- Foreign exchange risk

Содержание

- 2. AGENDA: FOREX RISK Sources of foreign exchange risk and FX trading activities; FX risk and hedging:

- 3. Sources of FX Risk Spot positions denominated in foreign currency Forward positions denominated in foreign currency

- 4. Problem 1 Bank has Euro 14 million in assets and Euro 23 million in liabilities and

- 5. FX Risk Exposure Greater exposure to a foreign currency combined with greater volatility of the foreign

- 6. Trading Activities Basically 4 trading activities: Purchase and sale of currencies to complete international transactions. Facilitating

- 7. Foreign Assets & Liabilities Mismatches between foreign asset and liability portfolios. Ability to raise funds from

- 8. Return and Risk of Foreign Investments Returns are affected by: Spread between costs and revenues Changes

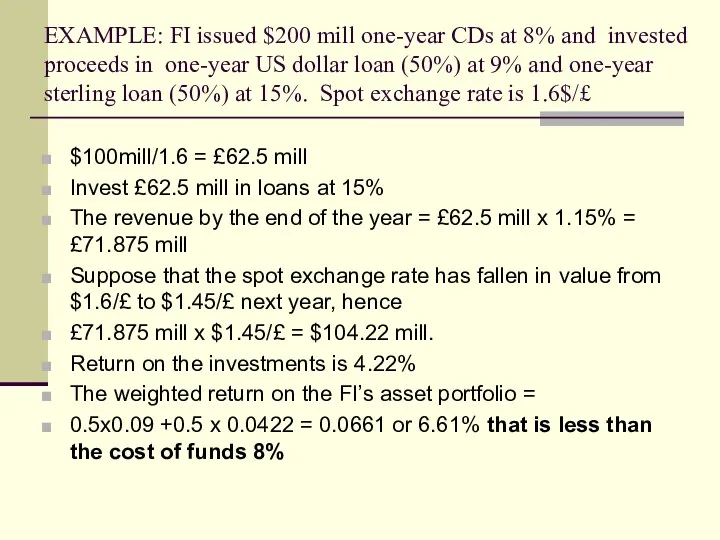

- 9. EXAMPLE: FI issued $200 mill one-year CDs at 8% and invested proceeds in one-year US dollar

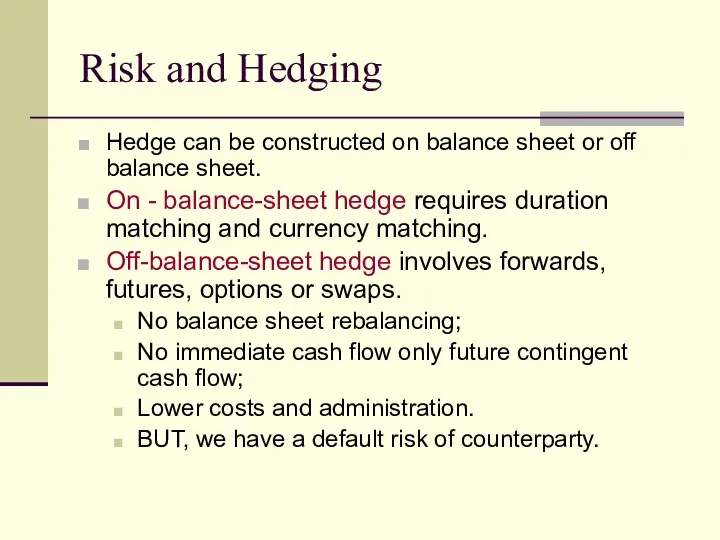

- 10. Risk and Hedging Hedge can be constructed on balance sheet or off balance sheet. On -

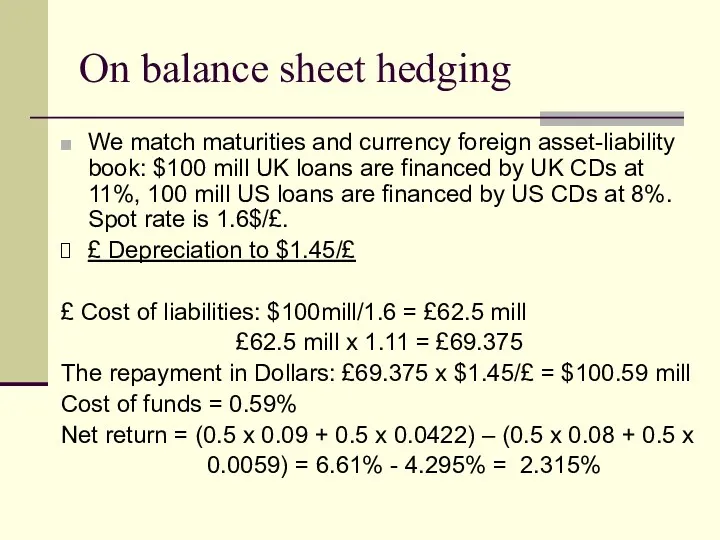

- 11. On balance sheet hedging We match maturities and currency foreign asset-liability book: $100 mill UK loans

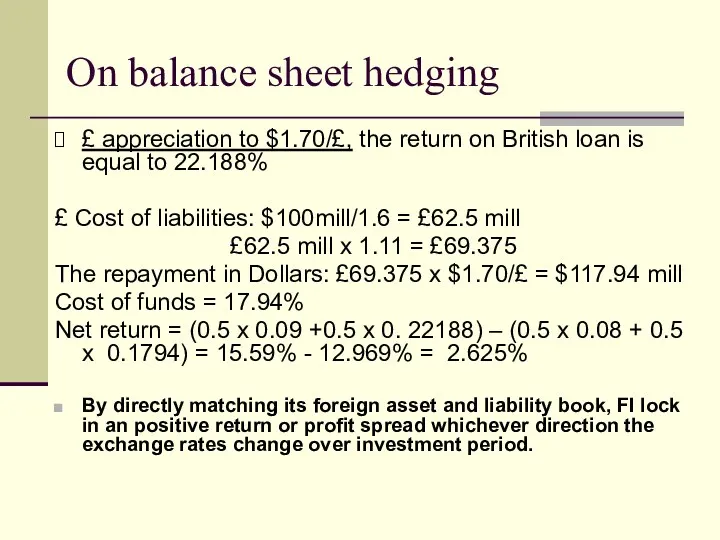

- 12. £ appreciation to $1.70/£, the return on British loan is equal to 22.188% £ Cost of

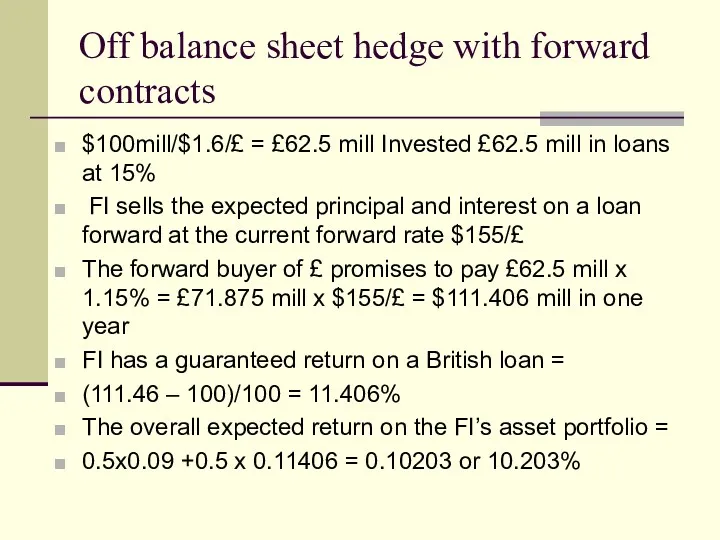

- 13. Off balance sheet hedge with forward contracts $100mill/$1.6/£ = £62.5 mill Invested £62.5 mill in loans

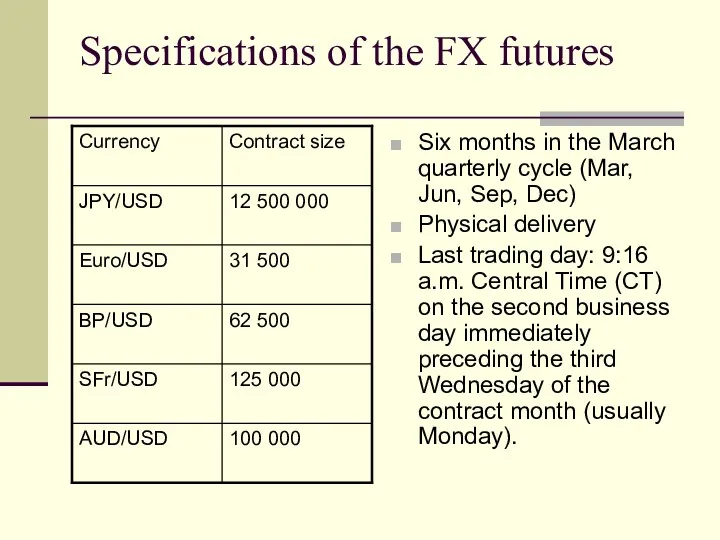

- 14. Specifications of the FX futures Six months in the March quarterly cycle (Mar, Jun, Sep, Dec)

- 15. Hedging with futures. What is your risk if you have a long position in FX futures?

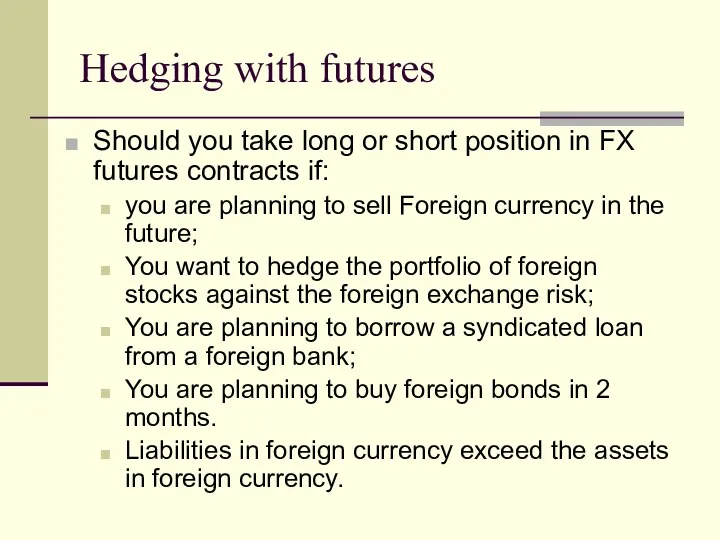

- 16. Hedging with futures Should you take long or short position in FX futures contracts if: you

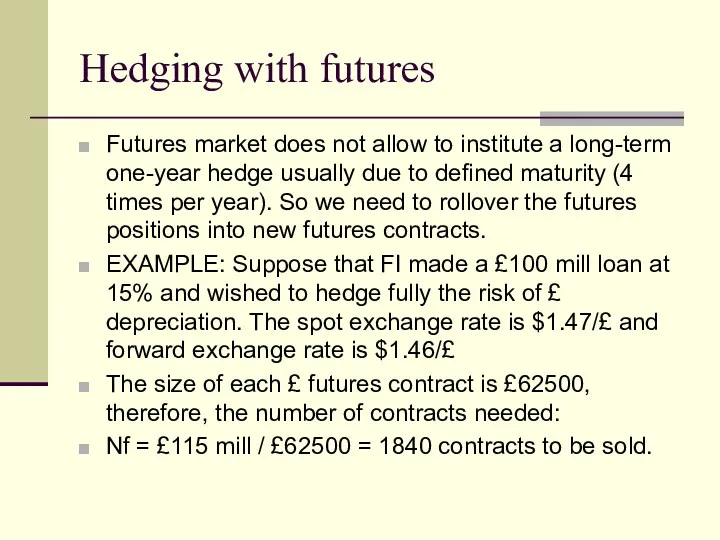

- 17. Hedging with futures Futures market does not allow to institute a long-term one-year hedge usually due

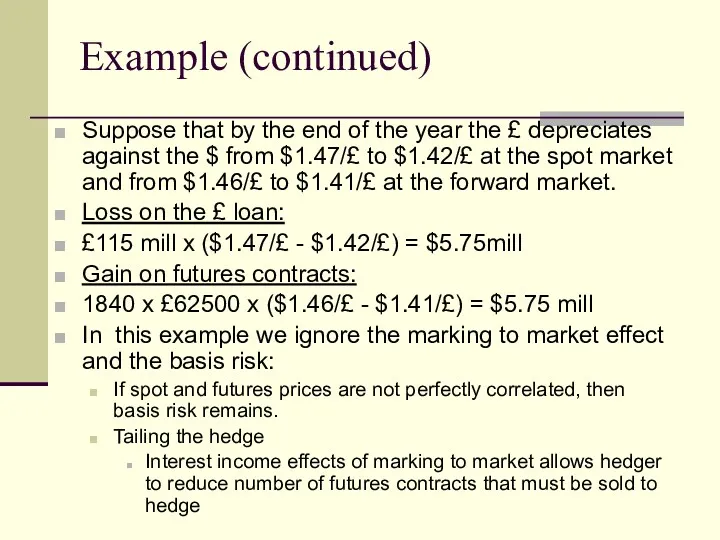

- 18. Example (continued) Suppose that by the end of the year the £ depreciates against the $

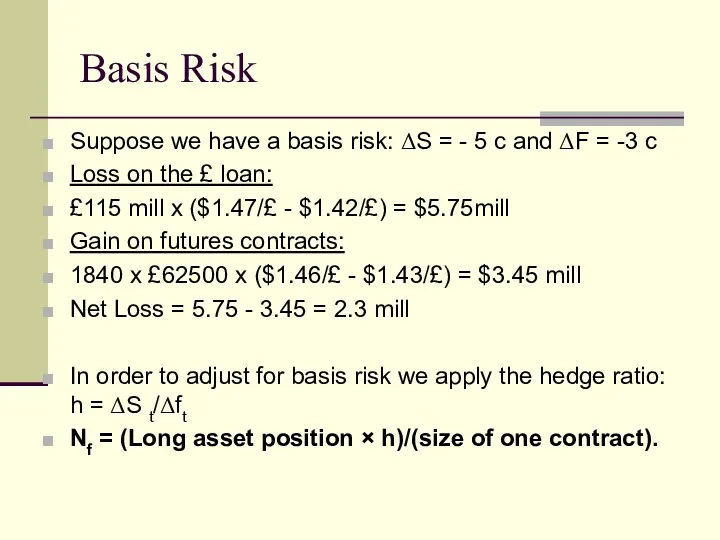

- 19. Basis Risk Suppose we have a basis risk: ΔS = - 5 c and ΔF =

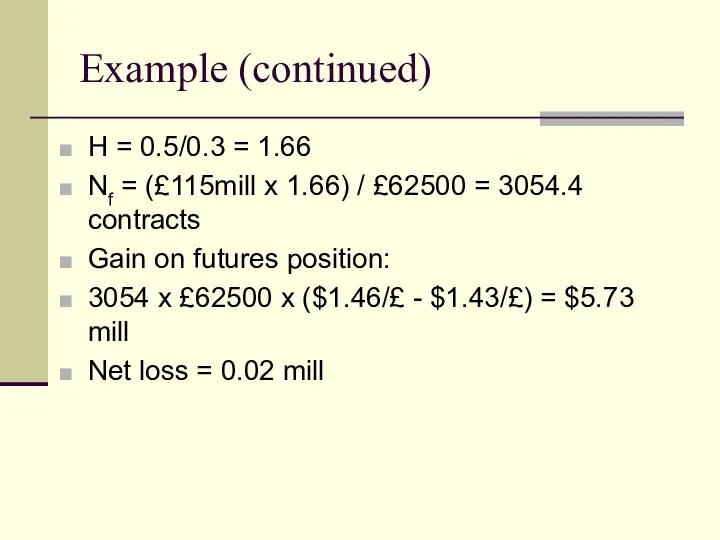

- 20. Example (continued) H = 0.5/0.3 = 1.66 Nf = (£115mill x 1.66) / £62500 = 3054.4

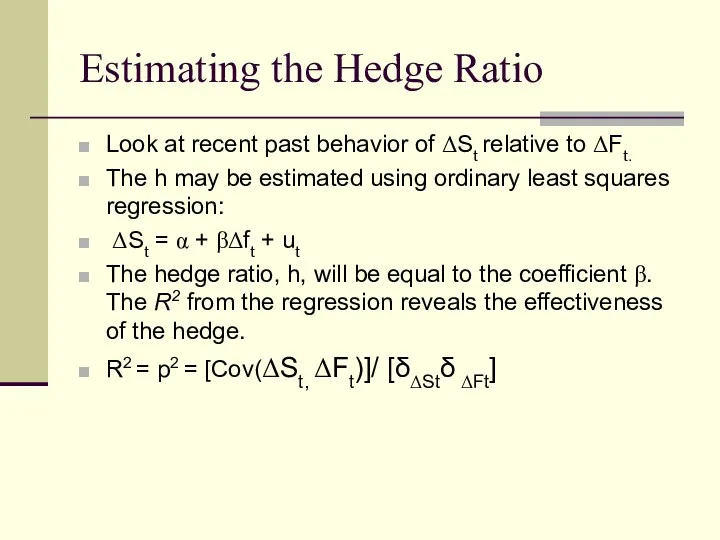

- 21. Estimating the Hedge Ratio Look at recent past behavior of ΔSt relative to ΔFt. The h

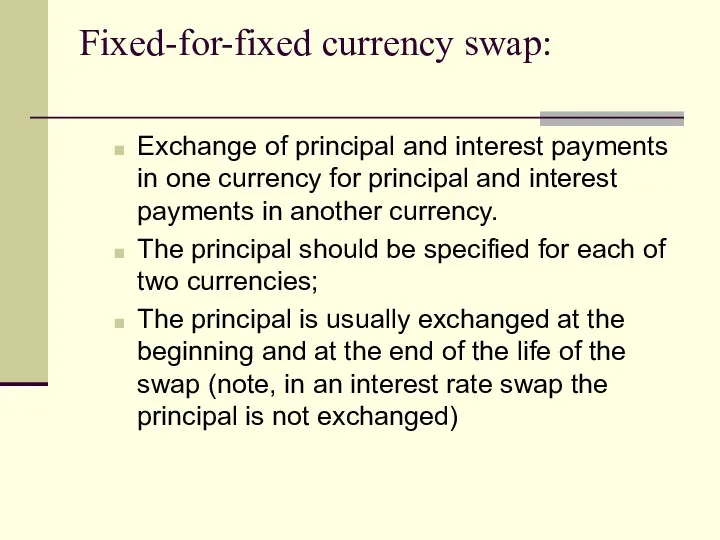

- 22. Fixed-for-fixed currency swap: Exchange of principal and interest payments in one currency for principal and interest

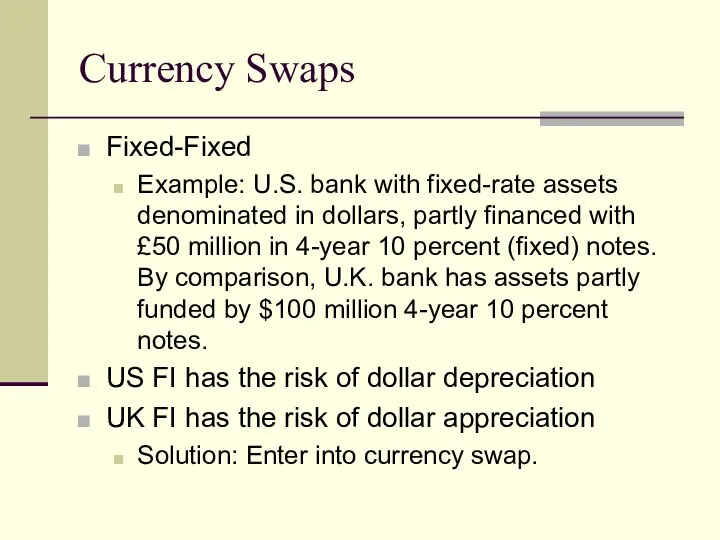

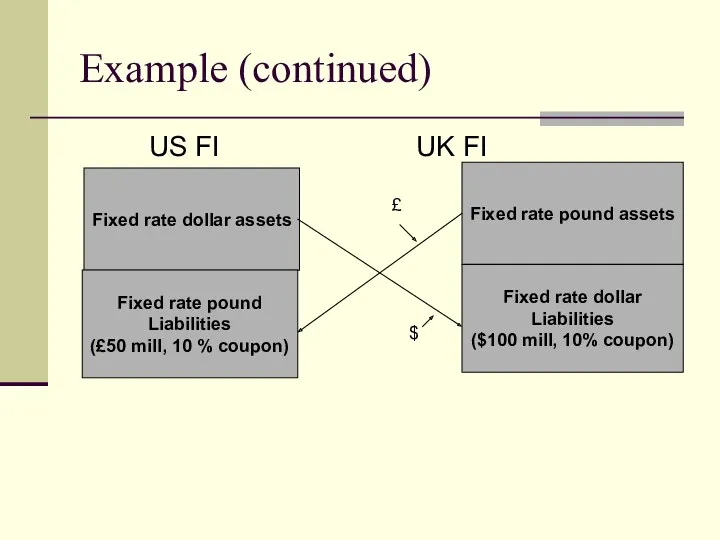

- 23. Currency Swaps Fixed-Fixed Example: U.S. bank with fixed-rate assets denominated in dollars, partly financed with £50

- 24. Example (continued) US FI UK FI Fixed rate dollar assets Fixed rate pound Liabilities (£50 mill,

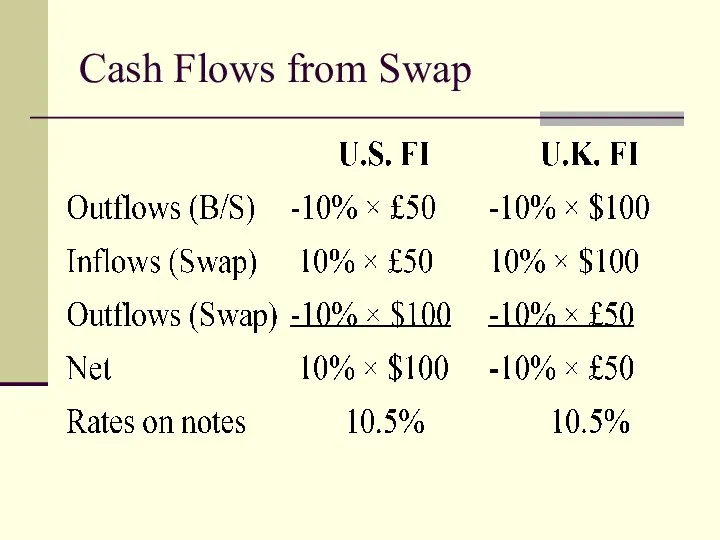

- 25. Cash Flows from Swap

- 26. Fixed-Floating + Currency Fixed-Floating currency swaps. Allows hedging of interest rate and currency exposures simultaneously Example:

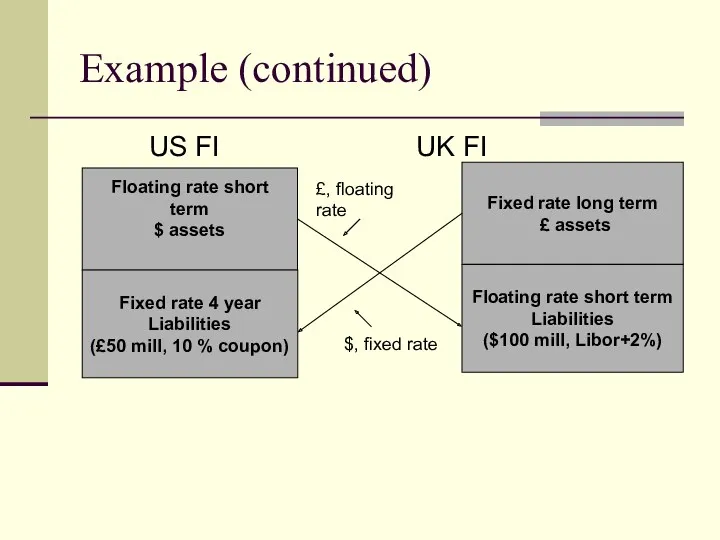

- 27. Example (continued) US FI UK FI Floating rate short term $ assets Fixed rate 4 year

- 29. Скачать презентацию

AGENDA: FOREX RISK

Sources of foreign exchange risk and FX trading activities;

FX

AGENDA: FOREX RISK

Sources of foreign exchange risk and FX trading activities;

FX

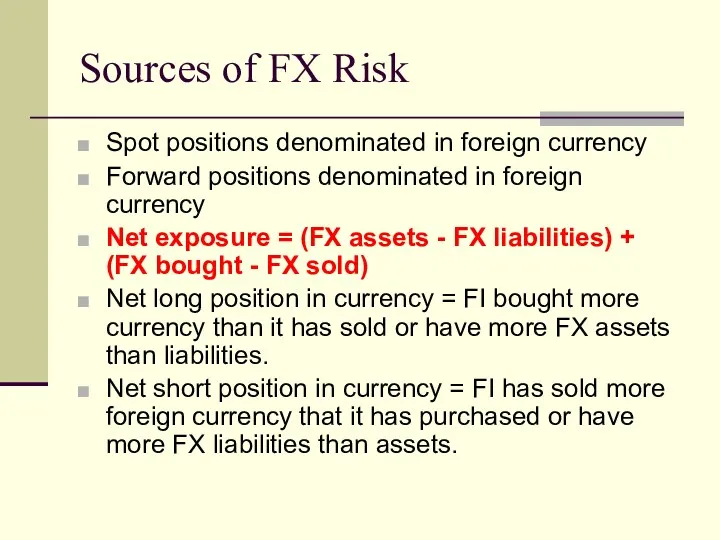

Sources of FX Risk

Spot positions denominated in foreign currency

Forward positions denominated

Sources of FX Risk

Spot positions denominated in foreign currency

Forward positions denominated

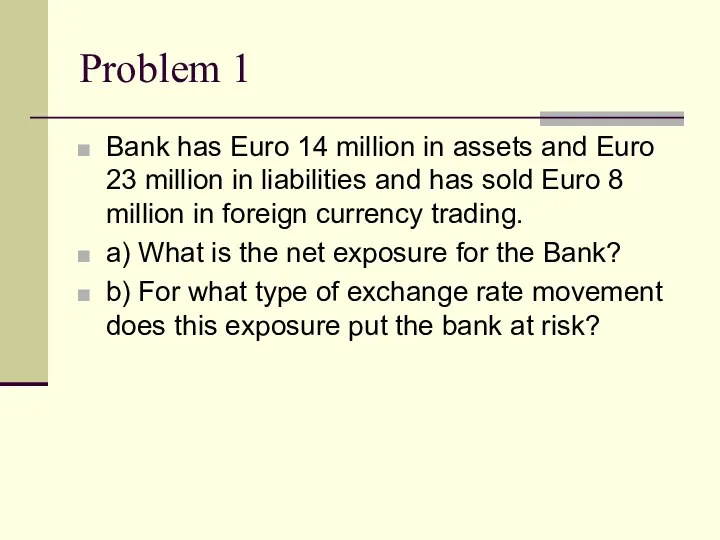

Problem 1

Bank has Euro 14 million in assets and Euro 23

Problem 1

Bank has Euro 14 million in assets and Euro 23

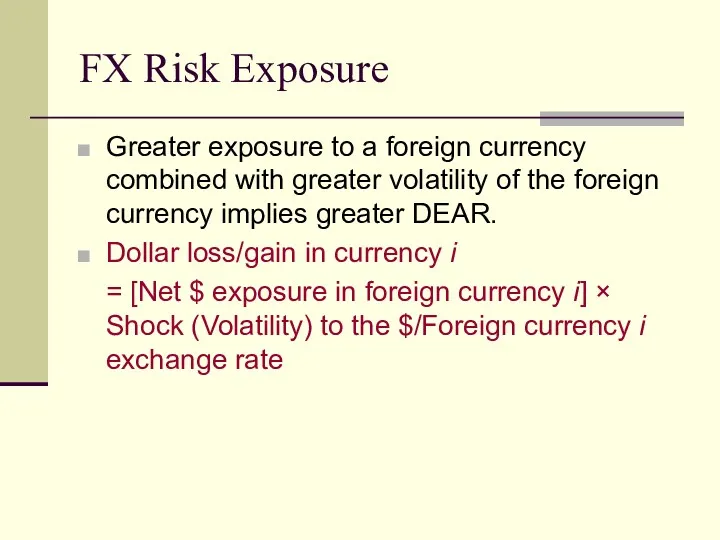

FX Risk Exposure

Greater exposure to a foreign currency combined with greater

FX Risk Exposure

Greater exposure to a foreign currency combined with greater

Trading Activities

Basically 4 trading activities:

Purchase and sale of currencies to complete

Trading Activities

Basically 4 trading activities:

Purchase and sale of currencies to complete

Foreign Assets & Liabilities

Mismatches between foreign asset and liability portfolios.

Ability

Foreign Assets & Liabilities

Mismatches between foreign asset and liability portfolios.

Ability

Return and Risk of

Foreign Investments

Returns are affected by:

Spread between costs

Return and Risk of

Foreign Investments

Returns are affected by:

Spread between costs

EXAMPLE: FI issued $200 mill one-year CDs at 8% and invested

EXAMPLE: FI issued $200 mill one-year CDs at 8% and invested

Risk and Hedging

Hedge can be constructed on balance sheet or off

Risk and Hedging

Hedge can be constructed on balance sheet or off

On balance sheet hedging

We match maturities and currency foreign asset-liability book:

On balance sheet hedging

We match maturities and currency foreign asset-liability book:

£ appreciation to $1.70/£, the return on British loan is

£ appreciation to $1.70/£, the return on British loan is

Off balance sheet hedge with forward contracts

$100mill/$1.6/£ = £62.5 mill Invested

Off balance sheet hedge with forward contracts

$100mill/$1.6/£ = £62.5 mill Invested

Specifications of the FX futures

Six months in the March quarterly cycle

Specifications of the FX futures

Six months in the March quarterly cycle

Hedging with futures.

What is your risk if you have a long

Hedging with futures.

What is your risk if you have a long

Hedging with futures

Should you take long or short position in FX

Hedging with futures

Should you take long or short position in FX

Hedging with futures

Futures market does not allow to institute a long-term

Hedging with futures

Futures market does not allow to institute a long-term

Example (continued)

Suppose that by the end of the year the £

Example (continued)

Suppose that by the end of the year the £

Basis Risk

Suppose we have a basis risk: ΔS = - 5

Basis Risk

Suppose we have a basis risk: ΔS = - 5

Example (continued)

H = 0.5/0.3 = 1.66

Nf = (£115mill x 1.66)

Example (continued)

H = 0.5/0.3 = 1.66

Nf = (£115mill x 1.66)

Estimating the Hedge Ratio

Look at recent past behavior of ΔSt relative

Estimating the Hedge Ratio

Look at recent past behavior of ΔSt relative

Fixed-for-fixed currency swap:

Exchange of principal and interest payments in one

Fixed-for-fixed currency swap:

Exchange of principal and interest payments in one

Currency Swaps

Fixed-Fixed

Example: U.S. bank with fixed-rate assets denominated in dollars,

Currency Swaps

Fixed-Fixed

Example: U.S. bank with fixed-rate assets denominated in dollars,

Example (continued)

US FI UK FI

Fixed rate dollar assets

Fixed rate

Example (continued)

US FI UK FI

Fixed rate dollar assets

Fixed rate

Cash Flows from Swap

Cash Flows from Swap

Fixed-Floating + Currency

Fixed-Floating currency swaps.

Allows hedging of interest rate and currency

Fixed-Floating + Currency

Fixed-Floating currency swaps.

Allows hedging of interest rate and currency

Example (continued)

US FI UK FI

Floating rate short term

$ assets

Fixed

Example (continued)

US FI UK FI

Floating rate short term

$ assets

Fixed

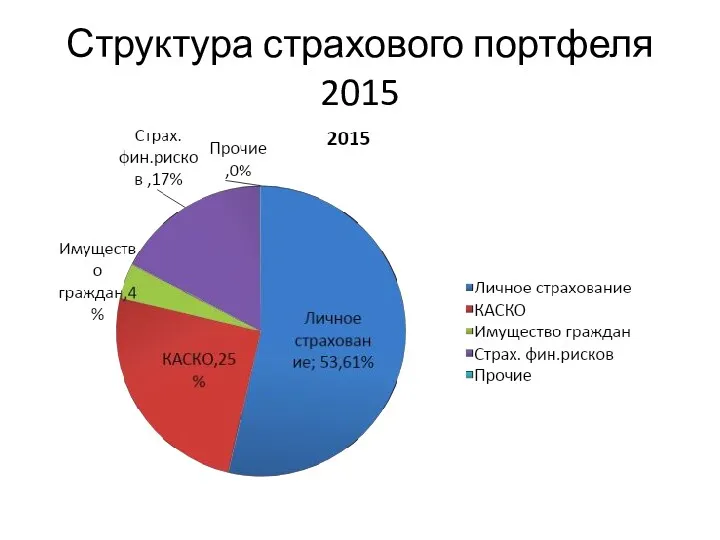

Структура страхового портфеля 2015

Структура страхового портфеля 2015 Отчет об исполнении бюджета Бардымского муниципального района за 2019 год

Отчет об исполнении бюджета Бардымского муниципального района за 2019 год Таможенные платежи в различных таможенных процедурах

Таможенные платежи в различных таможенных процедурах Бизнес-процесстерді ұйымдасыру мен ресурстарды қолданудың динамикалық талдауы

Бизнес-процесстерді ұйымдасыру мен ресурстарды қолданудың динамикалық талдауы Финансовый раздел. Ожидаемые финансовые результаты деятельности проектируемого предприятия

Финансовый раздел. Ожидаемые финансовые результаты деятельности проектируемого предприятия Налоги. Практикум

Налоги. Практикум Финансовые аспекты страховой деятельности

Финансовые аспекты страховой деятельности Появление денег на Руси

Появление денег на Руси Доходы. Общие правила определения доходов для целей налогообложения

Доходы. Общие правила определения доходов для целей налогообложения Учет материально-производственных запасов

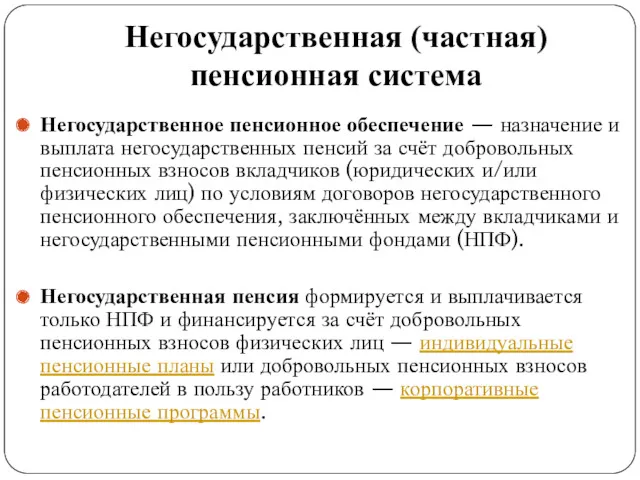

Учет материально-производственных запасов Негосударственная (частная) пенсионная система

Негосударственная (частная) пенсионная система Программно – целевое управление в муниципальных образованиях

Программно – целевое управление в муниципальных образованиях Правила призначення стипендій у Кременецькому медичному училищі

Правила призначення стипендій у Кременецькому медичному училищі Налог на добычу полезных ископаемых

Налог на добычу полезных ископаемых Страхование ответсвенности

Страхование ответсвенности О заполнении формы справки о доходах, расходах, об имуществе и обязательствах имущественного характера в 2018 году

О заполнении формы справки о доходах, расходах, об имуществе и обязательствах имущественного характера в 2018 году Лизинг как метод финансирования инвестиционных проектов

Лизинг как метод финансирования инвестиционных проектов Банковская карта для зачислений пенсий Карта Долголетия

Банковская карта для зачислений пенсий Карта Долголетия Платежная система России: проблемы и перспективы развития

Платежная система России: проблемы и перспективы развития Семейный бюджет (2). 3 класс

Семейный бюджет (2). 3 класс Риск- диверсификация и CAPM

Риск- диверсификация и CAPM Ўзбекистон Республикаси Марказий банки

Ўзбекистон Республикаси Марказий банки Ипотека. Новое по ипотеке: ипотечный брокер для агентств недвижимости

Ипотека. Новое по ипотеке: ипотечный брокер для агентств недвижимости Медиация в страховании

Медиация в страховании Контроль выплаты пенсий и иных социальных выплат

Контроль выплаты пенсий и иных социальных выплат Фундаментальный анализ финансовых рынков

Фундаментальный анализ финансовых рынков The problems of the active operations of commercial banks

The problems of the active operations of commercial banks Налоговый контроль

Налоговый контроль