- Loan Repayment Options: What You Need to Know

Содержание

- 2. Topics Multiple Servicer Environment: Background & Update Grace Period & Repayment Plans: The Basics Know Your

- 3. Multiple Servicer Environment The ECASLA legislation (2008) allowed Lenders to sell FFEL loans to ED to

- 4. Multiple Servicer Environment: Split Borrowers “Split Borrowers”—Created when FFEL loans were purchased by ED, it resulted

- 5. Multiple Servicer Environment: Split Borrowers Solution: FSA has a transfer process that aligns all federally-held loans

- 6. Making it work… With the addition of new servicers challenges accompany growth and change Remember …

- 7. Grace Periods and Repayment Plans: The Basics

- 8. Grace Periods After a student graduates, leaves school, or drops below half-time enrollment, there is a

- 9. Reminder: Protect the Grace Period Of the borrowers who defaulted, most did not receive their full

- 10. Servicer Repayment Counseling Continue to establish a relationship with the borrower Update and enhance borrower contact

- 11. Repayment Plans Borrowers may repay their student loans through one of several repayment plans: Standard Repayment

- 12. Standard Plan Borrower pays a fixed amount each month Monthly payments will be at least $50.00

- 13. Graduated Plan Payments start out low and increase every two years The length of the repayment

- 14. Extended Plan Borrowers pay a fixed or graduated payment Repayment period is for up to 25

- 15. Alternative Plans An alternative repayment plan may be used when the terms and conditions of other

- 16. Income-Sensitive Repayment Income-Sensitive Repayment Plan for FFEL Loans only Monthly loan payment is based on the

- 17. Income Contingent Repayment (ICR) Direct Loans only Monthly payments are calculated on the basis of the

- 18. ICR - Continued The maximum repayment period is 25 years. If not fully repaid after 25

- 19. Income-Based Repayment (IBR) Income-Based Repayment is a plan created in 2007, for the major types of

- 20. IBR – New Application Process FSA is creating an electronic IBR application with an IRS data

- 21. Know Your Entitlements

- 22. Know Your Entitlements Understand Entitlements Deferments Forbearances Discharges Forgiveness Programs Loan Consolidation

- 23. Deferments Deferments allow a borrower to temporarily suspend or postpone their monthly payment in certain circumstances:

- 24. In-school Deferment In-school deferments are unlimited for borrowers enrolled at least half-time There are special parent

- 25. In-school Deferment Enrollment changes occur when students: Do not enroll at least half-time for the loan

- 26. In-school Deferment A scheduled break in enrollment, such as the summer session at many traditional 4-year

- 27. Graduate Fellowship/Rehabilitation Training Program Applies to Direct Loans (under special circumstances), FFEL, and Federal Perkins Loans

- 28. Unemployment Deferment Applicable for Direct Loans, FFEL, and Federal Perkins Loans Up to three years, usually

- 29. Economic Hardship Deferment Up to three years in 12-month increments if borrower is: Receiving payment under

- 30. Economic Hardship Deferment Available for Direct, FFEL, or Federal Perkins Loans For PLUS loans and Unsubsidized

- 31. Military Deferment Active Duty Available to borrowers in the Direct, FFEL, and Perkins Loan programs Borrowers

- 32. Available for Direct, FFEL, or Perkins Loan borrowers Must be a member of the National Guard

- 33. Forbearance Forbearance is a temporary postponement or reduction of payments for a period of time due

- 34. Forbearance May be requested: Based on poor health or other acceptable reason During medical internship or

- 35. Loan Forgiveness Borrowers may qualify to have all or a portion of their loan forgiven under

- 36. Teacher Loan Forgiveness Teacher service. If the borrower is a new borrower* and a full-time teacher

- 37. Public Service Loan Forgiveness In 2007, Congress created the Public Service Loan Forgiveness (PSLF) Program to

- 38. Loan Discharge Discharge or cancellation is the release of a borrower from their obligations to repay

- 39. Consolidation Loans A Consolidation Loan allows a borrower to consolidate (combine) multiple federal student loans into

- 40. Loan Consolidation Most federal student loans are eligible for consolidation, including subsidized and unsubsidized Direct and

- 41. Loan Consolidation If the borrower is in default, they must meet certain requirements before they can

- 42. Loan Consolidation Benefits of Consolidation: One Lender and One Monthly Payment Flexible Repayment Options Lower Monthly

- 43. What Students Should Know

- 44. NSLDS National Student Loan Data System (NSLDS)—A centralized database that stores information on all Department loans

- 45. Know Your Servicer Servicers are assigned when a Direct loan is disbursed/booked Borrowers receive welcome letters

- 46. Communication Channels for Borrowers All servicers have toll free numbers for borrowers to contact (phone, fax,

- 47. Repayment Tips for Students Borrow only what is needed Contact lender or financial aid office if

- 48. Repayment Tips for Students Once in default, loans are transferred to a collection agency Student loan

- 49. Tips for Students When students say : “I don’t need to borrow all this money” –

- 50. Tips for Students: Recordkeeping Create a file for: Financial aid award letters Loan counseling material Promissory

- 51. Know the Details of a Loan Students should know the details of their loan: Yearly and

- 52. Know About Capitalization Capitalization adds unpaid interest to the loan amount borrowed, and increases the unpaid

- 53. Calculators Repayment calculators are available for students to estimate their monthly payment amount under the different

- 54. Federal Servicer Contacts Nelnet www.nelnet.com 1-888-486-4722 Great Lakes Educational Loan Services, Inc. www.mygreatlakes.org 1-800-236-4300 Sallie Mae

- 56. Скачать презентацию

Topics

Multiple Servicer Environment: Background & Update

Grace Period & Repayment Plans: The

Topics

Multiple Servicer Environment: Background & Update

Grace Period & Repayment Plans: The

Multiple Servicer Environment

The ECASLA legislation (2008) allowed Lenders to sell FFEL

Multiple Servicer Environment

The ECASLA legislation (2008) allowed Lenders to sell FFEL

Multiple Servicer Environment: Split Borrowers

“Split Borrowers”—Created when FFEL loans were purchased

Multiple Servicer Environment: Split Borrowers

“Split Borrowers”—Created when FFEL loans were purchased

Multiple Servicer Environment:

Split Borrowers

Solution:

FSA has a transfer process that aligns

Multiple Servicer Environment:

Split Borrowers

Solution:

FSA has a transfer process that aligns

Making it work…

With the addition of new servicers

challenges accompany growth

Making it work…

With the addition of new servicers

challenges accompany growth

Grace Periods and Repayment Plans:

The Basics

The Basics

Grace Periods

After a student graduates, leaves school, or drops below

Grace Periods

After a student graduates, leaves school, or drops below

Reminder:

Protect the Grace Period

Of the borrowers who defaulted, most did

not

Reminder:

Protect the Grace Period

Of the borrowers who defaulted, most did

not

Servicer Repayment Counseling

Continue to establish a relationship with the borrower

Update and

Servicer Repayment Counseling

Continue to establish a relationship with the borrower

Update and

Repayment Plans

Borrowers may repay their student loans through one of several

Repayment Plans

Borrowers may repay their student loans through one of several

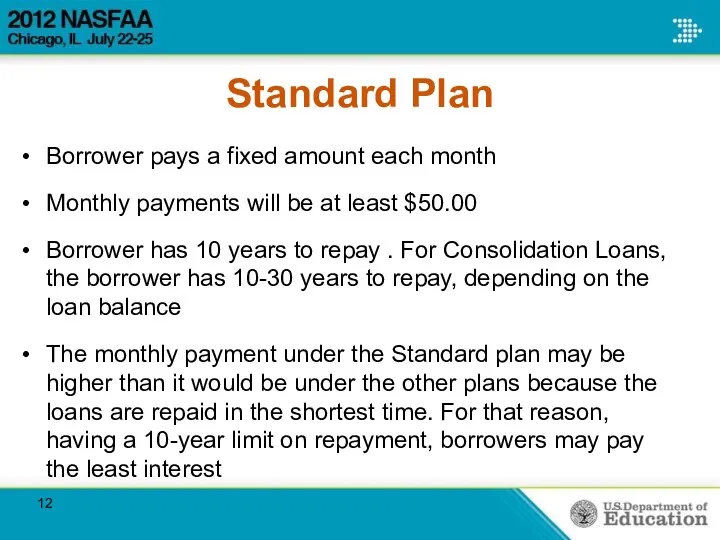

Standard Plan

Borrower pays a fixed amount each month

Monthly payments will be

Standard Plan

Borrower pays a fixed amount each month

Monthly payments will be

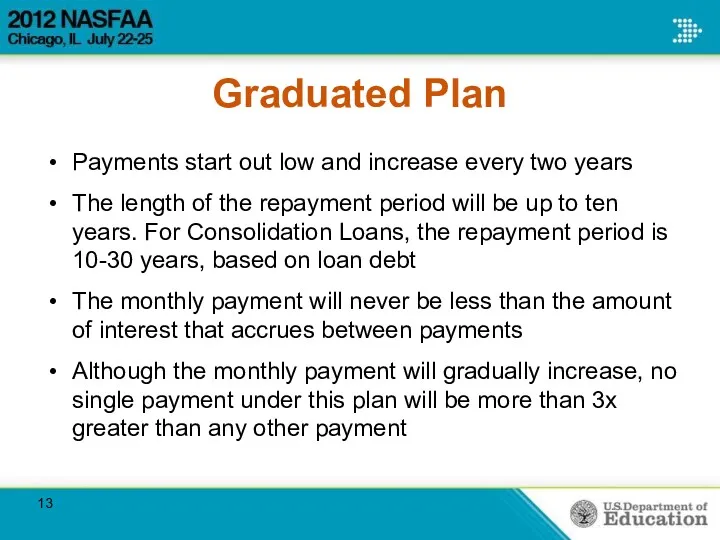

Graduated Plan

Payments start out low and increase every two years

The length

Graduated Plan

Payments start out low and increase every two years

The length

Extended Plan

Borrowers pay a fixed or graduated payment

Repayment period is

Extended Plan

Borrowers pay a fixed or graduated payment

Repayment period is

Alternative Plans

An alternative repayment plan may be used when the terms

Alternative Plans

An alternative repayment plan may be used when the terms

Income-Sensitive Repayment

Income-Sensitive Repayment Plan for FFEL Loans only

Monthly loan payment is

Income-Sensitive Repayment

Income-Sensitive Repayment Plan for FFEL Loans only

Monthly loan payment is

Income Contingent Repayment (ICR)

Direct Loans only

Monthly payments are calculated on the

Income Contingent Repayment (ICR)

Direct Loans only

Monthly payments are calculated on the

ICR - Continued

The maximum repayment period is 25 years. If not

ICR - Continued

The maximum repayment period is 25 years. If not

Income-Based Repayment (IBR)

Income-Based Repayment is a plan created in 2007,

Income-Based Repayment (IBR)

Income-Based Repayment is a plan created in 2007,

IBR – New Application Process

FSA is creating an electronic IBR application

IBR – New Application Process

FSA is creating an electronic IBR application

Know Your Entitlements

Know Your Entitlements

Understand Entitlements

Deferments

Forbearances

Discharges

Forgiveness Programs

Loan Consolidation

Know Your Entitlements

Understand Entitlements

Deferments

Forbearances

Discharges

Forgiveness Programs

Loan Consolidation

Deferments

Deferments allow a borrower to temporarily suspend or postpone their monthly

Deferments

Deferments allow a borrower to temporarily suspend or postpone their monthly

In-school Deferment

In-school deferments are unlimited for borrowers enrolled at least half-time

There

In-school Deferment

In-school deferments are unlimited for borrowers enrolled at least half-time

There

In-school Deferment

Enrollment changes occur when students:

Do not enroll at least half-time

In-school Deferment

Enrollment changes occur when students:

Do not enroll at least half-time

In-school Deferment

A scheduled break in enrollment, such as the summer session

In-school Deferment

A scheduled break in enrollment, such as the summer session

Graduate Fellowship/Rehabilitation Training Program

Applies to Direct Loans (under special circumstances), FFEL,

Graduate Fellowship/Rehabilitation Training Program

Applies to Direct Loans (under special circumstances), FFEL,

Unemployment Deferment

Applicable for Direct Loans, FFEL, and Federal Perkins Loans

Up to

Unemployment Deferment

Applicable for Direct Loans, FFEL, and Federal Perkins Loans

Up to

Economic Hardship Deferment

Up to three years in 12-month increments if borrower

Economic Hardship Deferment

Up to three years in 12-month increments if borrower

Economic Hardship Deferment

Available for Direct, FFEL, or Federal Perkins Loans

For PLUS

Economic Hardship Deferment

Available for Direct, FFEL, or Federal Perkins Loans

For PLUS

Military Deferment

Active Duty

Available to borrowers in the Direct, FFEL, and Perkins

Military Deferment

Active Duty

Available to borrowers in the Direct, FFEL, and Perkins

Available for Direct, FFEL, or Perkins Loan borrowers

Must be a

Available for Direct, FFEL, or Perkins Loan borrowers

Must be a

Forbearance

Forbearance is a temporary postponement or reduction of payments for a period

Forbearance

Forbearance is a temporary postponement or reduction of payments for a period

Forbearance

May be requested:

Based on poor health or other acceptable reason

During

Forbearance

May be requested:

Based on poor health or other acceptable reason

During

Loan Forgiveness

Borrowers may qualify to have all or a portion of

Loan Forgiveness

Borrowers may qualify to have all or a portion of

Teacher Loan Forgiveness

Teacher service. If the borrower is a new borrower*

Teacher Loan Forgiveness

Teacher service. If the borrower is a new borrower*

Public Service Loan Forgiveness

In 2007, Congress created the Public Service Loan

Public Service Loan Forgiveness

In 2007, Congress created the Public Service Loan

Loan Discharge

Discharge or cancellation is the release of a borrower from

Loan Discharge

Discharge or cancellation is the release of a borrower from

Consolidation Loans

A Consolidation Loan allows a borrower to consolidate (combine) multiple

Consolidation Loans

A Consolidation Loan allows a borrower to consolidate (combine) multiple

Loan Consolidation

Most federal student loans are eligible for consolidation, including subsidized

Loan Consolidation

Most federal student loans are eligible for consolidation, including subsidized

Loan Consolidation

If the borrower is in default, they must meet certain

Loan Consolidation

If the borrower is in default, they must meet certain

Loan Consolidation

Benefits of Consolidation:

One Lender and One Monthly Payment

Flexible

Loan Consolidation

Benefits of Consolidation:

One Lender and One Monthly Payment

Flexible

What Students Should Know

NSLDS

National Student Loan Data System (NSLDS)—A centralized database that stores information

NSLDS

National Student Loan Data System (NSLDS)—A centralized database that stores information

Know Your Servicer

Servicers are assigned when a Direct loan is disbursed/booked

Borrowers

Know Your Servicer

Servicers are assigned when a Direct loan is disbursed/booked

Borrowers

Communication Channels for Borrowers

All servicers have toll free numbers for borrowers

Communication Channels for Borrowers

All servicers have toll free numbers for borrowers

Repayment Tips for Students

Borrow only what is needed

Contact lender or financial

Repayment Tips for Students

Borrow only what is needed

Contact lender or financial

Repayment Tips for Students

Once in default, loans are transferred to a

Repayment Tips for Students

Once in default, loans are transferred to a

Tips for Students

When students say : “I don’t need to borrow

Tips for Students

When students say : “I don’t need to borrow

Tips for Students: Recordkeeping

Create a file for:

Financial aid award letters

Loan counseling

Tips for Students: Recordkeeping

Create a file for:

Financial aid award letters

Loan counseling

Know the Details of a Loan

Students should know the details of

Know the Details of a Loan

Students should know the details of

Know About Capitalization

Capitalization adds unpaid interest to the loan amount borrowed,

Know About Capitalization

Capitalization adds unpaid interest to the loan amount borrowed,

Calculators

Repayment calculators are available for students to estimate their monthly payment

Calculators

Repayment calculators are available for students to estimate their monthly payment

Federal Servicer Contacts

Nelnet

www.nelnet.com

1-888-486-4722

Great Lakes Educational Loan Services, Inc.

Federal Servicer Contacts

Nelnet

www.nelnet.com

1-888-486-4722

Great Lakes Educational Loan Services, Inc.

Финансы и кредит

Финансы и кредит Инвестиционный анализ и инвестиционное проектирование на предприятии

Инвестиционный анализ и инвестиционное проектирование на предприятии Становление и развитие социального страхования

Становление и развитие социального страхования Финансовый менеджмент международной фирмы

Финансовый менеджмент международной фирмы Participation banks in the financial system of Turkey

Participation banks in the financial system of Turkey Источники дохода. Стратегии финансового развития

Источники дохода. Стратегии финансового развития Временная стоимость денег. Тема 3

Временная стоимость денег. Тема 3 SCP-анализ

SCP-анализ Теория организации

Теория организации Финансовый анализ компании

Финансовый анализ компании Capital adequacy: BASEL 2 and BASEL 3

Capital adequacy: BASEL 2 and BASEL 3 Материнский капитал как социальная защита населения

Материнский капитал как социальная защита населения Финансирование инновационной деятельности

Финансирование инновационной деятельности Как работать с единым налоговым платежом

Как работать с единым налоговым платежом Теории, методы и инструменты управления банковской ликвидностью

Теории, методы и инструменты управления банковской ликвидностью Структура и объекты социальной защиты населения

Структура и объекты социальной защиты населения Основные задачи и функции Федеральной налоговой службы

Основные задачи и функции Федеральной налоговой службы Жилой Комплекс Окский берег. Государственная программа “Жилье для российской семьи” Нижний Новгород

Жилой Комплекс Окский берег. Государственная программа “Жилье для российской семьи” Нижний Новгород Образовательные мероприятия. Система Госфинансы. Обучающая презентация для сотрудников

Образовательные мероприятия. Система Госфинансы. Обучающая презентация для сотрудников Учет расчетов с покупателями и заказчиками. Анализ дебиторской и кредиторской задолженности на примере ООО ЧОП Далекс

Учет расчетов с покупателями и заказчиками. Анализ дебиторской и кредиторской задолженности на примере ООО ЧОП Далекс Электронный аукцион

Электронный аукцион Ипотечное кредитование для физических лиц

Ипотечное кредитование для физических лиц Механизм управления финансовым состоянием и пути его совершенствования

Механизм управления финансовым состоянием и пути его совершенствования Ценовая политика государства

Ценовая политика государства Анализ учета труда и заработной платы

Анализ учета труда и заработной платы Дистанционное хищение денежных средств граждан

Дистанционное хищение денежных средств граждан Управление проектами. Расчетная часть бизнес-проекта

Управление проектами. Расчетная часть бизнес-проекта Вопросник по внутреннему контролю финансового бизнес-цикла

Вопросник по внутреннему контролю финансового бизнес-цикла