- Financial Statement. Analysis

Содержание

- 2. Profitability Margins and return ratios provide information on the profitability of a company and the efficiency

- 3. Profitability ratios

- 4. Profitability ratios: Margins

- 5. Earnings, (or net income,) are simply revenues minus costs. They are an accounting measure of profits.

- 6. Retained earnings Retained earnings are the earnings re-invested into the firm: Retained earnings = earnings -

- 7. Measuring profit Return on equity (ROE) uses accounting values: earnings divided by book value of equity.

- 8. Return on assets Return on assets (ROA) is another important measure of portability. Again, ROA uses

- 9. AAA’s Balance Sheet (Asset Side) a. How the firm stands on a specific date. b. What

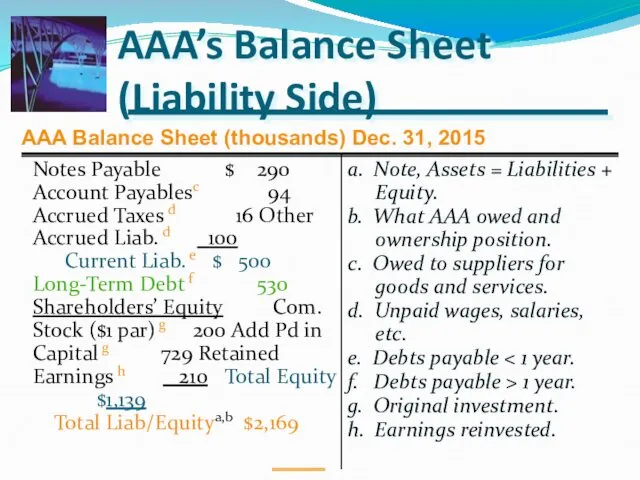

- 10. AAA’s Balance Sheet (Liability Side) a. Note, Assets = Liabilities + Equity. b. What AAA owed

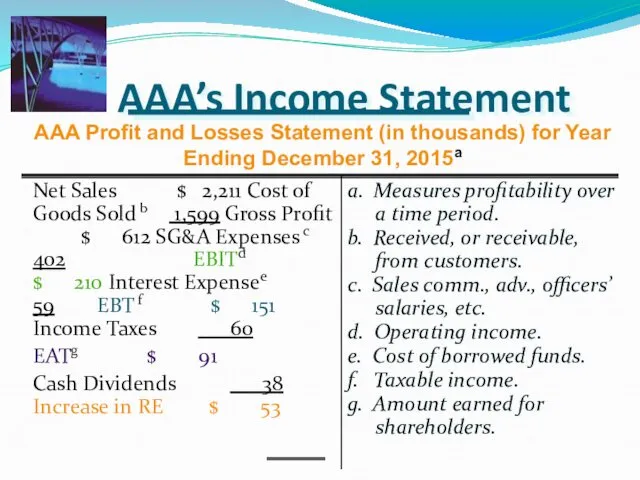

- 11. AAA’s Income Statement a. Measures profitability over a time period. b. Received, or receivable, from customers.

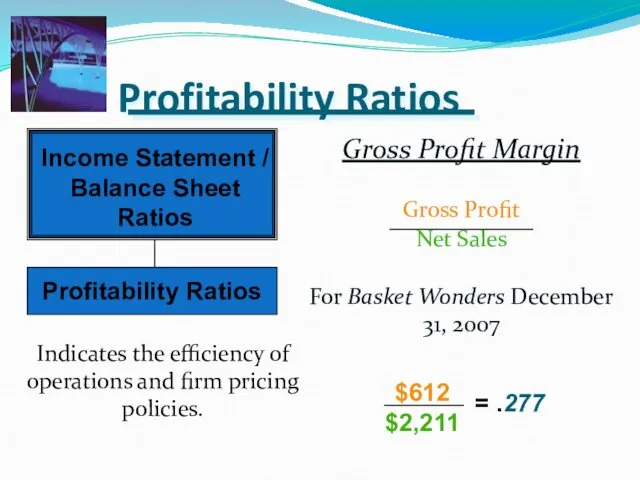

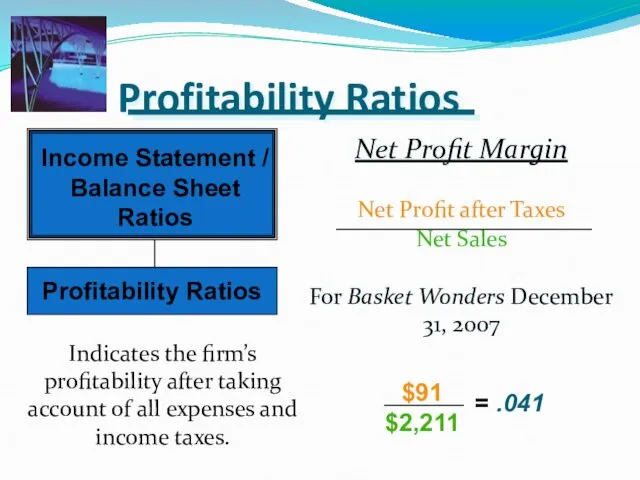

- 12. Profitability Ratios Gross Profit Margin Gross Profit Net Sales For Basket Wonders December 31, 2007 Indicates

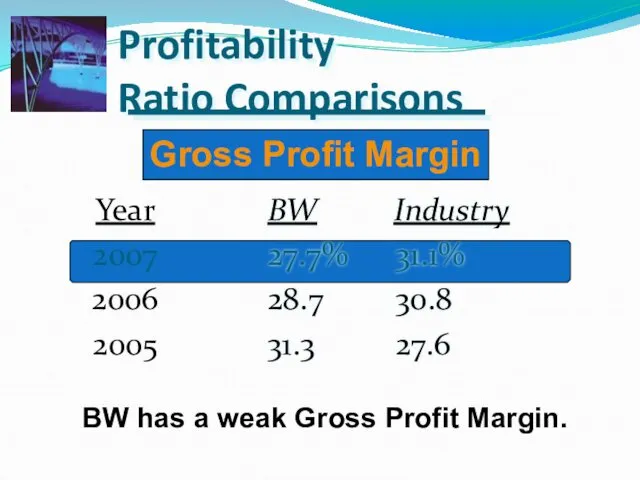

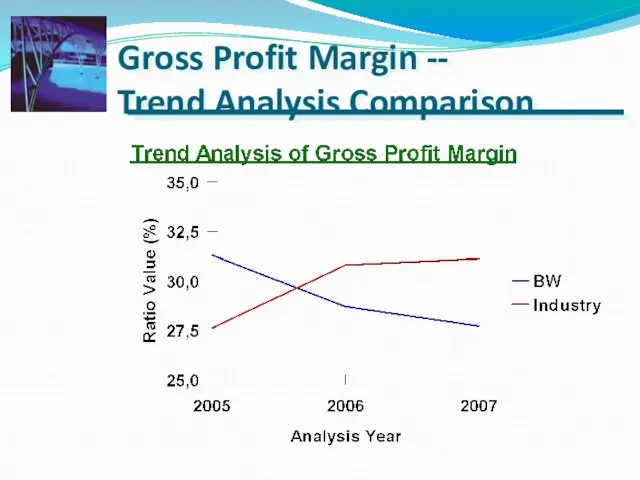

- 13. Profitability Ratio Comparisons BW Industry 27.7% 31.1% 28.7 30.8 31.3 27.6 Year 2007 2006 2005 Gross

- 14. Gross Profit Margin -- Trend Analysis Comparison

- 15. Profitability Ratios Net Profit Margin Net Profit after Taxes Net Sales For Basket Wonders December 31,

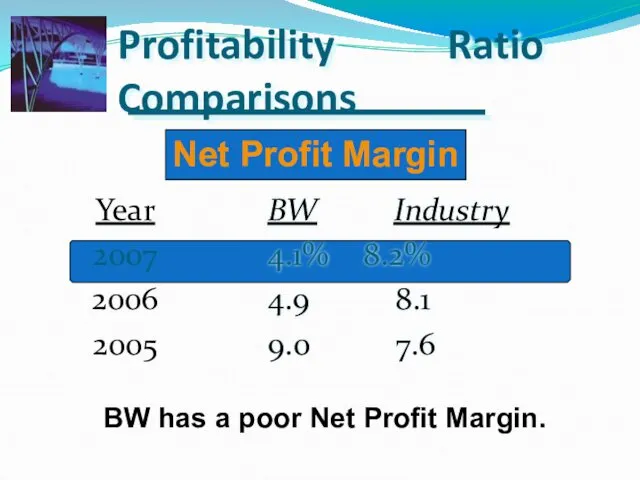

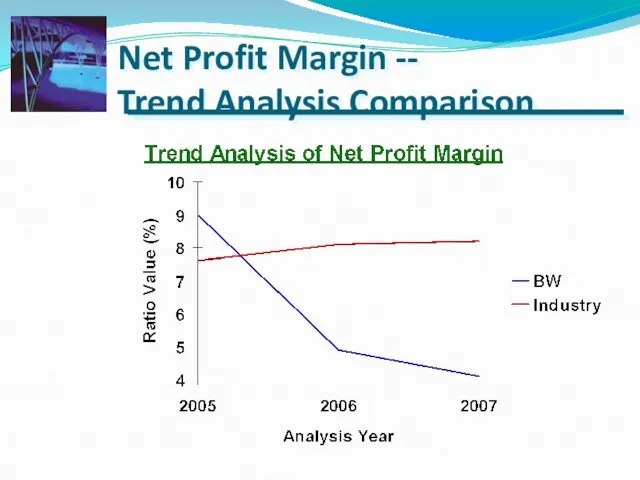

- 16. Profitability Ratio Comparisons BW Industry 4.1% 8.2% 4.9 8.1 9.0 7.6 Year 2007 2006 2005 Net

- 17. Net Profit Margin -- Trend Analysis Comparison

- 18. Profitability Ratios: Returns

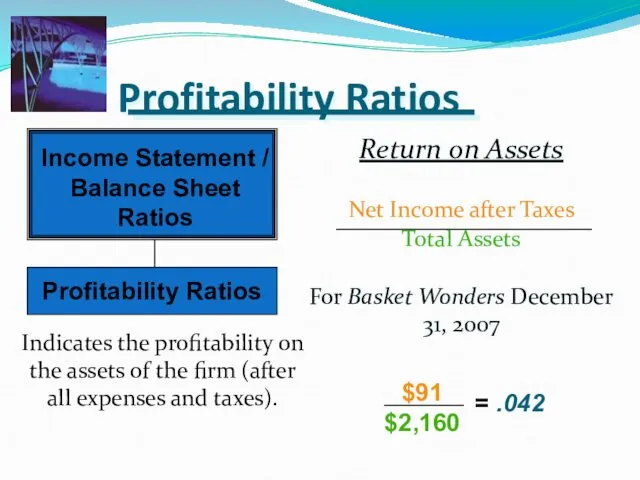

- 19. Profitability Ratios Return on Assets Net Income after Taxes Total Assets For Basket Wonders December 31,

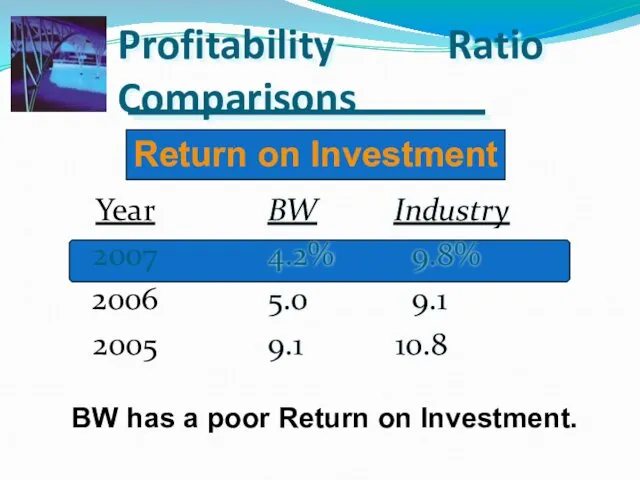

- 20. Profitability Ratio Comparisons BW Industry 4.2% 9.8% 5.0 9.1 9.1 10.8 Year 2007 2006 2005 Return

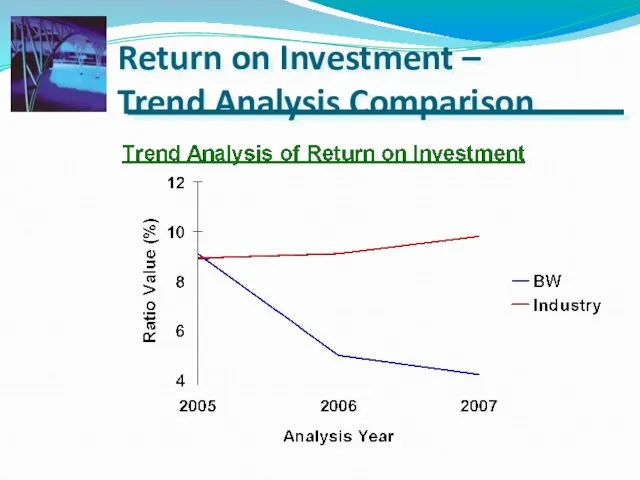

- 21. Return on Investment – Trend Analysis Comparison

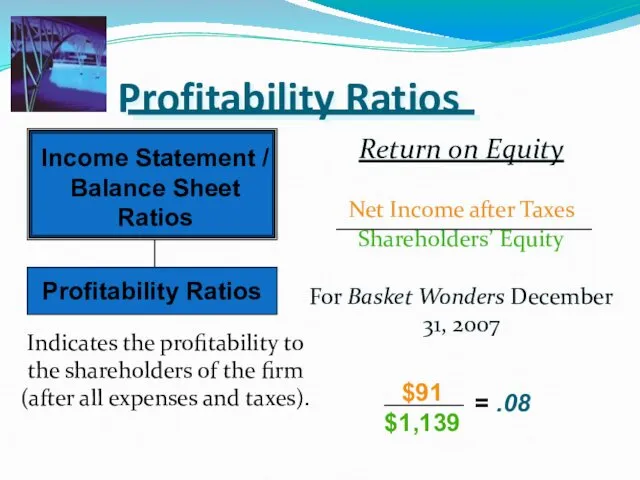

- 22. Profitability Ratios Return on Equity Net Income after Taxes Shareholders’ Equity For Basket Wonders December 31,

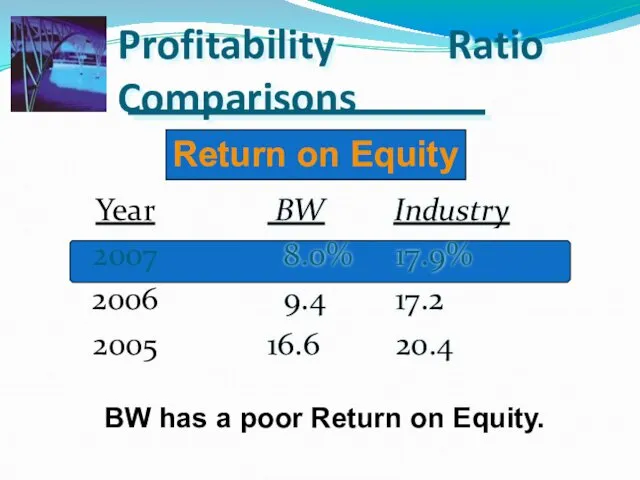

- 23. Profitability Ratio Comparisons BW Industry 8.0% 17.9% 9.4 17.2 16.6 20.4 Year 2007 2006 2005 Return

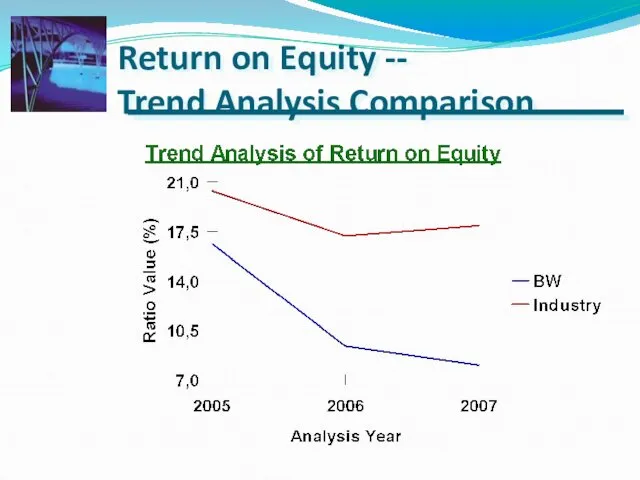

- 24. Return on Equity -- Trend Analysis Comparison

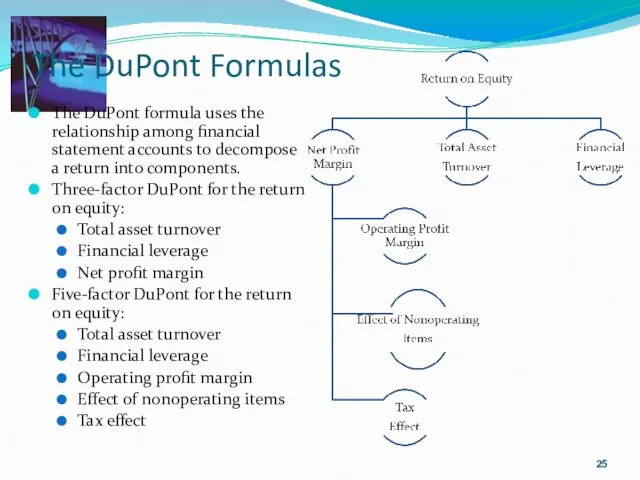

- 25. The DuPont Formulas The DuPont formula uses the relationship among financial statement accounts to decompose a

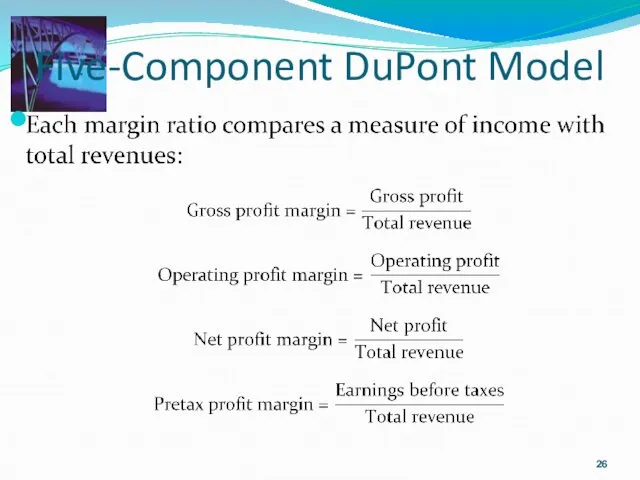

- 26. Five-Component DuPont Model

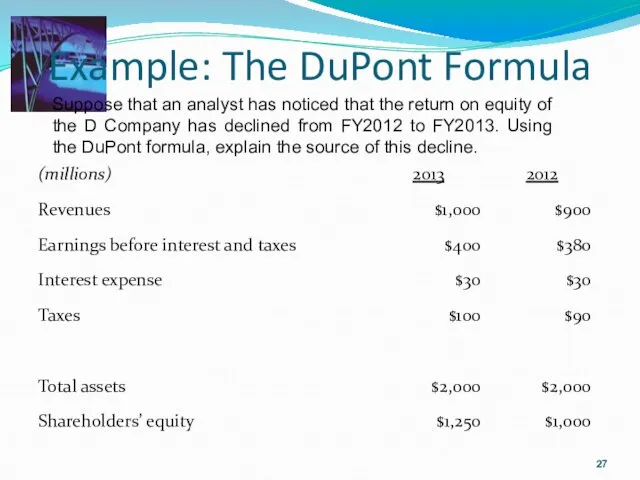

- 27. Example: The DuPont Formula Suppose that an analyst has noticed that the return on equity of

- 28. Example: the DuPont Formula

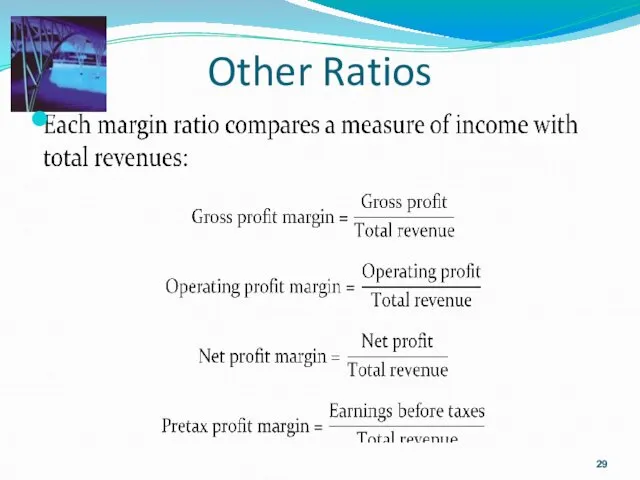

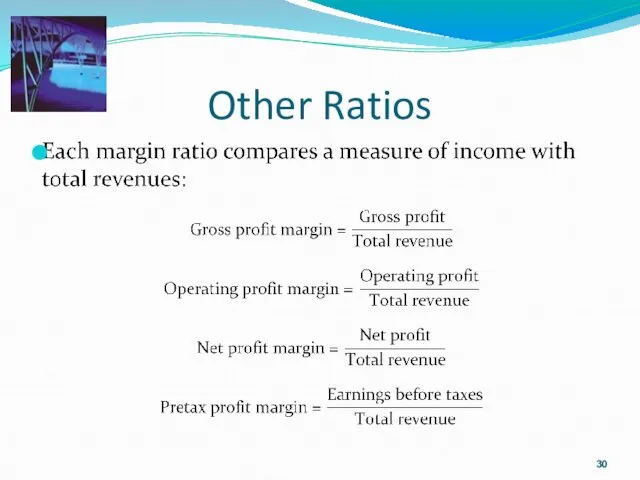

- 29. Other Ratios

- 30. Other Ratios

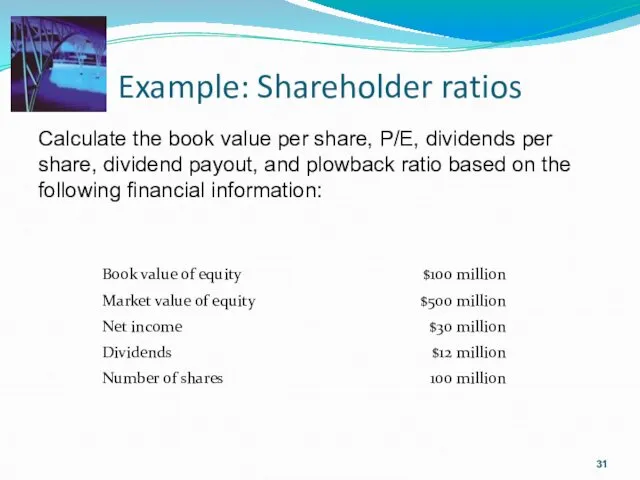

- 31. Example: Shareholder ratios Calculate the book value per share, P/E, dividends per share, dividend payout, and

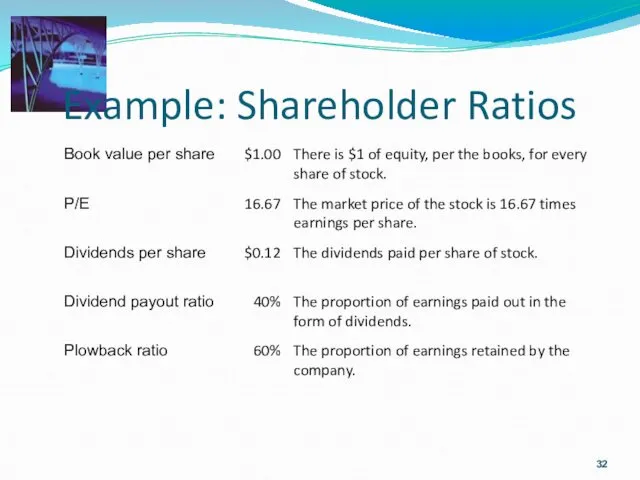

- 32. Example: Shareholder Ratios

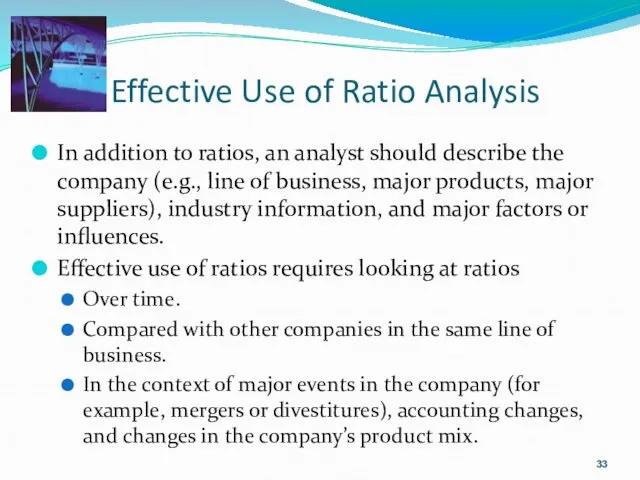

- 33. Effective Use of Ratio Analysis In addition to ratios, an analyst should describe the company (e.g.,

- 35. Скачать презентацию

Profitability

Margins and return ratios provide information on the profitability of a

Profitability

Margins and return ratios provide information on the profitability of a

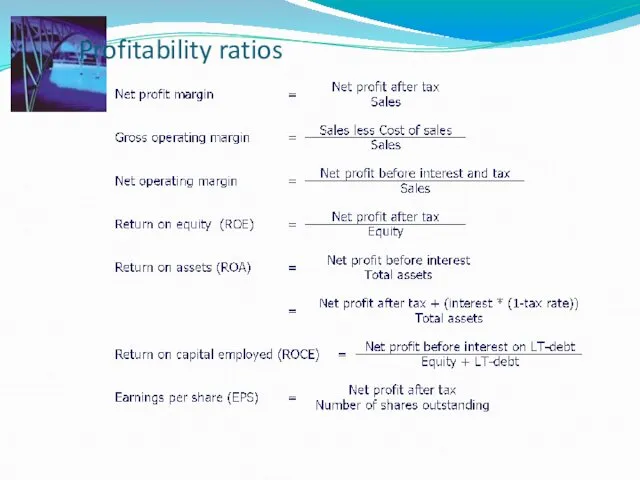

Profitability ratios

Profitability ratios

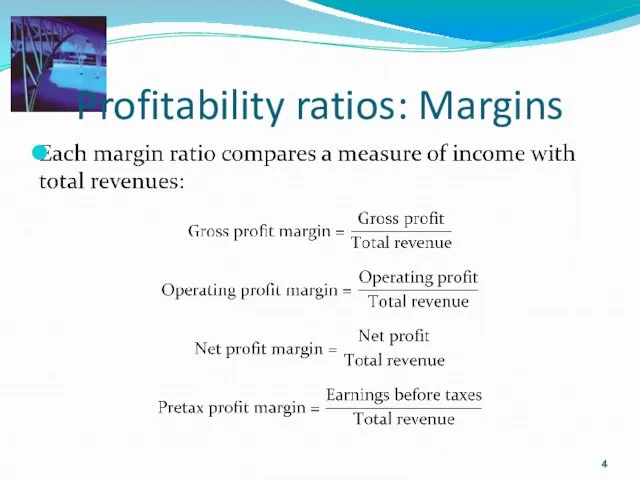

Profitability ratios: Margins

Profitability ratios: Margins

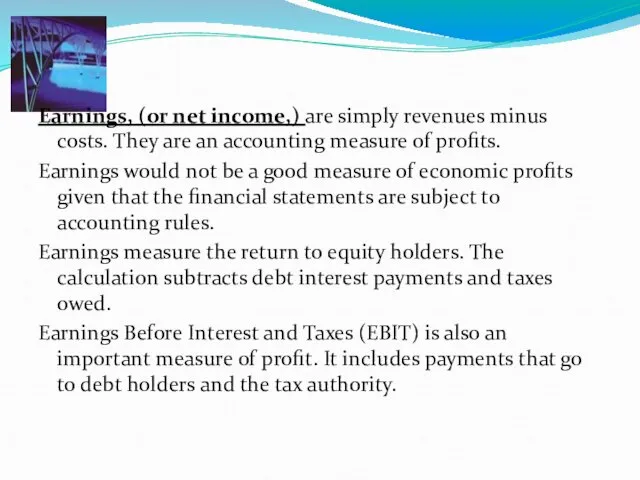

Earnings, (or net income,) are simply revenues minus costs. They are

Retained earnings

Retained earnings are the earnings re-invested into the firm:

Retained

Retained earnings

Retained earnings are the earnings re-invested into the firm:

Retained

Measuring profit

Return on equity (ROE) uses accounting values: earnings divided

Measuring profit

Return on equity (ROE) uses accounting values: earnings divided

Return on assets

Return on assets (ROA) is another important measure

Return on assets

Return on assets (ROA) is another important measure

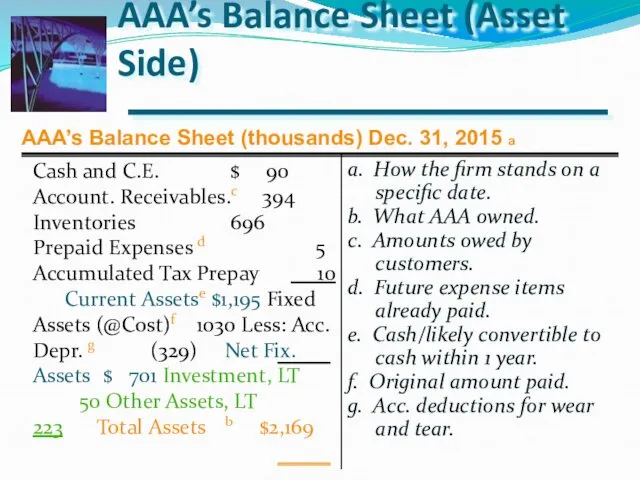

AAA’s Balance Sheet (Asset Side)

a. How the firm stands on a

AAA’s Balance Sheet (Asset Side)

a. How the firm stands on a

AAA’s Balance Sheet (Liability Side)

a. Note, Assets = Liabilities + Equity.

b.

AAA’s Balance Sheet (Liability Side)

a. Note, Assets = Liabilities + Equity.

b.

AAA’s Income Statement

a. Measures profitability over a time period.

b. Received, or

AAA’s Income Statement

a. Measures profitability over a time period.

b. Received, or

Profitability Ratios

Gross Profit Margin

Gross Profit

Net Sales

For Basket Wonders December 31, 2007

Indicates

Profitability Ratios

Gross Profit Margin

Gross Profit

Net Sales

For Basket Wonders December 31, 2007

Indicates

Profitability

Ratio Comparisons

BW Industry

27.7% 31.1%

28.7 30.8

31.3 27.6

Year

2007

2006

2005

Gross Profit Margin

BW has a weak Gross Profit Margin.

Profitability

Ratio Comparisons

BW Industry

27.7% 31.1%

28.7 30.8

31.3 27.6

Year

2007

2006

2005

Gross Profit Margin

BW has a weak Gross Profit Margin.

Gross Profit Margin --

Trend Analysis Comparison

Gross Profit Margin --

Trend Analysis Comparison

Profitability Ratios

Net Profit Margin

Net Profit after Taxes

Net Sales

For Basket Wonders December

Profitability Ratios

Net Profit Margin

Net Profit after Taxes

Net Sales

For Basket Wonders December

Profitability Ratio Comparisons

BW Industry

4.1% 8.2%

4.9 8.1

9.0 7.6

Year

2007

2006

2005

Net Profit Margin

BW has a poor Net Profit

Profitability Ratio Comparisons

BW Industry

4.1% 8.2%

4.9 8.1

9.0 7.6

Year

2007

2006

2005

Net Profit Margin

BW has a poor Net Profit

Net Profit Margin --

Trend Analysis Comparison

Net Profit Margin --

Trend Analysis Comparison

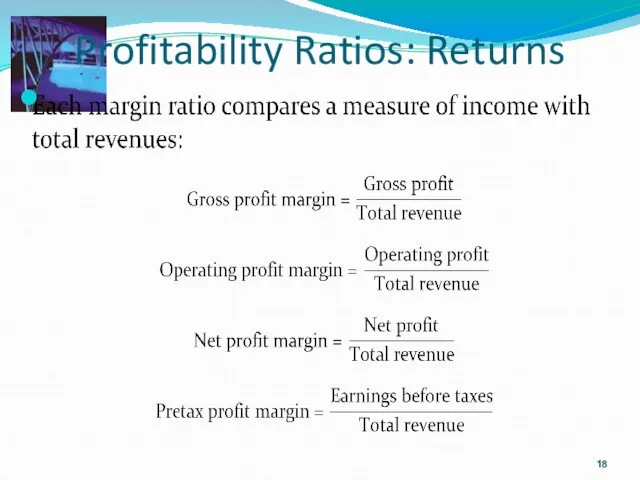

Profitability Ratios: Returns

Profitability Ratios: Returns

Profitability Ratios

Return on Assets

Net Income after Taxes

Total Assets

For Basket Wonders December

Profitability Ratios

Return on Assets

Net Income after Taxes

Total Assets

For Basket Wonders December

Profitability Ratio Comparisons

BW Industry

4.2% 9.8%

5.0 9.1

9.1 10.8

Year

2007

2006

2005

Return on Investment

BW has a poor

Profitability Ratio Comparisons

BW Industry

4.2% 9.8%

5.0 9.1

9.1 10.8

Year

2007

2006

2005

Return on Investment

BW has a poor

Return on Investment –

Trend Analysis Comparison

Return on Investment –

Trend Analysis Comparison

Profitability Ratios

Return on Equity

Net Income after Taxes

Shareholders’ Equity

For Basket Wonders December

Profitability Ratios

Return on Equity

Net Income after Taxes

Shareholders’ Equity

For Basket Wonders December

Profitability Ratio Comparisons

BW Industry

8.0% 17.9%

9.4 17.2

16.6 20.4

Year

2007

2006

2005

Return on Equity

BW has a

Profitability Ratio Comparisons

BW Industry

8.0% 17.9%

9.4 17.2

16.6 20.4

Year

2007

2006

2005

Return on Equity

BW has a

Return on Equity --

Trend Analysis Comparison

Return on Equity --

Trend Analysis Comparison

The DuPont Formulas

The DuPont formula uses the relationship among financial statement

The DuPont Formulas

The DuPont formula uses the relationship among financial statement

Five-Component DuPont Model

Five-Component DuPont Model

Example: The DuPont Formula

Suppose that an analyst has noticed that the

Example: The DuPont Formula

Suppose that an analyst has noticed that the

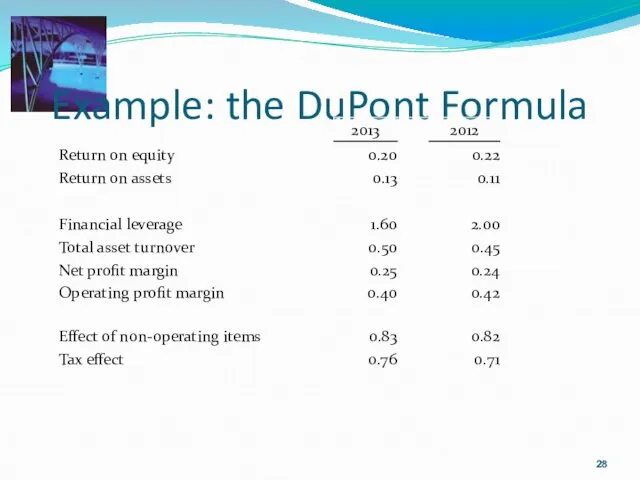

Example: the DuPont Formula

Example: the DuPont Formula

Other Ratios

Other Ratios

Other Ratios

Other Ratios

Example: Shareholder ratios

Calculate the book value per share, P/E, dividends per

Example: Shareholder ratios

Calculate the book value per share, P/E, dividends per

Example: Shareholder Ratios

Example: Shareholder Ratios

Effective Use of Ratio Analysis

In addition to ratios, an analyst should

Effective Use of Ratio Analysis

In addition to ratios, an analyst should

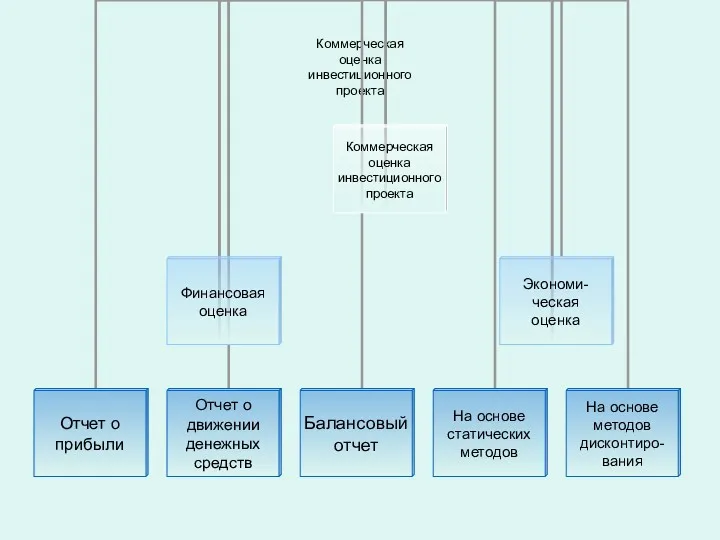

Оценка инвестиционного проекта

Оценка инвестиционного проекта Повышение заработной платы классным руководителям и молодым специалистам общеобразовательных организаций с 01.09. 2018 года

Повышение заработной платы классным руководителям и молодым специалистам общеобразовательных организаций с 01.09. 2018 года Спрос на деньги (классическая и кейнсианская концепции). Модель предложения денег. Равновесие на денежном рынке

Спрос на деньги (классическая и кейнсианская концепции). Модель предложения денег. Равновесие на денежном рынке Продукт Доктор Ресо. Екатеринбург. Добровольное медицинское страхование физических лиц

Продукт Доктор Ресо. Екатеринбург. Добровольное медицинское страхование физических лиц Валюта_2023_УЧЕБНАЯ

Валюта_2023_УЧЕБНАЯ Андеррайтинговые операции банков

Андеррайтинговые операции банков Правове регулювання ринку цінних паперів

Правове регулювання ринку цінних паперів Внесення змін до стипендійного забезпечення студентів

Внесення змін до стипендійного забезпечення студентів Формирование и анализ финансовой отчетности

Формирование и анализ финансовой отчетности Учет кассовых операций. Презентации и их роль в образовательном процессе

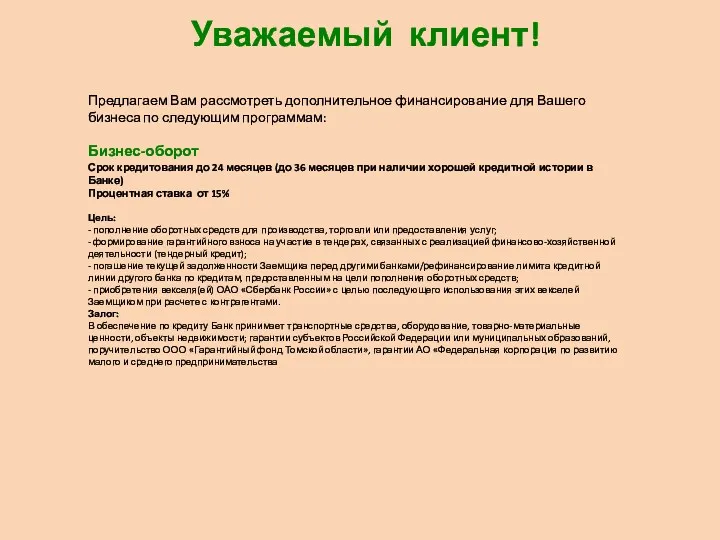

Учет кассовых операций. Презентации и их роль в образовательном процессе Коммерческое предложение по кредитованию и банковской гарантии

Коммерческое предложение по кредитованию и банковской гарантии Оказание поддержки субъектам малого и среднего предпринимательства Корпорацией МСП в период 2015-2018 годов

Оказание поддержки субъектам малого и среднего предпринимательства Корпорацией МСП в период 2015-2018 годов Операции на международном валютном рынке

Операции на международном валютном рынке Сущность, функции и роль страхования

Сущность, функции и роль страхования Тарифная политика в страховании

Тарифная политика в страховании Роль грошей у ринковій економіці

Роль грошей у ринковій економіці Банковские услуги и отношения людей с банками

Банковские услуги и отношения людей с банками Дробление бизнеса

Дробление бизнеса Правовое регулирование рынка ценных бумаг

Правовое регулирование рынка ценных бумаг Единый налог на вменённый доход для отдельных видов деятельности (ЕНВД)

Единый налог на вменённый доход для отдельных видов деятельности (ЕНВД) Зарубіжний досвід забезпечення безпеки банківської діяльності

Зарубіжний досвід забезпечення безпеки банківської діяльності Российская компания “Сonsulting club”

Российская компания “Сonsulting club” Коммерческие предложения. Продажа объектов недвижимости

Коммерческие предложения. Продажа объектов недвижимости Історія виникнення та розвитку аудиту

Історія виникнення та розвитку аудиту Этика оценщиков

Этика оценщиков Инициативное предложение члена бюджетной комиссии Ефимовой Ольги Александровны в рамках проекта Народный бюджет

Инициативное предложение члена бюджетной комиссии Ефимовой Ольги Александровны в рамках проекта Народный бюджет Учет поступления и расходования денежных средств (на примере НИИЦ (г. Курск) ФГУП 18 ЦНИИ МО РФ)

Учет поступления и расходования денежных средств (на примере НИИЦ (г. Курск) ФГУП 18 ЦНИИ МО РФ) Учет операций по привлечению денежных средств по договорам займа и кредитным договорам. Глава 6

Учет операций по привлечению денежных средств по договорам займа и кредитным договорам. Глава 6