- Value at Risk

Содержание

- 2. The Question Being Asked in VaR “What loss level is such that we are X% confident

- 3. VaR and Regulatory Capital (Business Snapshot 18.1, page 436) Regulators base the capital they require banks

- 4. VaR vs. C-VaR (See Figures 18.1 and 18.2) VaR is the loss level that will not

- 5. Advantages of VaR It captures an important aspect of risk in a single number It is

- 6. Time Horizon Instead of calculating the 10-day, 99% VaR directly analysts usually calculate a 1-day 99%

- 7. Historical Simulation (See Tables 18.1 and 18.2, page 438-439)) Create a database of the daily movements

- 8. Historical Simulation continued Suppose we use m days of historical data Let vi be the value

- 9. The Model-Building Approach The main alternative to historical simulation is to make assumptions about the probability

- 10. Daily Volatilities In option pricing we measure volatility “per year” In VaR calculations we measure volatility

- 11. Daily Volatility continued Strictly speaking we should define σday as the standard deviation of the continuously

- 12. Microsoft Example (page 440) We have a position worth $10 million in Microsoft shares The volatility

- 13. Microsoft Example continued The standard deviation of the change in the portfolio in 1 day is

- 14. Microsoft Example continued We assume that the expected change in the value of the portfolio is

- 15. AT&T Example (page 441) Consider a position of $5 million in AT&T The daily volatility of

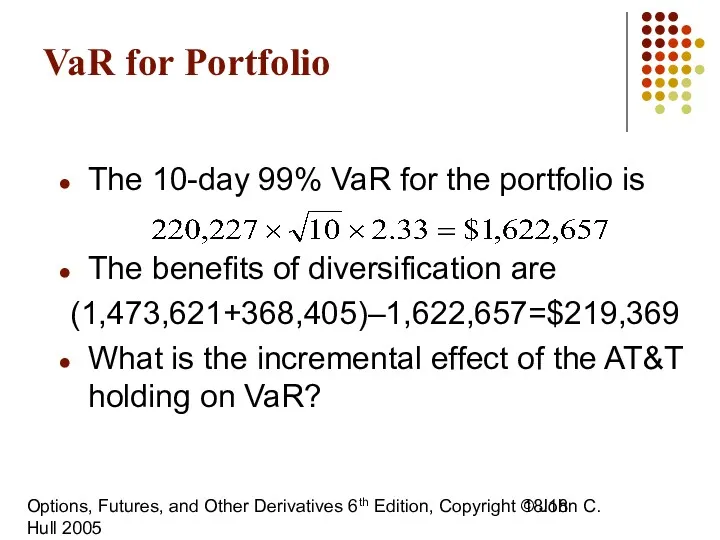

- 16. Portfolio Now consider a portfolio consisting of both Microsoft and AT&T Suppose that the correlation between

- 17. S.D. of Portfolio A standard result in statistics states that In this case σX = 200,000

- 18. Options, Futures, and Other Derivatives 6th Edition, Copyright © John C. Hull 2005 18. VaR for

- 19. Value at Risk

- 20. Overview Concepts Components Calculations Corporate perspective Comments

- 21. I VALUE AT RISK - CONCEPTS

- 22. Risk Financial Risks - Market Risk, Credit Risk, Liquidity Risk, Operational Risk Risk is the variability

- 23. VAR measures Market risk Credit risk of late

- 24. VAR is an estimate of the adverse impact on P&L in a conservative scenario. It is

- 25. Ingredients - Exposure to market variable Sensitivity Probability of adverse market movement Probability distribution of market

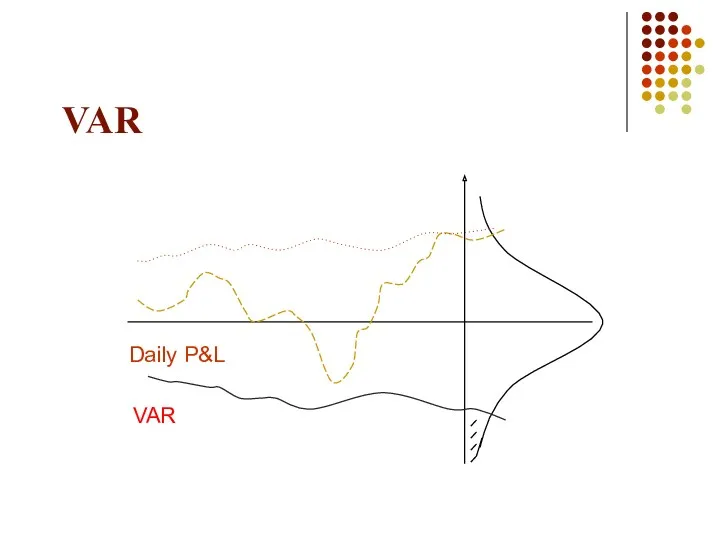

- 26. VAR Daily P&L VAR

- 27. VAR Daily P&L VAR

- 28. II VALUE AT RISK - COMPONENTS

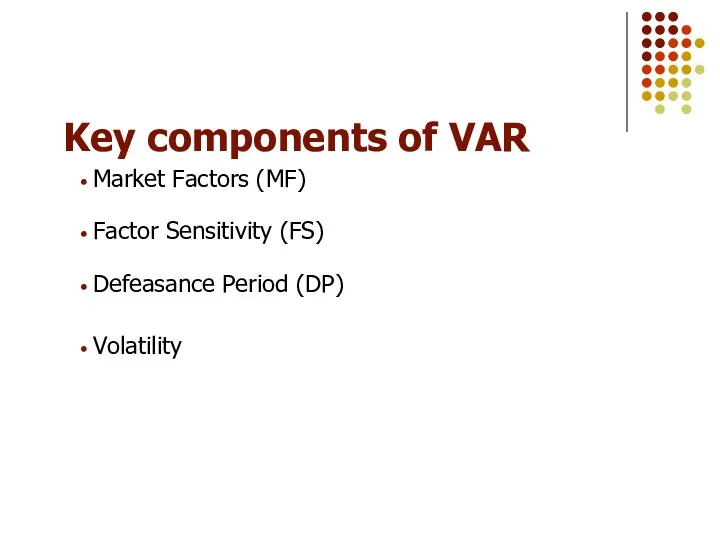

- 29. Key components of VAR Market Factors (MF) Factor Sensitivity (FS) Defeasance Period (DP) Volatility

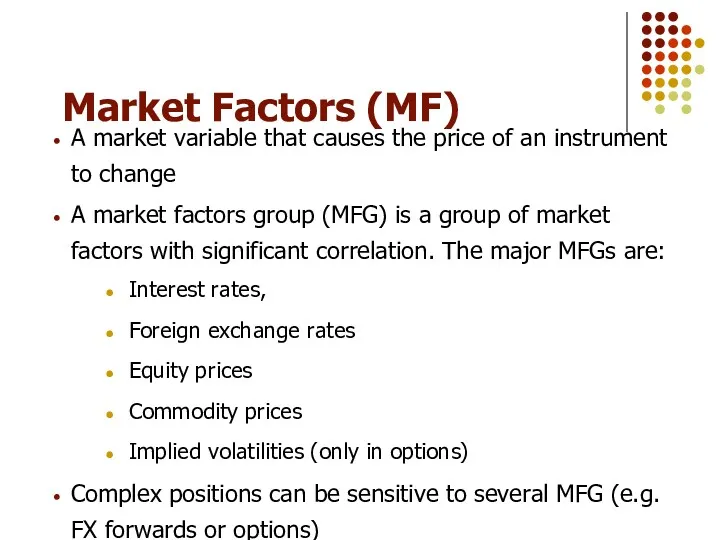

- 30. Market Factors (MF) A market variable that causes the price of an instrument to change A

- 31. Factor Sensitivity (FS) FS is the change in the value of a position due to a

- 32. Factor Sensitivity - Zero Coupon Bond What is the 1 BP FS of a $2,100 1-year

- 33. Market Volatility Volatility is a measure of the dispersion of a market variable against its mean

- 34. Estimating Volatility 1. Historical data analysis 2. Judgmental 3. Implied (from options prices)

- 35. Defeasance period This is defined as the time elapsed (normally expressed in days) before a position

- 36. Defeasance Factor (DF) DF is the total volatility over the defeasance period On the assumption that

- 37. VAR formula VAR = zα σp √Δt * FS Where: zα is the constant giving the

- 38. VAR Daily P&L VAR

- 39. III VALUE AT RISK - CALCULATIONS

- 40. Sample VAR Calculations Let us consider the following positions: Long EUR against the USD : $

- 41. Sample VAR Calculations Annual volatility of DEM is 9% Volatility for N days = annual volatility

- 42. Sample VAR Calculations Now, a 1% change has an impact of 10,000 (FS) So, a 1.30%

- 43. Sample VAR Calculations Similarly, for JPY, the annual volatility is 12% The 1 day volatility =

- 44. IV VALUE AT RISK FOR CORPORATIONS

- 45. VAR FOR CORPORATIONS Trading portfolios Longer time horizons for close outs Business risk as opposed to

- 46. VAR FOR CORPORATIONS Identify market variables impacting business Map income sensitivity to market variables - Scenario

- 47. VAR FOR CORPORATIONS Hedging tools Forward FX Currency swaps Interest Rate swaps Options on non-INR market

- 48. V VALUE AT RISK- A FEW COMMENTS

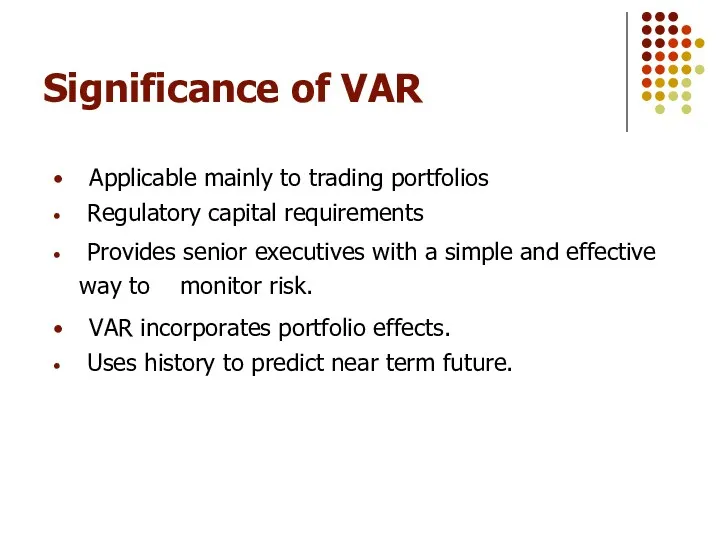

- 49. Significance of VAR Applicable mainly to trading portfolios Regulatory capital requirements Provides senior executives with a

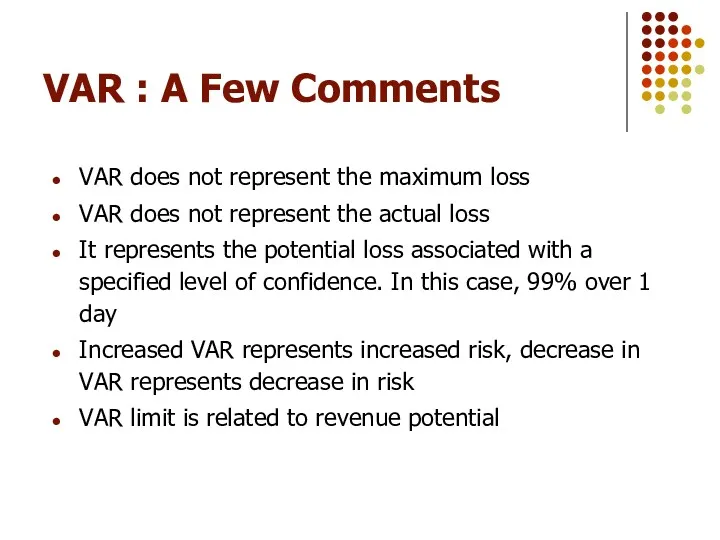

- 50. VAR : A Few Comments VAR does not represent the maximum loss VAR does not represent

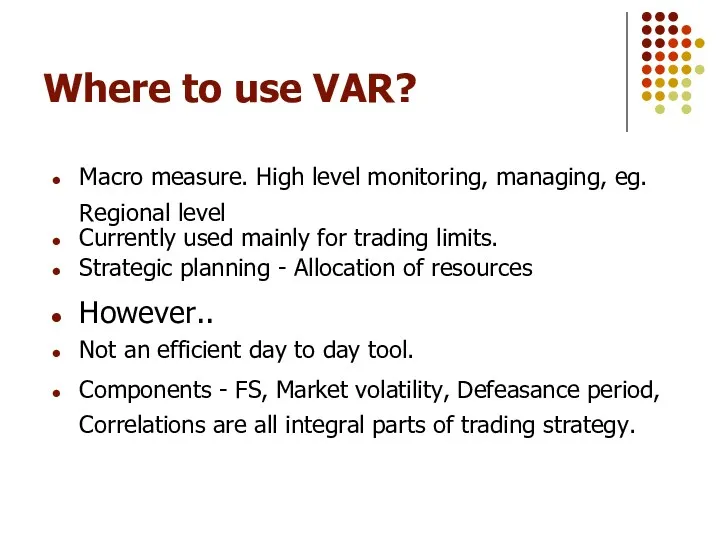

- 51. Where to use VAR? Macro measure. High level monitoring, managing, eg. Regional level Currently used mainly

- 52. How to use Var Stress Testing : * “worst case” scenario * Multiple Stress Scenarios *

- 53. General Market Risk Issues Integrity - Rate Reasonability - At Inception - Revaluation Model Certification Control

- 55. Скачать презентацию

The Question Being Asked in VaR

“What loss level is such that

The Question Being Asked in VaR

“What loss level is such that

VaR and Regulatory Capital

(Business Snapshot 18.1, page 436)

Regulators base the capital

VaR and Regulatory Capital

(Business Snapshot 18.1, page 436)

Regulators base the capital

VaR vs. C-VaR

(See Figures 18.1 and 18.2)

VaR is the loss

VaR vs. C-VaR

(See Figures 18.1 and 18.2)

VaR is the loss

Advantages of VaR

It captures an important aspect of risk

in a single

Advantages of VaR

It captures an important aspect of risk

in a single

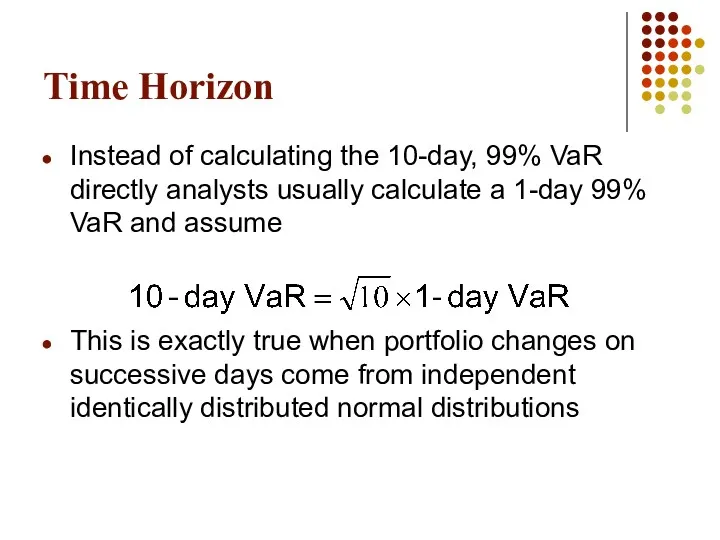

Time Horizon

Instead of calculating the 10-day, 99% VaR directly analysts usually

Time Horizon

Instead of calculating the 10-day, 99% VaR directly analysts usually

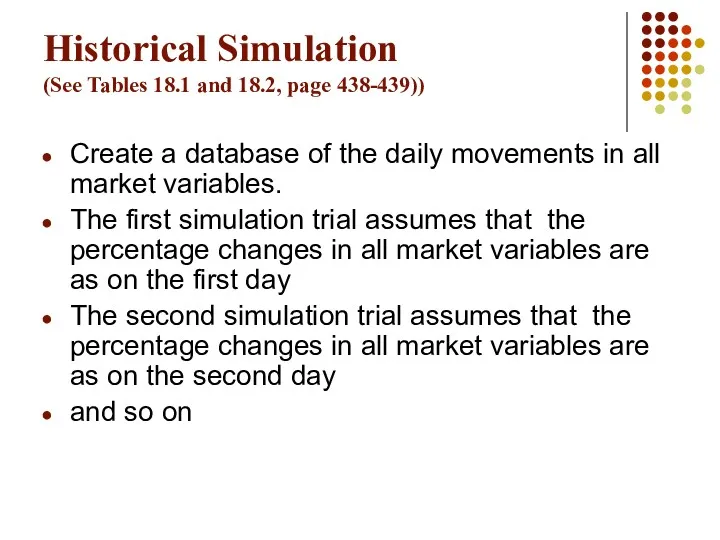

Historical Simulation

(See Tables 18.1 and 18.2, page 438-439))

Create a database

Historical Simulation

(See Tables 18.1 and 18.2, page 438-439))

Create a database

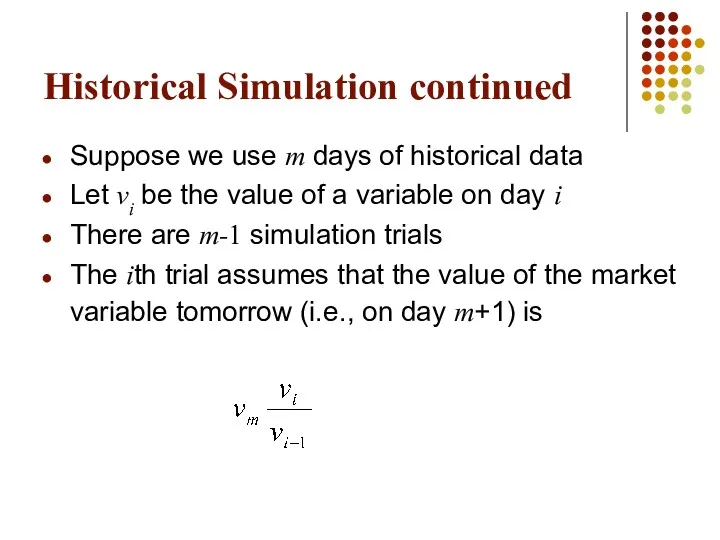

Historical Simulation continued

Suppose we use m days of historical data

Let vi

Historical Simulation continued

Suppose we use m days of historical data

Let vi

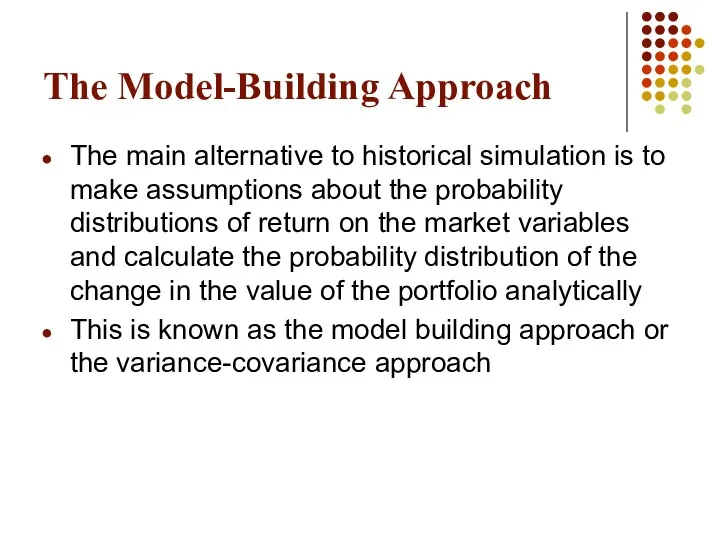

The Model-Building Approach

The main alternative to historical simulation is to make

The Model-Building Approach

The main alternative to historical simulation is to make

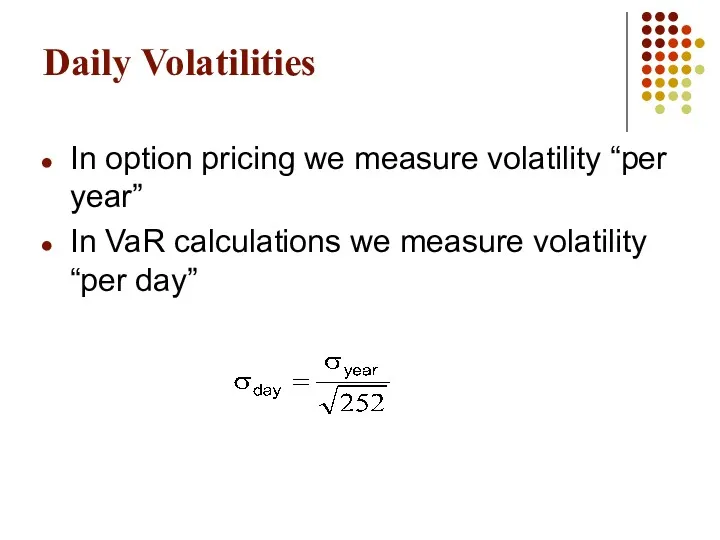

Daily Volatilities

In option pricing we measure volatility “per year”

In VaR calculations

Daily Volatilities

In option pricing we measure volatility “per year”

In VaR calculations

Daily Volatility continued

Strictly speaking we should define σday as the standard

Daily Volatility continued

Strictly speaking we should define σday as the standard

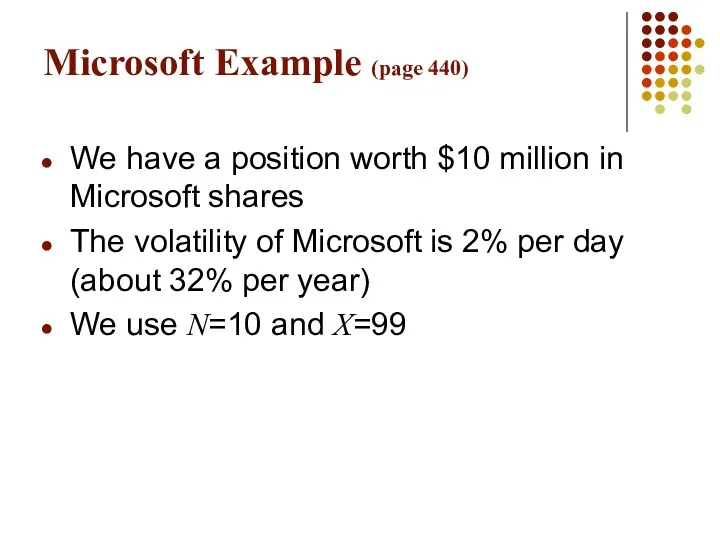

Microsoft Example (page 440)

We have a position worth $10 million in

Microsoft Example (page 440)

We have a position worth $10 million in

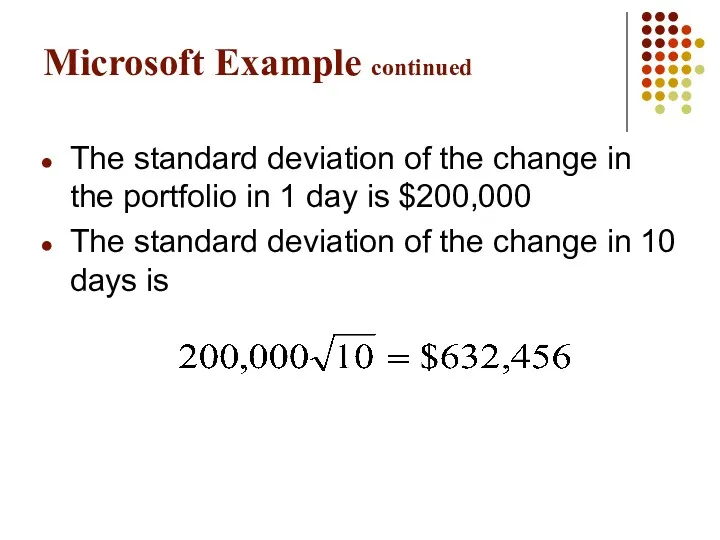

Microsoft Example continued

The standard deviation of the change in the portfolio

Microsoft Example continued

The standard deviation of the change in the portfolio

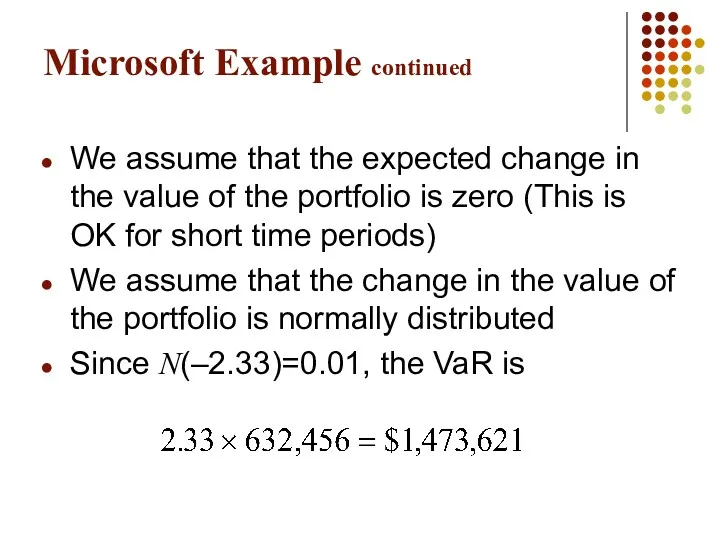

Microsoft Example continued

We assume that the expected change in the value

Microsoft Example continued

We assume that the expected change in the value

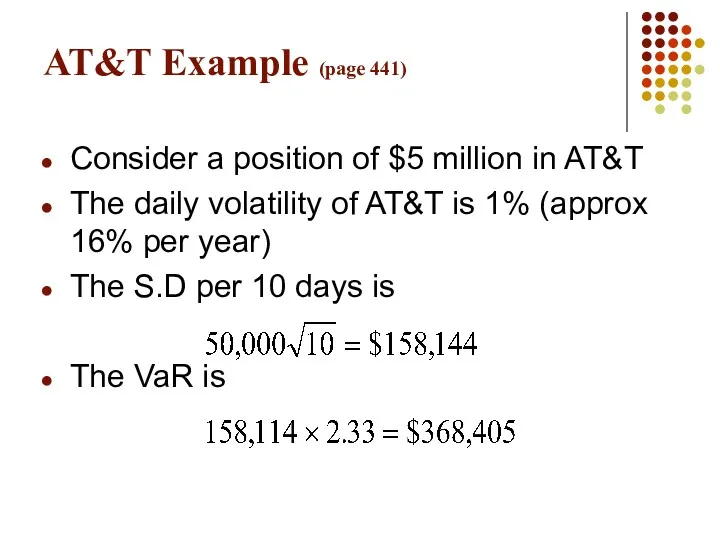

AT&T Example (page 441)

Consider a position of $5 million in AT&T

The

AT&T Example (page 441)

Consider a position of $5 million in AT&T

The

Portfolio

Now consider a portfolio consisting of both Microsoft and AT&T

Suppose that

Portfolio

Now consider a portfolio consisting of both Microsoft and AT&T

Suppose that

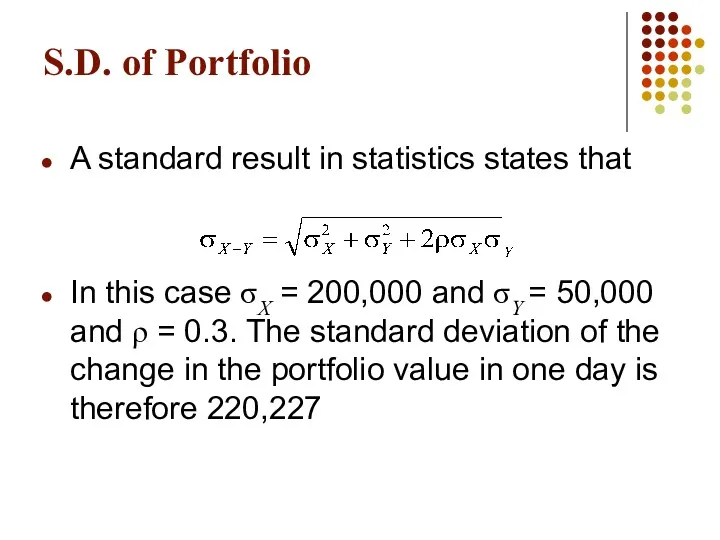

S.D. of Portfolio

A standard result in statistics states that

In this case

S.D. of Portfolio

A standard result in statistics states that

In this case

Options, Futures, and Other Derivatives 6th Edition, Copyright © John C.

Options, Futures, and Other Derivatives 6th Edition, Copyright © John C.

Value at Risk

Value at Risk

Overview

Concepts

Components

Calculations

Corporate perspective

Comments

Overview

Concepts

Components

Calculations

Corporate perspective

Comments

I VALUE AT RISK - CONCEPTS

I VALUE AT RISK - CONCEPTS

Risk

Financial Risks - Market Risk, Credit Risk, Liquidity Risk, Operational Risk

Risk

Risk

Financial Risks - Market Risk, Credit Risk, Liquidity Risk, Operational Risk

Risk

VAR measures

Market risk

Credit risk of late

VAR measures

Market risk

Credit risk of late

VAR is an estimate of the adverse impact on P&L in

Ingredients -

Exposure to market variable

Sensitivity

Probability of adverse

Exposure to market variable

Sensitivity

Probability of adverse

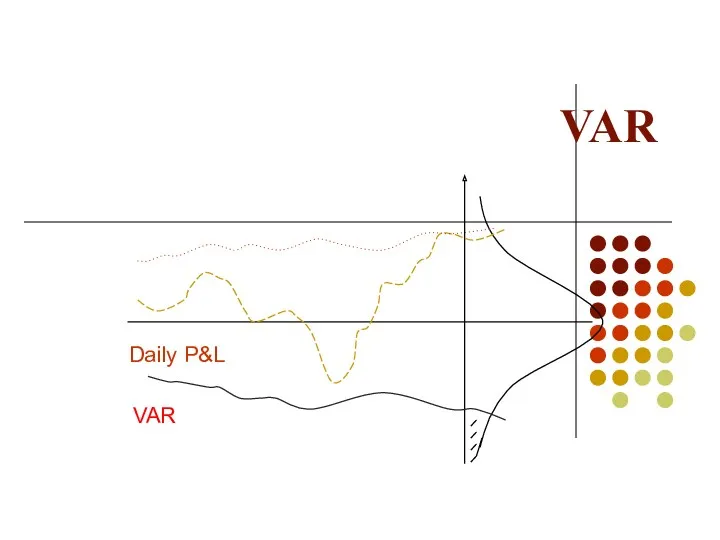

VAR

Daily P&L

VAR

VAR

Daily P&L

VAR

VAR

Daily P&L

VAR

VAR

Daily P&L

VAR

II VALUE AT RISK - COMPONENTS

II VALUE AT RISK - COMPONENTS

Key components of VAR

Market Factors (MF)

Factor Sensitivity (FS)

Defeasance Period (DP)

Volatility

Key components of VAR

Market Factors (MF)

Factor Sensitivity (FS)

Defeasance Period (DP)

Volatility

Market Factors (MF)

A market variable that causes the price of an

Market Factors (MF)

A market variable that causes the price of an

Factor Sensitivity (FS)

FS is the change in the value of a

Factor Sensitivity (FS)

FS is the change in the value of a

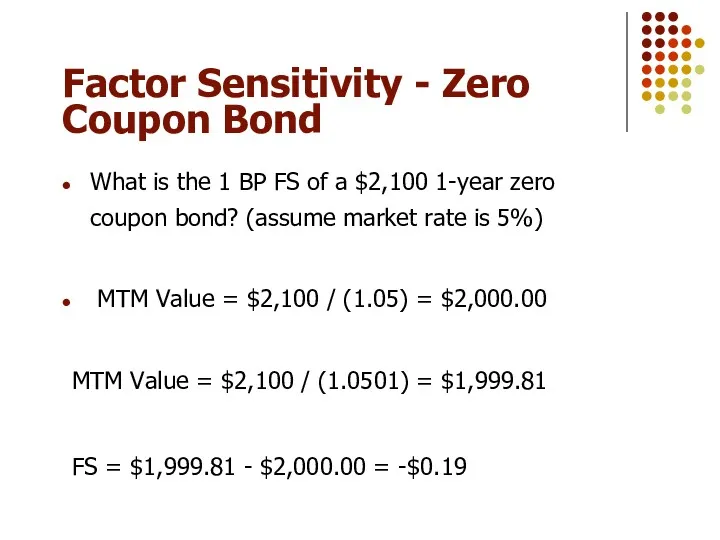

Factor Sensitivity - Zero Coupon Bond

What is the 1 BP FS

Factor Sensitivity - Zero Coupon Bond

What is the 1 BP FS

Market Volatility

Volatility is a measure of the dispersion of a market

Market Volatility

Volatility is a measure of the dispersion of a market

Estimating Volatility

1. Historical data analysis

2. Judgmental

3. Implied (from options

Estimating Volatility

1. Historical data analysis

2. Judgmental

3. Implied (from options

Defeasance period

This is defined as the time elapsed (normally expressed in

Defeasance period

This is defined as the time elapsed (normally expressed in

Defeasance Factor (DF)

DF is the total volatility over the defeasance period

On

Defeasance Factor (DF)

DF is the total volatility over the defeasance period

On

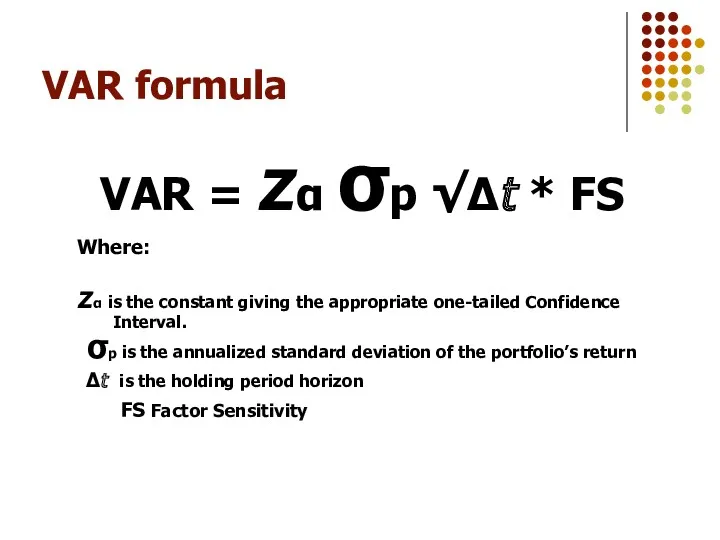

VAR formula

VAR = zα σp √Δt * FS

Where:

zα is the constant

VAR formula

VAR = zα σp √Δt * FS

Where:

zα is the constant

VAR

Daily P&L

VAR

VAR

Daily P&L

VAR

III VALUE AT RISK - CALCULATIONS

III VALUE AT RISK - CALCULATIONS

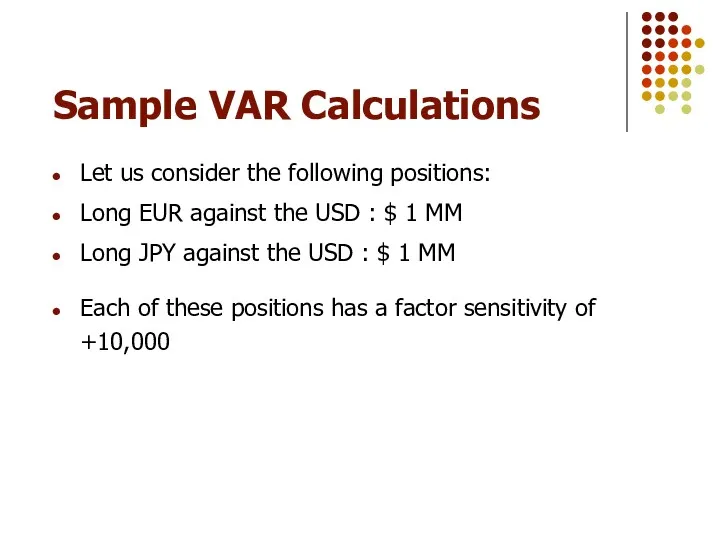

Sample VAR Calculations

Let us consider the following positions:

Long EUR against the

Sample VAR Calculations

Let us consider the following positions:

Long EUR against the

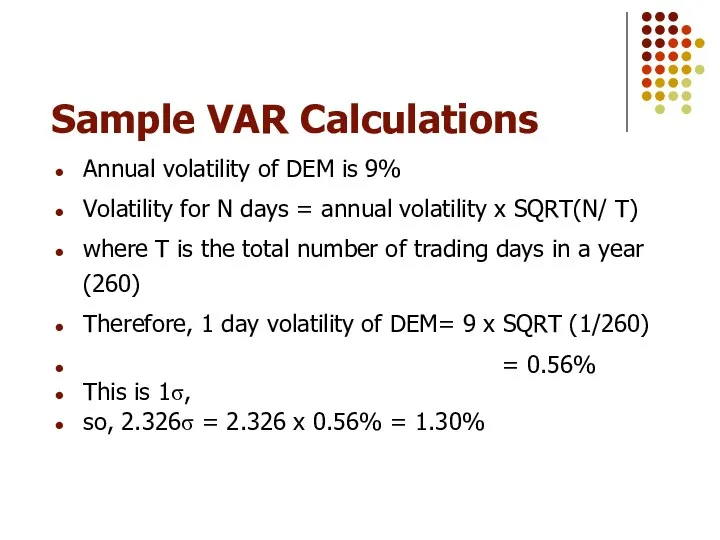

Sample VAR Calculations

Annual volatility of DEM is 9%

Volatility for N days

Sample VAR Calculations

Annual volatility of DEM is 9%

Volatility for N days

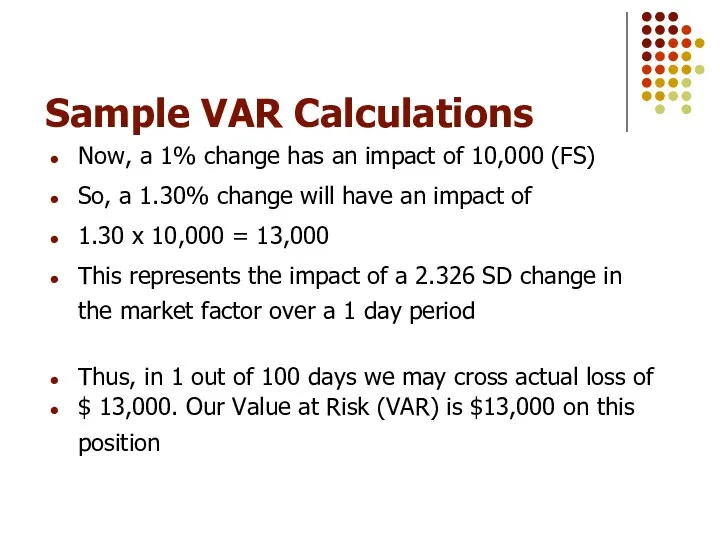

Sample VAR Calculations

Now, a 1% change has an impact of 10,000

Sample VAR Calculations

Now, a 1% change has an impact of 10,000

Sample VAR Calculations

Similarly, for JPY, the annual volatility is 12%

The 1

Sample VAR Calculations

Similarly, for JPY, the annual volatility is 12%

The 1

IV VALUE AT RISK FOR CORPORATIONS

IV VALUE AT RISK FOR CORPORATIONS

VAR FOR CORPORATIONS

Trading portfolios

Longer time horizons for close outs

VAR FOR CORPORATIONS

Trading portfolios

Longer time horizons for close outs

VAR FOR CORPORATIONS

Identify market variables impacting business

Map income

VAR FOR CORPORATIONS

Identify market variables impacting business

Map income

VAR FOR CORPORATIONS

Hedging tools

Forward FX

Currency swaps

Interest

VAR FOR CORPORATIONS

Hedging tools

Forward FX

Currency swaps

Interest

V VALUE AT RISK- A FEW COMMENTS

V VALUE AT RISK- A FEW COMMENTS

Significance of VAR

Applicable mainly to trading portfolios

Regulatory capital requirements

Significance of VAR

Applicable mainly to trading portfolios

Regulatory capital requirements

VAR : A Few Comments

VAR does not represent the maximum loss

VAR

VAR : A Few Comments

VAR does not represent the maximum loss

VAR

Where to use VAR?

Macro measure. High level monitoring, managing, eg. Regional

Where to use VAR?

Macro measure. High level monitoring, managing, eg. Regional

How to use Var

Stress Testing : * “worst case” scenario

*

How to use Var

Stress Testing : * “worst case” scenario

*

General Market Risk Issues

Integrity - Rate Reasonability

- At Inception

General Market Risk Issues

Integrity - Rate Reasonability

- At Inception

Семейный бюджет

Семейный бюджет Финансы. Задачи. Тема 1

Финансы. Задачи. Тема 1 Деловая игра Налогообложение граждан

Деловая игра Налогообложение граждан Ең төменгі жалақы және кедейлер

Ең төменгі жалақы және кедейлер Деньги и их функции

Деньги и их функции Учет сырья, продуктов и тары в кладовых п о п

Учет сырья, продуктов и тары в кладовых п о п Внешнеторговые документарные операции (2)

Внешнеторговые документарные операции (2) Инвестиции и методы финансирования

Инвестиции и методы финансирования Центральный банк и его роль в банковской системе

Центральный банк и его роль в банковской системе Перевод работников АО Красная звезда на новые условия оплаты труда

Перевод работников АО Красная звезда на новые условия оплаты труда Муниципальное образование город Алапаевск. Бюджет для граждан

Муниципальное образование город Алапаевск. Бюджет для граждан Інформаційне забезпечення фінансового аналізу. Лекція 2

Інформаційне забезпечення фінансового аналізу. Лекція 2 Страховой рынок и его структура

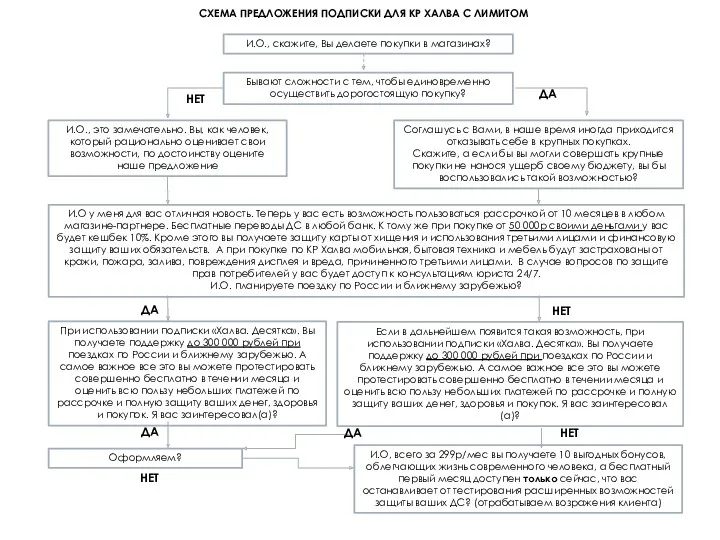

Страховой рынок и его структура Схема предложения подписки Халва. Десятка

Схема предложения подписки Халва. Десятка Учет в бюджетных учреждениях

Учет в бюджетных учреждениях Бюджетирование проектов. (Лекция 7)

Бюджетирование проектов. (Лекция 7) Составление смет на пусконаладочные работы

Составление смет на пусконаладочные работы Оценка целостных имущественных комплексов

Оценка целостных имущественных комплексов Бухгалтерлік есеп нысандары

Бухгалтерлік есеп нысандары Виды кредитов

Виды кредитов Портфель финансовых активов

Портфель финансовых активов Денежный оборот и его структура

Денежный оборот и его структура Налоговая и бухгалтерская отчетность садоводческих товариществ

Налоговая и бухгалтерская отчетность садоводческих товариществ Бухгалтерский Учет кредитов и займов

Бухгалтерский Учет кредитов и займов Выручка. Международные стандарты финансовой отчётности (МСФО 18)

Выручка. Международные стандарты финансовой отчётности (МСФО 18) Страховой надзор

Страховой надзор Международные ценные бумаги. Эффективная система внешних заимствований. Тема 5

Международные ценные бумаги. Эффективная система внешних заимствований. Тема 5 Фінансові інвестиції

Фінансові інвестиції