- Financial basics

Содержание

- 2. COPYRIGHT/PERMISSION TO REPRODUCE The Financial Basics workshop materials are covered by the provisions of the Copyright

- 3. INTRODUCTION

- 4. How to manage your spending and prepare a realistic budget. Ways to save. How to manage

- 5. Control your financial future. Achieve your life goals. Provide for yourself and your family. Be a

- 6. The current average percentage of their income that Canadians save is: a) 5% b) 7.5% c)

- 7. In 2010, the average household debt of Canadians was: a) $26,000 b) $56,000 c) $96,000 INTRODUCTION

- 8. In 2009, the total reported dollar loss by victims of identity theft in Canada was about:

- 9. In 2009, the average debt: For college graduates was: $3,500 $8,500 $13,500 For a university graduates

- 10. The percentage of Canadian youth whose parents are not expected to contribute any savings to their

- 11. BUDGETING

- 12. Income Expenses Difference between the two: surplus or deficit Parts of a budget BUDGETING

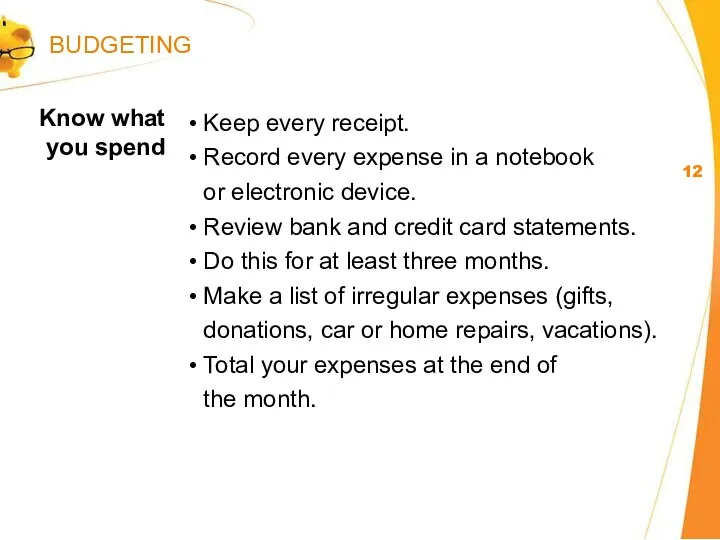

- 13. Keep every receipt. Record every expense in a notebook or electronic device. Review bank and credit

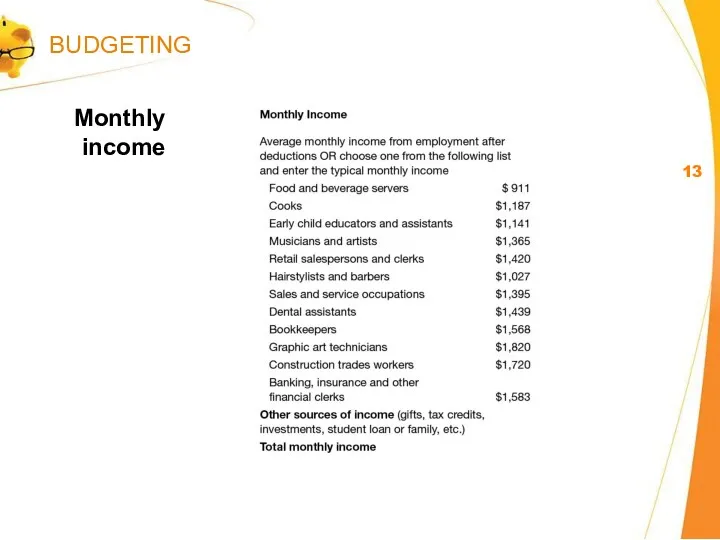

- 14. Monthly income BUDGETING

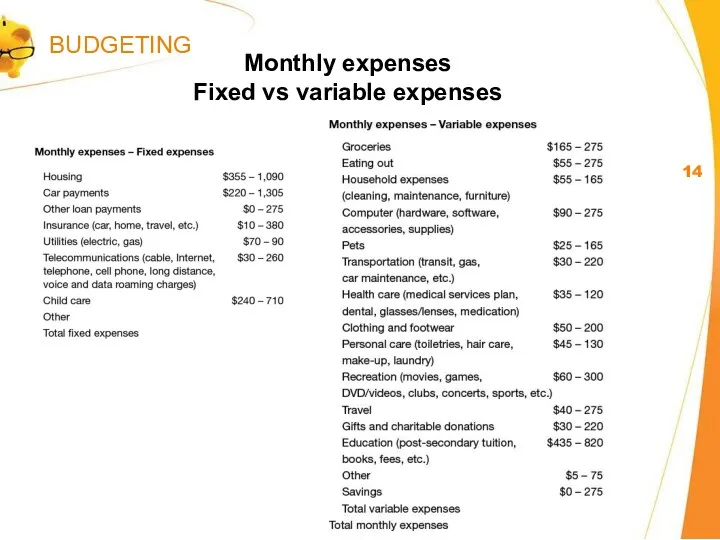

- 15. Monthly expenses Fixed vs variable expenses BUDGETING

- 16. Difference between total monthly income and total monthly expenses = Net surplus _______________ OR Net deficit

- 17. MANAGING YOUR COST OF LIVING – BE A SMART CONSUMER

- 18. Check your bills. Negotiate better plans (banking fees and services, telephone, cell phone). Pack a lunch.

- 19. Spot mistakes and overcharges. Pay less in late fees, interest and penalties. Get errors corrected before

- 20. Call each service provider and ask: • How can I cut back my monthly bills? •

- 21. What am I paying in monthly service charges? How much am I paying for ATM fees?

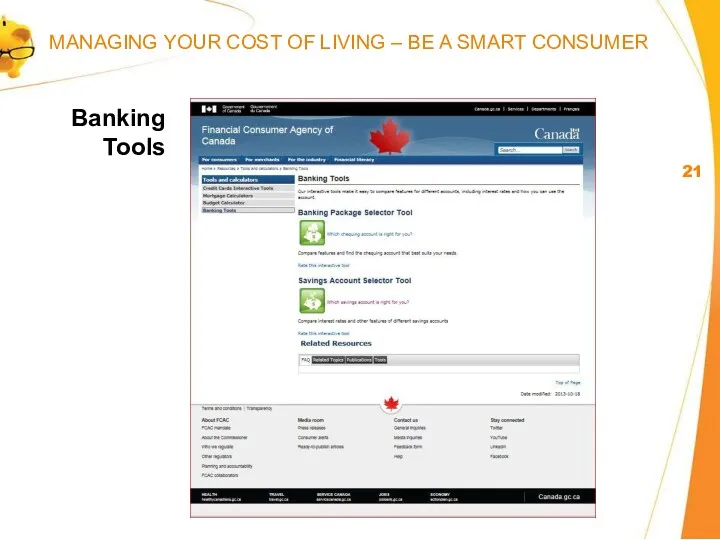

- 22. Banking Tools MANAGING YOUR COST OF LIVING – BE A SMART CONSUMER

- 23. What am I paying for land line and cell phone? How much do my long-distance calls

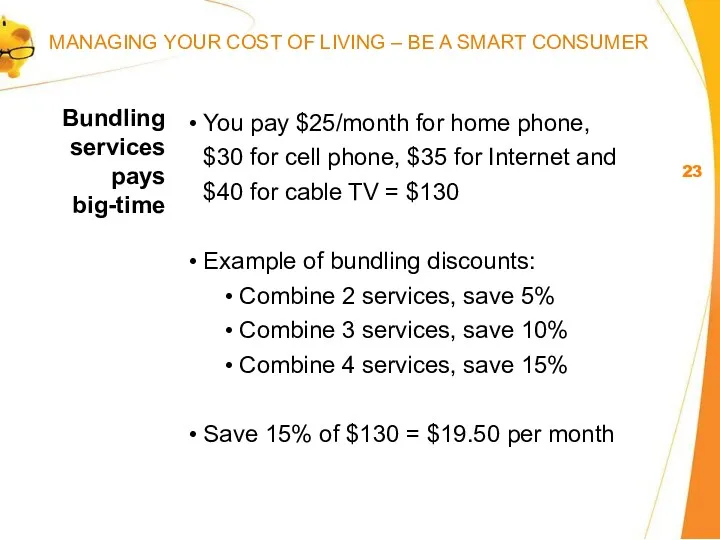

- 24. You pay $25/month for home phone, $30 for cell phone, $35 for Internet and $40 for

- 25. Eat breakfast at home. Bring your lunch, drinks and snacks (and coffee). “Veg out” on meatless

- 26. Add up the real costs of ownership (gas, insurance, depreciation, interest and maintenance). Check out Driving

- 27. When you move frequently: It takes at least 5 years to make it worthwhile. If you

- 28. Try it out: Put the monthly costs of owning a home (mortgage, property taxes, maintenance, etc.)

- 29. How to cut $100/month of spending MANAGING YOUR COST OF LIVING – BE A SMART CONSUMER

- 30. MANAGING YOUR COST OF LIVING – NEEDS AND WANTS

- 31. “We’ve all got a latte factor, regardless of our income level.” – David Bach Designer coffees

- 32. When does a want become a need? What motivates you to buy – advertising, friends, trendy

- 33. Avoid trips to stores and shopping malls and online buying sites. Pay cash or cheque for

- 34. CREDIT AND MANAGEMENT

- 35. Paying your credit card bill just a couple of days after the due date won't affect

- 36. All credit cards have the same grace period (also known as an interest-free period). True or

- 37. Last month, your credit card balance was zero. This month, your statement shows that you made

- 38. If you use your credit card to take money out as a “cash advance”, you don’t

- 39. Without a good credit history… Your bank may charge you higher interest rates on a personal

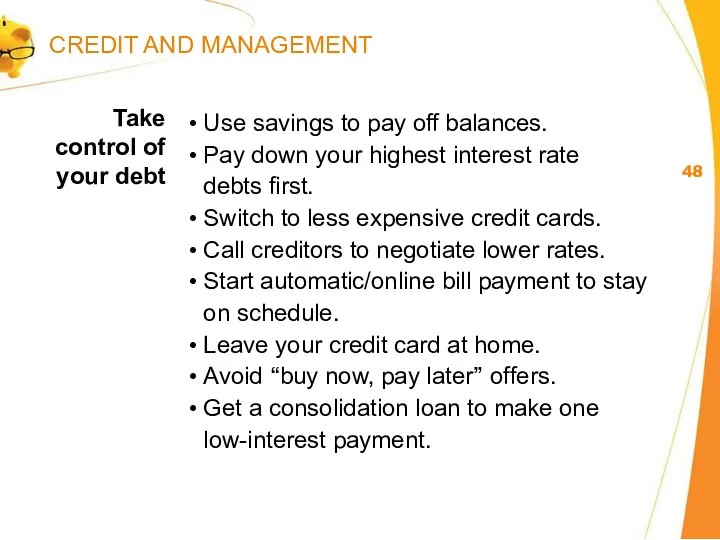

- 40. Pay the balance in full each month. If you can’t pay it in full, pay as

- 41. Initial balance: $3,000 Interest rate: 18% Minimum vs. fixed payments CREDIT AND MANAGEMENT

- 42. Shop around. Compare interest rates. Don’t accept your first offer. Keep within your budget. Borrow only

- 43. For students in financial needs Interest-free while you are enrolled in post-secondary education Become payable 6

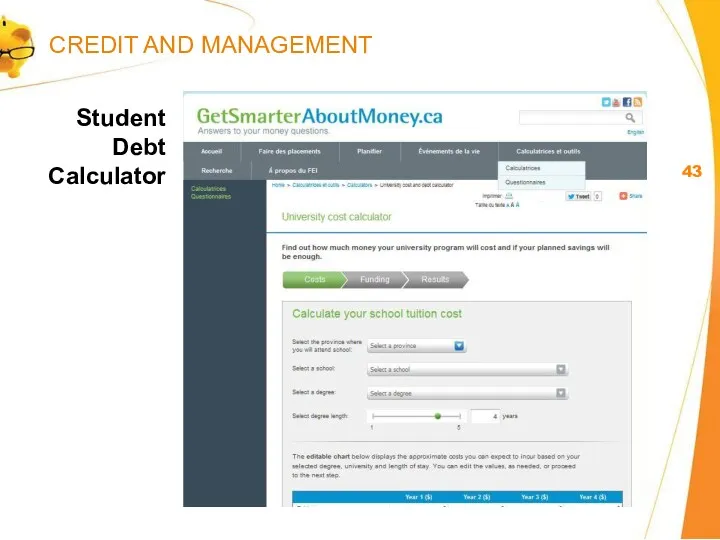

- 44. Student Debt Calculator CREDIT AND MANAGEMENT

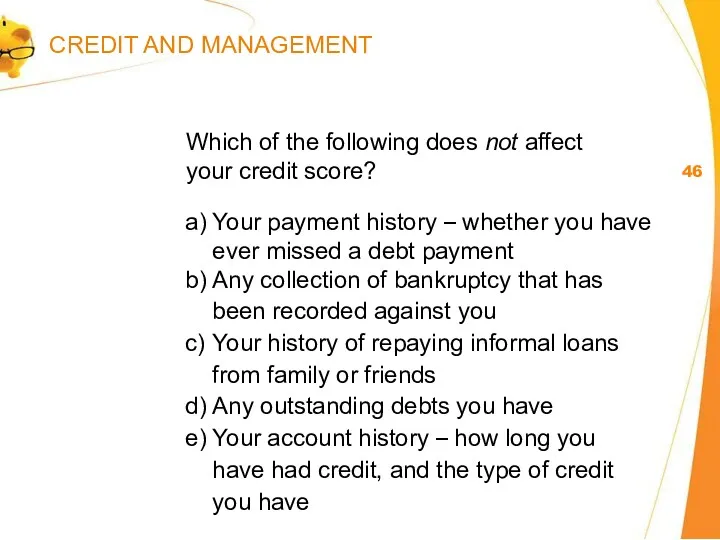

- 45. Getting a copy of your credit report is: a) A good way to check for identity

- 46. If you have applied for several credit cards or other forms of credit within a short

- 47. a) Your payment history – whether you have ever missed a debt payment b) Any collection

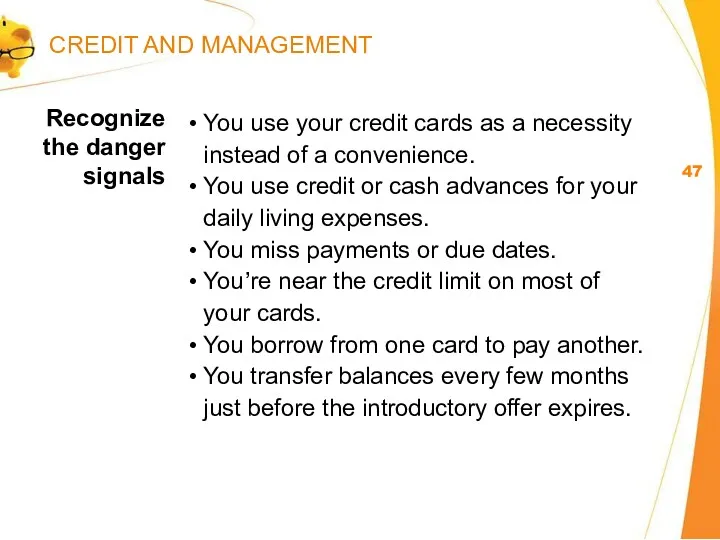

- 48. You use your credit cards as a necessity instead of a convenience. You use credit or

- 49. Use savings to pay off balances. Pay down your highest interest rate debts first. Switch to

- 50. SAVING AND INVESTING

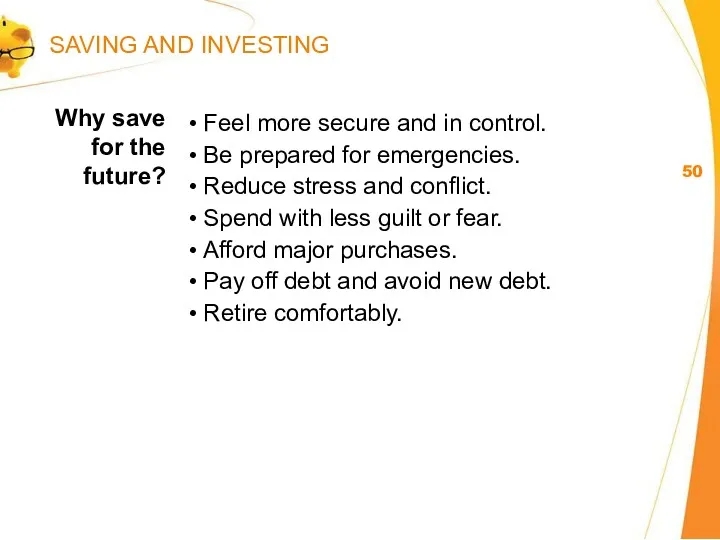

- 51. Feel more secure and in control. Be prepared for emergencies. Reduce stress and conflict. Spend with

- 52. Set a dollar amount and deadline. Break your goal into smaller goals. Write down your goal

- 53. Set up an emergency fund. Pay yourself first. Make savings automatic. Grow your savings. Savings SAVING

- 54. Set up direct debits from your bank account or paycheque. Save 5% to 10% of your

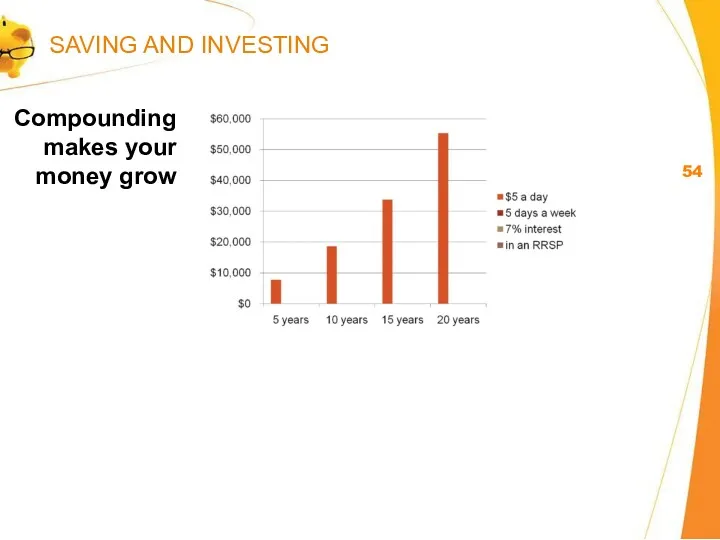

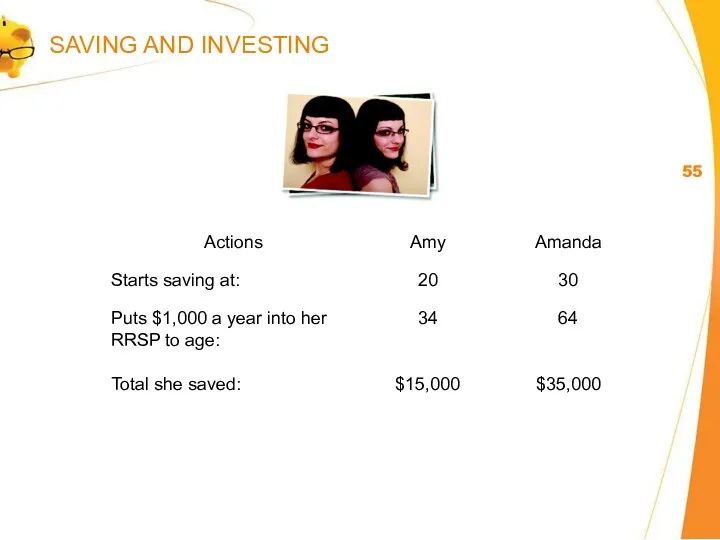

- 55. Compounding makes your money grow SAVING AND INVESTING

- 56. SAVING AND INVESTING

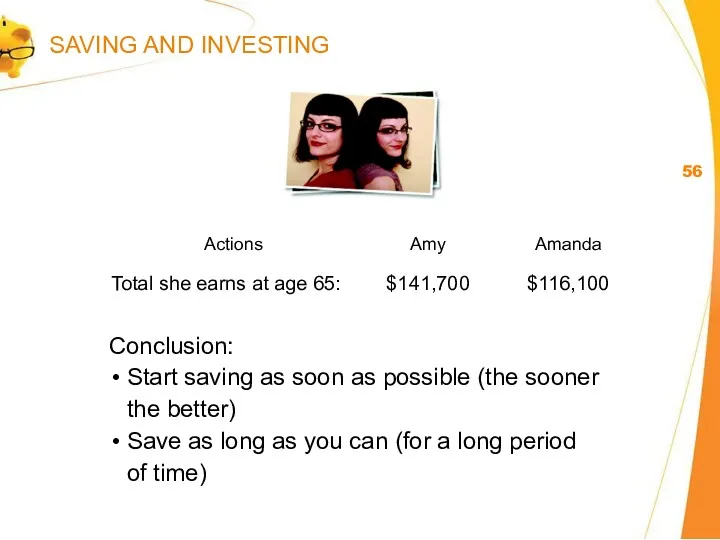

- 57. Conclusion: Start saving as soon as possible (the sooner the better) Save as long as you

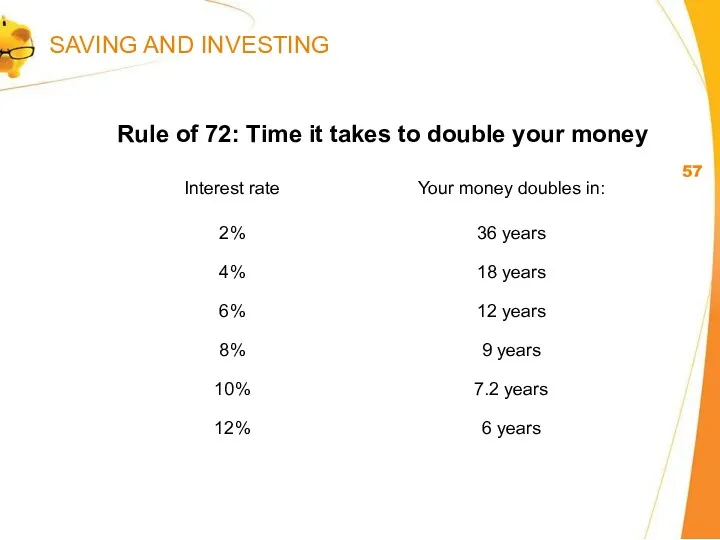

- 58. Rule of 72: Time it takes to double your money SAVING AND INVESTING

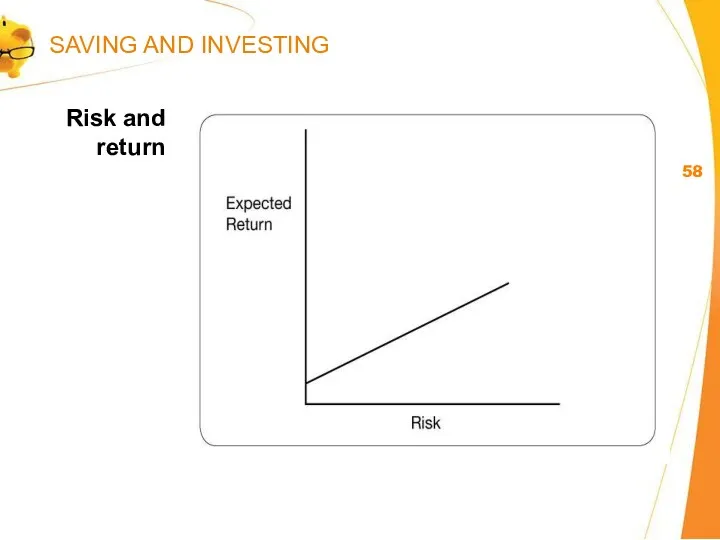

- 59. Risk and return SAVING AND INVESTING

- 60. Four types of investments Investments that pay interest (savings accounts, CSBs, GICs, etc.) Shares in a

- 61. Savings Account Selector Tool SAVING AND INVESTING

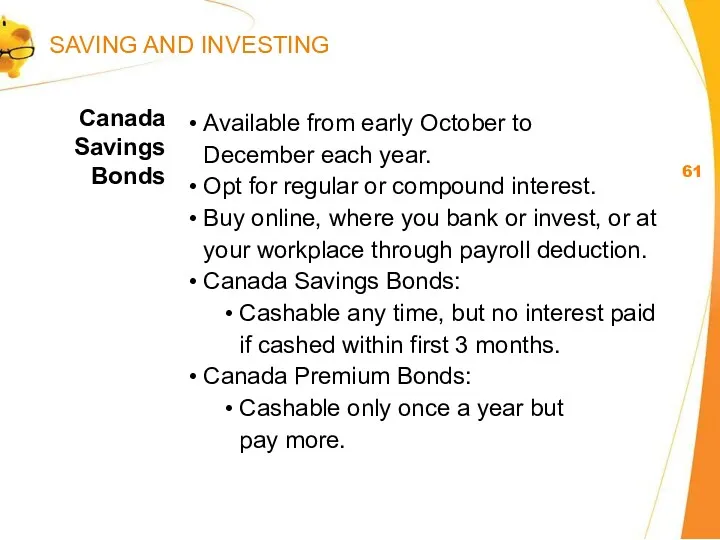

- 62. Canada Savings Bonds Available from early October to December each year. Opt for regular or compound

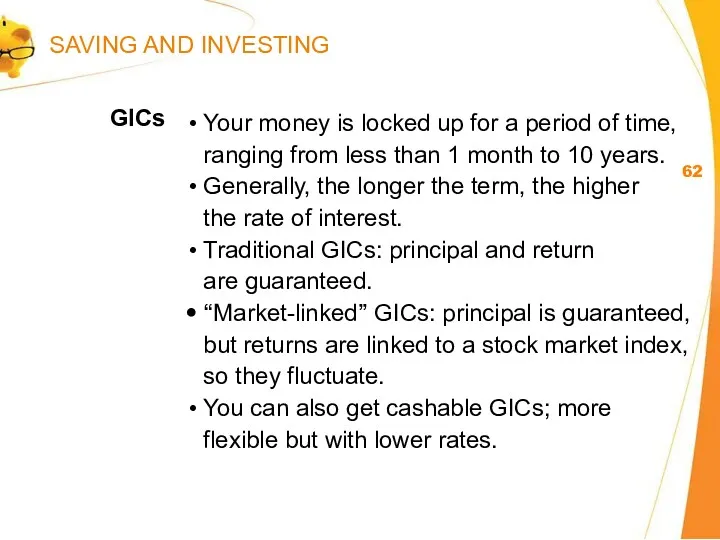

- 63. GICs Your money is locked up for a period of time, ranging from less than 1

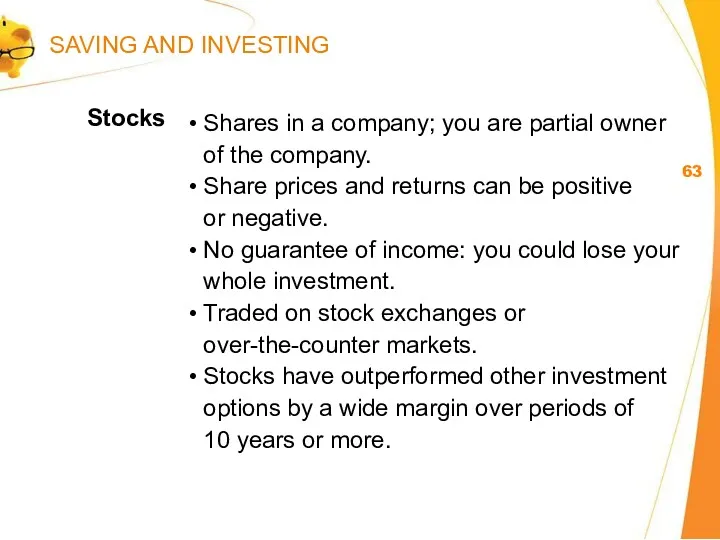

- 64. Stocks Shares in a company; you are partial owner of the company. Share prices and returns

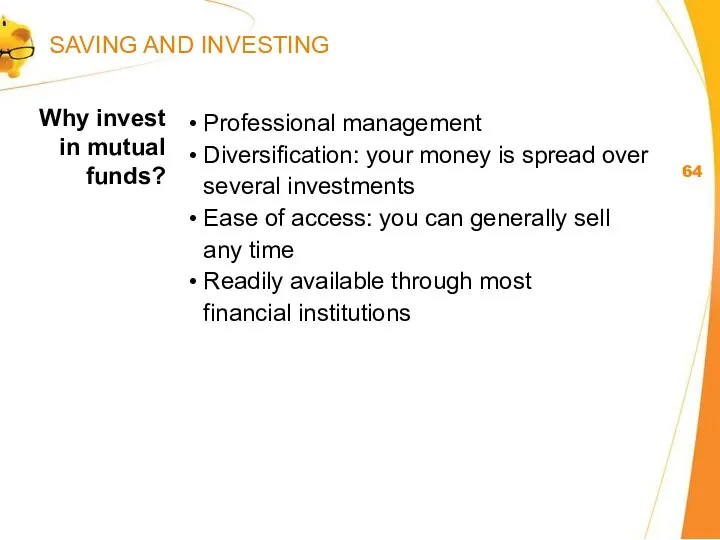

- 65. Why invest in mutual funds? Professional management Diversification: your money is spread over several investments Ease

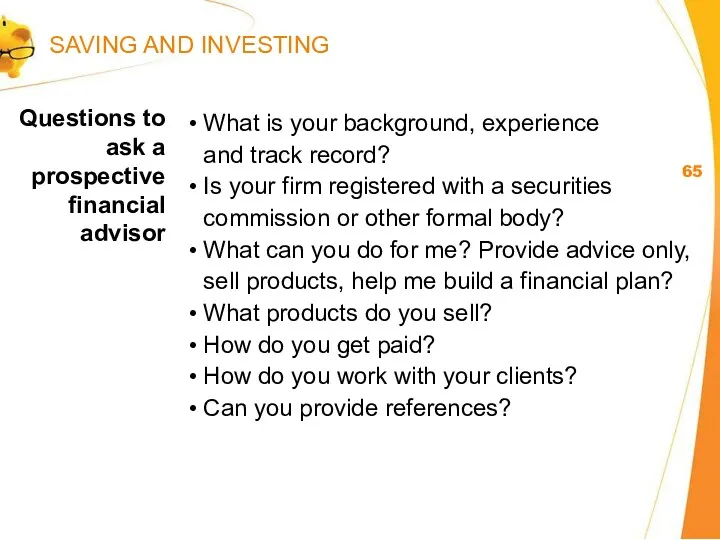

- 66. Questions to ask a prospective financial advisor What is your background, experience and track record? Is

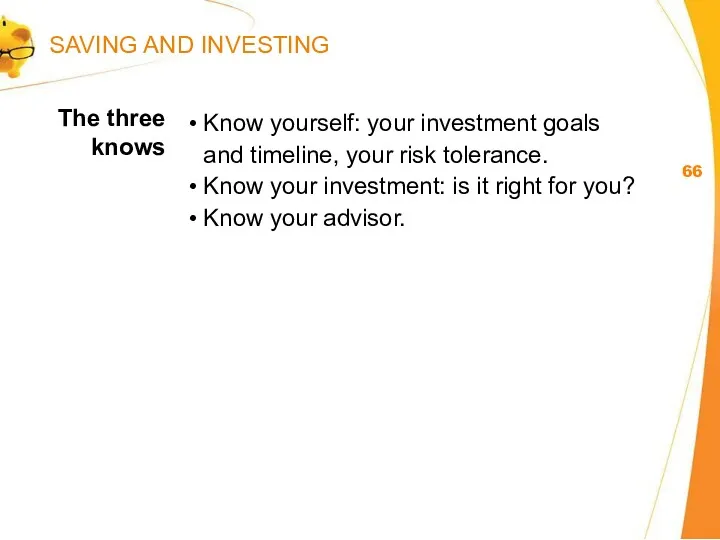

- 67. The three knows Know yourself: your investment goals and timeline, your risk tolerance. Know your investment:

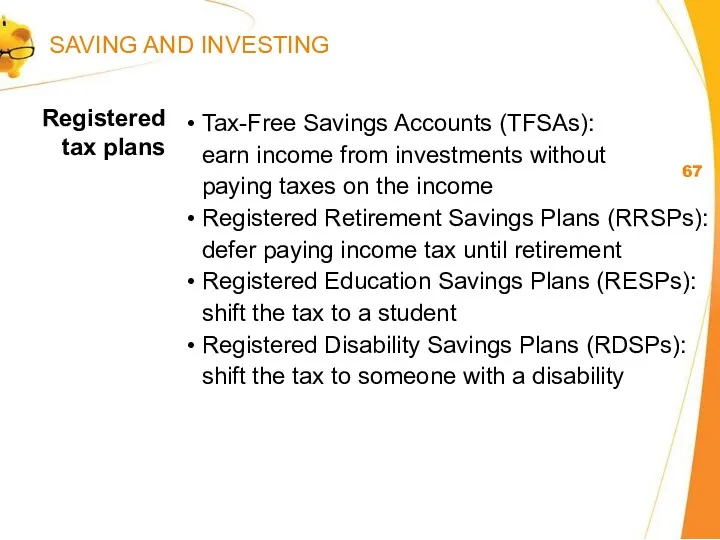

- 68. Registered tax plans Tax-Free Savings Accounts (TFSAs): earn income from investments without paying taxes on the

- 69. FINANCIAL PLANNING

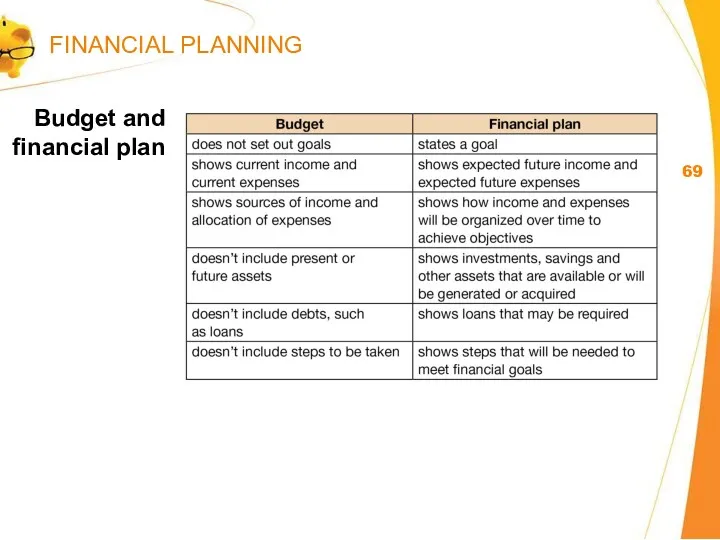

- 70. Budget and financial plan FINANCIAL PLANNING

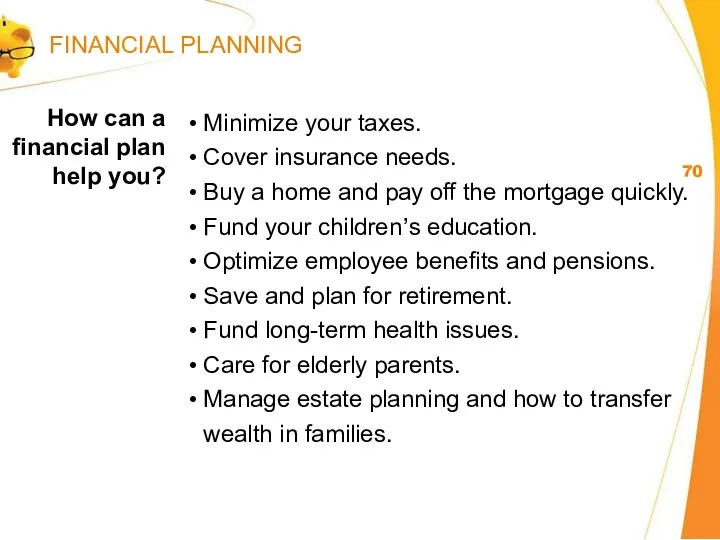

- 71. How can a financial plan help you? Minimize your taxes. Cover insurance needs. Buy a home

- 72. FINANCIAL PLANNING

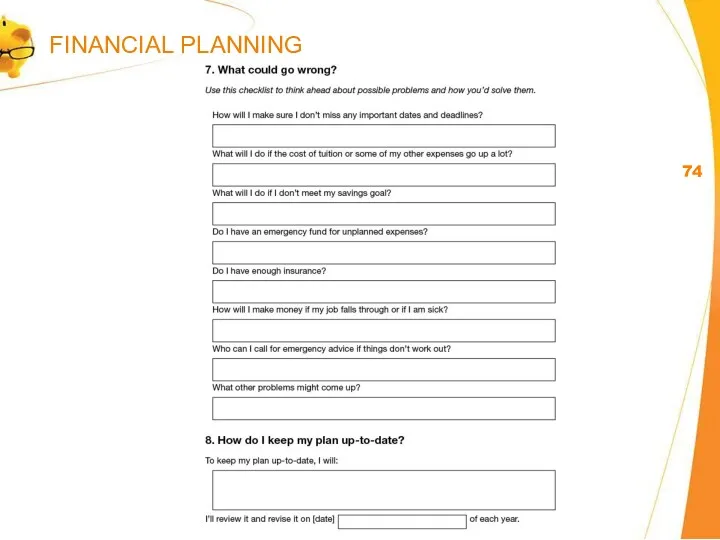

- 73. FINANCIAL PLANNING

- 74. FINANCIAL PLANNING

- 75. FINANCIAL PLANNING

- 76. PROTECT YOURSELF

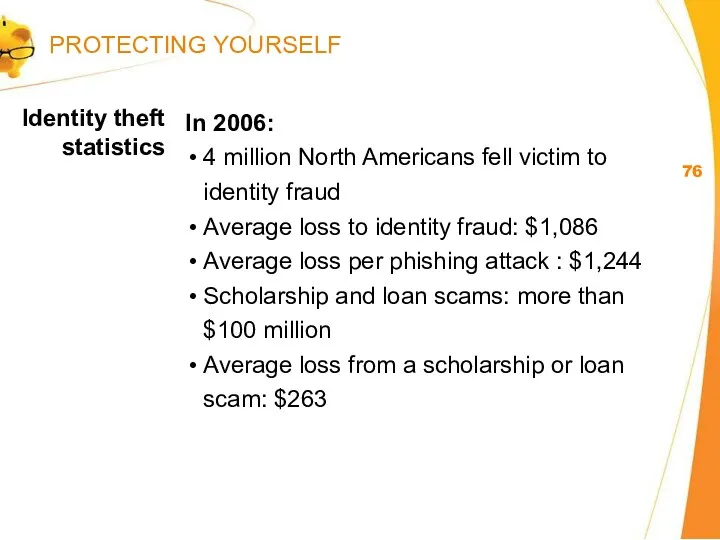

- 77. Identity theft statistics In 2006: 4 million North Americans fell victim to identity fraud Average loss

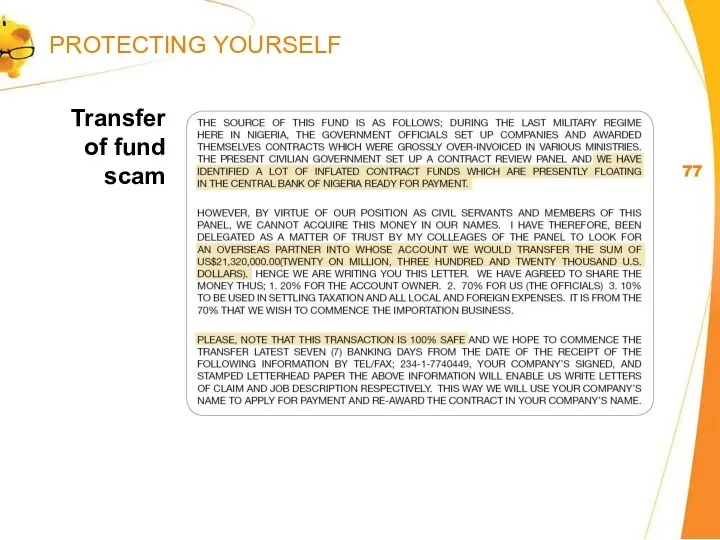

- 78. Transfer of fund scam PROTECTING YOURSELF

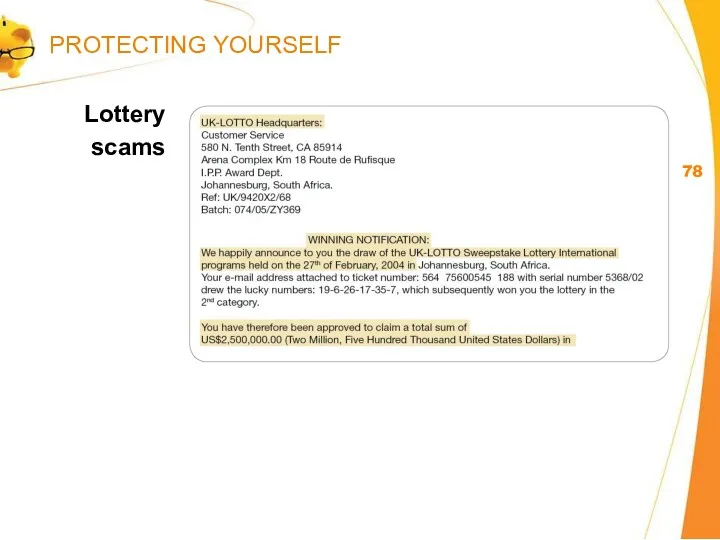

- 79. Lottery scams PROTECTING YOURSELF

- 80. Phishing emails and phony Web pages PROTECTING YOURSELF

- 81. Items for sale over-payment scam PROTECTING YOURSELF

- 82. Signs of bogus job ads Offer considerable pay with few to no duties Promise payment of

- 83. Protect yourself Don’t share personal information freely. Destroy documents with personal information. Keep your wallet or

- 84. Protect yourself, cont. Limit the number of credit cards you hold. Check your credit report once

- 85. Protect yourself, cont. Keep your computer passwords safe. Don’t give telemarketers personal information. Destroy old documents

- 86. What to do Contact your financial institution immediately. Notify Canada’s credit bureaus (Equifax Canada at www.equifax.ca

- 87. SUMMARY AND WRAP-UP

- 88. What have we learned? Keep track of your income and your expenses in a budget. Save

- 90. Скачать презентацию

COPYRIGHT/PERMISSION TO REPRODUCE

The Financial Basics workshop materials are covered by the

COPYRIGHT/PERMISSION TO REPRODUCE The Financial Basics workshop materials are covered by the

INTRODUCTION

INTRODUCTION

How to manage your spending

and prepare a realistic budget.

Ways to

How to manage your spending

and prepare a realistic budget.

Ways to

Control your financial future.

Achieve your life goals.

Provide for yourself and your

Control your financial future.

Achieve your life goals.

Provide for yourself and your

The current average percentage of their income that Canadians save is:

a)

The current average percentage of their income that Canadians save is:

a)

In 2010, the average household debt of Canadians was:

a) $26,000

b)

In 2010, the average household debt of Canadians was:

a) $26,000

b)

In 2009, the total reported dollar loss by victims of identity

In 2009, the total reported dollar loss by victims of identity

In 2009, the average debt:

For college graduates was:

$3,500

$8,500

$13,500

For a university graduates

In 2009, the average debt:

For college graduates was:

$3,500

$8,500

$13,500

For a university graduates

The percentage of Canadian youth whose parents are not expected to

The percentage of Canadian youth whose parents are not expected to

BUDGETING

BUDGETING

Income

Expenses

Difference between the two:

surplus or deficit

Parts of a budget

BUDGETING

Income

Expenses

Difference between the two:

surplus or deficit

Parts of a budget

BUDGETING

Keep every receipt.

Record every expense in a notebook

or electronic device.

Review

Keep every receipt.

Record every expense in a notebook

or electronic device.

Review

Monthly income

BUDGETING

Monthly income

BUDGETING

Monthly expenses

Fixed vs variable expenses

BUDGETING

Monthly expenses

Fixed vs variable expenses

BUDGETING

Difference between total monthly income and total monthly expenses =

Net surplus

Difference between total monthly income and total monthly expenses =

Net surplus

MANAGING YOUR COST

OF LIVING –

BE A SMART CONSUMER

MANAGING YOUR COST

OF LIVING –

BE A SMART CONSUMER

Check your bills.

Negotiate better plans (banking fees and

services, telephone, cell

Check your bills.

Negotiate better plans (banking fees and

services, telephone, cell

Spot mistakes and overcharges.

Pay less in late fees, interest and penalties.

Get

Spot mistakes and overcharges.

Pay less in late fees, interest and penalties.

Get

Call each service provider and ask:

• How can I cut back

Call each service provider and ask:

• How can I cut back

What am I paying in monthly

service charges?

How much am I

What am I paying in monthly

service charges?

How much am I

Banking Tools

MANAGING YOUR COST OF LIVING – BE A SMART CONSUMER

Banking Tools

MANAGING YOUR COST OF LIVING – BE A SMART CONSUMER

What am I paying for land line and

cell phone?

How much

What am I paying for land line and

cell phone?

How much

You pay $25/month for home phone,

$30 for cell phone, $35

You pay $25/month for home phone, $30 for cell phone, $35

Eat breakfast at home.

Bring your lunch, drinks and snacks

(and coffee).

“Veg

Eat breakfast at home.

Bring your lunch, drinks and snacks

(and coffee).

“Veg

Add up the real costs of ownership (gas, insurance, depreciation, interest

Add up the real costs of ownership (gas, insurance, depreciation, interest

When you move frequently:

It takes at least 5 years to make

When you move frequently:

It takes at least 5 years to make

Try it out:

Put the monthly costs of owning a home

Try it out:

Put the monthly costs of owning a home

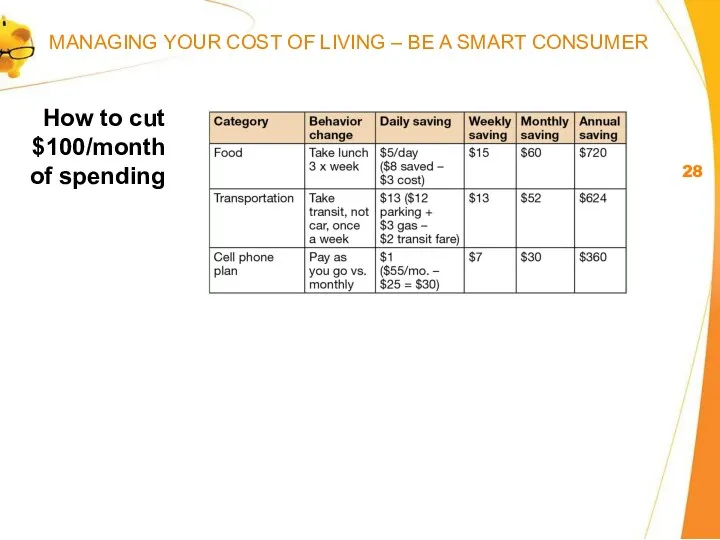

How to cut $100/month

of spending

MANAGING YOUR COST OF LIVING –

How to cut $100/month

of spending

MANAGING YOUR COST OF LIVING –

MANAGING YOUR COST

OF LIVING –

NEEDS AND WANTS

MANAGING YOUR COST

OF LIVING –

NEEDS AND WANTS

“We’ve all got a latte factor, regardless of our income level.”

“We’ve all got a latte factor, regardless of our income level.”

When does a want become a need?

What motivates you to buy

When does a want become a need?

What motivates you to buy

Avoid trips to stores and shopping malls

and online buying sites.

Pay

Avoid trips to stores and shopping malls

and online buying sites.

Pay

CREDIT AND MANAGEMENT

CREDIT AND MANAGEMENT

Paying your credit card bill just a couple of days after

Paying your credit card bill just a couple of days after

All credit cards have the same grace period (also known as

All credit cards have the same grace period (also known as

Last month, your credit card balance was zero. This month, your

Last month, your credit card balance was zero. This month, your

If you use your credit card to take money out as

If you use your credit card to take money out as

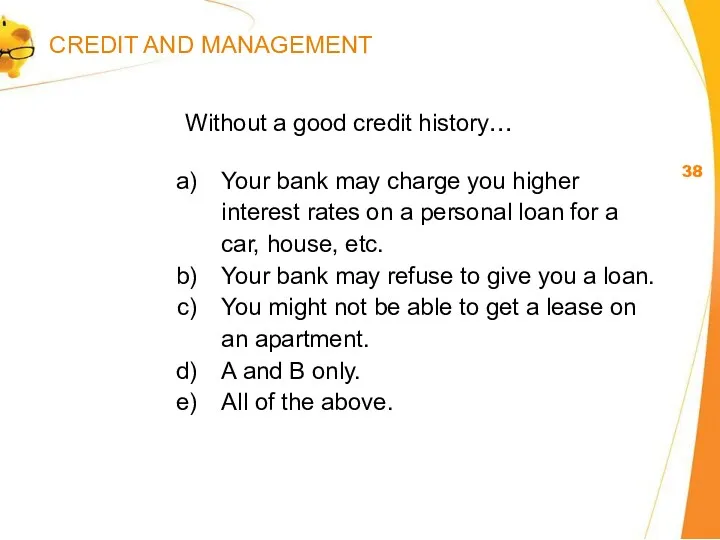

Without a good credit history…

Your bank may charge you higher

interest

Without a good credit history…

Your bank may charge you higher

interest

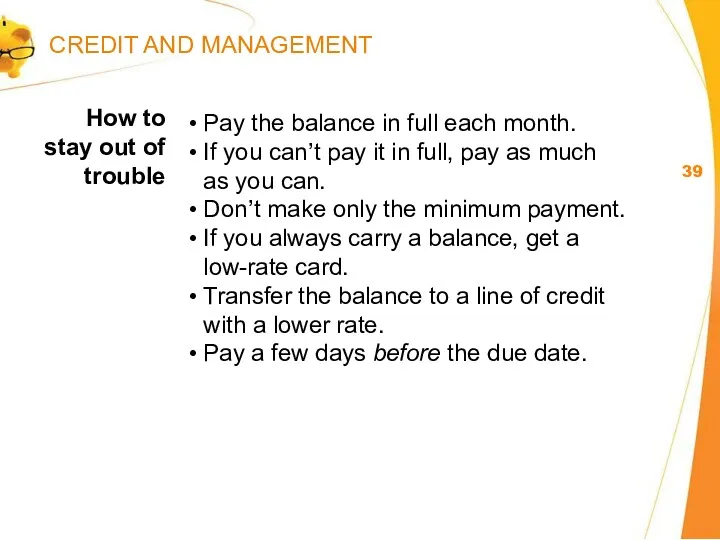

Pay the balance in full each month.

If you can’t pay it

Pay the balance in full each month.

If you can’t pay it

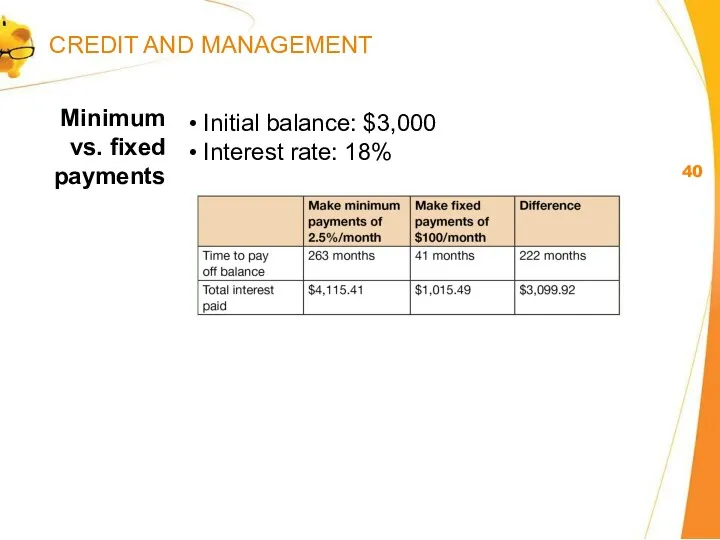

Initial balance: $3,000

Interest rate: 18%

Minimum vs. fixed payments

CREDIT AND MANAGEMENT

Initial balance: $3,000

Interest rate: 18%

Minimum vs. fixed payments

CREDIT AND MANAGEMENT

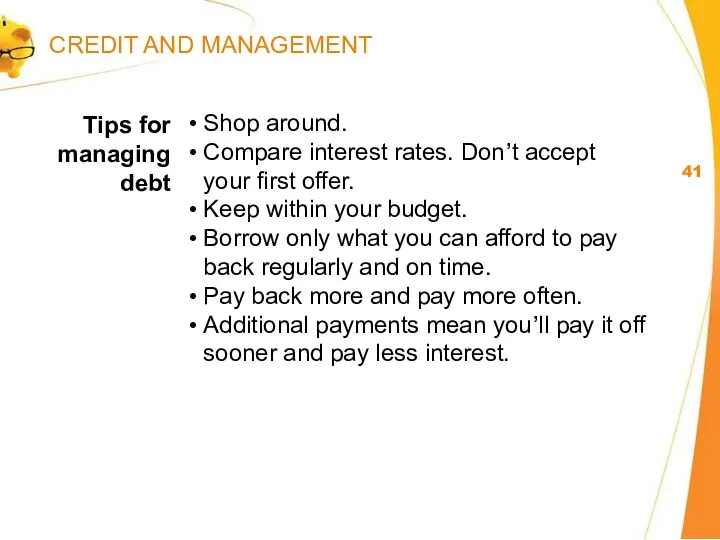

Shop around.

Compare interest rates. Don’t accept

your first offer.

Keep within

Shop around.

Compare interest rates. Don’t accept

your first offer.

Keep within

For students in financial needs

Interest-free while you are enrolled in post-secondary

For students in financial needs

Interest-free while you are enrolled in post-secondary

Student Debt Calculator

CREDIT AND MANAGEMENT

Student Debt Calculator

CREDIT AND MANAGEMENT

Getting a copy of your credit report is:

a) A good way to

Getting a copy of your credit report is:

a) A good way to

If you have applied for several credit cards or other forms

If you have applied for several credit cards or other forms

a) Your payment history – whether you have

ever missed a debt

a) Your payment history – whether you have ever missed a debt

You use your credit cards as a necessity

instead of a

You use your credit cards as a necessity instead of a

Use savings to pay off balances.

Pay down your highest interest rate

Use savings to pay off balances.

Pay down your highest interest rate

SAVING AND INVESTING

SAVING AND INVESTING

Feel more secure and in control.

Be prepared for emergencies.

Reduce stress and

Feel more secure and in control.

Be prepared for emergencies.

Reduce stress and

Set a dollar amount and deadline.

Break your goal into smaller goals.

Write

Set a dollar amount and deadline.

Break your goal into smaller goals.

Write

Set up an emergency fund.

Pay yourself first.

Make savings automatic.

Grow your

Set up an emergency fund.

Pay yourself first.

Make savings automatic.

Grow your

Set up direct debits from your bank account

or paycheque.

Save 5%

Set up direct debits from your bank account

or paycheque.

Save 5%

Compounding

makes your money grow

SAVING AND INVESTING

Compounding

makes your money grow

SAVING AND INVESTING

SAVING AND INVESTING

SAVING AND INVESTING

Conclusion:

Start saving as soon as possible (the sooner

the better)

Save as

Conclusion:

Start saving as soon as possible (the sooner

the better)

Save as

Rule of 72: Time it takes to double your money

SAVING AND

Rule of 72: Time it takes to double your money

SAVING AND

Risk and return

SAVING AND INVESTING

Risk and return

SAVING AND INVESTING

Four types of investments

Investments that pay interest

(savings accounts, CSBs, GICs,

Four types of investments

Investments that pay interest (savings accounts, CSBs, GICs,

Savings Account Selector Tool

SAVING AND INVESTING

Savings Account Selector Tool

SAVING AND INVESTING

Canada Savings Bonds

Available from early October to

December each year.

Opt for

Canada Savings Bonds

Available from early October to

December each year.

Opt for

GICs

Your money is locked up for a period of time,

ranging

GICs

Your money is locked up for a period of time, ranging

Stocks

Shares in a company; you are partial owner

of the company.

Share

Stocks

Shares in a company; you are partial owner

of the company.

Share

Why invest

in mutual funds?

Professional management

Diversification: your money is spread over

Why invest

in mutual funds?

Professional management

Diversification: your money is spread over

Questions to ask a prospective financial advisor

What is your background, experience

Questions to ask a prospective financial advisor

What is your background, experience

The three knows

Know yourself: your investment goals

and timeline, your risk

The three knows

Know yourself: your investment goals and timeline, your risk

Registered

tax plans

Tax-Free Savings Accounts (TFSAs):

earn income from investments

Registered

tax plans

Tax-Free Savings Accounts (TFSAs): earn income from investments

FINANCIAL PLANNING

FINANCIAL PLANNING

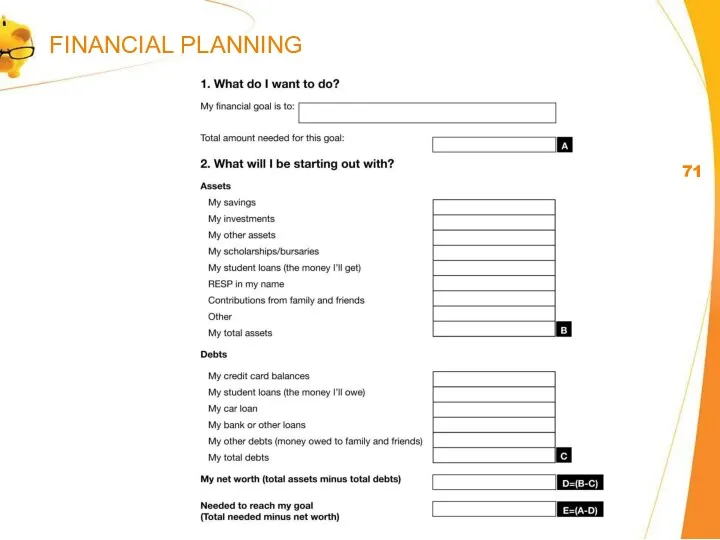

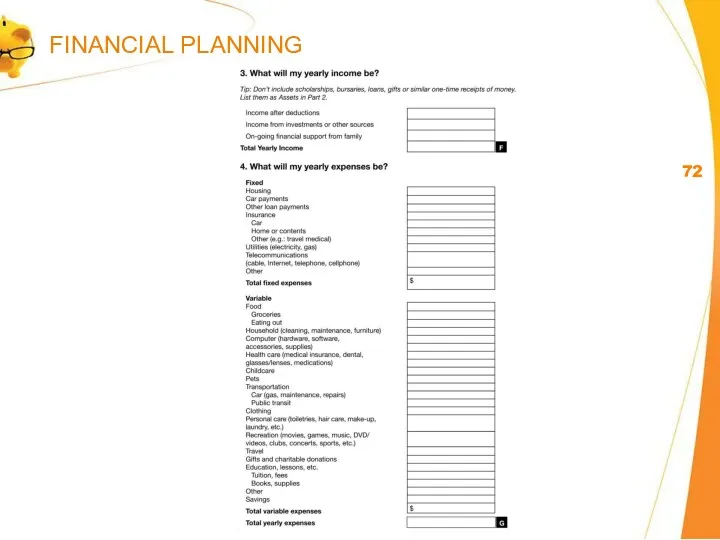

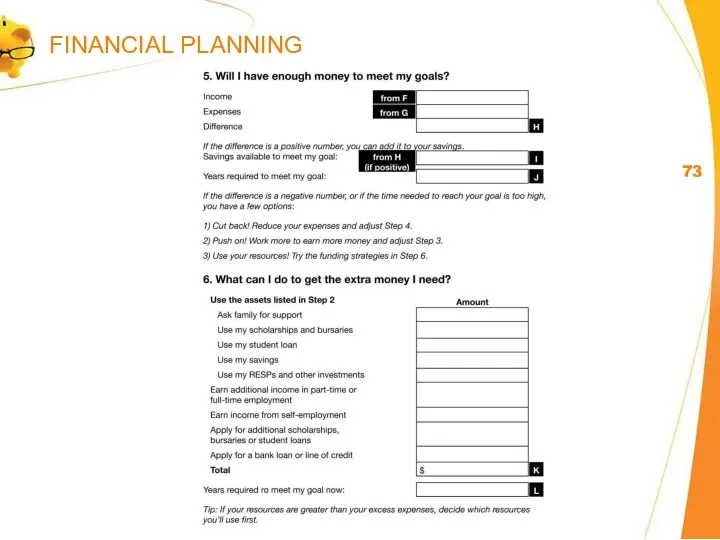

Budget and financial plan

FINANCIAL PLANNING

Budget and financial plan

FINANCIAL PLANNING

How can a financial plan help you?

Minimize your taxes.

Cover insurance needs.

How can a financial plan help you?

Minimize your taxes.

Cover insurance needs.

FINANCIAL PLANNING

FINANCIAL PLANNING

FINANCIAL PLANNING

FINANCIAL PLANNING

FINANCIAL PLANNING

FINANCIAL PLANNING

FINANCIAL PLANNING

FINANCIAL PLANNING

PROTECT YOURSELF

PROTECT YOURSELF

Identity theft statistics

In 2006:

4 million North Americans fell victim to

Identity theft statistics

In 2006:

4 million North Americans fell victim to

Transfer of fund scam

PROTECTING YOURSELF

Transfer of fund scam

PROTECTING YOURSELF

Lottery

scams

PROTECTING YOURSELF

Lottery

scams

PROTECTING YOURSELF

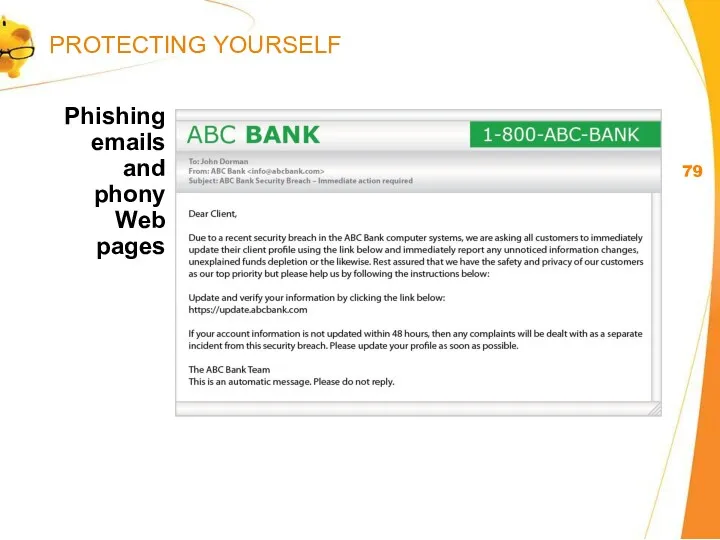

Phishing

emails

and

phony Web

pages

PROTECTING YOURSELF

Phishing

emails

and

phony Web

pages

PROTECTING YOURSELF

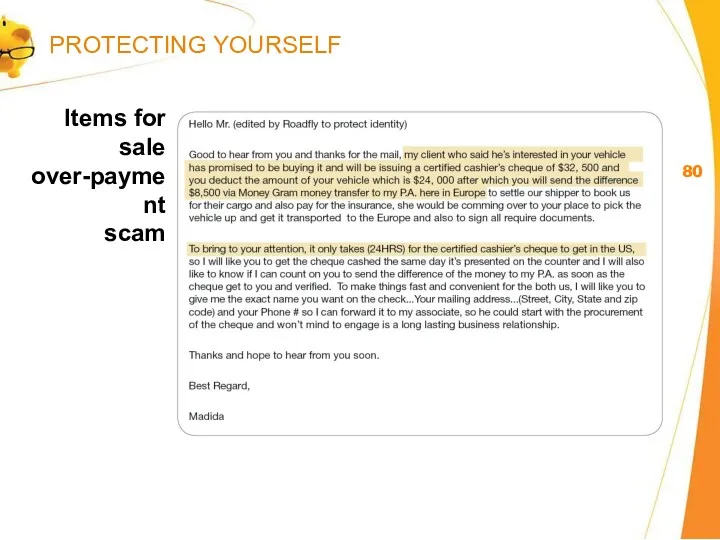

Items for sale over-payment

scam

PROTECTING YOURSELF

Items for sale over-payment

scam

PROTECTING YOURSELF

Signs of bogus

job ads

Offer considerable pay with few to no

Signs of bogus

job ads

Offer considerable pay with few to no

Protect yourself

Don’t share personal information freely.

Destroy documents with personal information.

Keep your

Protect yourself

Don’t share personal information freely.

Destroy documents with personal information.

Keep your

Protect yourself,

cont.

Limit the number of credit cards you hold.

Check

Protect yourself,

cont.

Limit the number of credit cards you hold.

Check

Protect yourself,

cont.

Keep your computer passwords safe.

Don’t give telemarketers personal information.

Destroy

Protect yourself,

cont.

Keep your computer passwords safe.

Don’t give telemarketers personal information.

Destroy

What to do

Contact your financial institution immediately.

Notify Canada’s credit bureaus (Equifax

What to do

Contact your financial institution immediately.

Notify Canada’s credit bureaus (Equifax

SUMMARY AND WRAP-UP

SUMMARY AND WRAP-UP

What have we learned?

Keep track of your income and your

What have we learned?

Keep track of your income and your

Налог на транспортные средства

Налог на транспортные средства Аудит издержек производства

Аудит издержек производства Развитие зеленого туризма на территории Никольского сельского совета. Комплекс Ингулка. Инвестиционное предложение

Развитие зеленого туризма на территории Никольского сельского совета. Комплекс Ингулка. Инвестиционное предложение Мотивация профсоюзного членства. Особенности вовлечения в Профсоюз

Мотивация профсоюзного членства. Особенности вовлечения в Профсоюз Статистика оплаты труда на предприятии

Статистика оплаты труда на предприятии Инвестициялық шешімдерді бағалау әдістері

Инвестициялық шешімдерді бағалау әдістері Планирование заявок на конкурсы для финансирования научно-исследовательских проектов

Планирование заявок на конкурсы для финансирования научно-исследовательских проектов Бухгалтерський контроль та юридична відповідальність на підприємстві

Бухгалтерський контроль та юридична відповідальність на підприємстві Гранты. Опыт участия

Гранты. Опыт участия ОСАО РЕСО-Гарантия. Страхование имущества юридических лиц

ОСАО РЕСО-Гарантия. Страхование имущества юридических лиц Лекция № 2

Лекция № 2 Дифференциация заработной платы в России

Дифференциация заработной платы в России Участники бюджетного процесса Челябинской области

Участники бюджетного процесса Челябинской области Анализ использования персонала предприятия и фонда заработной платы

Анализ использования персонала предприятия и фонда заработной платы Добро пожаловать в Компанию iCredit

Добро пожаловать в Компанию iCredit Расходы бюджетов

Расходы бюджетов Управление денежным потоком

Управление денежным потоком Деньги и их роль в экономической кредитно-денежной политике

Деньги и их роль в экономической кредитно-денежной политике Формы оплаты труда. Лекция 8

Формы оплаты труда. Лекция 8 Преимущества карт линейки GOLD

Преимущества карт линейки GOLD Функції податків

Функції податків Облигации: виды, доходность и обращение на рынке ценных бумаг

Облигации: виды, доходность и обращение на рынке ценных бумаг Единый налог на вменённый доход

Единый налог на вменённый доход Аналіз грошових коштів. Розділ 6

Аналіз грошових коштів. Розділ 6 Гарантийные и компенсационные выплаты

Гарантийные и компенсационные выплаты Financial Accounting Risks and their preventives

Financial Accounting Risks and their preventives Формирование и развитие банковской системы, как объекта государственного управления. (Тема 1)

Формирование и развитие банковской системы, как объекта государственного управления. (Тема 1) Финансовое состояние организации ООО Горем-3 и формирование направлений по его улучшению

Финансовое состояние организации ООО Горем-3 и формирование направлений по его улучшению