- Interest rates. (Lecture 3)

Содержание

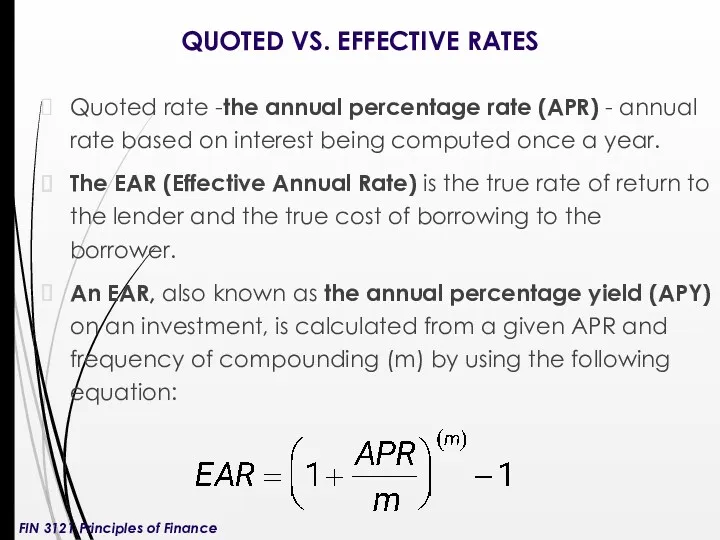

- 2. QUOTED VS. EFFECTIVE RATES Quoted rate -the annual percentage rate (APR) - annual rate based on

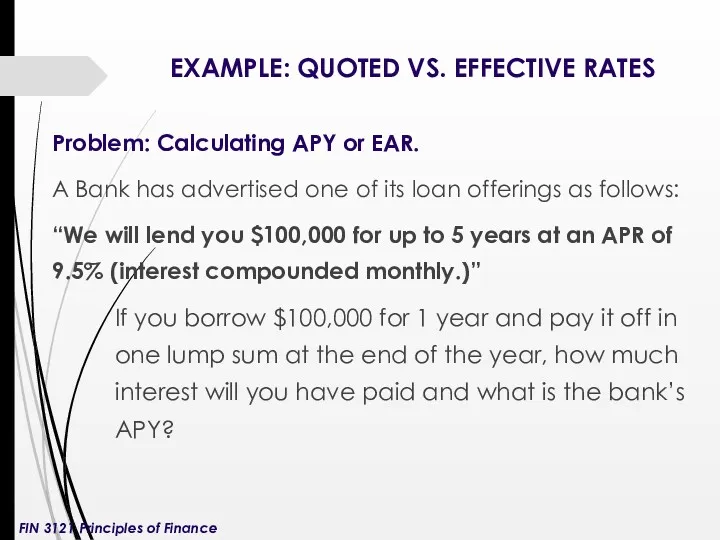

- 3. EXAMPLE: QUOTED VS. EFFECTIVE RATES Problem: Calculating APY or EAR. A Bank has advertised one of

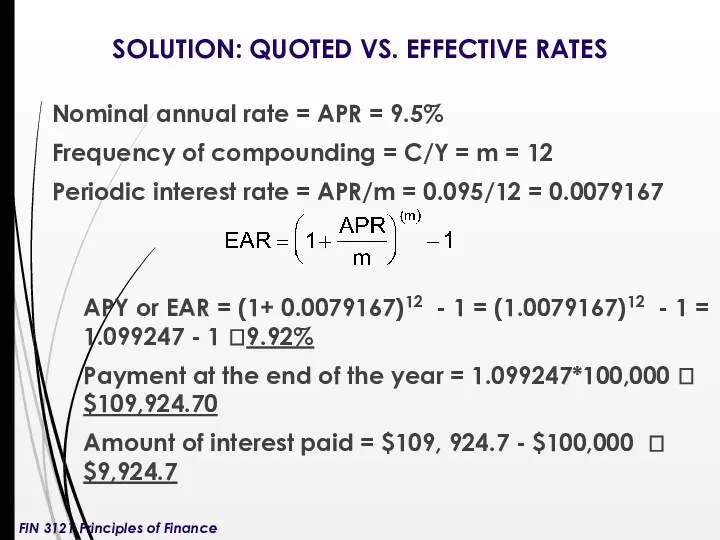

- 4. SOLUTION: QUOTED VS. EFFECTIVE RATES Nominal annual rate = APR = 9.5% Frequency of compounding =

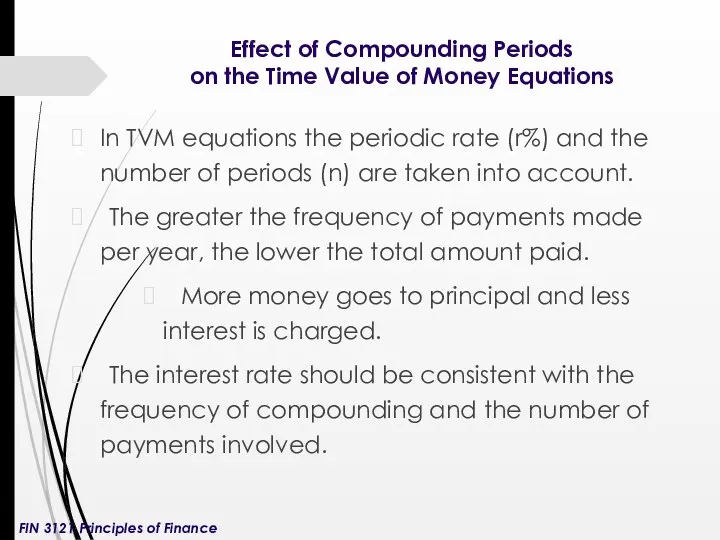

- 5. Effect of Compounding Periods on the Time Value of Money Equations In TVM equations the periodic

- 6. Example I: Effect of Compounding Periods on the Time Value of Money Equations Problem: Monthly versus

- 7. Solution: Effect of Compounding Periods on the Time Value of Money Equations If it is compounded

- 8. Solution: Effect of Compounding Periods on the Time Value of Money Equations Calculate monthly payment: n=5

- 9. Solution: Effect of Compounding Periods on the Time Value of Money Equations Total interest paid under

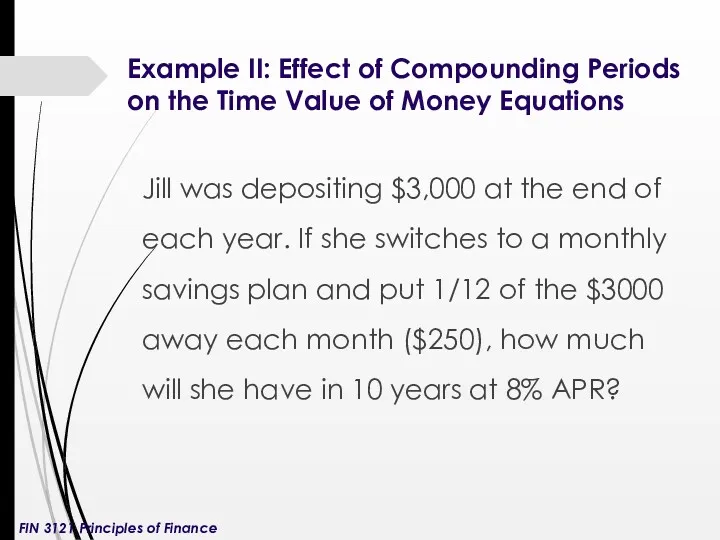

- 10. Example II: Effect of Compounding Periods on the Time Value of Money Equations Jill was depositing

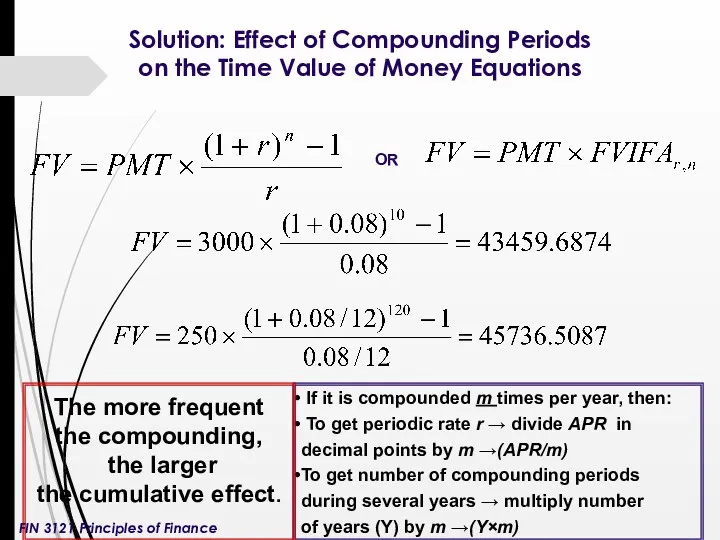

- 11. Solution: Effect of Compounding Periods on the Time Value of Money Equations If it is compounded

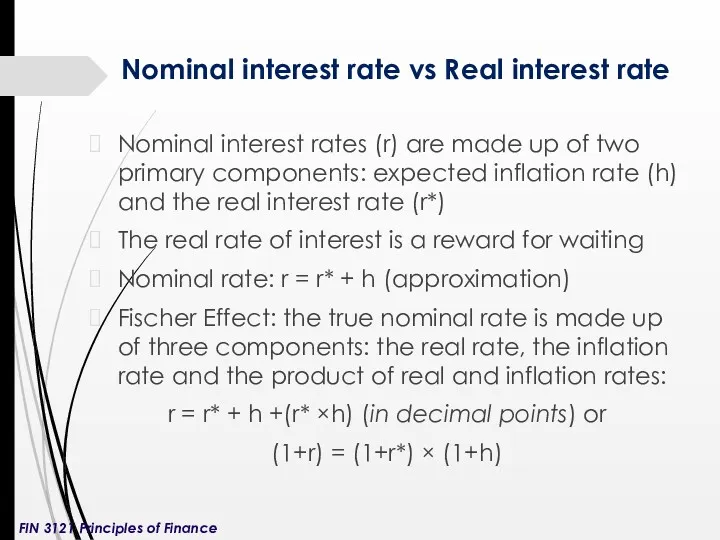

- 12. Nominal interest rate vs Real interest rate Nominal interest rates (r) are made up of two

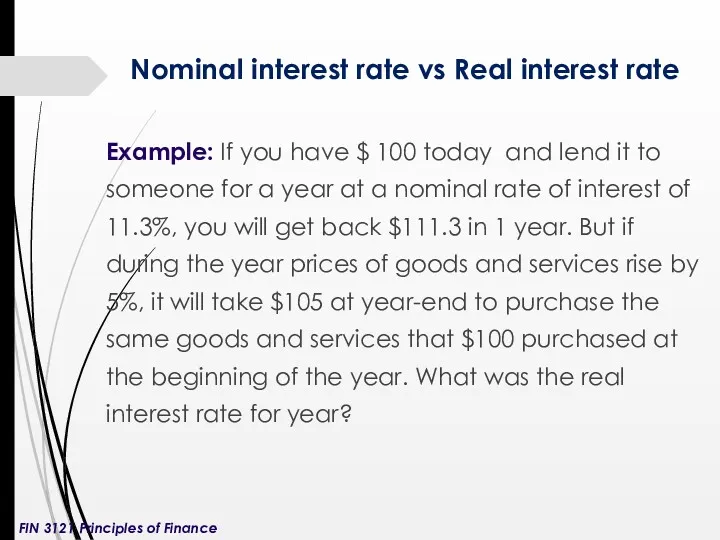

- 13. Example: If you have $ 100 today and lend it to someone for a year at

- 14. REAL INTEREST RATE The quick answer: 11.3% - 5% = 6.3%. To get more precise answer,

- 15. Default Risk Premium, Risk Free Rate & Maturity Risk Premium The rate of return on investments

- 17. Скачать презентацию

QUOTED VS. EFFECTIVE RATES

Quoted rate -the annual percentage rate (APR) -

QUOTED VS. EFFECTIVE RATES

Quoted rate -the annual percentage rate (APR) -

EXAMPLE: QUOTED VS. EFFECTIVE RATES

Problem: Calculating APY or EAR.

A Bank

EXAMPLE: QUOTED VS. EFFECTIVE RATES

Problem: Calculating APY or EAR.

A Bank

SOLUTION: QUOTED VS. EFFECTIVE RATES

Nominal annual rate = APR = 9.5%

Frequency

SOLUTION: QUOTED VS. EFFECTIVE RATES

Nominal annual rate = APR = 9.5%

Frequency

Effect of Compounding Periods

on the Time Value of Money Equations

In

Effect of Compounding Periods

on the Time Value of Money Equations

In

Example I: Effect of Compounding Periods

on the Time Value of

Example I: Effect of Compounding Periods on the Time Value of

Solution: Effect of Compounding Periods

on the Time Value of Money

Solution: Effect of Compounding Periods on the Time Value of Money

Solution: Effect of Compounding Periods

on the Time Value of Money

Solution: Effect of Compounding Periods on the Time Value of Money

Solution: Effect of Compounding Periods

on the Time Value of Money

Solution: Effect of Compounding Periods on the Time Value of Money

Example II: Effect of Compounding Periods

on the Time Value of

Example II: Effect of Compounding Periods on the Time Value of

Solution: Effect of Compounding Periods

on the Time Value of Money

Solution: Effect of Compounding Periods on the Time Value of Money

Nominal interest rate vs Real interest rate

Nominal interest rates (r) are

Nominal interest rate vs Real interest rate

Nominal interest rates (r) are

Example: If you have $ 100 today and lend it to

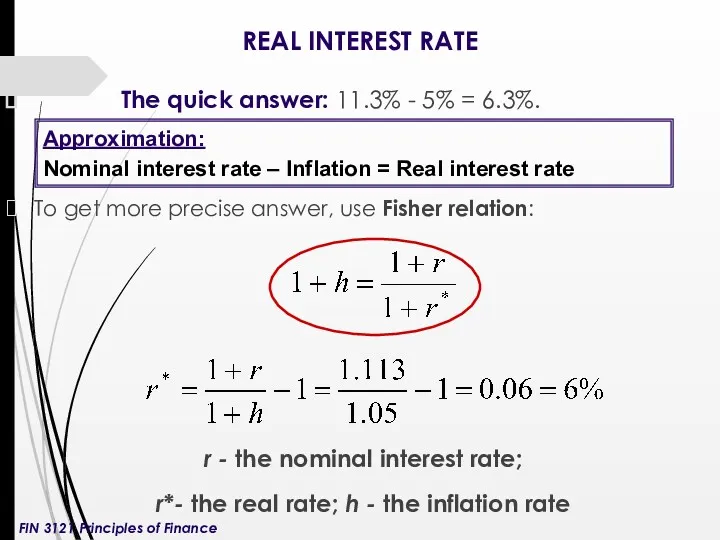

REAL INTEREST RATE

The quick answer: 11.3% - 5% = 6.3%.

REAL INTEREST RATE

The quick answer: 11.3% - 5% = 6.3%.

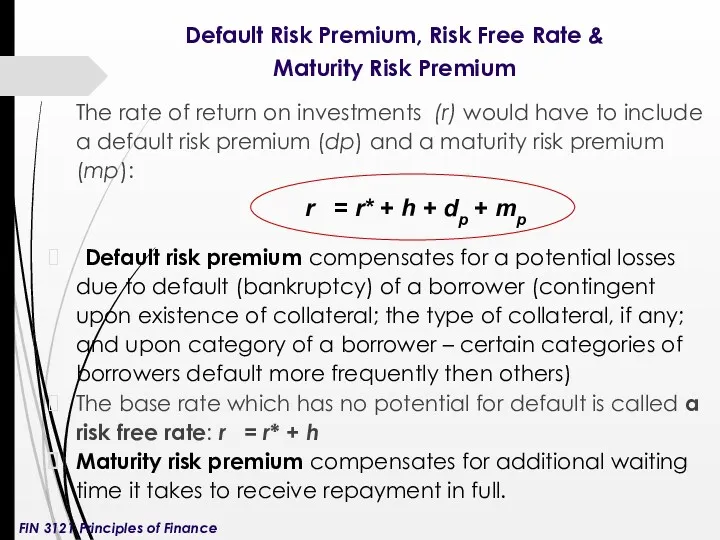

Default Risk Premium, Risk Free Rate &

Maturity Risk Premium

The rate

Default Risk Premium, Risk Free Rate &

Maturity Risk Premium

The rate

Страховые брокеры в России

Страховые брокеры в России МСФО (IFRS) 16 Аренда

МСФО (IFRS) 16 Аренда Доллар США

Доллар США Порядок заполнения справок о доходах, расходах, об имуществе с использованием специального программного обеспечения Справка БК+

Порядок заполнения справок о доходах, расходах, об имуществе с использованием специального программного обеспечения Справка БК+ Инициативное (партисипаторное) бюджетирование

Инициативное (партисипаторное) бюджетирование Лизинг медицинского оборудования

Лизинг медицинского оборудования Продукты и услуги ПАО АК БАРС Банк

Продукты и услуги ПАО АК БАРС Банк Публічний звіт голови державного космічного агентства України

Публічний звіт голови державного космічного агентства України Теория и методология ценообразования

Теория и методология ценообразования Оптимизация налогов для субъектов МСП

Оптимизация налогов для субъектов МСП Инвестиционный анализ и инвестиционное проектирование на предприятии

Инвестиционный анализ и инвестиционное проектирование на предприятии Денежные доходы и поступления предприятия

Денежные доходы и поступления предприятия Оценка общественной эффективности инвестиционного проекта

Оценка общественной эффективности инвестиционного проекта Expedite. Month of December

Expedite. Month of December Аудит расчетов с персоналом и подотчетными лицами

Аудит расчетов с персоналом и подотчетными лицами The Burden of Debt

The Burden of Debt Изменения в бухгалтерском учете учреждений бюджетной сферы

Изменения в бухгалтерском учете учреждений бюджетной сферы 1С:Зарплата и кадры государственного учреждения 8 - от концепции до реализации

1С:Зарплата и кадры государственного учреждения 8 - от концепции до реализации Financial stability and macroprudential oversight in Germany

Financial stability and macroprudential oversight in Germany Бухгалтерский и налоговый учёт (иностранные сотрудники)

Бухгалтерский и налоговый учёт (иностранные сотрудники) Организация и функционирование рынка ценных бумаг. Тема 4.2

Организация и функционирование рынка ценных бумаг. Тема 4.2 Зоны риска кредитных вложений

Зоны риска кредитных вложений Налоговая система в РФ. Виды налогов. Функции налогов. Налоги, уплачиваемые предприятиями

Налоговая система в РФ. Виды налогов. Функции налогов. Налоги, уплачиваемые предприятиями Корпоративні фінанси. Робочий капітал корпоративних підприємств. (Тема 8)

Корпоративні фінанси. Робочий капітал корпоративних підприємств. (Тема 8) Деньги и их функции. Урок обществознания в 7 классе

Деньги и их функции. Урок обществознания в 7 классе Оценка готовой продукции: аспект бухгалтерской отчётности

Оценка готовой продукции: аспект бухгалтерской отчётности Глобализация

Глобализация Принципы банковского кредитования и их развитие в современных условиях. Курсовая работа

Принципы банковского кредитования и их развитие в современных условиях. Курсовая работа