- How much for your company?

Содержание

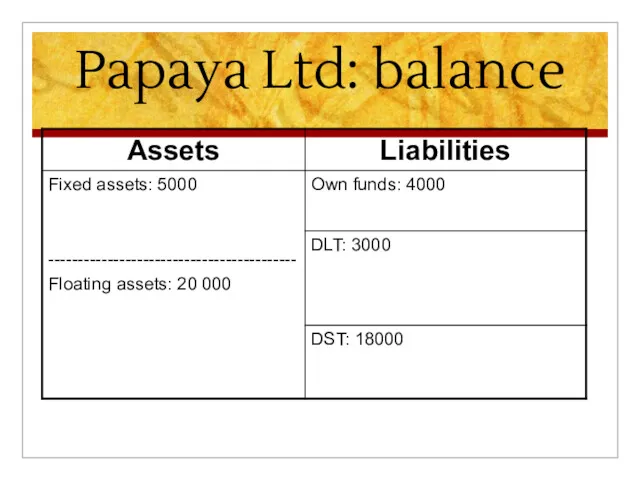

- 2. Papaya Ltd: balance

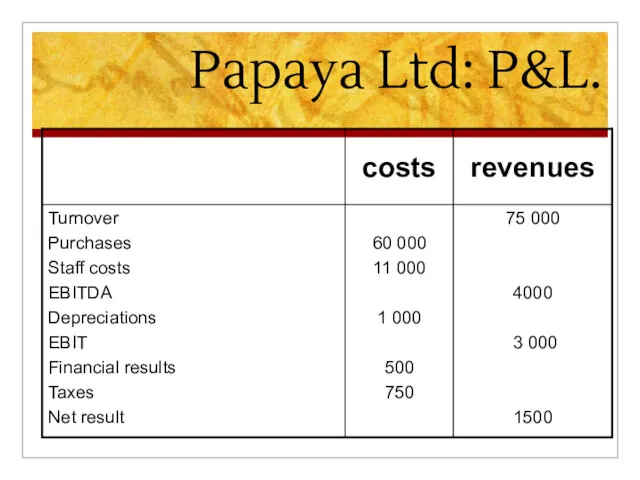

- 3. Papaya Ltd: P&L.

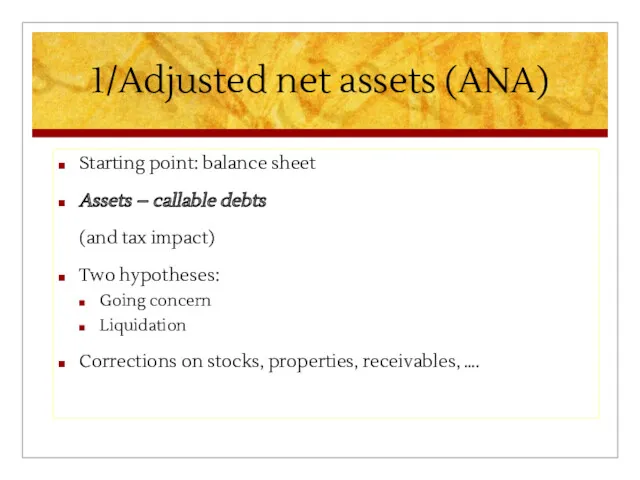

- 4. 1/Adjusted net assets (ANA) Starting point: balance sheet Assets – callable debts (and tax impact) Two

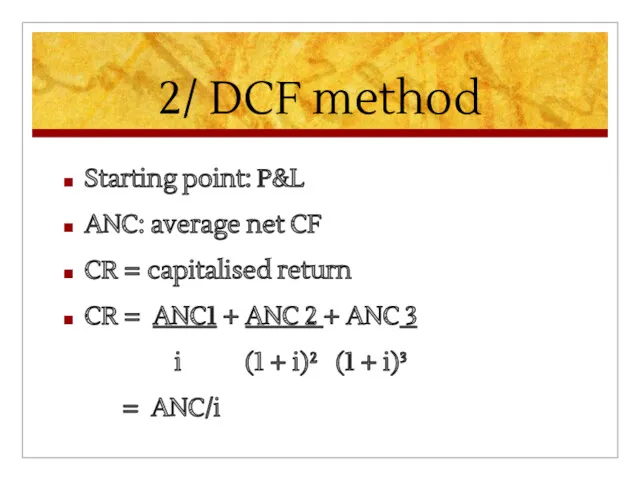

- 5. 2/ DCF method Starting point: P&L ANC: average net CF CR = capitalised return CR =

- 6. 3/ « objective » value ANA + CR 2 The value of a company is what

- 7. 4. Multiples or multiplier Value of the company multiplier Times turnover or EBIT or EBITDA (earnings

- 8. Multiples: Mid market index

- 9. Anorganic growth Assets very limited Mainly human resources Few « tangibles » No CF, only cash

- 10. Anorganic growth CF The valley of death Time

- 11. 1.Comparables Compare with: Quoted companies: p/e ratio X x EBIT Similar companies Info via solicitors, chambers

- 12. 2. Option approach V = ΣCF/i + go GO = growth-opportunities USP R&D Example: Compaq, Microsoft,

- 13. 3. De residual value: six steps approach Determine at what point the company will get profitable

- 14. Kimberley Ltd Toothbrush on solar energy BR1: 100 000, BR 2: 50 000, BR3 = 0

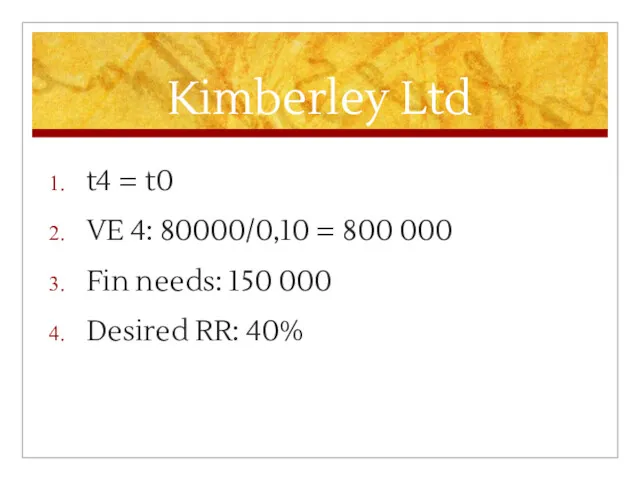

- 15. Kimberley Ltd t4 = t0 VE 4: 80000/0,10 = 800 000 Fin needs: 150 000 Desired

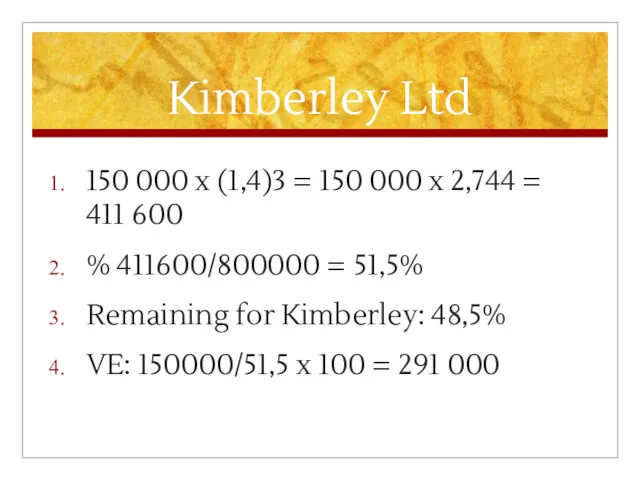

- 16. Kimberley Ltd 150 000 x (1,4)3 = 150 000 x 2,744 = 411 600 % 411600/800000

- 17. 3. De residual value: without investor Time: from yr 5: CF 250 000 DCF: 250 000/10%

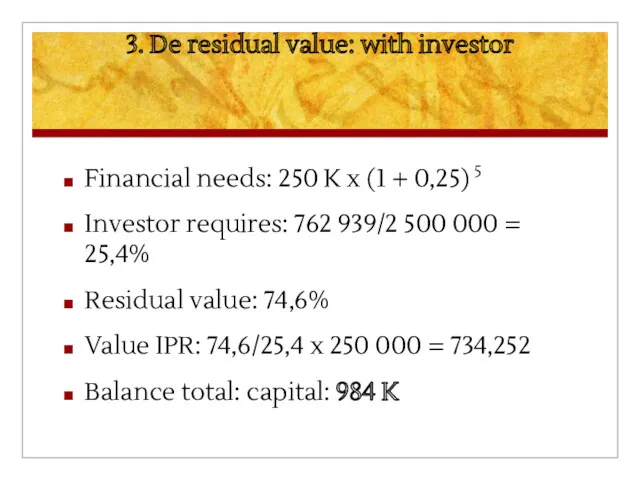

- 18. 3. De residual value: with investor Financial needs: 250 K x (1 + 0,25) 5 Investor

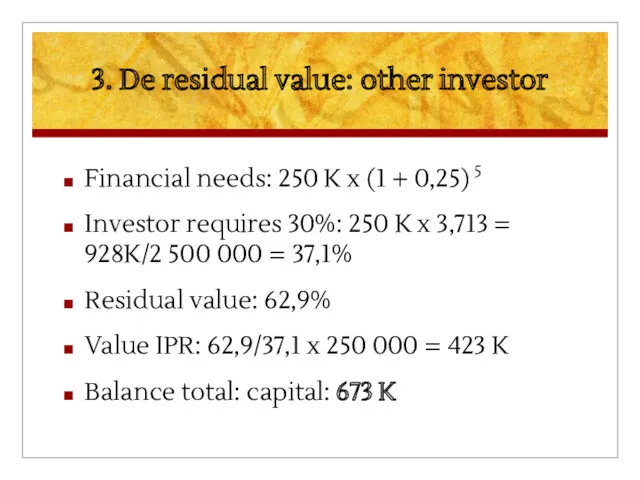

- 19. 3. De residual value: other investor Financial needs: 250 K x (1 + 0,25) 5 Investor

- 21. Скачать презентацию

Papaya Ltd: balance

Papaya Ltd: balance

Papaya Ltd: P&L.

Papaya Ltd: P&L.

1/Adjusted net assets (ANA)

Starting point: balance sheet

Assets – callable debts

(and

1/Adjusted net assets (ANA)

Starting point: balance sheet

Assets – callable debts

(and

2/ DCF method

Starting point: P&L

ANC: average net CF

CR = capitalised return

CR

2/ DCF method

Starting point: P&L

ANC: average net CF

CR = capitalised return

CR

3/ « objective » value

ANA + CR

2

The value of a

3/ « objective » value

ANA + CR

2

The value of a

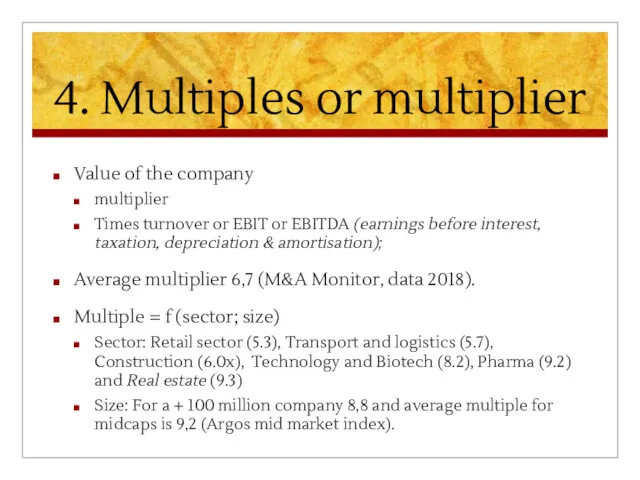

4. Multiples or multiplier

Value of the company

multiplier

Times turnover or EBIT or

4. Multiples or multiplier

Value of the company

multiplier

Times turnover or EBIT or

Multiples:

Mid market index

Multiples:

Mid market index

Anorganic growth

Assets very limited

Mainly human resources

Few « tangibles »

No CF, only cash drain

Value

Anorganic growth

Assets very limited

Mainly human resources

Few « tangibles »

No CF, only cash drain

Value

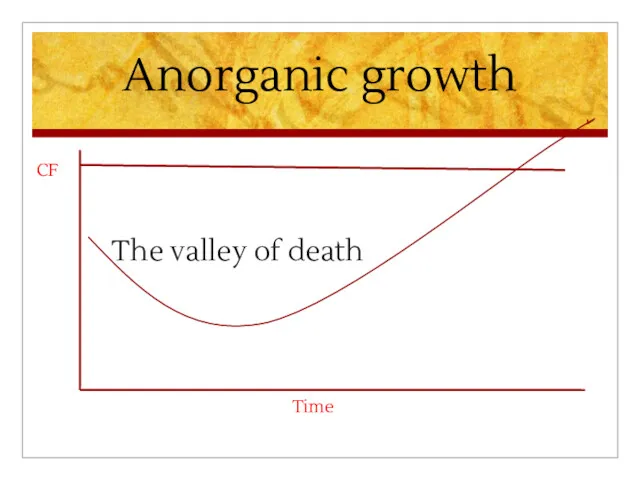

Anorganic growth

CF

The valley of death

Time

Anorganic growth

CF

The valley of death

Time

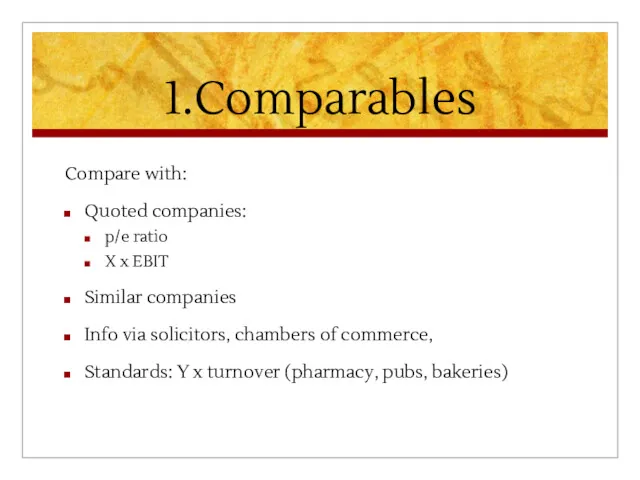

1.Comparables

Compare with:

Quoted companies:

p/e ratio

X x EBIT

Similar companies

Info via solicitors, chambers of

1.Comparables

Compare with:

Quoted companies:

p/e ratio

X x EBIT

Similar companies

Info via solicitors, chambers of

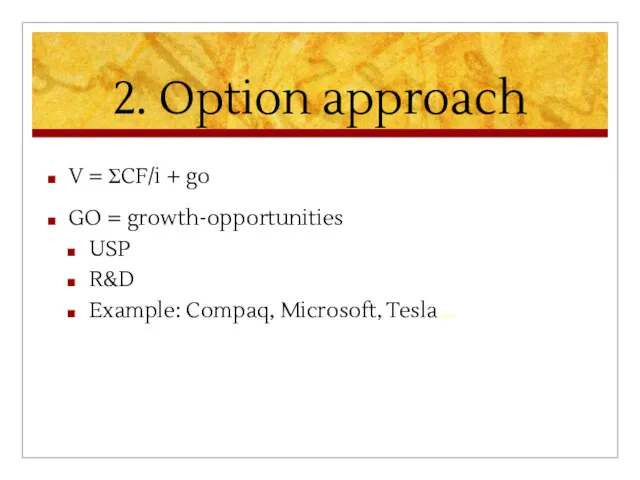

2. Option approach

V = ΣCF/i + go

GO = growth-opportunities

USP

R&D

Example: Compaq, Microsoft,

2. Option approach

V = ΣCF/i + go

GO = growth-opportunities

USP

R&D

Example: Compaq, Microsoft,

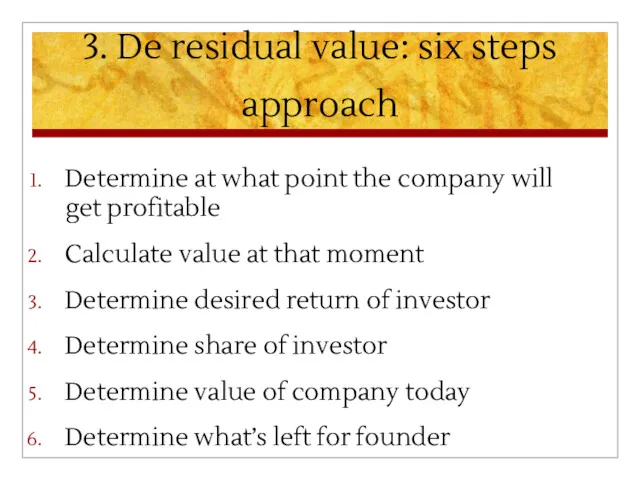

3. De residual value: six steps approach

Determine at what point the

3. De residual value: six steps approach

Determine at what point the

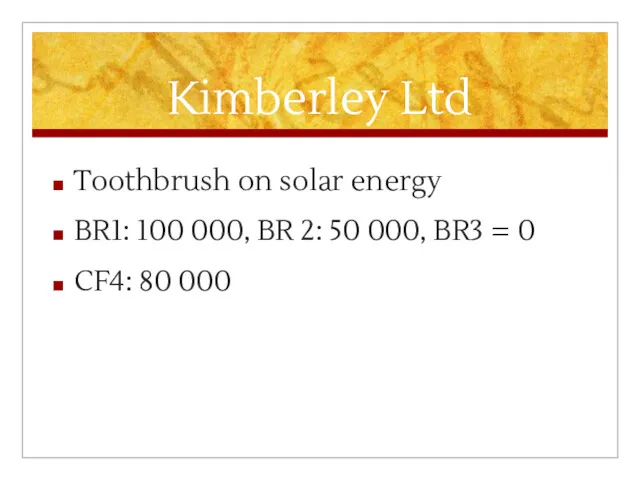

Kimberley Ltd

Toothbrush on solar energy

BR1: 100 000, BR 2: 50

Kimberley Ltd

Toothbrush on solar energy

BR1: 100 000, BR 2: 50

Kimberley Ltd

t4 = t0

VE 4: 80000/0,10 = 800 000

Fin needs: 150

Kimberley Ltd

t4 = t0

VE 4: 80000/0,10 = 800 000

Fin needs: 150

Kimberley Ltd

150 000 x (1,4)3 = 150 000 x 2,744 =

Kimberley Ltd

150 000 x (1,4)3 = 150 000 x 2,744 =

3. De residual value: without investor

Time: from yr 5: CF 250

3. De residual value: without investor

Time: from yr 5: CF 250

3. De residual value: with investor

Financial needs: 250 K x (1

3. De residual value: with investor

Financial needs: 250 K x (1

3. De residual value: other investor

Financial needs: 250 K x (1

3. De residual value: other investor

Financial needs: 250 K x (1

Страхование раритетных автомобилей

Страхование раритетных автомобилей Основные фонды предприятия

Основные фонды предприятия Доходы. Сбережения. Потребления

Доходы. Сбережения. Потребления Исполнение бюджета городского округа ЗАТО Фокино за 2022 год

Исполнение бюджета городского округа ЗАТО Фокино за 2022 год Порядок расчета платы за коммунальные услуги. Лекция 4 часть 2

Порядок расчета платы за коммунальные услуги. Лекция 4 часть 2 Этика предпринимательской деятельности

Этика предпринимательской деятельности Национальная платежная система (2)

Национальная платежная система (2) Готовимся к проведению годовой инвентаризации 2023 года (сентябрь 2023 года)

Готовимся к проведению годовой инвентаризации 2023 года (сентябрь 2023 года) Інформація щодо фінансового стану гуртожитків

Інформація щодо фінансового стану гуртожитків Заработная плата. Гарантийные и компенсационные выплаты

Заработная плата. Гарантийные и компенсационные выплаты Финансовое обеспечение мер по сокращению производственного травматизма и профессиональных заболеваний работников

Финансовое обеспечение мер по сокращению производственного травматизма и профессиональных заболеваний работников Налог на доходы физических лиц: оптимизация, применение налоговых вычетов

Налог на доходы физических лиц: оптимизация, применение налоговых вычетов Монетарная политика (1). Тема 5

Монетарная политика (1). Тема 5 Опыт многих - для успеха каждого. Простая математика

Опыт многих - для успеха каждого. Простая математика Пилотный проект Прямые выплаты

Пилотный проект Прямые выплаты Определение надежности, сравнительный анализ и прогнозирование страховых компаний

Определение надежности, сравнительный анализ и прогнозирование страховых компаний Банківський кредит. (Тема 5)

Банківський кредит. (Тема 5) Государственная пенсия по инвалидности

Государственная пенсия по инвалидности Анализ ликвидности и платежеспособности предприятия средств на примере ОАО Пермский завод Машиностроитель

Анализ ликвидности и платежеспособности предприятия средств на примере ОАО Пермский завод Машиностроитель Налогообложение в Российской Федерации

Налогообложение в Российской Федерации Страховое общество Ресо-гарантия Краснодар • 2020

Страховое общество Ресо-гарантия Краснодар • 2020 Оцінка нематеріальних активів

Оцінка нематеріальних активів Расчет аннуитетного платежа по формуле. Задача 6.11

Расчет аннуитетного платежа по формуле. Задача 6.11 Понятие, функции и структурная организация финансового рынка

Понятие, функции и структурная организация финансового рынка Валютная система и валютные отношения

Валютная система и валютные отношения МодульКасса. Регистрация, перерегистрация, снятие с учета

МодульКасса. Регистрация, перерегистрация, снятие с учета Таможенные органы РФ

Таможенные органы РФ Семинар для потенциальных предпринимателей Повышение уровня финансовой грамотности населения Ставропольского края

Семинар для потенциальных предпринимателей Повышение уровня финансовой грамотности населения Ставропольского края