- The Capital Asset Pricing Model (CAPM). Corporate Finance

Содержание

- 2. 10.1 Individual Securities 10.2 Expected Return, Variance, and Covariance 10.3 The Return and Risk for Portfolios

- 3. 10.1 Individual Securities The characteristics of individual securities that are of interest are the: Expected Return

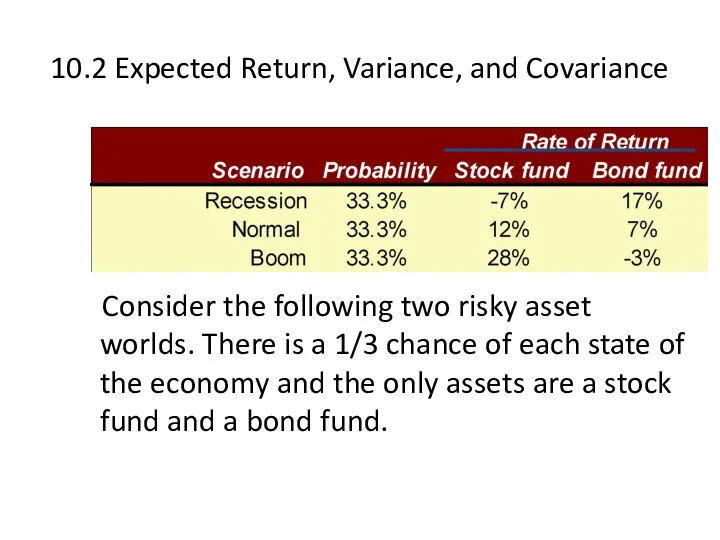

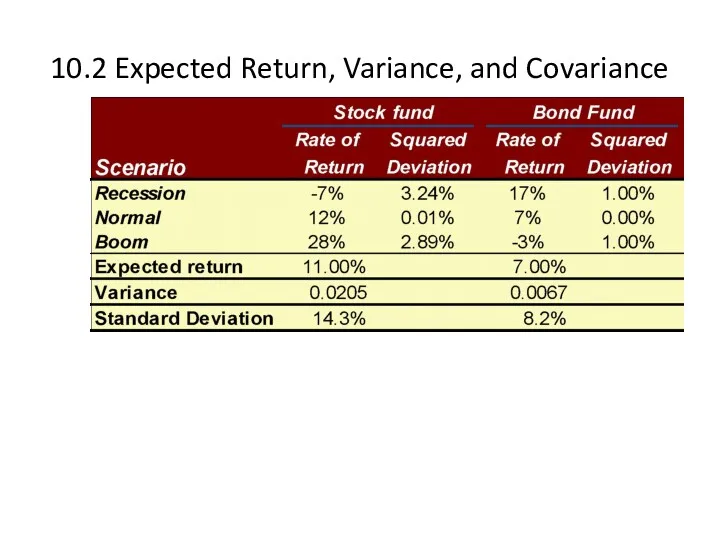

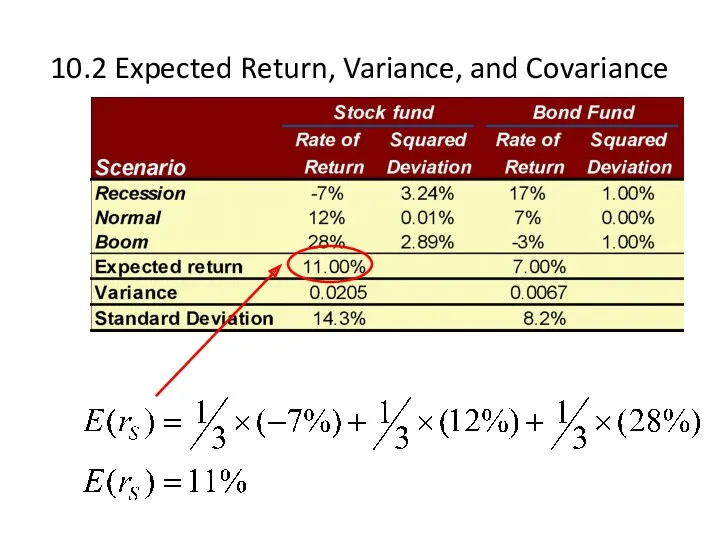

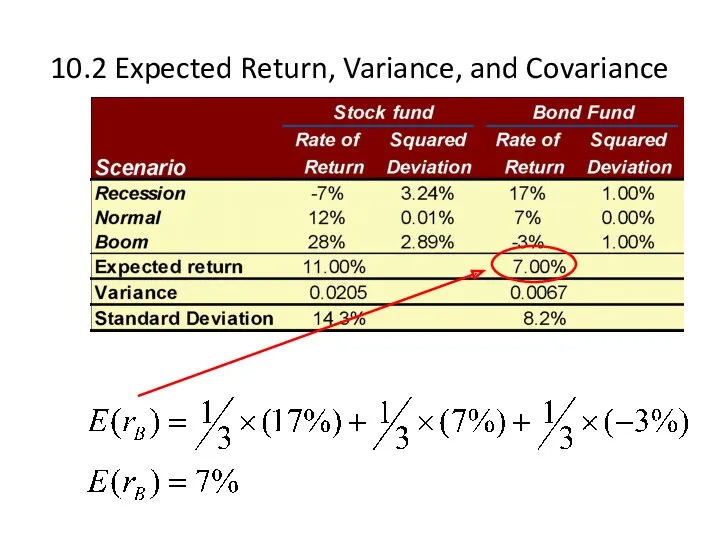

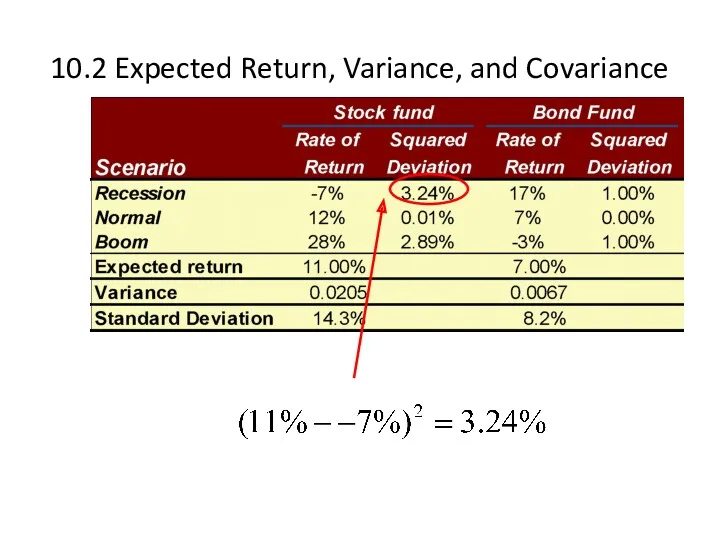

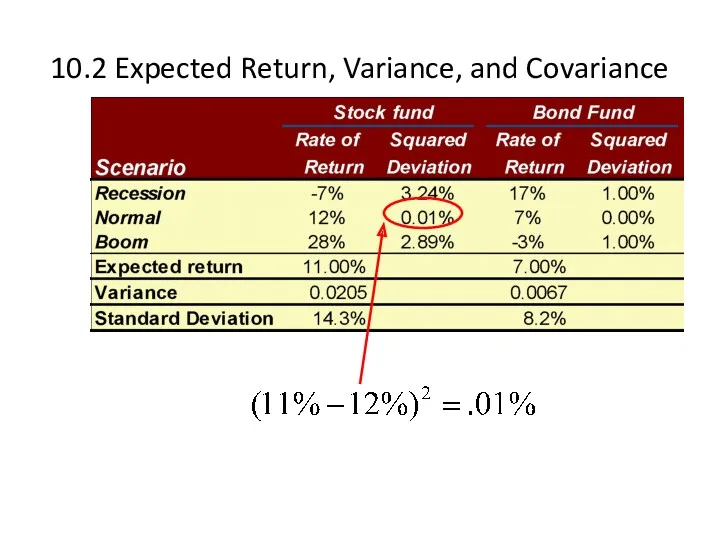

- 4. 10.2 Expected Return, Variance, and Covariance Consider the following two risky asset worlds. There is a

- 5. 10.2 Expected Return, Variance, and Covariance

- 6. 10.2 Expected Return, Variance, and Covariance

- 7. 10.2 Expected Return, Variance, and Covariance

- 8. 10.2 Expected Return, Variance, and Covariance

- 9. 10.2 Expected Return, Variance, and Covariance

- 10. 10.2 Expected Return, Variance, and Covariance

- 11. 10.2 Expected Return, Variance, and Covariance

- 12. 10.2 Expected Return, Variance, and Covariance

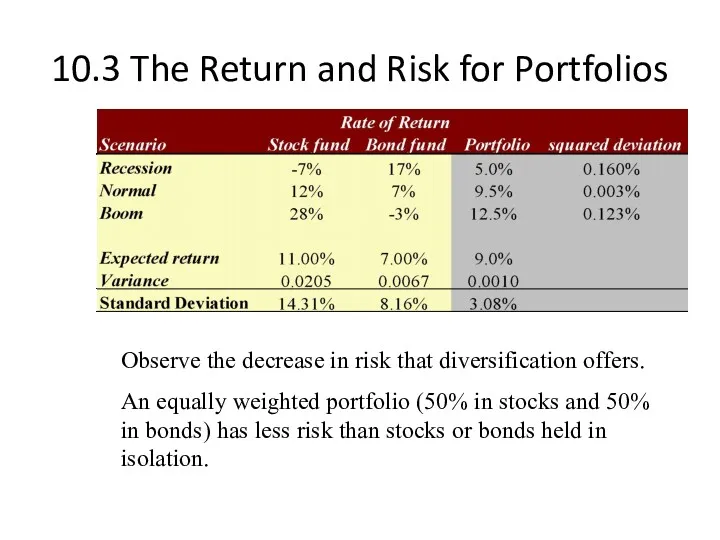

- 13. 10.3 The Return and Risk for Portfolios Note that stocks have a higher expected return than

- 14. 10.3 The Return and Risk for Portfolios The rate of return on the portfolio is a

- 15. 10.3 The Return and Risk for Portfolios The rate of return on the portfolio is a

- 16. 10.3 The Return and Risk for Portfolios The rate of return on the portfolio is a

- 17. 10.3 The Return and Risk for Portfolios The expected rate of return on the portfolio is

- 18. 10.3 The Return and Risk for Portfolios The variance of the rate of return on the

- 19. 10.3 The Return and Risk for Portfolios Observe the decrease in risk that diversification offers. An

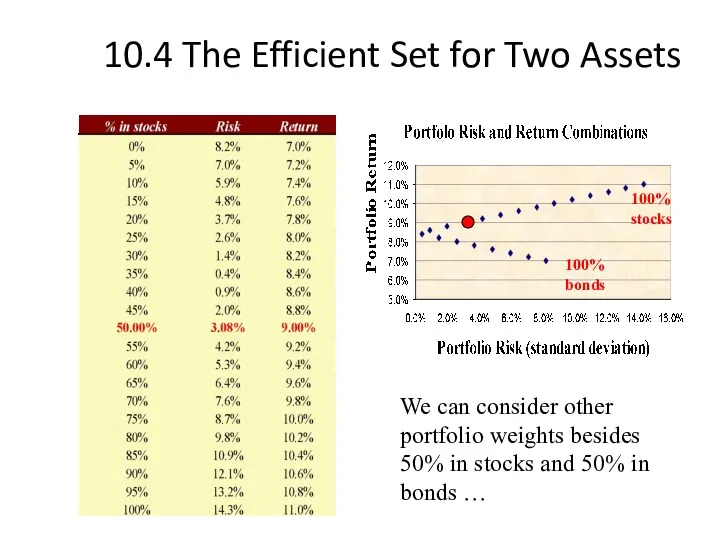

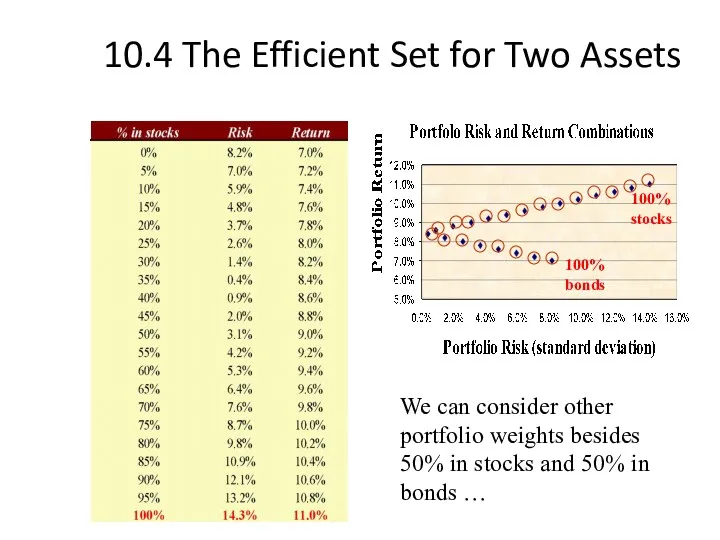

- 20. 10.4 The Efficient Set for Two Assets We can consider other portfolio weights besides 50% in

- 21. 10.4 The Efficient Set for Two Assets We can consider other portfolio weights besides 50% in

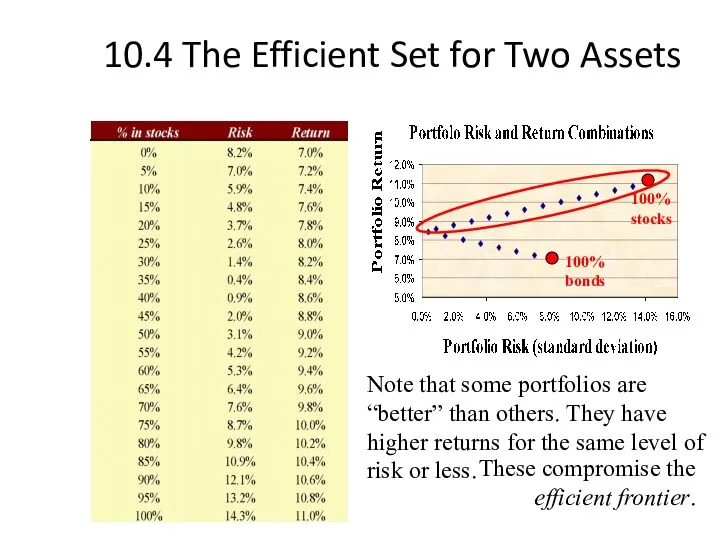

- 22. 10.4 The Efficient Set for Two Assets 100% stocks 100% bonds Note that some portfolios are

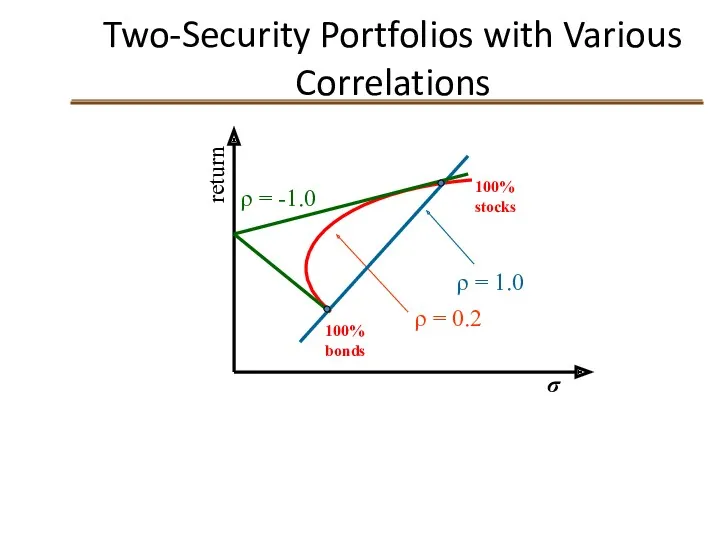

- 23. Two-Security Portfolios with Various Correlations 100% bonds return σ 100% stocks ρ = 0.2 ρ =

- 24. Portfolio Risk/Return Two Securities: Correlation Effects Relationship depends on correlation coefficient -1.0 The smaller the correlation,

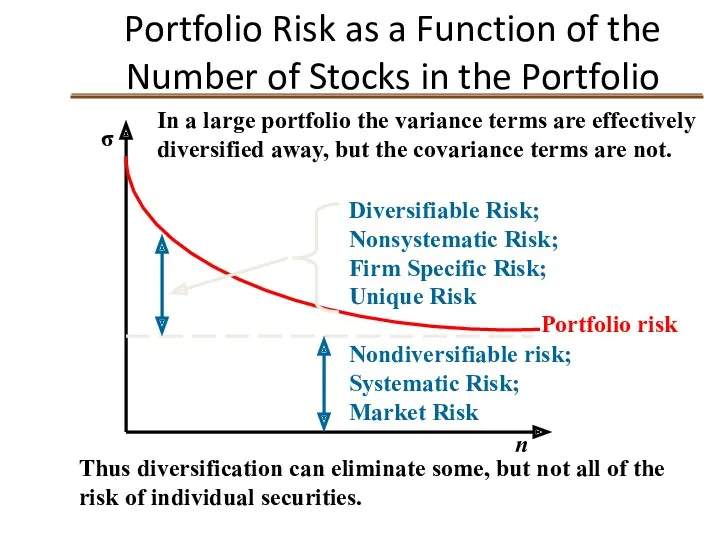

- 25. Portfolio Risk as a Function of the Number of Stocks in the Portfolio Nondiversifiable risk; Systematic

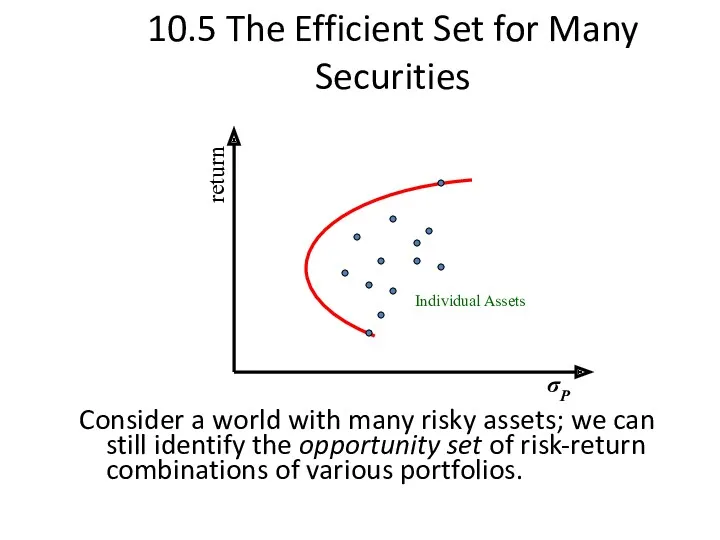

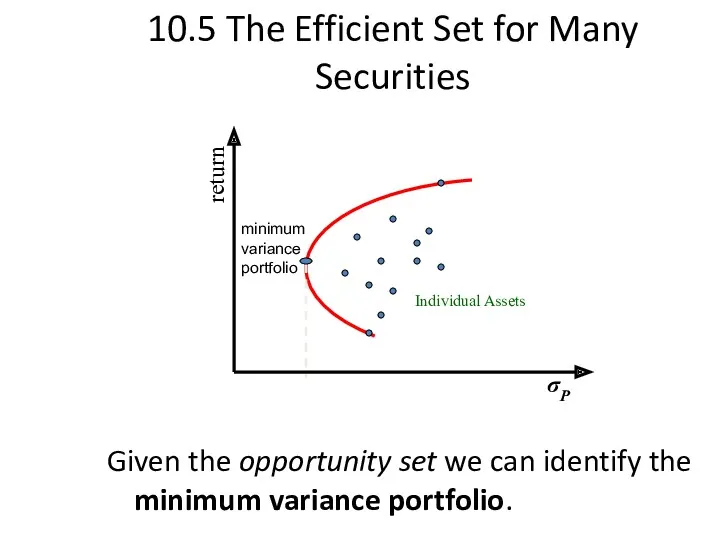

- 26. 10.5 The Efficient Set for Many Securities Consider a world with many risky assets; we can

- 27. 10.5 The Efficient Set for Many Securities Given the opportunity set we can identify the minimum

- 28. 10.5 The Efficient Set for Many Securities The section of the opportunity set above the minimum

- 29. Optimal Risky Portfolio with a Risk-Free Asset In addition to stocks and bonds, consider a world

- 30. 10.7 Riskless Borrowing and Lending Now investors can allocate their money across the T-bills and a

- 31. 10.7 Riskless Borrowing and Lending With a risk-free asset available and the efficient frontier identified, we

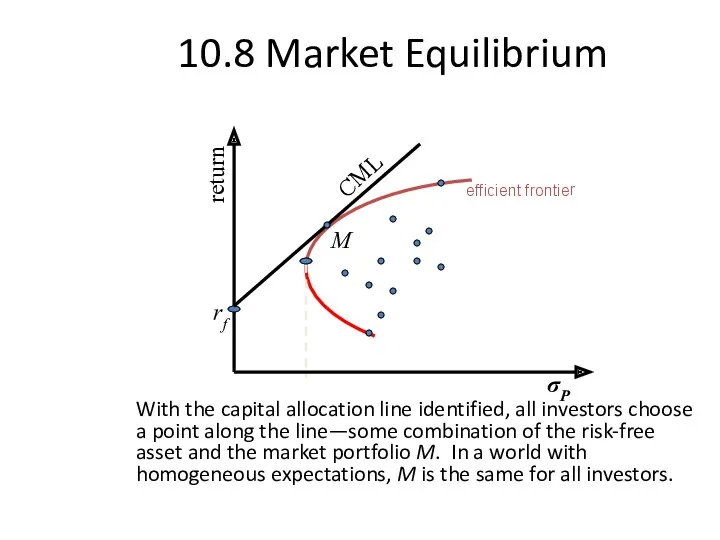

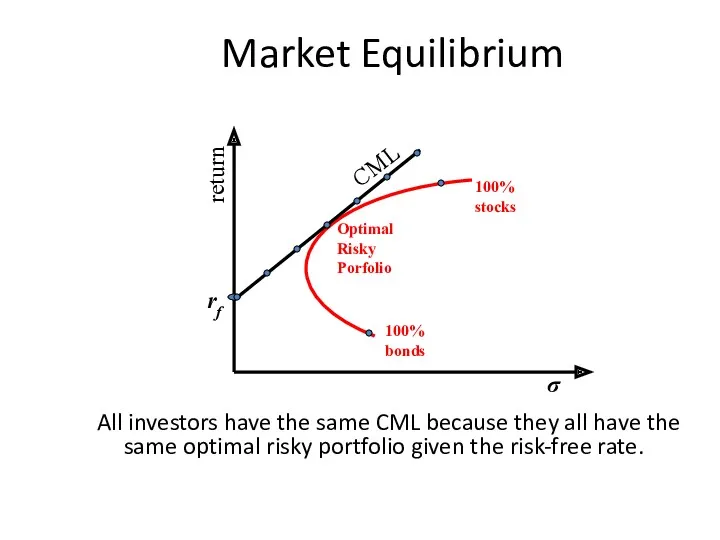

- 32. 10.8 Market Equilibrium With the capital allocation line identified, all investors choose a point along the

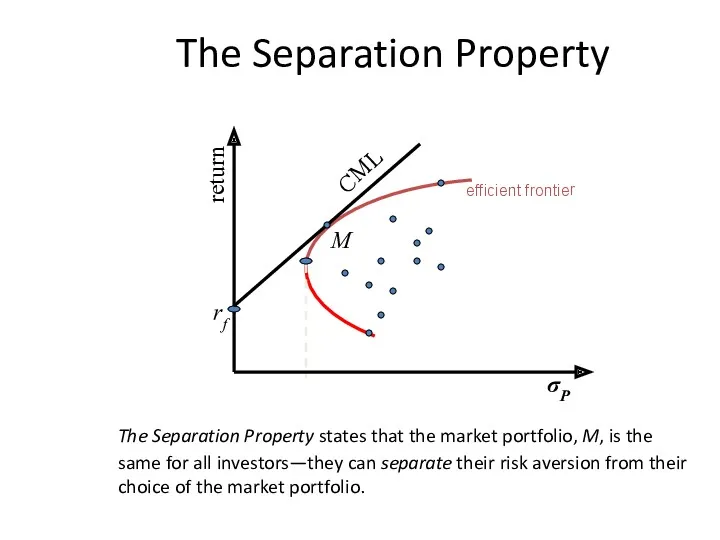

- 33. The Separation Property The Separation Property states that the market portfolio, M, is the same for

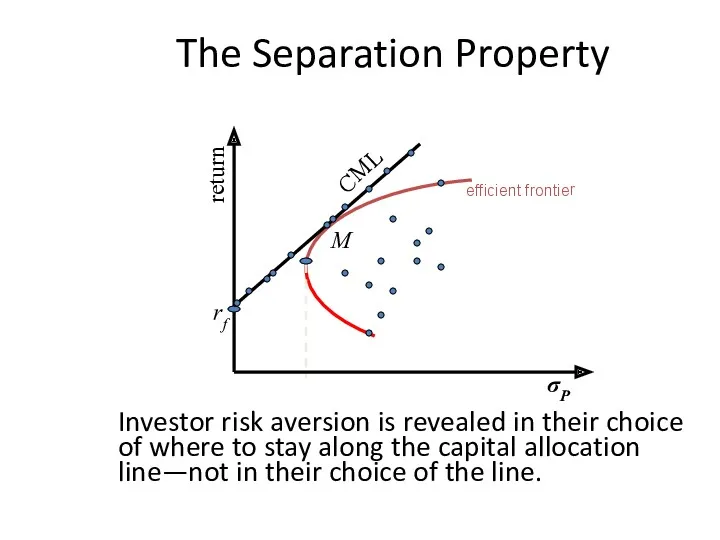

- 34. The Separation Property Investor risk aversion is revealed in their choice of where to stay along

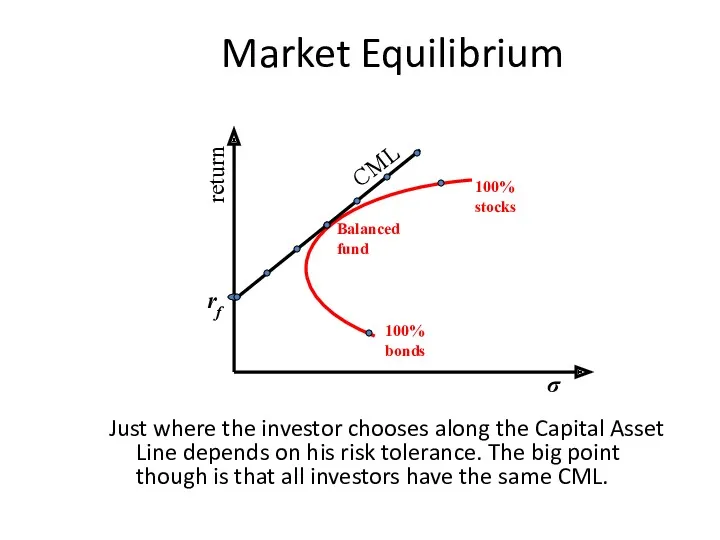

- 35. Market Equilibrium Just where the investor chooses along the Capital Asset Line depends on his risk

- 36. Market Equilibrium All investors have the same CML because they all have the same optimal risky

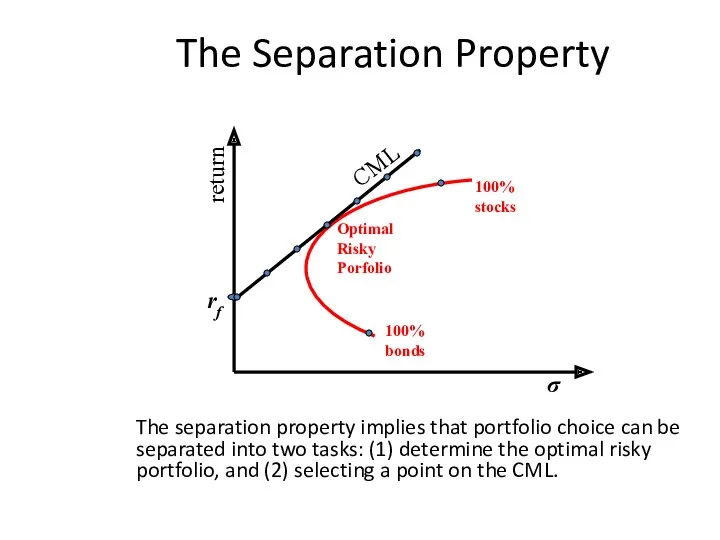

- 37. The Separation Property The separation property implies that portfolio choice can be separated into two tasks:

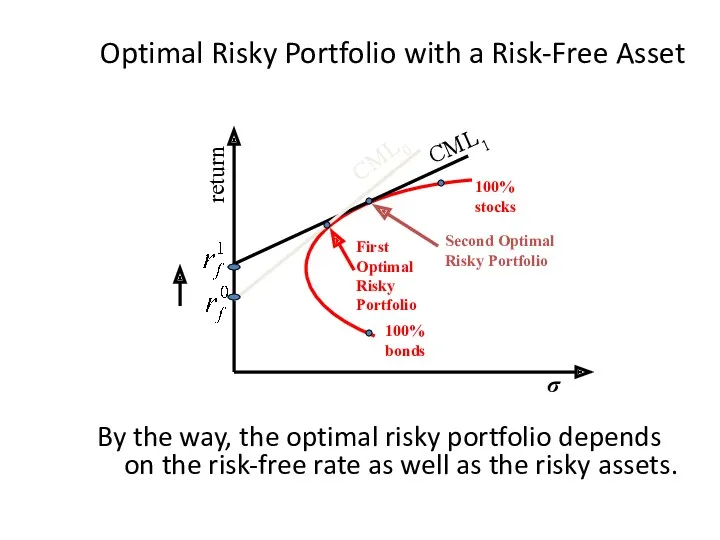

- 38. Optimal Risky Portfolio with a Risk-Free Asset By the way, the optimal risky portfolio depends on

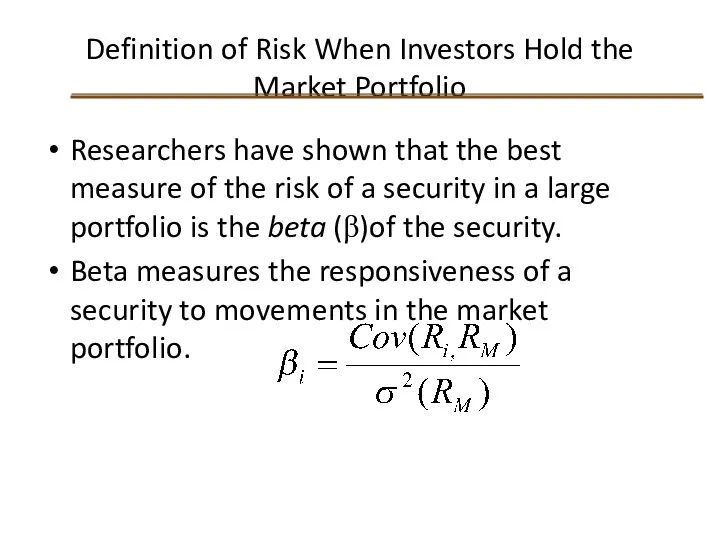

- 39. Definition of Risk When Investors Hold the Market Portfolio Researchers have shown that the best measure

- 40. Estimating β with regression Security Returns Return on market % Ri = α i + βiRm

- 41. Estimates of β for Selected Stocks

- 42. The Formula for Beta Clearly, your estimate of beta will depend upon your choice of a

- 43. 10.9 Relationship between Risk and Expected Return (CAPM) Expected Return on the Market: Expected return on

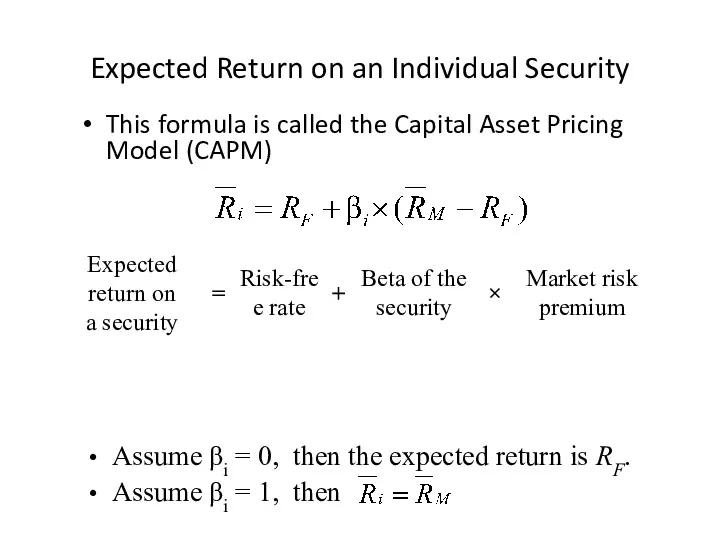

- 44. Expected Return on an Individual Security This formula is called the Capital Asset Pricing Model (CAPM)

- 45. Relationship Between Risk & Expected Return Expected return β 1.0

- 46. Relationship Between Risk & Expected Return Expected return β 1.5

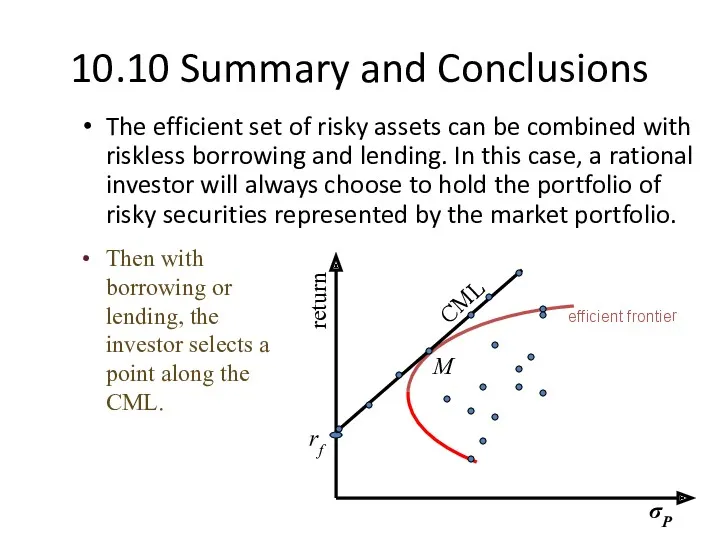

- 47. 10.10 Summary and Conclusions This chapter sets forth the principles of modern portfolio theory. The expected

- 48. 10.10 Summary and Conclusions The efficient set of risky assets can be combined with riskless borrowing

- 50. Скачать презентацию

10.1 Individual Securities

10.2 Expected Return, Variance, and Covariance

10.3 The Return and

10.1 Individual Securities

10.2 Expected Return, Variance, and Covariance

10.3 The Return and

10.1 Individual Securities

The characteristics of individual securities that are of interest

10.1 Individual Securities

The characteristics of individual securities that are of interest

10.2 Expected Return, Variance, and Covariance

Consider the following two risky

10.2 Expected Return, Variance, and Covariance

Consider the following two risky

10.2 Expected Return, Variance, and Covariance

10.2 Expected Return, Variance, and Covariance

10.2 Expected Return, Variance, and Covariance

10.2 Expected Return, Variance, and Covariance

10.2 Expected Return, Variance, and Covariance

10.2 Expected Return, Variance, and Covariance

10.2 Expected Return, Variance, and Covariance

10.2 Expected Return, Variance, and Covariance

10.2 Expected Return, Variance, and Covariance

10.2 Expected Return, Variance, and Covariance

10.2 Expected Return, Variance, and Covariance

10.2 Expected Return, Variance, and Covariance

10.2 Expected Return, Variance, and Covariance

10.2 Expected Return, Variance, and Covariance

10.2 Expected Return, Variance, and Covariance

10.2 Expected Return, Variance, and Covariance

10.3 The Return and Risk for Portfolios

Note that stocks have a

10.3 The Return and Risk for Portfolios

Note that stocks have a

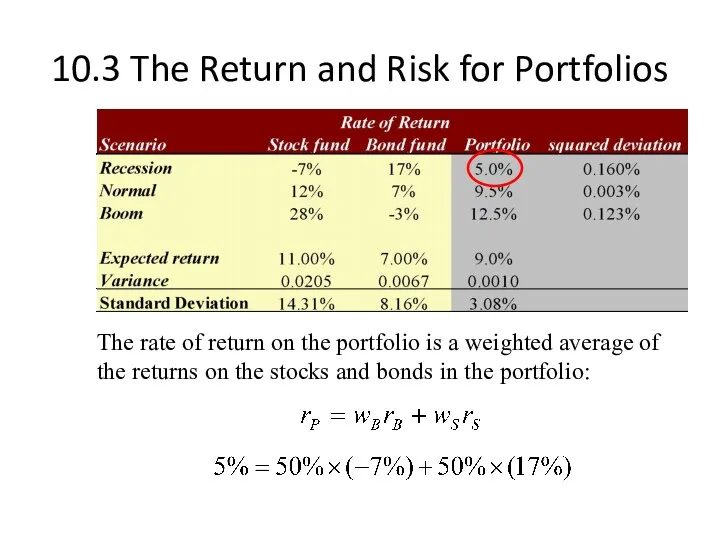

10.3 The Return and Risk for Portfolios

The rate of return on

10.3 The Return and Risk for Portfolios

The rate of return on

10.3 The Return and Risk for Portfolios

The rate of return on

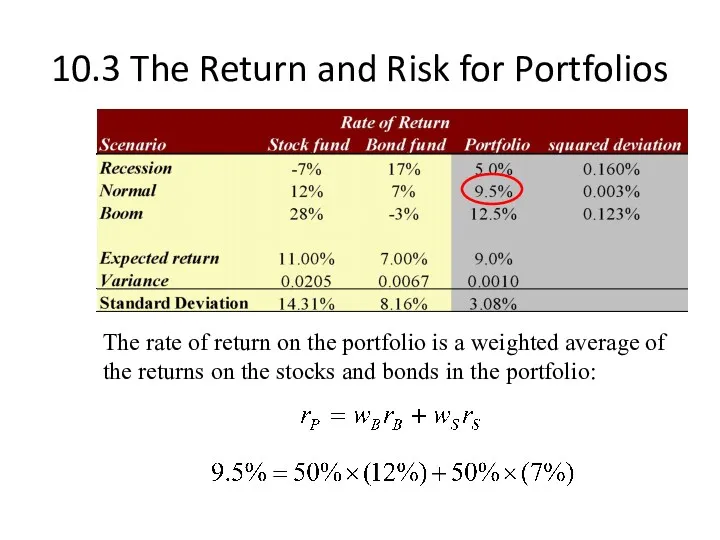

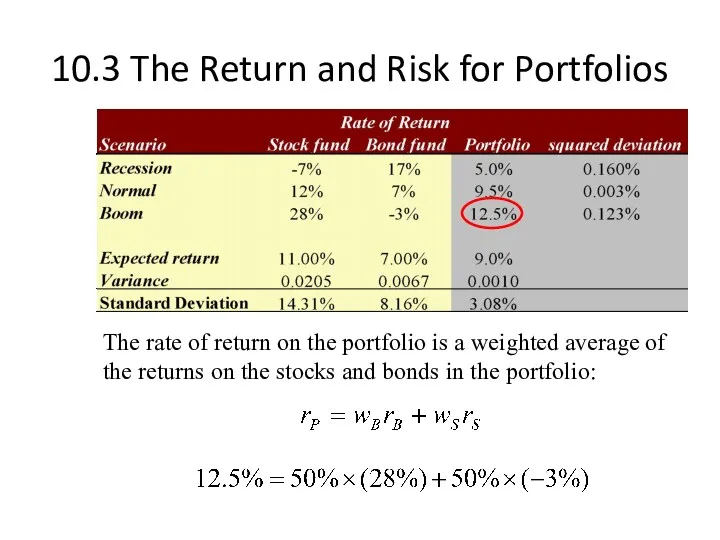

10.3 The Return and Risk for Portfolios

The rate of return on

10.3 The Return and Risk for Portfolios

The rate of return on

10.3 The Return and Risk for Portfolios

The rate of return on

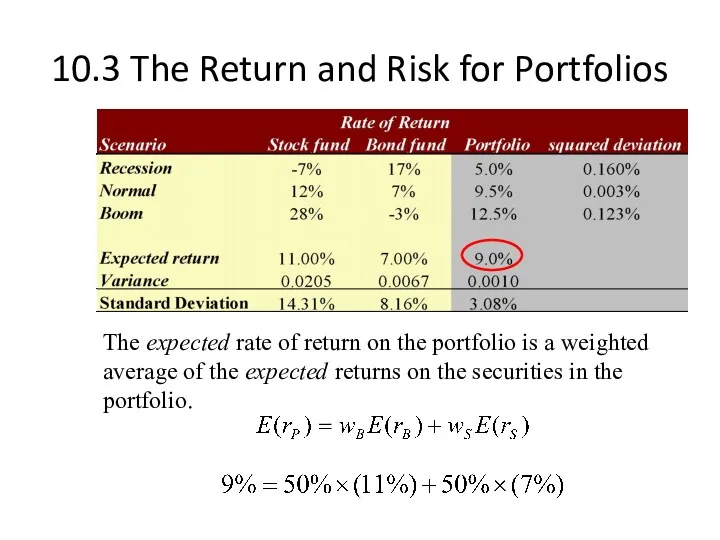

10.3 The Return and Risk for Portfolios

The expected rate of return

10.3 The Return and Risk for Portfolios

The expected rate of return

10.3 The Return and Risk for Portfolios

The variance of the rate

10.3 The Return and Risk for Portfolios

The variance of the rate

10.3 The Return and Risk for Portfolios

Observe the decrease in risk

10.3 The Return and Risk for Portfolios

Observe the decrease in risk

10.4 The Efficient Set for Two Assets

We can consider other portfolio

10.4 The Efficient Set for Two Assets

We can consider other portfolio

10.4 The Efficient Set for Two Assets

We can consider other portfolio

10.4 The Efficient Set for Two Assets

We can consider other portfolio

10.4 The Efficient Set for Two Assets

100% stocks

100% bonds

Note that some

10.4 The Efficient Set for Two Assets

100% stocks

100% bonds

Note that some

Two-Security Portfolios with Various Correlations

100% bonds

return

σ

100% stocks

ρ = 0.2

ρ =

Two-Security Portfolios with Various Correlations

100% bonds

return

σ

100% stocks

ρ = 0.2

ρ =

Portfolio Risk/Return Two Securities: Correlation Effects

Relationship depends on correlation coefficient

-1.0 <

Portfolio Risk/Return Two Securities: Correlation Effects

Relationship depends on correlation coefficient

-1.0 <

Portfolio Risk as a Function of the Number of Stocks in

Portfolio Risk as a Function of the Number of Stocks in

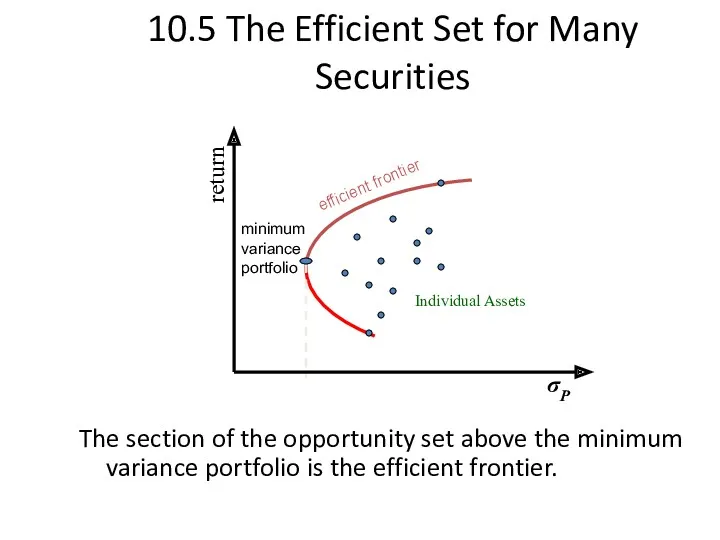

10.5 The Efficient Set for Many Securities

Consider a world with many

10.5 The Efficient Set for Many Securities

Consider a world with many

10.5 The Efficient Set for Many Securities

Given the opportunity set we

10.5 The Efficient Set for Many Securities

Given the opportunity set we

10.5 The Efficient Set for Many Securities

The section of the opportunity

10.5 The Efficient Set for Many Securities

The section of the opportunity

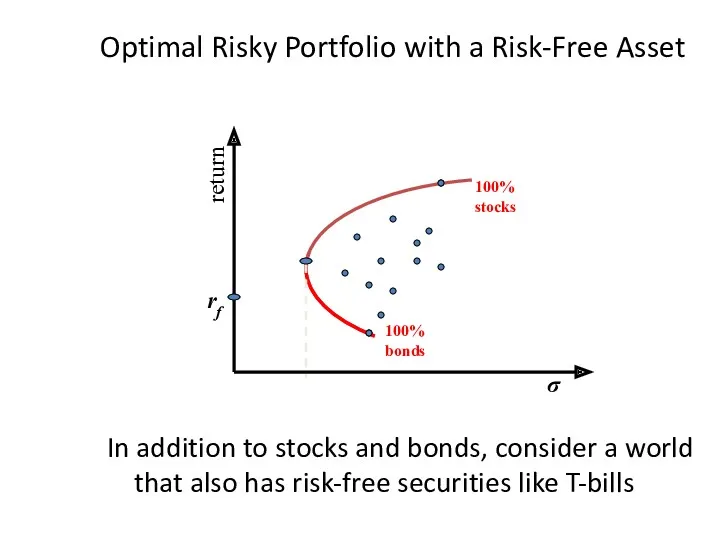

Optimal Risky Portfolio with a Risk-Free Asset

In addition to stocks

Optimal Risky Portfolio with a Risk-Free Asset

In addition to stocks

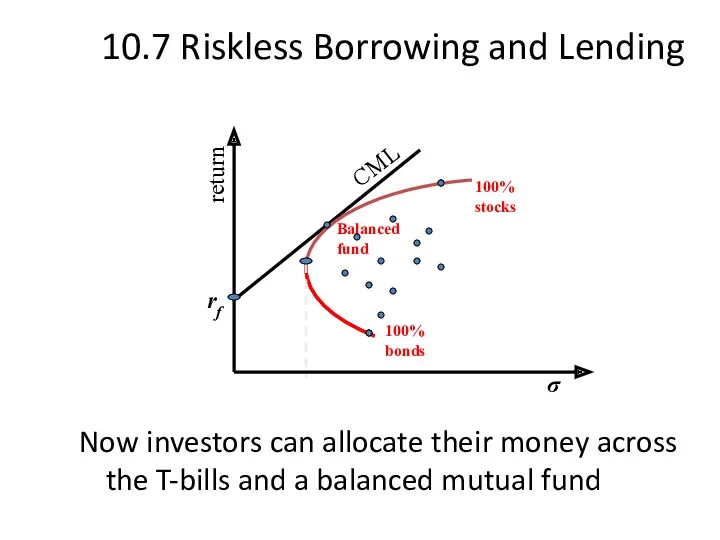

10.7 Riskless Borrowing and Lending

Now investors can allocate their money across

10.7 Riskless Borrowing and Lending

Now investors can allocate their money across

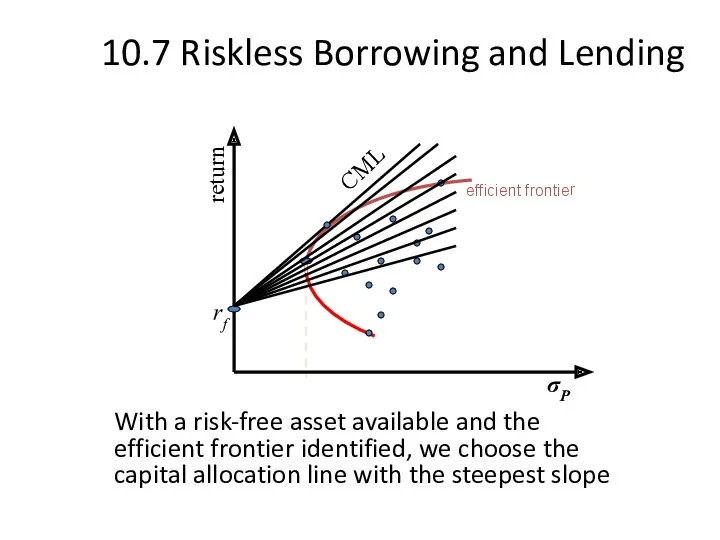

10.7 Riskless Borrowing and Lending

With a risk-free asset available and the

10.7 Riskless Borrowing and Lending

With a risk-free asset available and the

10.8 Market Equilibrium

With the capital allocation line identified, all investors choose

10.8 Market Equilibrium

With the capital allocation line identified, all investors choose

The Separation Property

The Separation Property states that the market portfolio,

The Separation Property

The Separation Property states that the market portfolio,

The Separation Property

Investor risk aversion is revealed in their choice

The Separation Property

Investor risk aversion is revealed in their choice

Market Equilibrium

Just where the investor chooses along the Capital Asset Line

Market Equilibrium

Just where the investor chooses along the Capital Asset Line

Market Equilibrium

All investors have the same CML because they all have

Market Equilibrium

All investors have the same CML because they all have

The Separation Property

The separation property implies that portfolio choice can be

The Separation Property

The separation property implies that portfolio choice can be

Optimal Risky Portfolio with a Risk-Free Asset

By the way, the

Optimal Risky Portfolio with a Risk-Free Asset

By the way, the

Definition of Risk When Investors Hold the Market Portfolio

Researchers have shown

Definition of Risk When Investors Hold the Market Portfolio

Researchers have shown

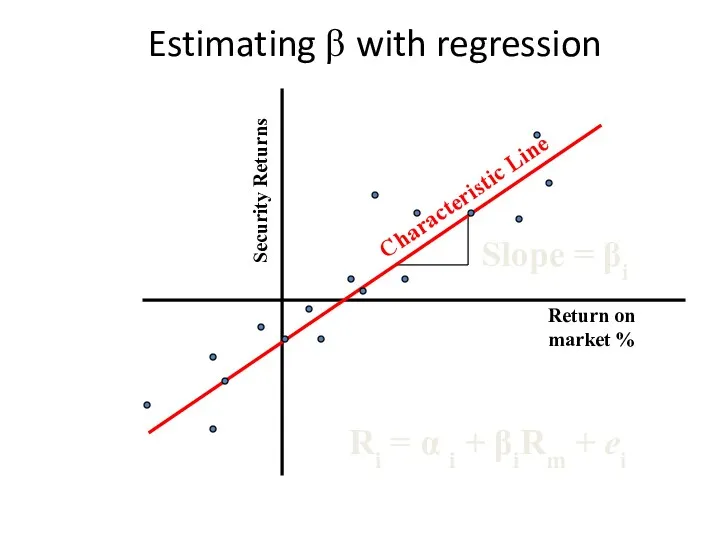

Estimating β with regression

Security Returns

Return on market %

Ri = α i

Estimating β with regression

Security Returns

Return on market %

Ri = α i

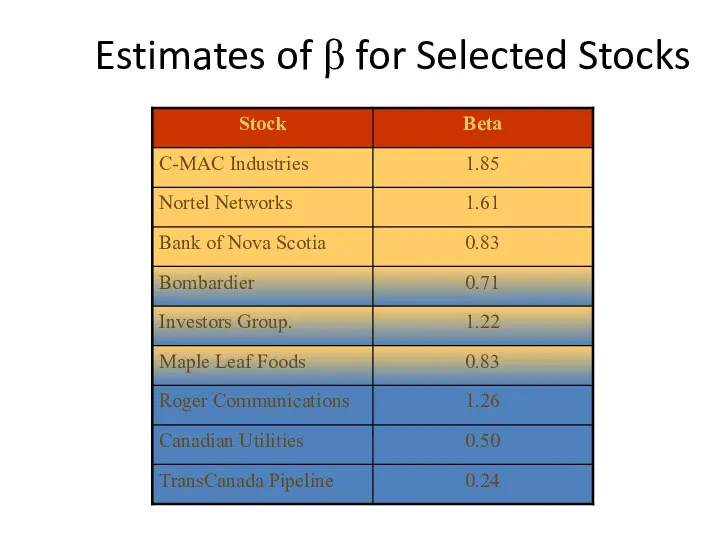

Estimates of β for Selected Stocks

Estimates of β for Selected Stocks

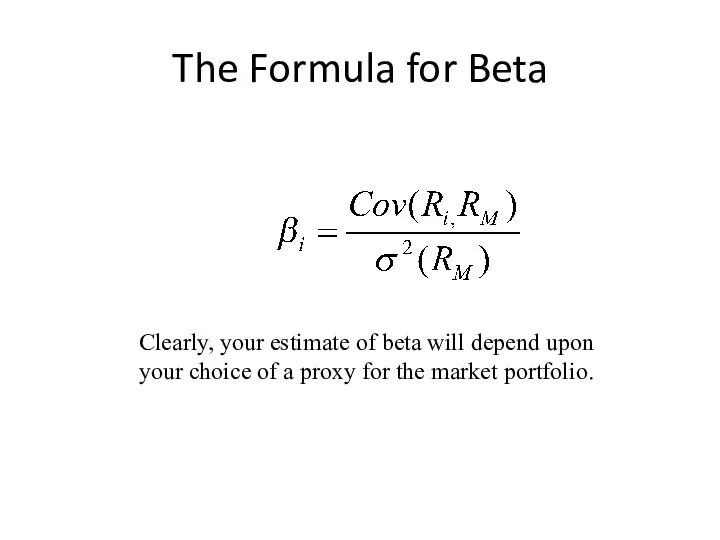

The Formula for Beta

Clearly, your estimate of beta will depend upon

The Formula for Beta

Clearly, your estimate of beta will depend upon

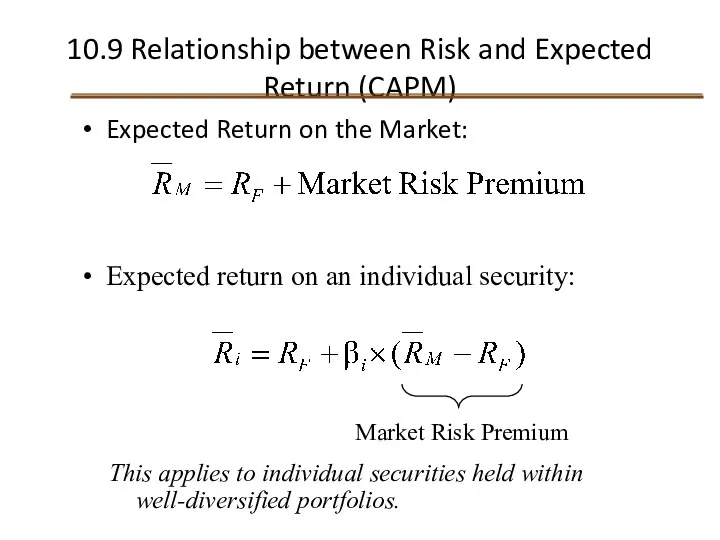

10.9 Relationship between Risk and Expected Return (CAPM)

Expected Return on the

10.9 Relationship between Risk and Expected Return (CAPM)

Expected Return on the

Expected Return on an Individual Security

This formula is called the Capital

Expected Return on an Individual Security

This formula is called the Capital

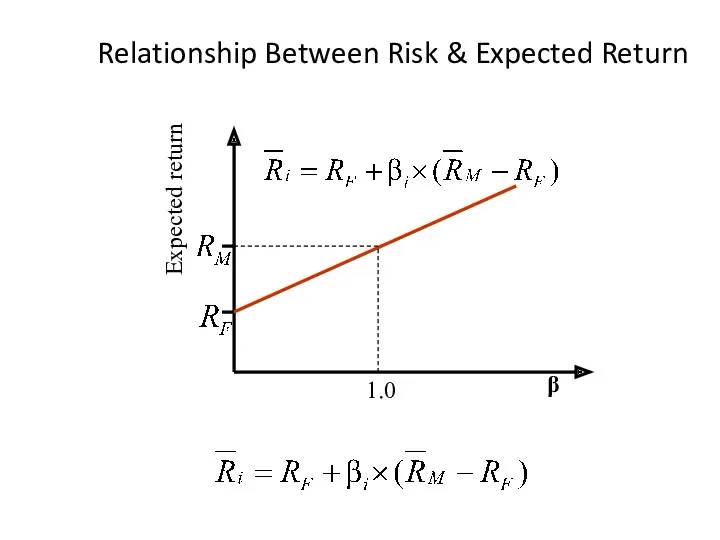

Relationship Between Risk & Expected Return

Expected return

β

1.0

Relationship Between Risk & Expected Return

Expected return

β

1.0

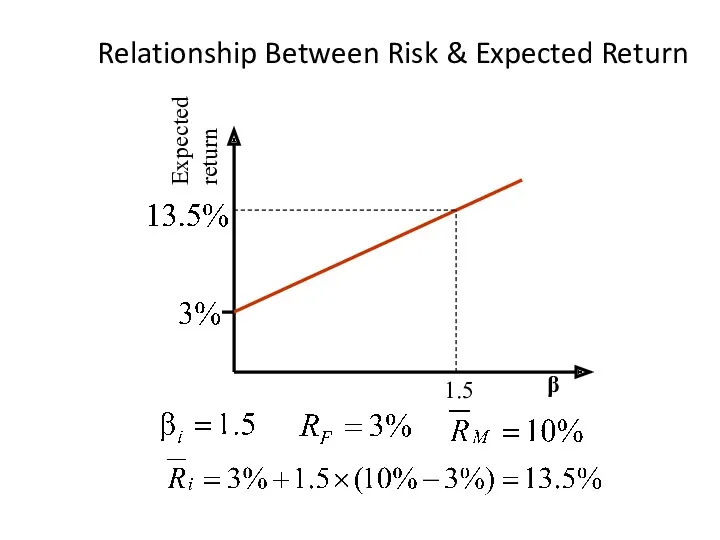

Relationship Between Risk & Expected Return

Expected return

β

1.5

Relationship Between Risk & Expected Return

Expected return

β

1.5

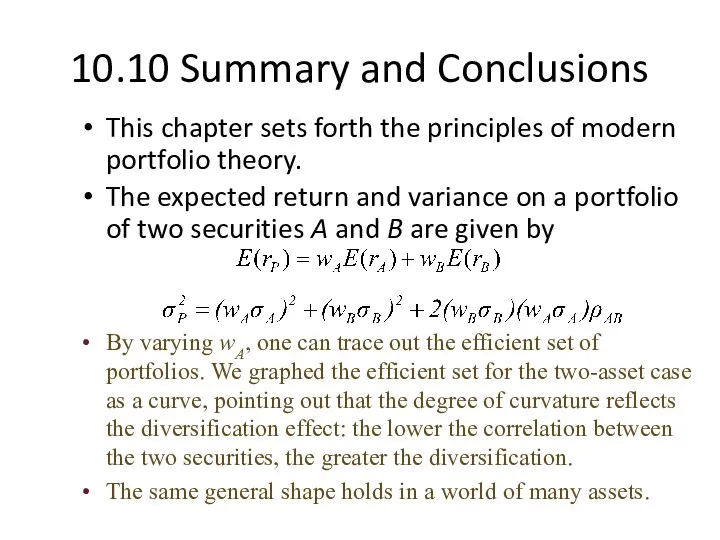

10.10 Summary and Conclusions

This chapter sets forth the principles of modern

10.10 Summary and Conclusions

This chapter sets forth the principles of modern

10.10 Summary and Conclusions

The efficient set of risky assets can be

10.10 Summary and Conclusions

The efficient set of risky assets can be

Методология таможенной статистики

Методология таможенной статистики Международная академия бизнеса. Международные стандарты финансовой отчётности

Международная академия бизнеса. Международные стандарты финансовой отчётности Страхование экспортных кредитов в Чехии

Страхование экспортных кредитов в Чехии Итоги работы управления Федерального казначейства по Курской области

Итоги работы управления Федерального казначейства по Курской области Виды стипендий. Оcобенности назначения государственной социальной стипендии,

Виды стипендий. Оcобенности назначения государственной социальной стипендии, Loan Repayment Options: What You Need to Know

Loan Repayment Options: What You Need to Know Анализ капитальных вложений

Анализ капитальных вложений Инвестиция. Инвестициялар төмендегі мақсаттарды шешуге көмектеседі

Инвестиция. Инвестициялар төмендегі мақсаттарды шешуге көмектеседі Налог на доходы физических лиц

Налог на доходы физических лиц Персонал предприятия. Понятие и классификация персонала. Показатели эффективности использования трудовых ресурсов

Персонал предприятия. Понятие и классификация персонала. Показатели эффективности использования трудовых ресурсов Организационные основы проведения финансового контроля. (Лекция 3)

Организационные основы проведения финансового контроля. (Лекция 3) Как заработать больше, а тратить меньше

Как заработать больше, а тратить меньше Проект поддержки местных инициатив (ППМИ)

Проект поддержки местных инициатив (ППМИ) Денежные фонды и резервы организации

Денежные фонды и резервы организации Оценка финансово-хозяйственной деятельности предприятия в системе экономической безопасности предприятия

Оценка финансово-хозяйственной деятельности предприятия в системе экономической безопасности предприятия Зарплатный проект Газпромбанк

Зарплатный проект Газпромбанк О публичных обязательствах в 2018 году

О публичных обязательствах в 2018 году Price. Pricing Considerations

Price. Pricing Considerations Сутність страхування

Сутність страхування Фінансова стратегія підприємства

Фінансова стратегія підприємства Money show film - history of money

Money show film - history of money The official currency japanese, yen

The official currency japanese, yen Нормативная база ценообразования в строительстве. Сметно-нормативная база

Нормативная база ценообразования в строительстве. Сметно-нормативная база Государственный кредит

Государственный кредит Финансовый сектор экономики и основы его функционирования

Финансовый сектор экономики и основы его функционирования Бизнес-ангелы и их роль в современной экономике

Бизнес-ангелы и их роль в современной экономике Ценовая политика

Ценовая политика Бонистика. Виды бумажных денежных знаков и ценных бумаг

Бонистика. Виды бумажных денежных знаков и ценных бумаг