- Introduction to finance

Содержание

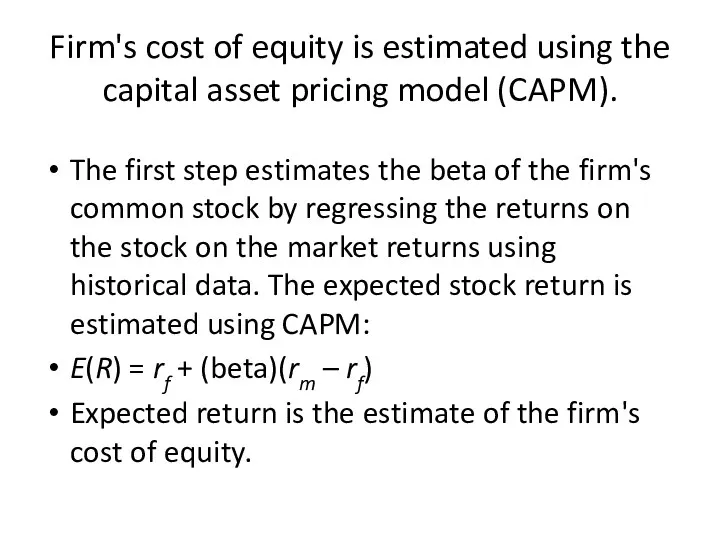

- 2. Firm's cost of equity is estimated using the capital asset pricing model (CAPM). The first step

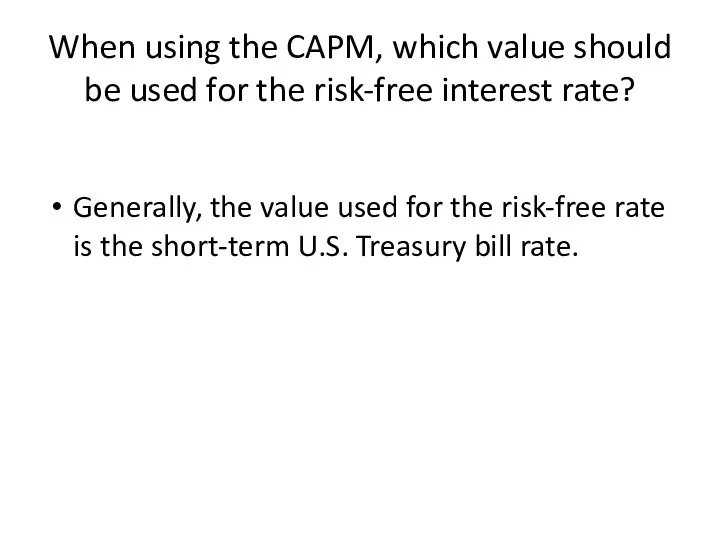

- 3. When using the CAPM, which value should be used for the risk-free interest rate? Generally, the

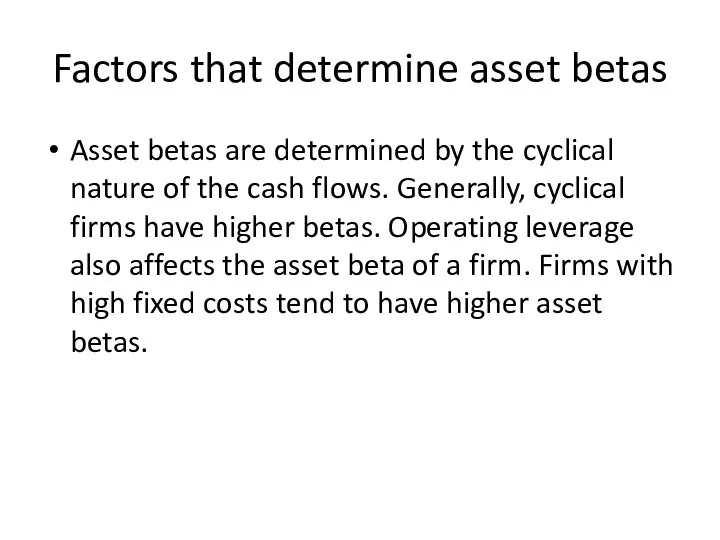

- 4. Factors that determine asset betas Asset betas are determined by the cyclical nature of the cash

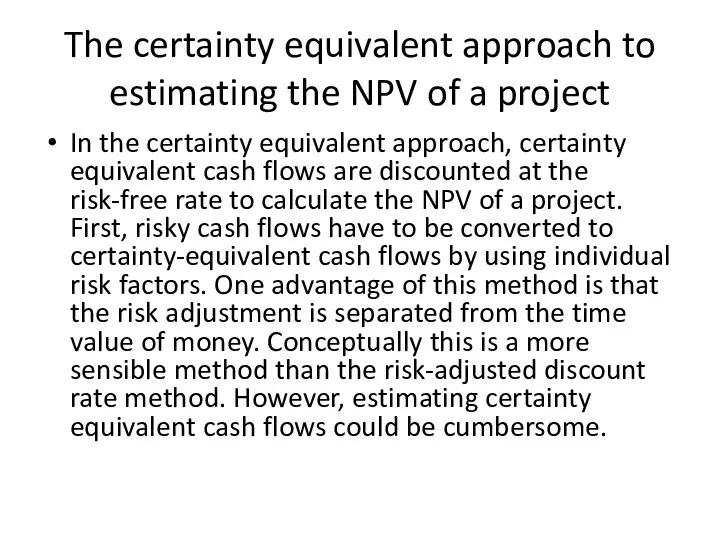

- 5. The certainty equivalent approach to estimating the NPV of a project In the certainty equivalent approach,

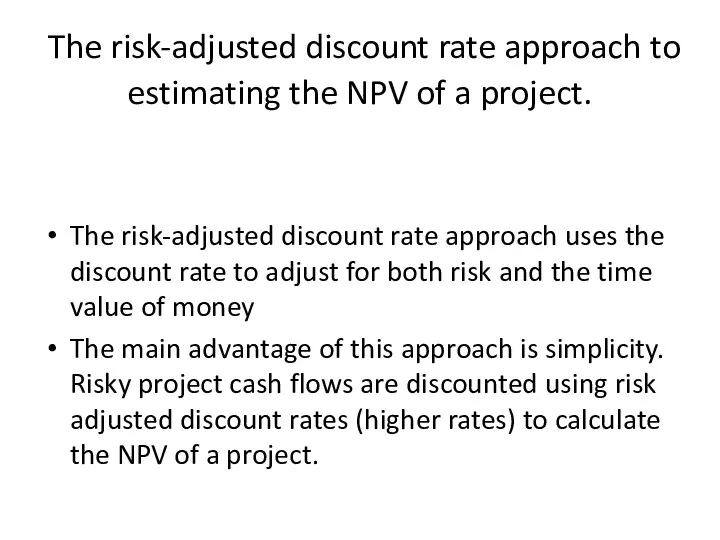

- 6. The risk-adjusted discount rate approach to estimating the NPV of a project. The risk-adjusted discount rate

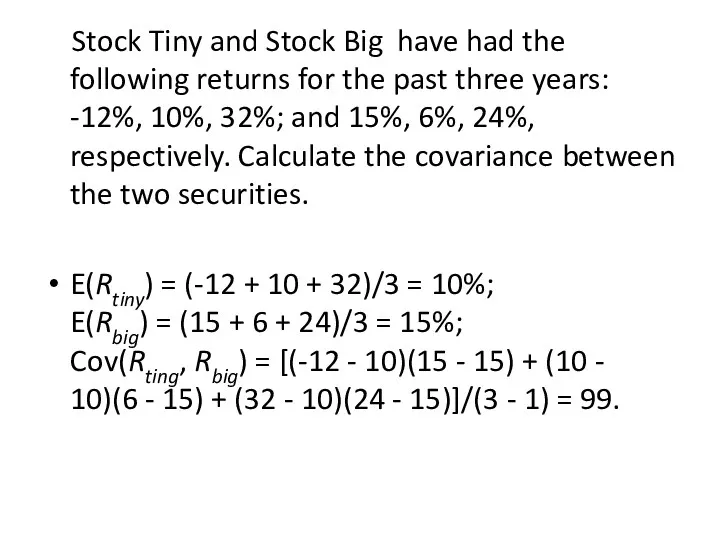

- 7. Stock Tiny and Stock Big have had the following returns for the past three years: -12%,

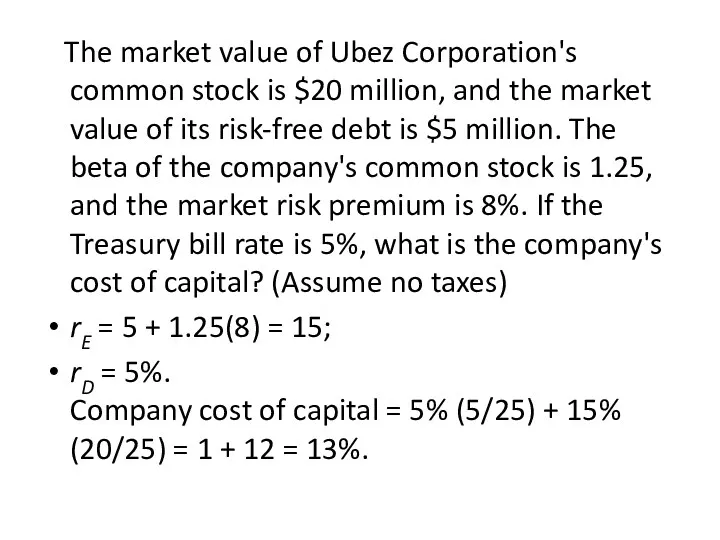

- 8. The market value of Ubez Corporation's common stock is $20 million, and the market value of

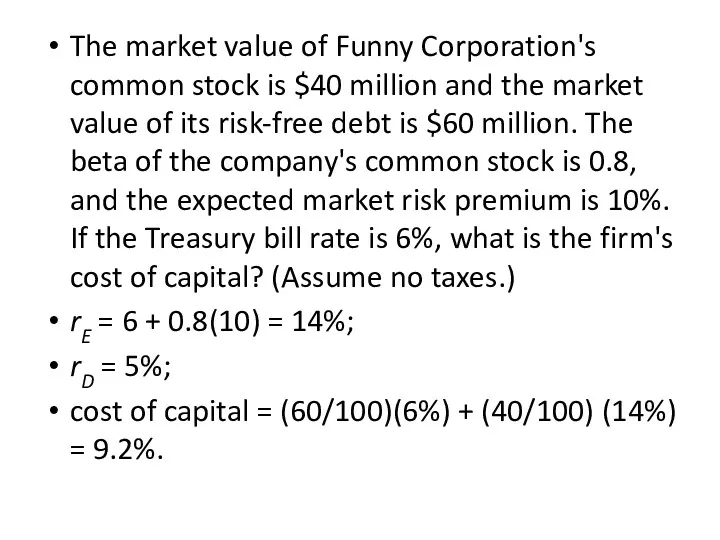

- 9. The market value of Funny Corporation's common stock is $40 million and the market value of

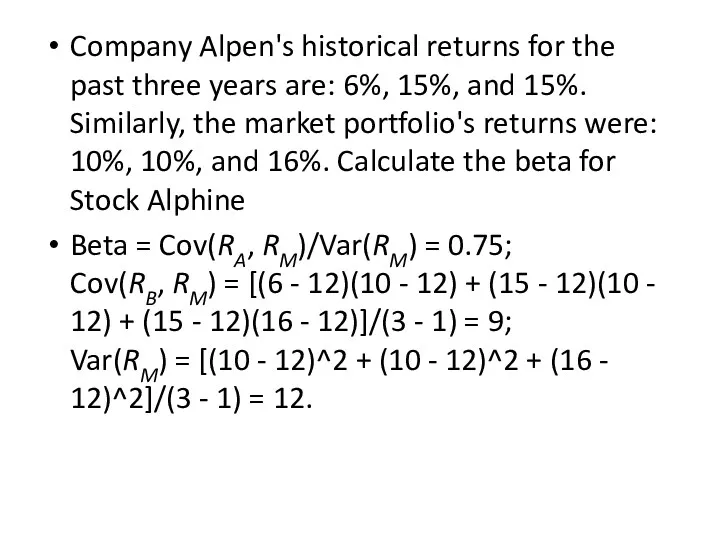

- 10. Company Alpen's historical returns for the past three years are: 6%, 15%, and 15%. Similarly, the

- 11. The market portfolio's historical returns for the past three years were 10%, 10%, and 16%. Suppose

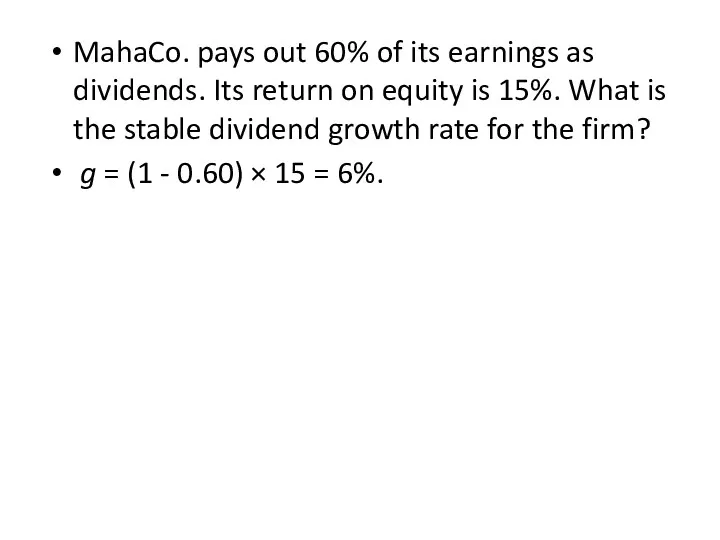

- 12. MahaCo. pays out 60% of its earnings as dividends. Its return on equity is 15%. What

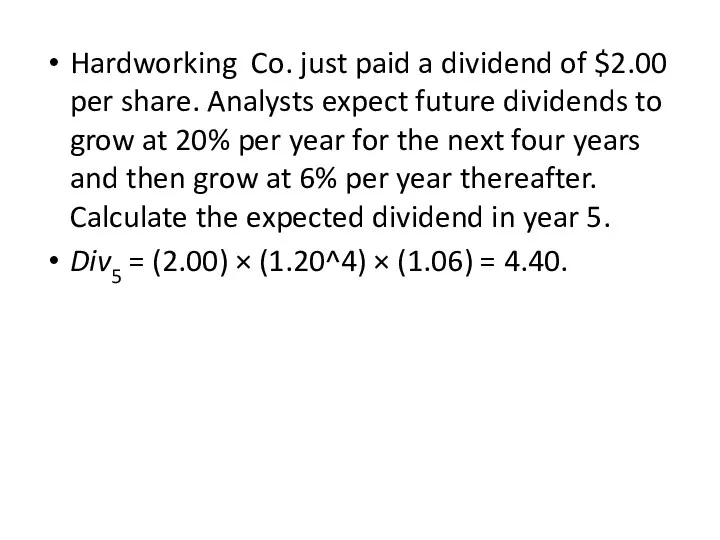

- 13. Hardworking Co. just paid a dividend of $2.00 per share. Analysts expect future dividends to grow

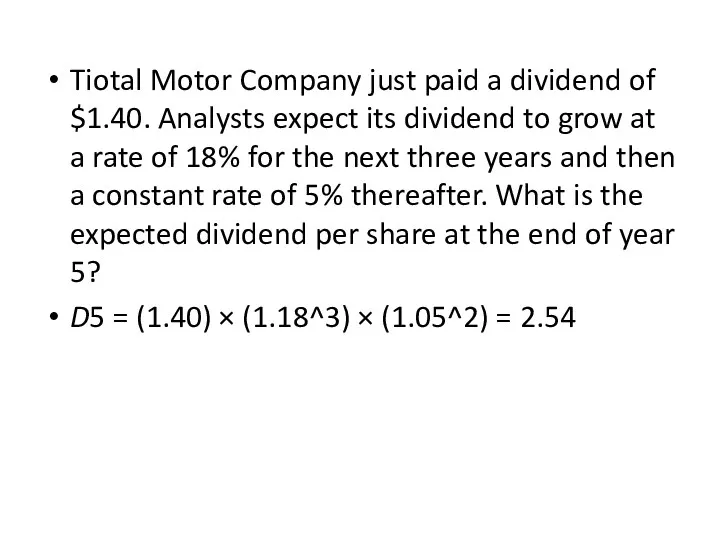

- 14. Tiotal Motor Company just paid a dividend of $1.40. Analysts expect its dividend to grow at

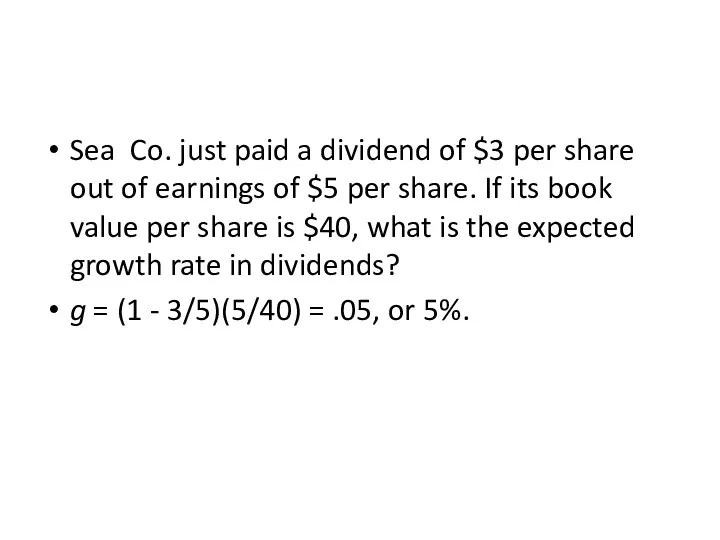

- 15. Sea Co. just paid a dividend of $3 per share out of earnings of $5 per

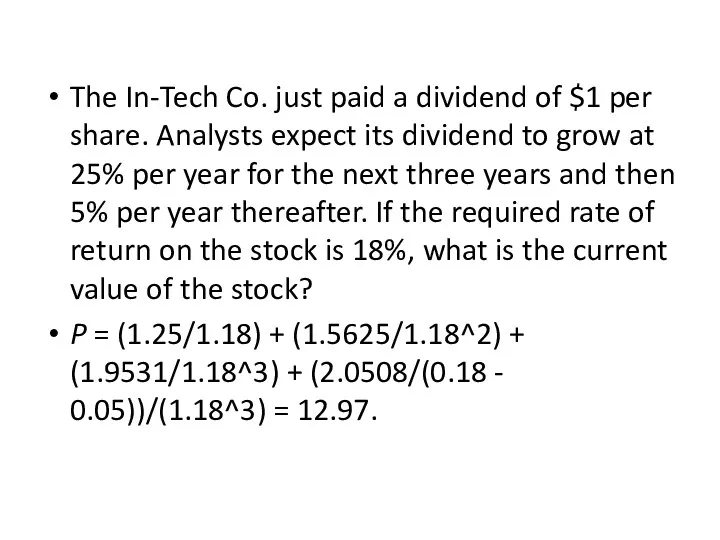

- 16. The In-Tech Co. just paid a dividend of $1 per share. Analysts expect its dividend to

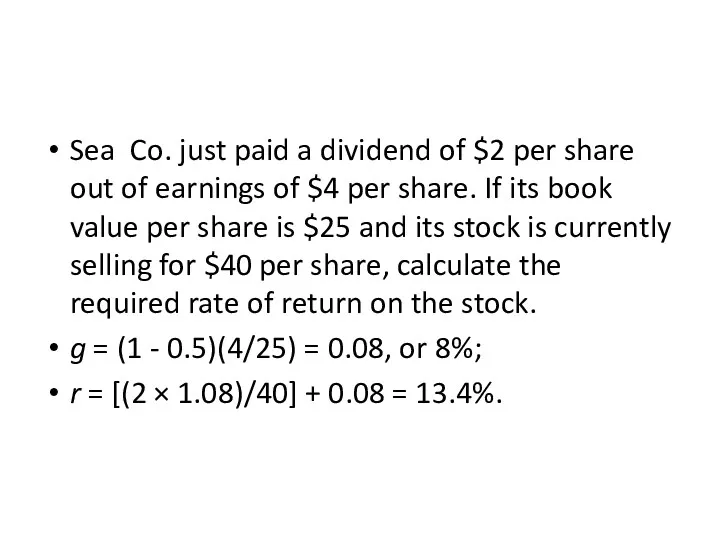

- 17. Sea Co. just paid a dividend of $2 per share out of earnings of $4 per

- 18. Issues a company must take into consideration when determining the firms’ dividend policy In determining the

- 19. The trade-offs in setting a firm’s dividend policy A. If a company pays a large dividend,

- 20. Real options associated with capital budgeting projects There are four types of real options. They are:

- 21. Production options provide a firm with additional flexibility to alter inputs or processes. These have value

- 22. Dividend Policy Matter to Stockholders? Three views about the importance of a firm’s dividend policy. View

- 23. 3. Under the foregoing assumptions, it may be shown that the market price of a corporation’s

- 24. View 2: High dividends increase stock value. 1. Dividends are more predictable than capital gains because

- 25. View 3: Low dividends increase value. Stocks that allow us to defer taxes (low dividends-high capital

- 26. Sensitivity analysis as used for project analysis. By using sensitivity analysis one can determine the factors

- 27. The term price-earnings (P/E) ratio The P/E ratio is a widely used financial indicator, but is

- 29. Скачать презентацию

Firm's cost of equity is estimated using the capital asset pricing

Firm's cost of equity is estimated using the capital asset pricing

When using the CAPM, which value should be used for the

When using the CAPM, which value should be used for the

Factors that determine asset betas

Asset betas are determined by the cyclical

Factors that determine asset betas

Asset betas are determined by the cyclical

The certainty equivalent approach to estimating the NPV of a project

In

The certainty equivalent approach to estimating the NPV of a project

In

The risk-adjusted discount rate approach to estimating the NPV of a

The risk-adjusted discount rate approach to estimating the NPV of a

Stock Tiny and Stock Big have had the following returns

Stock Tiny and Stock Big have had the following returns

The market value of Ubez Corporation's common stock is $20

The market value of Ubez Corporation's common stock is $20

The market value of Funny Corporation's common stock is $40 million

The market value of Funny Corporation's common stock is $40 million

Company Alpen's historical returns for the past three years are: 6%,

Company Alpen's historical returns for the past three years are: 6%,

The market portfolio's historical returns for the past three years were

The market portfolio's historical returns for the past three years were

MahaCo. pays out 60% of its earnings as dividends. Its return

MahaCo. pays out 60% of its earnings as dividends. Its return

Hardworking Co. just paid a dividend of $2.00 per share. Analysts

Hardworking Co. just paid a dividend of $2.00 per share. Analysts

Tiotal Motor Company just paid a dividend of $1.40. Analysts expect

Tiotal Motor Company just paid a dividend of $1.40. Analysts expect

Sea Co. just paid a dividend of $3 per share out

Sea Co. just paid a dividend of $3 per share out

The In-Tech Co. just paid a dividend of $1 per share.

The In-Tech Co. just paid a dividend of $1 per share.

Sea Co. just paid a dividend of $2 per share out

Sea Co. just paid a dividend of $2 per share out

Issues a company must take into consideration when determining the firms’

Issues a company must take into consideration when determining the firms’

The trade-offs in setting a firm’s dividend policy

A. If a company

The trade-offs in setting a firm’s dividend policy

A. If a company

Real options associated with capital budgeting projects

There are four types of

Real options associated with capital budgeting projects

There are four types of

Production options provide a firm with additional flexibility to alter inputs

Production options provide a firm with additional flexibility to alter inputs

Dividend Policy Matter to Stockholders?

Three views about the importance of a

Dividend Policy Matter to Stockholders?

Three views about the importance of a

3. Under the foregoing assumptions, it may be shown that the

3. Under the foregoing assumptions, it may be shown that the

View 2: High dividends increase stock value.

1. Dividends are more predictable

View 2: High dividends increase stock value.

1. Dividends are more predictable

View 3: Low dividends increase value.

Stocks that allow us to defer

View 3: Low dividends increase value.

Stocks that allow us to defer

Sensitivity analysis as used for project analysis.

By using sensitivity analysis one

Sensitivity analysis as used for project analysis.

By using sensitivity analysis one

The term price-earnings (P/E) ratio

The P/E ratio is a widely used

The term price-earnings (P/E) ratio

The P/E ratio is a widely used

Бюджетирование в системе управленческого учета. Бюджетирование в 1С: Управление производственным предприятием

Бюджетирование в системе управленческого учета. Бюджетирование в 1С: Управление производственным предприятием Суть, мета і завдання управлінського обліку (тема 1)

Суть, мета і завдання управлінського обліку (тема 1) Предмет инвестиции. Инвестиционный проект. Лекция 2

Предмет инвестиции. Инвестиционный проект. Лекция 2 Доходы, расходы и сбалансированность бюджетов

Доходы, расходы и сбалансированность бюджетов Документация в бухгалтерском учете

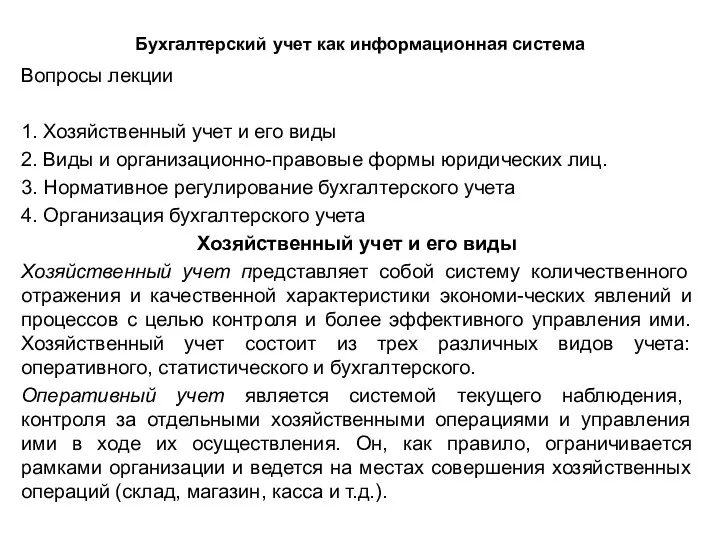

Документация в бухгалтерском учете Бухгалтерский учет как информационная система

Бухгалтерский учет как информационная система Податки та збори в Україні, загальні засади їх встановлення

Податки та збори в Україні, загальні засади їх встановлення Учет основных средств организации

Учет основных средств организации Финансы и кредит

Финансы и кредит Об уровне тарифов на коммунальные услуги с 1 июля 2018

Об уровне тарифов на коммунальные услуги с 1 июля 2018 Взаимосвязь отмывания преступных доходов и финансирования терроризма с иными противоправными деяниями на международном уровне

Взаимосвязь отмывания преступных доходов и финансирования терроризма с иными противоправными деяниями на международном уровне Деньги. Функции денег

Деньги. Функции денег Налог на прибыль организаций. Налогоплательщики

Налог на прибыль организаций. Налогоплательщики Учет доходов, расходов (издержек) фармацевтических организаций. Выведение результатов хозяйственно-финансовой деятельности

Учет доходов, расходов (издержек) фармацевтических организаций. Выведение результатов хозяйственно-финансовой деятельности Итоги деятельности ФНС России (январь - июль 2022 года)

Итоги деятельности ФНС России (январь - июль 2022 года) Продукт страхования от несчастных случаев Вариант

Продукт страхования от несчастных случаев Вариант Деловая активность предприятия

Деловая активность предприятия Что такое деньги

Что такое деньги Отчетность за 9 месяцев 2018 года. Актуальные вопросы. Срок представления налоговой отчетности

Отчетность за 9 месяцев 2018 года. Актуальные вопросы. Срок представления налоговой отчетности Ипотечное кредитование ВТБ 24

Ипотечное кредитование ВТБ 24 Социальная поддержка отдельных категорий граждан

Социальная поддержка отдельных категорий граждан Государственные внебюджетные фонды

Государственные внебюджетные фонды Учет нематериальных активов. (Тема 7)

Учет нематериальных активов. (Тема 7) История налогообложения. Понятие налога

История налогообложения. Понятие налога Характеристика бухгалтерского учета. Основы калькуляции и учета

Характеристика бухгалтерского учета. Основы калькуляции и учета Бюджет для граждан. К решению Земского собрания Варнавинского муниципального района О районном бюджете на 2017 год

Бюджет для граждан. К решению Земского собрания Варнавинского муниципального района О районном бюджете на 2017 год Предмет и метод бухгалтерского учета

Предмет и метод бухгалтерского учета Организация ипотечного кредитования в коммерческом банке

Организация ипотечного кредитования в коммерческом банке