- Research proposal Liquidity risk management in banks

Содержание

- 2. Problem statement Financial crisis in 2008-2009 years disclosed that liquidity management is not efficient in Russian

- 3. Purpose statement The purpose of this explanatory study is to proof the suggestion that structure of

- 4. Type of research applied research quantitative research explanatory research

- 5. Objectives 1. To determine the effect of liquidity management on the performance of commercial banks; 2.

- 6. Research questions 1. What is nature of the relationship between bank liquidity management and bank profitability?

- 7. Hypothesis 1. There is a significant relationship between bank liquidity management and bank profitability. 2. The

- 8. A sample design – stratified random sampling and simple random sampling Data collection method – documentary

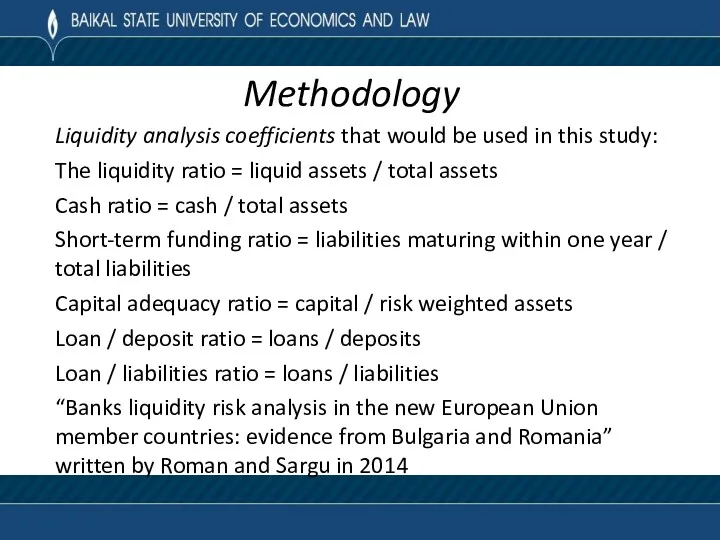

- 9. Methodology Liquidity analysis coefficients that would be used in this study: The liquidity ratio = liquid

- 10. Methodology Method of analysis is the regression analysis. The function for this study is given as:

- 11. Literature review “Liquidity risk in banking” written by Bonfim and Kim in 2012 Definitions of liquidity,

- 12. Literature review “Some Quantitative Aspects of Stability Management Strategy in a Bank” written by Sksonova and

- 14. Скачать презентацию

Problem statement

Financial crisis in 2008-2009 years disclosed that liquidity management is

Problem statement

Financial crisis in 2008-2009 years disclosed that liquidity management is

Purpose statement

The purpose of this explanatory study is to proof the

Purpose statement

The purpose of this explanatory study is to proof the

Type of research

applied research

quantitative research

explanatory research

Type of research

applied research

quantitative research

explanatory research

Objectives

1. To determine the effect of liquidity management on the performance

Objectives

1. To determine the effect of liquidity management on the performance

Research questions

1. What is nature of the relationship between bank liquidity

Research questions

1. What is nature of the relationship between bank liquidity

Hypothesis

1. There is a significant relationship between bank liquidity management and

Hypothesis

1. There is a significant relationship between bank liquidity management and

A sample design – stratified random sampling and simple random sampling

Data

A sample design – stratified random sampling and simple random sampling

Data

Methodology

Liquidity analysis coefficients that would be used in this study:

The liquidity

Methodology

Liquidity analysis coefficients that would be used in this study:

The liquidity

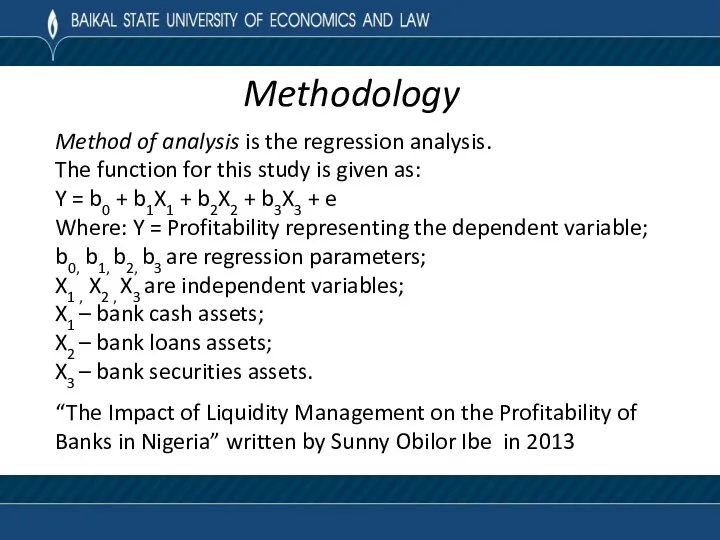

Methodology

Method of analysis is the regression analysis.

The function for this study

Methodology

Method of analysis is the regression analysis.

The function for this study

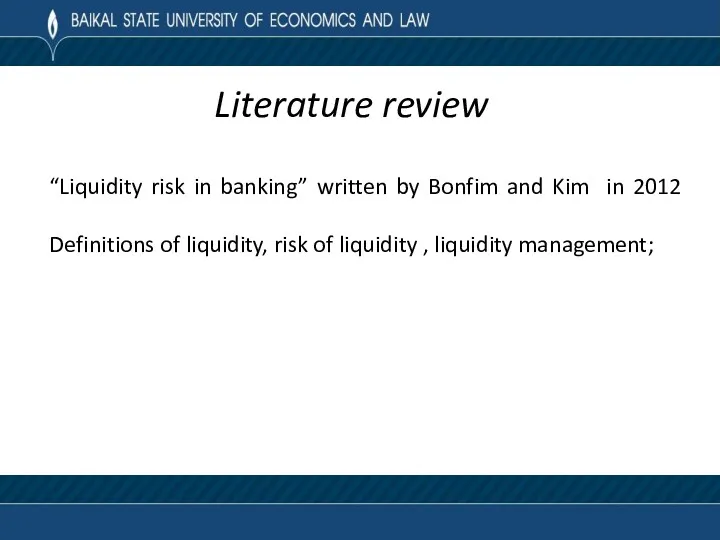

Literature review

“Liquidity risk in banking” written by Bonfim and Kim in

Literature review

“Liquidity risk in banking” written by Bonfim and Kim in

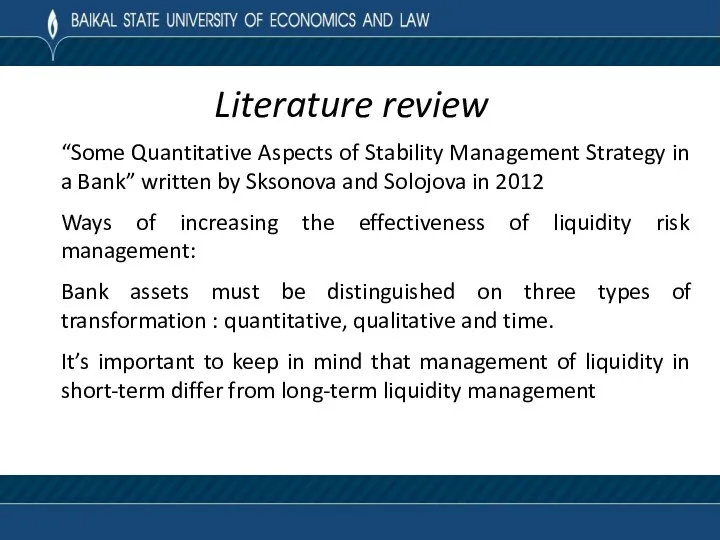

Literature review

“Some Quantitative Aspects of Stability Management Strategy in a Bank”

Literature review

“Some Quantitative Aspects of Stability Management Strategy in a Bank”

Оптимизация структуры капитала малого предприятия

Оптимизация структуры капитала малого предприятия Кәсіпкерлік қызметтегі тәуекелдер

Кәсіпкерлік қызметтегі тәуекелдер Коммерческое предложение для туристов. Банк Русский Стандарт

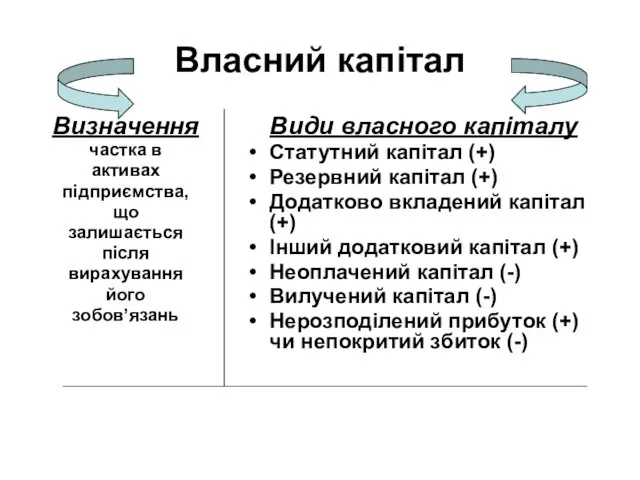

Коммерческое предложение для туристов. Банк Русский Стандарт Власний капітал

Власний капітал Банктің мөлшерлеме саясаты: пайыздық тәуекелдің қалыптастыру принциптері және басқару

Банктің мөлшерлеме саясаты: пайыздық тәуекелдің қалыптастыру принциптері және басқару Учет внеоборотных активов. Тема 7.5

Учет внеоборотных активов. Тема 7.5 Страхование имущества физических лиц САО ВСК. Страховые продукты

Страхование имущества физических лиц САО ВСК. Страховые продукты Доходы населения

Доходы населения История сотрудничества с ГК Уралэлектрострой и анализ причин образования проблемной задолженности

История сотрудничества с ГК Уралэлектрострой и анализ причин образования проблемной задолженности Особенности учета и аудита кредиторской задолженности на предприятии торговли Челябинский филиал ОАО ЖТК

Особенности учета и аудита кредиторской задолженности на предприятии торговли Челябинский филиал ОАО ЖТК Налог на имущество физических лиц

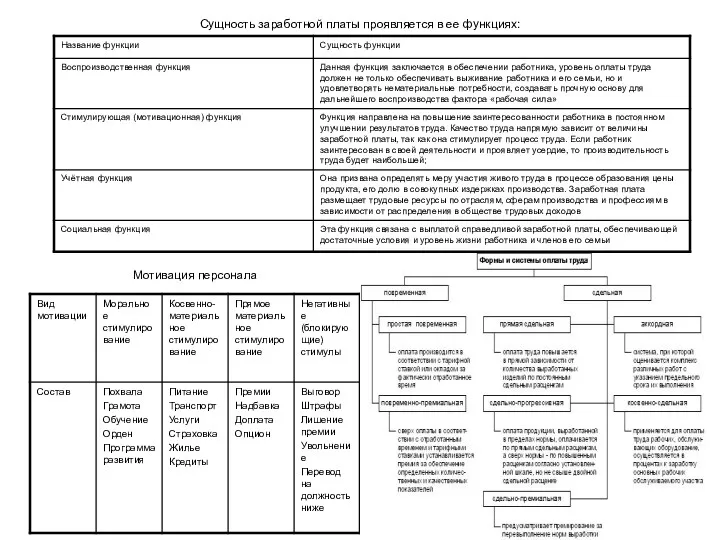

Налог на имущество физических лиц Заработная плата

Заработная плата Финансы домашних хозяйств

Финансы домашних хозяйств Налог на доходы физических лиц

Налог на доходы физических лиц Комерческое предложение по БВД

Комерческое предложение по БВД Доходность и риск финансовой операции

Доходность и риск финансовой операции Бюджет для граждан. К решению Земского собрания Варнавинского муниципального района О районном бюджете на 2017 год

Бюджет для граждан. К решению Земского собрания Варнавинского муниципального района О районном бюджете на 2017 год Бухгалтерские информационные системы

Бухгалтерские информационные системы Доходы и расходы семей

Доходы и расходы семей Страховий ринок США

Страховий ринок США Классификация доходов бюджета

Классификация доходов бюджета Способи реалізації інвестиційних проектів

Способи реалізації інвестиційних проектів Себестоимость продукции

Себестоимость продукции О введении обязательной маркировки

О введении обязательной маркировки Правовое регулирование и учет расчетов с персоналом по оплате труда

Правовое регулирование и учет расчетов с персоналом по оплате труда Сущность и классификация инвестиций. Инвестиционный проект: сущность, классификация

Сущность и классификация инвестиций. Инвестиционный проект: сущность, классификация Страховые формальности. Страхование в туризме. Виды страховых программ

Страховые формальности. Страхование в туризме. Виды страховых программ Бухгалтерский учет договоров аренды отдельными некредитными финансовыми организациями. Глава 13

Бухгалтерский учет договоров аренды отдельными некредитными финансовыми организациями. Глава 13