- Financial Statement Analysis

Содержание

- 2. Outline Meaning of Financial Statements and Financial Statement Analysis Significance of Financial Statements Types of Financial

- 3. Focus The focus will be on financial statement analysis and its use in corporate finance. financial

- 4. Meaning of Financial Statements Financial statements are summaries of the operating, financing, and investment activities of

- 5. The financial statements are expected to be prepared in accordance with a set of standards known

- 6. Significance of Financial Statements Wall Street analysts and other sophisticated investors prefer such financial disclosure documents

- 7. For example, are inventories adequate to support the projected level of sales? Does the firm have

- 8. Types of Financial Statements and Reports ⮚ The Income Statement ⮚ The Balance Sheet ⮚ The

- 9. The Income Statement ⮚ An income statement is a summary of the revenues and expenses of

- 10. Results of financing decisions are reflected in the remainder of the income statement. When interest expenses

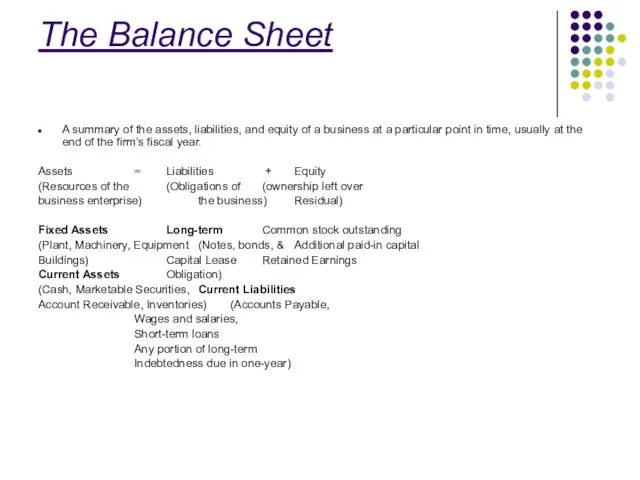

- 11. The Balance Sheet A summary of the assets, liabilities, and equity of a business at a

- 12. THE STATEMENT OF CASH FLOWS The statement is designed to show how the firm’s operations have

- 13. RATIO ANALYSIS Financial statements report both on a firm’s position at a point in time and

- 14. Ratio analysis begins with the calculation of a set of financial ratios designed to show the

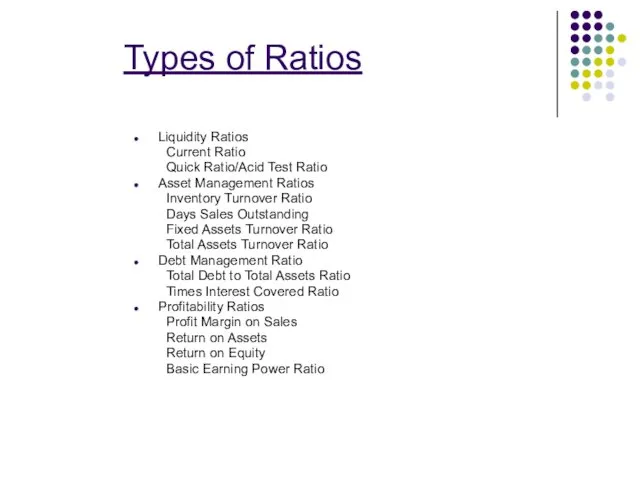

- 15. Types of Ratios Liquidity Ratios Current Ratio Quick Ratio/Acid Test Ratio Asset Management Ratios Inventory Turnover

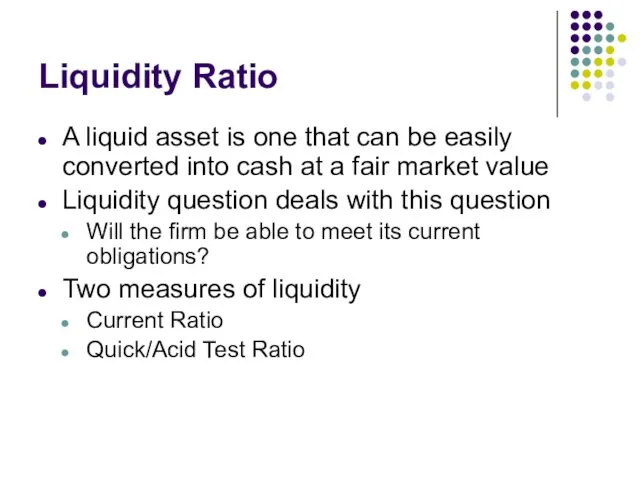

- 16. Liquidity Ratio A liquid asset is one that can be easily converted into cash at a

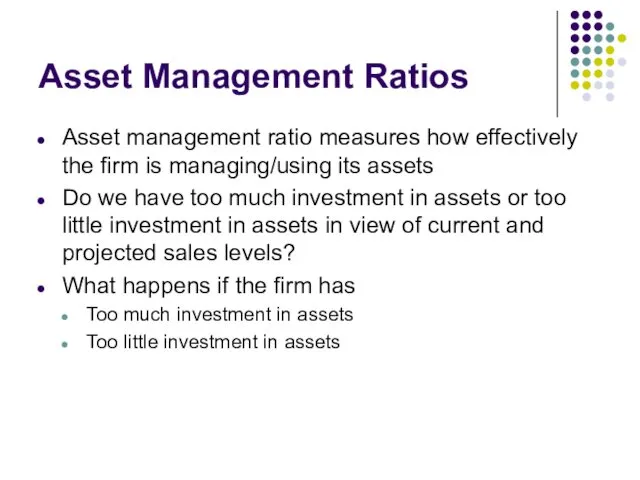

- 17. Asset Management Ratios Asset management ratio measures how effectively the firm is managing/using its assets Do

- 18. Asset Management Ratios Inventory Turnover Ratio Measures the efficiency of Inventory Management A high ratio indicates

- 19. Asset Management Ratio Days Sales Outstanding (DSO) To appraise the quality of accounts receivables Average length

- 20. Asset Management Ratios Fixed Assets Turnover Ratio Measures efficiency of long-term capital investment How effectively a

- 21. Asset Management Ratio Total Asset Turnover Ratio Measure efficiency of total assets for the company as

- 22. Debt Management Ratio Implications of use of borrowings Creditors look to Stockholders’ equity as a safety

- 23. Total Debt to Total Assets Ratio Measures percentage of assets being financed through borrowings Too high

- 24. Times Earned Interest (TIE) Measure the extent to which operating income can decline before the firm

- 25. Profitability Ratios Net result of a number of policies and decisions Show the combined effect of

- 26. Net Profit Margin on Sales Relates net income available to common stockholders to sales Basic Earning

- 28. Скачать презентацию

Outline

Meaning of Financial Statements and Financial Statement Analysis

Significance of Financial Statements

Types

Outline

Meaning of Financial Statements and Financial Statement Analysis

Significance of Financial Statements

Types

Focus

The focus will be on financial statement analysis and its use

Focus

The focus will be on financial statement analysis and its use

Meaning of Financial Statements

Financial statements are summaries of the operating, financing,

Meaning of Financial Statements

Financial statements are summaries of the operating, financing,

The financial statements are expected to be prepared in accordance with

The financial statements are expected to be prepared in accordance with

Significance of Financial Statements

Wall Street analysts and other sophisticated investors

Significance of Financial Statements

Wall Street analysts and other sophisticated investors

For example, are inventories adequate to support the projected level of

For example, are inventories adequate to support the projected level of

Types of Financial Statements and Reports

⮚ The Income Statement

⮚ The

Types of Financial Statements and Reports

⮚ The Income Statement

⮚ The

The Income Statement

⮚ An income statement is a summary of the

The Income Statement

⮚ An income statement is a summary of the

Results of financing decisions are reflected in the remainder of the

Results of financing decisions are reflected in the remainder of the

The Balance Sheet

A summary of the assets, liabilities, and equity of

The Balance Sheet

A summary of the assets, liabilities, and equity of

THE STATEMENT OF CASH FLOWS

The statement is designed to show

THE STATEMENT OF CASH FLOWS

The statement is designed to show

RATIO ANALYSIS

Financial statements report both on a firm’s position at a

RATIO ANALYSIS

Financial statements report both on a firm’s position at a

Ratio analysis begins

with the calculation of a set of financial

Ratio analysis begins

with the calculation of a set of financial

Types of Ratios

Liquidity Ratios

Current Ratio

Quick Ratio/Acid Test Ratio

Asset Management Ratios

Inventory Turnover

Types of Ratios

Liquidity Ratios

Current Ratio

Quick Ratio/Acid Test Ratio

Asset Management Ratios

Inventory Turnover

Liquidity Ratio

A liquid asset is one that can be easily converted

Liquidity Ratio

A liquid asset is one that can be easily converted

Asset Management Ratios

Asset management ratio measures how effectively the firm is

Asset Management Ratios

Asset management ratio measures how effectively the firm is

Asset Management Ratios

Inventory Turnover Ratio

Measures the efficiency of Inventory Management

A high

Asset Management Ratios

Inventory Turnover Ratio

Measures the efficiency of Inventory Management

A high

Asset Management Ratio

Days Sales Outstanding (DSO)

To appraise the quality of accounts

Asset Management Ratio

Days Sales Outstanding (DSO)

To appraise the quality of accounts

Asset Management Ratios

Fixed Assets Turnover Ratio

Measures efficiency of long-term capital investment

How

Asset Management Ratios

Fixed Assets Turnover Ratio

Measures efficiency of long-term capital investment

How

Asset Management Ratio

Total Asset Turnover Ratio

Measure efficiency of total assets for

Asset Management Ratio

Total Asset Turnover Ratio

Measure efficiency of total assets for

Debt Management Ratio

Implications of use of borrowings

Creditors look to Stockholders’ equity

Debt Management Ratio

Implications of use of borrowings

Creditors look to Stockholders’ equity

Total Debt to Total Assets Ratio

Measures percentage of assets being financed

Total Debt to Total Assets Ratio

Measures percentage of assets being financed

Times Earned Interest (TIE)

Measure the extent to which operating income can

Times Earned Interest (TIE)

Measure the extent to which operating income can

Profitability Ratios

Net result of a number of policies and decisions

Show the

Profitability Ratios

Net result of a number of policies and decisions

Show the

Net Profit Margin on Sales

Relates net income available to common stockholders

Net Profit Margin on Sales

Relates net income available to common stockholders

Ндфл. НК РФ налог на доходы физических лиц

Ндфл. НК РФ налог на доходы физических лиц Бухгалтерский учет и анализ эффективности использования материально-производственных запасов

Бухгалтерский учет и анализ эффективности использования материально-производственных запасов Технический анализ финансовых рынков

Технический анализ финансовых рынков Ценообразование и цены на продукцию АПК

Ценообразование и цены на продукцию АПК Индивидуальные инвестиционные cчета

Индивидуальные инвестиционные cчета Сводная таблица расчетов транспортных издержек

Сводная таблица расчетов транспортных издержек Регулирование и надзор за деятельностью институтов кредитного рынка в России в сфере финансового посредничества

Регулирование и надзор за деятельностью институтов кредитного рынка в России в сфере финансового посредничества Финансовая система страны

Финансовая система страны Бюджетная система государства, основы ее построения

Бюджетная система государства, основы ее построения Ценные бумаги

Ценные бумаги Пенсионное обеспечение в Российской Федерации

Пенсионное обеспечение в Российской Федерации Налоги и налогообложение на предприятии

Налоги и налогообложение на предприятии Отчет о выполнении отраслевого соглашения в области оплаты труда. Росатом

Отчет о выполнении отраслевого соглашения в области оплаты труда. Росатом Налогообложение индивидуальных предпринимателей в РФ

Налогообложение индивидуальных предпринимателей в РФ Тест Хауи в США: современная практика его применения

Тест Хауи в США: современная практика его применения Исполнение налоговой обязанности

Исполнение налоговой обязанности Особенности определения налоговой базы налога на прибыль:

Особенности определения налоговой базы налога на прибыль: Всероссийская олимпиада по финансовой грамотности, финансовому рынку и защите прав потребителей финансовых услуг

Всероссийская олимпиада по финансовой грамотности, финансовому рынку и защите прав потребителей финансовых услуг Доходы и прибыль предприятия

Доходы и прибыль предприятия Валютні операції комерційного банку

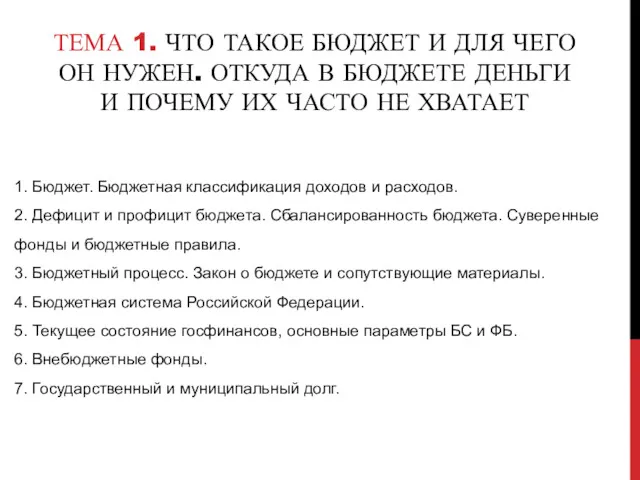

Валютні операції комерційного банку Бюджет. Бюджетная классификация доходов и расходов. (Тема 1)

Бюджет. Бюджетная классификация доходов и расходов. (Тема 1) Развитие банковской системы в России

Развитие банковской системы в России Товарные и фондовые биржи

Товарные и фондовые биржи Израиль банк жүйесі

Израиль банк жүйесі Взаимосвязь финансов с экономическими категориями (кредит, цена, право)

Взаимосвязь финансов с экономическими категориями (кредит, цена, право) Учет и анализ финансовых результатов в ОАО Псковавиа

Учет и анализ финансовых результатов в ОАО Псковавиа Антикризисный менеджмент. Сущность и причины неплатежеспособности предприятия. (Лекция 4)

Антикризисный менеджмент. Сущность и причины неплатежеспособности предприятия. (Лекция 4) Управление инвестиционной деятельностью компании

Управление инвестиционной деятельностью компании