- Procedures for student. Directional testing

Содержание

- 2. Contents Directional testing. IFAC: Bank and Cash. Non-current assets. Inventory Receivables & Payables Provisions Share capital,

- 3. Directional testing Concept of directional testing derives from principle of double entry bookkeeping for every debit

- 4. Corresponding assertions Overstatement The direction of testing is from the financial statements (where overstated item is

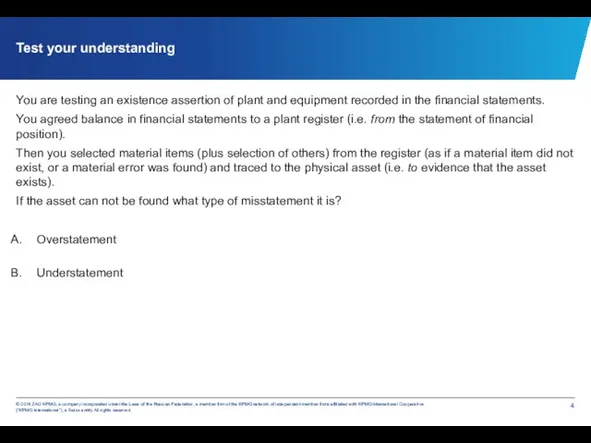

- 5. Test your understanding You are testing an existence assertion of plant and equipment recorded in the

- 6. Factors to consider before choosing procedures Audit risk Nature of internal controls and reliance on their

- 7. Bank & cash Reliable pieces of evidence: the bank confirmation letter; the bank reconciliation. Audit procedures

- 8. Bank & cash Audit procedures (continued) Examine any old unpresented cheques to assess if they need

- 9. Illustration. Bank reconciliation

- 10. Bank confirmation letter The bank confirmation letter provides direct confirmation of bank balances from the bank,

- 11. Bank confirmation letter (continued) Additional procedures in relation to loan payables include: Review disclosures of interest

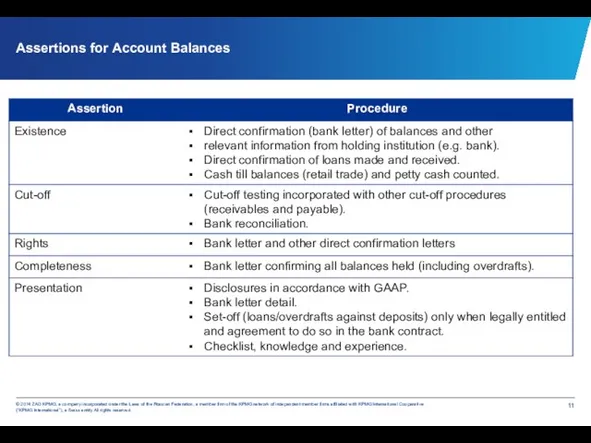

- 12. Assertions for Account Balances

- 13. Test your understanding Which assertions are tested for bank and cash in respect of classes of

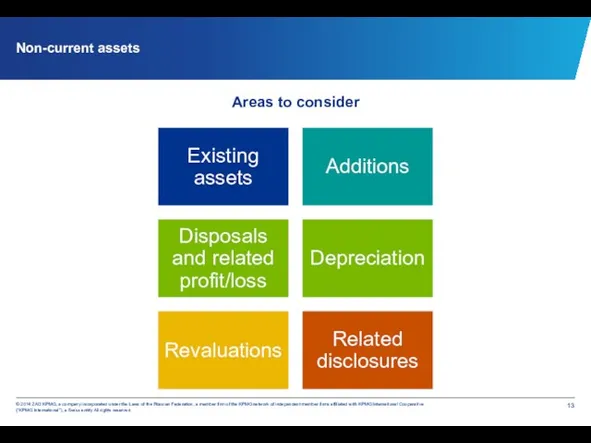

- 14. Non-current assets Areas to consider

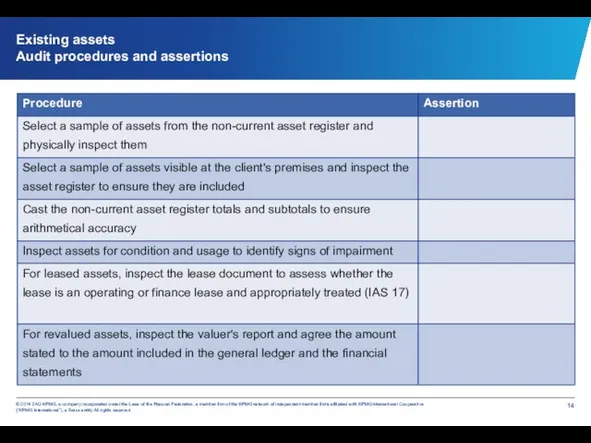

- 15. Existing assets Audit procedures and assertions

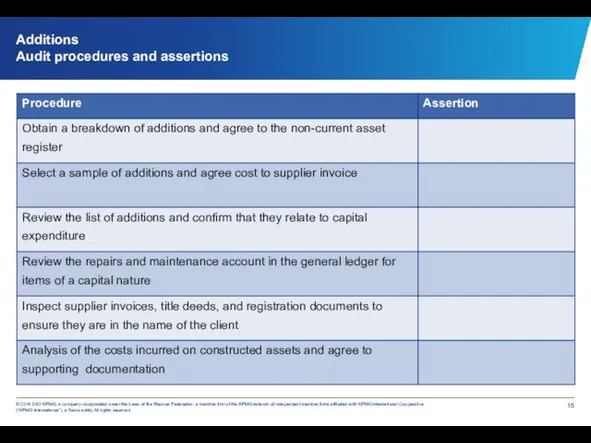

- 16. Additions Audit procedures and assertions

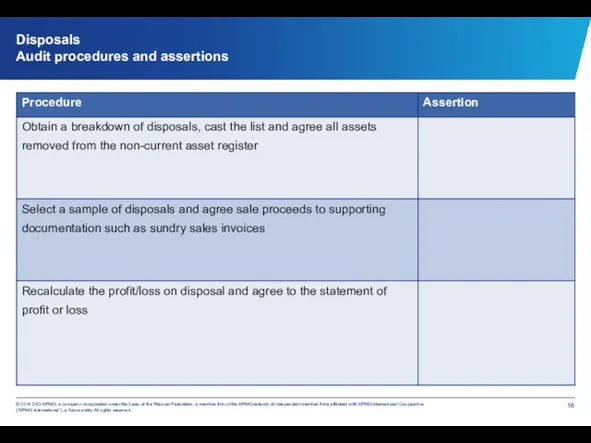

- 17. Disposals Audit procedures and assertions

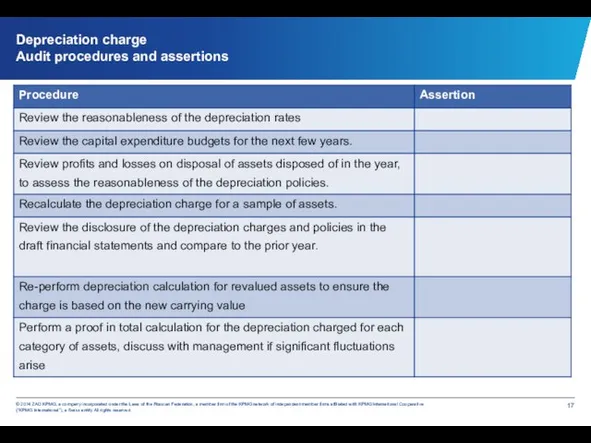

- 18. Depreciation charge Audit procedures and assertions

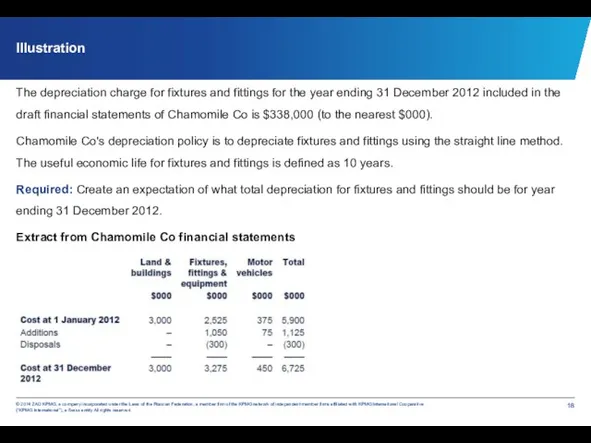

- 19. Illustration The depreciation charge for fixtures and fittings for the year ending 31 December 2012 included

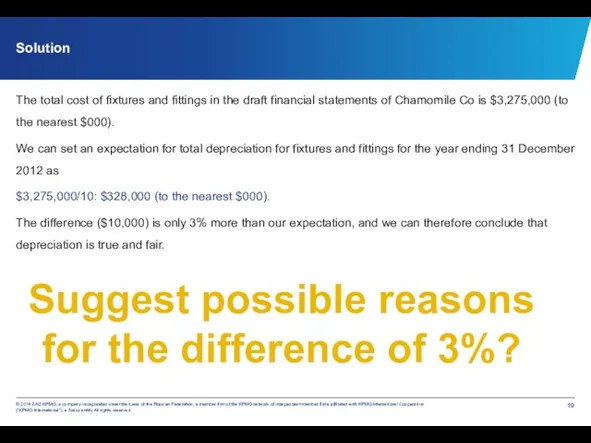

- 20. Solution The total cost of fixtures and fittings in the draft financial statements of Chamomile Co

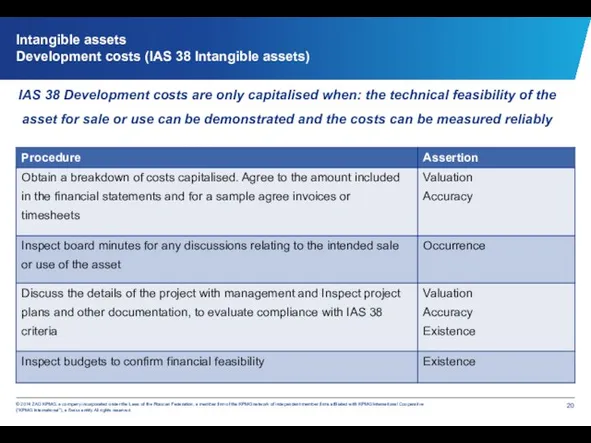

- 21. Intangible assets Development costs (IAS 38 Intangible assets) IAS 38 Development costs are only capitalised when:

- 22. Other intangible assets Note: audit procedures for ammortisation are similar to those for depreciation.

- 23. Inventory The inventory count - is the main source of evidence. According to ISA 501 “Audit

- 24. Audit procedures for inventory count

- 25. Before inventory count Contact client to obtain a copy of the inventory count instructions, to understand

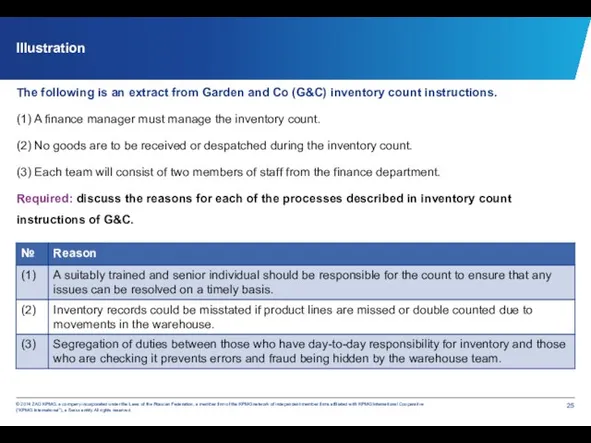

- 26. Illustration The following is an extract from Garden and Co (G&C) inventory count instructions. (1) A

- 27. During inventory count

- 28. After inventory count Final audit procedures

- 29. After inventory count Final audit procedures (continued)

- 30. After inventory count Final audit procedures (continued)

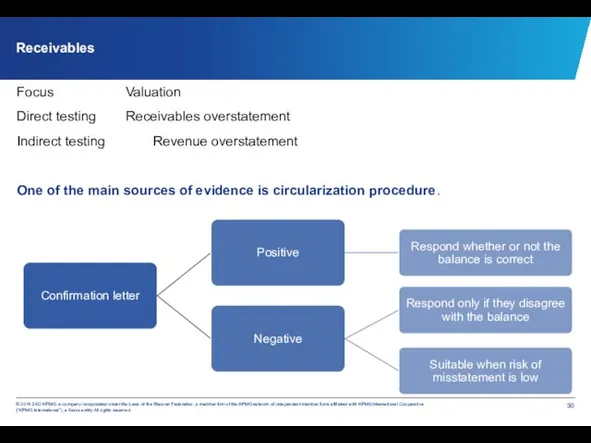

- 31. Receivables Focus Valuation Direct testing Receivables overstatement Indirect testing Revenue overstatement One of the main sources

- 32. Confirmation letters ISA 505 “External confirmations” requires the auditor to maintain control over external confirmation requests

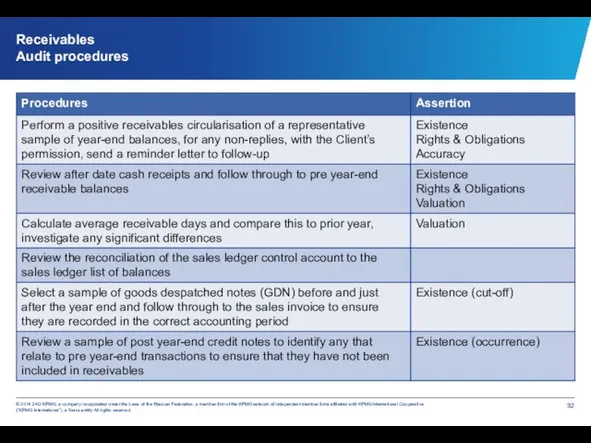

- 33. Receivables Audit procedures

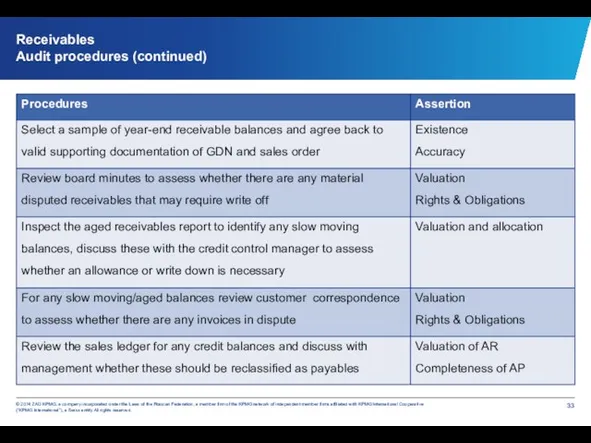

- 34. Receivables Audit procedures (continued)

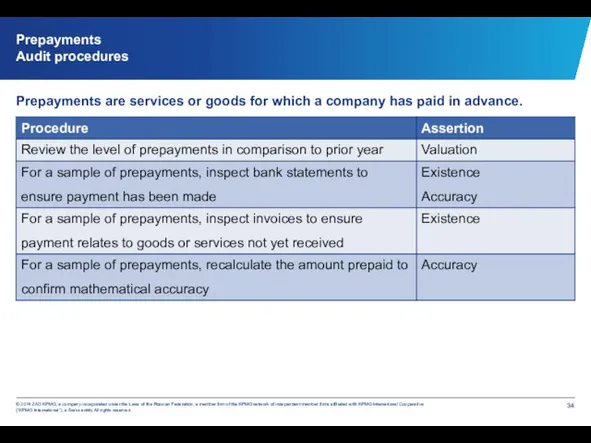

- 35. Prepayments Audit procedures Prepayments are services or goods for which a company has paid in advance.

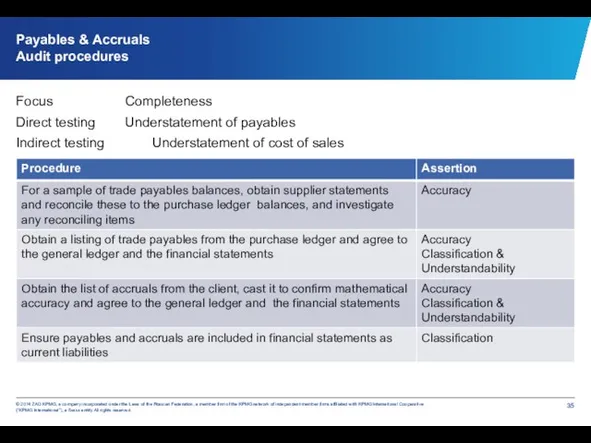

- 36. Payables & Accruals Audit procedures Focus Completeness Direct testing Understatement of payables Indirect testing Understatement of

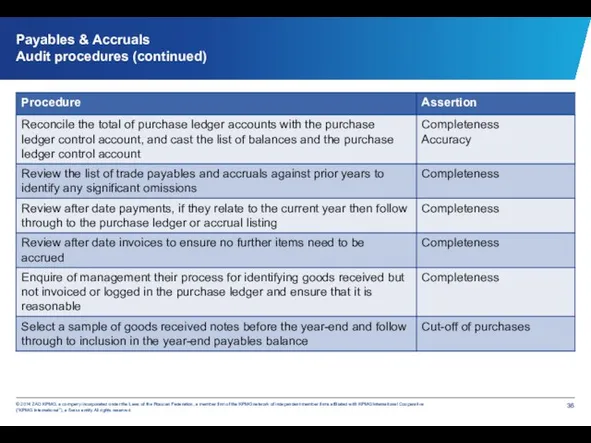

- 37. Payables & Accruals Audit procedures (continued)

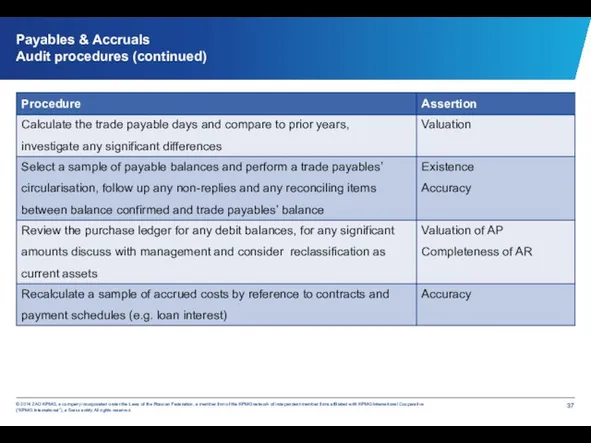

- 38. Payables & Accruals Audit procedures (continued)

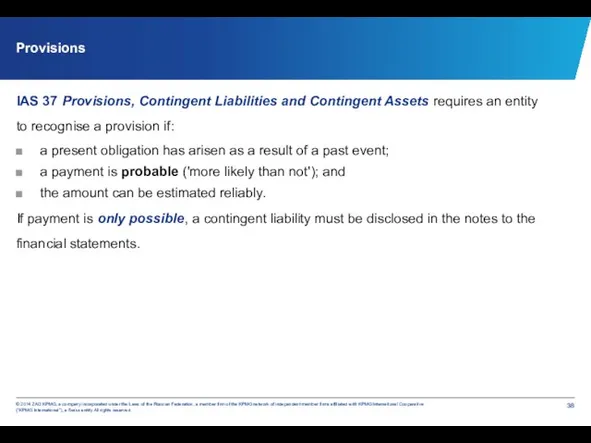

- 39. Provisions IAS 37 Provisions, Contingent Liabilities and Contingent Assets requires an entity to recognise a provision

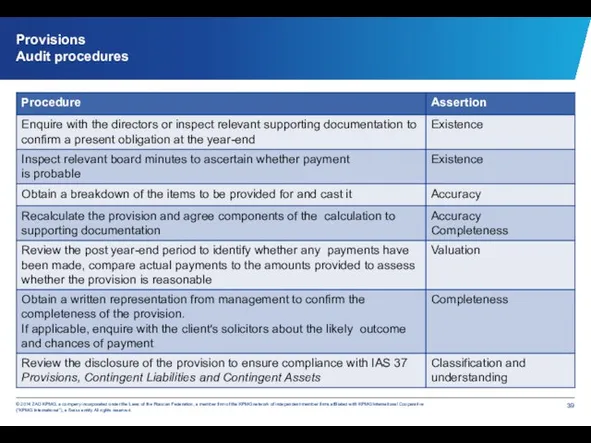

- 40. Provisions Audit procedures

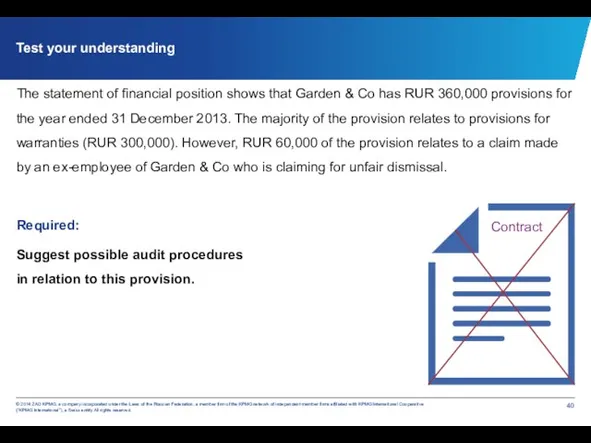

- 41. Test your understanding The statement of financial position shows that Garden & Co has RUR 360,000

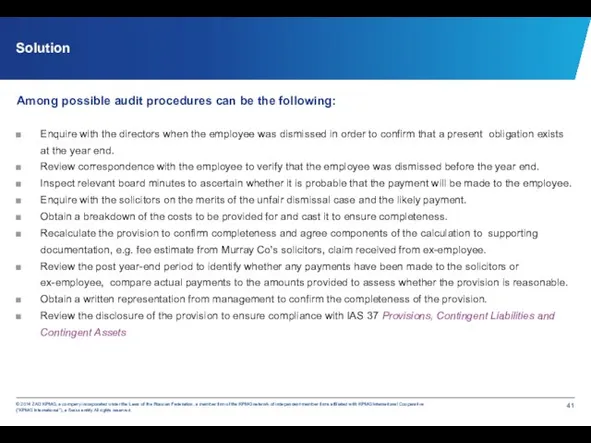

- 42. Solution Among possible audit procedures can be the following: Enquire with the directors when the employee

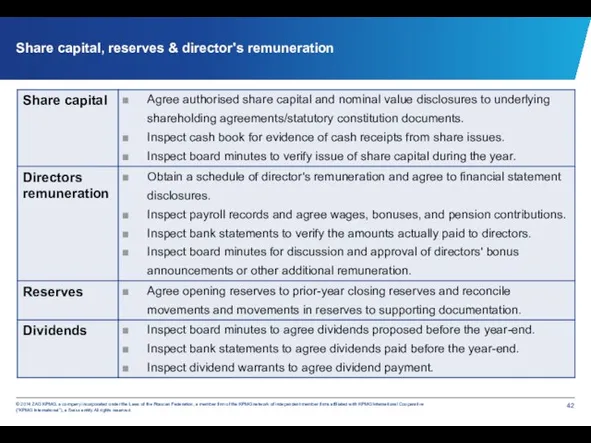

- 43. Share capital, reserves & director's remuneration

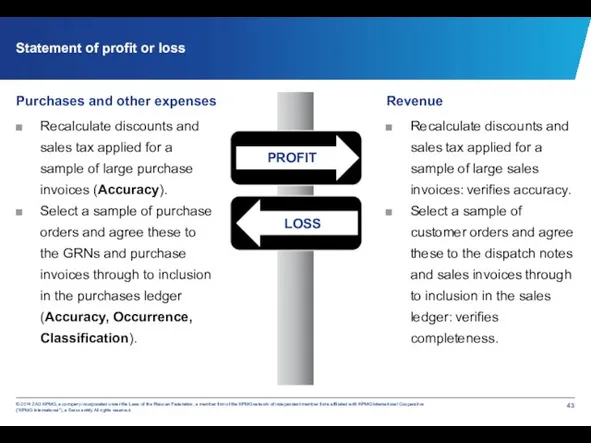

- 44. Statement of profit or loss Purchases and other expenses Recalculate discounts and sales tax applied for

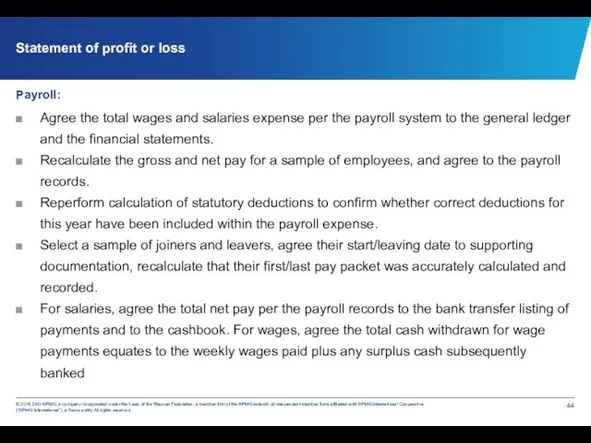

- 45. Statement of profit or loss Payroll: Agree the total wages and salaries expense per the payroll

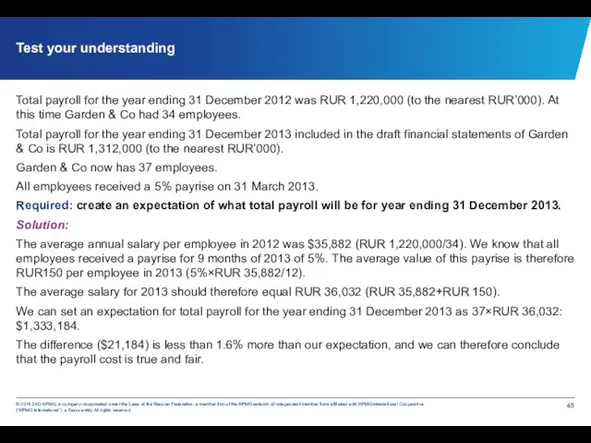

- 46. Test your understanding Total payroll for the year ending 31 December 2012 was RUR 1,220,000 (to

- 47. Accounting estimates ISA 540 “Auditing Accounting Estimates” requires the auditor to: Obtain an understanding of how

- 48. Accounting estimates – Smaller entities Smaller entities may well be engaged in activity that is relatively

- 49. Accounting estimates – Smaller entities Problems Management override a key director or manager have significant power

- 50. Related party is a person or entity that has control or significant influence, directly or indirectly

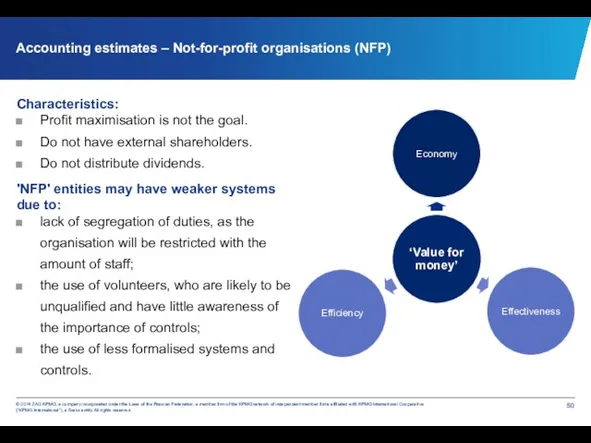

- 51. Accounting estimates – Not-for-profit organisations (NFP) Characteristics: Profit maximisation is not the goal. Do not have

- 52. Accounting estimates – Not-for-profit organisations (NFP) Audit implications Testing tends to concentrate on substantive procedures where

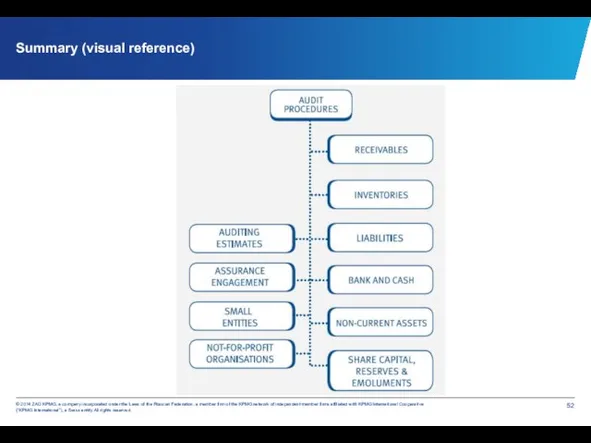

- 53. Summary (visual reference)

- 55. Скачать презентацию

Contents

Directional testing.

IFAC:

Bank and Cash.

Non-current assets.

Inventory

Receivables & Payables

Provisions

Share capital, reserves & director's

Contents

Directional testing.

IFAC:

Bank and Cash.

Non-current assets.

Inventory

Receivables & Payables

Provisions

Share capital, reserves & director's

Directional testing

Concept of directional testing derives from principle of double entry

Directional testing

Concept of directional testing derives from principle of double entry

Corresponding assertions

Overstatement

The direction of testing is from the financial statements (where

Corresponding assertions

Overstatement

The direction of testing is from the financial statements (where

Test your understanding

You are testing an existence assertion of plant and

Test your understanding

You are testing an existence assertion of plant and

Factors to consider before choosing procedures

Audit risk

Nature of internal controls and

Factors to consider before choosing procedures

Audit risk

Nature of internal controls and

Bank & cash

Reliable pieces of evidence:

the bank confirmation letter;

the bank

Bank & cash

Reliable pieces of evidence:

the bank confirmation letter;

the bank

Bank & cash

Audit procedures (continued)

Examine any old unpresented cheques to assess

Bank & cash

Audit procedures (continued)

Examine any old unpresented cheques to assess

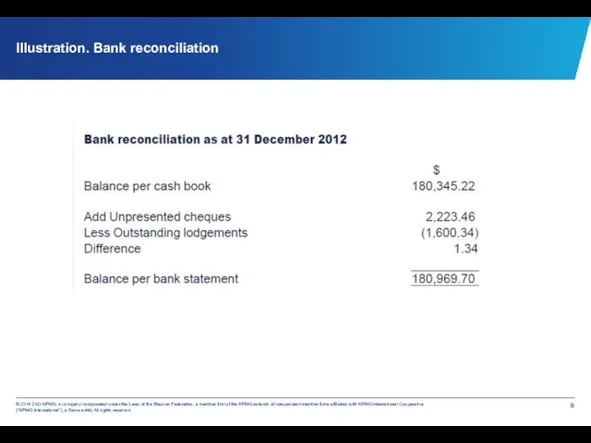

Illustration. Bank reconciliation

Illustration. Bank reconciliation

Bank confirmation letter

The bank confirmation letter provides direct confirmation of bank

Bank confirmation letter

The bank confirmation letter provides direct confirmation of bank

Bank confirmation letter (continued)

Additional procedures in relation to loan payables include:

Review

Bank confirmation letter (continued)

Additional procedures in relation to loan payables include:

Review

Assertions for Account Balances

Assertions for Account Balances

Test your understanding

Which assertions are tested for bank and cash in

Test your understanding

Which assertions are tested for bank and cash in

Non-current assets

Areas to consider

Non-current assets

Areas to consider

Existing assets

Audit procedures and assertions

Existing assets

Audit procedures and assertions

Additions

Audit procedures and assertions

Additions

Audit procedures and assertions

Disposals

Audit procedures and assertions

Disposals

Audit procedures and assertions

Depreciation charge

Audit procedures and assertions

Depreciation charge

Audit procedures and assertions

Illustration

The depreciation charge for fixtures and fittings for the year ending

Illustration

The depreciation charge for fixtures and fittings for the year ending

Solution

The total cost of fixtures and fittings in the draft financial

Solution

The total cost of fixtures and fittings in the draft financial

Intangible assets

Development costs (IAS 38 Intangible assets)

IAS 38 Development costs are

Intangible assets

Development costs (IAS 38 Intangible assets)

IAS 38 Development costs are

Other intangible assets

Note: audit procedures for ammortisation are similar to those

Other intangible assets

Note: audit procedures for ammortisation are similar to those

Inventory

The inventory count - is the main source of evidence.

According to

Inventory

The inventory count - is the main source of evidence.

According to

Audit procedures for inventory count

Audit procedures for inventory count

Before inventory count

Contact client to obtain a copy of the inventory

Before inventory count

Contact client to obtain a copy of the inventory

Illustration

The following is an extract from Garden and Co (G&C) inventory

Illustration

The following is an extract from Garden and Co (G&C) inventory

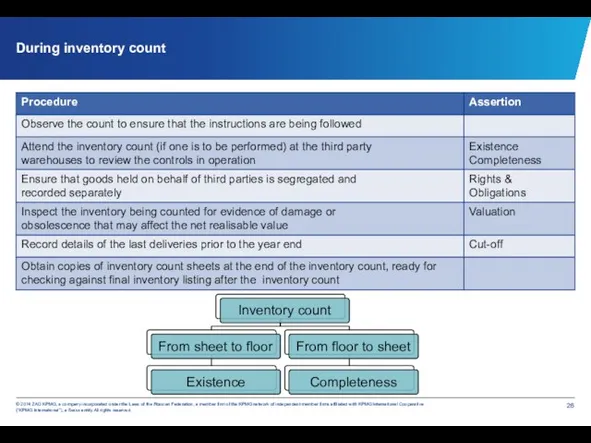

During inventory count

During inventory count

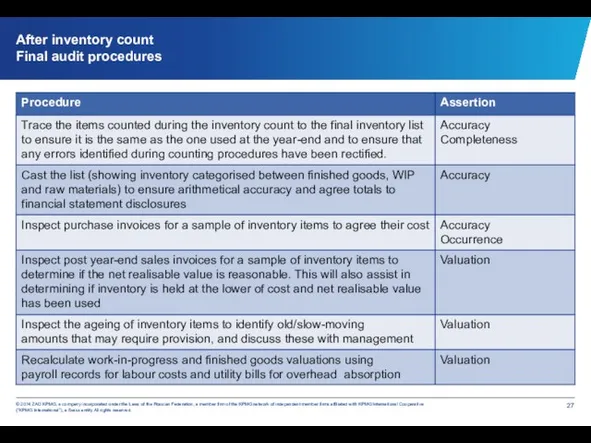

After inventory count

Final audit procedures

After inventory count

Final audit procedures

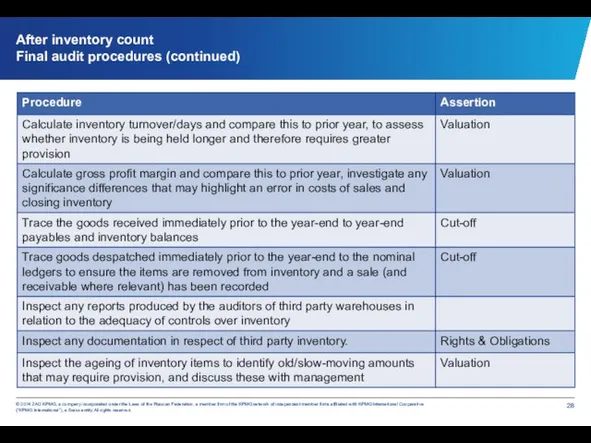

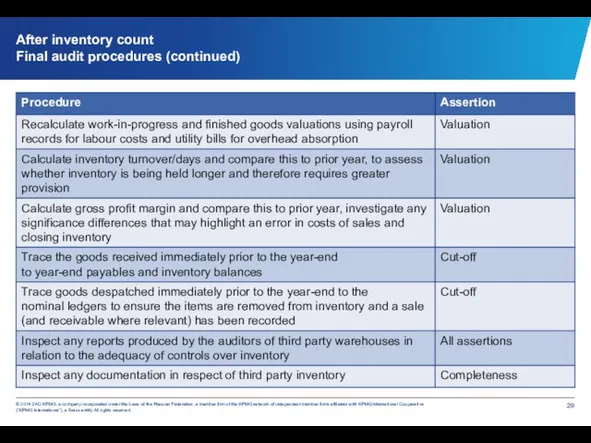

After inventory count

Final audit procedures (continued)

After inventory count

Final audit procedures (continued)

After inventory count

Final audit procedures (continued)

After inventory count

Final audit procedures (continued)

Receivables

Focus Valuation

Direct testing Receivables overstatement

Indirect testing Revenue overstatement

One of the main sources of evidence

Receivables

Focus Valuation

Direct testing Receivables overstatement

Indirect testing Revenue overstatement

One of the main sources of evidence

Confirmation letters

ISA 505 “External confirmations” requires the auditor to maintain control

Confirmation letters

ISA 505 “External confirmations” requires the auditor to maintain control

Receivables

Audit procedures

Receivables

Audit procedures

Receivables

Audit procedures (continued)

Receivables

Audit procedures (continued)

Prepayments

Audit procedures

Prepayments are services or goods for which a company has

Prepayments

Audit procedures

Prepayments are services or goods for which a company has

Payables & Accruals

Audit procedures

Focus Completeness

Direct testing Understatement of payables

Indirect testing Understatement of cost of

Payables & Accruals

Audit procedures

Focus Completeness

Direct testing Understatement of payables

Indirect testing Understatement of cost of

Payables & Accruals

Audit procedures (continued)

Payables & Accruals

Audit procedures (continued)

Payables & Accruals

Audit procedures (continued)

Payables & Accruals

Audit procedures (continued)

Provisions

IAS 37 Provisions, Contingent Liabilities and Contingent Assets requires an entity

Provisions

IAS 37 Provisions, Contingent Liabilities and Contingent Assets requires an entity

Provisions

Audit procedures

Provisions

Audit procedures

Test your understanding

The statement of financial position shows that Garden &

Test your understanding

The statement of financial position shows that Garden &

Solution

Among possible audit procedures can be the following:

Enquire with the directors

Solution

Among possible audit procedures can be the following:

Enquire with the directors

Share capital, reserves & director's remuneration

Share capital, reserves & director's remuneration

Statement of profit or loss

Purchases and other expenses

Recalculate discounts and sales

Statement of profit or loss

Purchases and other expenses

Recalculate discounts and sales

Statement of profit or loss

Payroll:

Agree the total wages and salaries expense

Statement of profit or loss

Payroll:

Agree the total wages and salaries expense

Test your understanding

Total payroll for the year ending 31 December 2012

Test your understanding

Total payroll for the year ending 31 December 2012

Accounting estimates

ISA 540 “Auditing Accounting Estimates” requires the auditor to:

Obtain an

Accounting estimates

ISA 540 “Auditing Accounting Estimates” requires the auditor to:

Obtain an

Accounting estimates – Smaller entities

Smaller entities may well be engaged in

Accounting estimates – Smaller entities

Smaller entities may well be engaged in

Accounting estimates – Smaller entities

Problems

Management override a key director or manager

Accounting estimates – Smaller entities

Problems

Management override a key director or manager

Related party is a person or entity that has control or

Related party is a person or entity that has control or

Accounting estimates – Not-for-profit organisations (NFP)

Characteristics:

Profit maximisation is not the goal.

Do

Accounting estimates – Not-for-profit organisations (NFP)

Characteristics:

Profit maximisation is not the goal.

Do

Accounting estimates – Not-for-profit organisations (NFP)

Audit implications

Testing tends to concentrate on

Accounting estimates – Not-for-profit organisations (NFP)

Audit implications

Testing tends to concentrate on

Summary (visual reference)

Summary (visual reference)

Организация работы бухгалтерской службы в кредитной организации

Организация работы бухгалтерской службы в кредитной организации ФСБУ 5. Изменения в учете запасов, реализация в 1С:Бухгалтерии 3.0

ФСБУ 5. Изменения в учете запасов, реализация в 1С:Бухгалтерии 3.0 Споживче кредитування

Споживче кредитування Фінанси підприємств. Фінансова санація підприємств. (Тема 11)

Фінанси підприємств. Фінансова санація підприємств. (Тема 11) Invest pres Invend. Внедрение киосков самостоятельной регистрации для отелей

Invest pres Invend. Внедрение киосков самостоятельной регистрации для отелей Жеке табыс салығы

Жеке табыс салығы Отчет об исполнении бюджета муниципального района. Стерлитамакский район Республики Башкортоста

Отчет об исполнении бюджета муниципального района. Стерлитамакский район Республики Башкортоста Влияние учета основных средств на объем производства на примере ООО ПКК Технорегион

Влияние учета основных средств на объем производства на примере ООО ПКК Технорегион Личные финансы (Финансы населения или финансы домохозяйств)

Личные финансы (Финансы населения или финансы домохозяйств) Венчурные фонды в России

Венчурные фонды в России Расчеты и платежи

Расчеты и платежи Вопросы назначения мер социальной поддержки и субсидий по оплате жилищно-коммунальных услуг в АС АСП

Вопросы назначения мер социальной поддержки и субсидий по оплате жилищно-коммунальных услуг в АС АСП Проект Прямые выплаты для страхователя. Ленинградское региональное отделение фонда социального страхования РФ

Проект Прямые выплаты для страхователя. Ленинградское региональное отделение фонда социального страхования РФ Изменения в налоговом законодательстве с 2023 года: Введение Единого налогового платежа

Изменения в налоговом законодательстве с 2023 года: Введение Единого налогового платежа Страхование автотранспорта

Страхование автотранспорта Техника и организация внешнеэкономической деятельности (ВЭД)

Техника и организация внешнеэкономической деятельности (ВЭД) Практикум по начислению и взиманию республиканских налогов и сборов

Практикум по начислению и взиманию республиканских налогов и сборов Международное налогооблажение

Международное налогооблажение Кредитный рынок

Кредитный рынок Бюджет для граждан Отчет об исполнении бюджета ГО Луховицы за 2018 год

Бюджет для граждан Отчет об исполнении бюджета ГО Луховицы за 2018 год Закони формування зарплати

Закони формування зарплати Анализ прибыли и рентабельности предприятия

Анализ прибыли и рентабельности предприятия Управление оборотом капитала

Управление оборотом капитала Бюджетное устройство и бюджетная система

Бюджетное устройство и бюджетная система Страхові фонди як матеріальна основа страхового захисту та його форми

Страхові фонди як матеріальна основа страхового захисту та його форми Зачем нужны деньги

Зачем нужны деньги Банк тарихы

Банк тарихы Счетная палата

Счетная палата