- Operational Risk Management: Best Practice Overview and Implementation

Содержание

- 2. Table of Contents

- 3. Table of Contents

- 4. Table of Contents

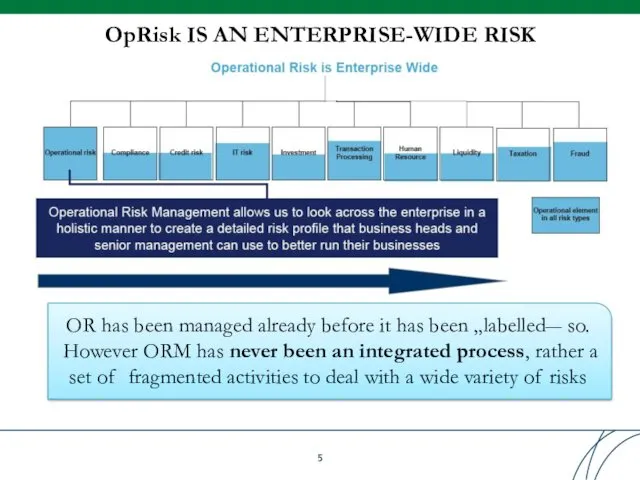

- 5. OpRisk IS AN ENTERPRISE-WIDE RISK OR has been managed already before it has been „labelled― so.

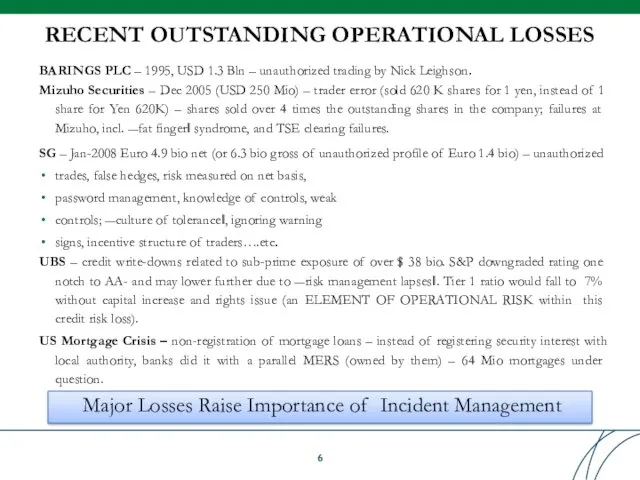

- 6. RECENT OUTSTANDING OPERATIONAL LOSSES BARINGS PLC – 1995, USD 1.3 Bln – unauthorized trading by Nick

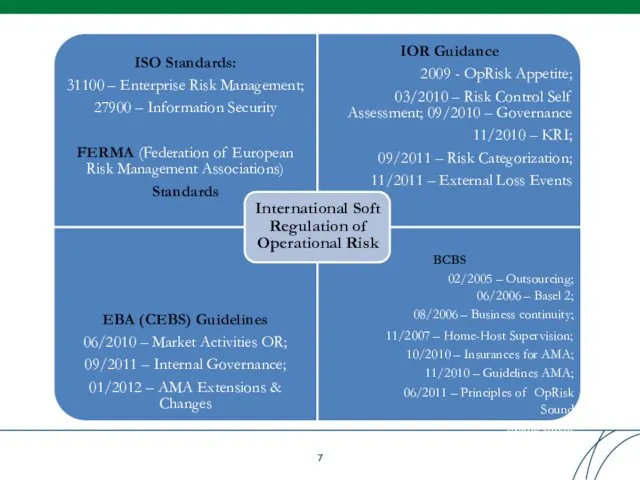

- 7. ISO Standards: 31100 – Enterprise Risk Management; 27900 – Information Security FERMA (Federation of European Risk

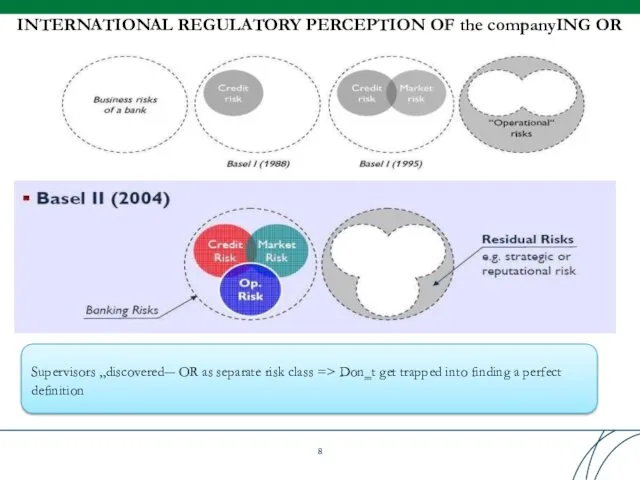

- 8. INTERNATIONAL REGULATORY PERCEPTION OF the companyING OR Supervisors „discovered― OR as separate risk class => Don‗t

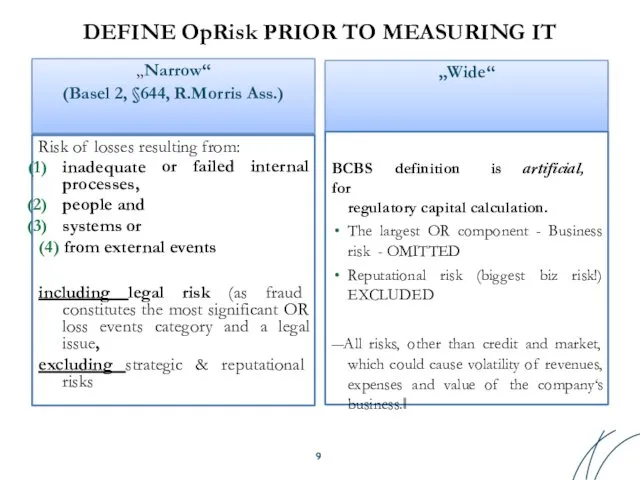

- 9. DEFINE OpRisk PRIOR TO MEASURING IT „Wide“ „Narrow“ (Basel 2, §644, R.Morris Ass.) Risk of losses

- 10. BANKING RISKS Strategic Risk Credit Risk Based on creditworthine ss Market Risk Based on market prices

- 11. OPERATIONAL RISK PORTION IN REGCAP OpRisk Diverse in its scope Encompasses the risks emanating from all

- 12. MANAGEMENT RISK - #1 OpRisk Management Risk components: conflicts of interest excessive pay levels breach of

- 13. LEGAL RISK Causes of legal risk materializing ❑Breakdown of the law enforcement ―industry‖ ❑ Corruption ❑Political

- 14. REPUT RISK INCLUSION INTO THE ORM Reputation is a key asset of a fin institution, as

- 15. Table of Contents

- 16. BASEL-2 PILLARS ON OpRisk Pillar 1 Minimum Capital Requirements (Objective: limit risk taking) Pillar 2 Capital

- 17. B2/PILLAR 1: ORM QUANTITATIVE & QUALITATIVE REQUIREMENTS OpRisk Capital allocation: 15% of average 3-y gross income

- 18. STAGES OF ORM DEVELOPMENT IN A BANK

- 19. GOALS OF OPERATIONAL RISK MANAGEMENT UNDER AMA Allocate - Budgets for Risk Reduction; - Capital Understand

- 20. COMPLEX BASEL AMA RISK GOVERNANCE FRAMEWORK Effective ORM Environment Governance & Organization ORM Function Design Committee

- 21. B2/PILLAR 2: PRINCIPLES FOR THE SOUND MANAGEMENT OF OpRisk (JUNE 2011) OpRisk mngt is especially important

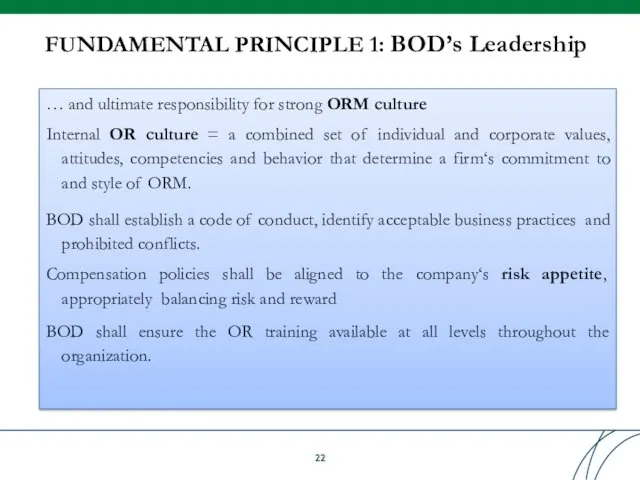

- 22. FUNDAMENTAL PRINCIPLE 1: BOD’s Leadership … and ultimate responsibility for strong ORM culture Internal OR culture

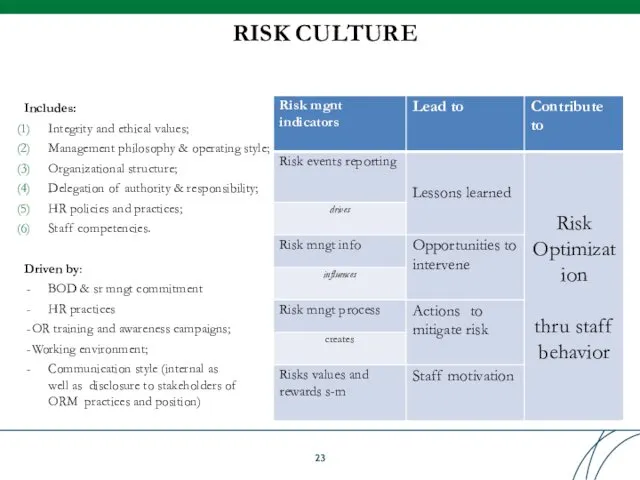

- 23. RISK CULTURE Includes: Integrity and ethical values; Management philosophy & operating style; Organizational structure; Delegation of

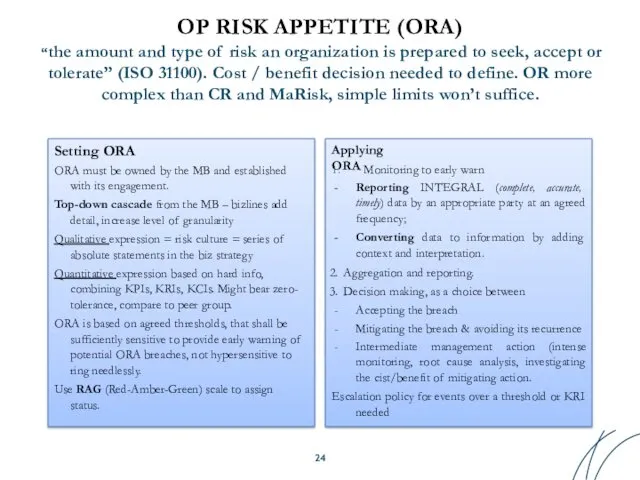

- 24. OP RISK APPETITE (ORA) “the amount and type of risk an organization is prepared to seek,

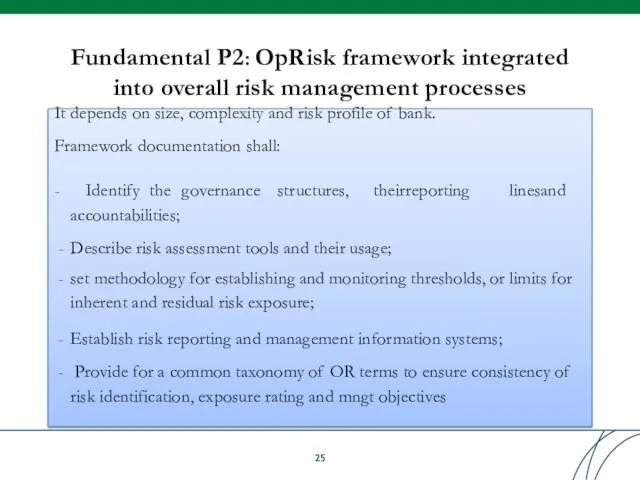

- 25. Fundamental P2: OpRisk framework integrated into overall risk management processes It depends on size, complexity and

- 26. B2: AMA – EXAMPLE OF ORM FRAMEWORK

- 27. MANAGING OpRisk THROUGH FRAMEWORK OR has been managed already before it has been „labelled― so: „4-eyes―-principle,

- 28. ORM FRAMEWORK IMPLEMENTATION I T ION DENTIFICA ASSESSMENT Find quantifiable means to track OR; Create Reporting

- 29. EXAMPLE OF COMPLEX ORM FRAMEWORK Mitigating actions Mitigating actions Net loss distribution Risk capital Capital allocation

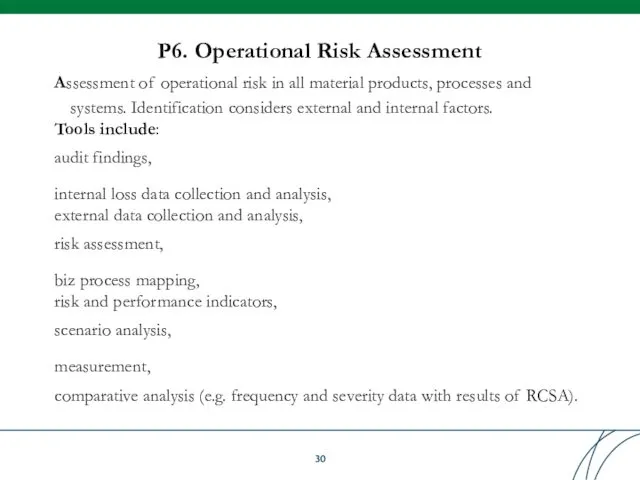

- 30. P6. Operational Risk Assessment Assessment of operational risk in all material products, processes and systems. Identification

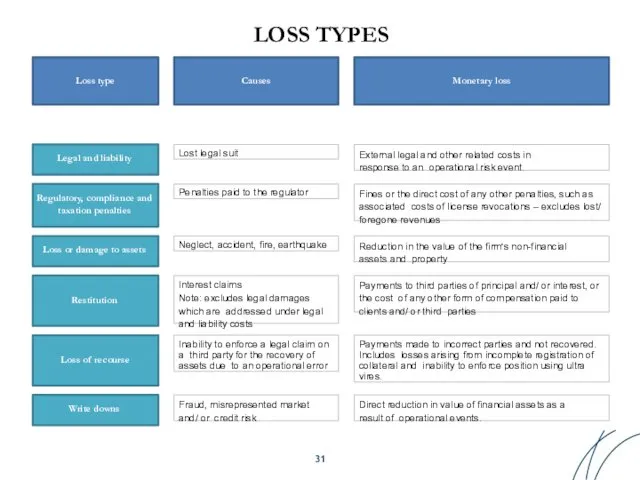

- 31. LOSS TYPES Loss type Causes Monetary loss Legal and liability Lost legal suit External legal and

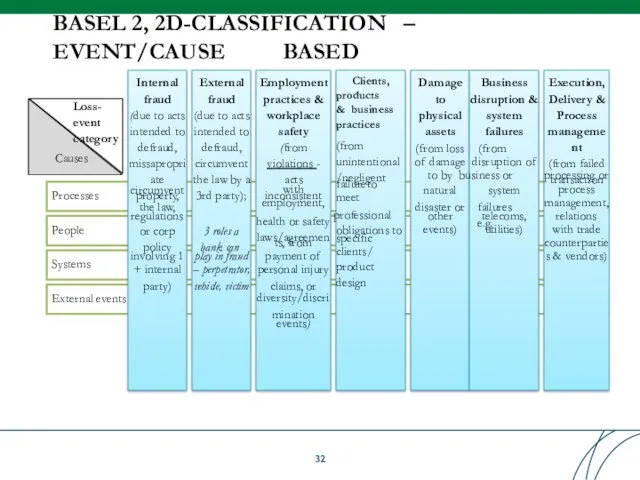

- 32. Processes People Systems External events BASEL 2, 2D-CLASSIFICATION – EVENT/CAUSE BASED Internal fraud (due to acts

- 33. Internal Fraud Unauthorized Activity (transactions intentionally not reported; transaction type unauthorized w/o monetary loss), intentional mismarking

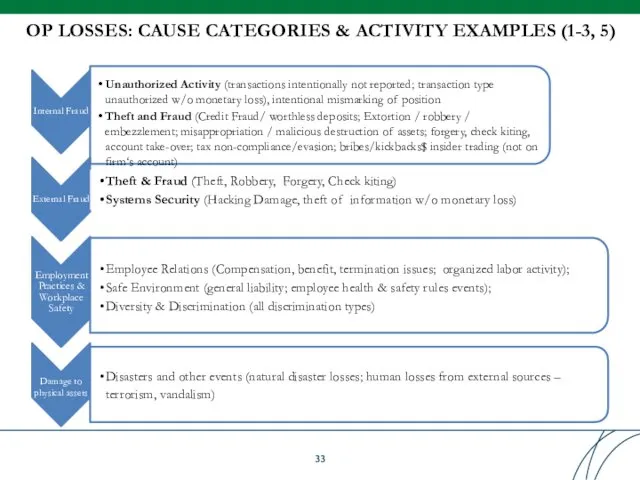

- 34. OP LOSSES: CAUSE CATEGORIES & ACTIVITY EXAMPLES Clients, Products & Biz Practices Suitability, Disclosure & Fiduciary

- 35. 3D OPERATIONAL LOSS CLASSIFICATION Internal fraud External fraud Damage to physical assets Business disruption & system

- 36. RISK MANAGEMENT ENVIRONMENT -OpRisk shall be managed as a distinct category of risks -Set principles for

- 37. RISK MANAGEMENT CONTROL ENVIRONMENT (P9) I. Internal controls: II. Risk mitigation strategies III. Risk transfer strategies

- 38. Table of Contents

- 39. Table of Contents

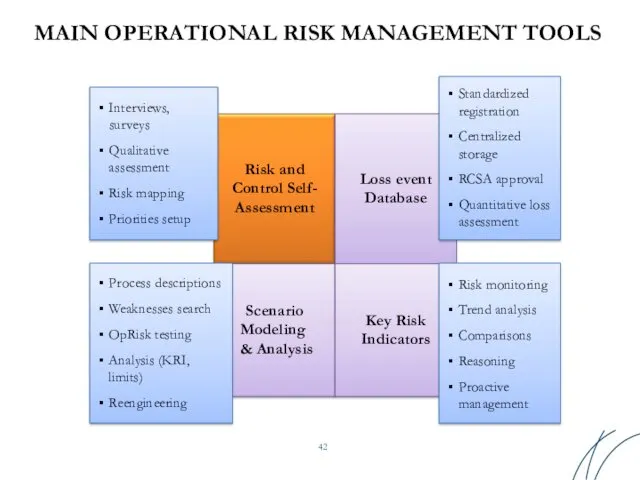

- 40. MAIN OPERATIONAL RISK MANAGEMENT TOOLS Risk and Control Self- Assessment Loss event Database Scenario Modeling &

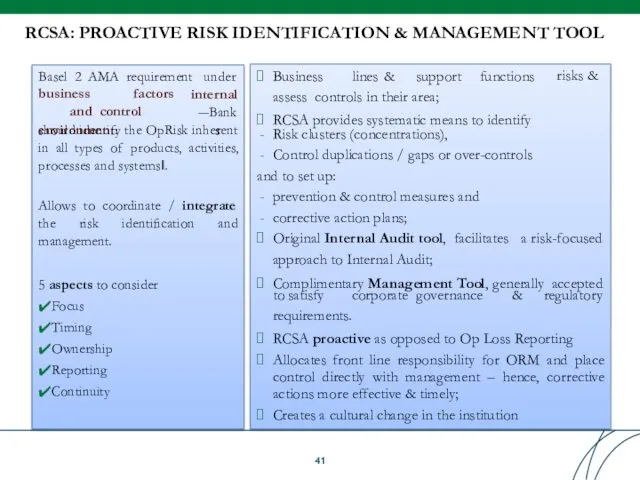

- 41. RCSA: PROACTIVE RISK IDENTIFICATION & MANAGEMENT TOOL risks & Business lines & support functions assess controls

- 42. RCSA AIMS Establish a contact with risk owners Qualitative risk assessment Get details on typical risk

- 43. RCSA MILESTONES Corrective Action Plans / Risk Mitigation Plans (RMPs) Exterminate weak areas in prevention &

- 44. RCSA WORKFLOW Define the implementation mode / Document the process Update KRIs, adjust scenario analysis, enhance

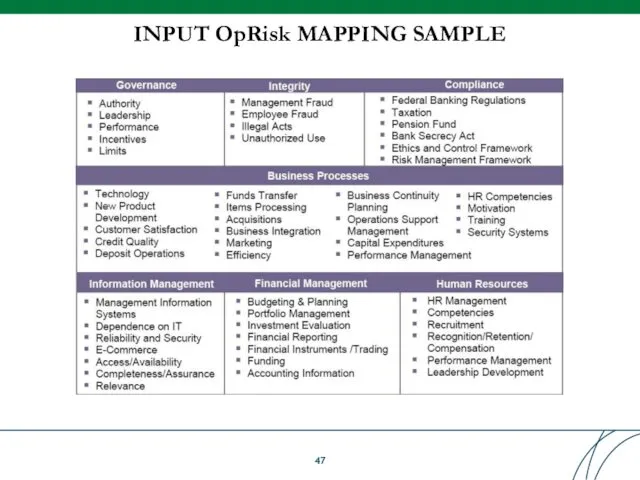

- 45. RCSA TOOLKIT-3: OpRisk MAPPING Risk register (also for output) High level business process (e.g. HR Mngt)

- 47. INPUT OpRisk MAPPING SAMPLE

- 48. MANAGEMENT RESULTS REPORTIG TOOLS Unless RCSA results are relevant for management decision making, the exercise is

- 49. OUTPUT RISK SCORECARD

- 50. HEAT MAPPING facilitates the assessment of the likelihood and impact of the risk materializing; Can also

- 51. OPERATIONAL FREQUENCY – SEVERITY RISK MAPPING Card fraud Frequency Severity High Low Low High Unauthorized access

- 52. RCSA FOLLOW UP RCSA results ought to be used in conjunction with other components of ORM

- 53. Table of Contents

- 54. Basel Committee on Banking Supervision Principles for the Sound Management of Operational Risk, June 2011 Indicators

- 55. Indicators Approach allows to track operational risk profile and monitor risk exposure with series of quantitative

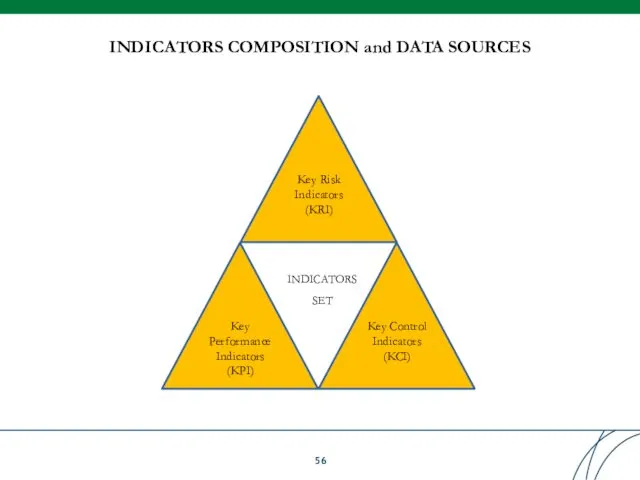

- 56. INDICATORS COMPOSITION and DATA SOURCES Key Risk Indicators (KRI) Key Performance Indicators (KPI) Key Control Indicators

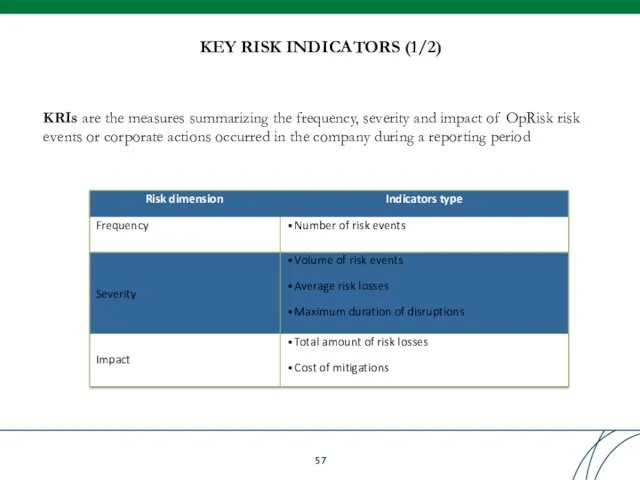

- 57. KRIs are the measures summarizing the frequency, severity and impact of OpRisk risk events or corporate

- 58. KEY RISK INDICATORS (2/2)

- 59. KPIs are the measures that evaluate scale of banking activities. According to many empirical observations that

- 60. KCIs are the measures that enables to monitor effectiveness of OpRisk management procedures established in the

- 61. DATA SOURCES Key Risk Indicators (KRI) Key Performance Indicators (KPI) Key Control Indicators (KCI) INDICATORS SET

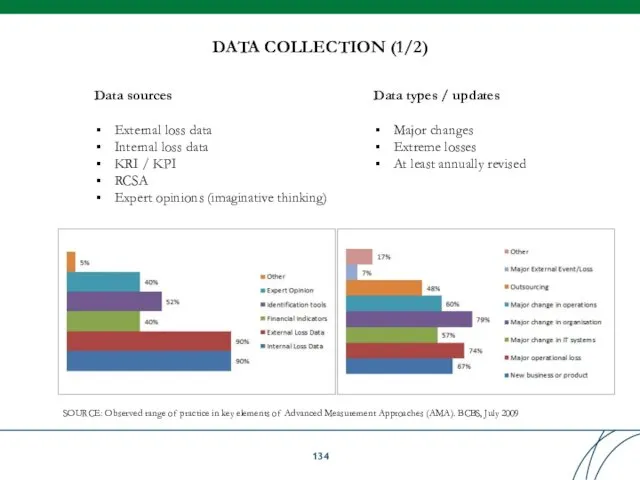

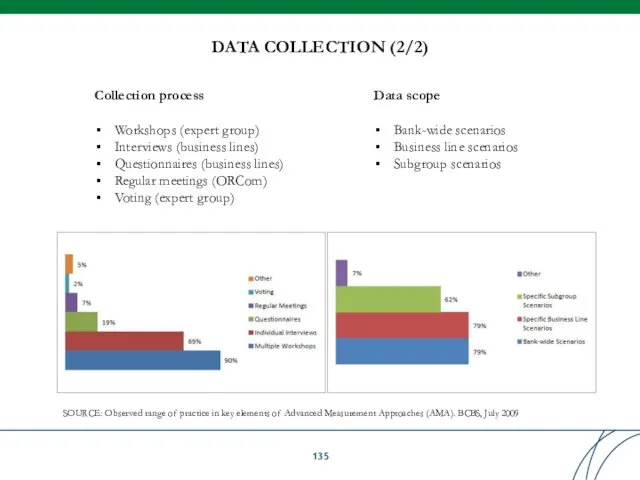

- 62. DATA COLLECTION FREQUENCY SOURCE: Observed range of practice in key elements of Advanced Measurement Approaches (AMA).

- 63. DATA BREAKDOWNS Upright Peers All bank Headquarter Branch network DATA ANALYSIS (1/2) Horizontal Business lines Departments

- 64. DATA ANALYSIS (2/2) Trend analysis Retrospective Business plan Regressions Peers KPI comparison Thresholds Control Peers line

- 65. REPORTING MATRIX

- 66. DECISION MAKING MATRIX

- 67. Table of Contents

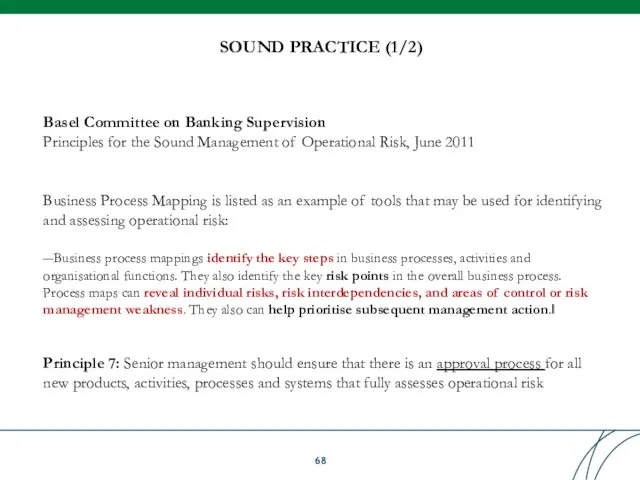

- 68. Basel Committee on Banking Supervision Principles for the Sound Management of Operational Risk, June 2011 Business

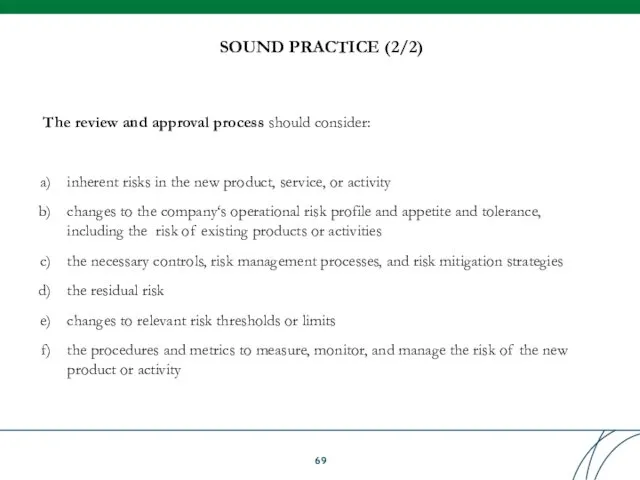

- 69. The review and approval process should consider: inherent risks in the new product, service, or activity

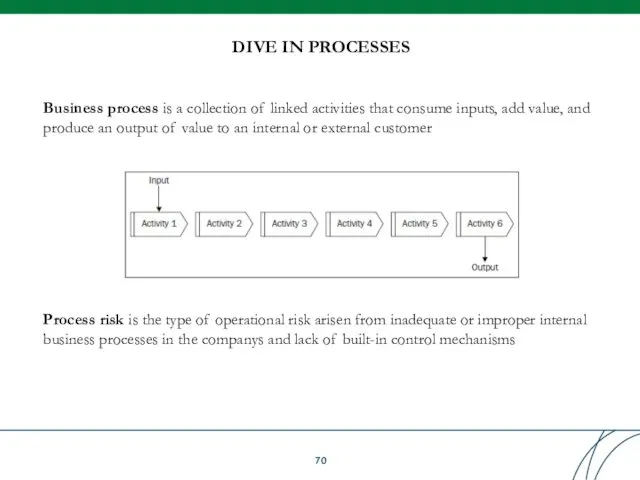

- 70. Business process is a collection of linked activities that consume inputs, add value, and produce an

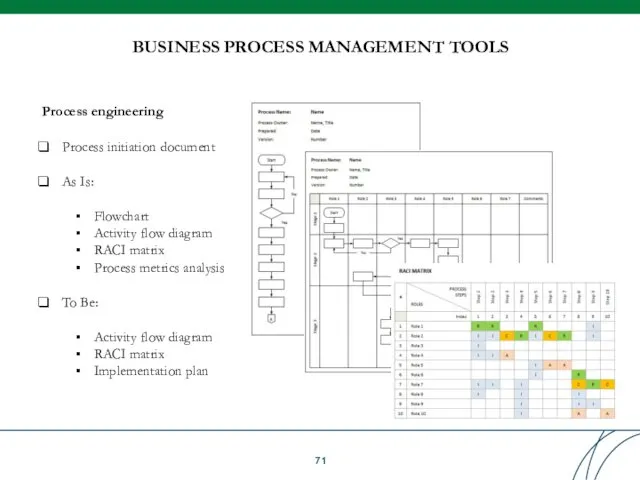

- 71. BUSINESS PROCESS MANAGEMENT TOOLS Process engineering Process initiation document As Is: Flowchart Activity flow diagram RACI

- 72. HOW RISK MANAGEMENT SIGN OFF THE PROCESS? PROCESS BENEFICIERY BUSINESS DEVELOPMENT ENDORSING DEPARTMENTS RISK MANAGEMENT Risk

- 73. Process risk map is composed and monitored by Risk management on the basis of key workflows

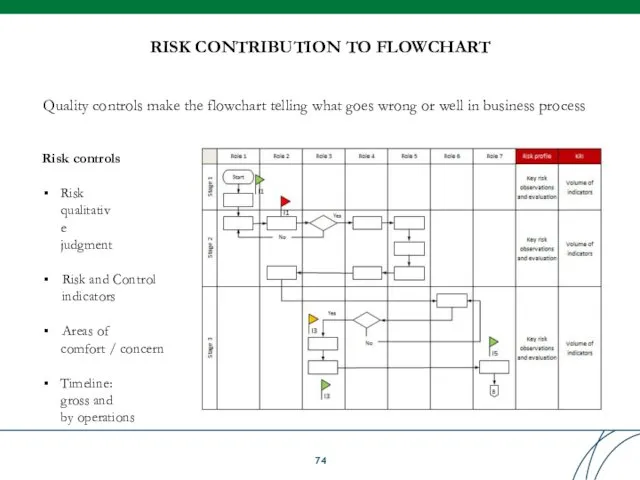

- 74. RISK CONTRIBUTION TO FLOWCHART Quality controls make the flowchart telling what goes wrong or well in

- 75. Table of Contents

- 76. Table of Contents

- 77. Basel Committee on Banking Supervision Principles for the Sound Management of Operational Risk, June 2011 Loss

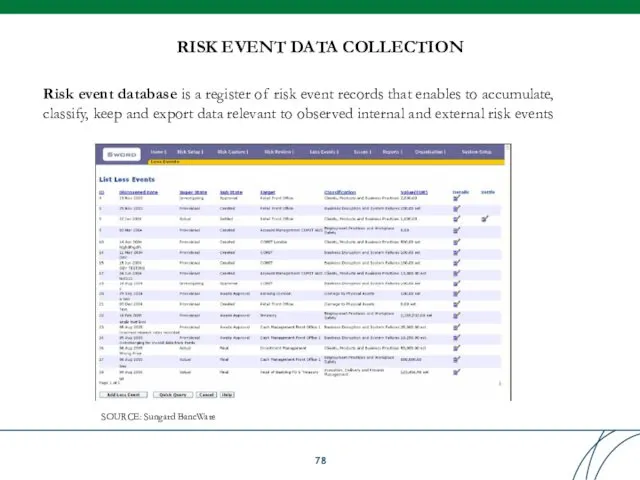

- 78. Risk event database is a register of risk event records that enables to accumulate, classify, keep

- 79. WHY COLLECT DATA? RISK EVENT DATABASE Immediate Actions Advanced Measurement Approach (AMA) 1 2 Risk Reporting

- 80. DATABASE DEVELOPMENT 1. Classify business lines, risk, loss types 2. Define risk event data and data

- 81. DATABASE CLASSIFICATORS (1/2) Business Areas Corporate Finance Trading & Sales Retail Banking Commercial Banking Payment and

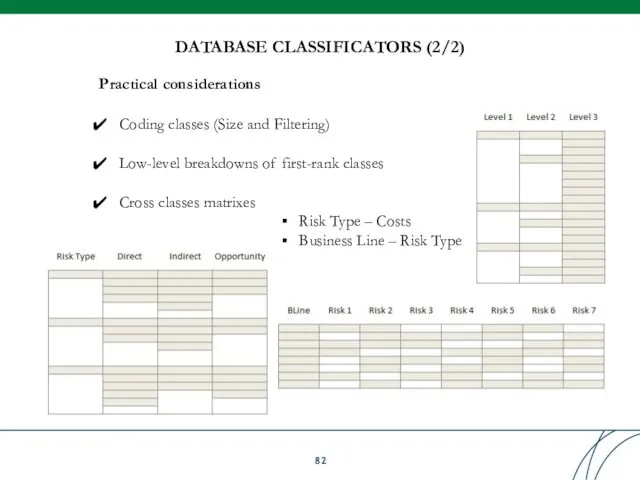

- 82. DATABASE CLASSIFICATORS (2/2) Practical considerations Coding classes (Size and Filtering) Low-level breakdowns of first-rank classes Cross

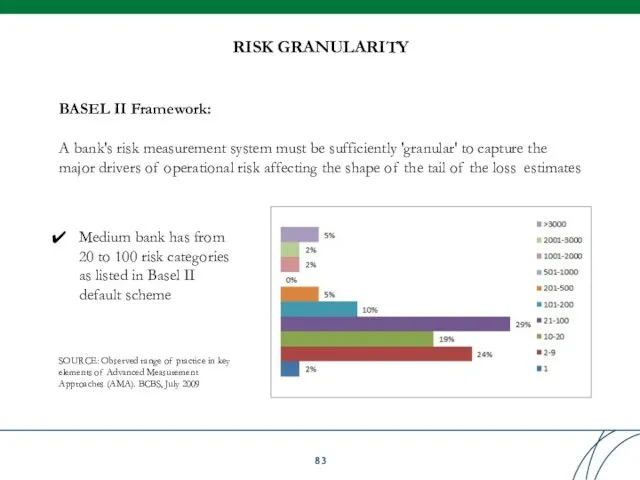

- 83. RISK GRANULARITY BASEL II Framework: A bank's risk measurement system must be sufficiently 'granular' to capture

- 84. WHAT DATA ARE ESSENTIAL TO COLLECT? • Risk Coordinator • Observer • Actions taken • Actions

- 85. DATABASE FUNCTIONAL MAP Data Upload Database Report confi- gurator Reports Data contributors Risk owners Audit reports

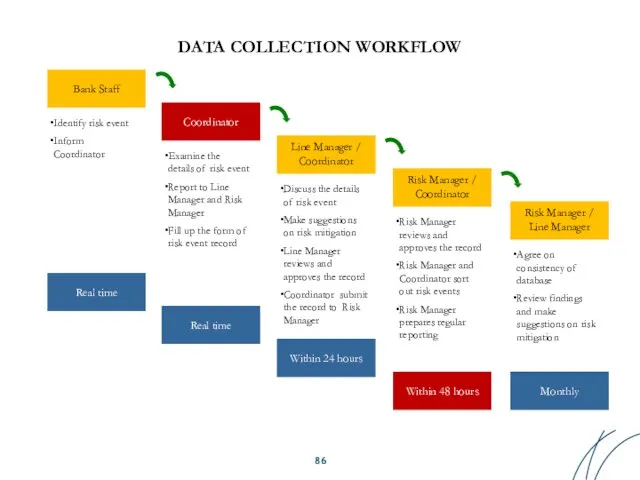

- 86. Bank Staff Coordinator Identify risk event Inform Coordinator Examine the details of risk event Report to

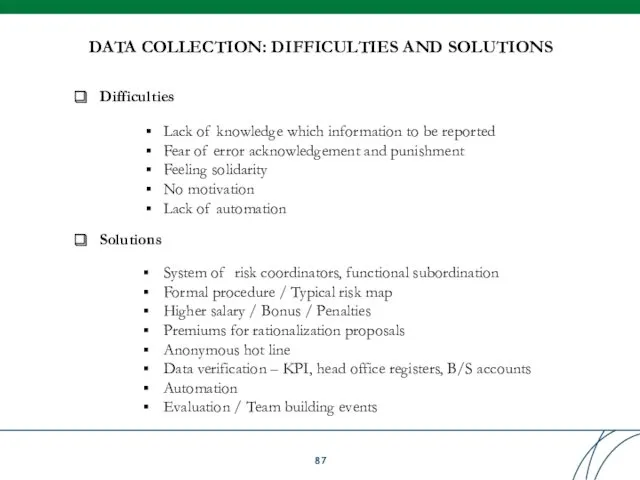

- 87. DATA COLLECTION: DIFFICULTIES AND SOLUTIONS Difficulties Lack of knowledge which information to be reported Fear of

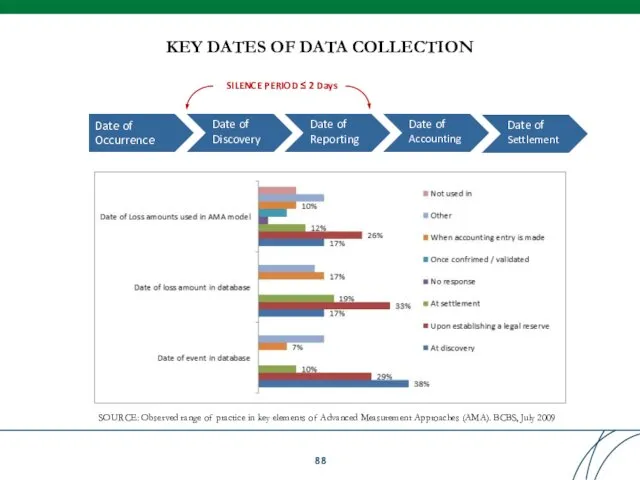

- 88. KEY DATES OF DATA COLLECTION SOURCE: Observed range of practice in key elements of Advanced Measurement

- 89. SPECIFIC EVENT TYPES (1/3) SOURCE: Operational Risk Reporting Standards. ORX, Edition 2011 OpRisk event is an

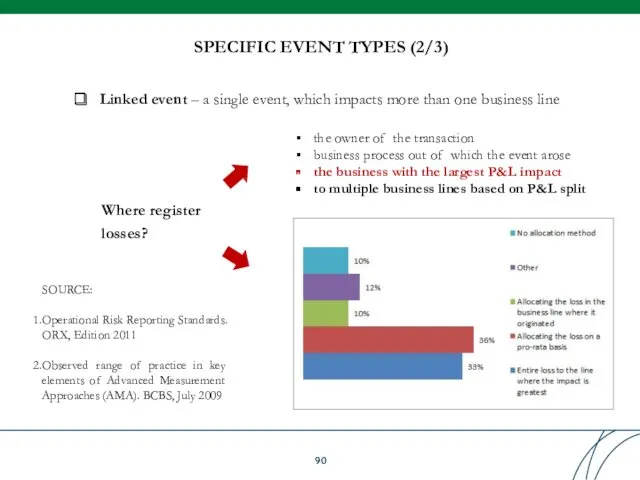

- 90. SPECIFIC EVENT TYPES (2/3) SOURCE: Operational Risk Reporting Standards. ORX, Edition 2011 Observed range of practice

- 91. SPECIFIC EVENT TYPES (3/3) Near-misses – operational risk events that did not lead to a loss,

- 92. SPECIFIC LOSS TYPES (1/2) SOURCE: Operational Risk Reporting Standards. ORX, Edition 2011 OpRisk loss – a

- 93. SPECIFIC LOSS TYPES (2/2) SOURCE: Operational Risk Reporting Standards. ORX, Edition 2011 Risk event type: Amount

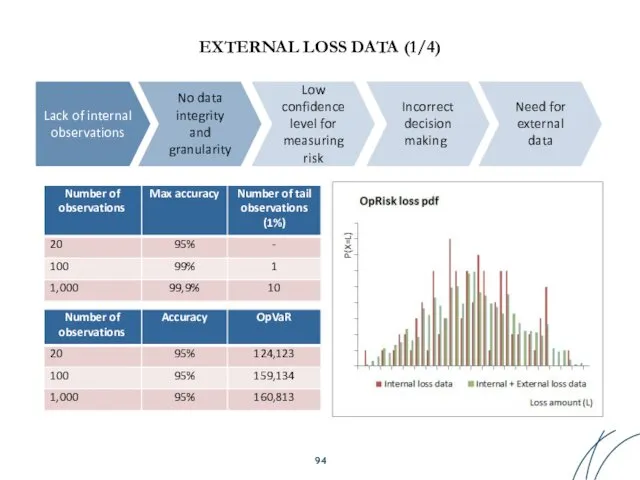

- 94. EXTERNAL LOSS DATA (1/4) Lack of internal observations No data integrity and granularity Low confidence level

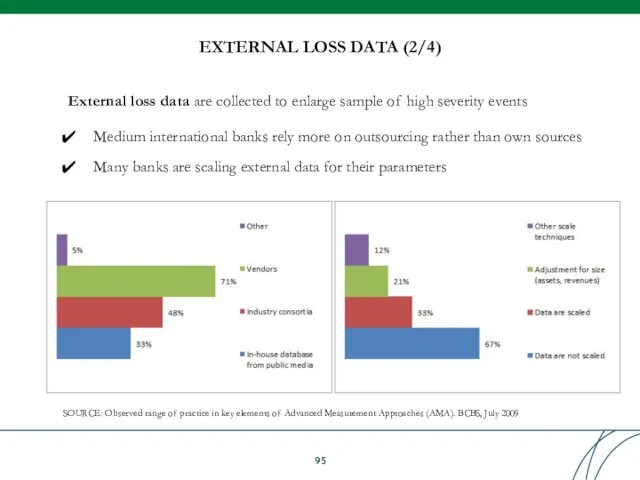

- 95. EXTERNAL LOSS DATA (2/4) SOURCE: Observed range of practice in key elements of Advanced Measurement Approaches

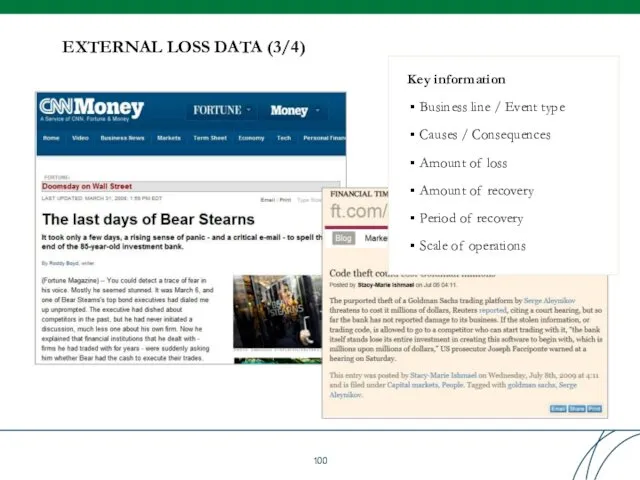

- 96. EXTERNAL LOSS DATA (3/4) Key information Business line / Event type Causes / Consequences Amount of

- 97. QUIZ: EXTERNAL LOSS DATA – local examples Internal fraud External fraud Reputational risk Products and processes

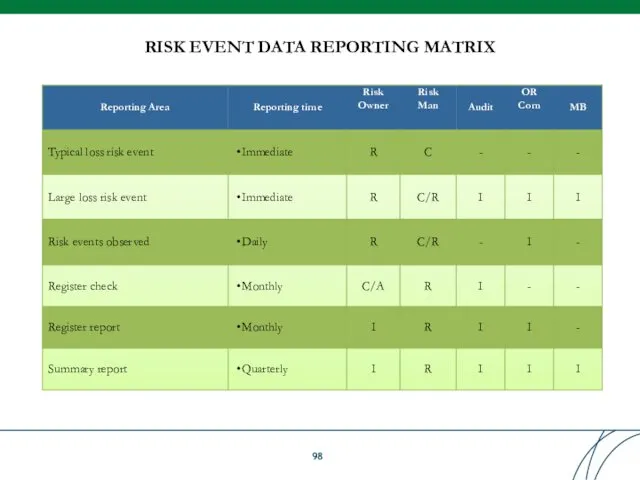

- 98. RISK EVENT DATA REPORTING MATRIX

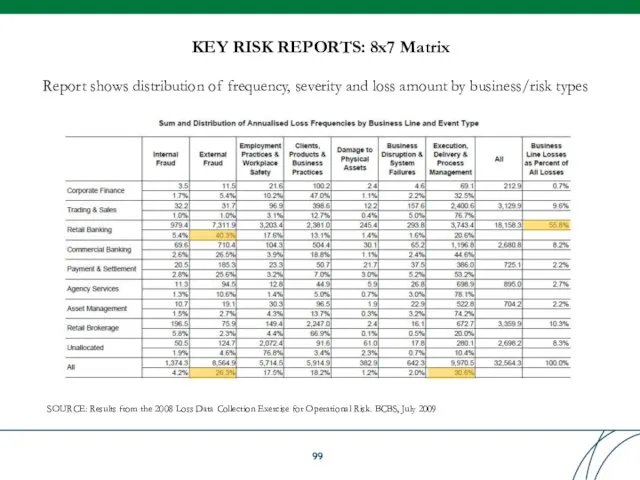

- 99. KEY RISK REPORTS: 8x7 Matrix SOURCE: Results from the 2008 Loss Data Collection Exercise for Operational

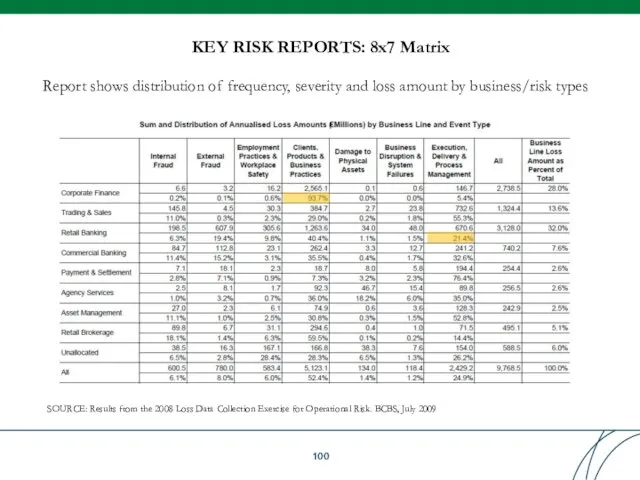

- 100. KEY RISK REPORTS: 8x7 Matrix SOURCE: Results from the 2008 Loss Data Collection Exercise for Operational

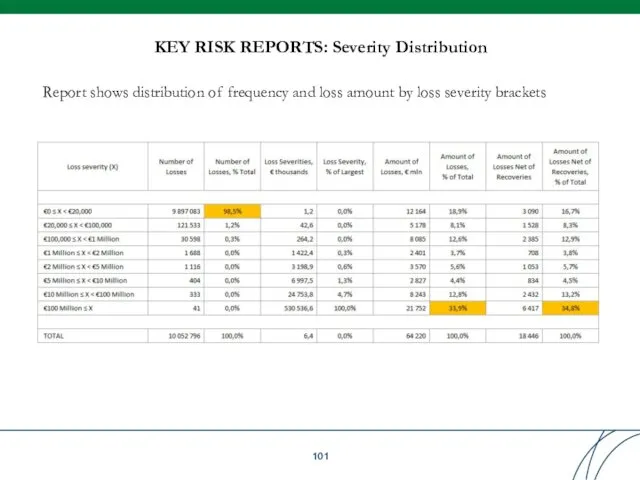

- 101. KEY RISK REPORTS: Severity Distribution Report shows distribution of frequency and loss amount by loss severity

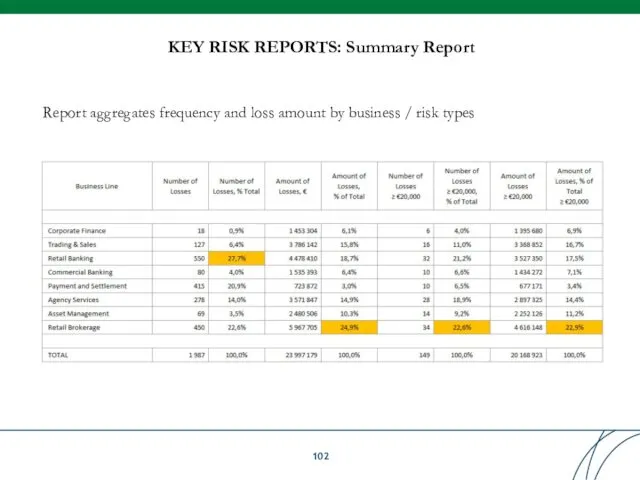

- 102. KEY RISK REPORTS: Summary Report Report aggregates frequency and loss amount by business / risk types

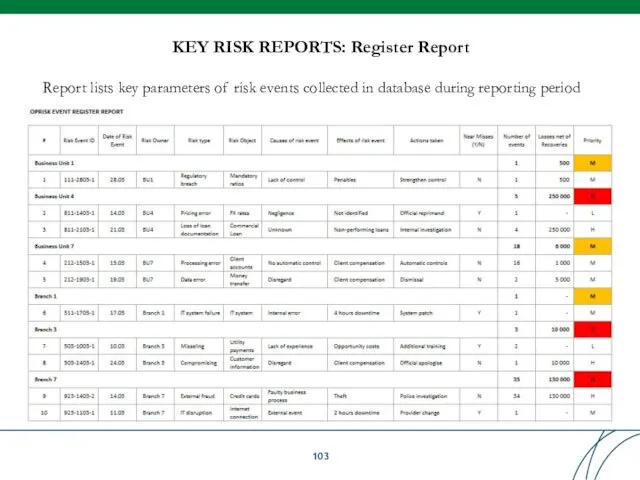

- 103. KEY RISK REPORTS: Register Report Report lists key parameters of risk events collected in database during

- 104. DATABASE SET INCLUDES: Classifications matrixes Data structure Reporting templates Workflow guidelines Job descriptions of key involved

- 105. Table of Contents

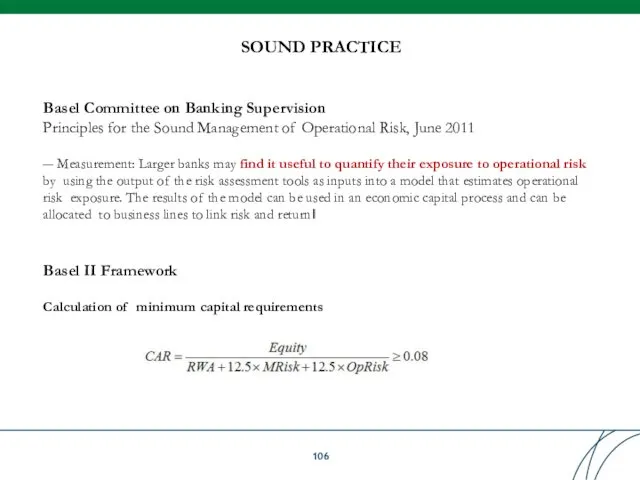

- 106. Basel Committee on Banking Supervision Principles for the Sound Management of Operational Risk, June 2011 ―

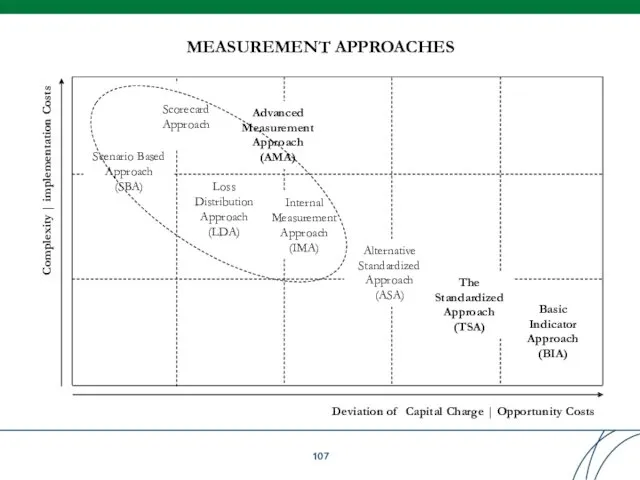

- 107. MEASUREMENT APPROACHES Deviation of Capital Charge | Opportunity Costs Complexity | implementation Costs Basic Indicator Approach

- 108. SELECTION CRITERIA Complexity or intensity of banking operations Meeting qualitative standards Partial use Restriction to revert

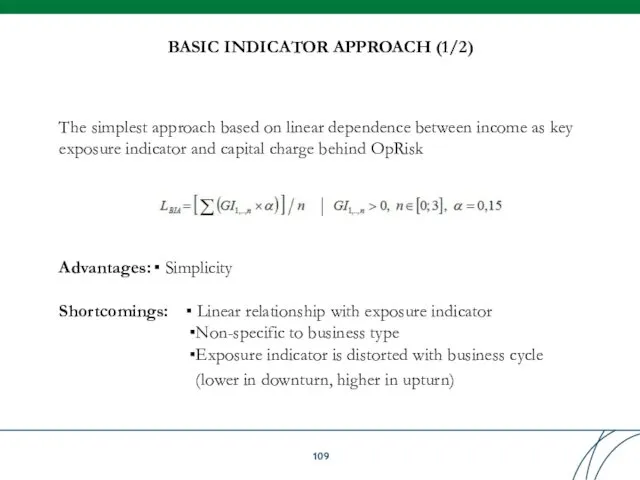

- 109. BASIC INDICATOR APPROACH (1/2) The simplest approach based on linear dependence between income as key exposure

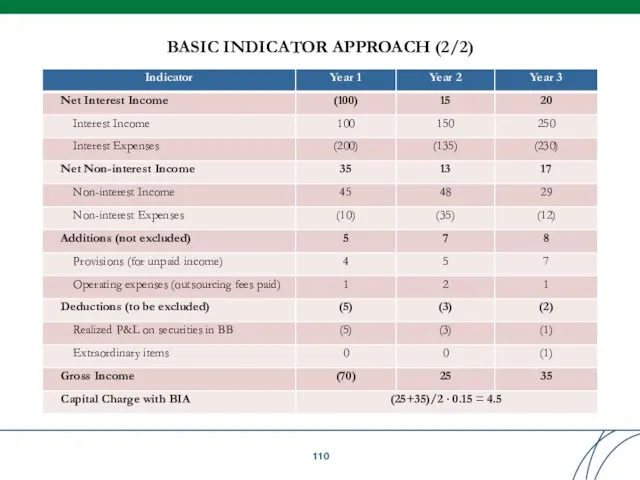

- 110. BASIC INDICATOR APPROACH (2/2)

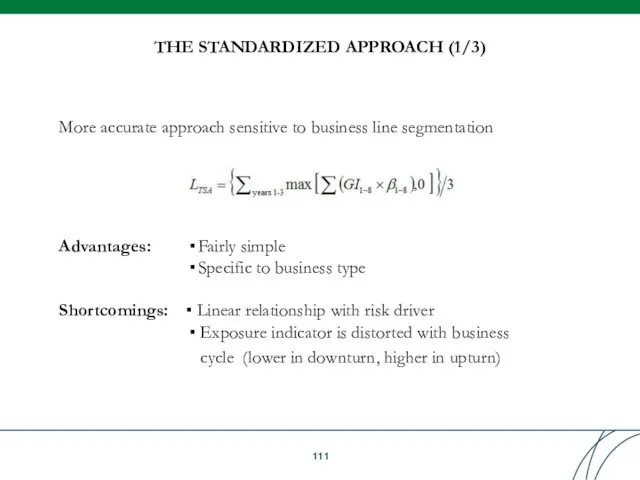

- 111. THE STANDARDIZED APPROACH (1/3) More accurate approach sensitive to business line segmentation Advantages: Fairly simple Specific

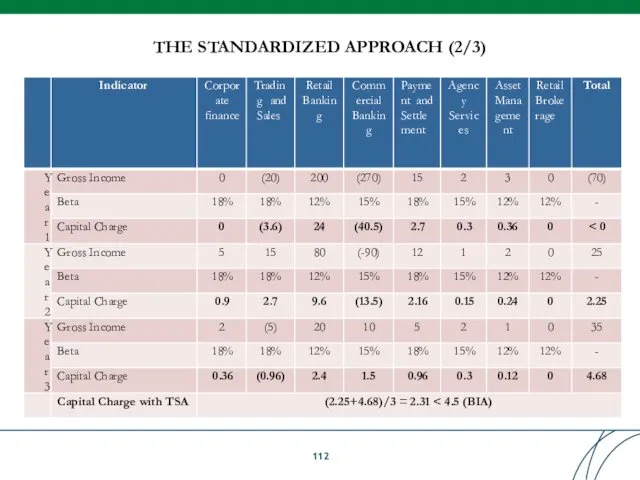

- 112. THE STANDARDIZED APPROACH (2/3)

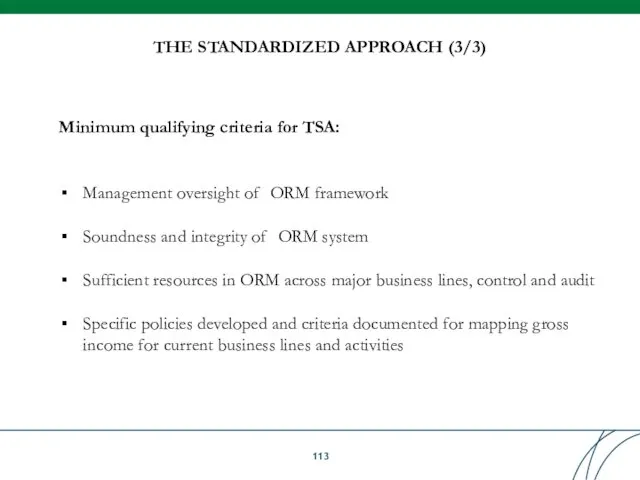

- 113. THE STANDARDIZED APPROACH (3/3) Minimum qualifying criteria for TSA: Management oversight of ORM framework Soundness and

- 114. ALTERNATIVE STANDARDIZED APPROACH (1/3) A modification to TSA encompassing volume exposure indicator Advantages: Fairly simple Specific

- 115. ALTERNATIVE STANDARDIZED APPROACH (2/3)

- 116. ALTERNATIVE STANDARDIZED APPROACH (3/3)

- 117. ADVANCED MEASUREMENT APPROACHES (1/3) Capital Charge with AMA Stress Losses VaR (L) E(L) Allowances Risk capital

- 118. Qualifying standards: Meeting minimum qualifying criteria used for TSA Having independent full-fledged ORM function ORM is

- 119. Quantitative standards: Capture potentially severe ‗tail‘ loss events at one year holding period and a 99.9th

- 120. INTERNAL MEASUREMENT APPROACH (1/2) Approach based on linear proxy between expected and unexpected losses Parameters γ

- 121. INTERNAL MEASUREMENT APPROACH (2/2) Advantages Flexibility of exposure indicators Specific to business type Dependent on internal

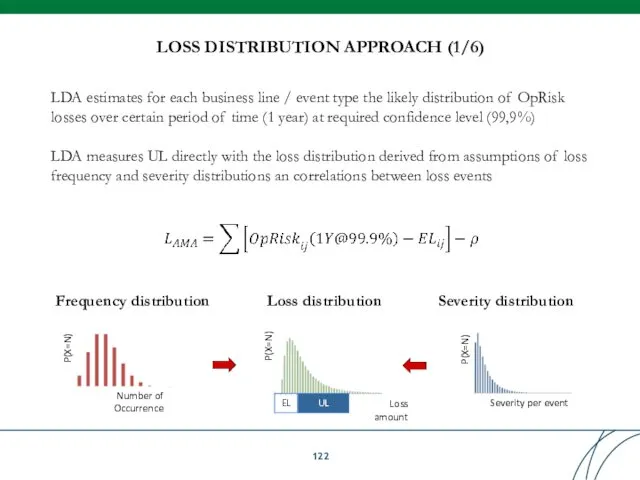

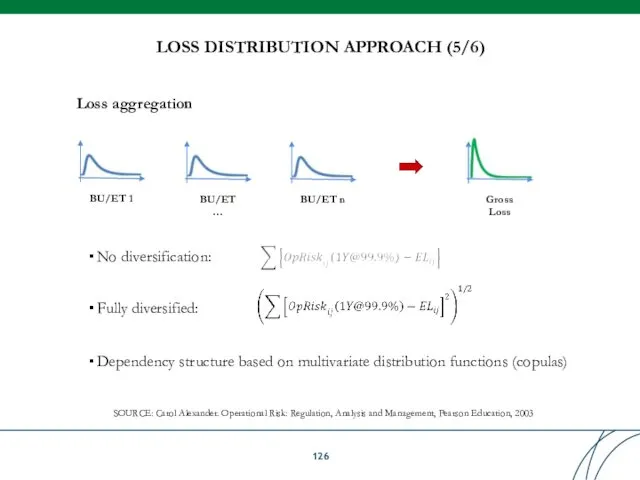

- 122. LOSS DISTRIBUTION APPROACH (1/6) LDA estimates for each business line / event type the likely distribution

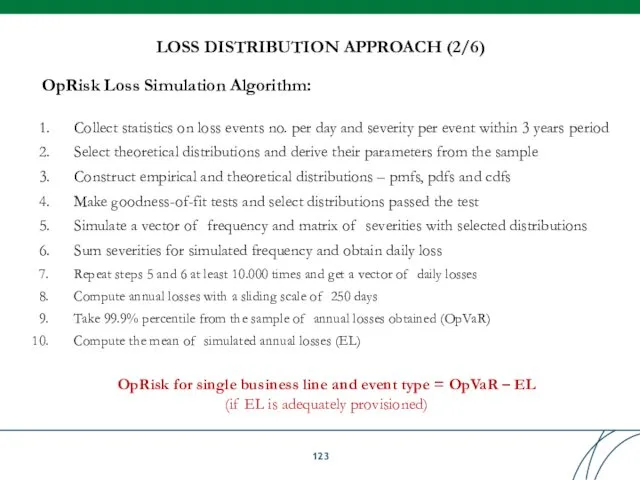

- 123. LOSS DISTRIBUTION APPROACH (2/6) OpRisk Loss Simulation Algorithm: Collect statistics on loss events no. per day

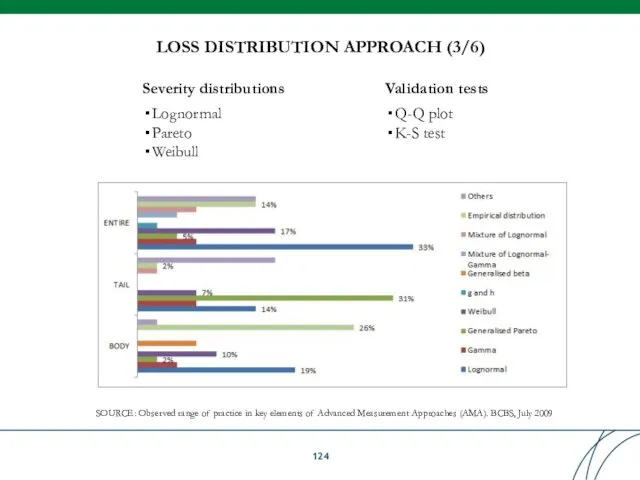

- 124. LOSS DISTRIBUTION APPROACH (3/6) Severity distributions Lognormal Pareto Weibull Validation tests Q-Q plot K-S test SOURCE:

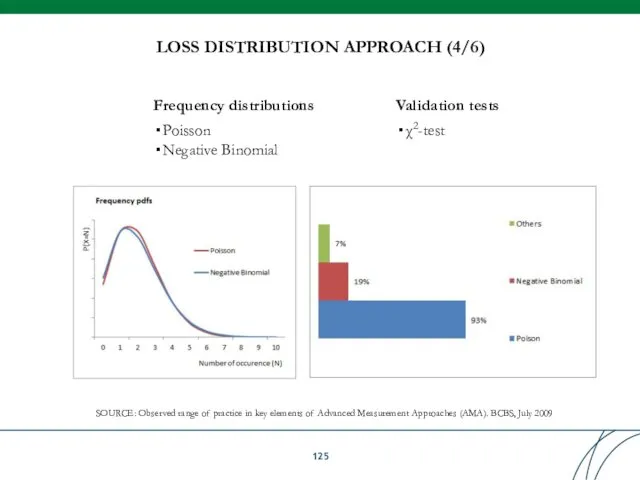

- 125. LOSS DISTRIBUTION APPROACH (4/6) Frequency distributions Poisson Negative Binomial Validation tests χ2-test SOURCE: Observed range of

- 126. LOSS DISTRIBUTION APPROACH (5/6) Loss aggregation BU/ET 1 BU/ET n BU/ET … Gross Loss SOURCE: Carol

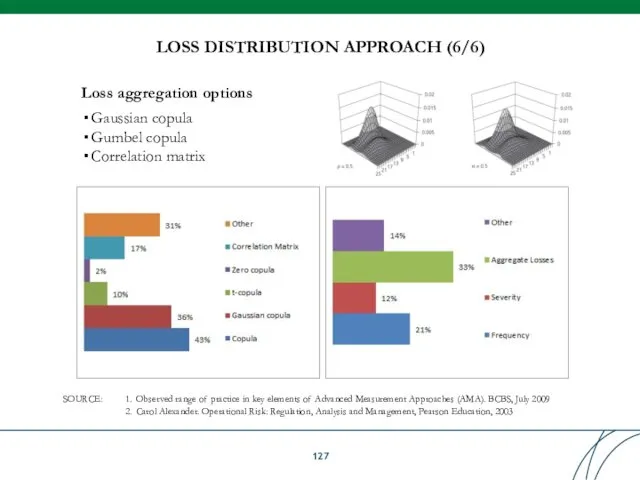

- 127. LOSS DISTRIBUTION APPROACH (6/6) SOURCE: Observed range of practice in key elements of Advanced Measurement Approaches

- 128. Table of Contents

- 129. Basel Committee on Banking Supervision > Principles for the Sound Management of Operational Risk, June 2011

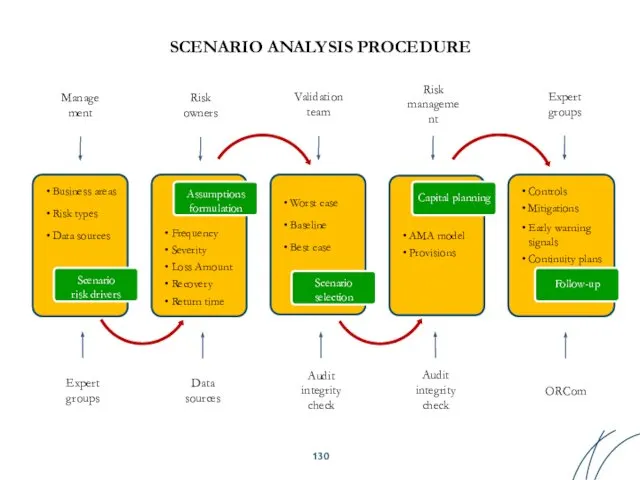

- 130. Business areas Risk types Data sources Scenario risk drivers Frequency Severity Loss Amount Recovery Return time

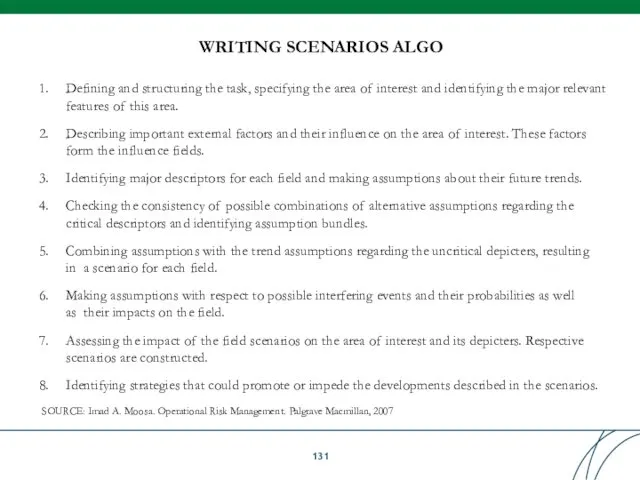

- 131. WRITING SCENARIOS ALGO Defining and structuring the task, specifying the area of interest and identifying the

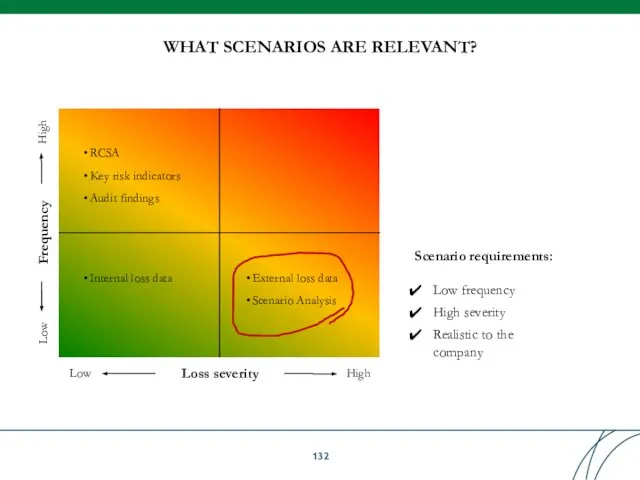

- 132. WHAT SCENARIOS ARE RELEVANT? Frequency Loss severity High Low High Low RCSA Key risk indicators Audit

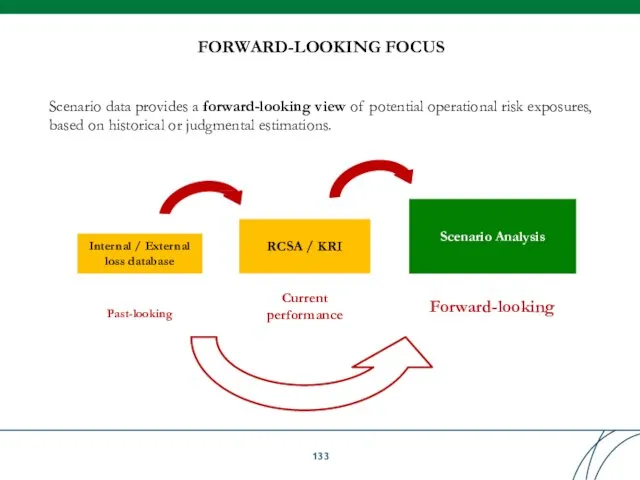

- 133. FORWARD-LOOKING FOCUS Internal / External loss database Past-looking RCSA / KRI Current performance Scenario Analysis Forward-looking

- 134. SOURCE: Observed range of practice in key elements of Advanced Measurement Approaches (AMA). BCBS, July 2009

- 135. SOURCE: Observed range of practice in key elements of Advanced Measurement Approaches (AMA). BCBS, July 2009

- 136. SCENARIO RISK DRIVERS RCSA may help to identify the business lines and event types of high

- 137. SCENARIO DISTRIBUTION SOURCE: Results from the 2008 Loss Data Collection Exercise for Operational Risk. BCBS, July

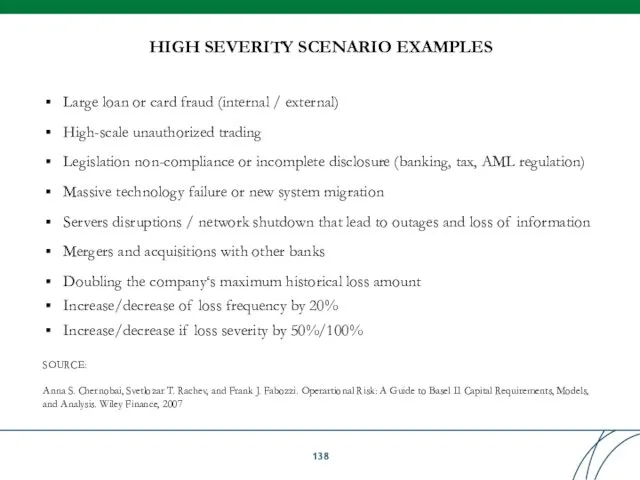

- 138. HIGH SEVERITY SCENARIO EXAMPLES Large loan or card fraud (internal / external) High-scale unauthorized trading Legislation

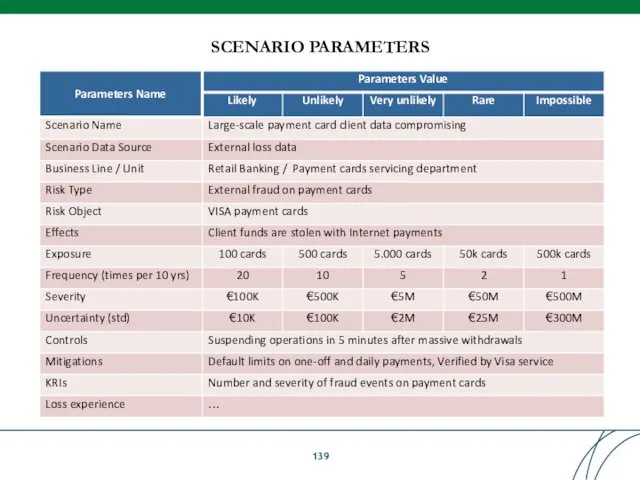

- 139. SCENARIO PARAMETERS

- 140. QUANTIFICATION USE Scenario estimates should add high frequency, but low severity internal loss data Scenarios account

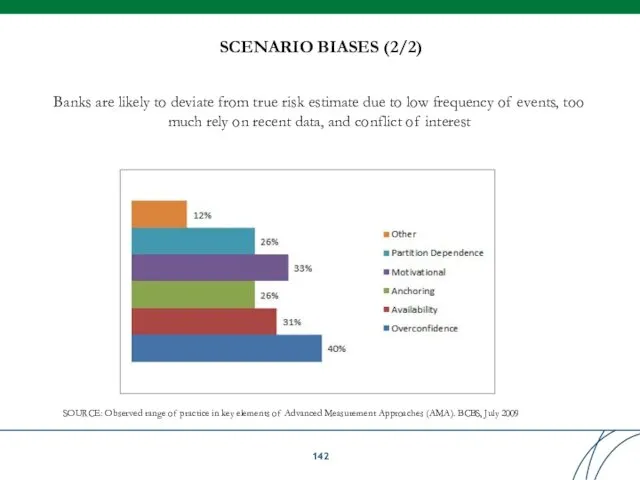

- 141. Overconfidence: underestimation of risk due to the number of observed events being small Availability: overestimation of

- 142. Banks are likely to deviate from true risk estimate due to low frequency of events, too

- 143. Established scenario framework should ensure the integrity and consistency of the estimates produced with the following

- 144. Table of Contents

- 145. Table of Contents

- 146. RISK TAKING & MANAGEMENT OPTIONS Profit>Ri sk Cost =>Perform activity => OpRisk taking Profit => abandon

- 147. Processes People Systems External events OP RISK MITIGATION Mitigate Cause s Risk managem ent options

- 148. BSBC PRINCIPLE 10: BUSINESS RESILIENCY AND CONTINUITY PLANNING BC-Plans shall take into account different types of

- 149. BUSINESS CONTINUITY PLANNING BCP = disaster prevention & disaster recovery planning. Disaster prevention aims to reduce

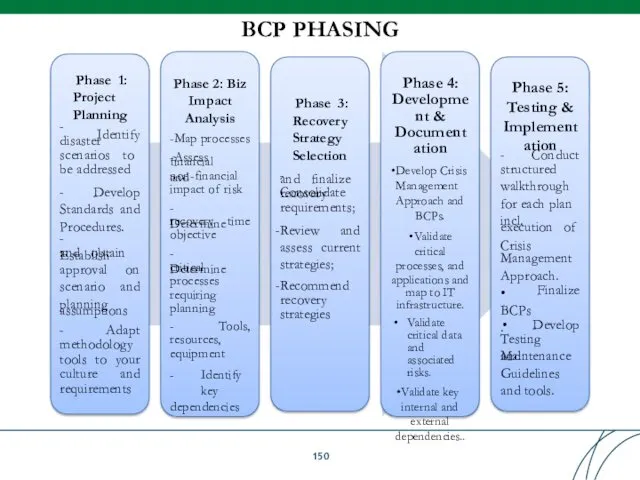

- 150. BCP PHASING - Phase 1: Project Planning Identify disaster scenarios to be addressed - Develop Standards

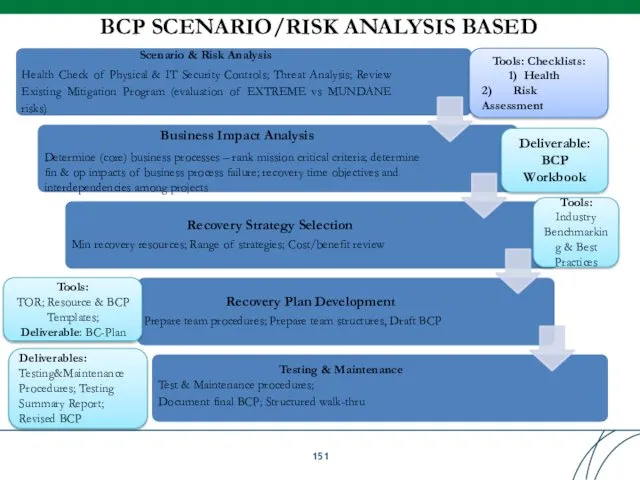

- 151. BCP SCENARIO/RISK ANALYSIS BASED Scenario & Risk Analysis Health Check of Physical & IT Security Controls;

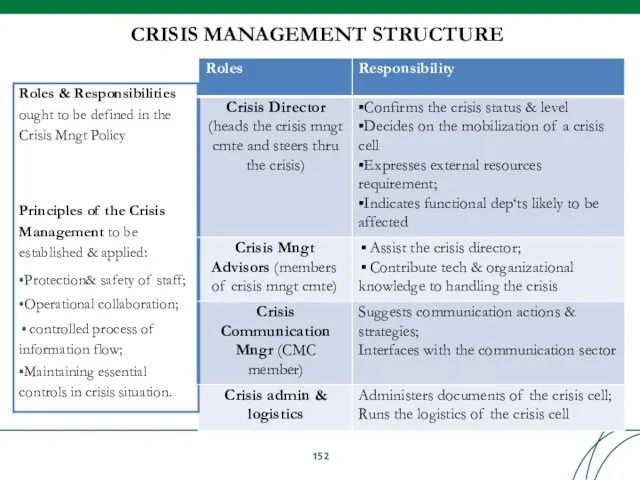

- 152. CRISIS MANAGEMENT STRUCTURE

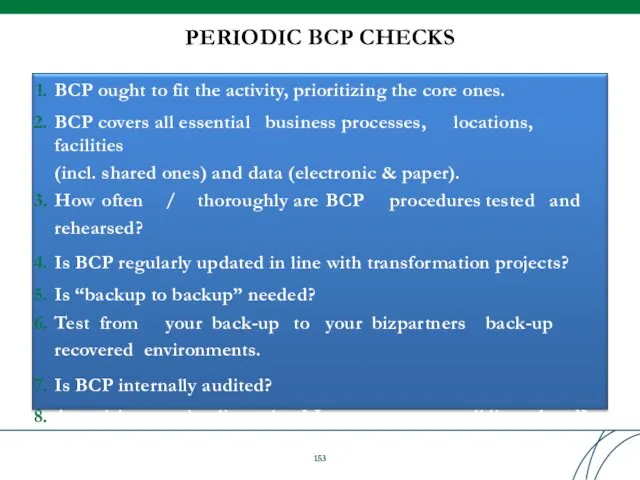

- 153. PERIODIC BCP CHECKS BCP ought to fit the activity, prioritizing the core ones. BCP covers all

- 154. BCP TIPS Simple preventive measures – geographic dispersion of intellectual capital; Implement alternative IT solutions for

- 155. Processes People Systems External events Insure X E.g.: Vault transport of cash X Bankers professional indemnity

- 156. INSURANCE Conditions: Must be related to actual risk exposure of bank to evidence need for mitigation,

- 157. INSURANCE MITIGATION UNDER AMA

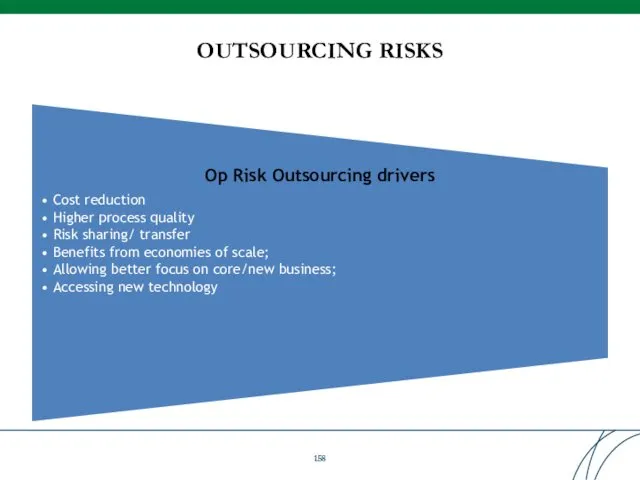

- 158. OUTSOURCING RISKS Op Risk Outsourcing drivers Cost reduction Higher process quality Risk sharing/ transfer Benefits from

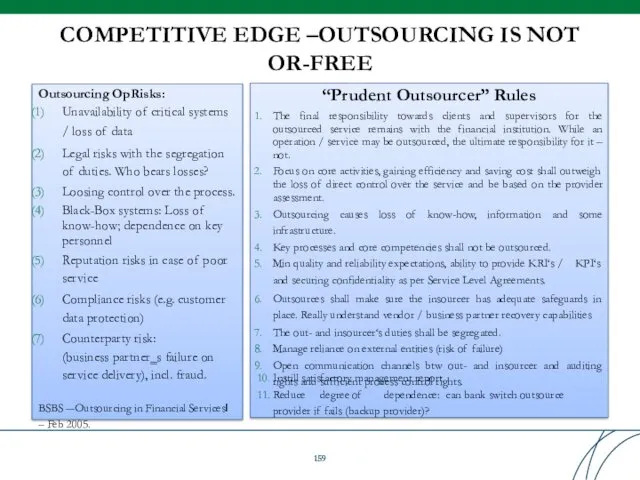

- 159. COMPETITIVE EDGE –OUTSOURCING IS NOT OR-FREE “Prudent Outsourcer” Rules The final responsibility towards clients and supervisors

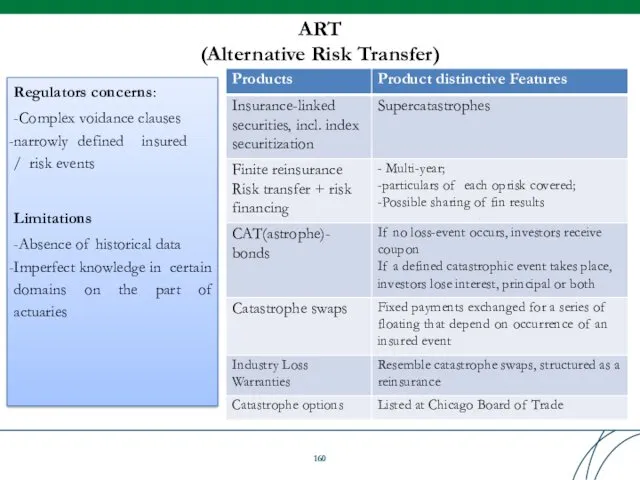

- 160. ART (Alternative Risk Transfer) Regulators concerns: -Complex voidance clauses narrowly defined insured / risk events Limitations

- 161. Table of Contents

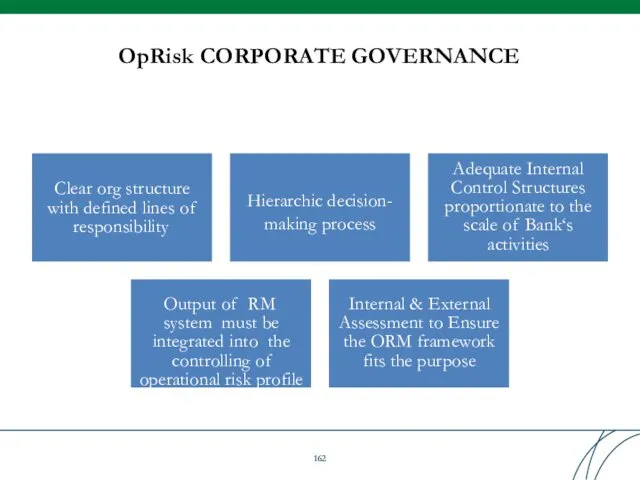

- 162. OpRisk CORPORATE GOVERNANCE Clear org structure with defined lines of responsibility Hierarchic decision- making process Adequate

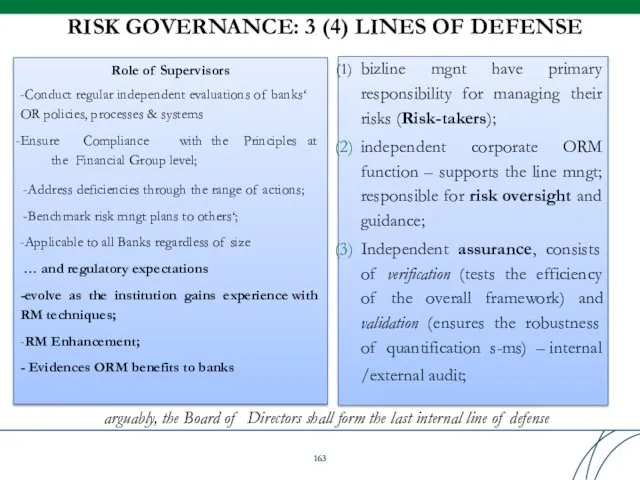

- 163. RISK GOVERNANCE: 3 (4) LINES OF DEFENSE Role of Supervisors -Conduct regular independent evaluations of banks‘

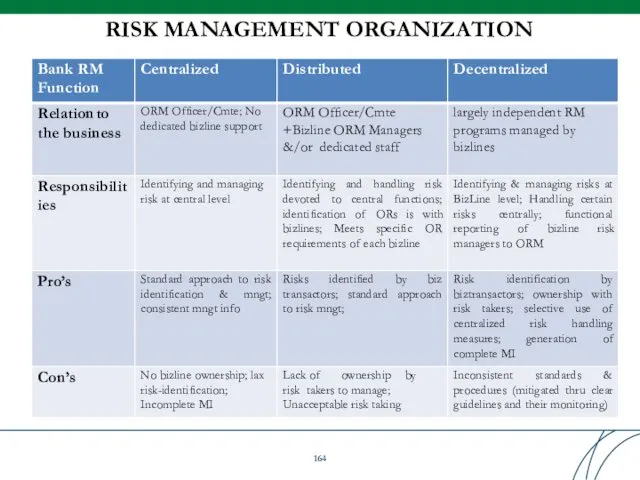

- 164. RISK MANAGEMENT ORGANIZATION

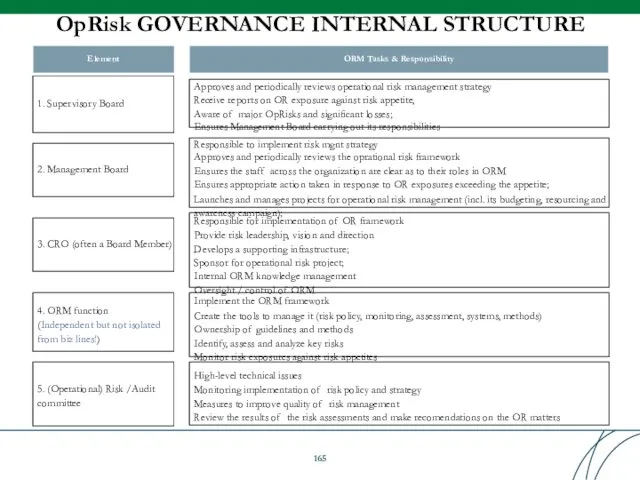

- 165. OpRisk GOVERNANCE INTERNAL STRUCTURE 1. Supervisory Board Responsible to implement risk mgnt strategy Approves and periodically

- 166. OpRisk Governance Support Element ORM Tasks & Responsibility

- 167. SPECIAL ROLE OF RISK FUNCTION Policy Monitoring Assessment Systems Methodology Other (optional) Develop, adapt & maintain

- 168. RISK GOVERNANCE ELEMENTS

- 169. ORM GOVERNANCE FRAMEWORK Evolving Governance Model: (1)a central OpRisk Mngr reporting to the CRO. The role

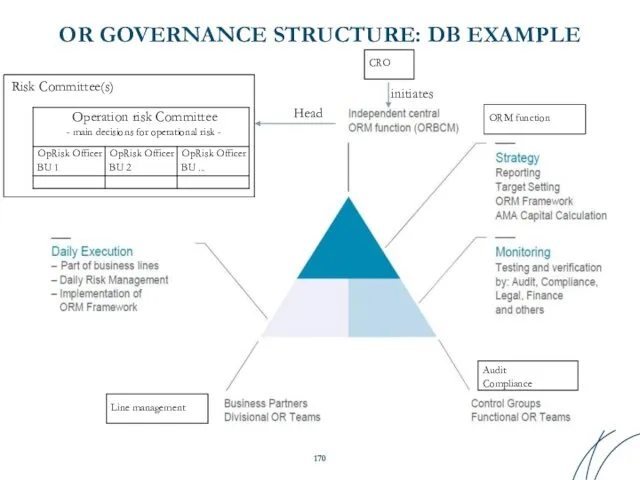

- 170. OR GOVERNANCE STRUCTURE: DB EXAMPLE Head Risk Committee(s) initiates Line management ORM function Audit Compliance CRO

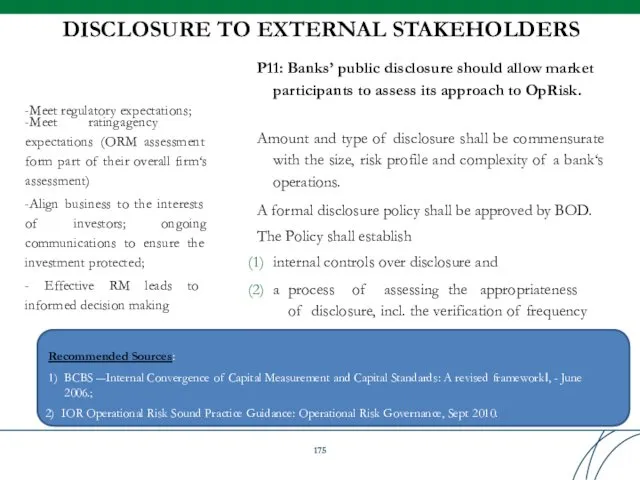

- 171. DISCLOSURE TO EXTERNAL STAKEHOLDERS -Meet rating agency expectations (ORM assessment form part of their overall firm‘s

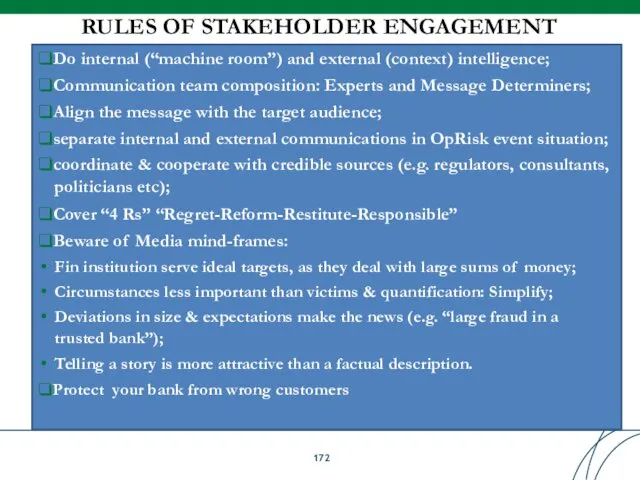

- 172. RULES OF STAKEHOLDER ENGAGEMENT ❑Do internal (“machine room”) and external (context) intelligence; ❑Communication team composition: Experts

- 173. - Who are your stakeholders? -What’s your Symbol (Brand, Reputation)? - Is it worth protecting?

- 174. BENEFITS OF OR GOVERNANCE ✔ Reduction of operational losses; ✔ Improved business and performance management; ✔Protection

- 175. ORM IS SIMPLY GOOD CORPORATE GOVERNANCE Good ORM Fewer Surprises Increased shareholder value

- 176. Table of Contents

- 177. Contact information INTERNATIONAL FINANCE CORPORATION (IFC) Bank Advisory Program Central Asia and Eastern Europe Yevgeni Prokopenko,

- 179. Скачать презентацию

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

OpRisk IS AN ENTERPRISE-WIDE RISK

OR has been managed already before it

OpRisk IS AN ENTERPRISE-WIDE RISK

OR has been managed already before it

RECENT OUTSTANDING OPERATIONAL LOSSES

BARINGS PLC – 1995, USD 1.3 Bln –

RECENT OUTSTANDING OPERATIONAL LOSSES

BARINGS PLC – 1995, USD 1.3 Bln –

ISO Standards:

31100 – Enterprise Risk Management;

27900 – Information Security

FERMA (Federation of

ISO Standards:

31100 – Enterprise Risk Management;

27900 – Information Security

FERMA (Federation of

INTERNATIONAL REGULATORY PERCEPTION OF the companyING OR

Supervisors „discovered― OR as separate

INTERNATIONAL REGULATORY PERCEPTION OF the companyING OR

Supervisors „discovered― OR as separate

DEFINE OpRisk PRIOR TO MEASURING IT

„Wide“

„Narrow“

(Basel 2, §644, R.Morris Ass.)

Risk of

DEFINE OpRisk PRIOR TO MEASURING IT

„Wide“

„Narrow“

(Basel 2, §644, R.Morris Ass.)

Risk of

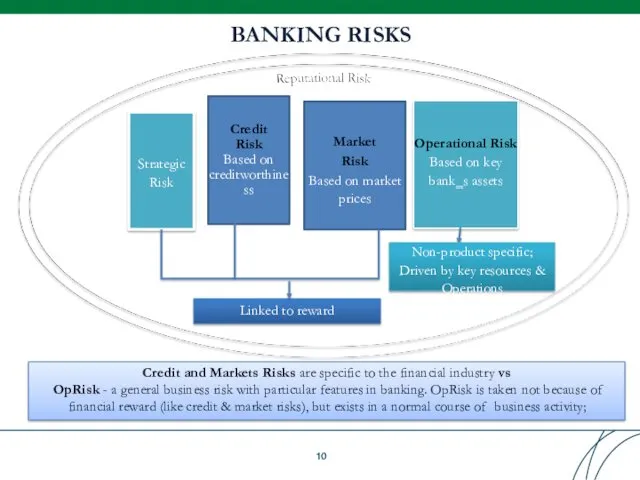

BANKING RISKS

Strategic Risk

Credit Risk Based on

creditworthine

ss

Market

Risk

Based on market prices

Operational Risk Based

BANKING RISKS

Strategic Risk

Credit Risk Based on

creditworthine

ss

Market

Risk

Based on market prices

Operational Risk Based

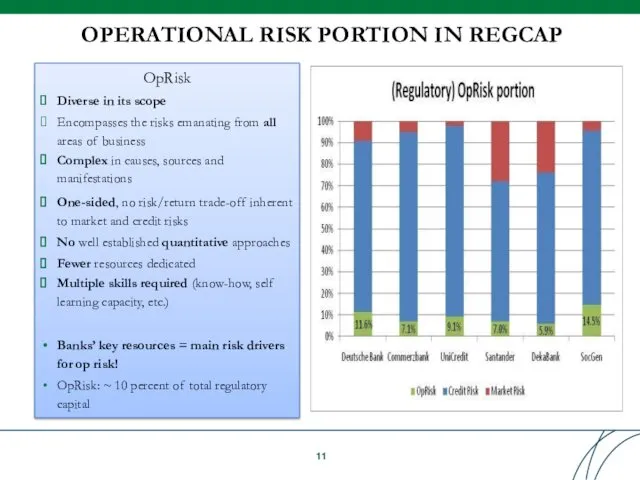

OPERATIONAL RISK PORTION IN REGCAP

OpRisk

Diverse in its scope

Encompasses the risks emanating

OPERATIONAL RISK PORTION IN REGCAP

OpRisk

Diverse in its scope

Encompasses the risks emanating

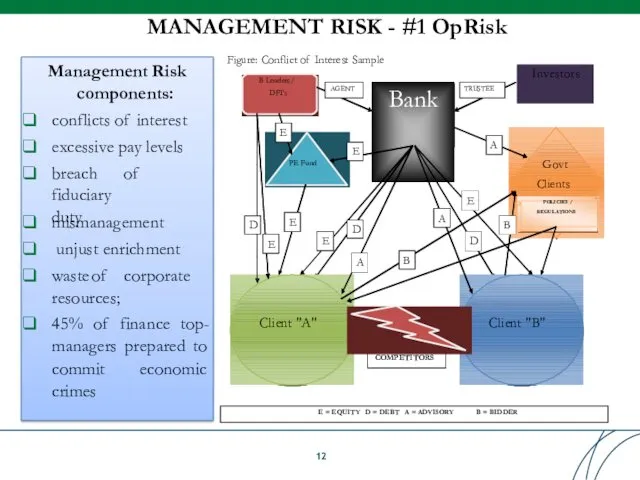

MANAGEMENT RISK - #1 OpRisk

Management Risk

components:

conflicts of interest

excessive pay levels

breach of fiduciary

duty

mismanagement

unjust enrichment

waste of corporate

resources;

45%

MANAGEMENT RISK - #1 OpRisk

Management Risk

components:

conflicts of interest

excessive pay levels

breach of fiduciary

duty

mismanagement

unjust enrichment

waste of corporate

resources;

45%

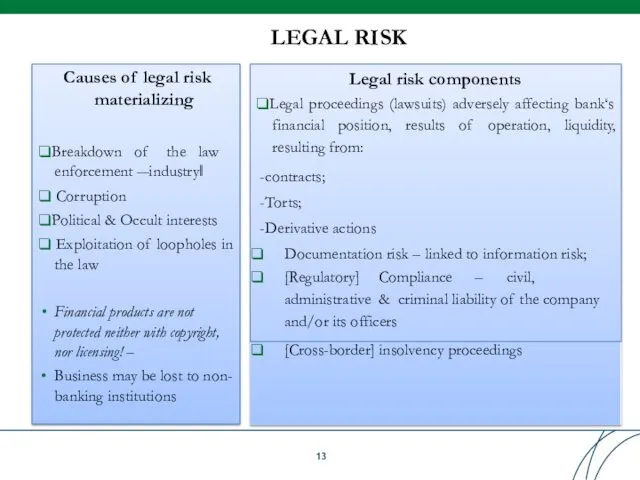

LEGAL RISK

Causes of legal risk materializing

❑Breakdown of the law enforcement ―industry‖

❑ Corruption

❑Political & Occult

LEGAL RISK

Causes of legal risk materializing

❑Breakdown of the law enforcement ―industry‖

❑ Corruption

❑Political & Occult

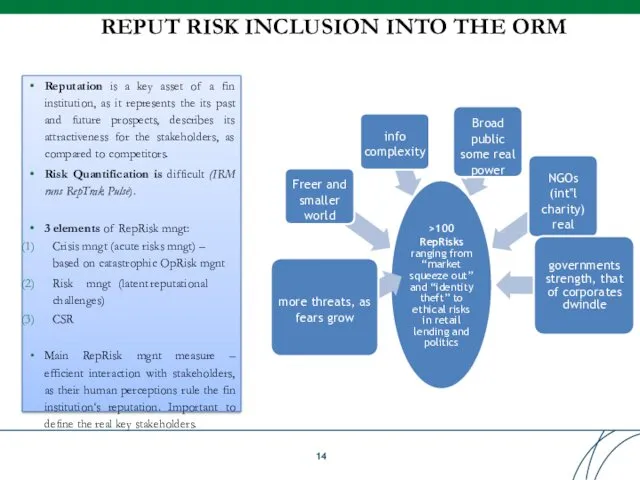

REPUT RISK INCLUSION INTO THE ORM

Reputation is a key asset of

REPUT RISK INCLUSION INTO THE ORM

Reputation is a key asset of

Table of Contents

Table of Contents

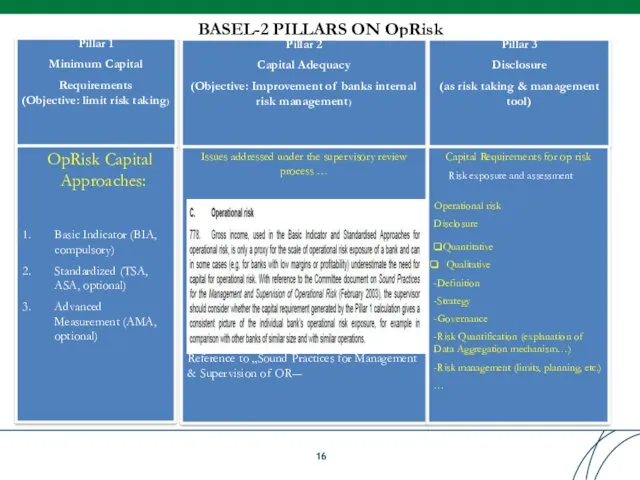

BASEL-2 PILLARS ON OpRisk

Pillar 1 Minimum Capital

Requirements (Objective: limit risk taking)

Pillar

BASEL-2 PILLARS ON OpRisk

Pillar 1 Minimum Capital

Requirements (Objective: limit risk taking)

Pillar

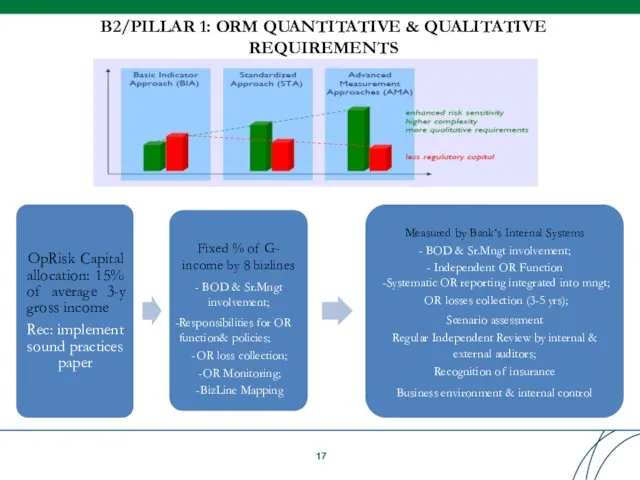

B2/PILLAR 1: ORM QUANTITATIVE & QUALITATIVE

REQUIREMENTS

OpRisk Capital allocation: 15% of average

B2/PILLAR 1: ORM QUANTITATIVE & QUALITATIVE

REQUIREMENTS

OpRisk Capital allocation: 15% of average

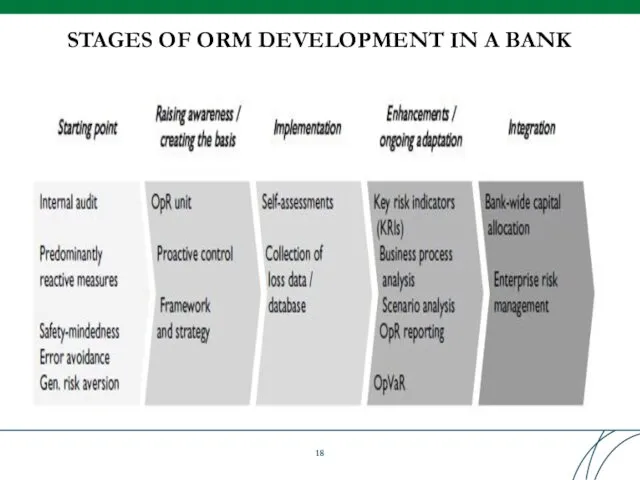

STAGES OF ORM DEVELOPMENT IN A BANK

STAGES OF ORM DEVELOPMENT IN A BANK

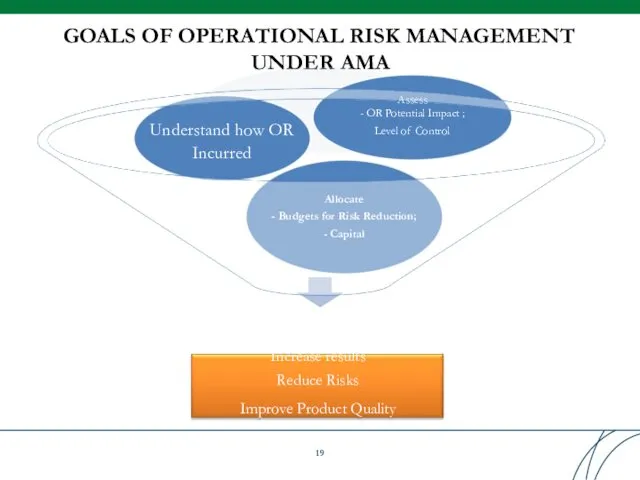

GOALS OF OPERATIONAL RISK MANAGEMENT UNDER AMA

Allocate

- Budgets for Risk Reduction;

-

GOALS OF OPERATIONAL RISK MANAGEMENT UNDER AMA

Allocate

- Budgets for Risk Reduction;

-

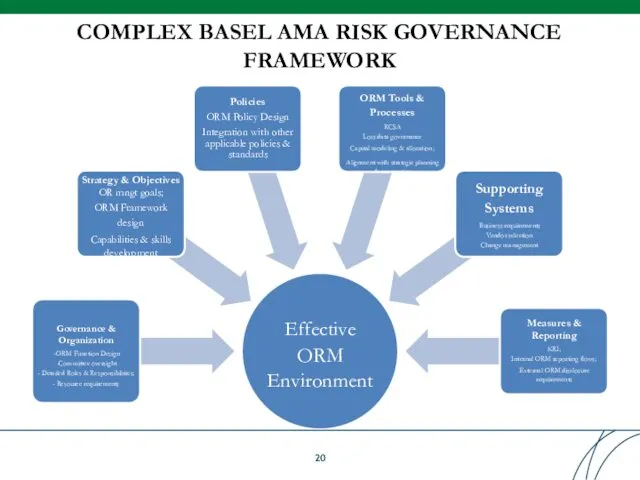

COMPLEX BASEL AMA RISK GOVERNANCE FRAMEWORK

Effective

ORM

Environment

Governance & Organization

ORM Function Design

Committee oversight

-

COMPLEX BASEL AMA RISK GOVERNANCE FRAMEWORK

Effective

ORM

Environment

Governance & Organization

ORM Function Design

Committee oversight

-

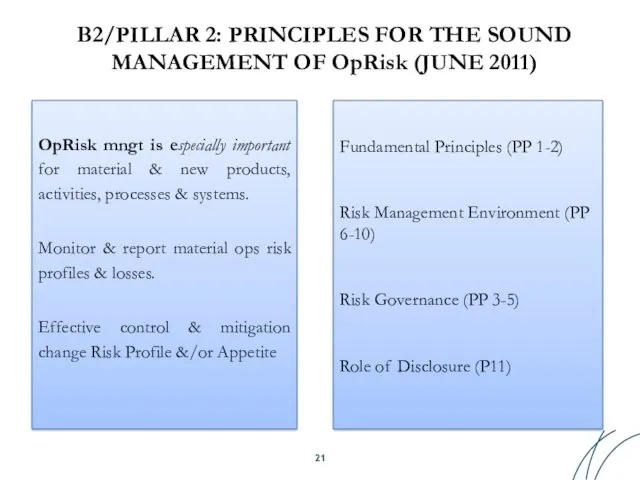

B2/PILLAR 2: PRINCIPLES FOR THE SOUND

MANAGEMENT OF OpRisk (JUNE 2011)

OpRisk mngt

B2/PILLAR 2: PRINCIPLES FOR THE SOUND

MANAGEMENT OF OpRisk (JUNE 2011)

OpRisk mngt

FUNDAMENTAL PRINCIPLE 1: BOD’s Leadership

… and ultimate responsibility for strong ORM

FUNDAMENTAL PRINCIPLE 1: BOD’s Leadership

… and ultimate responsibility for strong ORM

RISK CULTURE

Includes:

Integrity and ethical values;

Management philosophy & operating style;

Organizational structure;

Delegation of

RISK CULTURE

Includes:

Integrity and ethical values;

Management philosophy & operating style;

Organizational structure;

Delegation of

OP RISK APPETITE (ORA)

“the amount and type of risk an organization

OP RISK APPETITE (ORA)

“the amount and type of risk an organization

Fundamental P2: OpRisk framework integrated into overall risk management processes

It depends

Fundamental P2: OpRisk framework integrated into overall risk management processes

It depends

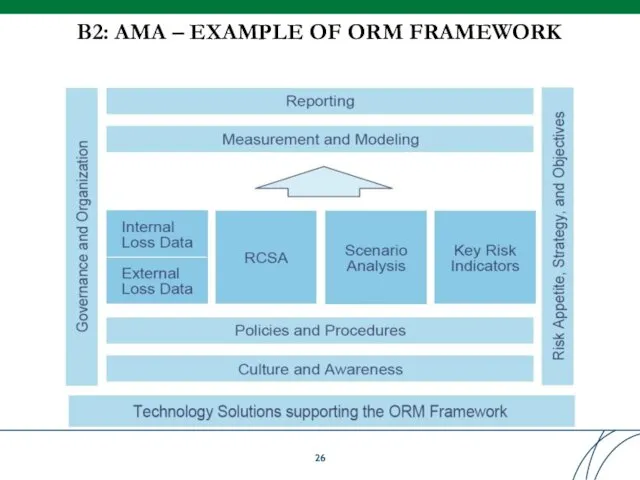

B2: AMA – EXAMPLE OF ORM FRAMEWORK

B2: AMA – EXAMPLE OF ORM FRAMEWORK

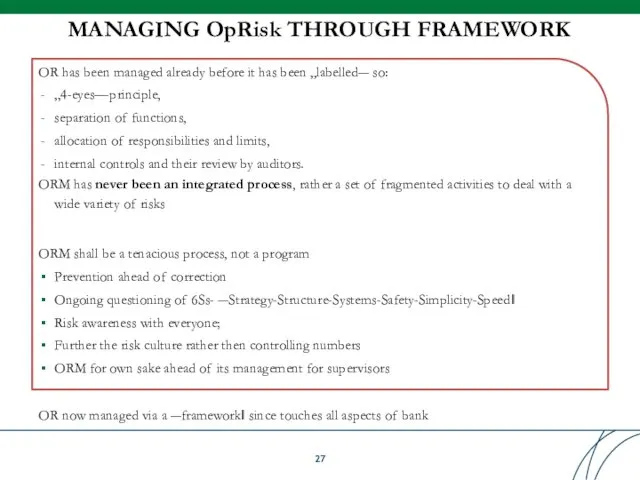

MANAGING OpRisk THROUGH FRAMEWORK

OR has been managed already before it has

MANAGING OpRisk THROUGH FRAMEWORK

OR has been managed already before it has

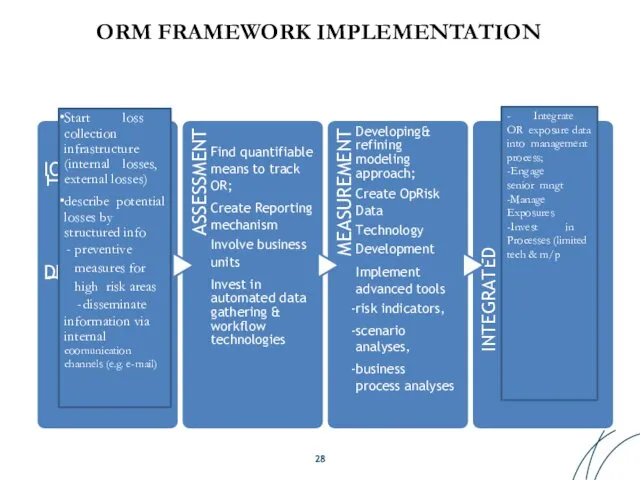

ORM FRAMEWORK IMPLEMENTATION

I

T

ION

DENTIFICA

ASSESSMENT

Find quantifiable means to track OR;

Create Reporting mechanism

Involve business

units

Invest

ORM FRAMEWORK IMPLEMENTATION

I

T

ION

DENTIFICA

ASSESSMENT

Find quantifiable means to track OR;

Create Reporting mechanism

Involve business

units

Invest

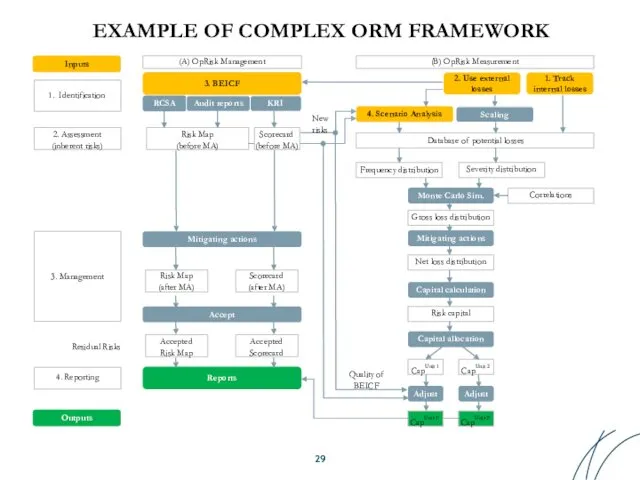

EXAMPLE OF COMPLEX ORM FRAMEWORK

Mitigating actions

Mitigating actions

Net loss distribution

Risk capital

Capital allocation

CapUnit

EXAMPLE OF COMPLEX ORM FRAMEWORK

Mitigating actions

Mitigating actions

Net loss distribution

Risk capital

Capital allocation

CapUnit

P6. Operational Risk Assessment

Assessment of operational risk in all material products,

P6. Operational Risk Assessment

Assessment of operational risk in all material products,

LOSS TYPES

Loss type

Causes

Monetary loss

Legal and liability

Lost legal suit

External legal and other

LOSS TYPES

Loss type

Causes

Monetary loss

Legal and liability

Lost legal suit

External legal and other

Processes

People

Systems

External events

BASEL 2, 2D-CLASSIFICATION – EVENT/CAUSE

BASED

Internal fraud

(due to acts intended to defraud,

Processes

People

Systems

External events

BASEL 2, 2D-CLASSIFICATION – EVENT/CAUSE

BASED

Internal fraud

(due to acts intended to defraud,

Internal Fraud

Unauthorized Activity (transactions intentionally not reported; transaction type unauthorized w/o

Internal Fraud

Unauthorized Activity (transactions intentionally not reported; transaction type unauthorized w/o

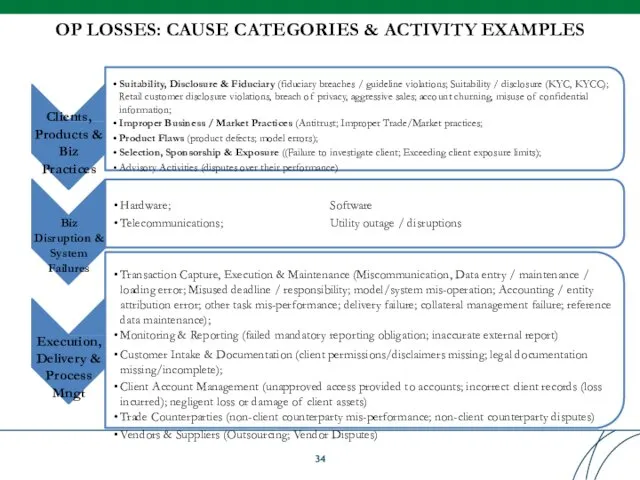

OP LOSSES: CAUSE CATEGORIES & ACTIVITY EXAMPLES

Clients, Products & Biz Practices

Suitability,

OP LOSSES: CAUSE CATEGORIES & ACTIVITY EXAMPLES

Clients, Products & Biz Practices

Suitability,

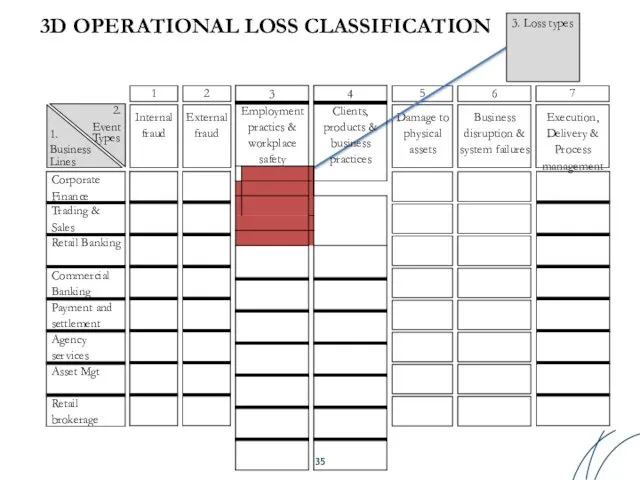

3D OPERATIONAL LOSS CLASSIFICATION

Internal fraud

External fraud

Damage to physical assets

Business disruption &

3D OPERATIONAL LOSS CLASSIFICATION

Internal fraud

External fraud

Damage to physical assets

Business disruption &

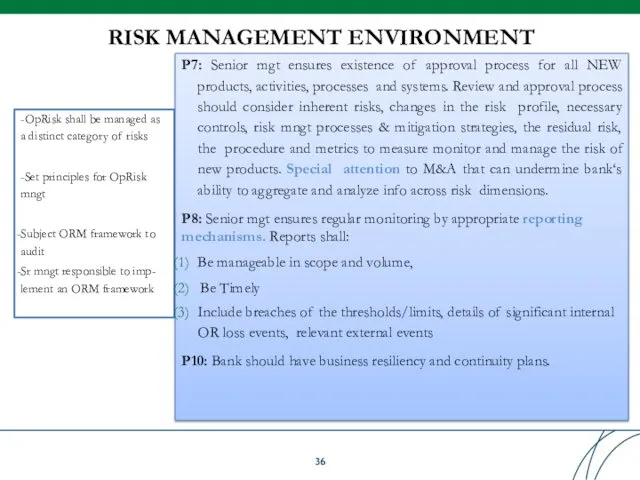

RISK MANAGEMENT ENVIRONMENT

-OpRisk shall be managed as a distinct category of

RISK MANAGEMENT ENVIRONMENT

-OpRisk shall be managed as a distinct category of

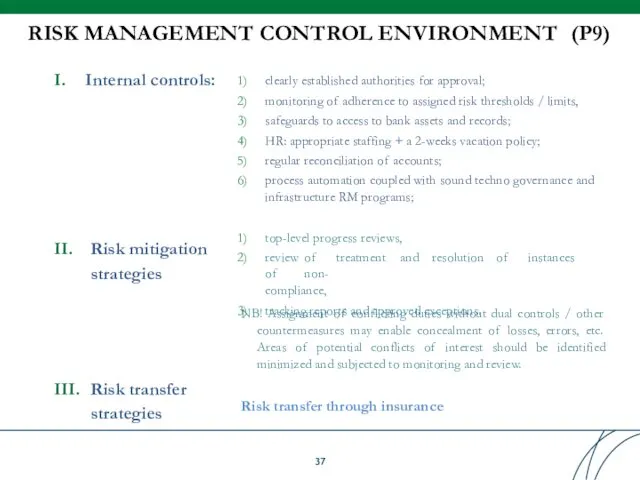

RISK MANAGEMENT CONTROL ENVIRONMENT (P9)

I. Internal controls:

II. Risk mitigation strategies

III. Risk transfer strategies

clearly established authorities

RISK MANAGEMENT CONTROL ENVIRONMENT (P9)

I. Internal controls:

II. Risk mitigation strategies

III. Risk transfer strategies

clearly established authorities

Table of Contents

Table of Contents

Table of Contents

Table of Contents

MAIN OPERATIONAL RISK MANAGEMENT TOOLS

Risk and

Control Self-

Assessment

Loss event Database

Scenario Modeling &

MAIN OPERATIONAL RISK MANAGEMENT TOOLS

Risk and

Control Self-

Assessment

Loss event Database

Scenario Modeling &

RCSA: PROACTIVE RISK IDENTIFICATION & MANAGEMENT TOOL

risks &

Business lines & support functions assess controls in their area;

RCSA

RCSA: PROACTIVE RISK IDENTIFICATION & MANAGEMENT TOOL

risks &

Business lines & support functions assess controls in their area;

RCSA

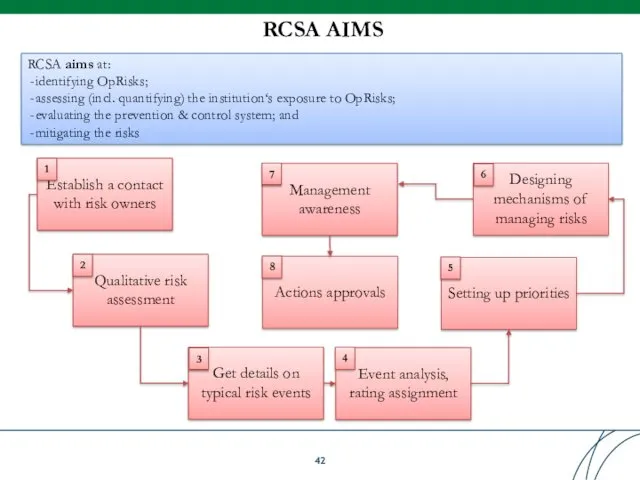

RCSA AIMS

Establish a contact

with risk owners

Qualitative risk

assessment

Get details on

typical risk events

Event

RCSA AIMS

Establish a contact

with risk owners

Qualitative risk

assessment

Get details on

typical risk events

Event

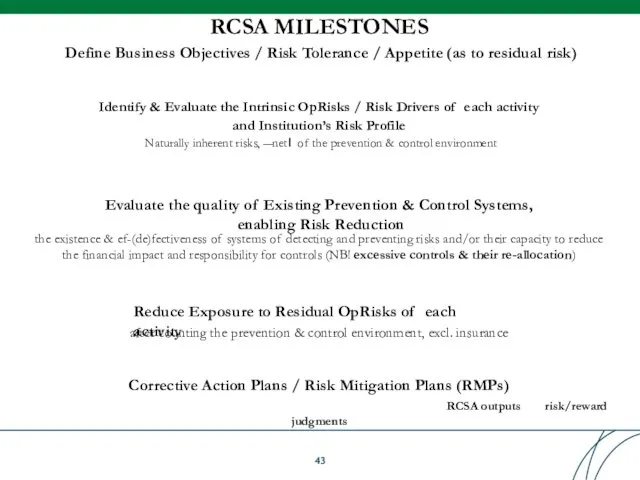

RCSA MILESTONES

Corrective Action Plans / Risk Mitigation Plans (RMPs)

Exterminate weak areas

RCSA MILESTONES

Corrective Action Plans / Risk Mitigation Plans (RMPs)

Exterminate weak areas

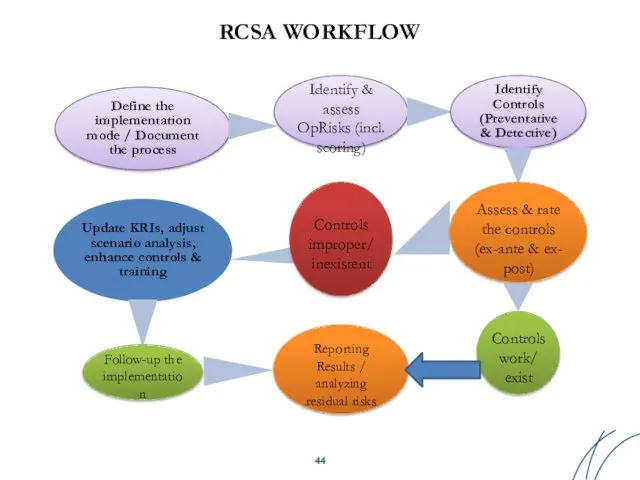

RCSA WORKFLOW

Define the implementation mode / Document the process

Update KRIs, adjust

RCSA WORKFLOW

Define the implementation mode / Document the process

Update KRIs, adjust

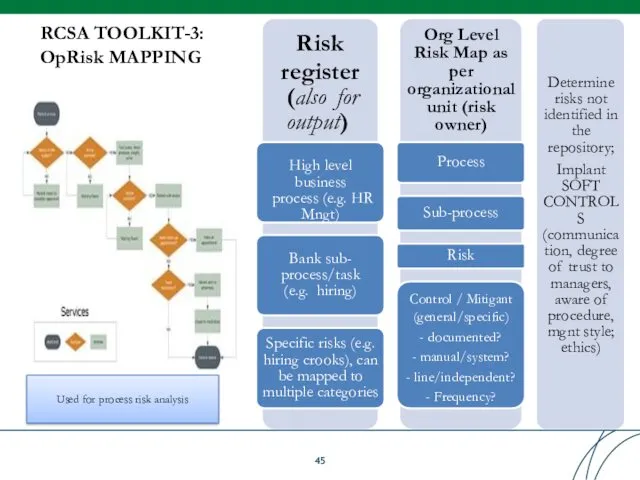

RCSA TOOLKIT-3:

OpRisk MAPPING

Risk

register (also for output)

High level business process (e.g. HR

RCSA TOOLKIT-3:

OpRisk MAPPING

Risk

register (also for output)

High level business process (e.g. HR

INPUT OpRisk MAPPING SAMPLE

INPUT OpRisk MAPPING SAMPLE

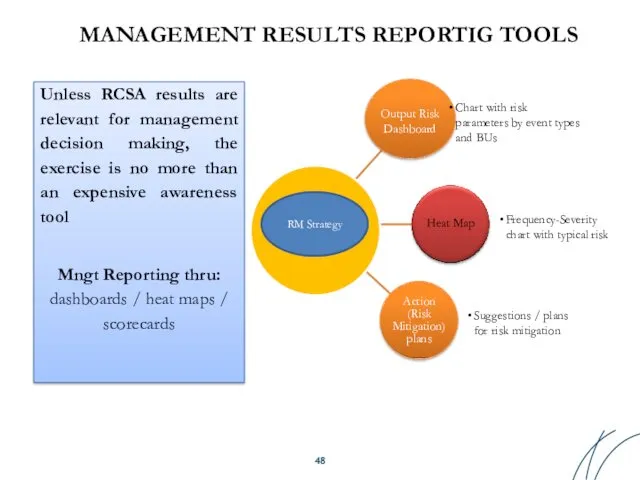

MANAGEMENT RESULTS REPORTIG TOOLS

Unless RCSA results are relevant for management decision

MANAGEMENT RESULTS REPORTIG TOOLS

Unless RCSA results are relevant for management decision

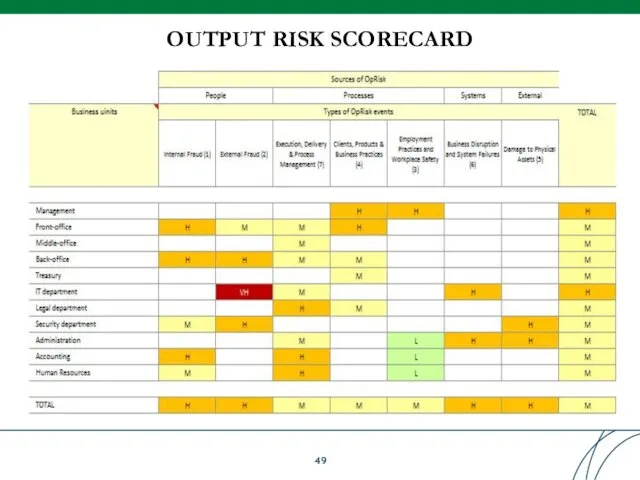

OUTPUT RISK SCORECARD

OUTPUT RISK SCORECARD

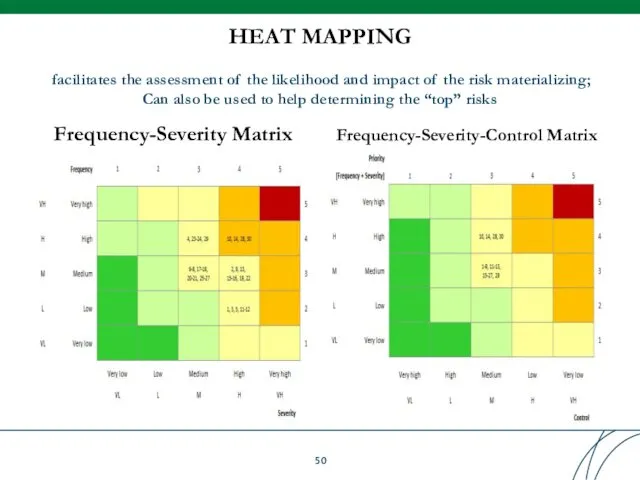

HEAT MAPPING

facilitates the assessment of the likelihood and impact of the

HEAT MAPPING

facilitates the assessment of the likelihood and impact of the

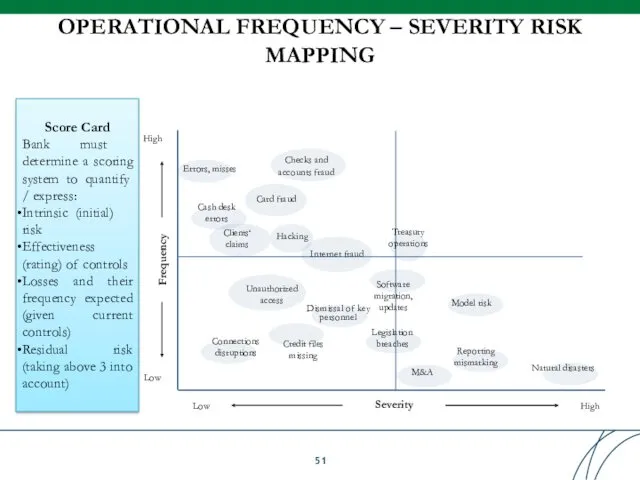

OPERATIONAL FREQUENCY – SEVERITY RISK

MAPPING

Card fraud

Frequency

Severity

High

Low

Low

High

Unauthorized access

Checks and

accounts fraud

Errors, misses

Internet fraud

Hacking

Connections

OPERATIONAL FREQUENCY – SEVERITY RISK

MAPPING

Card fraud

Frequency

Severity

High

Low

Low

High

Unauthorized access

Checks and

accounts fraud

Errors, misses

Internet fraud

Hacking

Connections

RCSA FOLLOW UP

RCSA results ought to be used in conjunction with

RCSA FOLLOW UP

RCSA results ought to be used in conjunction with

Table of Contents

Table of Contents

Basel Committee on Banking Supervision

Principles for the Sound Management of Operational

Basel Committee on Banking Supervision

Principles for the Sound Management of Operational

Indicators Approach allows to track operational risk profile and monitor risk

Indicators Approach allows to track operational risk profile and monitor risk

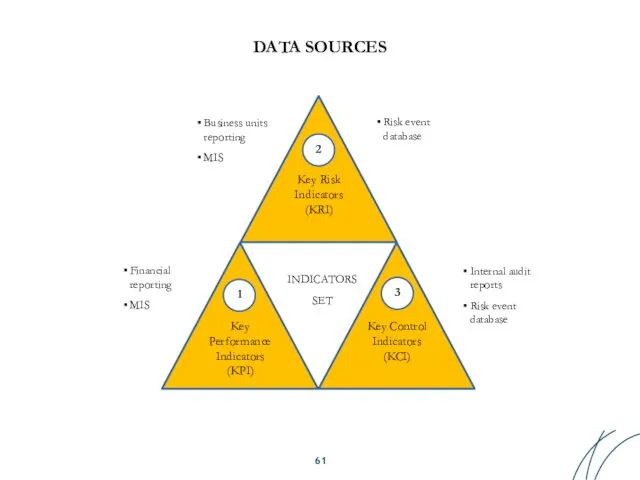

INDICATORS COMPOSITION and DATA SOURCES

Key Risk Indicators (KRI)

Key Performance Indicators (KPI)

Key

INDICATORS COMPOSITION and DATA SOURCES

Key Risk Indicators (KRI)

Key Performance Indicators (KPI)

Key

KRIs are the measures summarizing the frequency, severity and impact of

KRIs are the measures summarizing the frequency, severity and impact of

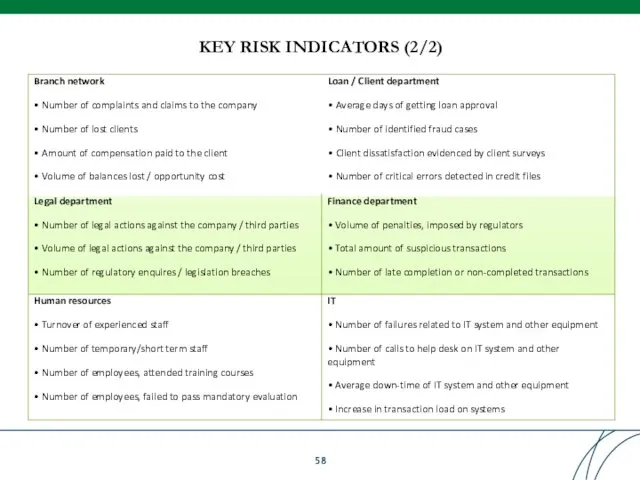

KEY RISK INDICATORS (2/2)

KEY RISK INDICATORS (2/2)

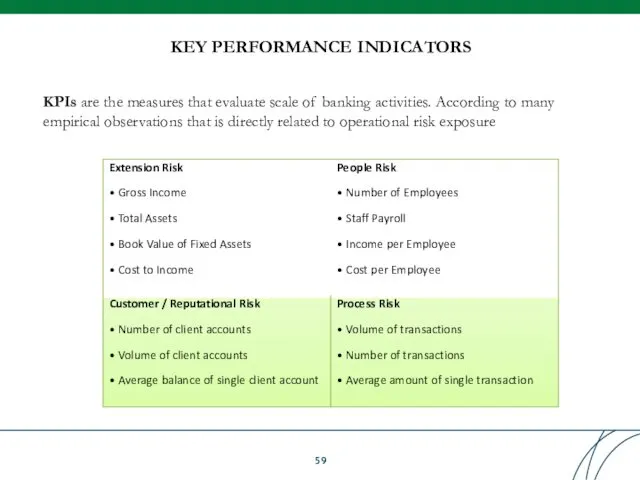

KPIs are the measures that evaluate scale of banking activities. According

KPIs are the measures that evaluate scale of banking activities. According

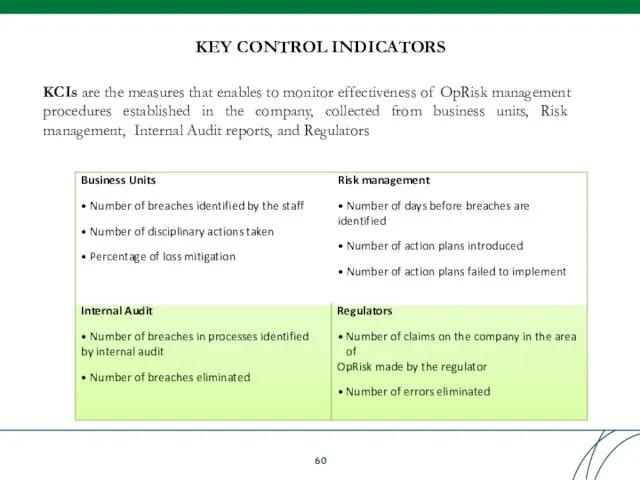

KCIs are the measures that enables to monitor effectiveness of OpRisk

KCIs are the measures that enables to monitor effectiveness of OpRisk

DATA SOURCES

Key Risk Indicators (KRI)

Key Performance Indicators (KPI)

Key Control Indicators (KCI)

INDICATORS

DATA SOURCES

Key Risk Indicators (KRI)

Key Performance Indicators (KPI)

Key Control Indicators (KCI)

INDICATORS

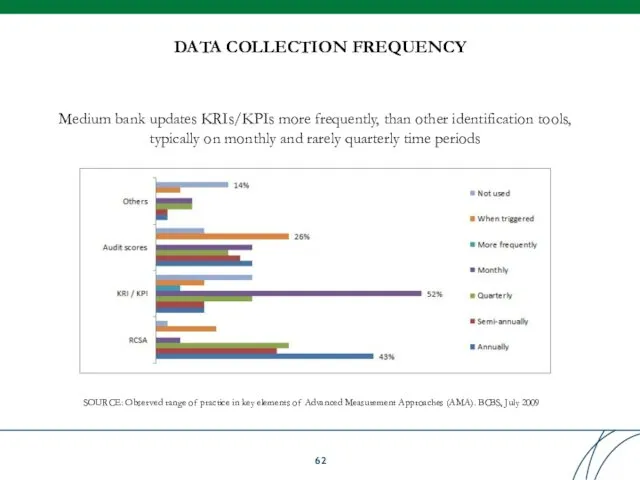

DATA COLLECTION FREQUENCY

SOURCE: Observed range of practice in key elements of

DATA COLLECTION FREQUENCY

SOURCE: Observed range of practice in key elements of

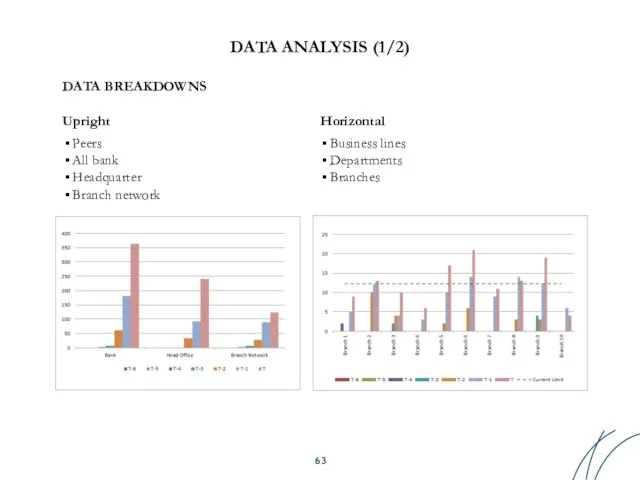

DATA BREAKDOWNS

Upright

Peers

All bank

Headquarter

Branch network

DATA ANALYSIS (1/2)

Horizontal

Business lines

Departments

Branches

DATA BREAKDOWNS

Upright

Peers

All bank

Headquarter

Branch network

DATA ANALYSIS (1/2)

Horizontal

Business lines

Departments

Branches

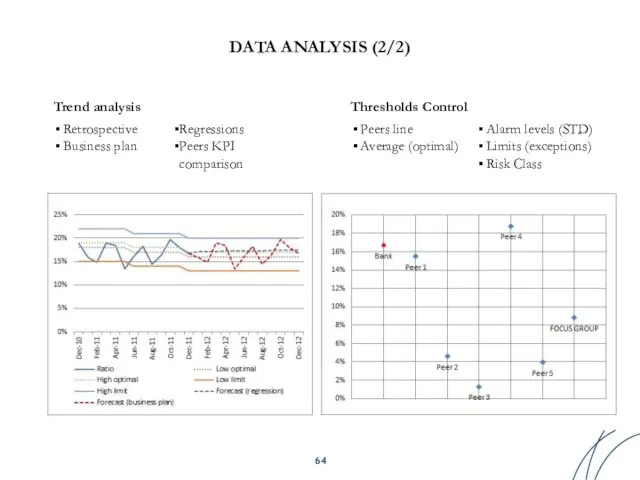

DATA ANALYSIS (2/2)

Trend analysis

Retrospective

Business plan

Regressions

Peers KPI comparison

Thresholds Control

Peers line

Average (optimal)

Alarm levels

DATA ANALYSIS (2/2)

Trend analysis

Retrospective

Business plan

Regressions

Peers KPI comparison

Thresholds Control

Peers line

Average (optimal)

Alarm levels

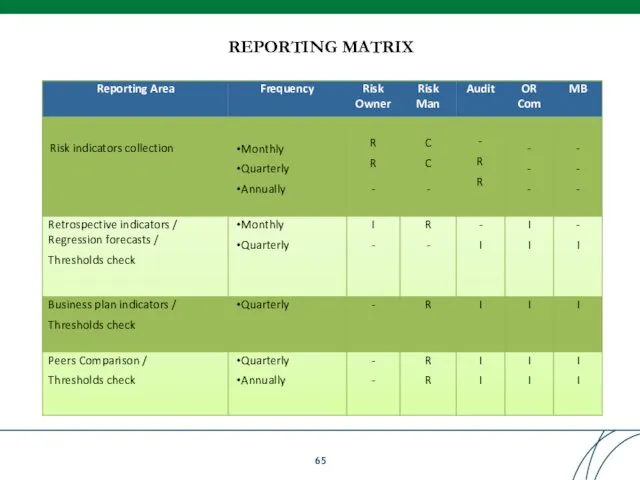

REPORTING MATRIX

REPORTING MATRIX

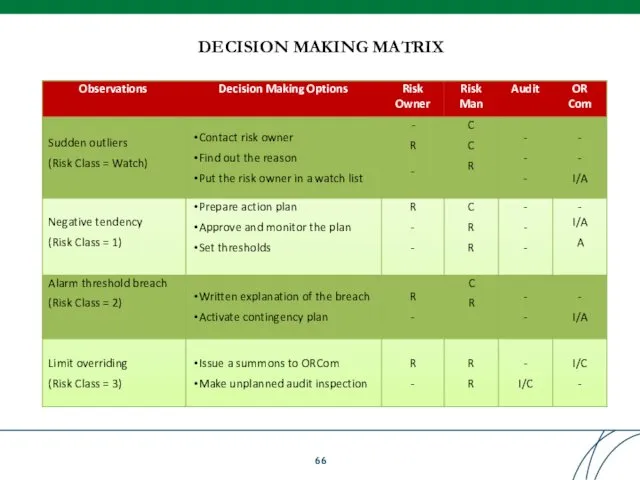

DECISION MAKING MATRIX

DECISION MAKING MATRIX

Table of Contents

Table of Contents

Basel Committee on Banking Supervision

Principles for the Sound Management of Operational

Basel Committee on Banking Supervision

Principles for the Sound Management of Operational

The review and approval process should consider:

inherent risks in the new

The review and approval process should consider:

inherent risks in the new

Business process is a collection of linked activities that consume inputs,

Business process is a collection of linked activities that consume inputs,

BUSINESS PROCESS MANAGEMENT TOOLS

Process engineering

Process initiation document

As Is:

Flowchart

Activity flow diagram

RACI matrix

Process

BUSINESS PROCESS MANAGEMENT TOOLS

Process engineering

Process initiation document

As Is:

Flowchart

Activity flow diagram

RACI matrix

Process

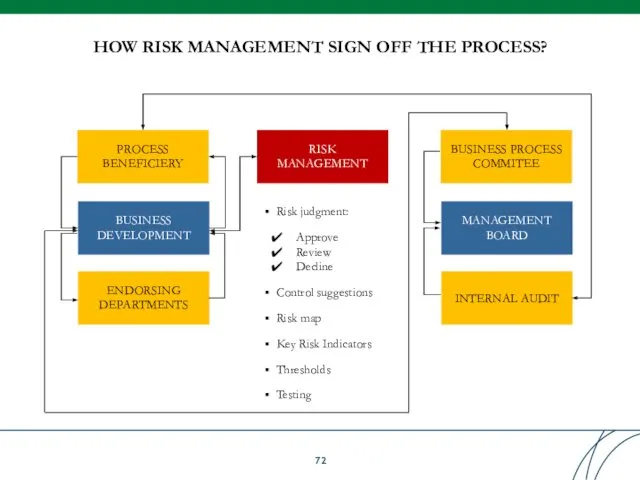

HOW RISK MANAGEMENT SIGN OFF THE PROCESS?

PROCESS BENEFICIERY

BUSINESS DEVELOPMENT

ENDORSING

DEPARTMENTS

RISK MANAGEMENT

Risk judgment:

Approve

Review

Decline

Control

HOW RISK MANAGEMENT SIGN OFF THE PROCESS?

PROCESS BENEFICIERY

BUSINESS DEVELOPMENT

ENDORSING

DEPARTMENTS

RISK MANAGEMENT

Risk judgment:

Approve

Review

Decline

Control

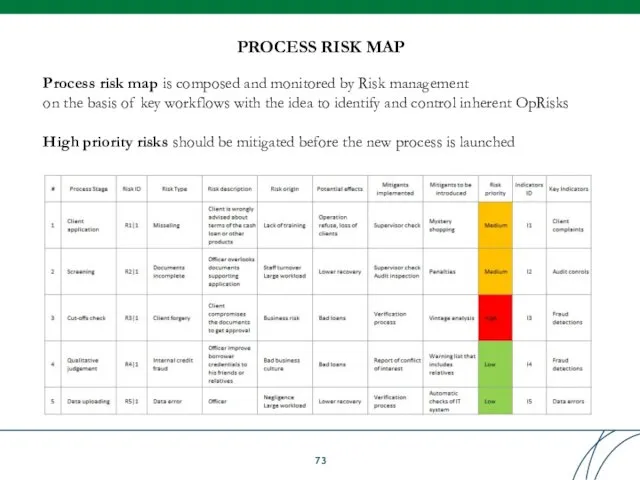

Process risk map is composed and monitored by Risk management

on the

Process risk map is composed and monitored by Risk management

on the

RISK CONTRIBUTION TO FLOWCHART

Quality controls make the flowchart telling what goes

RISK CONTRIBUTION TO FLOWCHART

Quality controls make the flowchart telling what goes

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Basel Committee on Banking Supervision

Principles for the Sound Management of Operational

Basel Committee on Banking Supervision

Principles for the Sound Management of Operational

Risk event database is a register of risk event records that

Risk event database is a register of risk event records that

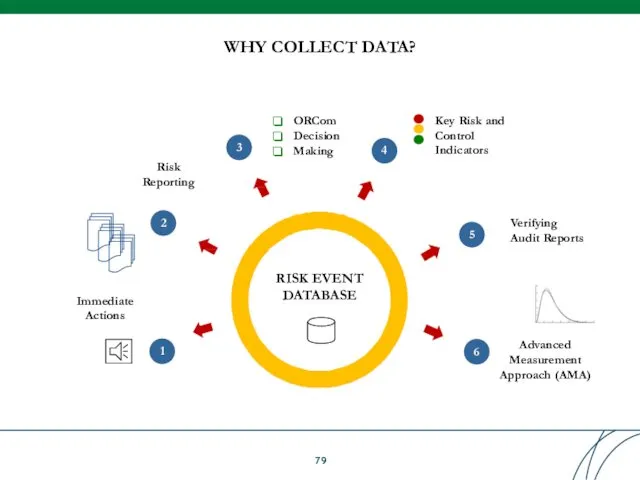

WHY COLLECT DATA?

RISK EVENT DATABASE

Immediate Actions

Advanced Measurement Approach (AMA)

1

2

Risk Reporting

4

Key Risk

WHY COLLECT DATA?

RISK EVENT DATABASE

Immediate Actions

Advanced Measurement Approach (AMA)

1

2

Risk Reporting

4

Key Risk

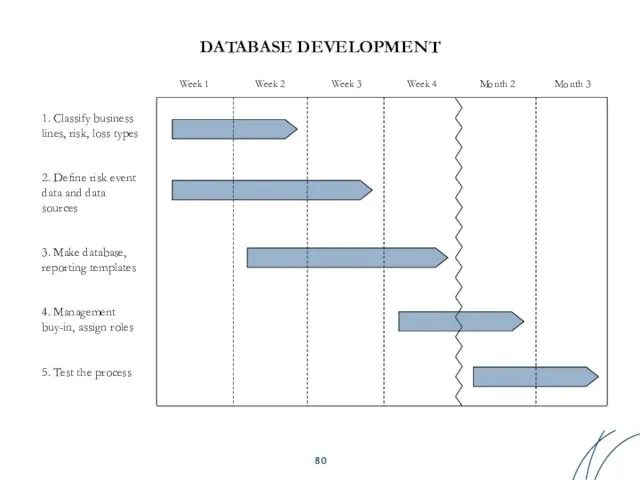

DATABASE DEVELOPMENT

1. Classify business lines, risk, loss types

2. Define risk event

DATABASE DEVELOPMENT

1. Classify business lines, risk, loss types

2. Define risk event

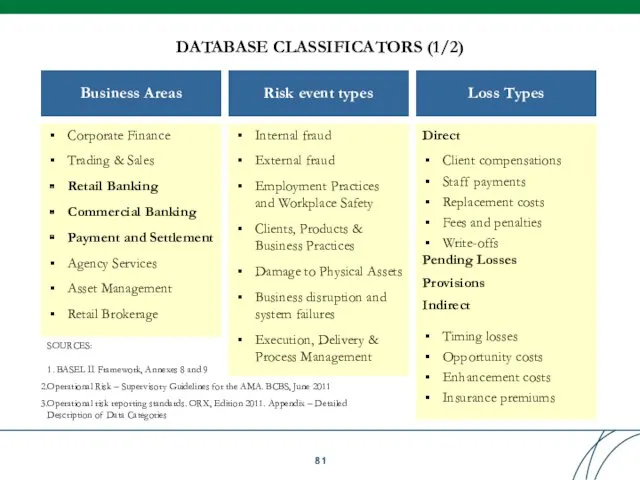

DATABASE CLASSIFICATORS (1/2)

Business Areas

Corporate Finance

Trading & Sales

Retail Banking

Commercial Banking

Payment and Settlement

Agency

DATABASE CLASSIFICATORS (1/2)

Business Areas

Corporate Finance

Trading & Sales

Retail Banking

Commercial Banking

Payment and Settlement

Agency

DATABASE CLASSIFICATORS (2/2)

Practical considerations

Coding classes (Size and Filtering)

Low-level breakdowns of first-rank

DATABASE CLASSIFICATORS (2/2)

Practical considerations

Coding classes (Size and Filtering)

Low-level breakdowns of first-rank

RISK GRANULARITY

BASEL II Framework:

A bank's risk measurement system must be sufficiently

RISK GRANULARITY

BASEL II Framework:

A bank's risk measurement system must be sufficiently

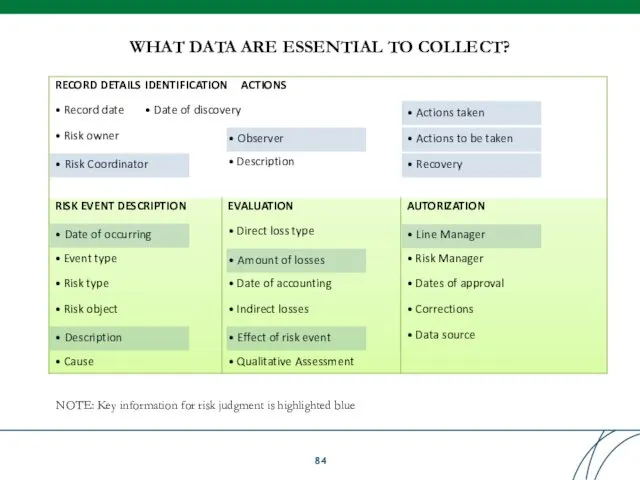

WHAT DATA ARE ESSENTIAL TO COLLECT?

• Risk Coordinator

• Observer

• Actions taken

•

WHAT DATA ARE ESSENTIAL TO COLLECT?

• Risk Coordinator

• Observer

• Actions taken

•

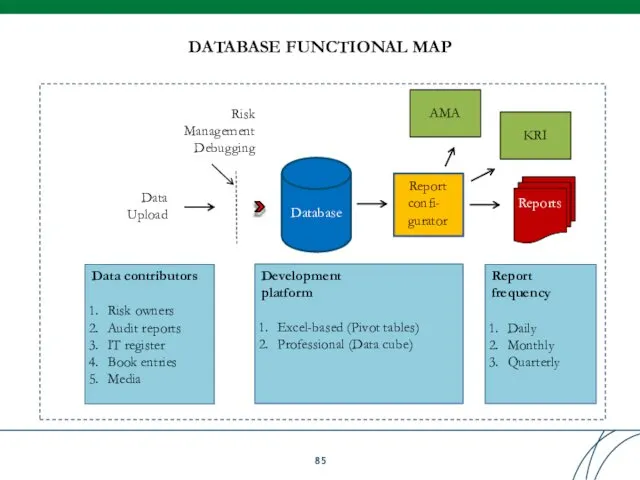

DATABASE FUNCTIONAL MAP

Data

Upload

Database

Report confi- gurator

Reports

Data contributors

Risk owners

Audit reports

IT register

Book entries

Media

Development platform

Excel-based

DATABASE FUNCTIONAL MAP

Data

Upload

Database

Report confi- gurator

Reports

Data contributors

Risk owners

Audit reports

IT register

Book entries

Media

Development platform

Excel-based

Bank Staff

Coordinator

Identify risk event

Inform Coordinator

Examine the details of risk event

Report to

Coordinator

Identify risk event

Inform Coordinator

Examine the details of risk event

Report to

DATA COLLECTION: DIFFICULTIES AND SOLUTIONS

Difficulties

Lack of knowledge which information to be

DATA COLLECTION: DIFFICULTIES AND SOLUTIONS

Difficulties

Lack of knowledge which information to be

KEY DATES OF DATA COLLECTION

SOURCE: Observed range of practice in key

KEY DATES OF DATA COLLECTION

SOURCE: Observed range of practice in key

SPECIFIC EVENT TYPES (1/3)

SOURCE: Operational Risk Reporting Standards. ORX, Edition 2011

OpRisk

SPECIFIC EVENT TYPES (1/3)

SOURCE: Operational Risk Reporting Standards. ORX, Edition 2011

OpRisk

SPECIFIC EVENT TYPES (2/3)

SOURCE:

Operational Risk Reporting Standards. ORX, Edition 2011

Observed range

SPECIFIC EVENT TYPES (2/3)

SOURCE:

Operational Risk Reporting Standards. ORX, Edition 2011

Observed range

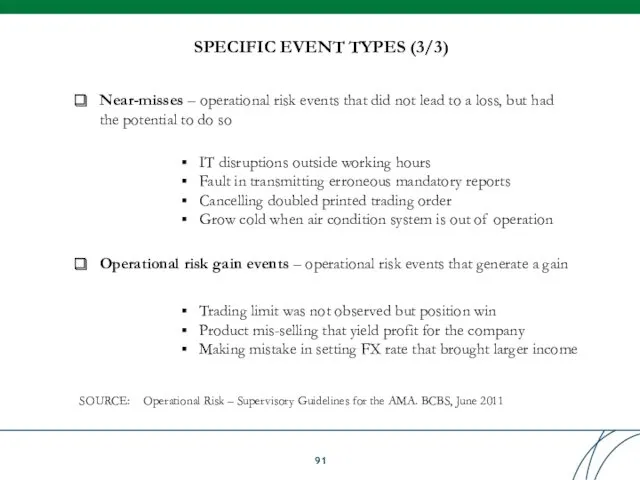

SPECIFIC EVENT TYPES (3/3)

Near-misses – operational risk events that did not

SPECIFIC EVENT TYPES (3/3)

Near-misses – operational risk events that did not

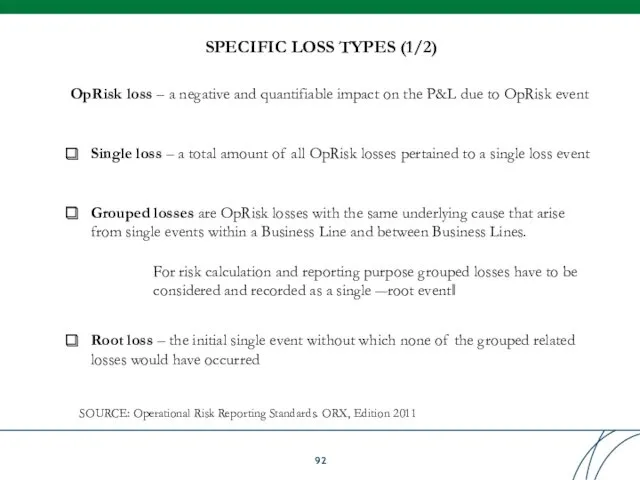

SPECIFIC LOSS TYPES (1/2)

SOURCE: Operational Risk Reporting Standards. ORX, Edition 2011

OpRisk

SPECIFIC LOSS TYPES (1/2)

SOURCE: Operational Risk Reporting Standards. ORX, Edition 2011

OpRisk

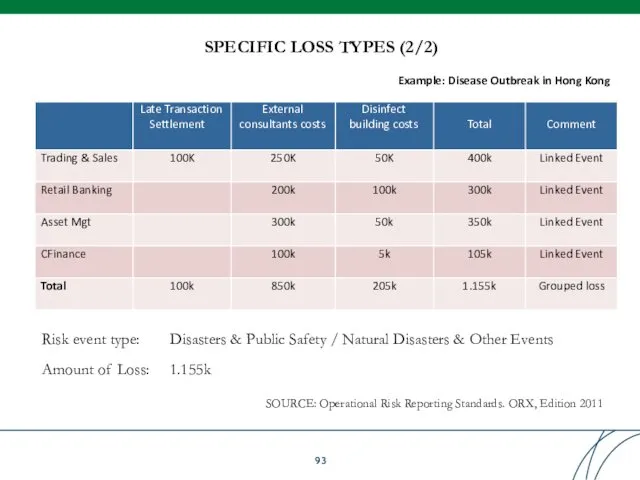

SPECIFIC LOSS TYPES (2/2)

SOURCE: Operational Risk Reporting Standards. ORX, Edition 2011

Risk

SPECIFIC LOSS TYPES (2/2)

SOURCE: Operational Risk Reporting Standards. ORX, Edition 2011

Risk

EXTERNAL LOSS DATA (1/4)

Lack of internal observations

No data integrity and granularity

Low

EXTERNAL LOSS DATA (1/4)

Lack of internal observations

No data integrity and granularity

Low

EXTERNAL LOSS DATA (2/4)

SOURCE: Observed range of practice in key elements

EXTERNAL LOSS DATA (2/4)

SOURCE: Observed range of practice in key elements

EXTERNAL LOSS DATA (3/4)

Key information

Business line / Event type

Causes / Consequences

Amount

EXTERNAL LOSS DATA (3/4)

Key information

Business line / Event type

Causes / Consequences

Amount

QUIZ: EXTERNAL LOSS DATA – local examples

Internal fraud

External fraud Reputational risk

QUIZ: EXTERNAL LOSS DATA – local examples

Internal fraud

External fraud Reputational risk

RISK EVENT DATA REPORTING MATRIX

RISK EVENT DATA REPORTING MATRIX

KEY RISK REPORTS: 8x7 Matrix

SOURCE: Results from the 2008 Loss Data

KEY RISK REPORTS: 8x7 Matrix

SOURCE: Results from the 2008 Loss Data

KEY RISK REPORTS: 8x7 Matrix

SOURCE: Results from the 2008 Loss Data

KEY RISK REPORTS: 8x7 Matrix

SOURCE: Results from the 2008 Loss Data

KEY RISK REPORTS: Severity Distribution

Report shows distribution of frequency and loss

KEY RISK REPORTS: Severity Distribution

Report shows distribution of frequency and loss

KEY RISK REPORTS: Summary Report

Report aggregates frequency and loss amount by

KEY RISK REPORTS: Summary Report

Report aggregates frequency and loss amount by

KEY RISK REPORTS: Register Report

Report lists key parameters of risk events

KEY RISK REPORTS: Register Report

Report lists key parameters of risk events

DATABASE SET INCLUDES:

Classifications matrixes

Data structure

Reporting templates

Workflow guidelines

Job descriptions of key involved

DATABASE SET INCLUDES:

Classifications matrixes

Data structure

Reporting templates

Workflow guidelines

Job descriptions of key involved

Table of Contents

Table of Contents

Basel Committee on Banking Supervision

Principles for the Sound Management of Operational

Basel Committee on Banking Supervision

Principles for the Sound Management of Operational

MEASUREMENT APPROACHES

Deviation of Capital Charge | Opportunity Costs

Complexity | implementation Costs

Basic

MEASUREMENT APPROACHES

Deviation of Capital Charge | Opportunity Costs

Complexity | implementation Costs

Basic

SELECTION CRITERIA

Complexity or intensity of banking operations

Meeting qualitative standards

Partial use

Restriction to

SELECTION CRITERIA

Complexity or intensity of banking operations

Meeting qualitative standards

Partial use

Restriction to

BASIC INDICATOR APPROACH (1/2)

The simplest approach based on linear dependence between

BASIC INDICATOR APPROACH (1/2)

The simplest approach based on linear dependence between

BASIC INDICATOR APPROACH (2/2)

BASIC INDICATOR APPROACH (2/2)

THE STANDARDIZED APPROACH (1/3)

More accurate approach sensitive to business line segmentation

Advantages:

Fairly

THE STANDARDIZED APPROACH (1/3)

More accurate approach sensitive to business line segmentation

Advantages:

Fairly

THE STANDARDIZED APPROACH (2/3)

THE STANDARDIZED APPROACH (2/3)

THE STANDARDIZED APPROACH (3/3)

Minimum qualifying criteria for TSA:

Management oversight of ORM

THE STANDARDIZED APPROACH (3/3)

Minimum qualifying criteria for TSA:

Management oversight of ORM

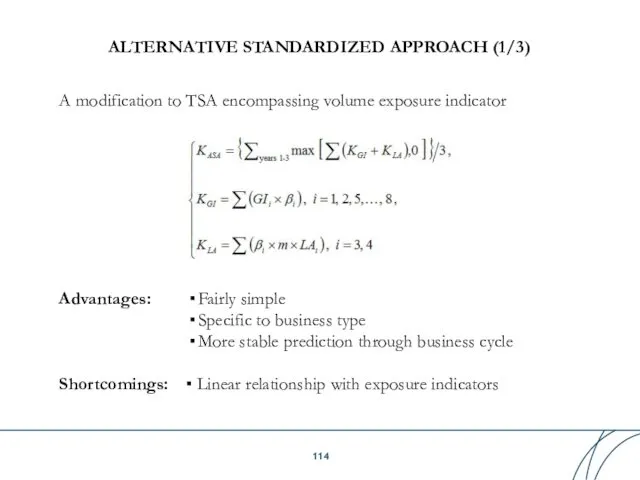

ALTERNATIVE STANDARDIZED APPROACH (1/3)

A modification to TSA encompassing volume exposure indicator

Advantages:

Fairly

ALTERNATIVE STANDARDIZED APPROACH (1/3)

A modification to TSA encompassing volume exposure indicator

Advantages:

Fairly

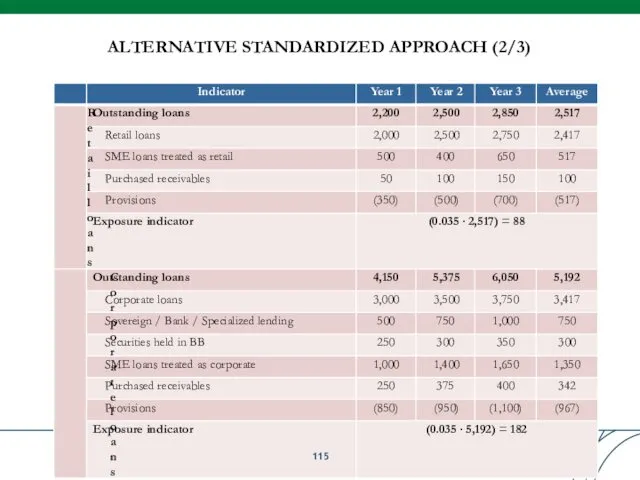

ALTERNATIVE STANDARDIZED APPROACH (2/3)

ALTERNATIVE STANDARDIZED APPROACH (2/3)

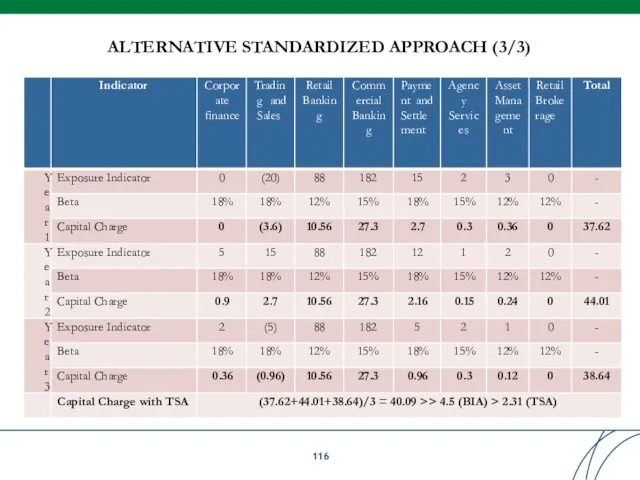

ALTERNATIVE STANDARDIZED APPROACH (3/3)

ALTERNATIVE STANDARDIZED APPROACH (3/3)

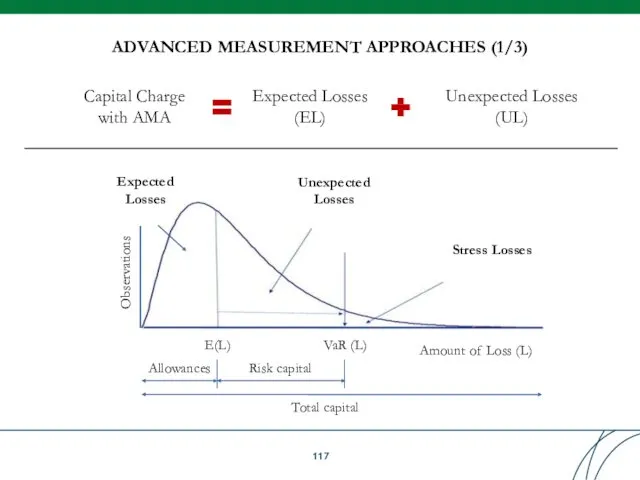

ADVANCED MEASUREMENT APPROACHES (1/3)

Capital Charge with AMA

Stress Losses

VaR (L)

E(L)

Allowances

Risk capital

Total capital

Unexpected

Losses

Expected

ADVANCED MEASUREMENT APPROACHES (1/3)

Capital Charge with AMA

Stress Losses

VaR (L)

E(L)

Allowances

Risk capital

Total capital

Unexpected

Losses

Expected

Qualifying standards:

Meeting minimum qualifying criteria used for TSA

Having independent full-fledged ORM

Qualifying standards:

Meeting minimum qualifying criteria used for TSA

Having independent full-fledged ORM

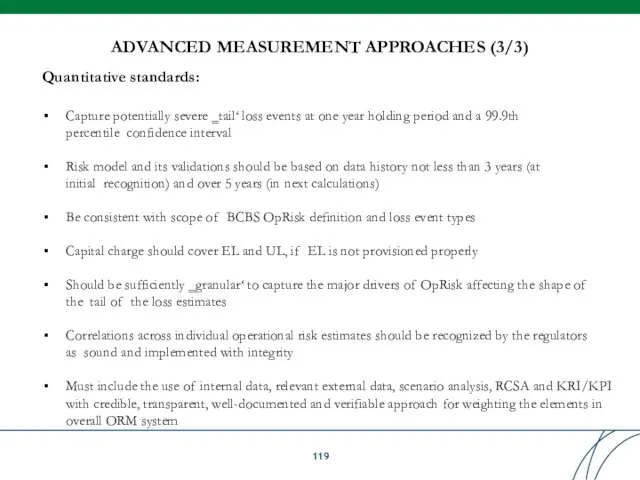

Quantitative standards:

Capture potentially severe ‗tail‘ loss events at one year holding

Quantitative standards:

Capture potentially severe ‗tail‘ loss events at one year holding

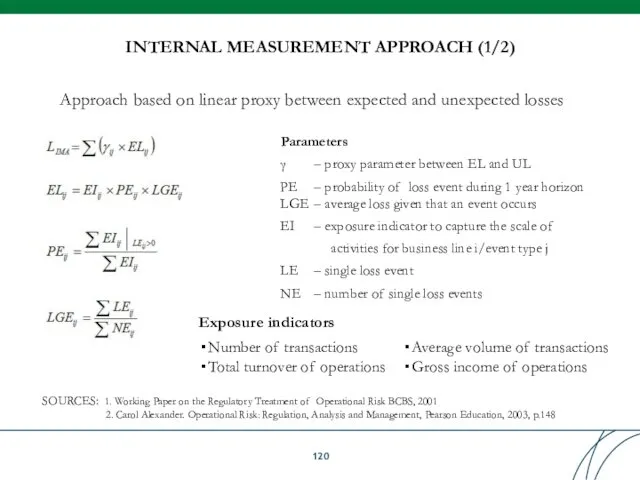

INTERNAL MEASUREMENT APPROACH (1/2)

Approach based on linear proxy between expected and

INTERNAL MEASUREMENT APPROACH (1/2)

Approach based on linear proxy between expected and

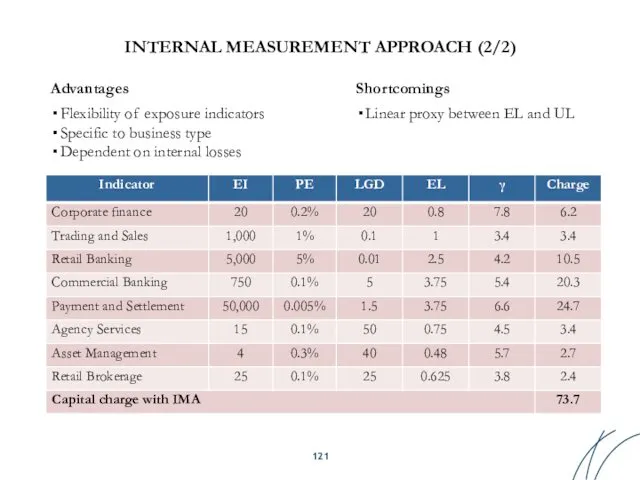

INTERNAL MEASUREMENT APPROACH (2/2)

Advantages

Flexibility of exposure indicators

Specific to business type

Dependent on

INTERNAL MEASUREMENT APPROACH (2/2)

Advantages

Flexibility of exposure indicators

Specific to business type

Dependent on

LOSS DISTRIBUTION APPROACH (1/6)

LDA estimates for each business line / event

LOSS DISTRIBUTION APPROACH (1/6)

LDA estimates for each business line / event

LOSS DISTRIBUTION APPROACH (2/6)

OpRisk Loss Simulation Algorithm:

Collect statistics on loss events

LOSS DISTRIBUTION APPROACH (2/6)

OpRisk Loss Simulation Algorithm:

Collect statistics on loss events

LOSS DISTRIBUTION APPROACH (3/6)

Severity distributions

Lognormal

Pareto

Weibull

Validation tests

Q-Q plot

K-S test

SOURCE: Observed range of

LOSS DISTRIBUTION APPROACH (3/6)

Severity distributions

Lognormal

Pareto

Weibull

Validation tests

Q-Q plot

K-S test

SOURCE: Observed range of

LOSS DISTRIBUTION APPROACH (4/6)

Frequency distributions

Poisson

Negative Binomial

Validation tests

χ2-test

SOURCE: Observed range of practice

LOSS DISTRIBUTION APPROACH (4/6)

Frequency distributions

Poisson

Negative Binomial

Validation tests

χ2-test

SOURCE: Observed range of practice

LOSS DISTRIBUTION APPROACH (5/6)

Loss aggregation

BU/ET 1

BU/ET n

BU/ET

…

Gross Loss

SOURCE: Carol Alexander. Operational

LOSS DISTRIBUTION APPROACH (5/6)

Loss aggregation

BU/ET 1

BU/ET n

BU/ET

…

Gross Loss

SOURCE: Carol Alexander. Operational

LOSS DISTRIBUTION APPROACH (6/6)

SOURCE:

Observed range of practice in key elements of

LOSS DISTRIBUTION APPROACH (6/6)

SOURCE:

Observed range of practice in key elements of

Table of Contents

Table of Contents

Basel Committee on Banking Supervision

> Principles for the Sound Management of

Basel Committee on Banking Supervision

> Principles for the Sound Management of

Business areas

Risk types

Data sources

Scenario risk drivers

Frequency

Severity

Loss Amount

Recovery

Return time

Assumptions formulation

Worst case

Baseline

Best case

Scenario

Business areas

Risk types

Data sources

Scenario risk drivers

Frequency

Severity

Loss Amount

Recovery

Return time

Assumptions formulation

Worst case

Baseline

Best case

Scenario

WRITING SCENARIOS ALGO

Defining and structuring the task, specifying the area of

WRITING SCENARIOS ALGO

Defining and structuring the task, specifying the area of

WHAT SCENARIOS ARE RELEVANT?

Frequency

Loss severity

High

Low

High

Low

RCSA

Key risk indicators

Audit findings

Internal loss data

External loss

WHAT SCENARIOS ARE RELEVANT?

Frequency

Loss severity

High

Low

High

Low

RCSA

Key risk indicators

Audit findings

Internal loss data

External loss

FORWARD-LOOKING FOCUS

Internal / External loss database

Past-looking

RCSA / KRI

Current performance

Scenario Analysis

Forward-looking

Scenario data

FORWARD-LOOKING FOCUS

Internal / External loss database

Past-looking

RCSA / KRI

Current performance

Scenario Analysis

Forward-looking

Scenario data

SOURCE: Observed range of practice in key elements of Advanced Measurement

SOURCE: Observed range of practice in key elements of Advanced Measurement

SOURCE: Observed range of practice in key elements of Advanced Measurement

SOURCE: Observed range of practice in key elements of Advanced Measurement

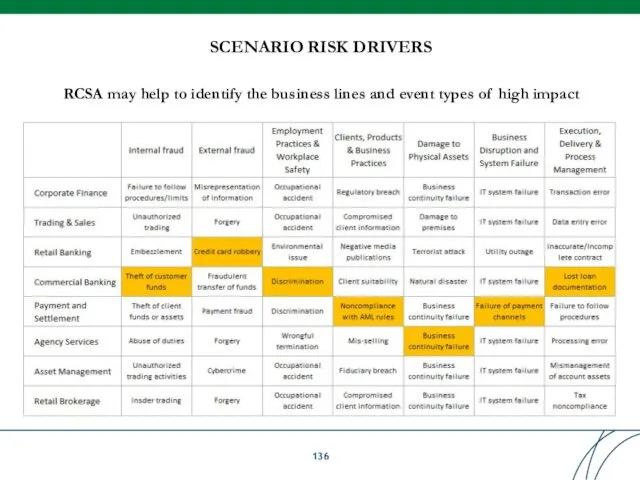

SCENARIO RISK DRIVERS

RCSA may help to identify the business lines and

SCENARIO RISK DRIVERS

RCSA may help to identify the business lines and

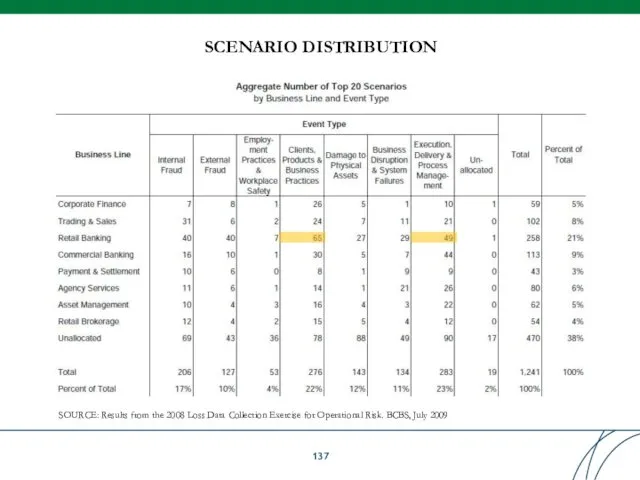

SCENARIO DISTRIBUTION

SOURCE: Results from the 2008 Loss Data Collection Exercise for

SCENARIO DISTRIBUTION

SOURCE: Results from the 2008 Loss Data Collection Exercise for

HIGH SEVERITY SCENARIO EXAMPLES

Large loan or card fraud (internal / external)

High-scale

HIGH SEVERITY SCENARIO EXAMPLES

Large loan or card fraud (internal / external)

High-scale

SCENARIO PARAMETERS

SCENARIO PARAMETERS

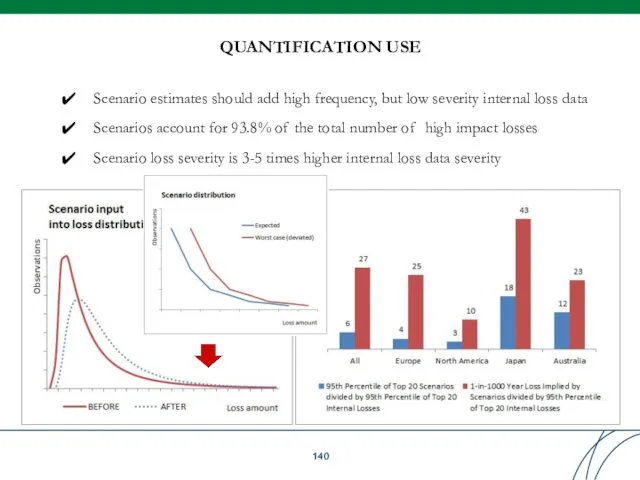

QUANTIFICATION USE

Scenario estimates should add high frequency, but low severity internal

QUANTIFICATION USE

Scenario estimates should add high frequency, but low severity internal

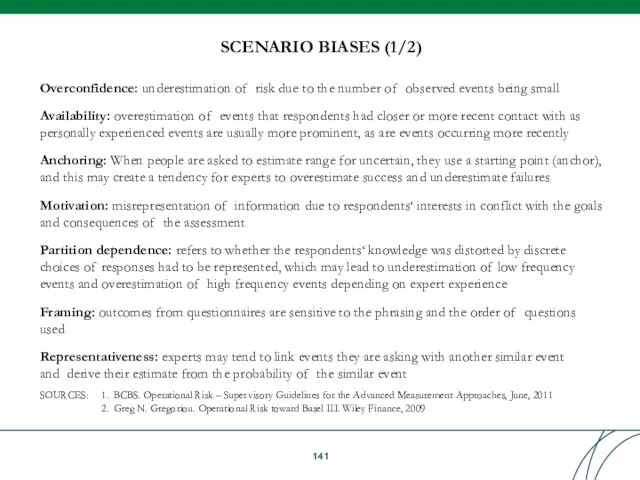

Overconfidence: underestimation of risk due to the number of observed events

Overconfidence: underestimation of risk due to the number of observed events

Banks are likely to deviate from true risk estimate due to

Banks are likely to deviate from true risk estimate due to

Established scenario framework should ensure the integrity and consistency of the

Established scenario framework should ensure the integrity and consistency of the

Table of Contents

Table of Contents

Table of Contents

Table of Contents

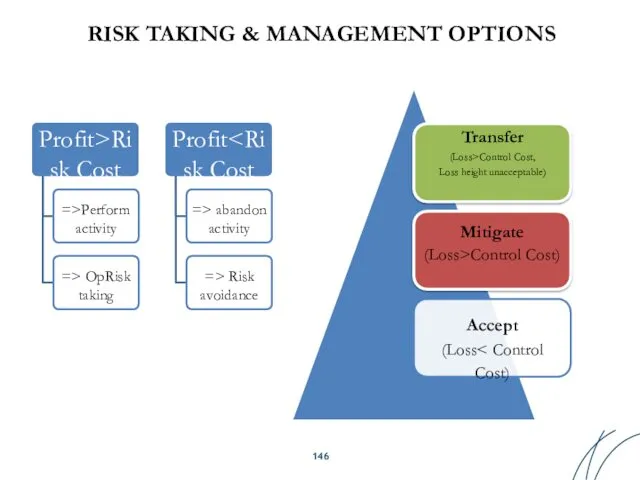

RISK TAKING & MANAGEMENT OPTIONS

Profit>Ri sk Cost

=>Perform activity

=> OpRisk taking

Profit

RISK TAKING & MANAGEMENT OPTIONS

Profit>Ri sk Cost

=>Perform activity

=> OpRisk taking

Profit

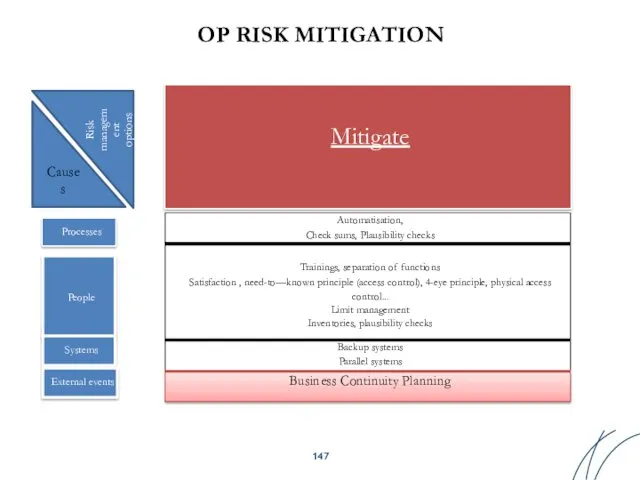

Processes

People

Systems

External events

OP RISK MITIGATION

Mitigate

Cause s

Risk

managem ent options

Processes

People

Systems

External events

OP RISK MITIGATION

Mitigate

Cause s

Risk

managem ent options

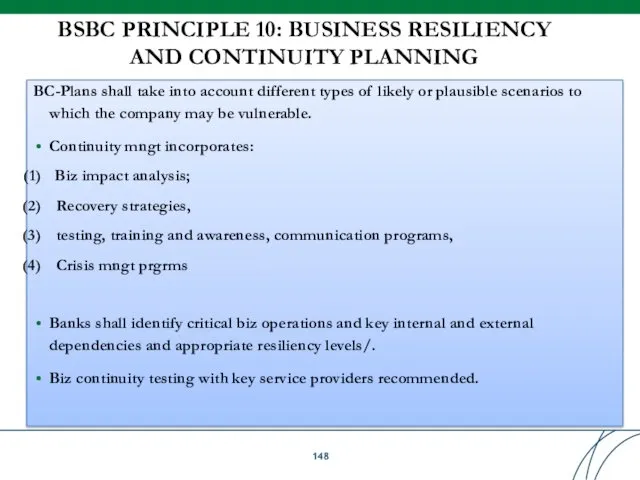

BSBC PRINCIPLE 10: BUSINESS RESILIENCY

AND CONTINUITY PLANNING

BC-Plans shall take into account

BSBC PRINCIPLE 10: BUSINESS RESILIENCY

AND CONTINUITY PLANNING

BC-Plans shall take into account

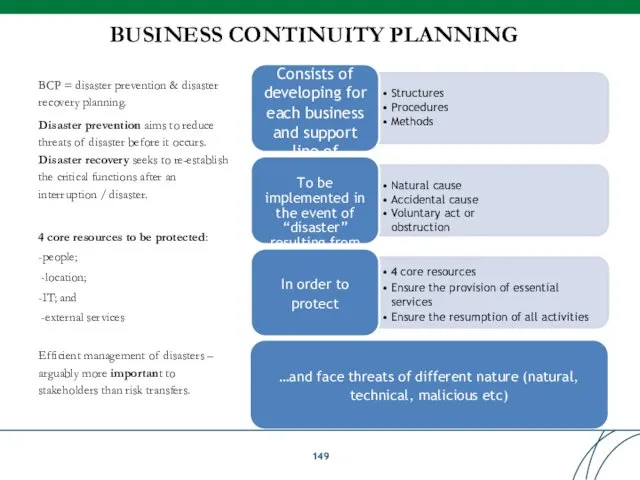

BUSINESS CONTINUITY PLANNING

BCP = disaster prevention & disaster recovery planning.

Disaster prevention

BUSINESS CONTINUITY PLANNING

BCP = disaster prevention & disaster recovery planning.

Disaster prevention

BCP PHASING

-

Phase 1: Project Planning

Identify

disaster

scenarios to

be addressed

- Develop Standards and Procedures.

- Establish

and obtain

approval on

BCP PHASING

-

Phase 1: Project Planning

Identify

disaster

scenarios to

be addressed

- Develop Standards and Procedures.

- Establish

and obtain

approval on

BCP SCENARIO/RISK ANALYSIS BASED

Scenario & Risk Analysis

Health Check of Physical &

BCP SCENARIO/RISK ANALYSIS BASED

Scenario & Risk Analysis

Health Check of Physical &

CRISIS MANAGEMENT STRUCTURE

CRISIS MANAGEMENT STRUCTURE

PERIODIC BCP CHECKS

BCP ought to fit the activity, prioritizing the core

PERIODIC BCP CHECKS

BCP ought to fit the activity, prioritizing the core

BCP TIPS

Simple preventive measures – geographic dispersion of intellectual capital;

Implement alternative

BCP TIPS

Simple preventive measures – geographic dispersion of intellectual capital;

Implement alternative

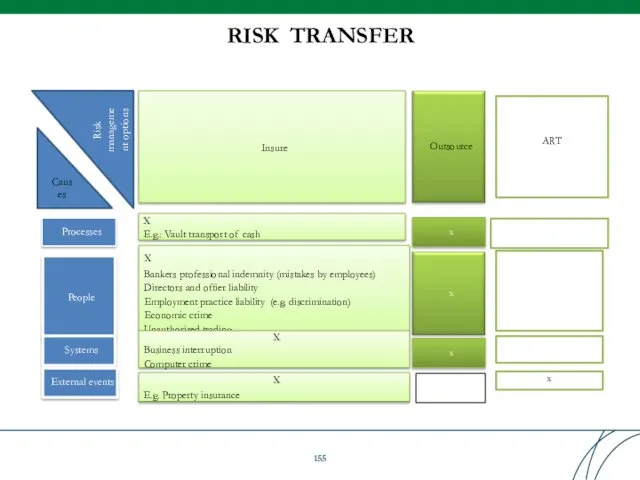

Processes

People

Systems

External events

Insure

X

E.g.: Vault transport of cash

X

Bankers professional indemnity (mistakes by employees)

Processes

People

Systems

External events

Insure

X

E.g.: Vault transport of cash

X

Bankers professional indemnity (mistakes by employees)

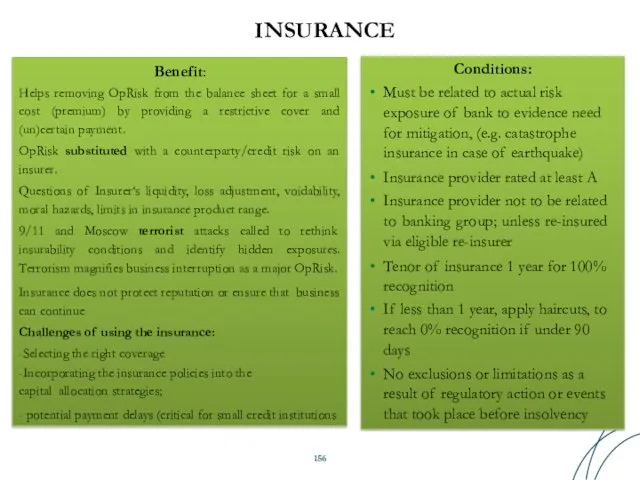

INSURANCE

Conditions:

Must be related to actual risk exposure of bank to evidence

INSURANCE

Conditions:

Must be related to actual risk exposure of bank to evidence

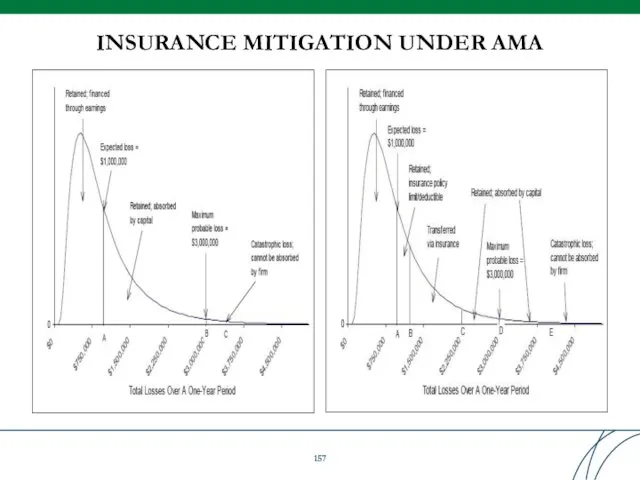

INSURANCE MITIGATION UNDER AMA

INSURANCE MITIGATION UNDER AMA

OUTSOURCING RISKS

Op Risk Outsourcing drivers

Cost reduction

Higher process quality

Risk sharing/ transfer

Benefits from

OUTSOURCING RISKS

Op Risk Outsourcing drivers

Cost reduction

Higher process quality

Risk sharing/ transfer

Benefits from

COMPETITIVE EDGE –OUTSOURCING IS NOT

OR-FREE

“Prudent Outsourcer” Rules

The final responsibility towards clients

COMPETITIVE EDGE –OUTSOURCING IS NOT

OR-FREE

“Prudent Outsourcer” Rules

The final responsibility towards clients

ART

(Alternative Risk Transfer)

Regulators concerns:

-Complex voidance clauses

narrowly defined insured / risk events

Limitations

-Absence of historical data

Imperfect

ART

(Alternative Risk Transfer)

Regulators concerns:

-Complex voidance clauses

narrowly defined insured / risk events

Limitations

-Absence of historical data

Imperfect

Table of Contents

Table of Contents

OpRisk CORPORATE GOVERNANCE

Clear org structure with defined lines of responsibility

Hierarchic decision-

OpRisk CORPORATE GOVERNANCE

Clear org structure with defined lines of responsibility

Hierarchic decision-

RISK GOVERNANCE: 3 (4) LINES OF DEFENSE

Role of Supervisors

-Conduct regular independent

RISK GOVERNANCE: 3 (4) LINES OF DEFENSE

Role of Supervisors

-Conduct regular independent

RISK MANAGEMENT ORGANIZATION

RISK MANAGEMENT ORGANIZATION

OpRisk GOVERNANCE INTERNAL STRUCTURE

1. Supervisory Board

Responsible to implement risk mgnt strategy

Approves

OpRisk GOVERNANCE INTERNAL STRUCTURE

1. Supervisory Board

Responsible to implement risk mgnt strategy

Approves

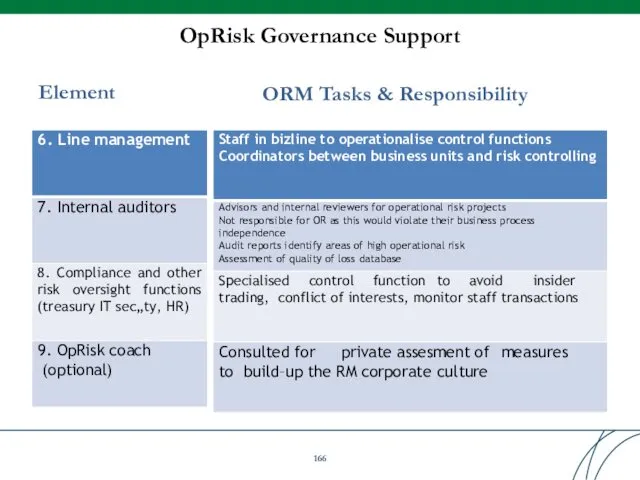

OpRisk Governance Support

Element

ORM Tasks & Responsibility

OpRisk Governance Support

Element

ORM Tasks & Responsibility

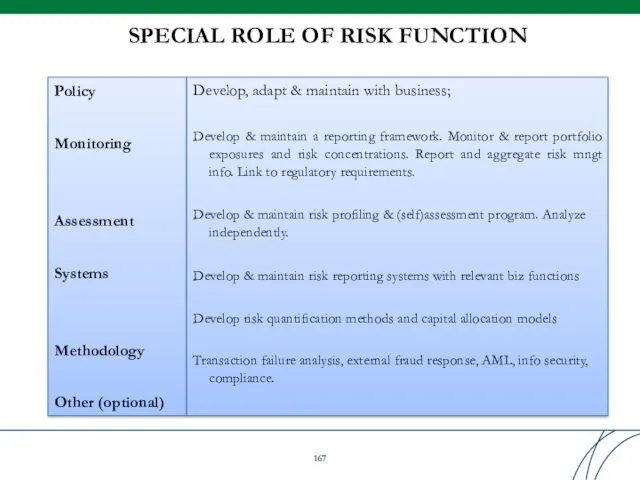

SPECIAL ROLE OF RISK FUNCTION

Policy

Monitoring

Assessment

Systems

Methodology

Other (optional)

Develop, adapt & maintain with business;

Develop

SPECIAL ROLE OF RISK FUNCTION

Policy

Monitoring

Assessment

Systems

Methodology

Other (optional)

Develop, adapt & maintain with business;

Develop

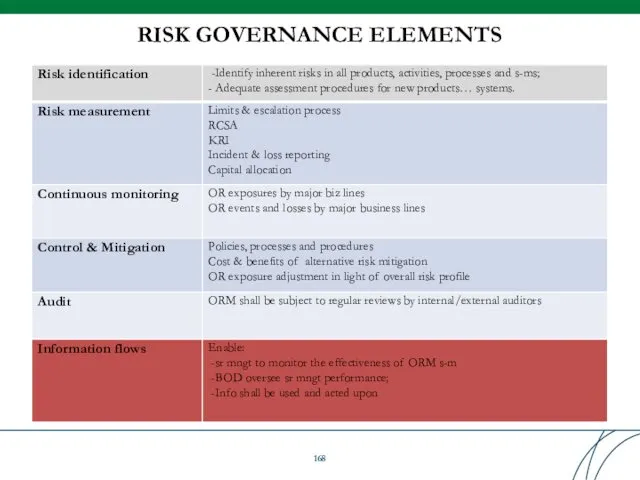

RISK GOVERNANCE ELEMENTS

RISK GOVERNANCE ELEMENTS

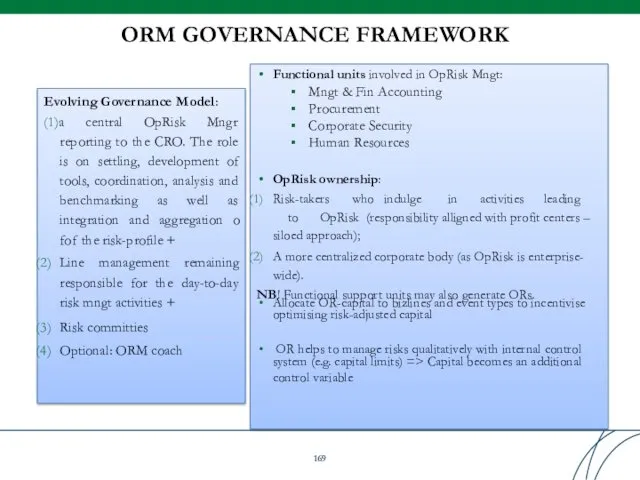

ORM GOVERNANCE FRAMEWORK

Evolving Governance Model:

(1)a central OpRisk Mngr reporting to the

ORM GOVERNANCE FRAMEWORK

Evolving Governance Model:

(1)a central OpRisk Mngr reporting to the

OR GOVERNANCE STRUCTURE: DB EXAMPLE

Head

Risk Committee(s)

initiates

Line management

ORM function

Audit Compliance

CRO

OR GOVERNANCE STRUCTURE: DB EXAMPLE

Head

Risk Committee(s)

initiates

Line management

ORM function

Audit Compliance

CRO

DISCLOSURE TO EXTERNAL STAKEHOLDERS

-Meet rating agency expectations (ORM assessment form part of their

DISCLOSURE TO EXTERNAL STAKEHOLDERS

-Meet rating agency expectations (ORM assessment form part of their

RULES OF STAKEHOLDER ENGAGEMENT

❑Do internal (“machine room”) and external (context) intelligence;

❑Communication

RULES OF STAKEHOLDER ENGAGEMENT

❑Do internal (“machine room”) and external (context) intelligence;

❑Communication

- Who are your stakeholders?

-What’s your Symbol (Brand, Reputation)?

- Is it

- Who are your stakeholders?

-What’s your Symbol (Brand, Reputation)?

- Is it

BENEFITS OF OR GOVERNANCE

✔ Reduction of operational losses;

✔ Improved business and performance management;

✔Protection against loss of

BENEFITS OF OR GOVERNANCE

✔ Reduction of operational losses;

✔ Improved business and performance management;

✔Protection against loss of

ORM IS SIMPLY GOOD CORPORATE

GOVERNANCE

Good ORM

Fewer Surprises

Increased

shareholder value

ORM IS SIMPLY GOOD CORPORATE

GOVERNANCE

Good ORM

Fewer Surprises

Increased

shareholder value

Table of Contents

Table of Contents

Contact information

INTERNATIONAL FINANCE CORPORATION (IFC)

Bank Advisory Program

Central Asia and Eastern Europe

Yevgeni

Contact information

INTERNATIONAL FINANCE CORPORATION (IFC)

Bank Advisory Program

Central Asia and Eastern Europe

Yevgeni

Стратегический менеджмент в образовании: формирование стратегического плана школы

Стратегический менеджмент в образовании: формирование стратегического плана школы Трудовые ресурсы предприятия. (Тема 8)

Трудовые ресурсы предприятия. (Тема 8) Менеджмент качества образования в высшей школе

Менеджмент качества образования в высшей школе Методы и формы управления в гостиничном бизнесе

Методы и формы управления в гостиничном бизнесе Мировые управленческие концепции. Американская, европейская, японская и российская модели менеджмента

Мировые управленческие концепции. Американская, европейская, японская и российская модели менеджмента How managers can make a decision in an uncertainty environment?

How managers can make a decision in an uncertainty environment? Time management. How to do everything

Time management. How to do everything Система внутреннего контроля современного предприятия

Система внутреннего контроля современного предприятия Оценка использования трудовых ресурсов и обоснование путей их улучшения ОАО Витебские ковры

Оценка использования трудовых ресурсов и обоснование путей их улучшения ОАО Витебские ковры Основы управления качеством и оценки соответствия

Основы управления качеством и оценки соответствия Организационный план. Персонал

Организационный план. Персонал Анализ кадровой политики ОАО РУСАЛ-ИркАЗ

Анализ кадровой политики ОАО РУСАЛ-ИркАЗ Совершенствование процесса адаптации персонала на предприятии на примере строительной организации ООО Застройщик

Совершенствование процесса адаптации персонала на предприятии на примере строительной организации ООО Застройщик Обще́ственное пита́ние

Обще́ственное пита́ние Теория поведения человека в организации

Теория поведения человека в организации Практическое задание по менеджменту

Практическое задание по менеджменту Вероятностные модели управления запасами

Вероятностные модели управления запасами Етапи процесу прийняття рішення

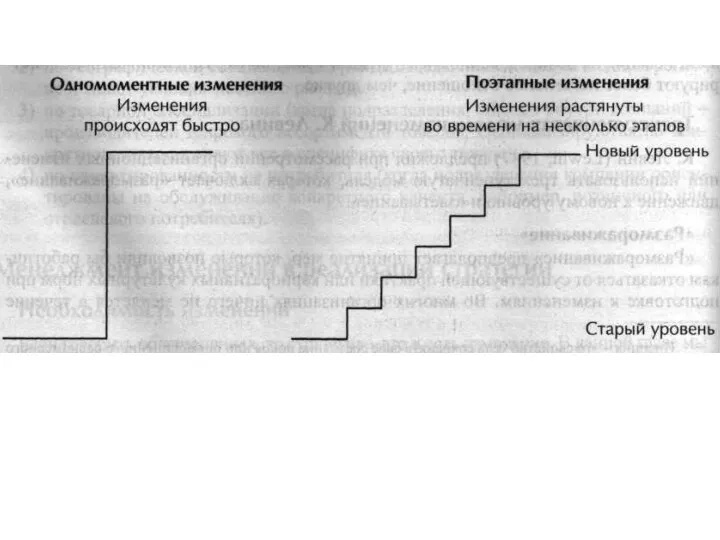

Етапи процесу прийняття рішення Изменения в организации и расходование ресурсов

Изменения в организации и расходование ресурсов Проект тайный ангел

Проект тайный ангел Экспертные методы оценки рисков

Экспертные методы оценки рисков Стратегический менеджмент

Стратегический менеджмент Школа менеджеров

Школа менеджеров Реинжиниринг бизнес-процессов. Основные концепции улучшения бизнес-процессов. (Тема 1)

Реинжиниринг бизнес-процессов. Основные концепции улучшения бизнес-процессов. (Тема 1) Понятие стратегического менеджмента

Понятие стратегического менеджмента Управление научными исследованиями и разработками. Разработки новых продуктов и технологий

Управление научными исследованиями и разработками. Разработки новых продуктов и технологий Оценка персонала компании

Оценка персонала компании Види туроперейтингу

Види туроперейтингу