- The Valuation of Long-Term Securities

Содержание

- 2. After studying Chapter 4, you should be able to: Distinguish among the various terms used to

- 3. The Valuation of Long-Term Securities Distinctions Among Valuation Concepts Bond Valuation Preferred Stock Valuation Common Stock

- 4. What is Value? Going-concern value represents the amount a firm could be sold for as a

- 5. What is Value? (2) a firm: total assets minus liabilities and preferred stock as listed on

- 6. What is Value? Intrinsic value represents the price a security “ought to have” based on all

- 7. Bond Valuation Important Terms Types of Bonds Valuation of Bonds Handling Semiannual Compounding

- 8. Important Bond Terms The maturity value (MV) [or face value] of a bond is the stated

- 9. Important Bond Terms The discount rate (capitalization rate) is dependent on the risk of the bond

- 10. Different Types of Bonds A perpetual bond is a bond that never matures. It has an

- 11. Perpetual Bond Example Bond P has a $1,000 face value and provides an 8% annual coupon.

- 12. Different Types of Bonds A non-zero coupon-paying bond is a coupon paying bond with a finite

- 13. Bond C has a $1,000 face value and provides an 8% annual coupon for 30 years.

- 14. Different Types of Bonds A zero coupon bond is a bond that pays no interest but

- 15. V = $1,000 (PVIF10%, 30) = $1,000 (.057) = $57.00 Zero-Coupon Bond Example Bond Z has

- 16. Semiannual Compounding (1) Divide kd by 2 (2) Multiply n by 2 (3) Divide I by

- 17. (1 + kd/2 ) 2*n (1 + kd/2 )1 Semiannual Compounding A non-zero coupon bond adjusted

- 18. V = $40 (PVIFA5%, 30) + $1,000 (PVIF5%, 30) = $40 (15.373) + $1,000 (.231) [Table

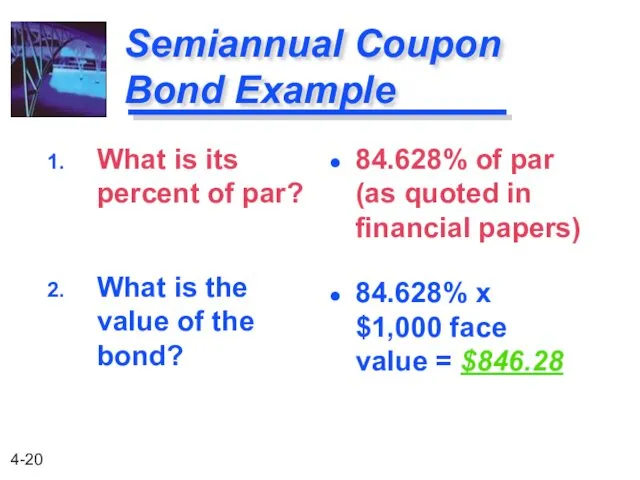

- 19. Semiannual Coupon Bond Example Let us use another worksheet on your calculator to solve this problem.

- 20. Semiannual Coupon Bond Example What is its percent of par? What is the value of the

- 21. Preferred Stock is a type of stock that promises a (usually) fixed dividend, but at the

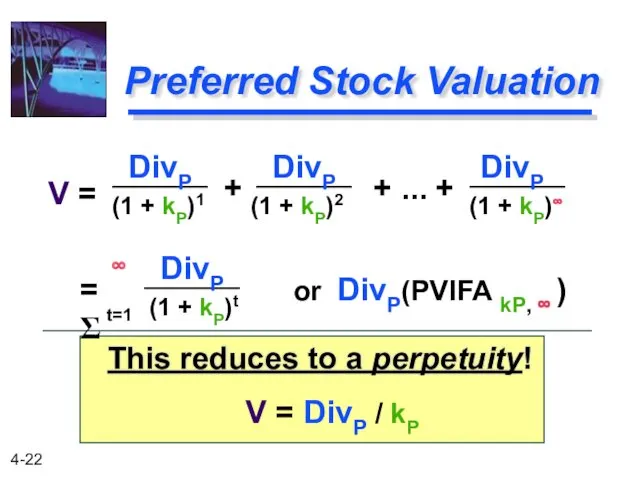

- 22. Preferred Stock Valuation This reduces to a perpetuity! (1 + kP)1 (1 + kP)2 (1 +

- 23. Preferred Stock Example DivP = $100 ( 8% ) = $8.00. kP = 10%. V =

- 24. Common Stock Valuation Pro rata share of future earnings after all other obligations of the firm

- 25. Common Stock Valuation (1) Future dividends (2) Future sale of the common stock shares What cash

- 26. Dividend Valuation Model Basic dividend valuation model accounts for the PV of all future dividends. (1

- 27. Adjusted Dividend Valuation Model The basic dividend valuation model adjusted for the future stock sale. (1

- 28. Dividend Growth Pattern Assumptions The dividend valuation model requires the forecast of all future dividends. The

- 29. Constant Growth Model The constant growth model assumes that dividends will grow forever at the rate

- 30. Constant Growth Model Example Stock CG has an expected dividend growth rate of 8%. Each share

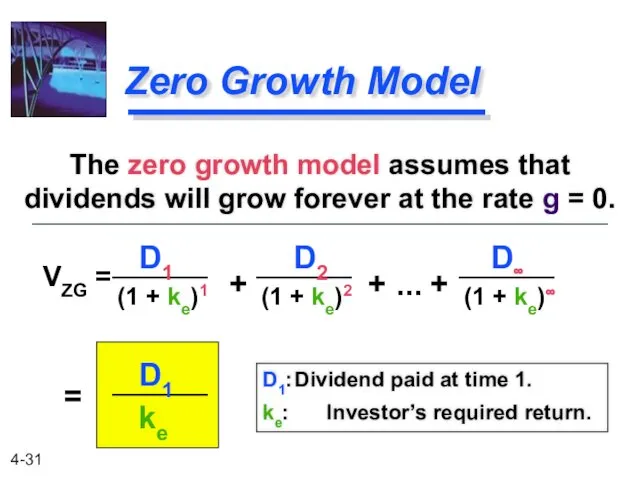

- 31. Zero Growth Model The zero growth model assumes that dividends will grow forever at the rate

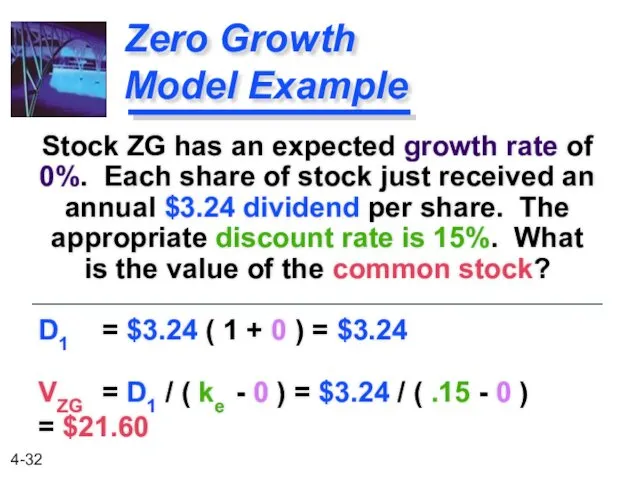

- 32. Zero Growth Model Example Stock ZG has an expected growth rate of 0%. Each share of

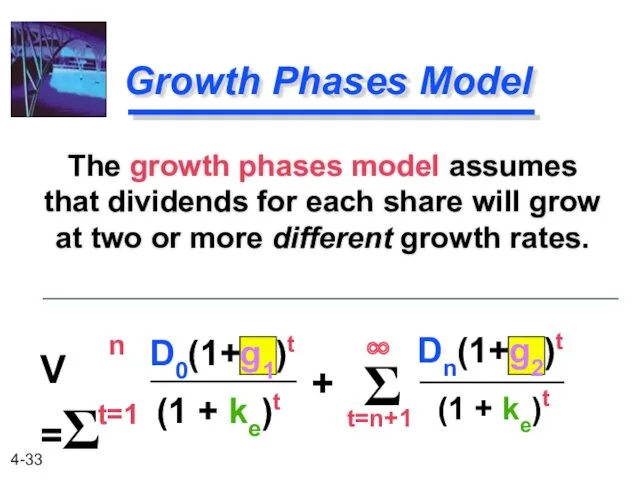

- 33. D0(1+g1)t Dn(1+g2)t Growth Phases Model The growth phases model assumes that dividends for each share will

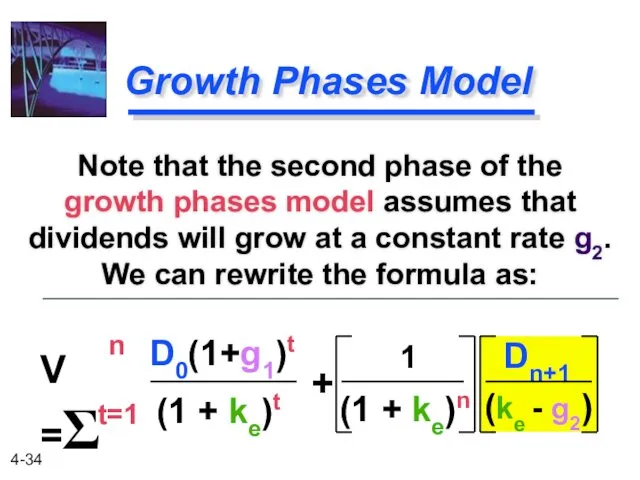

- 34. D0(1+g1)t Dn+1 Growth Phases Model Note that the second phase of the growth phases model assumes

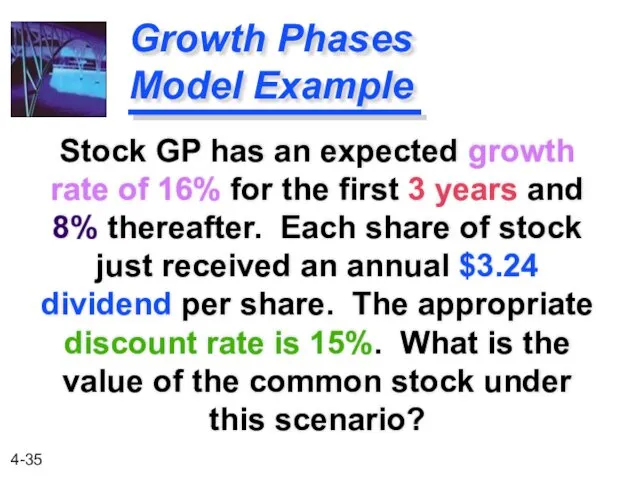

- 35. Growth Phases Model Example Stock GP has an expected growth rate of 16% for the first

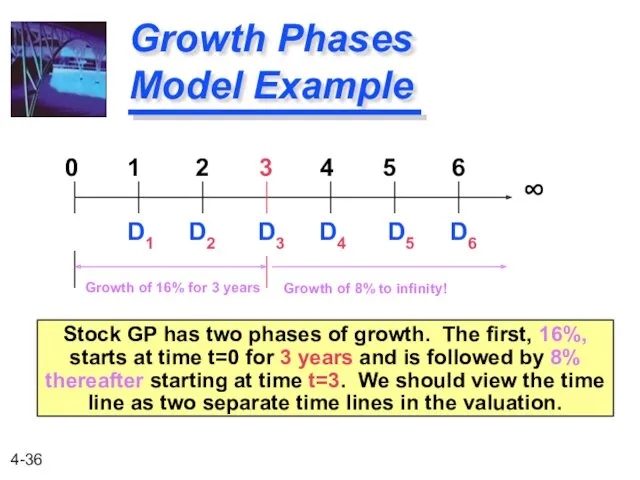

- 36. Growth Phases Model Example Stock GP has two phases of growth. The first, 16%, starts at

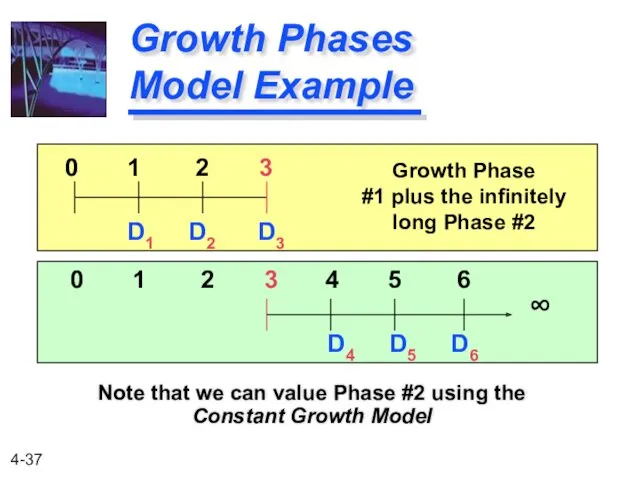

- 37. Growth Phases Model Example Note that we can value Phase #2 using the Constant Growth Model

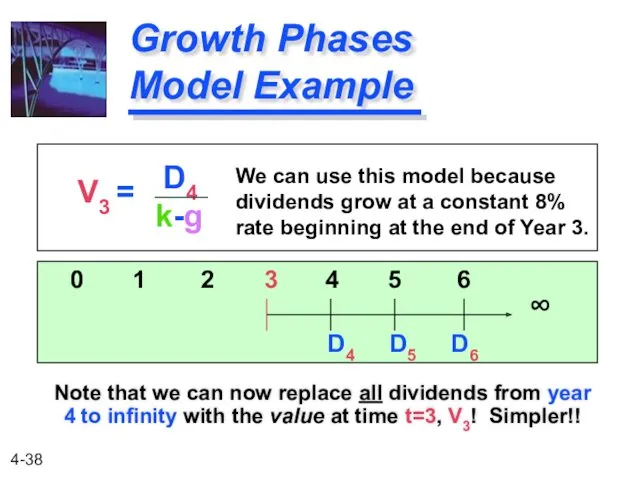

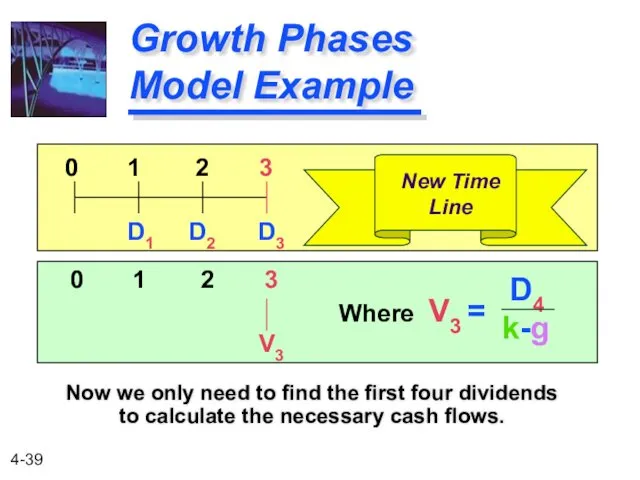

- 38. Growth Phases Model Example Note that we can now replace all dividends from year 4 to

- 39. Growth Phases Model Example Now we only need to find the first four dividends to calculate

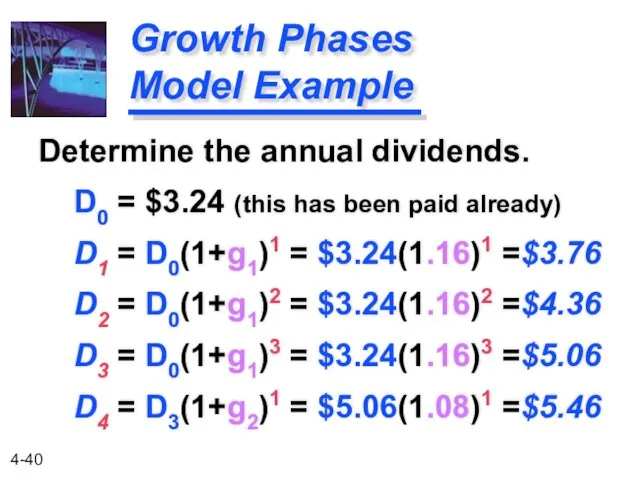

- 40. Growth Phases Model Example Determine the annual dividends. D0 = $3.24 (this has been paid already)

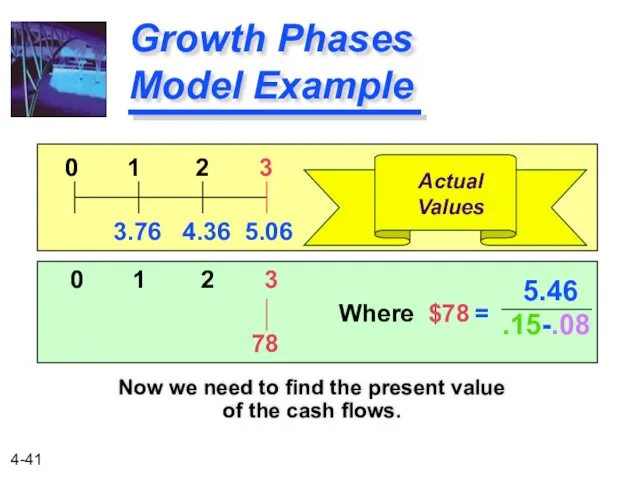

- 41. Growth Phases Model Example Now we need to find the present value of the cash flows.

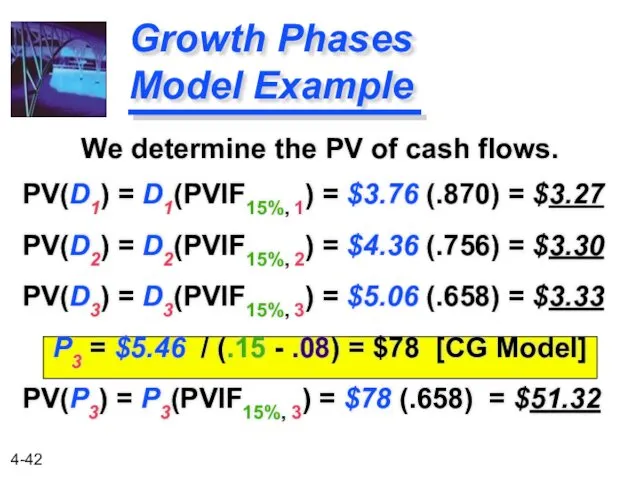

- 42. Growth Phases Model Example We determine the PV of cash flows. PV(D1) = D1(PVIF15%, 1) =

- 44. Скачать презентацию

After studying Chapter 4, you should be able to:

Distinguish among the

After studying Chapter 4, you should be able to:

Distinguish among the

The Valuation of

Long-Term Securities

Distinctions Among Valuation Concepts

Bond Valuation

Preferred Stock Valuation

Common

The Valuation of

Long-Term Securities

Distinctions Among Valuation Concepts

Bond Valuation

Preferred Stock Valuation

Common

What is Value?

Going-concern value represents the amount a firm could be

What is Value?

Going-concern value represents the amount a firm could be

What is Value?

(2) a firm: total assets minus liabilities and preferred

What is Value?

(2) a firm: total assets minus liabilities and preferred

What is Value?

Intrinsic value represents the price a security “ought to

What is Value?

Intrinsic value represents the price a security “ought to

Bond Valuation

Important Terms

Types of Bonds

Valuation of Bonds

Handling Semiannual Compounding

Bond Valuation

Important Terms

Types of Bonds

Valuation of Bonds

Handling Semiannual Compounding

![Important Bond Terms The maturity value (MV) [or face value]](/_ipx/f_webp&q_80&fit_contain&s_1440x1080/imagesDir/jpg/90227/slide-7.jpg)

Important Bond Terms

The maturity value (MV) [or face value] of a

Important Bond Terms

The maturity value (MV) [or face value] of a

Important Bond Terms

The discount rate (capitalization rate) is dependent on the

Important Bond Terms

The discount rate (capitalization rate) is dependent on the

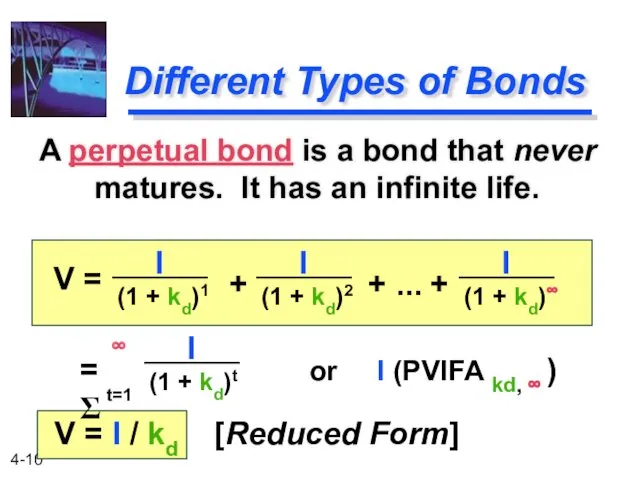

Different Types of Bonds

A perpetual bond is a bond that never

Different Types of Bonds

A perpetual bond is a bond that never

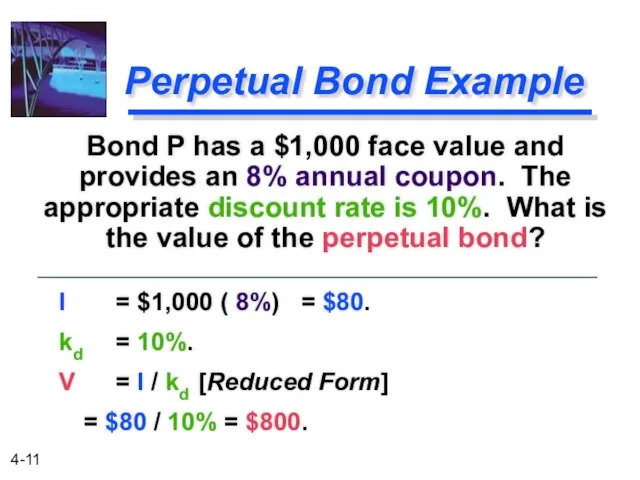

Perpetual Bond Example

Bond P has a $1,000 face value and provides

Perpetual Bond Example

Bond P has a $1,000 face value and provides

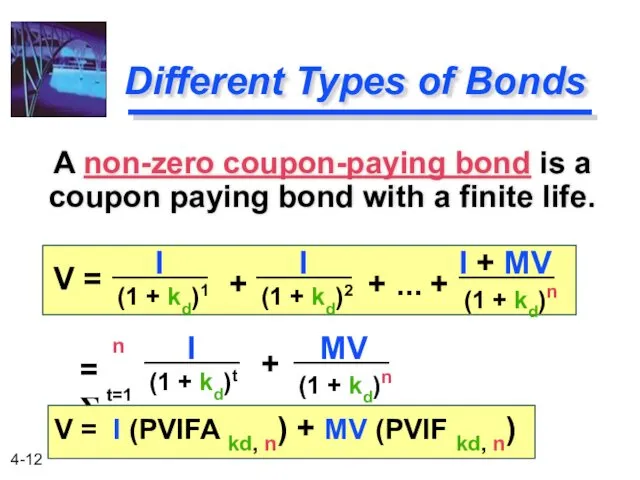

Different Types of Bonds

A non-zero coupon-paying bond is a coupon paying

Different Types of Bonds

A non-zero coupon-paying bond is a coupon paying

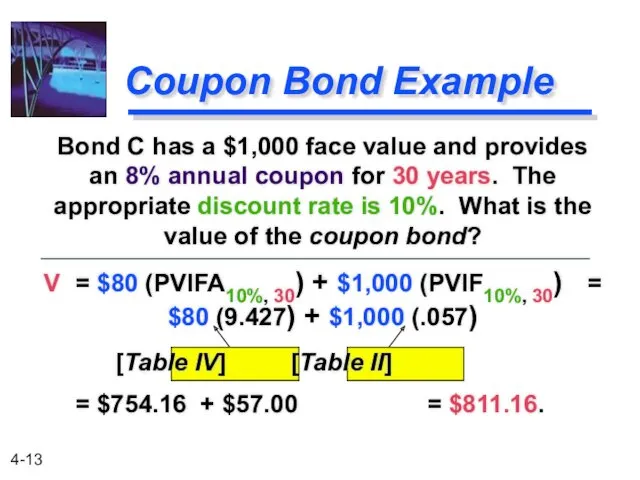

Bond C has a $1,000 face value and provides an 8%

Bond C has a $1,000 face value and provides an 8%

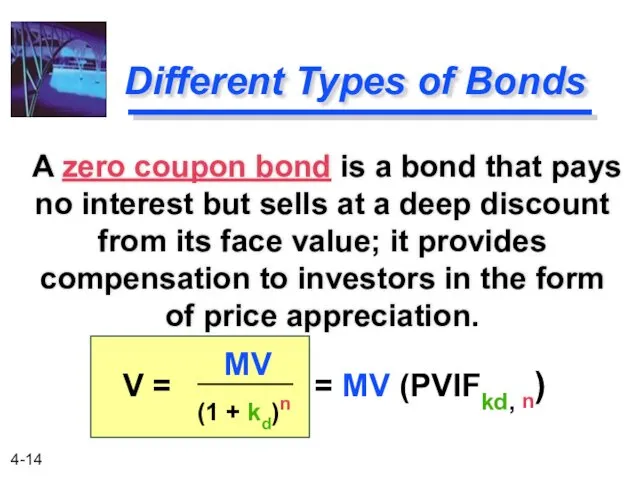

Different Types of Bonds

A zero coupon bond is a bond that

Different Types of Bonds

A zero coupon bond is a bond that

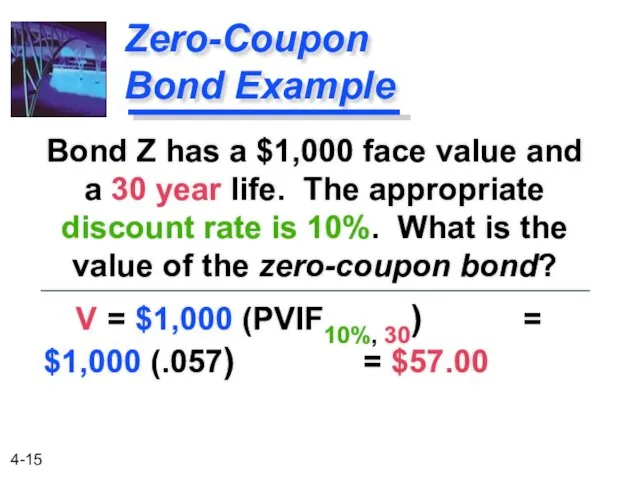

V = $1,000 (PVIF10%, 30) = $1,000 (.057) = $57.00

Zero-Coupon Bond Example

Bond Z has

V = $1,000 (PVIF10%, 30) = $1,000 (.057) = $57.00

Zero-Coupon Bond Example

Bond Z has

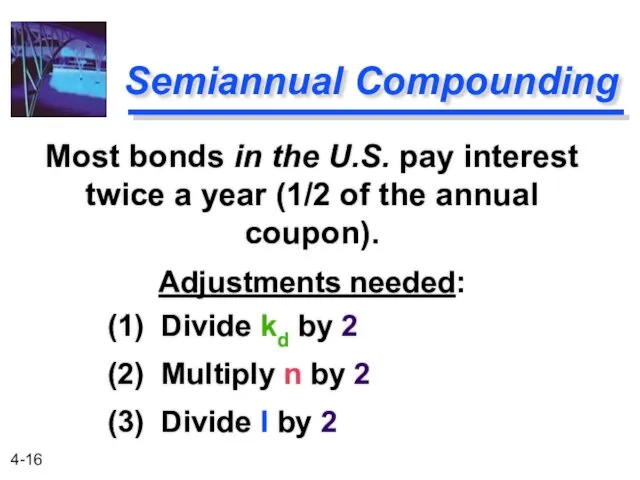

Semiannual Compounding

(1) Divide kd by 2

(2) Multiply n by 2

(3) Divide

Semiannual Compounding

(1) Divide kd by 2

(2) Multiply n by 2

(3) Divide

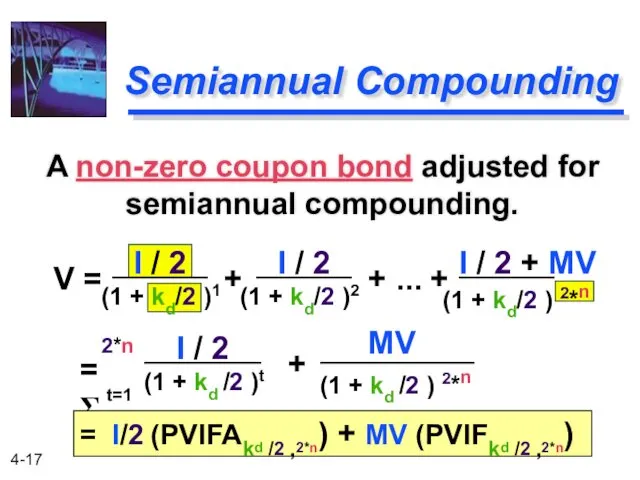

(1 + kd/2 ) 2*n

(1 + kd/2 )1

Semiannual Compounding

A non-zero coupon

(1 + kd/2 ) 2*n

(1 + kd/2 )1

Semiannual Compounding

A non-zero coupon

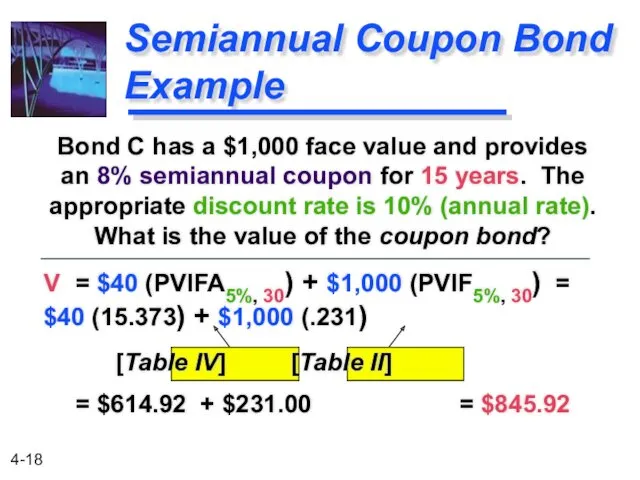

V = $40 (PVIFA5%, 30) + $1,000 (PVIF5%, 30) = $40 (15.373)

V = $40 (PVIFA5%, 30) + $1,000 (PVIF5%, 30) = $40 (15.373)

Semiannual Coupon Bond Example

Let us use another worksheet on your calculator

Semiannual Coupon Bond Example

Let us use another worksheet on your calculator

Semiannual Coupon Bond Example

What is its percent of par?

What is the

Semiannual Coupon Bond Example

What is its percent of par?

What is the

Preferred Stock is a type of stock that promises a (usually)

Preferred Stock is a type of stock that promises a (usually)

Preferred Stock Valuation

This reduces to a perpetuity!

(1 + kP)1

(1 + kP)2

(1

Preferred Stock Valuation

This reduces to a perpetuity!

(1 + kP)1

(1 + kP)2

(1

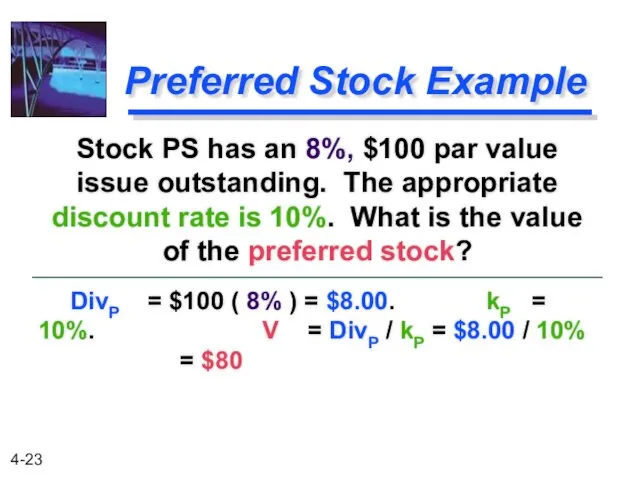

Preferred Stock Example

DivP = $100 ( 8% ) = $8.00. kP

Preferred Stock Example

DivP = $100 ( 8% ) = $8.00. kP

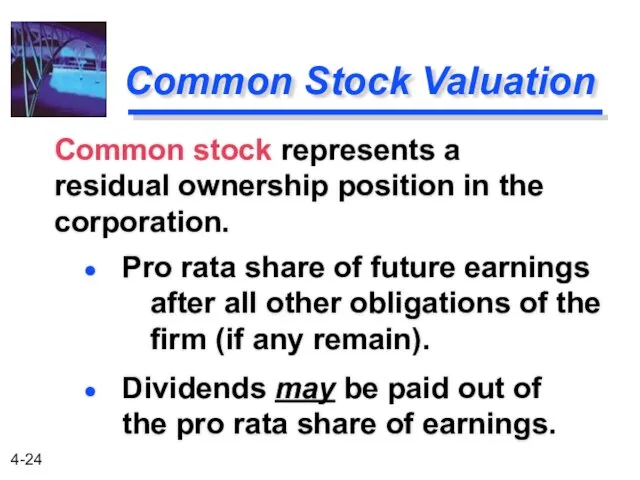

Common Stock Valuation

Pro rata share of future earnings after all other

Common Stock Valuation

Pro rata share of future earnings after all other

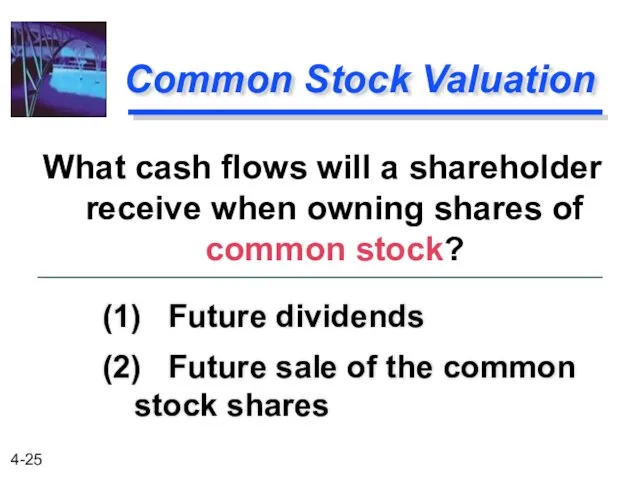

Common Stock Valuation

(1) Future dividends

(2) Future sale of the common stock

Common Stock Valuation

(1) Future dividends

(2) Future sale of the common stock

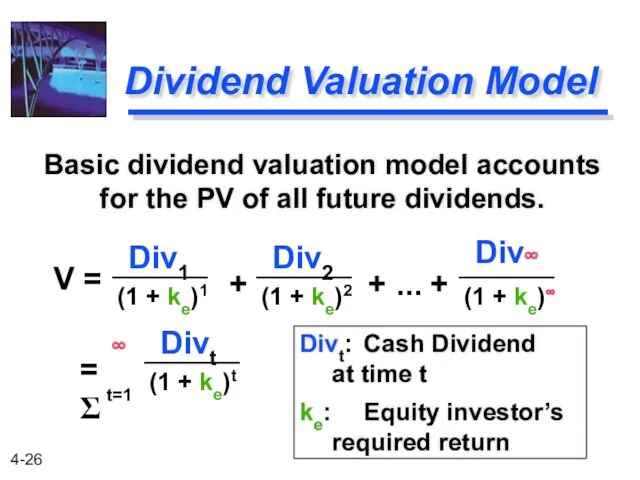

Dividend Valuation Model

Basic dividend valuation model accounts for the PV of

Dividend Valuation Model

Basic dividend valuation model accounts for the PV of

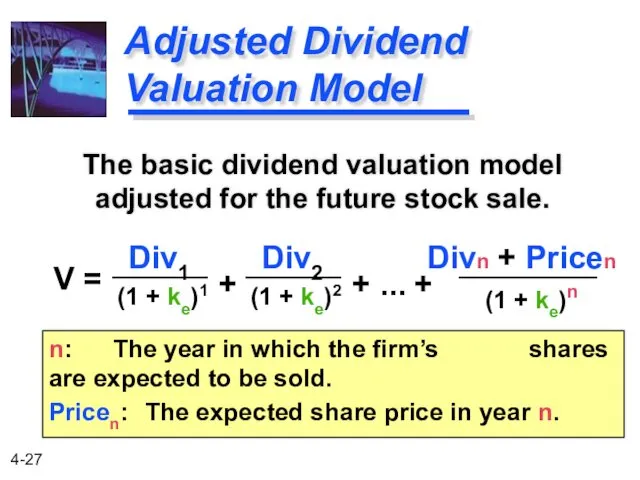

Adjusted Dividend Valuation Model

The basic dividend valuation model adjusted for the

Adjusted Dividend Valuation Model

The basic dividend valuation model adjusted for the

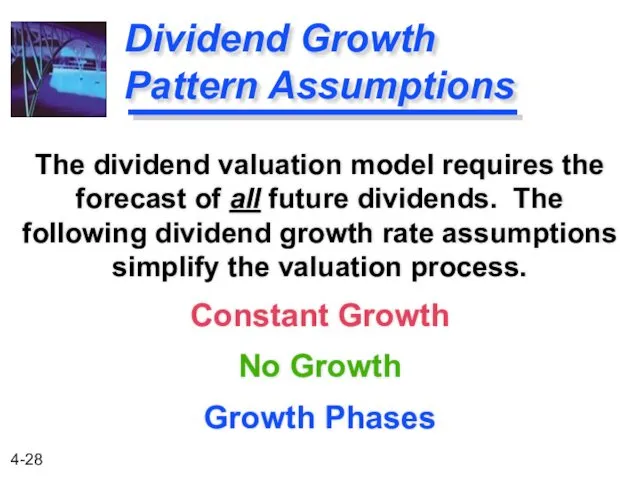

Dividend Growth Pattern Assumptions

The dividend valuation model requires the forecast of

Dividend Growth Pattern Assumptions

The dividend valuation model requires the forecast of

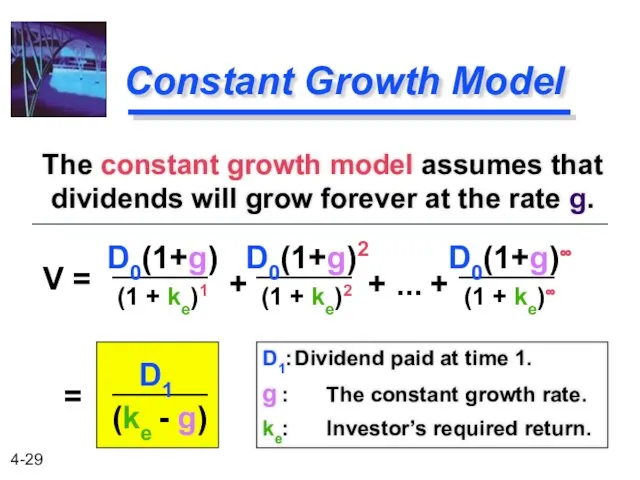

Constant Growth Model

The constant growth model assumes that dividends will grow

Constant Growth Model

The constant growth model assumes that dividends will grow

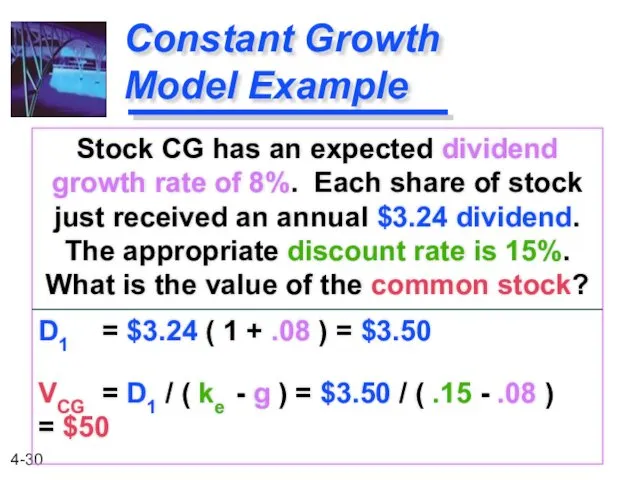

Constant Growth Model Example

Stock CG has an expected dividend growth rate

Constant Growth Model Example

Stock CG has an expected dividend growth rate

Zero Growth Model

The zero growth model assumes that dividends will grow

Zero Growth Model

The zero growth model assumes that dividends will grow

Zero Growth

Model Example

Stock ZG has an expected growth rate of

Zero Growth

Model Example

Stock ZG has an expected growth rate of

D0(1+g1)t

Dn(1+g2)t

Growth Phases Model

The growth phases model assumes that dividends for each

D0(1+g1)t

Dn(1+g2)t

Growth Phases Model

The growth phases model assumes that dividends for each

D0(1+g1)t

Dn+1

Growth Phases Model

Note that the second phase of the growth phases

D0(1+g1)t

Dn+1

Growth Phases Model

Note that the second phase of the growth phases

Growth Phases Model Example

Stock GP has an expected growth rate of

Growth Phases Model Example

Stock GP has an expected growth rate of

Growth Phases Model Example

Stock GP has two phases of growth. The

Growth Phases Model Example

Stock GP has two phases of growth. The

Growth Phases Model Example

Note that we can value Phase #2 using

Growth Phases Model Example

Note that we can value Phase #2 using

Growth Phases Model Example

Note that we can now replace all dividends

Growth Phases Model Example

Note that we can now replace all dividends

Growth Phases Model Example

Now we only need to find the first

Growth Phases Model Example

Now we only need to find the first

Growth Phases Model Example

Determine the annual dividends.

D0 = $3.24 (this

Growth Phases Model Example

Determine the annual dividends.

D0 = $3.24 (this

Growth Phases Model Example

Now we need to find the present value

Growth Phases Model Example

Now we need to find the present value

Growth Phases Model Example

We determine the PV of cash flows.

PV(D1) =

Growth Phases Model Example

We determine the PV of cash flows.

PV(D1) =

Ипотечное кредитование

Ипотечное кредитование Структура подразделения доставки банковских продуктов

Структура подразделения доставки банковских продуктов Роль системы внутреннего контроля в предотвращении мошенничества в финансовой отчетности

Роль системы внутреннего контроля в предотвращении мошенничества в финансовой отчетности New York Stock Exchange (NYSE)

New York Stock Exchange (NYSE) Роль и значение пенсионного фонда РФ в пенсионном обеспечении граждан. Схема назначения и выплаты пенсий

Роль и значение пенсионного фонда РФ в пенсионном обеспечении граждан. Схема назначения и выплаты пенсий Анализ и диагностика финансовых результатов деятельности предприятий торговли и общественного питания

Анализ и диагностика финансовых результатов деятельности предприятий торговли и общественного питания Оценка финансового состояния и финансовой устойчивости организации

Оценка финансового состояния и финансовой устойчивости организации Сергиево-Посадский городской округ. Персонифицированное финансирование дополнительного образования детей

Сергиево-Посадский городской округ. Персонифицированное финансирование дополнительного образования детей Финансовые рынки и институты

Финансовые рынки и институты Бухгалтерские счета и двойная запись

Бухгалтерские счета и двойная запись Индивидуальные инвестиционные счета. АО ФИНАМ

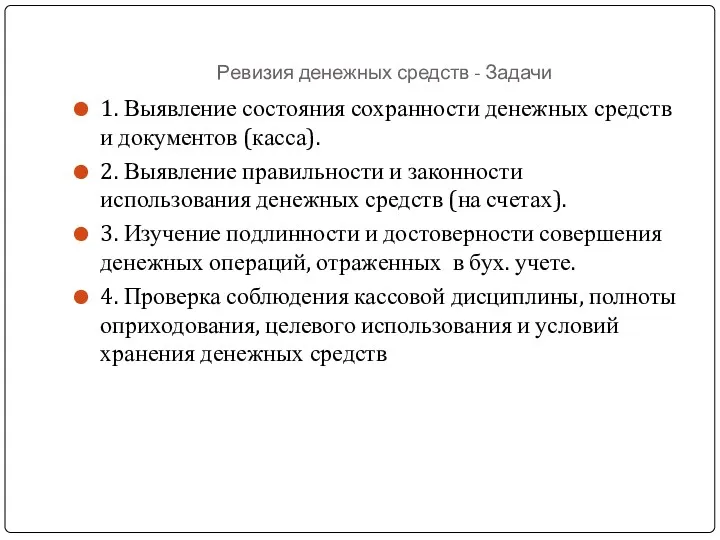

Индивидуальные инвестиционные счета. АО ФИНАМ Ревизия денежных средств. Задачи

Ревизия денежных средств. Задачи Депозитні операції з фізичними особами та управління ними в банку

Депозитні операції з фізичними особами та управління ними в банку Банковская Система РФ

Банковская Система РФ Теоретические основы затратного подхода к оценке предприятий

Теоретические основы затратного подхода к оценке предприятий Инвестиционные проекты и оценка их эффективности

Инвестиционные проекты и оценка их эффективности Упрощенная система налогообложения в издательской деятельности на примере ИП Смолина С.С

Упрощенная система налогообложения в издательской деятельности на примере ИП Смолина С.С Экономическая оценка инвестиций в логистических системах. Часть 1

Экономическая оценка инвестиций в логистических системах. Часть 1 Основы организации бухгалтерского учета в кредитных организациях

Основы организации бухгалтерского учета в кредитных организациях Эффект финансового рычага

Эффект финансового рычага Межбанковские расчеты РК и порядок их осуществления. (Тема 4)

Межбанковские расчеты РК и порядок их осуществления. (Тема 4) Продукты и услуги АО Альфа-Банк для Клиентов физических лиц

Продукты и услуги АО Альфа-Банк для Клиентов физических лиц Правовое регулирование деятельности бирж в Республике Беларусь

Правовое регулирование деятельности бирж в Республике Беларусь Финансирование малого и среднего инновационного бизнеса на территории Российской Федерации

Финансирование малого и среднего инновационного бизнеса на территории Российской Федерации Международный стандарт аудита 300. Планирование аудита финансовой отчетности

Международный стандарт аудита 300. Планирование аудита финансовой отчетности Риск. Количественная и качественная оценка рисков

Риск. Количественная и качественная оценка рисков Тест Хауи в США: современная практика его применения

Тест Хауи в США: современная практика его применения Жалпы және таза табыс

Жалпы және таза табыс