- Decision Making and Relevant Information

Содержание

- 2. Decision Models A decision model is a formal method of making a choice, often involving both

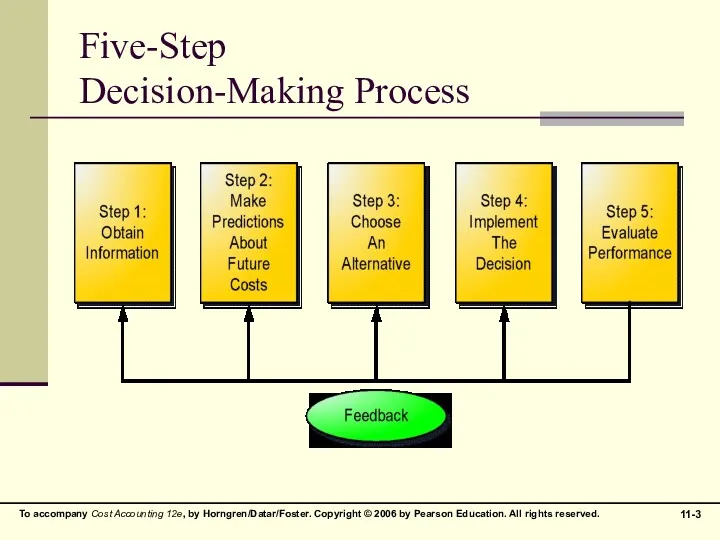

- 3. Five-Step Decision-Making Process

- 4. Relevance Relevant Information has two characteristics: It occurs in the future It differs among the alternative

- 5. Irrelevance Historical costs are past costs that are irrelevant to decision making Also called Sunk Costs

- 6. Types of Information Quantitative factors are outcomes that can be measured in numerical terms Qualitative factors

- 7. Terminology Incremental Cost – the additional total cost incurred for an activity Differential Cost – the

- 8. Types of Decisions One-Time-Only Special Orders Insourcing vs. Outsourcing Make or Buy Product-Mix Customer Profitability Branch

- 9. One-Time-Only Special Orders Accepting or rejecting special orders when there is idle production capacity and the

- 10. One-Time-Only Special Orders Compares relevant revenues and relevant costs to determine profitability

- 11. Potential Problems with Relevant-Cost Analysis Avoid incorrect general assumptions about information, especially: “All variable costs are

- 12. Potential Problems with Relevant-Cost Analysis Problems with using unit-cost data: Including irrelevant costs in error Using

- 13. Avoiding Potential Problems with Relevant-Cost Analysis Focus on Total Revenues and Total Costs, not their per-unit

- 14. Insourcing vs. Outsourcing Insourcing – producing goods or services within an organization Outsourcing – purchasing goods

- 15. Qualitative Factors Nonquantitative factors may be extremely important in an evaluation process, yet do not show

- 16. Opportunity Costs Opportunity Cost is the contribution to operating income that is forgone by not using

- 17. Product-Mix Decisions The decisions made by a company about which products to sell and in what

- 18. Adding or Dropping Customers Decision Rule: Does adding or dropping a customer add operating income to

- 19. Adding or Discontinuing Branches or Segments Decision Rule: Does adding or discontinuing a branch or segment

- 20. Equipment-Replacement Decisions Sometimes difficult due to amount of information at hand that is irrelevant: Cost, Accumulated

- 22. Скачать презентацию

Decision Models

A decision model is a formal method of making a

Decision Models

A decision model is a formal method of making a

Five-Step

Decision-Making Process

Five-Step

Decision-Making Process

Relevance

Relevant Information has two characteristics:

It occurs in the future

It differs among

Relevance

Relevant Information has two characteristics:

It occurs in the future

It differs among

Irrelevance

Historical costs are past costs that are irrelevant to decision making

Also

Irrelevance

Historical costs are past costs that are irrelevant to decision making

Also

Types of Information

Quantitative factors are outcomes that can be measured in

Types of Information

Quantitative factors are outcomes that can be measured in

Terminology

Incremental Cost – the additional total cost incurred for an activity

Differential

Terminology

Incremental Cost – the additional total cost incurred for an activity

Differential

Types of Decisions

One-Time-Only Special Orders

Insourcing vs. Outsourcing

Make or Buy

Product-Mix

Customer Profitability

Branch

Types of Decisions

One-Time-Only Special Orders

Insourcing vs. Outsourcing

Make or Buy

Product-Mix

Customer Profitability

Branch

One-Time-Only Special Orders

Accepting or rejecting special orders when there is idle

One-Time-Only Special Orders

Accepting or rejecting special orders when there is idle

One-Time-Only Special Orders

Compares relevant revenues and relevant costs to determine profitability

One-Time-Only Special Orders

Compares relevant revenues and relevant costs to determine profitability

Potential Problems with

Relevant-Cost Analysis

Avoid incorrect general assumptions about information, especially:

“All

Potential Problems with

Relevant-Cost Analysis

Avoid incorrect general assumptions about information, especially:

“All

Potential Problems with

Relevant-Cost Analysis

Problems with using unit-cost data:

Including irrelevant costs

Potential Problems with

Relevant-Cost Analysis

Problems with using unit-cost data:

Including irrelevant costs

Avoiding Potential Problems with

Relevant-Cost Analysis

Focus on Total Revenues and Total

Avoiding Potential Problems with

Relevant-Cost Analysis

Focus on Total Revenues and Total

Insourcing vs. Outsourcing

Insourcing – producing goods or services within an organization

Outsourcing

Insourcing vs. Outsourcing

Insourcing – producing goods or services within an organization

Outsourcing

Qualitative Factors

Nonquantitative factors may be extremely important in an evaluation process,

Qualitative Factors

Nonquantitative factors may be extremely important in an evaluation process,

Opportunity Costs

Opportunity Cost is the contribution to operating income that is

Opportunity Costs

Opportunity Cost is the contribution to operating income that is

Product-Mix Decisions

The decisions made by a company about which products to

Product-Mix Decisions

The decisions made by a company about which products to

Adding or Dropping Customers

Decision Rule: Does adding or dropping a customer

Adding or Dropping Customers

Decision Rule: Does adding or dropping a customer

Adding or Discontinuing

Branches or Segments

Decision Rule: Does adding or discontinuing a

Adding or Discontinuing

Branches or Segments

Decision Rule: Does adding or discontinuing a

Equipment-Replacement Decisions

Sometimes difficult due to amount of information at hand that

Equipment-Replacement Decisions

Sometimes difficult due to amount of information at hand that

Памятка вахтовика. Что взять с собой?

Памятка вахтовика. Что взять с собой? Основы проект-менеджмента

Основы проект-менеджмента Система 5S на практике

Система 5S на практике Самсунг. Антикризисное управление

Самсунг. Антикризисное управление Руководство, власть и лидерство. Формы власти. Теории лидерства. Стили руководства

Руководство, власть и лидерство. Формы власти. Теории лидерства. Стили руководства Базовые принципы ведения переговоров

Базовые принципы ведения переговоров Telephone etiquette

Telephone etiquette SWOT-анализ предприятия ООО ЭлектропультГрозный

SWOT-анализ предприятия ООО ЭлектропультГрозный Даяшы. Даяшы даярлығы

Даяшы. Даяшы даярлығы Вклад Генри Форда(1863-1947) в развитие управленческой деятельности

Вклад Генри Форда(1863-1947) в развитие управленческой деятельности Транспортно-логистический сервис

Транспортно-логистический сервис Source Code Manager

Source Code Manager Участники проекта и окружение проекта

Участники проекта и окружение проекта Профессиональное развитие персонала

Профессиональное развитие персонала Мозговой штурм (30)

Мозговой штурм (30) Информационные технологии в разработке и оптимизации системы управления организацией на примере Business Studio. (Лекция 5)

Информационные технологии в разработке и оптимизации системы управления организацией на примере Business Studio. (Лекция 5) Построение системы управления документами: организационный аспект

Построение системы управления документами: организационный аспект Management

Management Пять этапов управления рисками. Курс для субъектов малого и среднего предпринимательства

Пять этапов управления рисками. Курс для субъектов малого и среднего предпринимательства Идеальный день начальника ОПС Салми

Идеальный день начальника ОПС Салми Управление карьерой работника

Управление карьерой работника Кадровое и нормативное обеспечение управления персоналом

Кадровое и нормативное обеспечение управления персоналом Основополагающие идеи и принципы управления изменениями

Основополагающие идеи и принципы управления изменениями Основы управления проектами. Лекция 1

Основы управления проектами. Лекция 1 Менеджмент деген не?

Менеджмент деген не? Коммерческое предложение

Коммерческое предложение Совершенствование организации обслуживания на предприятиях общественного питания

Совершенствование организации обслуживания на предприятиях общественного питания Транспортная логистика. (Тема 6)

Транспортная логистика. (Тема 6)