- Insurance. Company. Operations

Содержание

- 2. Agenda Rating and Ratemaking Underwriting Production Claim settlement Reinsurance Investments

- 3. Rating and Ratemaking Ratemaking refers to the pricing of insurance and the calculation of insurance premiums

- 4. Underwriting Underwriting refers to the process of selecting, classifying, and pricing applicants for insurance A statement

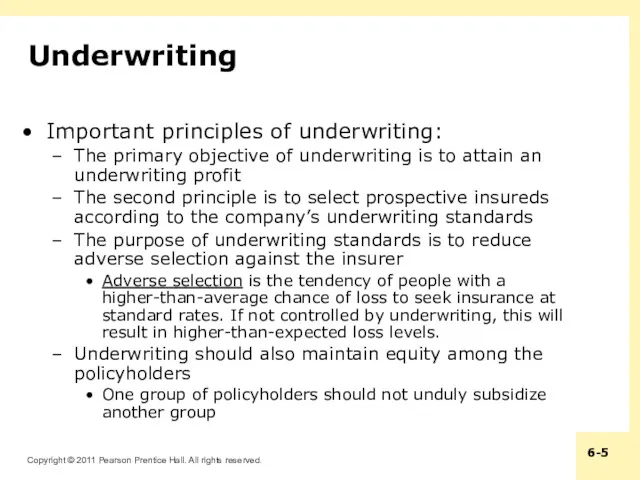

- 5. Underwriting Important principles of underwriting: The primary objective of underwriting is to attain an underwriting profit

- 6. Underwriting Underwriting starts with the agent in the field Information for underwriting comes from: The application

- 7. Production Production refers to the sales and marketing activities of insurers Agents are often referred to

- 8. Claim Settlement The objectives of claims settlement include: Verification of a covered loss Fair and prompt

- 9. Claim Settlement The claim process begins with a notice of loss Next, the claim is investigated

- 10. Reinsurance Reinsurance is an arrangement by which the primary insurer that initially writes the insurance transfers

- 11. Reinsurance Reinsurance is used to: Increase underwriting capacity Stabilize profits Reduce the unearned premium reserve The

- 12. Types of Reinsurance Agreements There are two principal forms of reinsurance: Facultative reinsurance is an optional,

- 13. Methods for Sharing Losses There are two basic methods for sharing losses: Under the Pro rata

- 14. Reinsurance Alternatives Some insurers use the capital markets as an alternative to traditional reinsurance Securitization of

- 15. Investments Because premiums are paid in advance, they can be invested until needed to pay claims

- 16. Exhibit 6.1 Growth of Life Insurers’ Assets

- 17. Exhibit 6.2 Asset Distribution of Life Insurers 2007

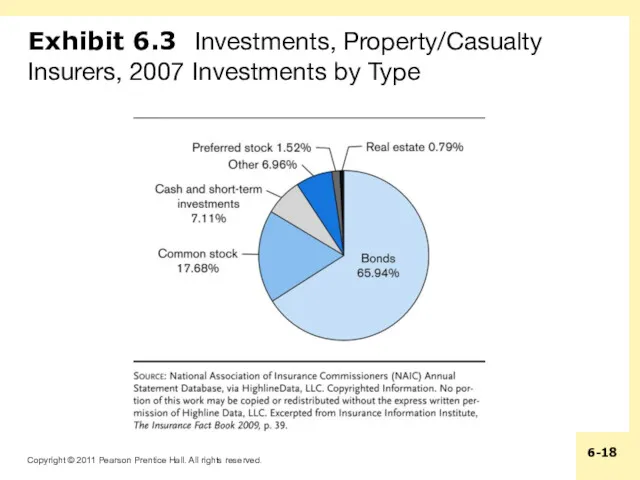

- 18. Exhibit 6.3 Investments, Property/Casualty Insurers, 2007 Investments by Type

- 20. Скачать презентацию

Agenda

Rating and Ratemaking

Underwriting

Production

Claim settlement

Reinsurance

Investments

Agenda

Rating and Ratemaking

Underwriting

Production

Claim settlement

Reinsurance

Investments

Rating and Ratemaking

Ratemaking refers to the pricing of insurance and the

Rating and Ratemaking

Ratemaking refers to the pricing of insurance and the

Underwriting

Underwriting refers to the process of selecting, classifying, and pricing applicants

Underwriting

Underwriting refers to the process of selecting, classifying, and pricing applicants

Underwriting

Important principles of underwriting:

The primary objective of underwriting is to attain

Underwriting

Important principles of underwriting:

The primary objective of underwriting is to attain

Underwriting

Underwriting starts with the agent in the field

Information for underwriting comes

Underwriting

Underwriting starts with the agent in the field

Information for underwriting comes

Production

Production refers to the sales and marketing activities of insurers

Agents are

Production

Production refers to the sales and marketing activities of insurers

Agents are

Claim Settlement

The objectives of claims settlement include:

Verification of a covered loss

Fair

Claim Settlement

The objectives of claims settlement include:

Verification of a covered loss

Fair

Claim Settlement

The claim process begins with a notice of loss

Next, the

Claim Settlement

The claim process begins with a notice of loss

Next, the

Reinsurance

Reinsurance is an arrangement by which the primary insurer that initially

Reinsurance

Reinsurance is an arrangement by which the primary insurer that initially

Reinsurance

Reinsurance is used to:

Increase underwriting capacity

Stabilize profits

Reduce the unearned premium reserve

The

Reinsurance

Reinsurance is used to:

Increase underwriting capacity

Stabilize profits

Reduce the unearned premium reserve

The

Types of Reinsurance Agreements

There are two principal forms of reinsurance:

Facultative reinsurance

Types of Reinsurance Agreements

There are two principal forms of reinsurance:

Facultative reinsurance

Methods for Sharing Losses

There are two basic methods for sharing losses:

Under

Methods for Sharing Losses

There are two basic methods for sharing losses:

Under

Reinsurance Alternatives

Some insurers use the capital markets as an alternative to

Reinsurance Alternatives

Some insurers use the capital markets as an alternative to

Investments

Because premiums are paid in advance, they can be invested until

Investments

Because premiums are paid in advance, they can be invested until

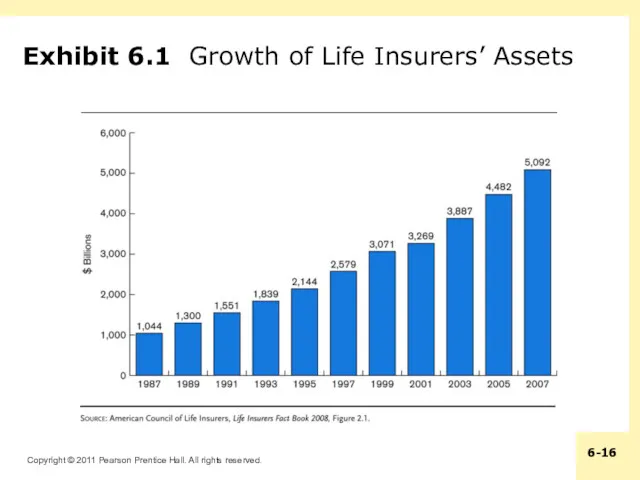

Exhibit 6.1 Growth of Life Insurers’ Assets

Exhibit 6.1 Growth of Life Insurers’ Assets

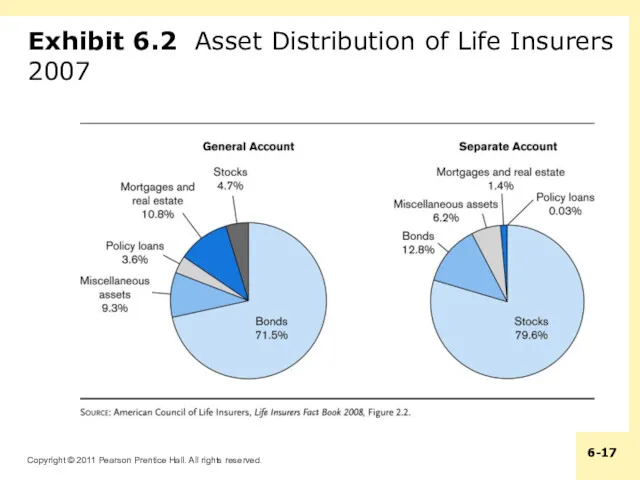

Exhibit 6.2 Asset Distribution of Life Insurers 2007

Exhibit 6.2 Asset Distribution of Life Insurers 2007

Exhibit 6.3 Investments, Property/Casualty Insurers, 2007 Investments by Type

Exhibit 6.3 Investments, Property/Casualty Insurers, 2007 Investments by Type

Анализ движения денежных потоков организации

Анализ движения денежных потоков организации Cost-Volume-Profit (CVP) Analysis

Cost-Volume-Profit (CVP) Analysis Социальный предприниматель

Социальный предприниматель Консолидированный бюджет и его значение

Консолидированный бюджет и его значение Бухгалтерский учет, анализ и управление основным капиталом предприятия

Бухгалтерский учет, анализ и управление основным капиталом предприятия Учет и отражение в отчетности финансовых инструментов

Учет и отражение в отчетности финансовых инструментов Выборочный контроль по альтернативным признакам

Выборочный контроль по альтернативным признакам Меры поддержки субъектов МСП

Меры поддержки субъектов МСП Бухгалтерский учет и анализ основных средств организации ооо Лагуна

Бухгалтерский учет и анализ основных средств организации ооо Лагуна Как увеличить денежный поток

Как увеличить денежный поток Таможенное декларирование товаров (тема 5)

Таможенное декларирование товаров (тема 5) Оцінка фінансового стану підприємства та шляхи його зміцнення

Оцінка фінансового стану підприємства та шляхи його зміцнення Финансы домашних хозяйств. Финансы и кредит

Финансы домашних хозяйств. Финансы и кредит Налоги, их виды и функции

Налоги, их виды и функции Единый налоговый платеж. Основные термины и понятия

Единый налоговый платеж. Основные термины и понятия Инвестиционные проекты и оценка их эффективности

Инвестиционные проекты и оценка их эффективности Сущность, функции, принципы финансового планирования

Сущность, функции, принципы финансового планирования Базовые и производные ценные бумаги

Базовые и производные ценные бумаги Автокредитование. Банковская группа Зенит

Автокредитование. Банковская группа Зенит Исполнение бюджета Юрьевецкого городского поселения

Исполнение бюджета Юрьевецкого городского поселения Центральный банк РФ

Центральный банк РФ Продажа программы Идеальный заемщик

Продажа программы Идеальный заемщик Определение рыночной стоимости объекта недвижимости на примере одноэтажного бревенчатого дома

Определение рыночной стоимости объекта недвижимости на примере одноэтажного бревенчатого дома Сущность и функции денег

Сущность и функции денег The financial market environment. (Chapter 2)

The financial market environment. (Chapter 2) Специальные налоговые режимы

Специальные налоговые режимы Кредитная и банковская системы

Кредитная и банковская системы Функционально-стоимостный анализ бизнес-процессов

Функционально-стоимостный анализ бизнес-процессов