- Risk management approaches

Содержание

- 2. Risk Risk can be defined as the combination of the probability of an event and its

- 3. Risk Management Risk Management is increasingly recognised as being concerned with both positive and negative aspects

- 4. Risk Management Risk management is a central part of any organisation’s strategic management. It is the

- 5. Risk Management The focus of good risk management is the identification and treatment of these risks.

- 6. Risk Management It increases the probability of success, and reduces both the probability of failure and

- 7. Risk Management It must be integrated into the culture of the organisation with an effective policy

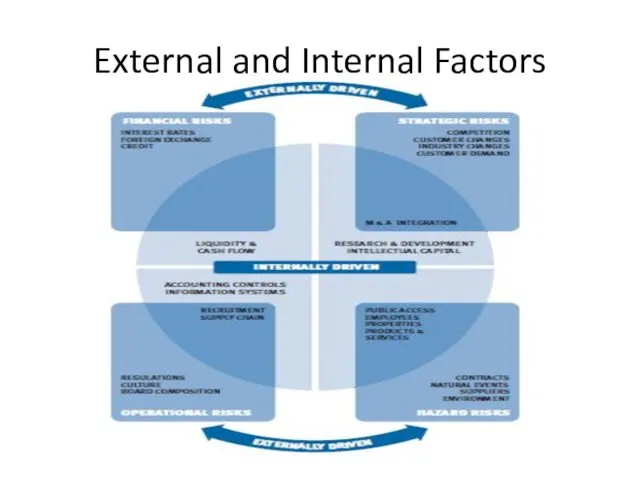

- 8. External and Internal Factors The risks facing an organisation and its operations can result from factors

- 9. External and Internal Factors

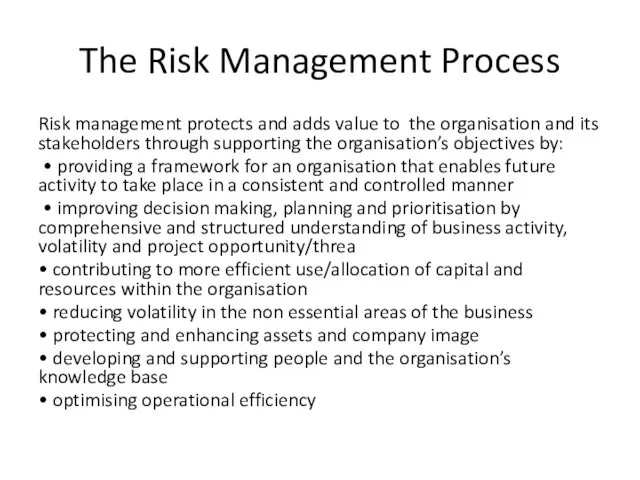

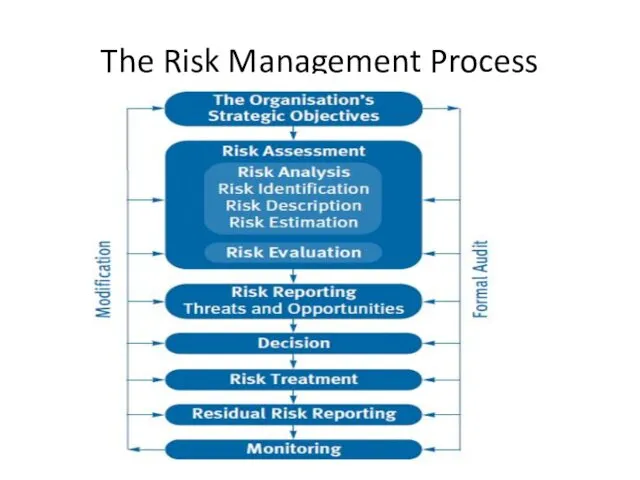

- 10. The Risk Management Process Risk management protects and adds value to the organisation and its stakeholders

- 11. The Risk Management Process

- 12. Risk Assessment Risk Assessment is defined by the ISO/ IEC Guide 73 as the overall process

- 13. Risk Analysis Risk identification sets out to identify an organisation’s exposure to uncertainty. This requires an

- 14. Risk identification should be approached in a methodical way to ensure that all significant activities within

- 15. All associated volatility related to these activities should be identified and categorised. • Financial - These

- 16. Knowledge management - These concern the effective management and control of the knowledge resources, the production,

- 17. Compliance - These concern such issues as health & safety, environmental, trade descriptions, consumer protection, data

- 18. Whilst risk identification can be carried out by outside consultants, an in-house approach with well communicated,

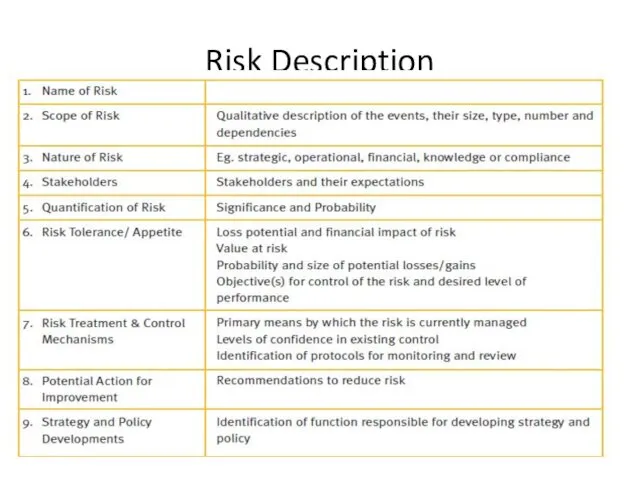

- 19. Risk Description The objective of risk description is to display the identified risks in a structured

- 20. Risk Description By considering the consequence and probability of each of the risks set out in

- 21. Risk Description

- 22. Risk Estimation Monitoring Risk estimation can be quantitative, semiquantitative or qualitative in terms of the probability

- 23. Consequences - Both Threats and Opportunities

- 24. Probability of Occurrence - Threats

- 25. Probability of Occurrence - Opportunities

- 26. Risk Analysis methods and techniques A range of techniques can be used to analyse risks. These

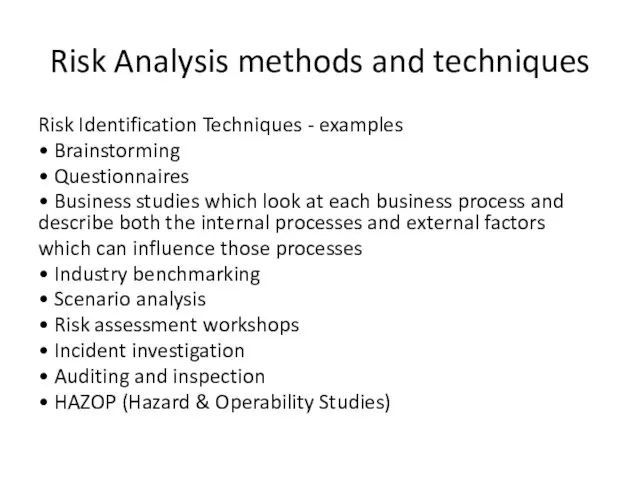

- 27. Risk Analysis methods and techniques Risk Identification Techniques - examples • Brainstorming • Questionnaires • Business

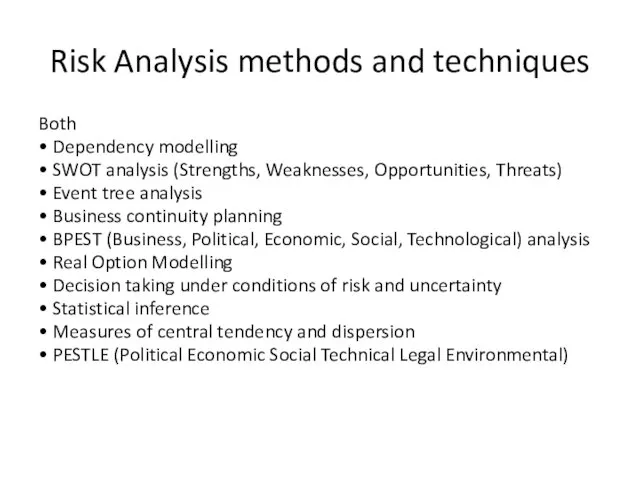

- 28. Risk Analysis methods and techniques Both • Dependency modelling • SWOT analysis (Strengths, Weaknesses, Opportunities, Threats)

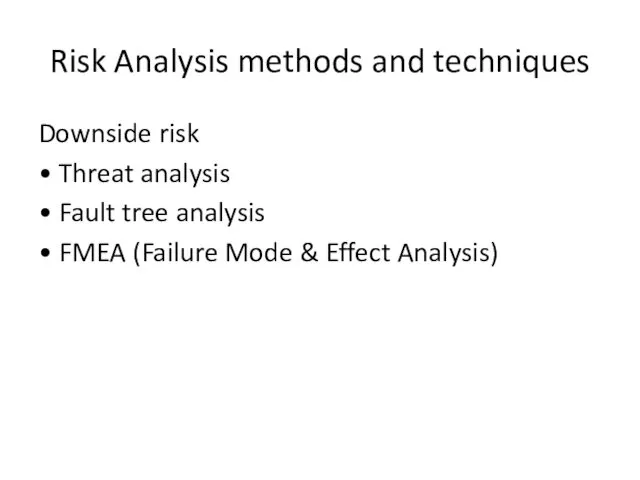

- 29. Risk Analysis methods and techniques Downside risk • Threat analysis • Fault tree analysis • FMEA

- 30. Risk Profile The result of the risk analysis process can be used to produce a risk

- 31. Risk Profile This process allows the risk to be mapped to the business area affected, describes

- 32. Risk Evaluation When the risk analysis process has been completed, it is necessary to compare the

- 33. Risk Treatment Risk treatment is the process of selecting and implementing measures to modify the risk.

- 34. Risk Treatment Any system of risk treatment should provide as a minimum: • effective and efficient

- 35. Risk Treatment The risk analysis process assists the effective and efficient operation of the organisation by

- 36. Risk Treatment Effectiveness of internal control is the degree to which the risk will either be

- 37. Risk Treatment The proposed controls need to be measured in terms of potential economic effect if

- 38. Risk Treatment Firstly, the cost of implementation has to be established. This has to be calculated

- 39. Risk Treatment Compliance with laws and regulations is not an option. An organisation must understand the

- 40. Risk Treatment One method of obtaining financial protection against the impact of risks is through risk

- 41. Risk Reporting and Communication Internal Reporting Different levels within an organisation need different information from the

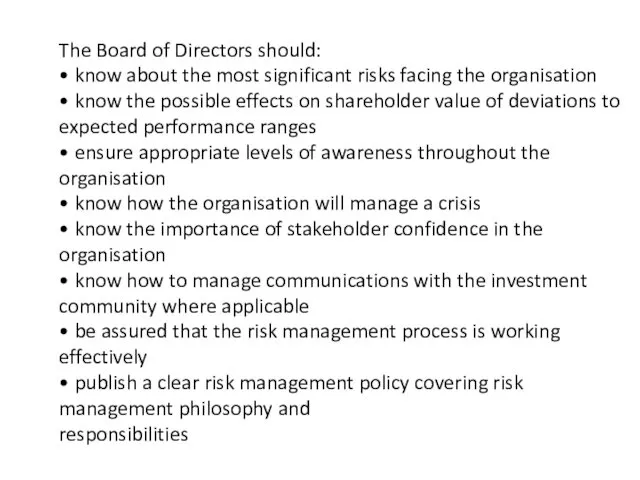

- 42. The Board of Directors should: • know about the most significant risks facing the organisation •

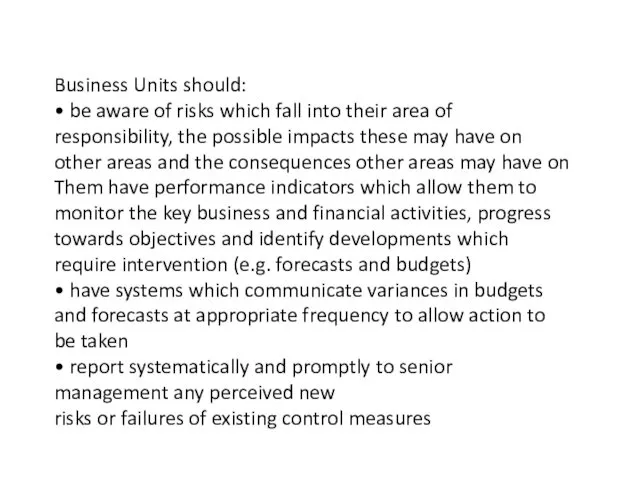

- 43. Business Units should: • be aware of risks which fall into their area of responsibility, the

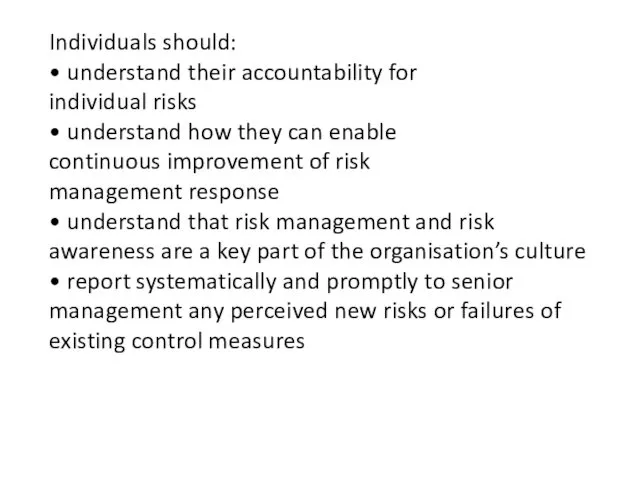

- 44. Individuals should: • understand their accountability for individual risks • understand how they can enable continuous

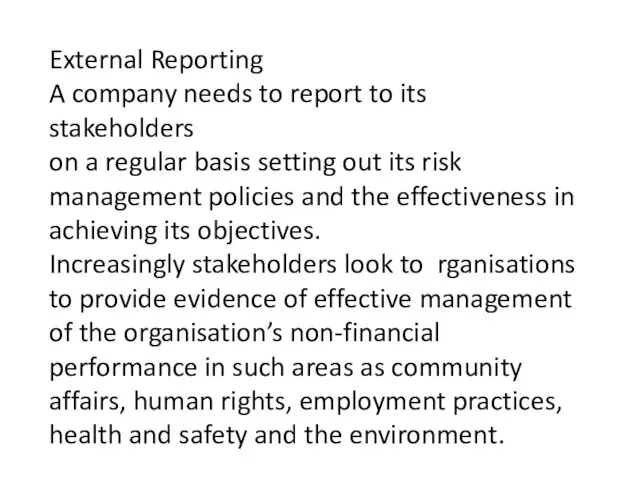

- 45. External Reporting A company needs to report to its stakeholders on a regular basis setting out

- 46. Good corporate governance requires that companies adopt a methodical approach to risk management which: • protects

- 47. The formal reporting should address: • the control methods – particularly management responsibilities for risk management

- 48. The Structure and Administration of Risk Management Furthermore, it should refer to any legal requirements for

- 49. The Structure and Administration of Risk Management Role of the Board The Board has responsibility for

- 50. The Structure and Administration of Risk Management Role of the Business Units This includes the following:

- 51. Role of the Risk Management Function Depending on the size of the organisation the risk management

- 52. • establishing internal risk policy and structures for business units • designing and reviewing processes for

- 53. Role of Internal Audit The role of Internal Audit is likely to differ from one organisation

- 54. In determining the most appropriate role for a particular organisation, Internal Audit should ensure that the

- 55. Resources and Implementation The resources required to implement the organisation’s risk management policy should be clearly

- 56. Resources and Implementation Risk management should be embedded within the organisation through the strategy and budget

- 57. Monitoring and Review of the Risk Management Process. Effective risk management requires a reporting and review

- 58. Monitoring and Review of the Risk Management Process. The monitoring process should provide assurance that there

- 59. Monitoring and Review of the Risk Management Process. Any monitoring and review process should also determine

- 61. Скачать презентацию

Risk

Risk can be defined as the combination of the

probability of an

Risk

Risk can be defined as the combination of the

probability of an

Risk Management

Risk Management is increasingly recognised as

being concerned with both positive

Risk Management

Risk Management is increasingly recognised as

being concerned with both positive

Risk Management

Risk management is a central part of any

organisation’s strategic management.

Risk Management

Risk management is a central part of any

organisation’s strategic management.

Risk Management

The focus of good risk management is the

identification and treatment

Risk Management

The focus of good risk management is the

identification and treatment

Risk Management

It increases the probability of success, and reduces both the

Risk Management

It increases the probability of success, and reduces both the

Risk Management

It must be integrated into the culture of the organisation

Risk Management

It must be integrated into the culture of the organisation

External and Internal Factors

The risks facing an organisation and its operations

External and Internal Factors

The risks facing an organisation and its operations

External and Internal Factors

External and Internal Factors

The Risk Management Process

Risk management protects and adds value to the

The Risk Management Process

Risk management protects and adds value to the

The Risk Management Process

The Risk Management Process

Risk Assessment

Risk Assessment is defined by the ISO/ IEC

Guide 73 as

Risk Assessment

Risk Assessment is defined by the ISO/ IEC

Guide 73 as

Risk Analysis

Risk identification sets out to identify an organisation’s exposure to

Risk Analysis

Risk identification sets out to identify an organisation’s exposure to

Risk identification should be approached in a

methodical way to ensure that

Risk identification should be approached in a

methodical way to ensure that

All associated volatility related to these

activities should be identified and categorised.

•

All associated volatility related to these

activities should be identified and categorised.

•

Knowledge management - These concern the effective management and control of

Knowledge management - These concern the effective management and control of

Compliance - These concern such issues as

health & safety, environmental, trade

descriptions,

Compliance - These concern such issues as

health & safety, environmental, trade

descriptions,

Whilst risk identification can be carried out by

outside consultants, an in-house

Whilst risk identification can be carried out by

outside consultants, an in-house

Risk Description

The objective of risk description is to display

the identified risks

Risk Description

The objective of risk description is to display

the identified risks

Risk Description

By considering the consequence and probability of

each of the risks

Risk Description

By considering the consequence and probability of

each of the risks

Risk Description

Risk Description

Risk Estimation Monitoring

Risk estimation can be quantitative, semiquantitative or qualitative in

Risk Estimation Monitoring

Risk estimation can be quantitative, semiquantitative or qualitative in

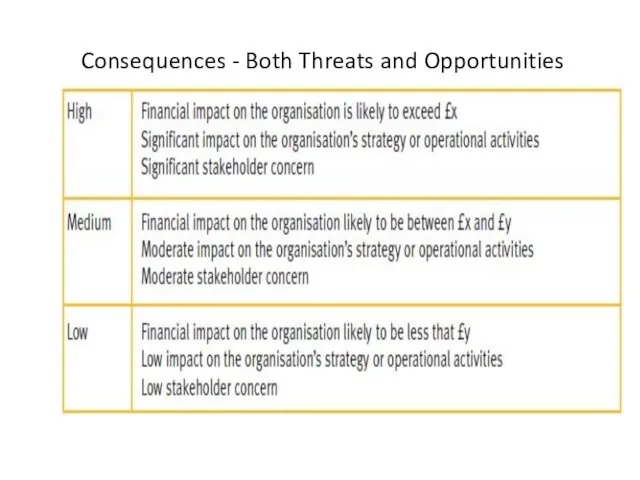

Consequences - Both Threats and Opportunities

Consequences - Both Threats and Opportunities

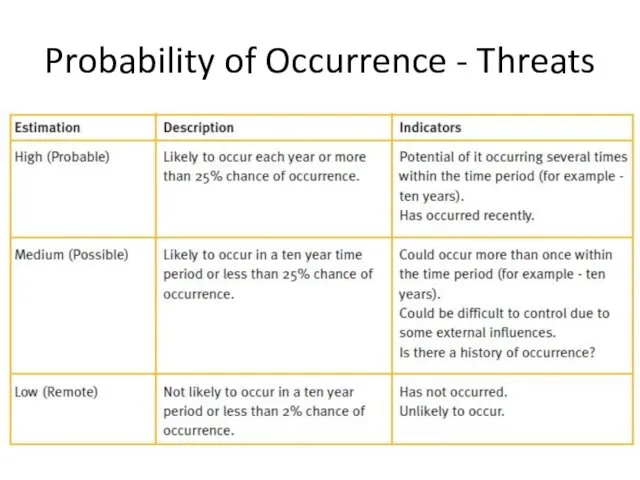

Probability of Occurrence - Threats

Probability of Occurrence - Threats

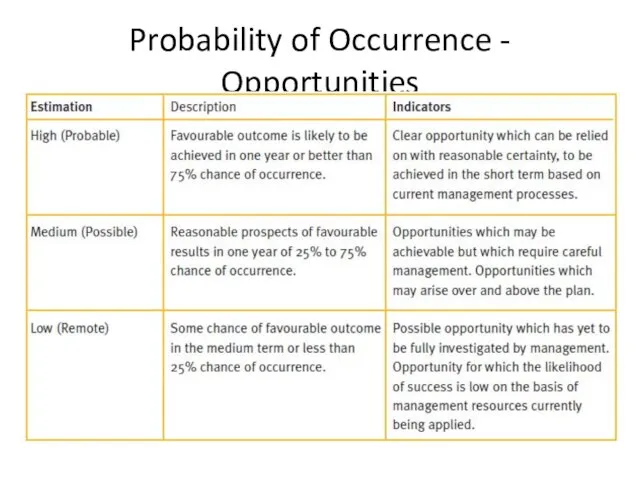

Probability of Occurrence - Opportunities

Probability of Occurrence - Opportunities

Risk Analysis methods and techniques

A range of techniques can be used

Risk Analysis methods and techniques

A range of techniques can be used

Risk Analysis methods and techniques

Risk Identification Techniques - examples

• Brainstorming

• Questionnaires

•

Risk Analysis methods and techniques

Risk Identification Techniques - examples

• Brainstorming

• Questionnaires

•

Risk Analysis methods and techniques

Both

• Dependency modelling

• SWOT analysis (Strengths, Weaknesses,

Risk Analysis methods and techniques

Both

• Dependency modelling

• SWOT analysis (Strengths, Weaknesses,

Risk Analysis methods and techniques

Downside risk

• Threat analysis

• Fault tree analysis

•

Risk Analysis methods and techniques

Downside risk

• Threat analysis

• Fault tree analysis

•

Risk Profile

The result of the risk analysis process can be

used to

Risk Profile

The result of the risk analysis process can be

used to

Risk Profile

This process allows the risk to be mapped to

the business

Risk Profile

This process allows the risk to be mapped to

the business

Risk Evaluation

When the risk analysis process has been completed, it is

Risk Evaluation

When the risk analysis process has been completed, it is

Risk Treatment

Risk treatment is the process of selecting and

implementing measures to

Risk Treatment

Risk treatment is the process of selecting and

implementing measures to

Risk Treatment

Any system of risk treatment should provide as

a minimum:

• effective

Risk Treatment

Any system of risk treatment should provide as

a minimum:

• effective

Risk Treatment

The risk analysis process assists the effective

and efficient operation of

Risk Treatment

The risk analysis process assists the effective

and efficient operation of

Risk Treatment

Effectiveness of internal control is the degree

to which the risk

Risk Treatment

Effectiveness of internal control is the degree

to which the risk

Risk Treatment

The proposed controls need to be measured in

terms of potential

Risk Treatment

The proposed controls need to be measured in

terms of potential

Risk Treatment

Firstly, the cost of implementation has to be

established. This has

Risk Treatment

Firstly, the cost of implementation has to be

established. This has

Risk Treatment

Compliance with laws and regulations is not an

option. An organisation

Risk Treatment

Compliance with laws and regulations is not an

option. An organisation

Risk Treatment

One method of obtaining financial protection

against the impact of risks

Risk Treatment

One method of obtaining financial protection

against the impact of risks

Risk Reporting and

Communication

Internal Reporting

Different levels within an organisation need

different information from

Risk Reporting and

Communication

Internal Reporting

Different levels within an organisation need

different information from

The Board of Directors should:

• know about the most significant risks

The Board of Directors should:

• know about the most significant risks

Business Units should:

• be aware of risks which fall into their

Business Units should:

• be aware of risks which fall into their

Individuals should:

• understand their accountability for

individual risks

• understand how they can

Individuals should:

• understand their accountability for

individual risks

• understand how they can

External Reporting

A company needs to report to its stakeholders

on a regular

External Reporting

A company needs to report to its stakeholders

on a regular

Good corporate governance requires that companies adopt a methodical approach to

Good corporate governance requires that companies adopt a methodical approach to

The formal reporting should address:

• the control methods – particularly management

The formal reporting should address:

• the control methods – particularly management

The Structure and Administration of Risk

Management

Furthermore, it should refer to any

The Structure and Administration of Risk

Management

Furthermore, it should refer to any

The Structure and Administration of Risk Management

Role of the Board

The Board

The Structure and Administration of Risk Management

Role of the Board

The Board

The Structure and Administration of Risk Management

Role of the Business Units

This

The Structure and Administration of Risk Management

Role of the Business Units

This

Role of the Risk Management Function

Depending on the size of the

Role of the Risk Management Function

Depending on the size of the

• establishing internal risk policy and structures for business units

• designing

• establishing internal risk policy and structures for business units

• designing

Role of Internal Audit

The role of Internal Audit is likely to

Role of Internal Audit

The role of Internal Audit is likely to

In determining the most appropriate role for a

particular organisation, Internal Audit

In determining the most appropriate role for a

particular organisation, Internal Audit

Resources and Implementation

The resources required to implement the organisation’s risk management

Resources and Implementation

The resources required to implement the organisation’s risk management

Resources and Implementation

Risk management should be embedded within

the organisation through the

Resources and Implementation

Risk management should be embedded within

the organisation through the

Monitoring and Review of the

Risk Management Process.

Effective risk management requires a

Monitoring and Review of the

Risk Management Process.

Effective risk management requires a

Monitoring and Review of the

Risk Management Process.

The monitoring process should provide

assurance

Monitoring and Review of the

Risk Management Process.

The monitoring process should provide

assurance

Monitoring and Review of the

Risk Management Process.

Any monitoring and review process

Monitoring and Review of the

Risk Management Process.

Any monitoring and review process

Управління екологічними ризиками в умовах підприємства “Хлібний дар”

Управління екологічними ризиками в умовах підприємства “Хлібний дар” Auditing & assurance. Introduction to course

Auditing & assurance. Introduction to course Навыки медицинского представителя. Тренинг

Навыки медицинского представителя. Тренинг Управление проектами. Стадии управления проектами

Управление проектами. Стадии управления проектами Статистические методы

Статистические методы Антикризова складова в системі управління промисловим підприємством

Антикризова складова в системі управління промисловим підприємством Международные тарифы на рынке мультимодальных перевозок

Международные тарифы на рынке мультимодальных перевозок Личность и коллектив как объект управления

Личность и коллектив как объект управления Система менеджмента качества

Система менеджмента качества Понятие, цели и этапы деловой оценки персонала

Понятие, цели и этапы деловой оценки персонала Знакомство с Agile

Знакомство с Agile Принятие решений в логике концепции обучающихся организаций. (Лекция 8)

Принятие решений в логике концепции обучающихся организаций. (Лекция 8) Проектирование бренда. Кафе Кошкин хвост

Проектирование бренда. Кафе Кошкин хвост Раздаточный материал к ВКР: Разработка и реализация стратегии развития предприятия

Раздаточный материал к ВКР: Разработка и реализация стратегии развития предприятия Разработка системы управления проектом, на основе программного комплекса MS Project

Разработка системы управления проектом, на основе программного комплекса MS Project Қоймадағы логистикалық процесстер. Түрлері, функциялары және қоймалардың жіктелуі

Қоймадағы логистикалық процесстер. Түрлері, функциялары және қоймалардың жіктелуі Памятка кандидату от ПАО РКК Энергия

Памятка кандидату от ПАО РКК Энергия Job search strategies

Job search strategies Internal control and deontology - Chapter 6 D. Human Resources

Internal control and deontology - Chapter 6 D. Human Resources Көтерме сауда қоймасындағы жүк өндеу материалдық ағынның үлгілеу барысы

Көтерме сауда қоймасындағы жүк өндеу материалдық ағынның үлгілеу барысы Лекция 2. Транспортное обслуживание

Лекция 2. Транспортное обслуживание Теории управления персоналом

Теории управления персоналом Планирование хозяйственной деятельности предприятия индустрии гостеприимства

Планирование хозяйственной деятельности предприятия индустрии гостеприимства Тайм-менеджмент / Самоменеджмент

Тайм-менеджмент / Самоменеджмент Kierowanie i motywowanie

Kierowanie i motywowanie договор морской перевозки груза

договор морской перевозки груза Project risk management

Project risk management El sistema constitucional argentino, los rasgos relevantes

El sistema constitucional argentino, los rasgos relevantes