Process-Costing Method

Weighted-average cost is the total of all costs in

Steps 1 - 5

Weighted-Average Method

Steps 1 - 5

Weighted-Average Method

Step 1: Summarize Output

Step 2: Compute Equivalent Units

Step 1: Summarize Output

Step 2: Compute Equivalent Units

Step 3: Compute Cost per Unit

Step 4: Summarize Total Costs

Step 3: Compute Cost per Unit

Step 4: Summarize Total Costs

Step 5: Assign Costs to Units Completed and Ending Work in

Step 5: Assign Costs to Units Completed and Ending Work in

Result of the Process (as before)

Two critical figures arise out of

Result of the Process (as before)

Two critical figures arise out of

Standard Costing and

Process Costing

Teams of design and process engineers, operations

Standard Costing and

Process Costing

Teams of design and process engineers, operations

Межбюджетные отношения

Межбюджетные отношения Операції банків в іноземній валюті

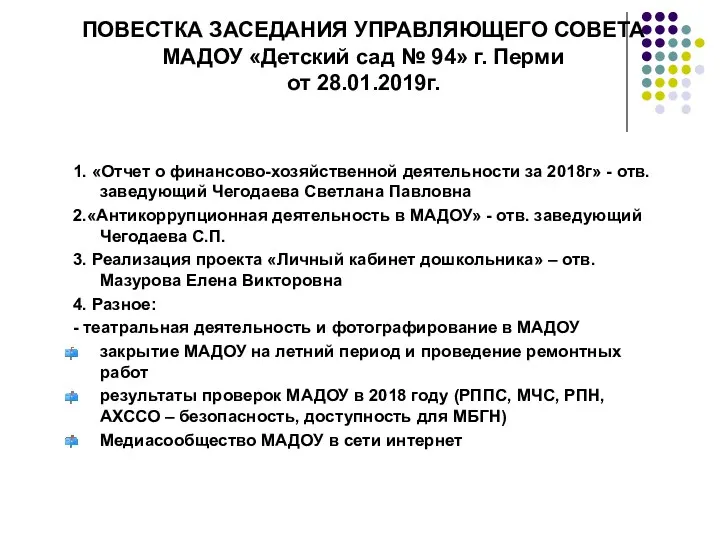

Операції банків в іноземній валюті Повестка заседания управляющего совета МАДОУ Детский сад № 94 г. Перми от 28.01.2019г

Повестка заседания управляющего совета МАДОУ Детский сад № 94 г. Перми от 28.01.2019г Характеристика финансовых институтов, как объекта оценки. (Лекция 1)

Характеристика финансовых институтов, как объекта оценки. (Лекция 1) Государственная экономическая политика. Лекция 5

Государственная экономическая политика. Лекция 5 Ценные бумаги

Ценные бумаги Финансы и управленческий учет

Финансы и управленческий учет Налоговое законодательство. Международные акты в системе налогового законодательства

Налоговое законодательство. Международные акты в системе налогового законодательства Финансовое прогнозирование

Финансовое прогнозирование Анализ отчета о движении денежных средств. (Тема 4)

Анализ отчета о движении денежных средств. (Тема 4) Финансовая политика

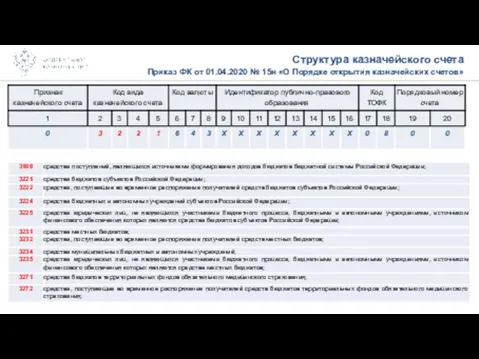

Финансовая политика Приказ ФК от 01.04.2020 № 15н О Порядке открытия казначейских счетов

Приказ ФК от 01.04.2020 № 15н О Порядке открытия казначейских счетов Организация и стимулирование труда персонала в системе менеджмента предприятия ЗАО Сервисный центр ремонта медицинской техники

Организация и стимулирование труда персонала в системе менеджмента предприятия ЗАО Сервисный центр ремонта медицинской техники Предложение способов пополнения счета. Тинькофф. День 3

Предложение способов пополнения счета. Тинькофф. День 3 Операции коммерческих банков на фондовом рынке

Операции коммерческих банков на фондовом рынке НДС 2019-2020: методология и практика исчисления с учетом последних изменений

НДС 2019-2020: методология и практика исчисления с учетом последних изменений Государственный аудит. Модель службы внутреннего контроля и аудита

Государственный аудит. Модель службы внутреннего контроля и аудита Финансовые инструменты

Финансовые инструменты Единый налог на вменённый доход (Енвд)

Единый налог на вменённый доход (Енвд) Cost-benefit analysis

Cost-benefit analysis Товар и деньги. (8 класс)

Товар и деньги. (8 класс) Основные вопросы бюджетного учета и отчетности 2023 года

Основные вопросы бюджетного учета и отчетности 2023 года Налог на добавленную стоимость (НДС)

Налог на добавленную стоимость (НДС) Бюджет для граждан

Бюджет для граждан Анализ прибыли и рентабельности компании

Анализ прибыли и рентабельности компании Разработка информационной системы складского учета средствами облачных вычислений

Разработка информационной системы складского учета средствами облачных вычислений Налоги. Налоговая система

Налоги. Налоговая система Зарплатный проект

Зарплатный проект