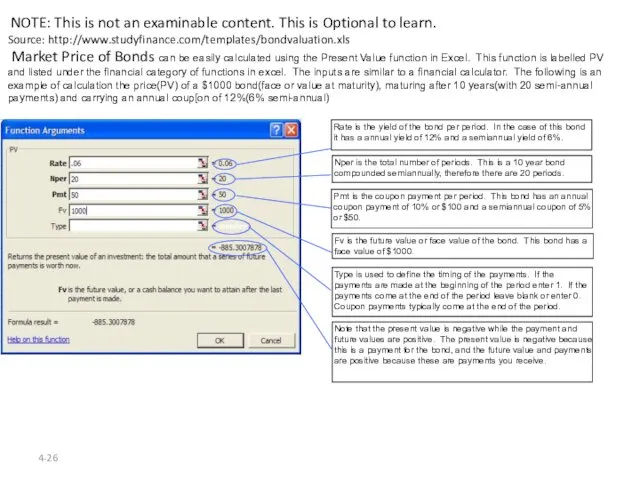

- Understanding Interest Rates. Ch 4 Money Banking Revised

Содержание

- 2. 4- Why Study Interest Rates ? -Interest Rate is known as the cost of credit(finance)and a

- 3. 4- HOW INTERESRT RATE IS DTEREMINED? Economists use three different models to explain how interest rates

- 4. Interest Rate As A Time Value of Money. Money has a time value because it can

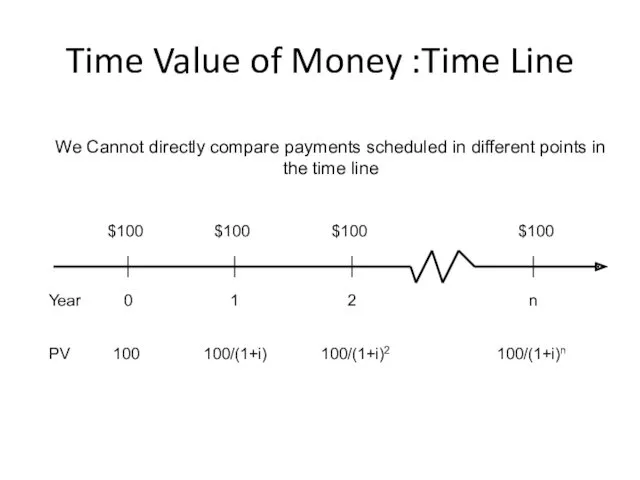

- 5. Time Value of Money :Time Line $100 $100 Year 0 1 PV 100 2 $100 $100

- 6. Present Value(Time Value of Money) A dollar paid to you one year from now is less

- 7. Future Value (It is the idea of compounding) FV of your $100 lending for 2 years

- 8. Applying the Present Value Concept to Credit Products We can apply the concept of Present value

- 9. Example of Present Value and Yield to Maturity: A Case of Coupon Bond If you buy

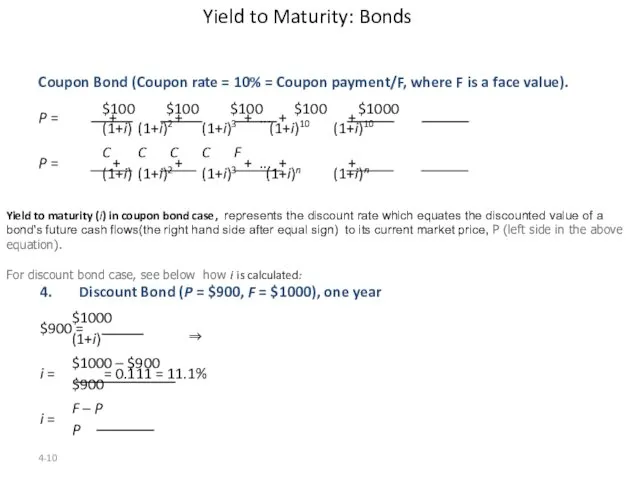

- 10. 4- Yield to Maturity: Bonds ⇒ 4. Discount Bond (P = $900, F = $1000), one

- 11. Taking a numerical example. Consider a bond issued by the Government of Canada, which pays 10%

- 12. On the basis of the previous slides, we can draw the following conclusions: (*) (a) Yield

- 13. 4- Relationship Between Price and Yield to Maturity Three Interesting Facts in Table 1 When bond

- 14. 4- Bonds Premiums & Discounts What happens to bond values if required return is not equal

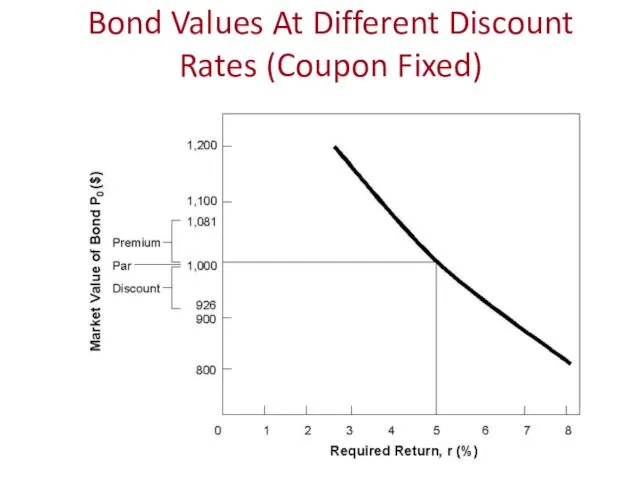

- 15. 4- Bond Values At Different Discount Rates (Coupon Fixed)

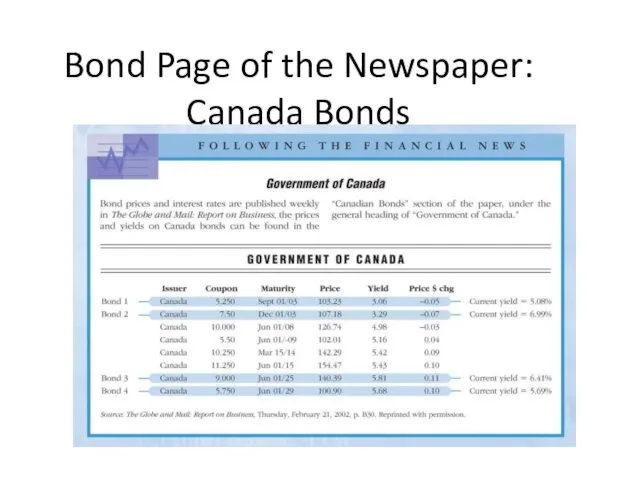

- 16. Bond Page of the Newspaper: Canada Bonds 4-

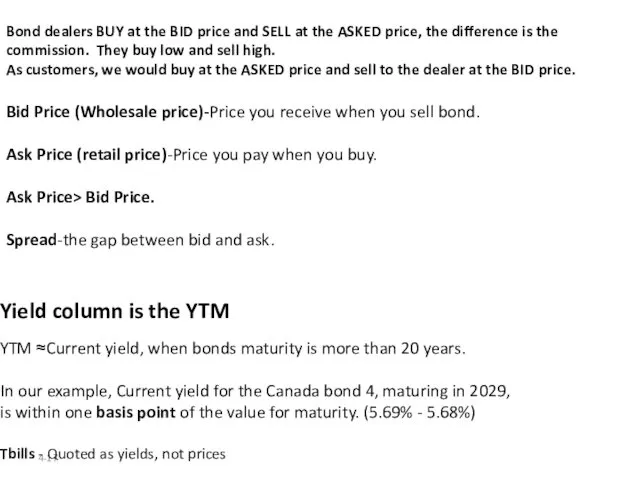

- 17. 4- Bond dealers BUY at the BID price and SELL at the ASKED price, the difference

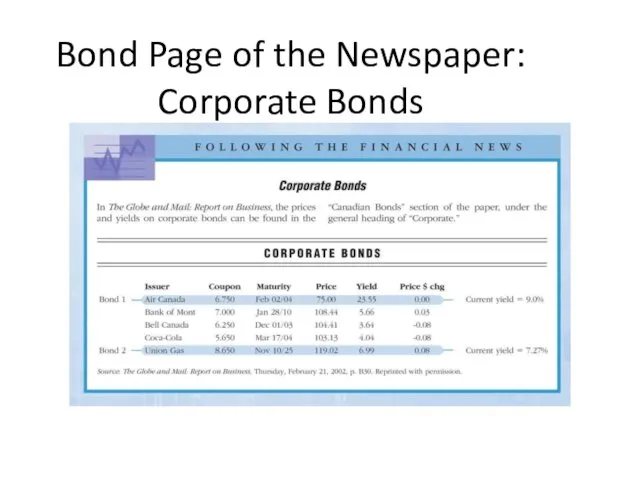

- 18. Bond Page of the Newspaper: Corporate Bonds 4-

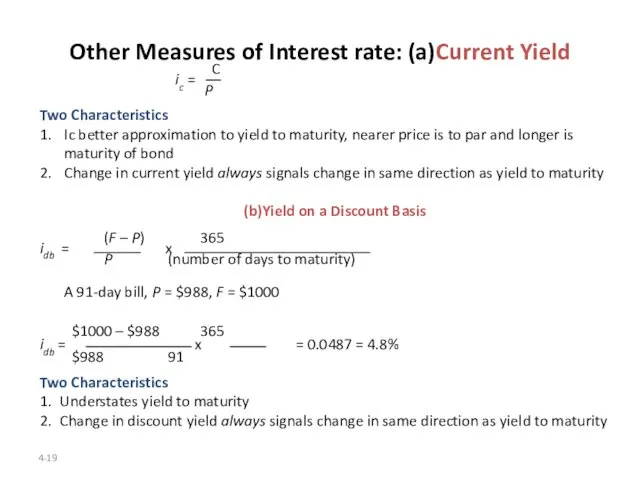

- 19. 4- Other Measures of Interest rate: (a)Current Yield C ic = P Two Characteristics 1. Ic

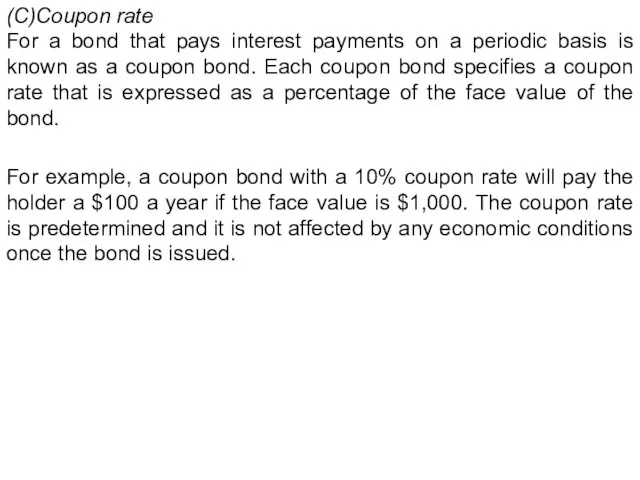

- 20. (C)Coupon rate For a bond that pays interest payments on a periodic basis is known as

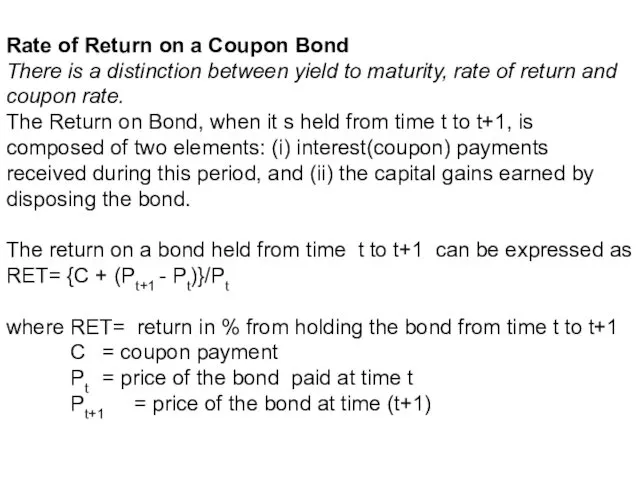

- 21. Rate of Return on a Coupon Bond There is a distinction between yield to maturity, rate

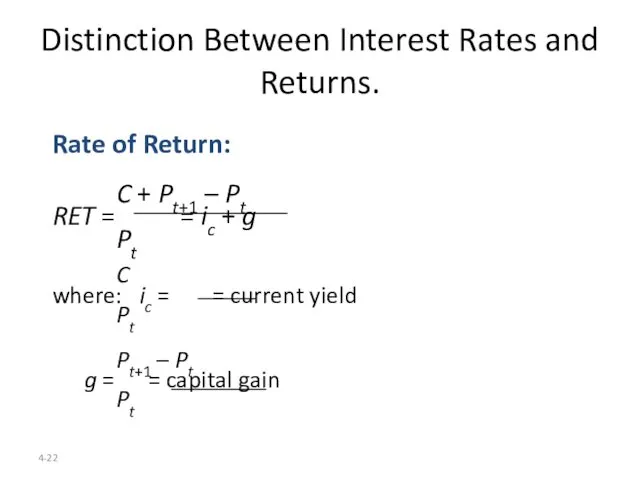

- 22. 4- Distinction Between Interest Rates and Returns. Rate of Return: C + Pt+1 – Pt RET

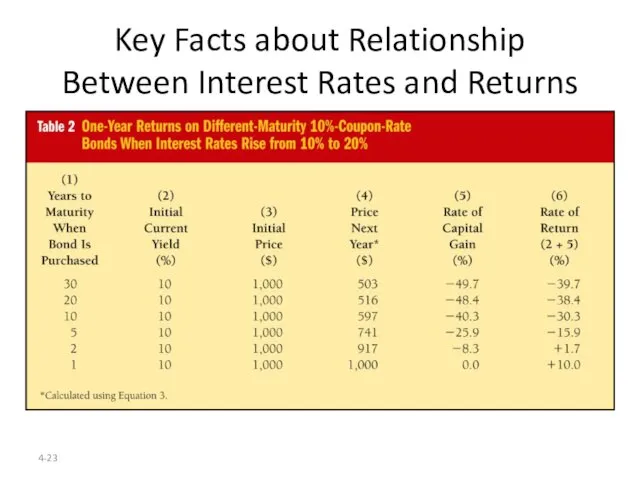

- 23. 4- Key Facts about Relationship Between Interest Rates and Returns

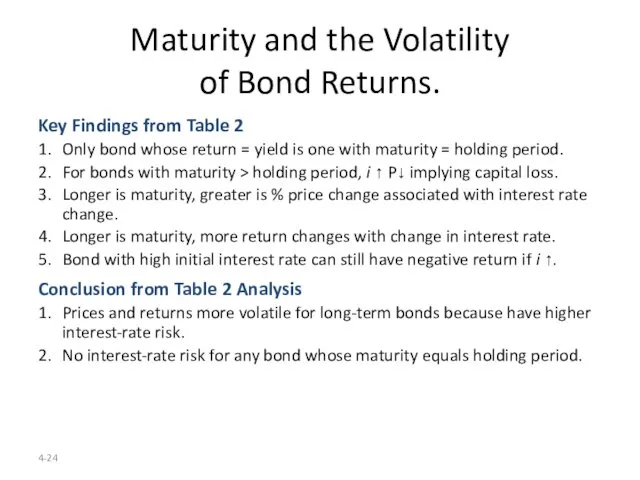

- 24. 4- Maturity and the Volatility of Bond Returns. Key Findings from Table 2 1. Only bond

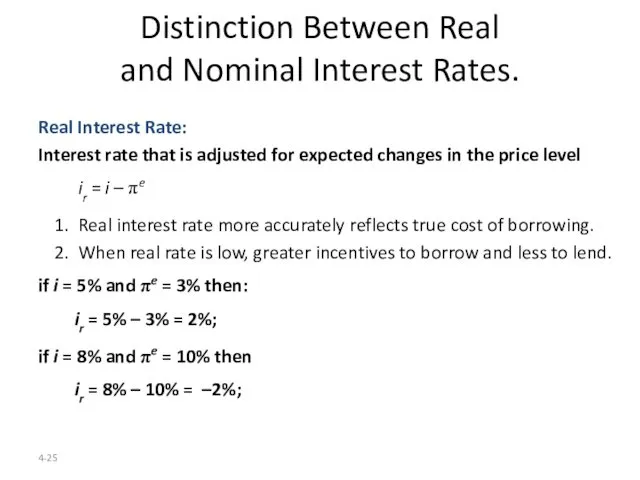

- 25. 4- Distinction Between Real and Nominal Interest Rates. Real Interest Rate: Interest rate that is adjusted

- 26. 4-

- 28. Скачать презентацию

4-

Why Study Interest Rates ?

-Interest Rate is known as the cost

4-

Why Study Interest Rates ?

-Interest Rate is known as the cost

4-

HOW INTERESRT RATE IS DTEREMINED?

Economists use three different models to explain

4-

HOW INTERESRT RATE IS DTEREMINED?

Economists use three different models to explain

Interest Rate As A Time Value of Money.

Money has a

Interest Rate As A Time Value of Money.

Money has a

Time Value of Money :Time Line

$100

$100

Year

0

1

PV

100

2

$100

$100

n

100/(1+i)

100/(1+i)2

100/(1+i)n

We Cannot directly compare payments scheduled

Time Value of Money :Time Line

$100

$100

Year

0

1

PV

100

2

$100

$100

n

100/(1+i)

100/(1+i)2

100/(1+i)n

We Cannot directly compare payments scheduled

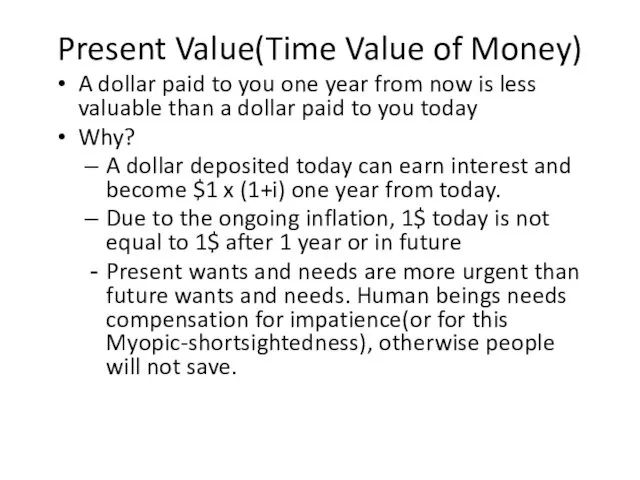

Present Value(Time Value of Money)

A dollar paid to you one year

Present Value(Time Value of Money)

A dollar paid to you one year

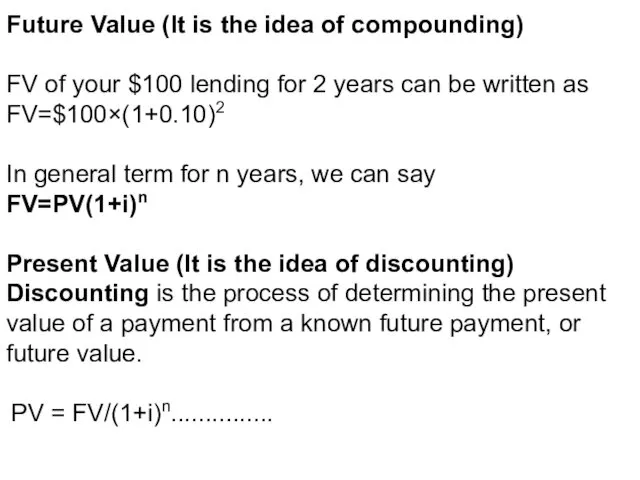

Future Value (It is the idea of compounding)

FV of your $100

Future Value (It is the idea of compounding)

FV of your $100

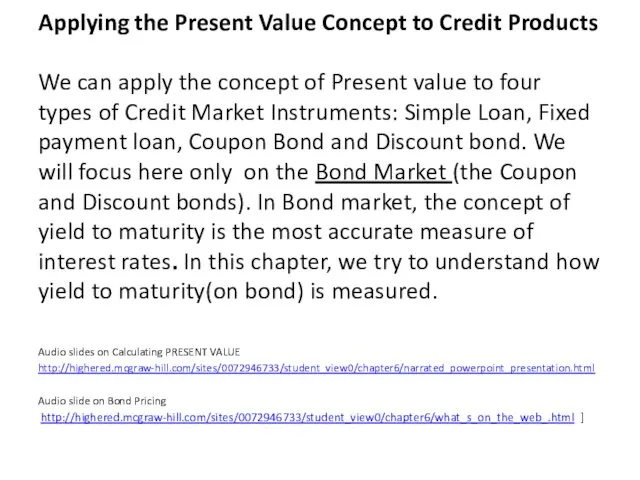

Applying the Present Value Concept to Credit Products

We can apply the

Applying the Present Value Concept to Credit Products We can apply the

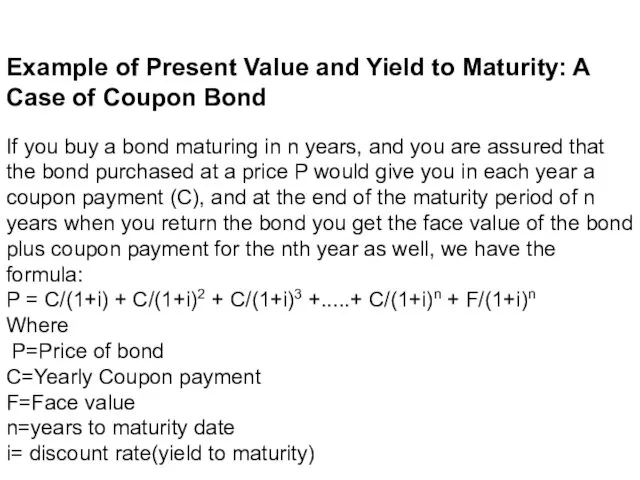

Example of Present Value and Yield to Maturity: A Case of

Example of Present Value and Yield to Maturity: A Case of

4-

Yield to Maturity: Bonds

⇒

4. Discount Bond (P = $900, F =

4-

Yield to Maturity: Bonds

⇒

4. Discount Bond (P = $900, F =

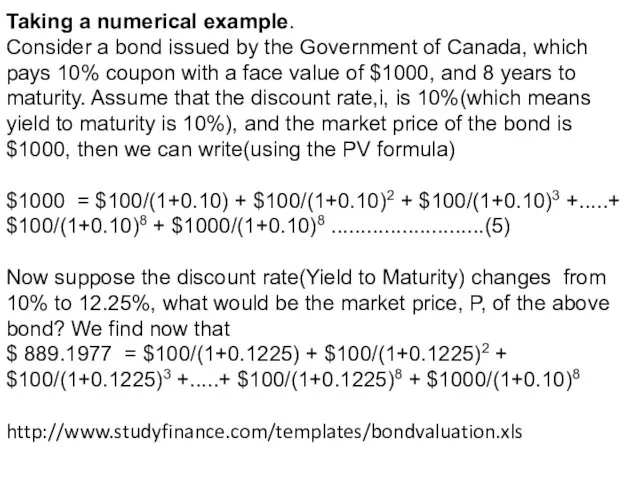

Taking a numerical example.

Consider a bond issued by the Government

Taking a numerical example.

Consider a bond issued by the Government

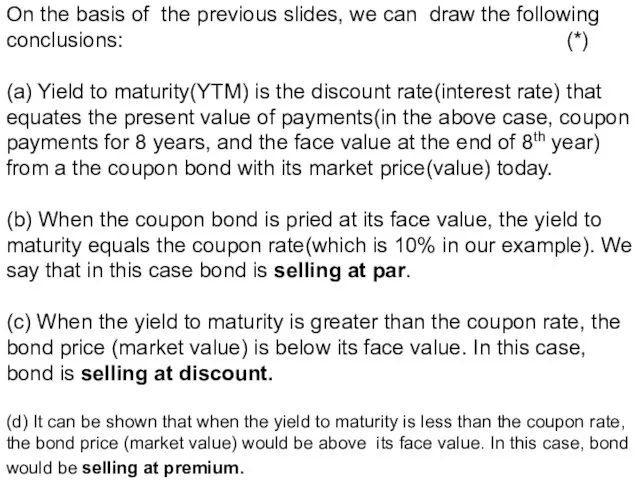

On the basis of the previous slides, we can draw the

On the basis of the previous slides, we can draw the

4-

Relationship Between Price and Yield to Maturity

Three Interesting Facts in Table

4-

Relationship Between Price and Yield to Maturity

Three Interesting Facts in Table

4-

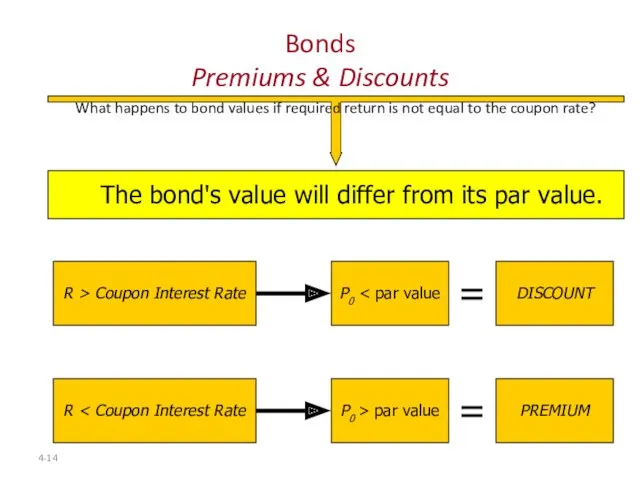

Bonds

Premiums & Discounts

What happens to bond values if required return is

4-

Bonds

Premiums & Discounts

What happens to bond values if required return is

4-

Bond Values At Different Discount Rates (Coupon Fixed)

4-

Bond Values At Different Discount Rates (Coupon Fixed)

Bond Page of the Newspaper:

Canada Bonds

4-

Bond Page of the Newspaper:

Canada Bonds

4-

4-

Bond dealers BUY at the BID price and SELL at the

4-

Bond dealers BUY at the BID price and SELL at the

Bond Page of the Newspaper:

Corporate Bonds

4-

Bond Page of the Newspaper:

Corporate Bonds

4-

4-

Other Measures of Interest rate: (a)Current Yield

C

ic =

4-

Other Measures of Interest rate: (a)Current Yield

C

ic =

(C)Coupon rate

For a bond that pays interest payments on a periodic

(C)Coupon rate

For a bond that pays interest payments on a periodic

Rate of Return on a Coupon Bond

There is a distinction between

Rate of Return on a Coupon Bond

There is a distinction between

4-

Distinction Between Interest Rates and Returns.

Rate of Return:

C + Pt+1 –

4-

Distinction Between Interest Rates and Returns.

Rate of Return:

C + Pt+1 –

4-

Key Facts about Relationship

Between Interest Rates and Returns

4-

Key Facts about Relationship

Between Interest Rates and Returns

4-

Maturity and the Volatility

of Bond Returns.

Key Findings from Table 2

1. Only

4-

Maturity and the Volatility

of Bond Returns.

Key Findings from Table 2

1. Only

4-

Distinction Between Real

and Nominal Interest Rates.

Real Interest Rate:

Interest rate that

4-

Distinction Between Real

and Nominal Interest Rates.

Real Interest Rate:

Interest rate that

4-

4-

Ипотечное кредитование

Ипотечное кредитование Структура подразделения доставки банковских продуктов

Структура подразделения доставки банковских продуктов Роль системы внутреннего контроля в предотвращении мошенничества в финансовой отчетности

Роль системы внутреннего контроля в предотвращении мошенничества в финансовой отчетности New York Stock Exchange (NYSE)

New York Stock Exchange (NYSE) Роль и значение пенсионного фонда РФ в пенсионном обеспечении граждан. Схема назначения и выплаты пенсий

Роль и значение пенсионного фонда РФ в пенсионном обеспечении граждан. Схема назначения и выплаты пенсий Анализ и диагностика финансовых результатов деятельности предприятий торговли и общественного питания

Анализ и диагностика финансовых результатов деятельности предприятий торговли и общественного питания Оценка финансового состояния и финансовой устойчивости организации

Оценка финансового состояния и финансовой устойчивости организации Сергиево-Посадский городской округ. Персонифицированное финансирование дополнительного образования детей

Сергиево-Посадский городской округ. Персонифицированное финансирование дополнительного образования детей Финансовые рынки и институты

Финансовые рынки и институты Бухгалтерские счета и двойная запись

Бухгалтерские счета и двойная запись Индивидуальные инвестиционные счета. АО ФИНАМ

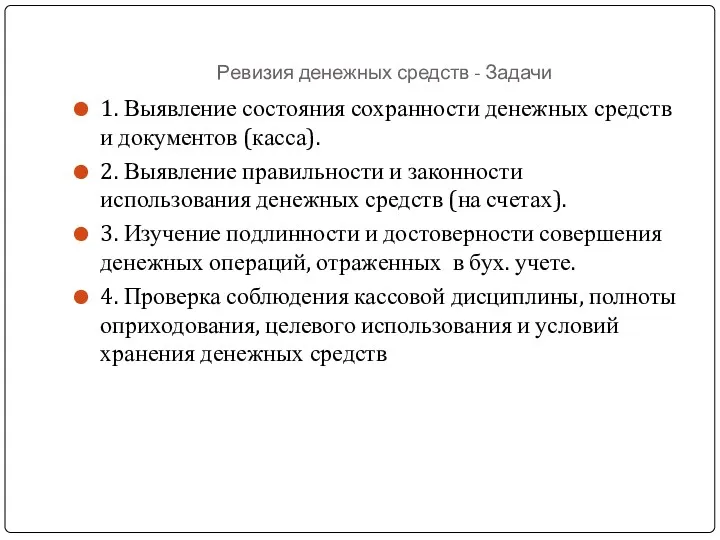

Индивидуальные инвестиционные счета. АО ФИНАМ Ревизия денежных средств. Задачи

Ревизия денежных средств. Задачи Депозитні операції з фізичними особами та управління ними в банку

Депозитні операції з фізичними особами та управління ними в банку Банковская Система РФ

Банковская Система РФ Теоретические основы затратного подхода к оценке предприятий

Теоретические основы затратного подхода к оценке предприятий Инвестиционные проекты и оценка их эффективности

Инвестиционные проекты и оценка их эффективности Упрощенная система налогообложения в издательской деятельности на примере ИП Смолина С.С

Упрощенная система налогообложения в издательской деятельности на примере ИП Смолина С.С Экономическая оценка инвестиций в логистических системах. Часть 1

Экономическая оценка инвестиций в логистических системах. Часть 1 Основы организации бухгалтерского учета в кредитных организациях

Основы организации бухгалтерского учета в кредитных организациях Эффект финансового рычага

Эффект финансового рычага Межбанковские расчеты РК и порядок их осуществления. (Тема 4)

Межбанковские расчеты РК и порядок их осуществления. (Тема 4) Продукты и услуги АО Альфа-Банк для Клиентов физических лиц

Продукты и услуги АО Альфа-Банк для Клиентов физических лиц Правовое регулирование деятельности бирж в Республике Беларусь

Правовое регулирование деятельности бирж в Республике Беларусь Финансирование малого и среднего инновационного бизнеса на территории Российской Федерации

Финансирование малого и среднего инновационного бизнеса на территории Российской Федерации Международный стандарт аудита 300. Планирование аудита финансовой отчетности

Международный стандарт аудита 300. Планирование аудита финансовой отчетности Риск. Количественная и качественная оценка рисков

Риск. Количественная и качественная оценка рисков Тест Хауи в США: современная практика его применения

Тест Хауи в США: современная практика его применения Жалпы және таза табыс

Жалпы және таза табыс