- The financial market environment. (Chapter 2)

Содержание

- 2. Financial Institutions & Markets Firms that require funds from external sources can obtain them in three

- 3. Financial Institutions & Markets: Financial Institutions Financial institutions are intermediaries that channel the savings of individuals,

- 4. Commercial Banks, Investment Banks, and the Shadow Banking System Commercial banks are institutions that: provide savers

- 5. Commercial Banks, Investment Banks, and the Shadow Banking System (cont.) The Glass-Steagall Act was an act

- 6. Matter of Fact Consolidation in the U.S. Banking Industry: The U.S. banking industry has been going

- 7. Financial Institutions & Markets: Financial Markets Financial markets are forums in which suppliers of funds and

- 8. Financial Institutions & Markets: Financial Markets (cont.) The primary market is the financial market in which

- 9. Figure 2.1 Flow of Funds

- 10. The Money Market The money market is created by a financial relationship between suppliers and demanders

- 11. The Money Market (cont.) The international equivalent of the domestic (U.S.) money market is the Eurocurrency

- 12. The Capital Market The capital market is a market that enables suppliers and demanders of long-term

- 13. The Capital Market Lakeview Industries, a major microprocessor manufacturer, has issued a 9 percent coupon interest

- 14. Focus on Practice Berkshire Hathaway – Can Buffett Be Replaced? Since the early 1980s, Berkshire Hathaway’s

- 15. Broker Markets and Dealer Markets Broker markets are securities exchanges on which the two sides of

- 16. Broker Markets and Dealer Markets (cont.) Dealer markets, such as Nasdaq, are markets in which the

- 17. Matter of Fact According to the World Federation of Exchanges, in 2012: NYSE Euronext is the

- 18. International Capital Markets In the Eurobond market, corporations and governments typically issue bonds denominated in dollars

- 19. The Role of Capital Markets From a firm’s perspective, the role of capital markets is to

- 20. The Role of Capital Markets (cont.) Advocates of behavioral finance, an emerging field that blends ideas

- 21. Focus on Ethics The Ethics of Insider Trading Bryan Shaw received inside information on Herbalife and

- 22. The Financial Crisis: Financial Institutions and Real Estate Finance Securitization is the process of pooling mortgages

- 23. The Financial Crisis: Falling Home Prices and Delinquent Mortgages Rising home prices between 1987 and 2006

- 24. The Financial Crisis: Falling Home Prices and Delinquent Mortgages Figure 2.2 House Prices Soar and then

- 25. The Financial Crisis: Crisis of Confidence in Banks The price of bank stocks fell 81% between

- 26. The Financial Crisis: Crisis of Confidence in Banks Figure 2.3 Bank Stocks Plummet During Financial Crisis

- 27. The Financial Crisis: Spillover Effects and the Great Recession As banks came under intense financial pressure

- 28. Regulation of Financial Institutions and Markets: Regulations Governing Financial Institutions The Glass-Steagall Act (1933) established the

- 29. Regulation of Financial Institutions and Markets: Regulations Governing Financial Institutions The Gramm-Leach-Bliley Act (1999) allows business

- 30. Regulation of Financial Institutions and Markets: Regulations Governing Financial Markets The Securities Act of 1933 regulates

- 31. Business Taxes Both individuals and businesses must pay taxes on income. The income of sole proprietorships

- 32. Table 2.1 Corporate Tax Rate Schedule

- 33. Business Taxes: Ordinary Income Ordinary income is earned through the sale of a firm’s goods or

- 34. Business Taxation: Marginal versus Average Tax Rates A firm’s marginal tax rate represents the rate at

- 35. Business Taxation: Interest and Dividend Income For corporations only, 70% of all dividend income received from

- 36. Business Taxation: Tax-Deductible Expenses In calculating taxes, corporations may deduct operating expenses and interest expense but

- 37. Business Taxation: Tax-Deductible Expenses (cont.)

- 38. Business Taxation: Tax-Deductible Expenses (cont.) As the example shows, the use of debt financing can increase

- 39. Business Taxation: Capital Gains A capital gain is the amount by which the sale price of

- 40. Review of Learning Goals LG1 Understand the role that financial institutions play in managerial finance. Financial

- 41. Review of Learning Goals (cont.) LG3 Describe the differences between the capital markets and the money

- 42. Review of Learning Goals (cont.) LG5 Understand the major regulations and regulatory bodies that affect financial

- 43. Review of Learning Goals (cont.) LG6 Discuss business taxes and their importance in financial decisions. Corporate

- 44. Chapter Resources on MyFinanceLab Chapter Cases Group Exercises Critical Thinking Problems

- 45. Integrative Case: Merit Enterprise Corp. Merit Enterprise Corporation’s CEO would like to dramatically expand the company’s

- 46. Integrative Case: Merit Enterprise Corp. Option 1 – Merit could approach JPMorgan Chase, a bank that

- 47. Integrative Case: Merit Enterprise Corp. Option 2 – Merit could convert to public ownership, issuing stock

- 49. Скачать презентацию

Financial Institutions & Markets

Firms that require funds from external sources can

Financial Institutions & Markets

Firms that require funds from external sources can

Financial Institutions & Markets: Financial Institutions

Financial institutions are intermediaries that channel

Financial Institutions & Markets: Financial Institutions

Financial institutions are intermediaries that channel

Commercial Banks, Investment Banks, and the Shadow Banking System

Commercial banks are

Commercial Banks, Investment Banks, and the Shadow Banking System

Commercial banks are

Commercial Banks, Investment Banks, and the Shadow Banking System (cont.)

The Glass-Steagall

Commercial Banks, Investment Banks, and the Shadow Banking System (cont.)

The Glass-Steagall

Matter of Fact

Consolidation in the U.S. Banking Industry:

The U.S. banking industry

Matter of Fact

Consolidation in the U.S. Banking Industry:

The U.S. banking industry

Financial Institutions & Markets: Financial Markets

Financial markets are forums in which

Financial Institutions & Markets: Financial Markets

Financial markets are forums in which

Financial Institutions & Markets: Financial Markets (cont.)

The primary market is the

Financial Institutions & Markets: Financial Markets (cont.)

The primary market is the

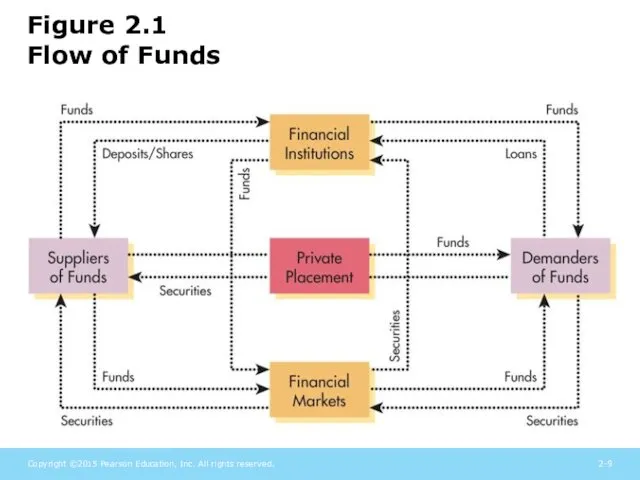

Figure 2.1

Flow of Funds

Figure 2.1

Flow of Funds

The Money Market

The money market is created by a financial relationship

The Money Market

The money market is created by a financial relationship

The Money Market (cont.)

The international equivalent of the domestic (U.S.) money

The Money Market (cont.)

The international equivalent of the domestic (U.S.) money

The Capital Market

The capital market is a market that enables suppliers

The Capital Market

The capital market is a market that enables suppliers

The Capital Market

Lakeview Industries, a major microprocessor manufacturer, has issued a

The Capital Market

Lakeview Industries, a major microprocessor manufacturer, has issued a

Focus on Practice

Berkshire Hathaway – Can Buffett Be Replaced?

Since the early

Focus on Practice

Berkshire Hathaway – Can Buffett Be Replaced?

Since the early

Broker Markets and

Dealer Markets

Broker markets are securities exchanges on which

Broker Markets and

Dealer Markets

Broker markets are securities exchanges on which

Broker Markets and

Dealer Markets (cont.)

Dealer markets, such as Nasdaq, are

Broker Markets and

Dealer Markets (cont.)

Dealer markets, such as Nasdaq, are

Matter of Fact

According to the World Federation of Exchanges, in 2012:

NYSE

Matter of Fact

According to the World Federation of Exchanges, in 2012:

NYSE

International Capital Markets

In the Eurobond market, corporations and governments typically issue

International Capital Markets

In the Eurobond market, corporations and governments typically issue

The Role of Capital Markets

From a firm’s perspective, the role of

The Role of Capital Markets

From a firm’s perspective, the role of

The Role of Capital Markets (cont.)

Advocates of behavioral finance, an emerging

The Role of Capital Markets (cont.)

Advocates of behavioral finance, an emerging

Focus on Ethics

The Ethics of Insider Trading

Bryan Shaw received inside information

Focus on Ethics

The Ethics of Insider Trading

Bryan Shaw received inside information

The Financial Crisis: Financial Institutions and Real Estate Finance

Securitization is the

The Financial Crisis: Financial Institutions and Real Estate Finance

Securitization is the

The Financial Crisis: Falling Home Prices and Delinquent Mortgages

Rising home prices

The Financial Crisis: Falling Home Prices and Delinquent Mortgages

Rising home prices

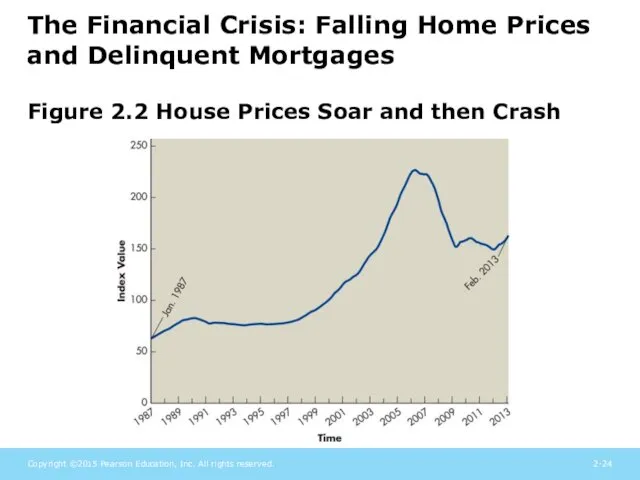

The Financial Crisis: Falling Home Prices and Delinquent Mortgages

Figure 2.2 House

The Financial Crisis: Falling Home Prices and Delinquent Mortgages

Figure 2.2 House

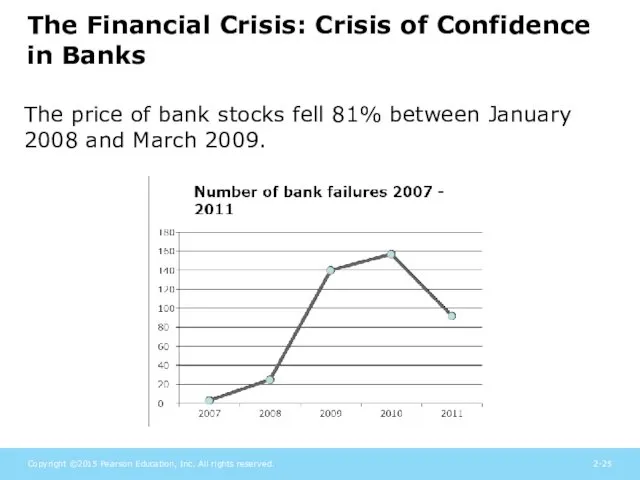

The Financial Crisis: Crisis of Confidence in Banks

The price of bank

The Financial Crisis: Crisis of Confidence in Banks

The price of bank

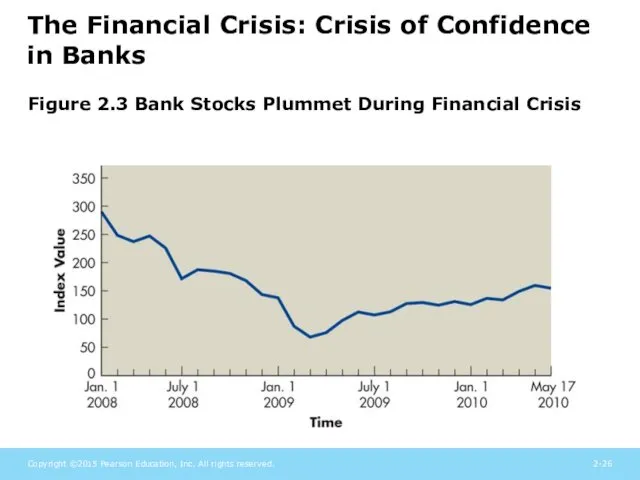

The Financial Crisis: Crisis of Confidence in Banks

Figure 2.3 Bank Stocks

The Financial Crisis: Crisis of Confidence in Banks

Figure 2.3 Bank Stocks

The Financial Crisis: Spillover Effects and the Great Recession

As banks came

The Financial Crisis: Spillover Effects and the Great Recession

As banks came

Regulation of Financial Institutions and Markets: Regulations Governing Financial Institutions

The Glass-Steagall

Regulation of Financial Institutions and Markets: Regulations Governing Financial Institutions

The Glass-Steagall

Regulation of Financial Institutions and Markets: Regulations Governing Financial Institutions

The Gramm-Leach-Bliley

Regulation of Financial Institutions and Markets: Regulations Governing Financial Institutions

The Gramm-Leach-Bliley

Regulation of Financial Institutions and Markets: Regulations Governing Financial Markets

The Securities

Regulation of Financial Institutions and Markets: Regulations Governing Financial Markets

The Securities

Business Taxes

Both individuals and businesses must pay taxes on income.

The income

Business Taxes

Both individuals and businesses must pay taxes on income.

The income

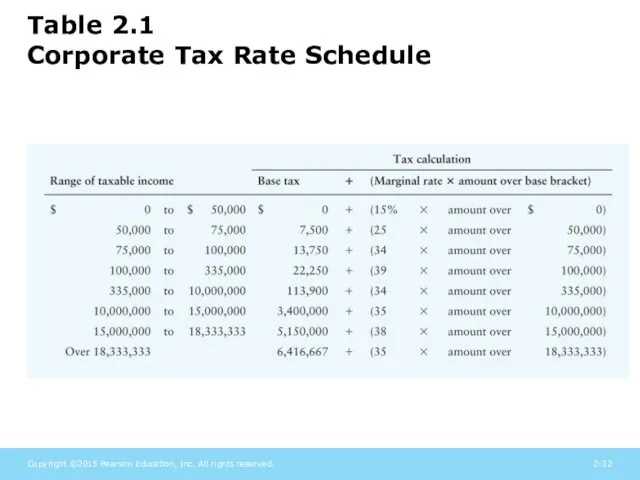

Table 2.1

Corporate Tax Rate Schedule

Table 2.1

Corporate Tax Rate Schedule

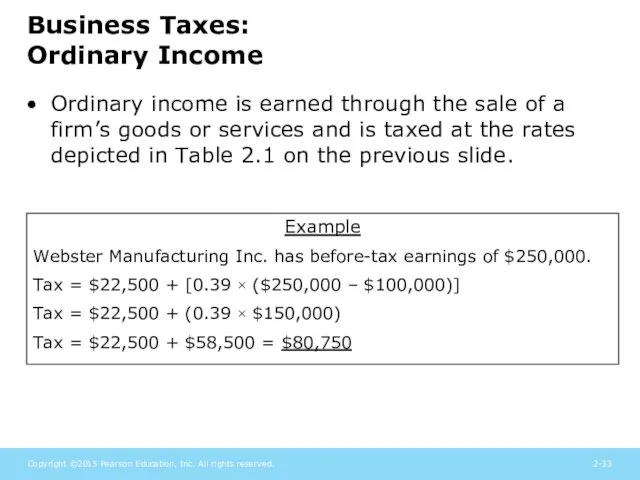

Business Taxes:

Ordinary Income

Ordinary income is earned through the sale of

Business Taxes:

Ordinary Income

Ordinary income is earned through the sale of

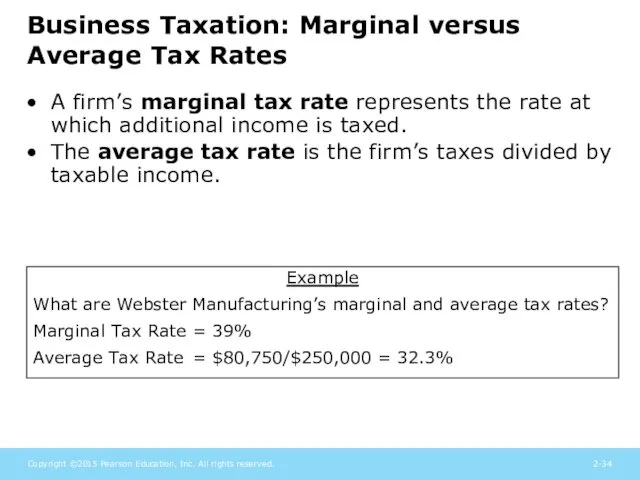

Business Taxation: Marginal versus Average Tax Rates

A firm’s marginal tax rate

Business Taxation: Marginal versus Average Tax Rates

A firm’s marginal tax rate

Business Taxation:

Interest and Dividend Income

For corporations only, 70% of all

Business Taxation:

Interest and Dividend Income

For corporations only, 70% of all

Business Taxation:

Tax-Deductible Expenses

In calculating taxes, corporations may deduct operating expenses

Business Taxation:

Tax-Deductible Expenses

In calculating taxes, corporations may deduct operating expenses

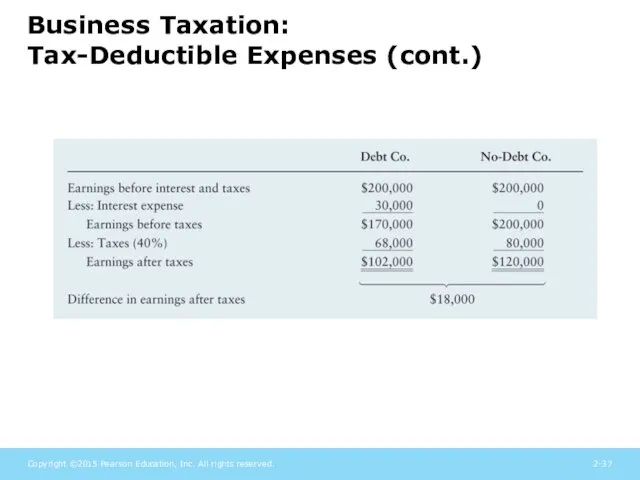

Business Taxation:

Tax-Deductible Expenses (cont.)

Business Taxation:

Tax-Deductible Expenses (cont.)

Business Taxation:

Tax-Deductible Expenses (cont.)

As the example shows, the use of

Business Taxation:

Tax-Deductible Expenses (cont.)

As the example shows, the use of

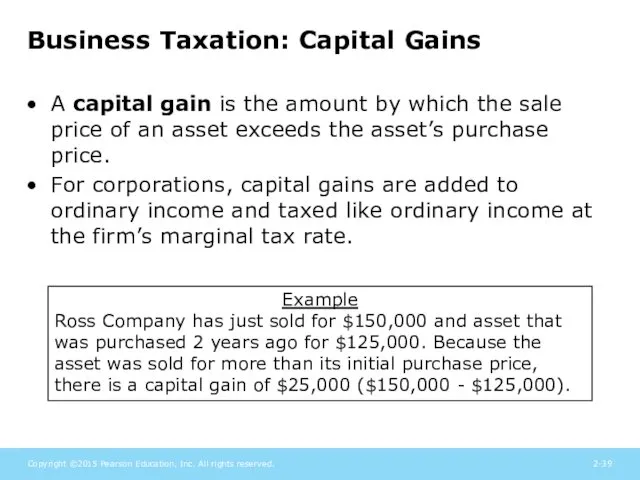

Business Taxation: Capital Gains

A capital gain is the amount by which

Business Taxation: Capital Gains

A capital gain is the amount by which

Review of Learning Goals

LG1 Understand the role that financial institutions play

Review of Learning Goals

LG1 Understand the role that financial institutions play

Review of Learning Goals (cont.)

LG3 Describe the differences between the capital

Review of Learning Goals (cont.)

LG3 Describe the differences between the capital

Review of Learning Goals (cont.)

LG5 Understand the major regulations and regulatory

Review of Learning Goals (cont.)

LG5 Understand the major regulations and regulatory

Review of Learning Goals (cont.)

LG6 Discuss business taxes and their importance

Review of Learning Goals (cont.)

LG6 Discuss business taxes and their importance

Chapter Resources on MyFinanceLab

Chapter Cases

Group Exercises

Critical Thinking Problems

Chapter Resources on MyFinanceLab

Chapter Cases

Group Exercises

Critical Thinking Problems

Integrative Case: Merit Enterprise Corp.

Merit Enterprise Corporation’s CEO would like to

Integrative Case: Merit Enterprise Corp.

Merit Enterprise Corporation’s CEO would like to

Integrative Case: Merit Enterprise Corp.

Option 1 – Merit could approach JPMorgan

Integrative Case: Merit Enterprise Corp.

Option 1 – Merit could approach JPMorgan

Integrative Case: Merit Enterprise Corp.

Option 2 – Merit could convert to

Integrative Case: Merit Enterprise Corp.

Option 2 – Merit could convert to

Рыночный подход к оценке бизнеса. Метод рынка капитала. Метод сделок. Метод отраслевых коэффициентов

Рыночный подход к оценке бизнеса. Метод рынка капитала. Метод сделок. Метод отраслевых коэффициентов Инвестициялық стратегия

Инвестициялық стратегия Фигуры технического анализа

Фигуры технического анализа Понятие, цели и организация оценки стоимости бизнеса. (Лекция 1)

Понятие, цели и организация оценки стоимости бизнеса. (Лекция 1) Asset Securitization in Russia

Asset Securitization in Russia Сопоставимость отчетных данных и принцип последовательности: МСФО (IAS) 8 Учетная политика, изменения в бухгалтерских

Сопоставимость отчетных данных и принцип последовательности: МСФО (IAS) 8 Учетная политика, изменения в бухгалтерских Отчетность за 9 месяцев 2018 года. Актуальные вопросы. Срок представления налоговой отчетности

Отчетность за 9 месяцев 2018 года. Актуальные вопросы. Срок представления налоговой отчетности Индивидуальный подоходный налог в Республике Казахстан и его учет

Индивидуальный подоходный налог в Республике Казахстан и его учет Налоги и налоговая система РФ

Налоги и налоговая система РФ Місцеві податки і збори

Місцеві податки і збори Доходность и убыточность операций с ценными бумагами

Доходность и убыточность операций с ценными бумагами Налоги. 7 класс

Налоги. 7 класс Инвестициялық жобалардың қаржылық механизмі және жобалық қаржыландыру

Инвестициялық жобалардың қаржылық механизмі және жобалық қаржыландыру Налог на прибыль организаций

Налог на прибыль организаций Relationship between liquidity ratios and profitability in Russian banks using regression analysis

Relationship between liquidity ratios and profitability in Russian banks using regression analysis Шығын айналымын болжау

Шығын айналымын болжау Бухгалтерские счета как элемент метода бухгалтерского учета

Бухгалтерские счета как элемент метода бухгалтерского учета Международные стандарты финансовой отчетности МСФО (IAS) 12 Налоги на прибыль

Международные стандарты финансовой отчетности МСФО (IAS) 12 Налоги на прибыль Тенденции развития современной финансовой науки

Тенденции развития современной финансовой науки Проведение операций по потребительскому кредитованию физических лиц

Проведение операций по потребительскому кредитованию физических лиц Криптовалюта. Доп. инструменты технического анализа

Криптовалюта. Доп. инструменты технического анализа Банки: чем они могут быть вам полезны в жизни

Банки: чем они могут быть вам полезны в жизни Қазақстанның қазіргі уақытта сыртқы қарызы қанша

Қазақстанның қазіргі уақытта сыртқы қарызы қанша Проект бюджета городского округа Судак на 2015 год

Проект бюджета городского округа Судак на 2015 год Финансовые инновации, финансовый инжиниринг. (Лекция 1)

Финансовые инновации, финансовый инжиниринг. (Лекция 1) Критерии оценки инвестиционных проектов

Критерии оценки инвестиционных проектов Планирование финансово-хозяйственной деятельности, как ключевой инструмент финансового менеджмента профсоюзной организации

Планирование финансово-хозяйственной деятельности, как ключевой инструмент финансового менеджмента профсоюзной организации Страхование жизни

Страхование жизни