- Credit Risk Measurement Introduction GFIR

Содержание

- 2. Risk introduction Introduce risk-adjusted capital concepts Describe components of credit risk measurement

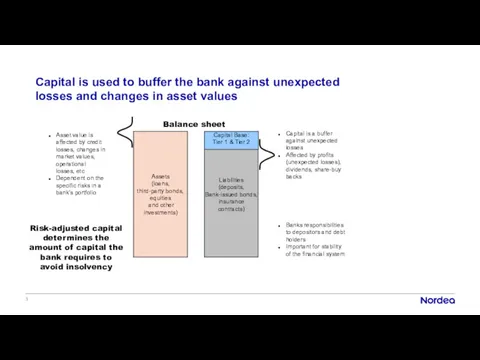

- 3. Capital is used to buffer the bank against unexpected losses and changes in asset values Assets

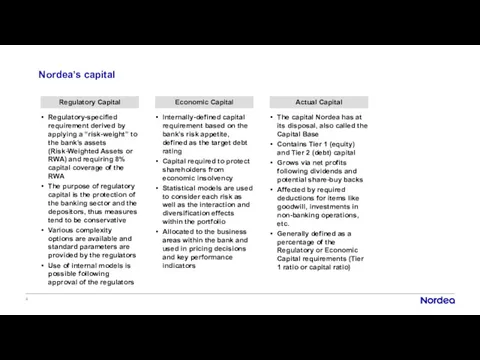

- 4. Regulatory-specified requirement derived by applying a “risk-weight” to the bank’s assets (Risk-Weighted Assets or RWA) and

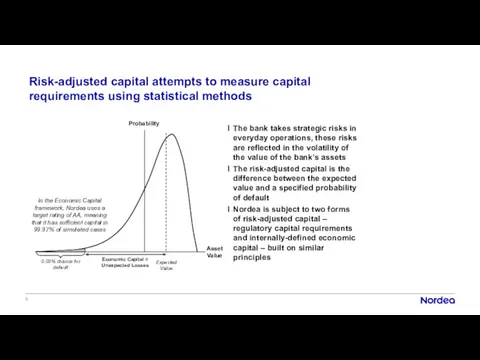

- 5. The bank takes strategic risks in everyday operations, these risks are reflected in the volatility of

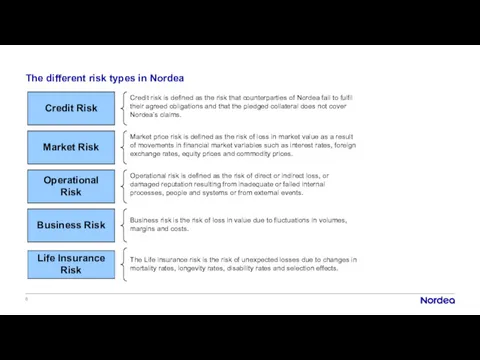

- 6. The different risk types in Nordea Business Risk Operational Risk Market Risk Credit Risk Life Insurance

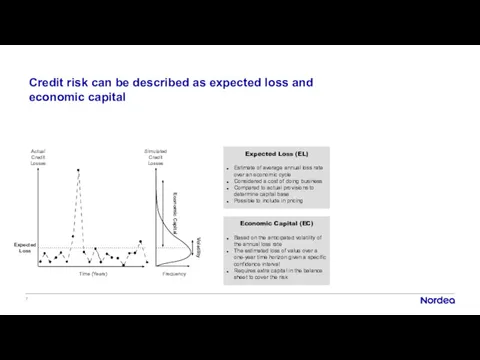

- 7. Economic Capital (EC) Based on the anticipated volatility of the annual loss rate The estimated loss

- 8. X X PD (%) Probability of default = What is the likelihood that a customer will

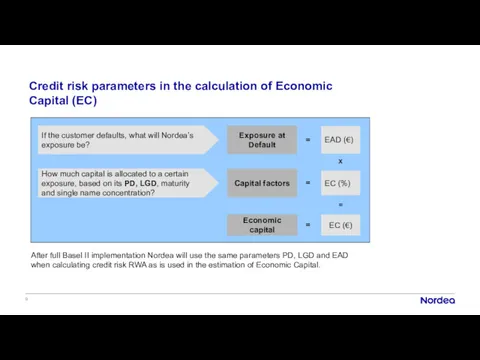

- 9. Exposure at Default EC (%) EAD (€) = = X Economic capital EC (€) = =

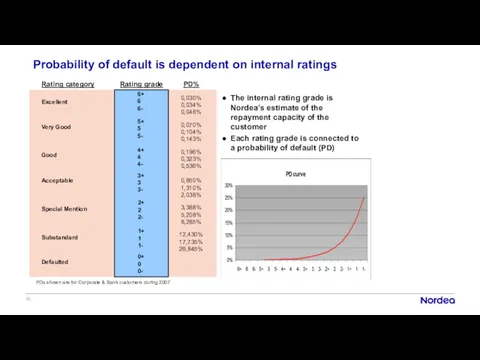

- 10. Rating grade Rating category PD% 0,030% 0,034% 0,048% 0,070% 0,104% 0,143% 0,196% 0,323% 0,536% 0,850% 1,310%

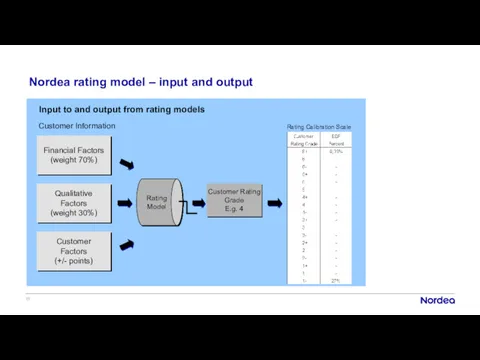

- 11. Financial Factors (weight 70%) Customer Information Rating Model Customer Rating Grade E.g. 4 Rating Calibration Scale

- 12. Loss given default is the percent of exposure lost in the event of customer default Loss

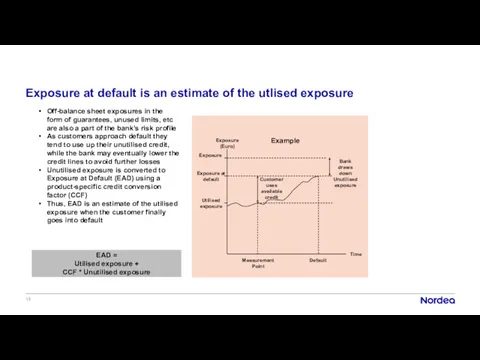

- 13. Exposure (Euro) Exposure Time Default Measurement Point Utilised exposure Customer uses available credit Bank draws down

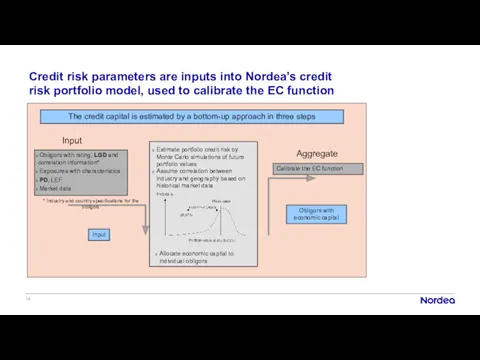

- 14. Credit risk parameters are inputs into Nordea’s credit risk portfolio model, used to calibrate the EC

- 15. Credit risk formulas Basel Capital for Corporates and Institutions Basel formula for Corporates and Institutions is

- 17. Скачать презентацию

Risk introduction

Introduce risk-adjusted capital concepts

Describe components of credit risk measurement

Risk introduction

Introduce risk-adjusted capital concepts

Describe components of credit risk measurement

Capital is used to buffer the bank against unexpected losses and

Capital is used to buffer the bank against unexpected losses and

Regulatory-specified requirement derived by applying a “risk-weight” to the bank’s assets

Regulatory-specified requirement derived by applying a “risk-weight” to the bank’s assets

The bank takes strategic risks in everyday operations, these risks are

The bank takes strategic risks in everyday operations, these risks are

The different risk types in Nordea

Business Risk

Operational Risk

Market Risk

Credit Risk

Life Insurance

The different risk types in Nordea

Business Risk

Operational Risk

Market Risk

Credit Risk

Life Insurance

Economic Capital (EC)

Based on the anticipated volatility of the annual loss

Economic Capital (EC)

Based on the anticipated volatility of the annual loss

X

X

PD (%)

Probability of default

=

What is the likelihood that a customer

X

X

PD (%)

Probability of default

=

What is the likelihood that a customer

Exposure at Default

EC (%)

EAD (€)

=

=

X

Economic capital

EC (€)

=

=

Capital factors

How much capital is

Exposure at Default

EC (%)

EAD (€)

=

=

X

Economic capital

EC (€)

=

=

Capital factors

How much capital is

Rating grade

Rating category

PD%

0,030%

0,034%

0,048%

0,070%

0,104%

0,143%

0,196%

0,323%

0,536%

0,850%

1,310%

2,038%

3,388%

5,208%

8,285%

12,430%

17,735%

26,845%

Excellent

Very Good

Good

Acceptable

Special Mention

Substandard

Defaulted

6+

6

6-

5+

5

5-

4+

4

4-

3+

3

3-

2+

2

2-

0+

0

0-

1+

1

1-

Probability of default is

Rating grade

Rating category

PD%

0,030%

0,034%

0,048%

0,070%

0,104%

0,143%

0,196%

0,323%

0,536%

0,850%

1,310%

2,038%

3,388%

5,208%

8,285%

12,430%

17,735%

26,845%

Excellent

Very Good

Good

Acceptable

Special Mention

Substandard

Defaulted

6+

6

6-

5+

5

5-

4+

4

4-

3+

3

3-

2+

2

2-

0+

0

0-

1+

1

1-

Probability of default is

Financial Factors

(weight 70%)

Customer Information

Rating

Model

Customer Rating Grade

E.g. 4

Rating Calibration Scale

Qualitative

Factors

(weight 30%)

Customer

Factors

(+/- points)

Input

Financial Factors

(weight 70%)

Customer Information

Rating

Model

Customer Rating Grade

E.g. 4

Rating Calibration Scale

Qualitative

Factors

(weight 30%)

Customer

Factors

(+/- points)

Input

Loss given default is the percent of exposure lost in the

Loss given default is the percent of exposure lost in the

Exposure (Euro)

Exposure

Time

Default

Measurement Point

Utilised exposure

Customer uses available credit

Bank draws down Unutilised exposure

Example

Exposure

Exposure (Euro)

Exposure

Time

Default

Measurement Point

Utilised exposure

Customer uses available credit

Bank draws down Unutilised exposure

Example

Exposure

Credit risk parameters are inputs into Nordea’s credit risk portfolio model,

Credit risk parameters are inputs into Nordea’s credit risk portfolio model,

Credit risk formulas

Basel Capital for Corporates and Institutions

Basel formula for Corporates

Credit risk formulas

Basel Capital for Corporates and Institutions

Basel formula for Corporates

Показатели ликвидности

Показатели ликвидности Кредитный договор

Кредитный договор Управление портфелем ценных бумаг

Управление портфелем ценных бумаг Материально-техническая база заготовок. Модуль 7

Материально-техническая база заготовок. Модуль 7 Фiнансовi iнструменти. Фінансовий інжиніринг

Фiнансовi iнструменти. Фінансовий інжиніринг Basic financial statements

Basic financial statements Базисные условия поставки. Инкотермс-2010

Базисные условия поставки. Инкотермс-2010 Денежно-кредитная система и монетарная политика государства

Денежно-кредитная система и монетарная политика государства Счетная палата РФ

Счетная палата РФ Учет материалов на счете 10

Учет материалов на счете 10 Мемлекеттің инвестициялық саясаты. Инвестициялық климат

Мемлекеттің инвестициялық саясаты. Инвестициялық климат Налоговый контроль

Налоговый контроль Основы технического анализа

Основы технического анализа Методы финансового анализа

Методы финансового анализа О состоянии финансового сектора Калининградской области

О состоянии финансового сектора Калининградской области Валютная политика и ее инструменты

Валютная политика и ее инструменты Бухгалтерский учет расчетов с поставщиками и покупателями

Бухгалтерский учет расчетов с поставщиками и покупателями Оценка объектов интеллектуальной собственности

Оценка объектов интеллектуальной собственности Финансы как экономическая категория. Тема 1

Финансы как экономическая категория. Тема 1 Бизнес план. Кафе быстрого обслуживания Hard Rock

Бизнес план. Кафе быстрого обслуживания Hard Rock Финансовый анализ. Формулировка понятия. Факторы и факторный анализ. Этапы и цели

Финансовый анализ. Формулировка понятия. Факторы и факторный анализ. Этапы и цели Фондовая биржа и ее экономический механизм

Фондовая биржа и ее экономический механизм Денежный рынок. Тема 3

Денежный рынок. Тема 3 Fundraising

Fundraising Понятие корпоротивной социальной ответсвенности. Генезис концепции КСО

Понятие корпоротивной социальной ответсвенности. Генезис концепции КСО Инициативное бюджетирование

Инициативное бюджетирование Цілі, задання, принципи бюджетної політики

Цілі, задання, принципи бюджетної політики Правовое регулирование и учёт нематериальных активов

Правовое регулирование и учёт нематериальных активов