- Venture deal types

Содержание

- 2. Common stock … is what most people think of when they think of owning part of

- 3. Common stock Common stock can pay cash dividends based on company earnings but only after preferred

- 4. Common stock Common stock can be issued in one or more classes. One frequently used company

- 5. Convertible debentures … are debt instruments that entitle the lender to exchange the right to receive

- 6. Convertible preferred stock … is a type of stock used frequently by venture capital investors. The

- 7. Convertible preferred stock A typical convertible preferred stock used by venture capitalist investors also entitles the

- 8. Convertible preferred stock The formula used to convert the convertible preferred stock into shares of common

- 9. Convertible preferred stock Some convertible preferred stocks also permit the investor to require the company to

- 10. Convertible securities … are equity or debt investments that can be exchanged for something else of

- 11. Convertible securities Convertible securities are a nice way for investors to hedge. They allow them to

- 12. Convertible securities Most venture capitalists like convertible securities because they help preserve their capital and give

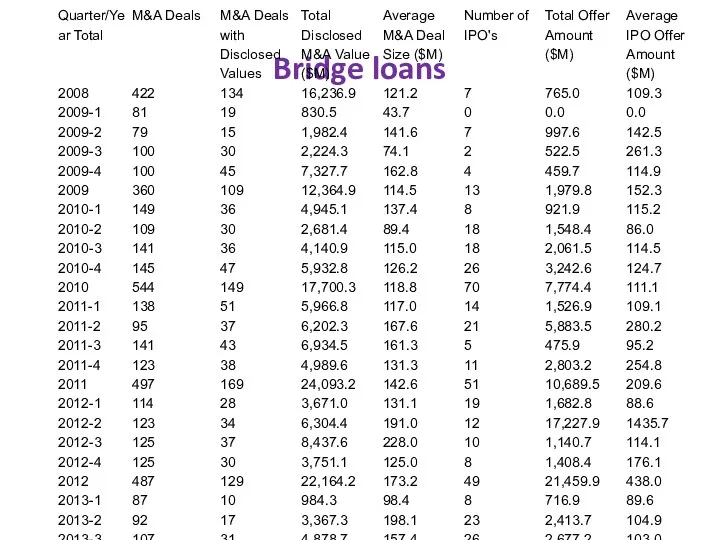

- 13. Bridge loans …are short-term financing agreements that fund a company's operations until it can arrange a

- 14. Bridge loans Bridge loans are risky. Whether a company's original investors or an outside lender provides

- 15. Bridge loans When accepting bridge financing, management should be careful to understand the consequences if the

- 16. Bridge loans

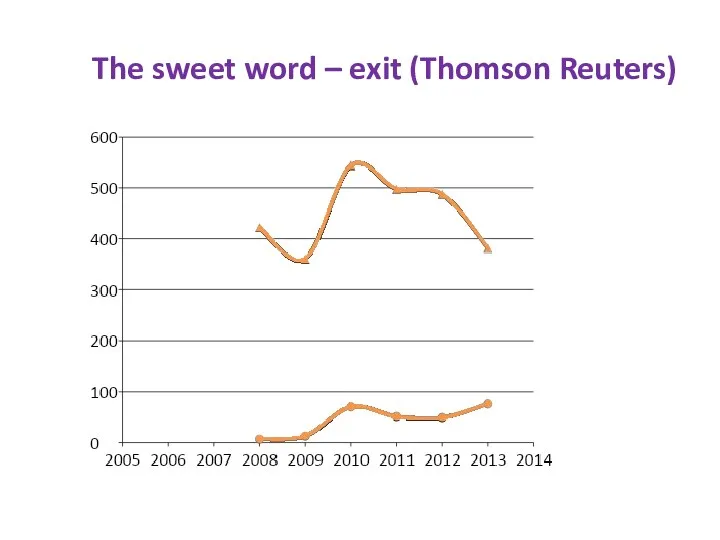

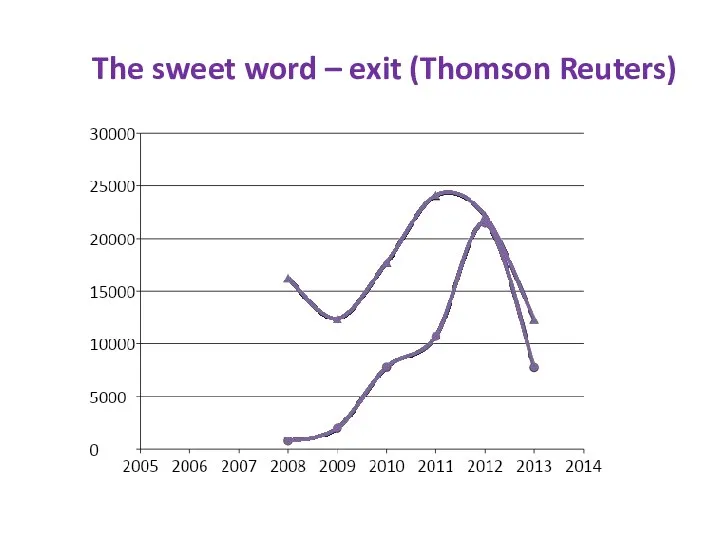

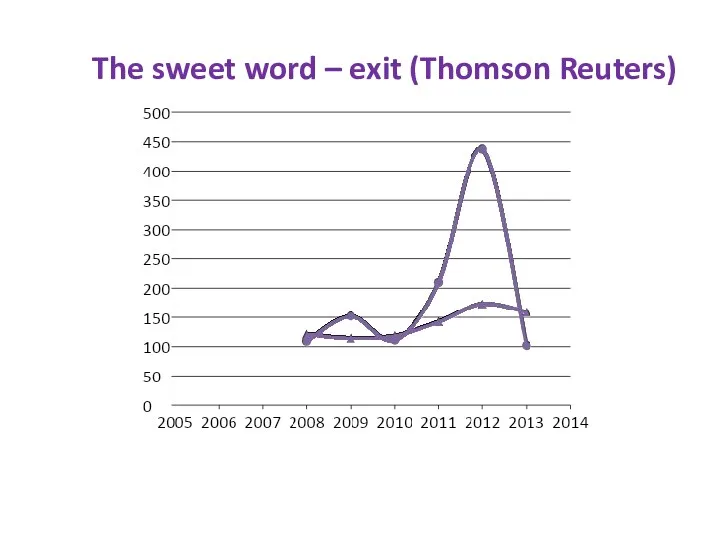

- 17. The sweet word – exit (Thomson Reuters)

- 18. The sweet word – exit (Thomson Reuters)

- 19. The sweet word – exit (Thomson Reuters)

- 21. Скачать презентацию

Common stock

… is what most people think of when they think

Common stock

… is what most people think of when they think

Common stock

Common stock can pay cash dividends based on company earnings

Common stock

Common stock can pay cash dividends based on company earnings

Common stock

Common stock can be issued in one or more classes.

Common stock

Common stock can be issued in one or more classes.

Convertible debentures

… are debt instruments that entitle the lender to exchange

Convertible debentures

… are debt instruments that entitle the lender to exchange

Convertible preferred stock

… is a type of stock used frequently by

Convertible preferred stock

… is a type of stock used frequently by

Convertible preferred stock

A typical convertible preferred stock used by venture capitalist

Convertible preferred stock

A typical convertible preferred stock used by venture capitalist

Convertible preferred stock

The formula used to convert the convertible preferred stock

Convertible preferred stock

The formula used to convert the convertible preferred stock

Convertible preferred stock

Some convertible preferred stocks also permit the investor to

Convertible preferred stock

Some convertible preferred stocks also permit the investor to

Convertible securities

… are equity or debt investments that can be exchanged

Convertible securities

… are equity or debt investments that can be exchanged

Convertible securities

Convertible securities are a nice way for investors to hedge.

Convertible securities

Convertible securities are a nice way for investors to hedge.

Convertible securities

Most venture capitalists like convertible securities because they help preserve

Convertible securities

Most venture capitalists like convertible securities because they help preserve

Bridge loans

…are short-term financing agreements that fund a company's operations until

Bridge loans

…are short-term financing agreements that fund a company's operations until

Bridge loans

Bridge loans are risky. Whether a company's original investors or

Bridge loans

Bridge loans are risky. Whether a company's original investors or

Bridge loans

When accepting bridge financing, management should be careful to understand

Bridge loans

When accepting bridge financing, management should be careful to understand

Bridge loans

Bridge loans

The sweet word – exit (Thomson Reuters)

The sweet word – exit (Thomson Reuters)

The sweet word – exit (Thomson Reuters)

The sweet word – exit (Thomson Reuters)

The sweet word – exit (Thomson Reuters)

The sweet word – exit (Thomson Reuters)

Рынок ценных бумаг

Рынок ценных бумаг Стоимость и структура капитала корпорации. (Тема 9)

Стоимость и структура капитала корпорации. (Тема 9) Приклад заповнення касової книги

Приклад заповнення касової книги Бухгалтерский учет для организаций общественного питания

Бухгалтерский учет для организаций общественного питания Қазақстан Халық Жинақ Банкі

Қазақстан Халық Жинақ Банкі Муниципальное образование город Алапаевск. Бюджет для граждан

Муниципальное образование город Алапаевск. Бюджет для граждан Оффшорные зоны

Оффшорные зоны Семейная экономика

Семейная экономика Права и обязанности страхователей, застрахованных лиц, федеральных органов гос.власти по обязательному пенсионному страхованию

Права и обязанности страхователей, застрахованных лиц, федеральных органов гос.власти по обязательному пенсионному страхованию Организация денежного обращения. Законы денежного обращения. Денежная масса и скорость обращения денег. Денежная база

Организация денежного обращения. Законы денежного обращения. Денежная масса и скорость обращения денег. Денежная база Финансовая система России

Финансовая система России Понятие бухгалтерского учёта

Понятие бухгалтерского учёта Басқару жүйесіндегі бухгальтерлік есептің жалпы сипаттамасы

Басқару жүйесіндегі бухгальтерлік есептің жалпы сипаттамасы Наш розумний дім

Наш розумний дім Основи побудови фінансово обліку

Основи побудови фінансово обліку Медицинское страхование

Медицинское страхование Депозитный портфель и депозитная политика коммерческого банка

Депозитный портфель и депозитная политика коммерческого банка Получение банковской лицензии

Получение банковской лицензии Финансовые институты. Ценные бумаги. Фондовый рынок

Финансовые институты. Ценные бумаги. Фондовый рынок Понятие денег и их роль в экономике

Понятие денег и их роль в экономике Обзор изменений законодательства, федеральные стандарты бухгалтерского учета для организаций государственного сектора

Обзор изменений законодательства, федеральные стандарты бухгалтерского учета для организаций государственного сектора Програма підтримки органів виконавчої влади Сокальського району

Програма підтримки органів виконавчої влади Сокальського району Фактическое исполнение инвестиционной программы

Фактическое исполнение инвестиционной программы Контроль качества аудита. (Тема 8)

Контроль качества аудита. (Тема 8) Способы принудительного исполнения налоговой обязанности

Способы принудительного исполнения налоговой обязанности Финансовые результаты деятельности страховых организаций

Финансовые результаты деятельности страховых организаций Финансовые инструменты

Финансовые инструменты Оплата труда

Оплата труда