- Inventory Costing and Capacity Analysis

Содержание

- 2. Inventory Costing Choices: Summary Absorption Costing – product costs are capitalized; period costs are expensed Variable

- 3. Comparative Income Statements

- 4. Costing Comparison Variable costing is a method of inventory costing in which only variable manufacturing costs

- 5. Differences in Income Operating Income will differ between Absorption and Variable Costing The amount of the

- 6. Comparative Income Effects

- 7. Comparative Income Effects

- 8. Comparative Income Effects

- 9. Comparison of Alternative Inventory Costing Systems Variable Direct Manufacturing Cost

- 10. Comparison of Alternative Inventory Costing Systems Variable Indirect Manufacturing Cost

- 11. Comparison of Alternative Inventory Costing Systems Fixed Direct Manufacturing Cost

- 12. Comparison of Alternative Inventory Costing Systems Fixed Indirect Manufacturing Cost

- 13. Performance Issues and Absorption Costing Managers may seek to manipulate income by producing too many units

- 14. Inventories and Costing Methods One way to prevent the unnecessary buildup of inventory for bonus purposes

- 15. Other Manipulation Schemes beyond Simple Overproduction Deciding to manufacture products to absorb the highest amount of

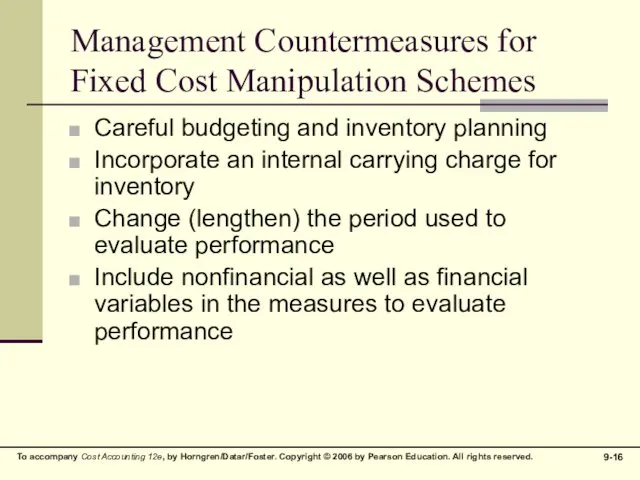

- 16. Management Countermeasures for Fixed Cost Manipulation Schemes Careful budgeting and inventory planning Incorporate an internal carrying

- 18. Скачать презентацию

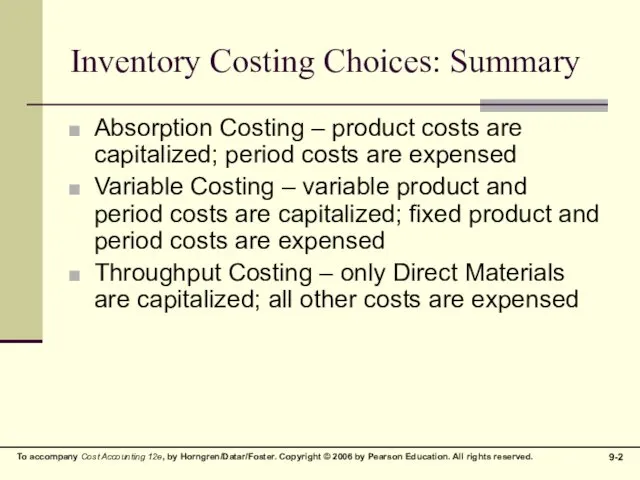

Inventory Costing Choices: Summary

Absorption Costing – product costs are capitalized; period

Inventory Costing Choices: Summary

Absorption Costing – product costs are capitalized; period

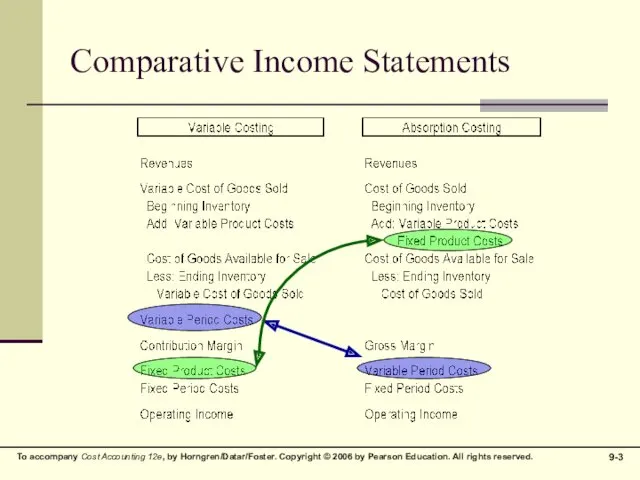

Comparative Income Statements

Comparative Income Statements

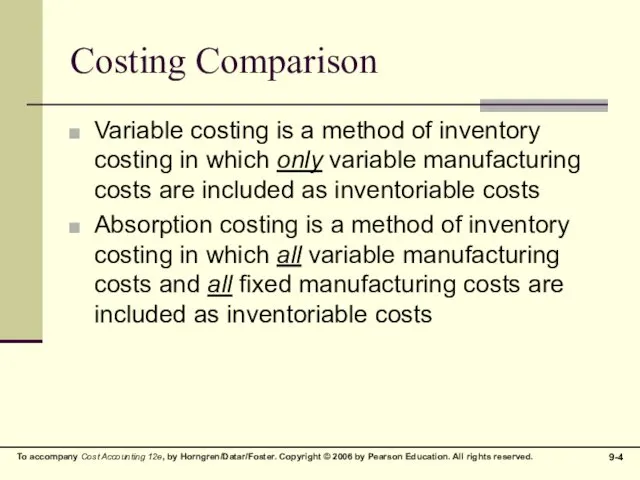

Costing Comparison

Variable costing is a method of inventory costing in which

Costing Comparison

Variable costing is a method of inventory costing in which

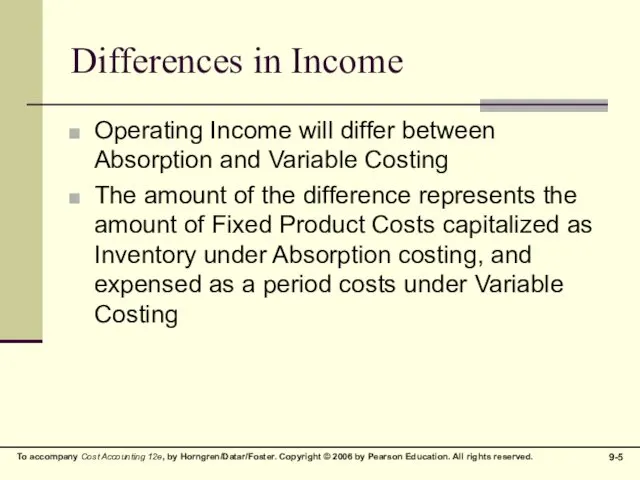

Differences in Income

Operating Income will differ between Absorption and Variable Costing

The

Differences in Income

Operating Income will differ between Absorption and Variable Costing

The

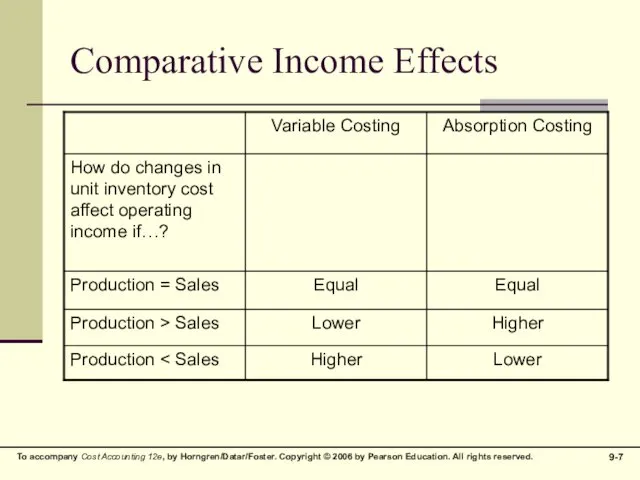

Comparative Income Effects

Comparative Income Effects

Comparative Income Effects

Comparative Income Effects

Comparative Income Effects

Comparative Income Effects

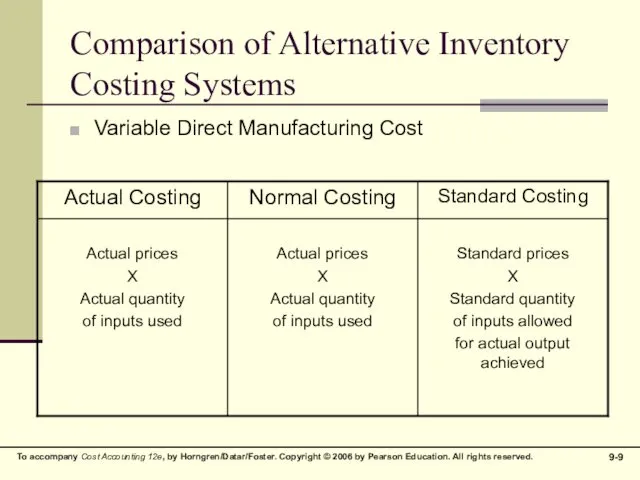

Comparison of Alternative Inventory Costing Systems

Variable Direct Manufacturing Cost

Comparison of Alternative Inventory Costing Systems

Variable Direct Manufacturing Cost

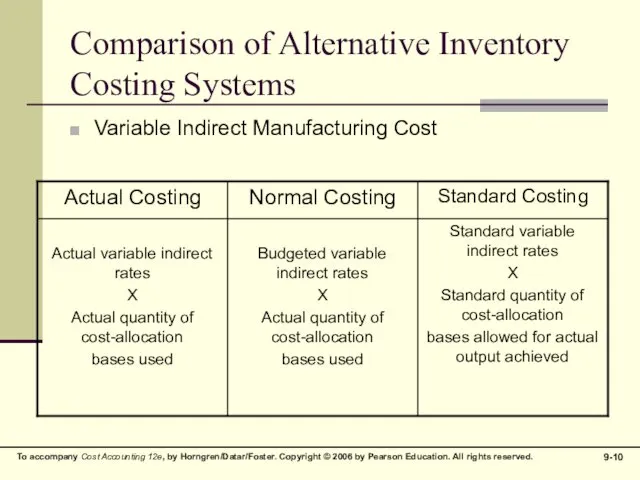

Comparison of Alternative Inventory Costing Systems

Variable Indirect Manufacturing Cost

Comparison of Alternative Inventory Costing Systems

Variable Indirect Manufacturing Cost

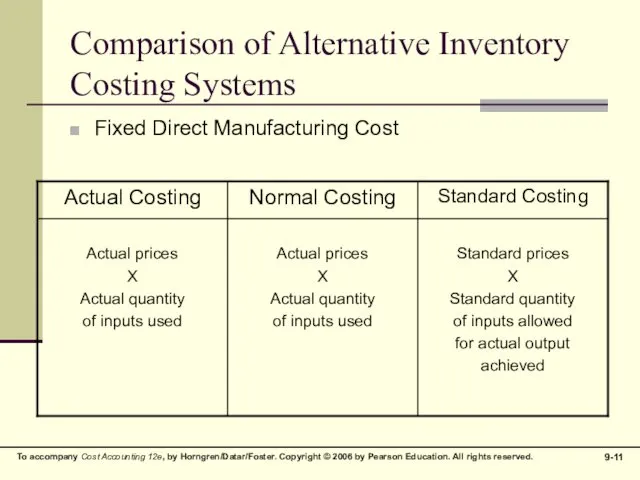

Comparison of Alternative Inventory Costing Systems

Fixed Direct Manufacturing Cost

Comparison of Alternative Inventory Costing Systems

Fixed Direct Manufacturing Cost

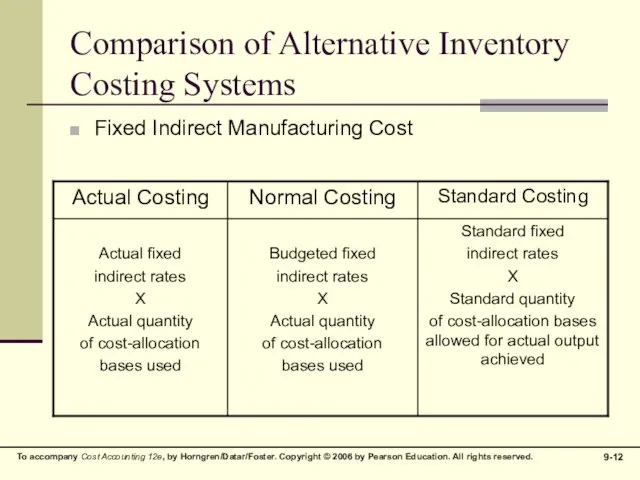

Comparison of Alternative Inventory Costing Systems

Fixed Indirect Manufacturing Cost

Comparison of Alternative Inventory Costing Systems

Fixed Indirect Manufacturing Cost

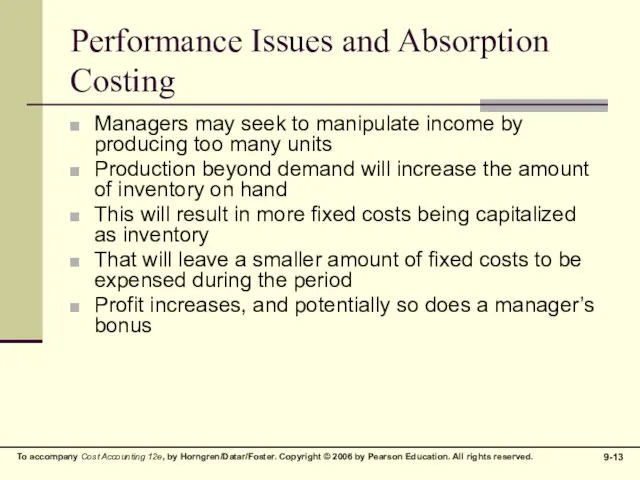

Performance Issues and Absorption Costing

Managers may seek to manipulate income by

Performance Issues and Absorption Costing

Managers may seek to manipulate income by

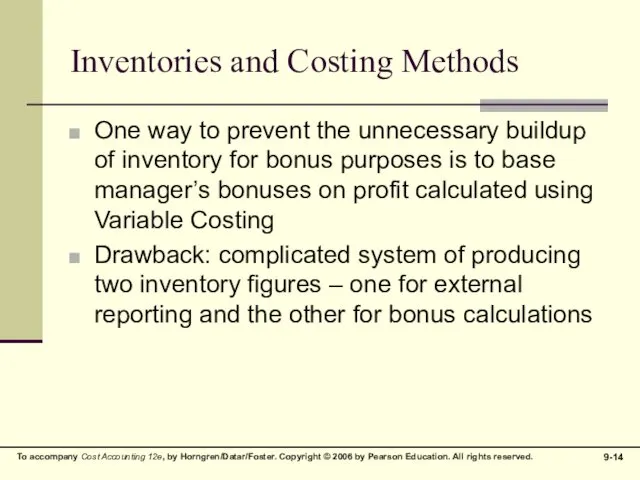

Inventories and Costing Methods

One way to prevent the unnecessary buildup of

Inventories and Costing Methods

One way to prevent the unnecessary buildup of

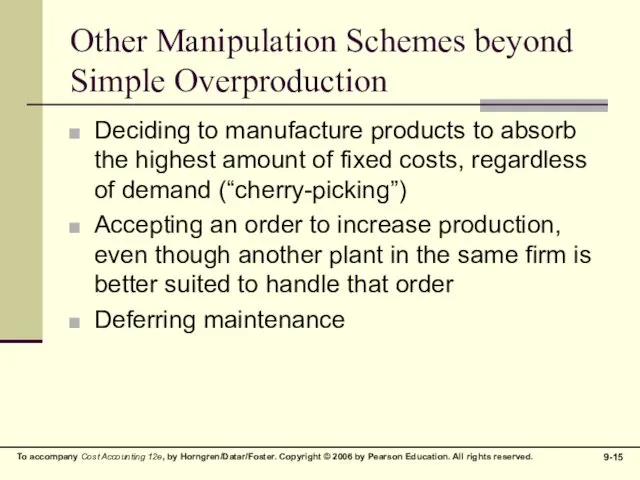

Other Manipulation Schemes beyond Simple Overproduction

Deciding to manufacture products to absorb

Other Manipulation Schemes beyond Simple Overproduction

Deciding to manufacture products to absorb

Management Countermeasures for Fixed Cost Manipulation Schemes

Careful budgeting and inventory planning

Incorporate

Management Countermeasures for Fixed Cost Manipulation Schemes

Careful budgeting and inventory planning

Incorporate

Международные тарифы, скидки, льготы

Международные тарифы, скидки, льготы Управление государственными и муниципальными закупками в системе образования

Управление государственными и муниципальными закупками в системе образования Межправительственная рабочая группа экспертов по международным стандартам учета и отчетности ( МСУО). Налоговые органы

Межправительственная рабочая группа экспертов по международным стандартам учета и отчетности ( МСУО). Налоговые органы Ценовая политика, как объект финансового менеджмента

Ценовая политика, как объект финансового менеджмента Бумажные деньги. Фиатные деньги. Электронные деньги

Бумажные деньги. Фиатные деньги. Электронные деньги Разъяснения по контролям в протоколах приема при размещении планов закупок и планов-графиков в ЕИС

Разъяснения по контролям в протоколах приема при размещении планов закупок и планов-графиков в ЕИС Урок финансовой грамотности. Слитки

Урок финансовой грамотности. Слитки Налог на доходы физических лиц

Налог на доходы физических лиц Расчет пенсии

Расчет пенсии Шесть предложений по финансированию

Шесть предложений по финансированию Распределительно-уравнительная система формирования пенсии

Распределительно-уравнительная система формирования пенсии Страховое общество Ресо-гарантия Краснодар • 2020

Страховое общество Ресо-гарантия Краснодар • 2020 Банк жүйесі

Банк жүйесі Основы правового регулирования иностранных инвестиций

Основы правового регулирования иностранных инвестиций Построение систем управления на базе ERP-технологий. Управление бизнес-процессами: бюджетирование, контроллинг. (Лекция 8)

Построение систем управления на базе ERP-технологий. Управление бизнес-процессами: бюджетирование, контроллинг. (Лекция 8) Оценка эффективности инвестиционного проекта по созданию LBS приложения

Оценка эффективности инвестиционного проекта по созданию LBS приложения Лекция № 2

Лекция № 2 Правила призначення стипендій у Кременецькому медичному училищі

Правила призначення стипендій у Кременецькому медичному училищі Сутність інвестиційного менеджменту. (Тема 1)

Сутність інвестиційного менеджменту. (Тема 1) Налог на имущество физических лиц

Налог на имущество физических лиц Оценка финансового состояния организации. Тема 8

Оценка финансового состояния организации. Тема 8 Создание сведений об операциях с целевыми средствами в ГИИС ЭБ ПУР (КС)

Создание сведений об операциях с целевыми средствами в ГИИС ЭБ ПУР (КС) Расчет критической точки безубыточности и запаса финансовой прочности

Расчет критической точки безубыточности и запаса финансовой прочности Бухгалтерский учет образовательных услуг

Бухгалтерский учет образовательных услуг Soliq ma’murchiligi

Soliq ma’murchiligi Управление коммерческими банками

Управление коммерческими банками Консультант в сфере финансового планирования жизни

Консультант в сфере финансового планирования жизни Обязательное пенсионное страхование ОАО НПФ РГС

Обязательное пенсионное страхование ОАО НПФ РГС