- Professional wealth management. Financial managemen

Содержание

- 2. AGENDA Part I – Financial Planning 101 How To Get Started Financial Plan, Budgeting, Net Worth

- 3. How To Get Started A Plan is a Must! Where Am I Now? Net Worth (Assets

- 4. Personal Financial Plan Data Gathering (Where Am I Now, Budget, Net Worth) Set Goals and Objectives

- 5. Financial Planning A financial plan is designed for your individual needs, whether you’re still working or

- 6. Personal Budget List all Income Items Net income, spouse’s net income Rental income, pension income, alimony,

- 7. Surplus or Deficit? How do I increase my monthly cash flow? Increase your income; or Decrease

- 8. Who Can Help? Who Can Help? Your Local Bank (Mutual Fund Rep, Financial Planner, Bank Manager)

- 9. Wealth Management Services Personal investment advice Portfolio management Financial plan Saving for education Retirement planning Maximizing

- 10. The Full Range of Investment Solutions Royalty trusts Preferred shares Common stocks World-class money management programs

- 11. Common Investment Solutions & Tax Treatment Types of Investments Cash or Cash Equivalents (T-Bills, GICs, Money

- 12. Types of Investment Accounts Registered Retirement Savings Plan Tax Deferred Registered Education Savings Plan Tax Deferred

- 13. RSP Strategies RSP Advantages Save for retirement Tax savings Tax-deferred growth

- 14. RSP Advantages The power of tax-deferred growth

- 15. The Power of Compounding Here is an interesting example: A person saves $200 per month and,

- 16. The Right Asset Mix Asset mix is the balance between stocks, bonds and cash Your asset

- 17. The Right Asset Mix Your ideal asset mix largely depends on your life stage

- 18. Eligible Investments Most types of investments are RSP-eligible Liquid investments, fixed income, equity, mutual funds Elimination

- 19. How to Use Tax Refunds Top up your RSP Make your current year’s RSP contribution Add

- 20. Making Contributions Contributions based on earned income Pension adjustment Carry forward

- 21. Consolidation Benefits Understand your financial “big picture” Easier to keep track of asset mix Reduced administrative

- 22. Maximize your Foreign Content No foreign content limit Reduced risk through diversification Greater return potential More

- 23. Maximize your Foreign Content The optimum balance of foreign content Source: FactSet

- 24. Spousal RSPs Legitimate form of income splitting Couples can benefit from a spousal RSP Tax savings

- 25. Options at Retirement Retirement What Does It Look Like? Longer Life Spans = Longer Retirements Options

- 26. Sources of Information www.globefund.ca www.morningstar.ca www.canadianbusiness.com www.canadianbusiness.com/moneysense_magazine The Wealthy Barber

- 27. Tim’s Contact Information Direct Office Line: 416-842-2468 Email: tim.patriquin@rbc.com Website: www.timpatriquin.com

- 29. Скачать презентацию

AGENDA

Part I – Financial Planning 101

How To Get Started

Financial Plan, Budgeting,

AGENDA

Part I – Financial Planning 101

How To Get Started

Financial Plan, Budgeting,

How To Get Started

A Plan is a Must!

Where Am I Now?

Net

How To Get Started

A Plan is a Must!

Where Am I Now?

Net

Personal Financial Plan

Data Gathering (Where Am I Now, Budget, Net Worth)

Set

Personal Financial Plan

Data Gathering (Where Am I Now, Budget, Net Worth)

Set

Financial Planning

A financial plan is designed for your individual needs, whether

Financial Planning

A financial plan is designed for your individual needs, whether

Personal Budget

List all Income Items

Net income, spouse’s net income

Rental income, pension

Personal Budget

List all Income Items

Net income, spouse’s net income

Rental income, pension

Surplus or Deficit?

How do I increase my monthly cash flow?

Increase your

Surplus or Deficit?

How do I increase my monthly cash flow?

Increase your

Who Can Help?

Who Can Help?

Your Local Bank (Mutual Fund Rep, Financial

Who Can Help?

Who Can Help?

Your Local Bank (Mutual Fund Rep, Financial

Wealth Management Services

Personal investment advice

Portfolio management

Financial plan

Saving for education

Retirement planning

Maximizing your

Wealth Management Services

Personal investment advice

Portfolio management

Financial plan

Saving for education

Retirement planning

Maximizing your

The Full Range of Investment Solutions

Royalty trusts

Preferred shares

Common stocks

World-class money management

The Full Range of Investment Solutions

Royalty trusts

Preferred shares

Common stocks

World-class money management

Common Investment Solutions & Tax Treatment

Types of Investments

Cash or Cash Equivalents

Common Investment Solutions & Tax Treatment

Types of Investments

Cash or Cash Equivalents

Types of Investment Accounts

Registered Retirement Savings Plan

Tax Deferred

Registered Education Savings Plan

Tax

Types of Investment Accounts

Registered Retirement Savings Plan

Tax Deferred

Registered Education Savings Plan

Tax

RSP Strategies

RSP Advantages

Save for retirement

Tax savings

Tax-deferred growth

RSP Strategies

RSP Advantages

Save for retirement

Tax savings

Tax-deferred growth

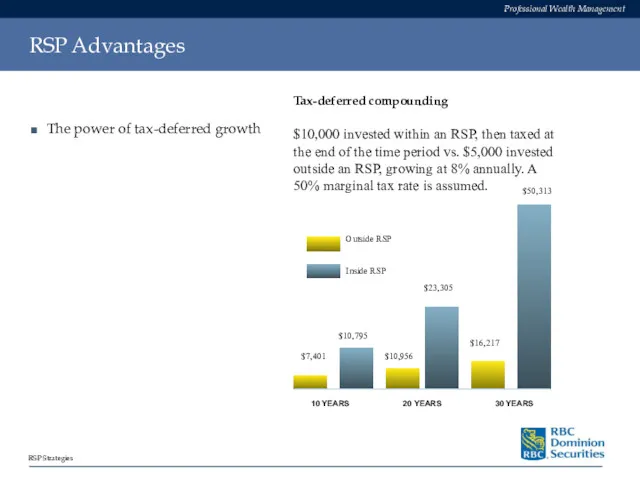

RSP Advantages

The power of tax-deferred growth

RSP Advantages

The power of tax-deferred growth

The Power of Compounding

Here is an interesting example:

A person saves

The Power of Compounding

Here is an interesting example:

A person saves

The Right Asset Mix

Asset mix is the balance between stocks, bonds

The Right Asset Mix

Asset mix is the balance between stocks, bonds

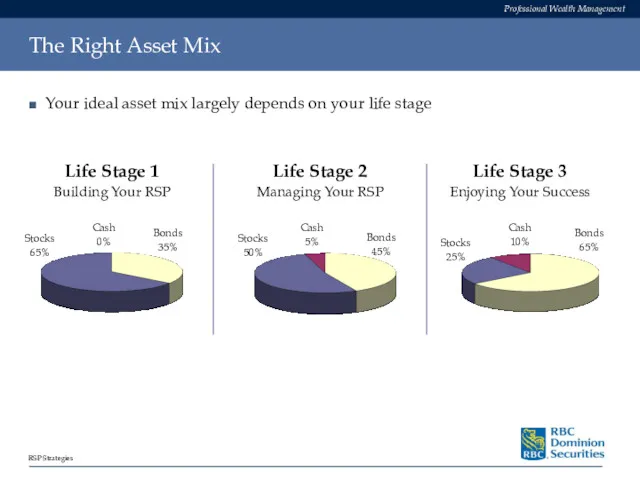

The Right Asset Mix

Your ideal asset mix largely depends on your

The Right Asset Mix

Your ideal asset mix largely depends on your

Eligible Investments

Most types of investments are RSP-eligible

Liquid investments, fixed income, equity,

Eligible Investments

Most types of investments are RSP-eligible

Liquid investments, fixed income, equity,

How to Use Tax Refunds

Top up your RSP

Make your current year’s

How to Use Tax Refunds

Top up your RSP

Make your current year’s

Making Contributions

Contributions based on earned income

Pension adjustment

Carry forward

Making Contributions

Contributions based on earned income

Pension adjustment

Carry forward

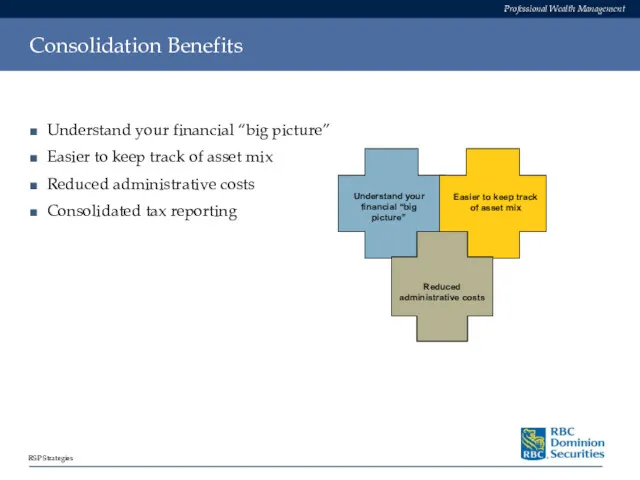

Consolidation Benefits

Understand your financial “big picture”

Easier to keep track of asset

Consolidation Benefits

Understand your financial “big picture”

Easier to keep track of asset

Maximize your Foreign Content

No foreign content limit

Reduced risk through diversification

Greater return

Maximize your Foreign Content

No foreign content limit

Reduced risk through diversification

Greater return

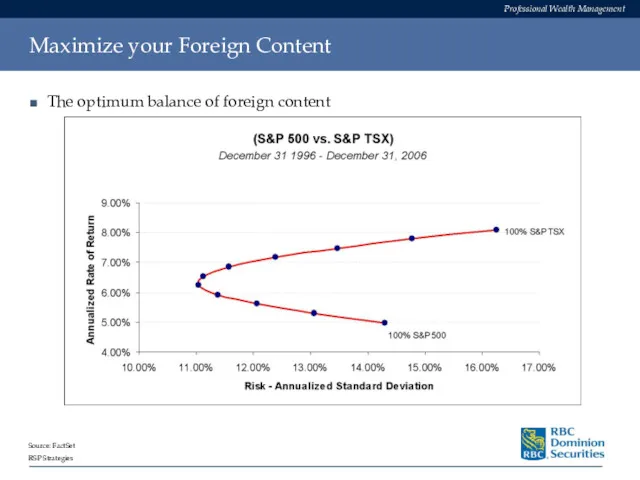

Maximize your Foreign Content

The optimum balance of foreign content

Source: FactSet

Maximize your Foreign Content

The optimum balance of foreign content

Source: FactSet

Spousal RSPs

Legitimate form of income splitting

Couples can benefit from a spousal

Spousal RSPs

Legitimate form of income splitting

Couples can benefit from a spousal

Options at Retirement

Retirement

What Does It Look Like?

Longer Life Spans =

Options at Retirement

Retirement

What Does It Look Like?

Longer Life Spans =

Sources of Information

www.globefund.ca

www.morningstar.ca

www.canadianbusiness.com

www.canadianbusiness.com/moneysense_magazine

The Wealthy Barber

Sources of Information

www.globefund.ca

www.morningstar.ca

www.canadianbusiness.com

www.canadianbusiness.com/moneysense_magazine

The Wealthy Barber

Tim’s Contact Information

Direct Office Line: 416-842-2468

Email: tim.patriquin@rbc.com

Website: www.timpatriquin.com

Tim’s Contact Information

Direct Office Line: 416-842-2468

Email: tim.patriquin@rbc.com

Website: www.timpatriquin.com

Стандарти державного фінансового аудиту

Стандарти державного фінансового аудиту Мотивация и стимулирование труда персонала

Мотивация и стимулирование труда персонала Банки. Страхование, 8 класс

Банки. Страхование, 8 класс Прибыль и рентабельность

Прибыль и рентабельность Supply and demand botanov

Supply and demand botanov Экономическая эффективность использования оборотных средств ОАО Пермский завод Машиностроитель

Экономическая эффективность использования оборотных средств ОАО Пермский завод Машиностроитель Программа накопительного страхования жизни Семья Престиж

Программа накопительного страхования жизни Семья Престиж Отчет главы Сосьвинского городского округа

Отчет главы Сосьвинского городского округа Тест по теме: Рынки факторов производства

Тест по теме: Рынки факторов производства ЗПП АО Альфа-Банк Ultra. Зарплатный проект

ЗПП АО Альфа-Банк Ultra. Зарплатный проект Основы продаж. Технический и графический анализ

Основы продаж. Технический и графический анализ ехнический анализ финансовых рынков

ехнический анализ финансовых рынков Ценовая политика. Тема 6

Ценовая политика. Тема 6 Электронный бюджет

Электронный бюджет Тау самал'' тұрғын үй кешенінің электрэнергетикасы шығынын төмендетуді есептеу мен саралау

Тау самал'' тұрғын үй кешенінің электрэнергетикасы шығынын төмендетуді есептеу мен саралау Компьютерный анализ. Осцилляторы. Контртрендовые индикаторы

Компьютерный анализ. Осцилляторы. Контртрендовые индикаторы Понятие и принципы инвестиционной деятельности

Понятие и принципы инвестиционной деятельности Практикум. Запас материальных ресурсов

Практикум. Запас материальных ресурсов Изменения в бухгалтерском учете учреждений бюджетной сферы вступающие в силу с 2023 года

Изменения в бухгалтерском учете учреждений бюджетной сферы вступающие в силу с 2023 года Міжнародні фінансово-кредитні установи та їх співробітництво з Україною

Міжнародні фінансово-кредитні установи та їх співробітництво з Україною Сметы в НКО. Составление смет к заявке на грант и субсидию. Финансовые отчеты в Фонд Президентских Грантов

Сметы в НКО. Составление смет к заявке на грант и субсидию. Финансовые отчеты в Фонд Президентских Грантов История становления и развития принципов налогообложения

История становления и развития принципов налогообложения Применение методов DCF

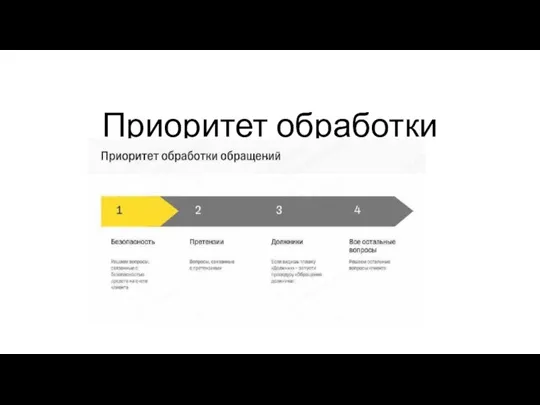

Применение методов DCF Приоритет обработки

Приоритет обработки Салық ұғымымен салық жүйесі ұғымы тығыз байланысты

Салық ұғымымен салық жүйесі ұғымы тығыз байланысты Заемщики. Отношения кредитор - заемщик

Заемщики. Отношения кредитор - заемщик Стоимостная оценка облигаций

Стоимостная оценка облигаций Инструменты повышения прозрачности бюджетной политики. Место России в рейтинге открытости бюджета

Инструменты повышения прозрачности бюджетной политики. Место России в рейтинге открытости бюджета