- Time Value of Money

Содержание

- 2. After studying Chapter 3, you should be able to: Understand what is meant by "the time

- 3. The Time Value of Money The Interest Rate Simple Interest Compound Interest Amortizing a Loan Compounding

- 4. Obviously, $10,000 today. You already recognize that there is TIME VALUE TO MONEY!! The Interest Rate

- 5. TIME allows you the opportunity to postpone consumption and earn INTEREST. Why TIME? Why is TIME

- 6. Types of Interest Compound Interest Interest paid (earned) on any previous interest earned, as well as

- 7. Simple Interest Formula Formula SI = P0(i)(n) SI: Simple Interest P0: Deposit today (t=0) i: Interest

- 8. SI = P0(i)(n) = $1,000(.07)(2) = $140 Simple Interest Example Assume that you deposit $1,000 in

- 9. FV = P0 + SI = $1,000 + $140 = $1,140 Future Value is the value

- 10. The Present Value is simply the $1,000 you originally deposited. That is the value today! Present

- 11. Why Compound Interest? Future Value (U.S. Dollars)

- 12. Assume that you deposit $1,000 at a compound interest rate of 7% for 2 years. Future

- 13. FV1 = P0 (1+i)1 = $1,000 (1.07) = $1,070 Compound Interest You earned $70 interest on

- 14. FV1 = P0 (1+i)1 = $1,000 (1.07) = $1,070 FV2 = FV1 (1+i)1 = P0 (1+i)(1+i)

- 15. FV1 = P0(1+i)1 FV2 = P0(1+i)2 General Future Value Formula: FVn = P0 (1+i)n or FVn

- 16. FVIFi,n is found on Table I at the end of the book. Valuation Using Table I

- 17. FV2 = $1,000 (FVIF7%,2) = $1,000 (1.145) = $1,145 [Due to Rounding] Using Future Value Tables

- 18. Using MS Excel =FV(rate, nper, pmt,pv) =FV is a function used for calculating future value Rate=

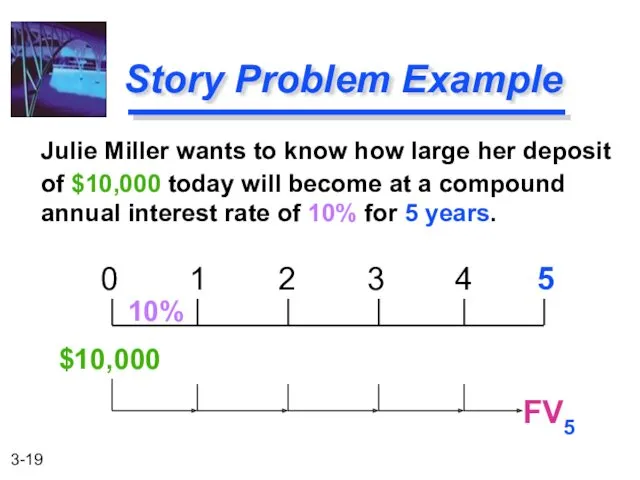

- 19. Julie Miller wants to know how large her deposit of $10,000 today will become at a

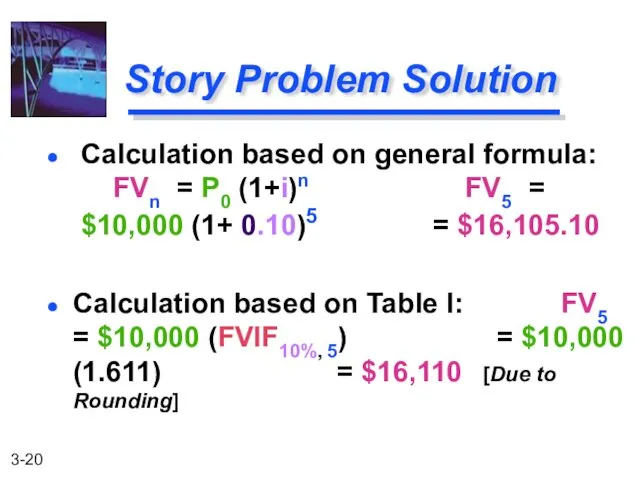

- 20. Calculation based on Table I: FV5 = $10,000 (FVIF10%, 5) = $10,000 (1.611) = $16,110 [Due

- 21. Using Excel =FV(0.1,5,,-10000) = $16,105.10 Interest = 10% or 0.1 Nper = 5 PV = -10,000

- 22. We will use the “Rule-of-72”. Double Your Money!!! Quick! How long does it take to double

- 23. Approx. Years to Double = 72 / i% 72 / 12% = 6 Years [Actual Time

- 24. Using Excel =nper(rate, pmt,pv, fv) =nper(.12,, -5000,10000) =6.11 years .

- 25. Assume that you need $1,000 in 2 years. Let’s examine the process to determine how much

- 26. PV0 = FV2 / (1+i)2 = $1,000 / (1.07)2 = FV2 / (1+i)2 = $873.44 Present

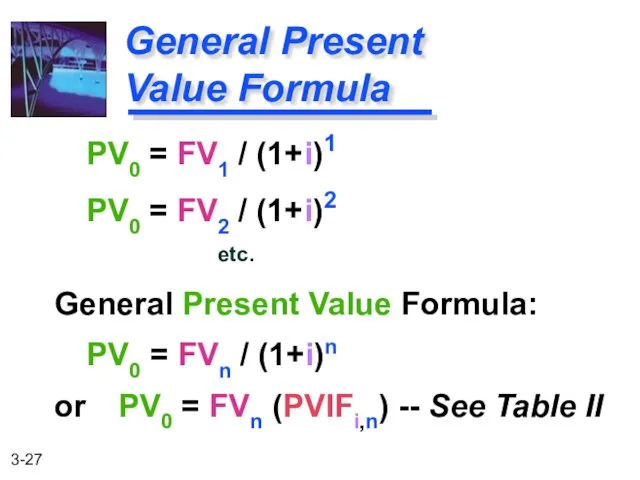

- 27. PV0 = FV1 / (1+i)1 PV0 = FV2 / (1+i)2 General Present Value Formula: PV0 =

- 28. PVIFi,n is found on Table II at the end of the book. Valuation Using Table II

- 29. PV2 = $1,000 (PVIF7%,2) = $1,000 (.873) = $873 [Due to Rounding] Using Present Value Tables

- 30. Julie Miller wants to know how large of a deposit to make so that the money

- 31. Calculation based on general formula: PV0 = FVn / (1+i)n PV0 = $10,000 / (1+ 0.10)5

- 32. Types of Annuities Ordinary Annuity: Payments or receipts occur at the end of each period. Annuity

- 33. Examples of Annuities Student Loan Payments Car Loan Payments Insurance Premiums Mortgage Payments Retirement Savings

- 34. Parts of an Annuity 0 1 2 3 $100 $100 $100 (Ordinary Annuity) End of Period

- 35. Parts of an Annuity 0 1 2 3 $100 $100 $100 (Annuity Due) Beginning of Period

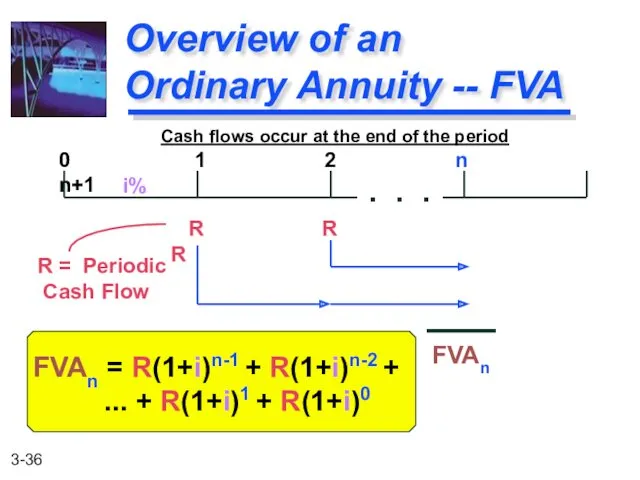

- 36. FVAn = R(1+i)n-1 + R(1+i)n-2 + ... + R(1+i)1 + R(1+i)0 Overview of an Ordinary Annuity

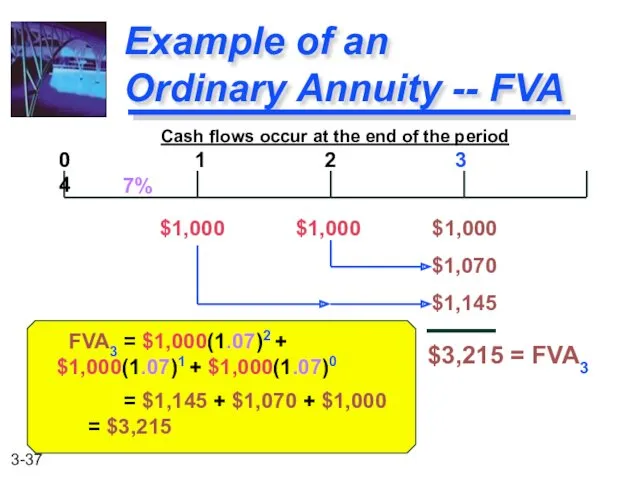

- 37. FVA3 = $1,000(1.07)2 + $1,000(1.07)1 + $1,000(1.07)0 = $1,145 + $1,070 + $1,000 = $3,215 Example

- 38. Hint on Annuity Valuation The future value of an ordinary annuity can be viewed as occurring

- 39. FVAn = R (FVIFAi%,n) FVA3 = $1,000 (FVIFA7%,3) = $1,000 (3.215) = $3,215 Valuation Using Table

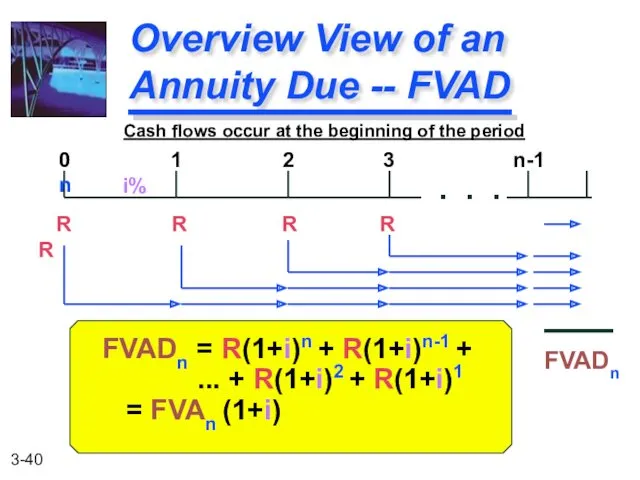

- 40. FVADn = R(1+i)n + R(1+i)n-1 + ... + R(1+i)2 + R(1+i)1 = FVAn (1+i) Overview View

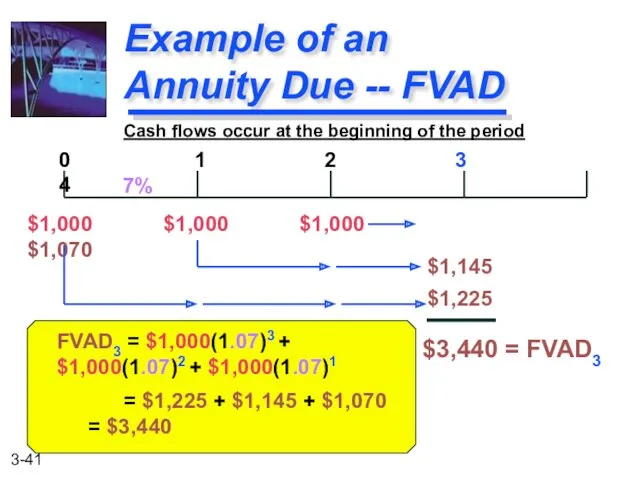

- 41. FVAD3 = $1,000(1.07)3 + $1,000(1.07)2 + $1,000(1.07)1 = $1,225 + $1,145 + $1,070 = $3,440 Example

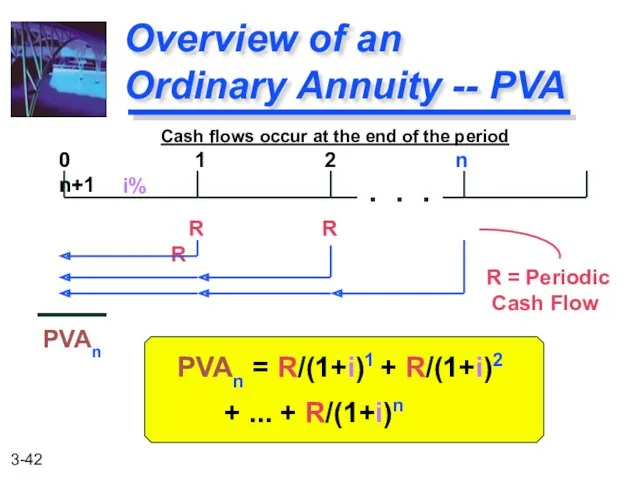

- 42. PVAn = R/(1+i)1 + R/(1+i)2 + ... + R/(1+i)n Overview of an Ordinary Annuity -- PVA

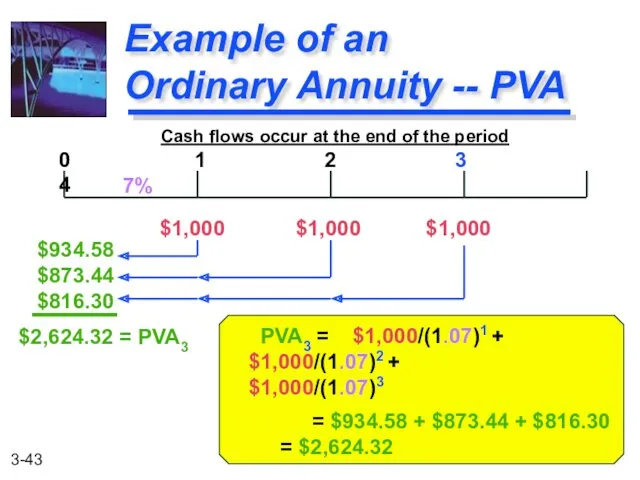

- 43. PVA3 = $1,000/(1.07)1 + $1,000/(1.07)2 + $1,000/(1.07)3 = $934.58 + $873.44 + $816.30 = $2,624.32 Example

- 44. Hint on Annuity Valuation The present value of an ordinary annuity can be viewed as occurring

- 45. PVAn = R (PVIFAi%,n) PVA3 = $1,000 (PVIFA7%,3) = $1,000 (2.624) = $2,624 Valuation Using Table

- 46. PVADn = R/(1+i)0 + R/(1+i)1 + ... + R/(1+i)n-1 = PVAn (1+i) Overview of an Annuity

- 47. PVADn = $1,000/(1.07)0 + $1,000/(1.07)1 + $1,000/(1.07)2 = $2,808.02 Example of an Annuity Due -- PVAD

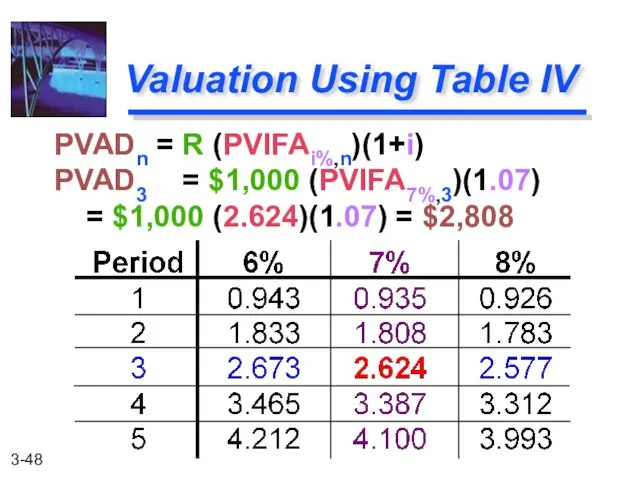

- 48. PVADn = R (PVIFAi%,n)(1+i) PVAD3 = $1,000 (PVIFA7%,3)(1.07) = $1,000 (2.624)(1.07) = $2,808 Valuation Using Table

- 49. Solving the PVAD Problem N I/Y PV PMT FV Inputs Compute 3 7 -1,000 0 2,808.02

- 50. 1. Read problem thoroughly 2. Create a time line 3. Put cash flows and arrows on

- 51. Julie Miller will receive the set of cash flows below. What is the Present Value at

- 52. 1. Solve a “piece-at-a-time” by discounting each piece back to t=0. 2. Solve a “group-at-a-time” by

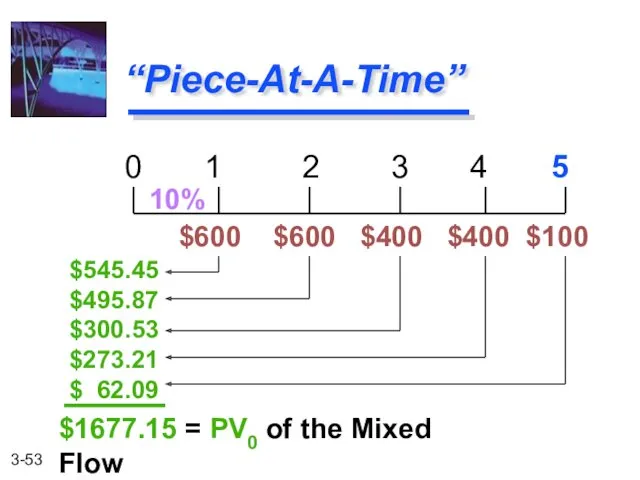

- 53. “Piece-At-A-Time” 0 1 2 3 4 5 $600 $600 $400 $400 $100 10% $545.45 $495.87 $300.53

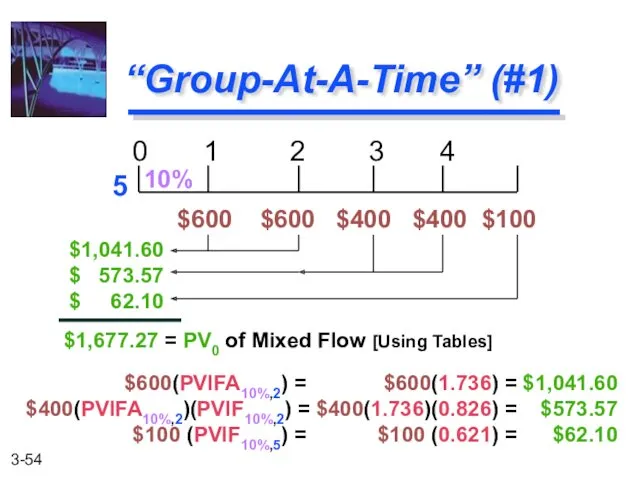

- 54. “Group-At-A-Time” (#1) 0 1 2 3 4 5 $600 $600 $400 $400 $100 10% $1,041.60 $

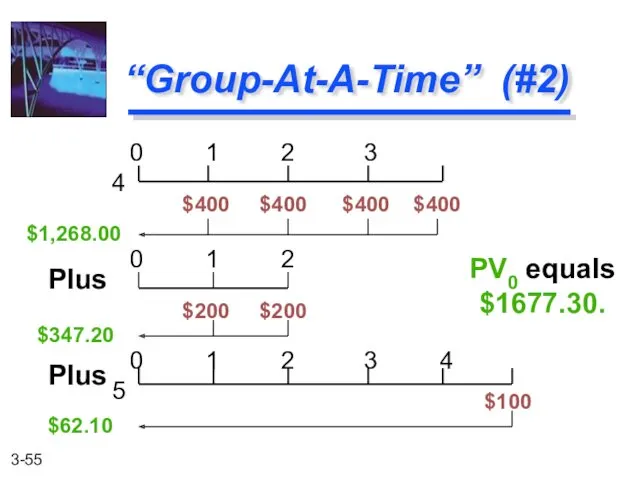

- 55. “Group-At-A-Time” (#2) 0 1 2 3 4 $400 $400 $400 $400 PV0 equals $1677.30. 0 1

- 56. General Formula: FVn = PV0(1 + [i/m])mn n: Number of Years m: Compounding Periods per Year

- 57. Julie Miller has $1,000 to invest for 2 Years at an annual interest rate of 12%.

- 58. Qrtly FV2 = 1,000(1+ [.12/4])(4)(2) = 1,266.77 Monthly FV2 = 1,000(1+ [.12/12])(12)(2) = 1,269.73 Daily FV2

- 59. Effective Annual Interest Rate The actual rate of interest earned (paid) after adjusting the nominal rate

- 60. Basket Wonders (BW) has a $1,000 CD at the bank. The interest rate is 6% compounded

- 61. 1. Calculate the payment per period. 2. Determine the interest in Period t. (Loan Balance at

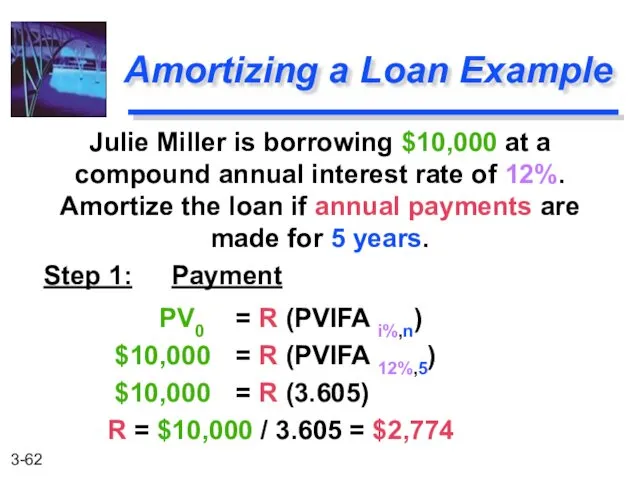

- 62. Julie Miller is borrowing $10,000 at a compound annual interest rate of 12%. Amortize the loan

- 63. Amortizing a Loan Example [Last Payment Slightly Higher Due to Rounding]

- 65. Скачать презентацию

After studying Chapter 3, you should be able to:

Understand what is

After studying Chapter 3, you should be able to:

Understand what is

The Time Value of Money

The Interest Rate

Simple Interest

Compound

The Time Value of Money

The Interest Rate

Simple Interest

Compound

Obviously, $10,000 today.

You already recognize that there is

TIME VALUE TO

Obviously, $10,000 today.

You already recognize that there is

TIME VALUE TO

TIME allows you the opportunity to postpone consumption and earn INTEREST.

Why

TIME allows you the opportunity to postpone consumption and earn INTEREST.

Why

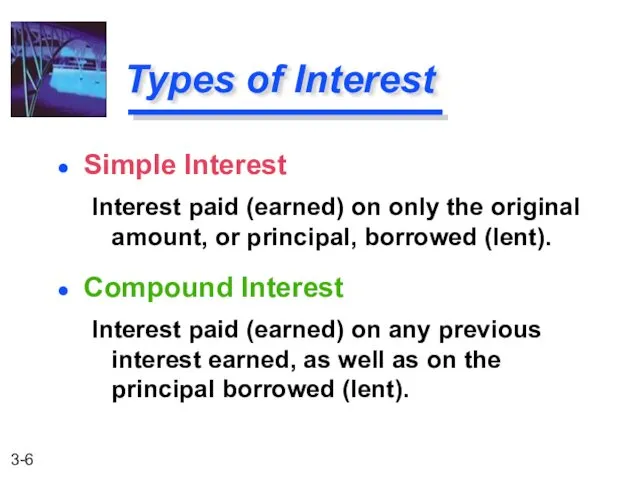

Types of Interest

Compound Interest

Interest paid (earned) on any previous interest earned,

Types of Interest

Compound Interest

Interest paid (earned) on any previous interest earned,

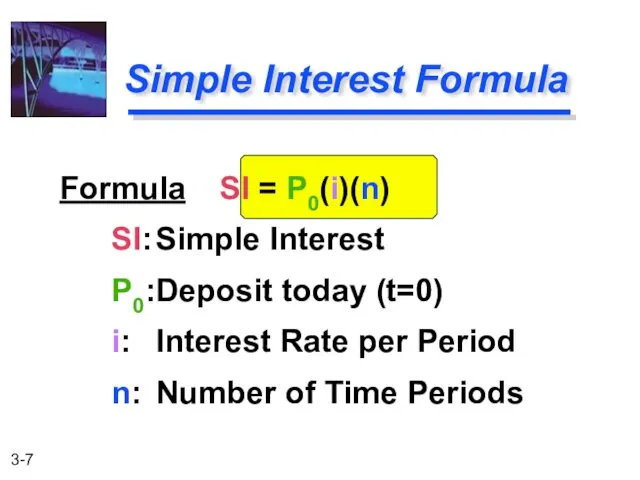

Simple Interest Formula

Formula SI = P0(i)(n)

SI: Simple Interest

P0: Deposit today (t=0)

i: Interest Rate per Period

n: Number

Simple Interest Formula

Formula SI = P0(i)(n)

SI: Simple Interest

P0: Deposit today (t=0)

i: Interest Rate per Period

n: Number

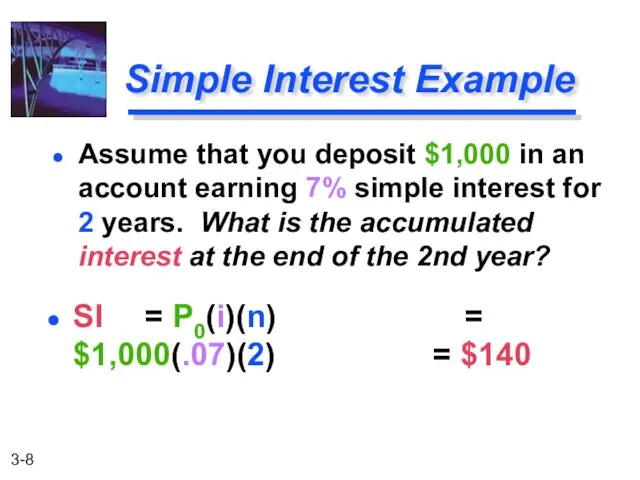

SI = P0(i)(n) = $1,000(.07)(2) = $140

Simple Interest Example

Assume that you deposit $1,000

SI = P0(i)(n) = $1,000(.07)(2) = $140

Simple Interest Example

Assume that you deposit $1,000

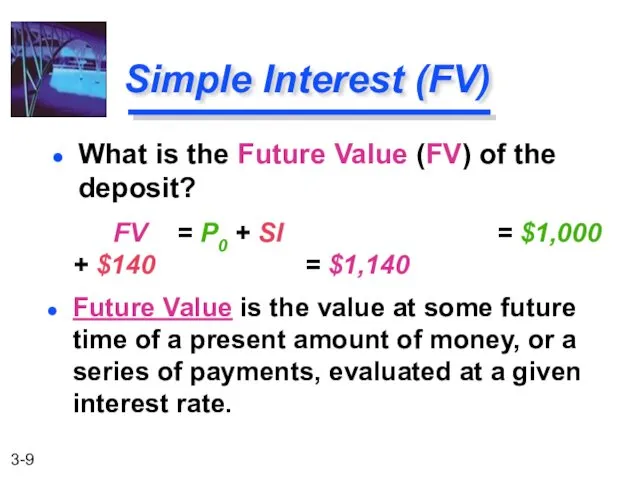

FV = P0 + SI = $1,000 + $140 = $1,140

Future Value

FV = P0 + SI = $1,000 + $140 = $1,140

Future Value

The Present Value is simply the $1,000 you originally deposited. That

The Present Value is simply the $1,000 you originally deposited. That

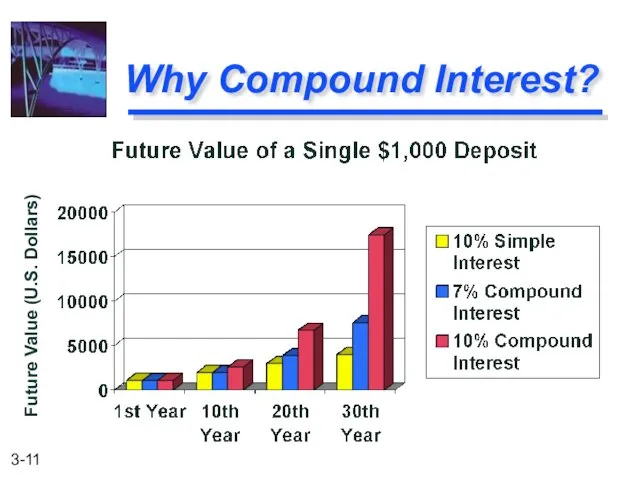

Why Compound Interest?

Future Value (U.S. Dollars)

Why Compound Interest?

Future Value (U.S. Dollars)

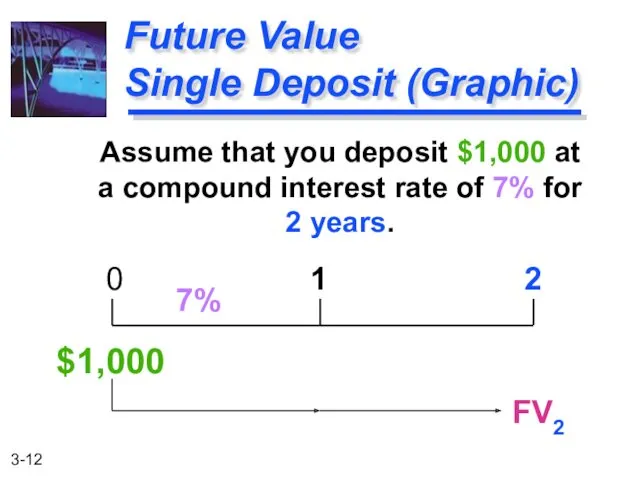

Assume that you deposit $1,000 at a compound interest rate of

Assume that you deposit $1,000 at a compound interest rate of

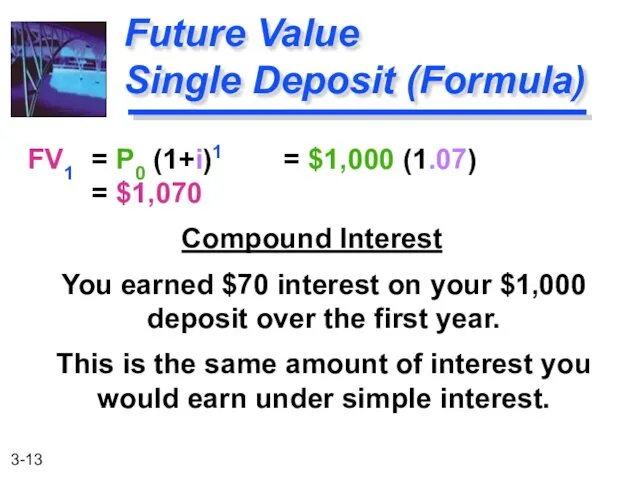

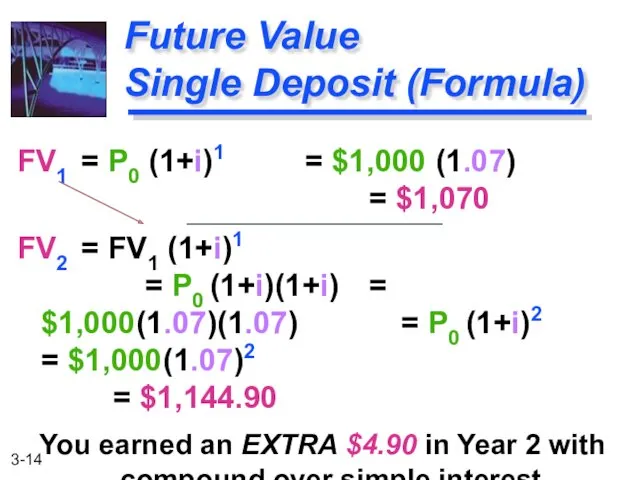

FV1 = P0 (1+i)1 = $1,000 (1.07) = $1,070

Compound Interest

You earned $70

FV1 = P0 (1+i)1 = $1,000 (1.07) = $1,070

Compound Interest

You earned $70

FV1 = P0 (1+i)1 = $1,000 (1.07) = $1,070

FV2 = FV1

FV1 = P0 (1+i)1 = $1,000 (1.07) = $1,070

FV2 = FV1

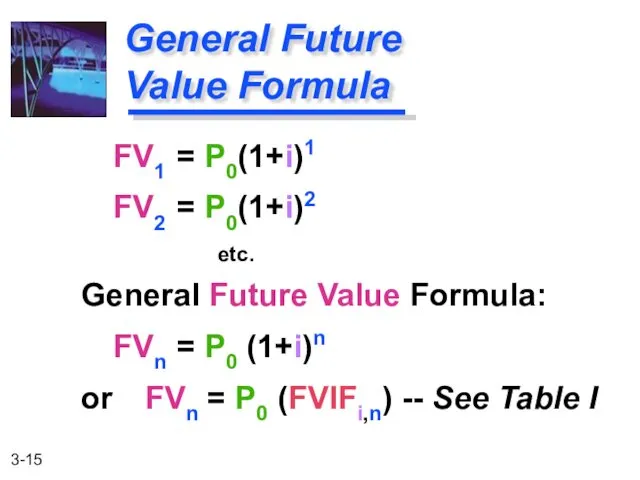

FV1 = P0(1+i)1

FV2 = P0(1+i)2

General Future Value Formula:

FVn = P0

FV1 = P0(1+i)1

FV2 = P0(1+i)2

General Future Value Formula:

FVn = P0

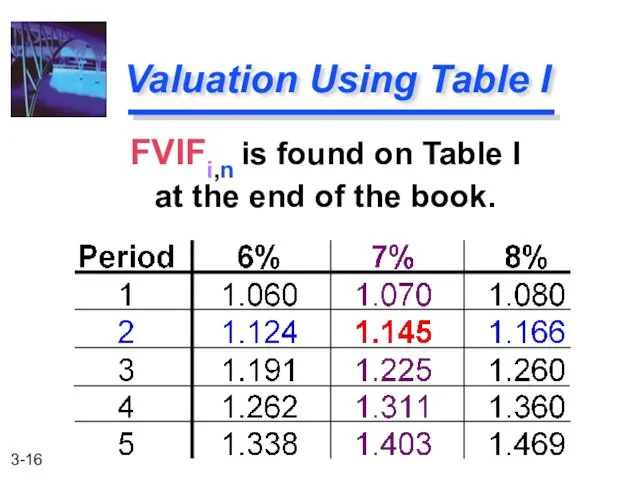

FVIFi,n is found on Table I

at the end of the

FVIFi,n is found on Table I

at the end of the

![FV2 = $1,000 (FVIF7%,2) = $1,000 (1.145) = $1,145 [Due to Rounding] Using Future Value Tables](/_ipx/f_webp&q_80&fit_contain&s_1440x1080/imagesDir/jpg/8371/slide-16.jpg)

FV2 = $1,000 (FVIF7%,2) = $1,000 (1.145) = $1,145 [Due to Rounding]

Using Future

FV2 = $1,000 (FVIF7%,2) = $1,000 (1.145) = $1,145 [Due to Rounding]

Using Future

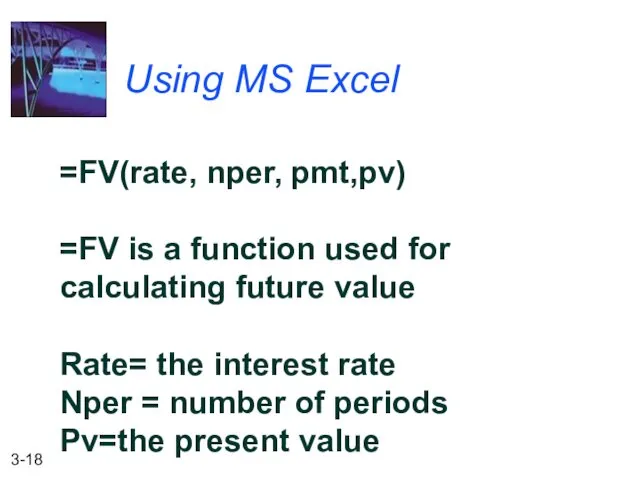

Using MS Excel

=FV(rate, nper, pmt,pv)

=FV is a function used for

Using MS Excel

=FV(rate, nper, pmt,pv)

=FV is a function used for

Julie Miller wants to know how large her deposit of $10,000

Julie Miller wants to know how large her deposit of $10,000

Calculation based on Table I: FV5 = $10,000 (FVIF10%, 5) = $10,000 (1.611) =

Calculation based on Table I: FV5 = $10,000 (FVIF10%, 5) = $10,000 (1.611) =

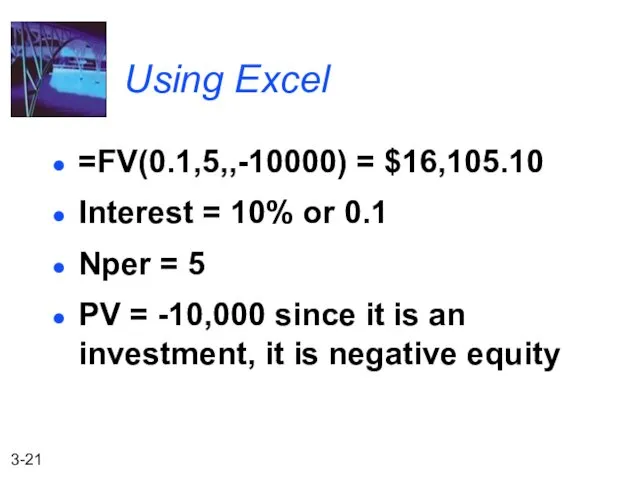

Using Excel

=FV(0.1,5,,-10000) = $16,105.10

Interest = 10% or 0.1

Nper = 5

PV

Using Excel

=FV(0.1,5,,-10000) = $16,105.10

Interest = 10% or 0.1

Nper = 5

PV

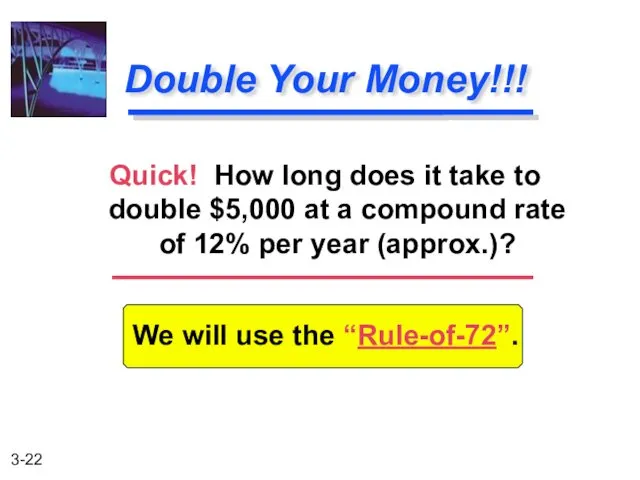

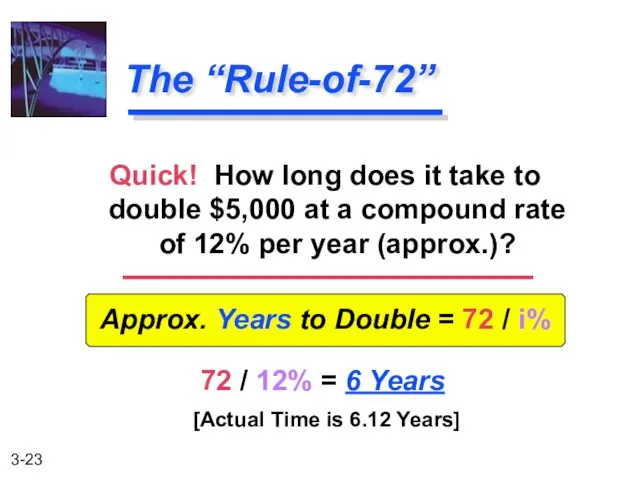

We will use the “Rule-of-72”.

Double Your Money!!!

Quick! How long does it

We will use the “Rule-of-72”.

Double Your Money!!!

Quick! How long does it

Approx. Years to Double = 72 / i%

72 / 12%

Approx. Years to Double = 72 / i%

72 / 12%

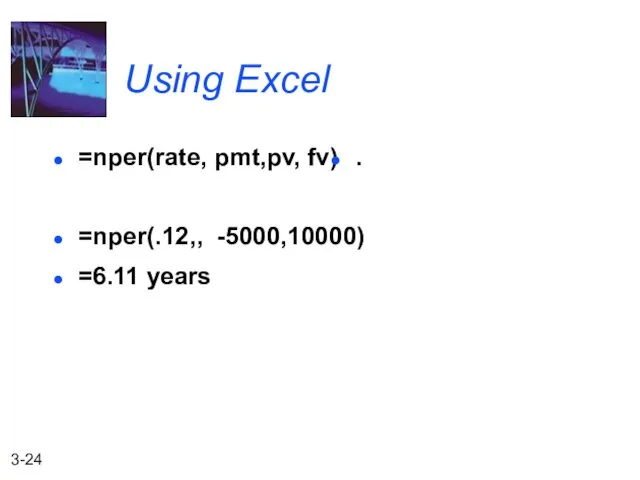

Using Excel

=nper(rate, pmt,pv, fv)

=nper(.12,, -5000,10000)

=6.11 years

.

Using Excel

=nper(rate, pmt,pv, fv)

=nper(.12,, -5000,10000)

=6.11 years

.

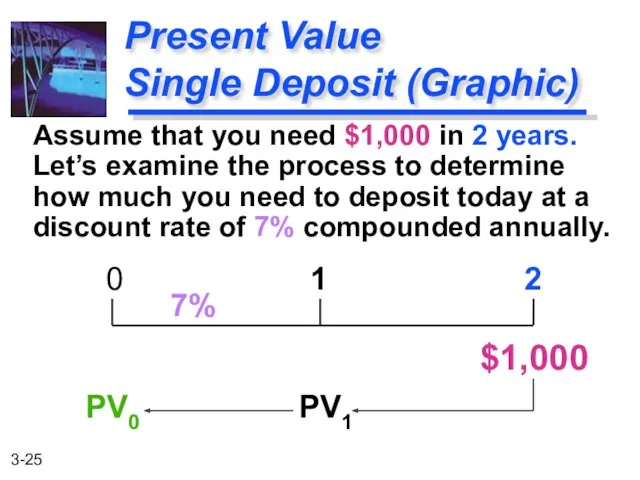

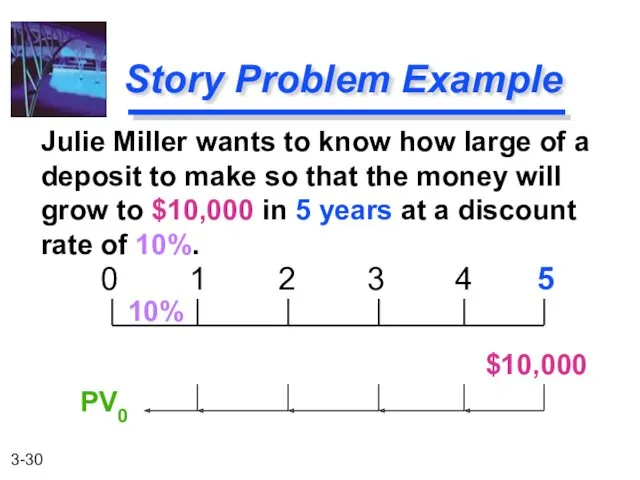

Assume that you need $1,000 in 2 years. Let’s examine the

Assume that you need $1,000 in 2 years. Let’s examine the

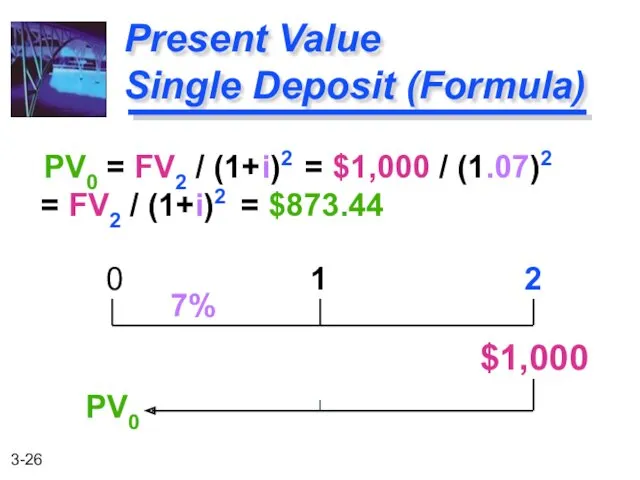

PV0 = FV2 / (1+i)2 = $1,000 / (1.07)2 =

PV0 = FV2 / (1+i)2 = $1,000 / (1.07)2 =

PV0 = FV1 / (1+i)1

PV0 = FV2 / (1+i)2

General Present

PV0 = FV1 / (1+i)1

PV0 = FV2 / (1+i)2

General Present

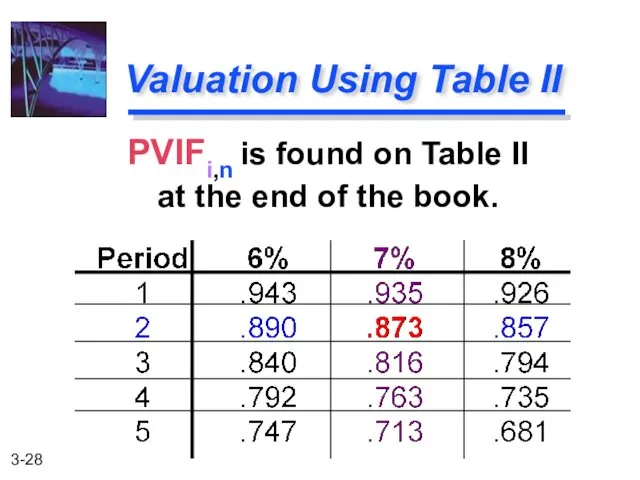

PVIFi,n is found on Table II

at the end of the

PVIFi,n is found on Table II

at the end of the

![PV2 = $1,000 (PVIF7%,2) = $1,000 (.873) = $873 [Due to Rounding] Using Present Value Tables](/_ipx/f_webp&q_80&fit_contain&s_1440x1080/imagesDir/jpg/8371/slide-28.jpg)

PV2 = $1,000 (PVIF7%,2) = $1,000 (.873) = $873 [Due to Rounding]

Using Present

PV2 = $1,000 (PVIF7%,2) = $1,000 (.873) = $873 [Due to Rounding]

Using Present

Julie Miller wants to know how large of a deposit to

Julie Miller wants to know how large of a deposit to

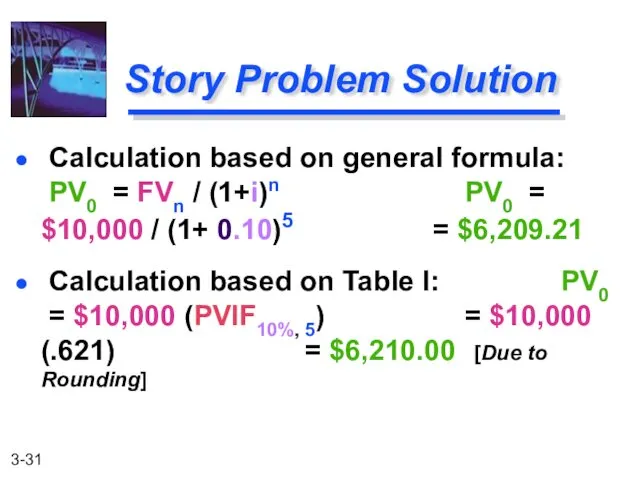

Calculation based on general formula: PV0 = FVn / (1+i)n PV0

Calculation based on general formula: PV0 = FVn / (1+i)n PV0

Types of Annuities

Ordinary Annuity: Payments or receipts occur at the end

Types of Annuities

Ordinary Annuity: Payments or receipts occur at the end

Examples of Annuities

Student Loan Payments

Car Loan Payments

Insurance Premiums

Examples of Annuities

Student Loan Payments

Car Loan Payments

Insurance Premiums

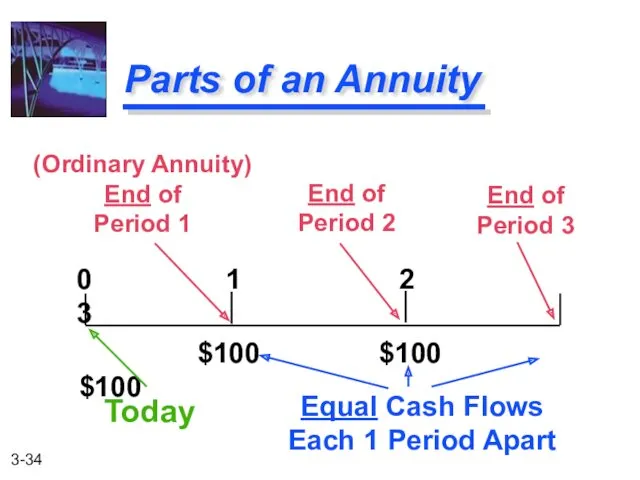

Parts of an Annuity

0 1 2 3

$100 $100 $100

(Ordinary Annuity)

End

Parts of an Annuity

0 1 2 3

$100 $100 $100

(Ordinary Annuity)

End

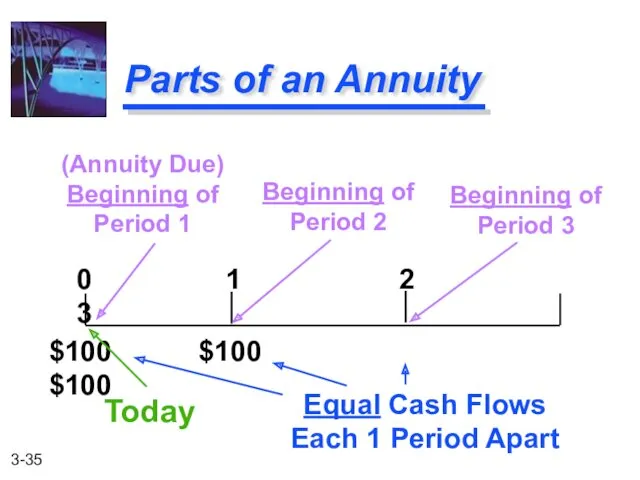

Parts of an Annuity

0 1 2 3

$100 $100 $100

(Annuity Due)

Beginning of

Period

Parts of an Annuity

0 1 2 3

$100 $100 $100

(Annuity Due)

Beginning of

Period

FVAn = R(1+i)n-1 + R(1+i)n-2 + ... + R(1+i)1 + R(1+i)0

Overview

FVAn = R(1+i)n-1 + R(1+i)n-2 + ... + R(1+i)1 + R(1+i)0

Overview

FVA3 = $1,000(1.07)2 + $1,000(1.07)1 + $1,000(1.07)0

= $1,145 +

FVA3 = $1,000(1.07)2 + $1,000(1.07)1 + $1,000(1.07)0

= $1,145 +

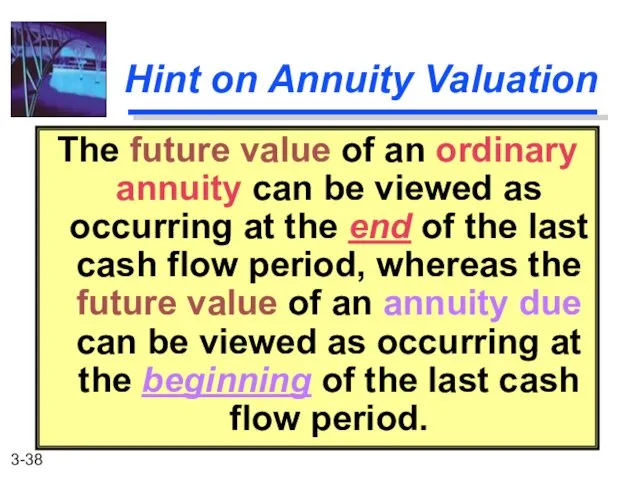

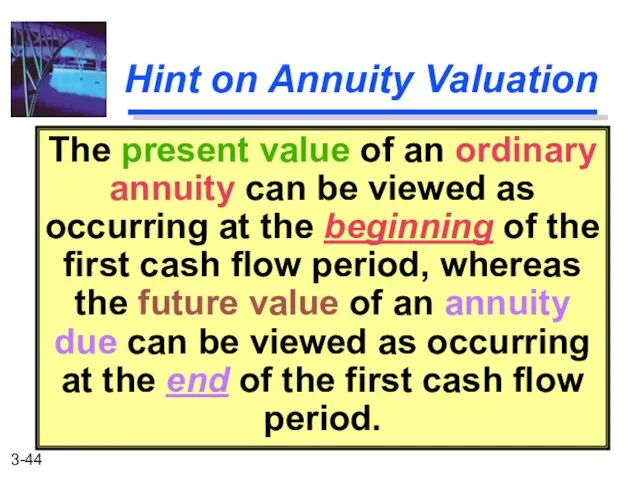

Hint on Annuity Valuation

The future value of an ordinary annuity can

Hint on Annuity Valuation

The future value of an ordinary annuity can

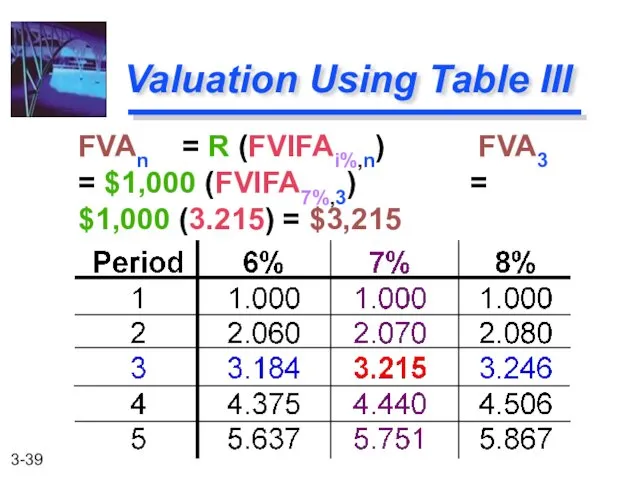

FVAn = R (FVIFAi%,n) FVA3 = $1,000 (FVIFA7%,3) = $1,000 (3.215) =

FVAn = R (FVIFAi%,n) FVA3 = $1,000 (FVIFA7%,3) = $1,000 (3.215) =

FVADn = R(1+i)n + R(1+i)n-1 + ... + R(1+i)2 + R(1+i)1

FVADn = R(1+i)n + R(1+i)n-1 + ... + R(1+i)2 + R(1+i)1

FVAD3 = $1,000(1.07)3 + $1,000(1.07)2 + $1,000(1.07)1

= $1,225 + $1,145

FVAD3 = $1,000(1.07)3 + $1,000(1.07)2 + $1,000(1.07)1

= $1,225 + $1,145

PVAn = R/(1+i)1 + R/(1+i)2

+ ... + R/(1+i)n

Overview of

PVAn = R/(1+i)1 + R/(1+i)2

+ ... + R/(1+i)n

Overview of

PVA3 = $1,000/(1.07)1 + $1,000/(1.07)2 + $1,000/(1.07)3

= $934.58 +

PVA3 = $1,000/(1.07)1 + $1,000/(1.07)2 + $1,000/(1.07)3

= $934.58 +

Hint on Annuity Valuation

The present value of an ordinary annuity can

Hint on Annuity Valuation

The present value of an ordinary annuity can

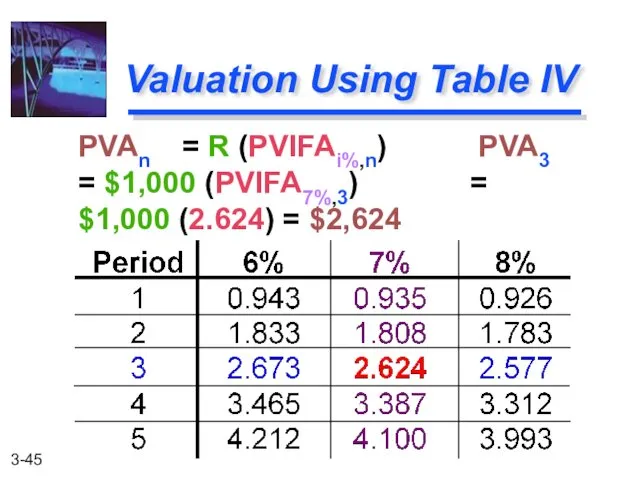

PVAn = R (PVIFAi%,n) PVA3 = $1,000 (PVIFA7%,3) = $1,000 (2.624) =

PVAn = R (PVIFAi%,n) PVA3 = $1,000 (PVIFA7%,3) = $1,000 (2.624) =

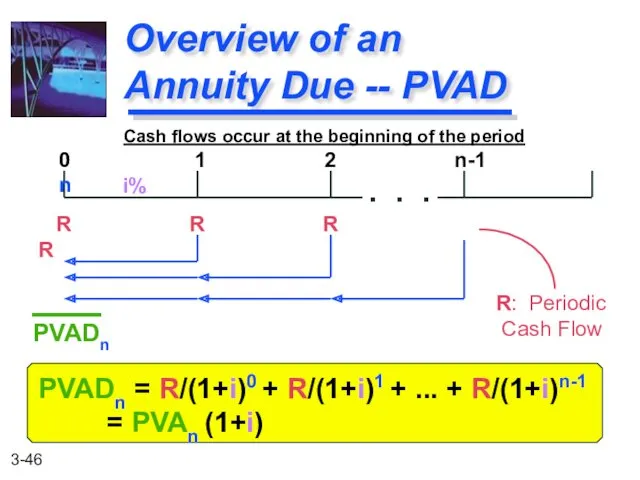

PVADn = R/(1+i)0 + R/(1+i)1 + ... + R/(1+i)n-1 = PVAn

PVADn = R/(1+i)0 + R/(1+i)1 + ... + R/(1+i)n-1 = PVAn

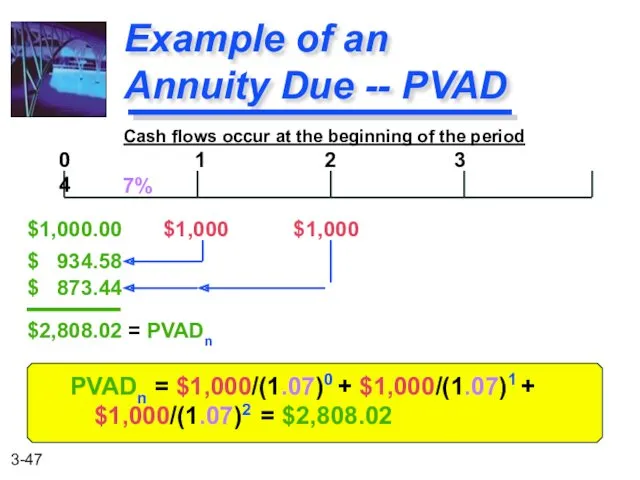

PVADn = $1,000/(1.07)0 + $1,000/(1.07)1 + $1,000/(1.07)2 = $2,808.02

Example of an

Annuity

PVADn = $1,000/(1.07)0 + $1,000/(1.07)1 + $1,000/(1.07)2 = $2,808.02

Example of an Annuity

PVADn = R (PVIFAi%,n)(1+i)

PVAD3 = $1,000 (PVIFA7%,3)(1.07) = $1,000 (2.624)(1.07) =

PVADn = R (PVIFAi%,n)(1+i)

PVAD3 = $1,000 (PVIFA7%,3)(1.07) = $1,000 (2.624)(1.07) =

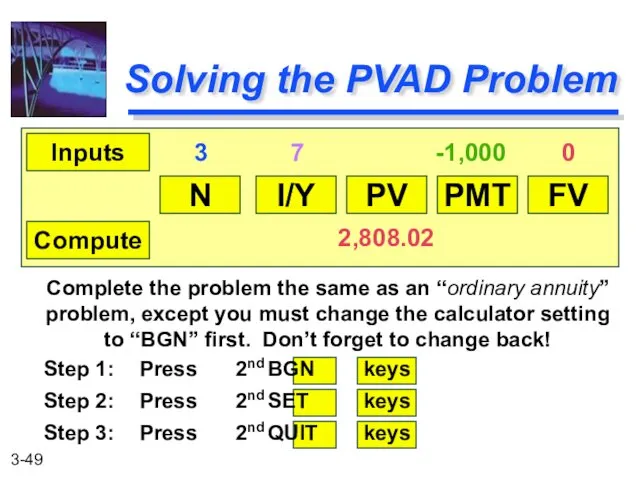

Solving the PVAD Problem

N

I/Y

PV

PMT

FV

Inputs

Compute

3 7 -1,000 0

2,808.02

Complete the problem

Solving the PVAD Problem

N

I/Y

PV

PMT

FV

Inputs

Compute

3 7 -1,000 0

2,808.02

Complete the problem

1. Read problem thoroughly

2. Create a time line

3. Put cash flows

1. Read problem thoroughly

2. Create a time line

3. Put cash flows

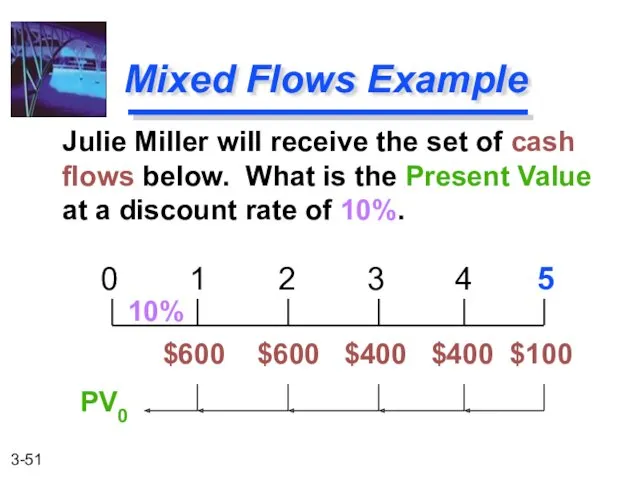

Julie Miller will receive the set of cash flows below. What

Julie Miller will receive the set of cash flows below. What

1. Solve a “piece-at-a-time” by discounting each piece back to t=0.

2. Solve a

1. Solve a “piece-at-a-time” by discounting each piece back to t=0.

2. Solve a

“Piece-At-A-Time”

0 1 2 3 4 5

$600 $600 $400 $400

“Piece-At-A-Time”

0 1 2 3 4 5

$600 $600 $400 $400

“Group-At-A-Time” (#1)

0 1 2 3 4 5

$600 $600 $400

“Group-At-A-Time” (#1)

0 1 2 3 4 5

$600 $600 $400

“Group-At-A-Time” (#2)

0 1 2 3 4

$400 $400 $400 $400

PV0

“Group-At-A-Time” (#2)

0 1 2 3 4

$400 $400 $400 $400

PV0

![General Formula: FVn = PV0(1 + [i/m])mn n: Number of](/_ipx/f_webp&q_80&fit_contain&s_1440x1080/imagesDir/jpg/8371/slide-55.jpg)

General Formula:

FVn = PV0(1 + [i/m])mn

n: Number of Years m: Compounding Periods per

General Formula:

FVn = PV0(1 + [i/m])mn

n: Number of Years m: Compounding Periods per

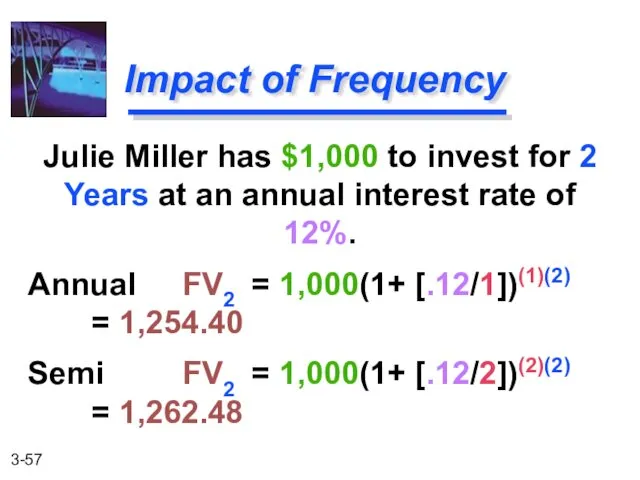

Julie Miller has $1,000 to invest for 2 Years at an

Julie Miller has $1,000 to invest for 2 Years at an

![Qrtly FV2 = 1,000(1+ [.12/4])(4)(2) = 1,266.77 Monthly FV2 =](/_ipx/f_webp&q_80&fit_contain&s_1440x1080/imagesDir/jpg/8371/slide-57.jpg)

Qrtly FV2 = 1,000(1+ [.12/4])(4)(2) = 1,266.77

Monthly FV2 = 1,000(1+ [.12/12])(12)(2) = 1,269.73

Daily

Qrtly FV2 = 1,000(1+ [.12/4])(4)(2) = 1,266.77

Monthly FV2 = 1,000(1+ [.12/12])(12)(2) = 1,269.73

Daily

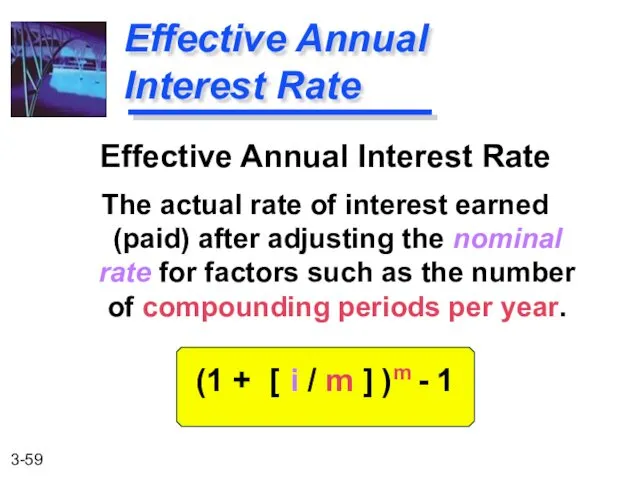

Effective Annual Interest Rate

The actual rate of interest earned (paid) after

Effective Annual Interest Rate

The actual rate of interest earned (paid) after

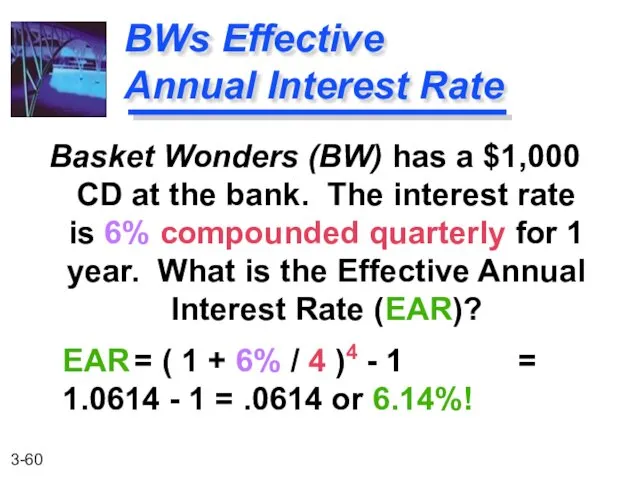

Basket Wonders (BW) has a $1,000 CD at the bank. The

Basket Wonders (BW) has a $1,000 CD at the bank. The

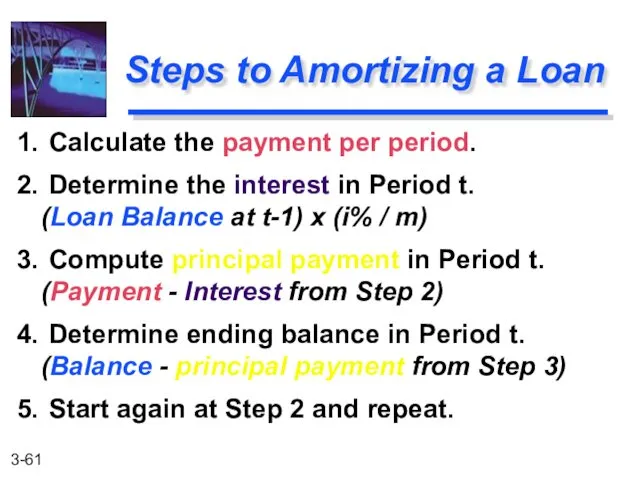

1. Calculate the payment per period.

2. Determine the interest in Period t. (Loan

1. Calculate the payment per period.

2. Determine the interest in Period t. (Loan

Julie Miller is borrowing $10,000 at a compound annual interest rate

Julie Miller is borrowing $10,000 at a compound annual interest rate

![Amortizing a Loan Example [Last Payment Slightly Higher Due to Rounding]](/_ipx/f_webp&q_80&fit_contain&s_1440x1080/imagesDir/jpg/8371/slide-62.jpg)

Amortizing a Loan Example

[Last Payment Slightly Higher Due to Rounding]

Amortizing a Loan Example

[Last Payment Slightly Higher Due to Rounding]

Понятная кредитная карта

Понятная кредитная карта Инструкция тайного покупателя

Инструкция тайного покупателя Понятие кризиса и антикризисного управления

Понятие кризиса и антикризисного управления Кредит, его сущность, содержание и виды

Кредит, его сущность, содержание и виды Потоки платежей

Потоки платежей Финансовый анализ

Финансовый анализ Износ и амортизация основных фондов

Износ и амортизация основных фондов Аналіз фінансового стану малого бізнесу

Аналіз фінансового стану малого бізнесу International Banking & Wealth Management. AML Quality & Control. Effective Anti – Money Laundering

International Banking & Wealth Management. AML Quality & Control. Effective Anti – Money Laundering Меры поддержки бизнеса в Пермском крае

Меры поддержки бизнеса в Пермском крае Единовременные ежегодные выплаты как форма поддержки молодых специалистов Калужской области

Единовременные ежегодные выплаты как форма поддержки молодых специалистов Калужской области Налог на добавленную стоимость – гл. 21 НК РФ

Налог на добавленную стоимость – гл. 21 НК РФ Составление смет на ремонтно-строительные работы

Составление смет на ремонтно-строительные работы Налоги и вычеты

Налоги и вычеты О ценообразовании в области регулируемых цен в электроэнергетике

О ценообразовании в области регулируемых цен в электроэнергетике Внутренние источники информации для финансового анализа российских организаций

Внутренние источники информации для финансового анализа российских организаций Бюджет для граждан Старооскольского городского округа на 2015 год и на плановый период 2016 и 2017 годов

Бюджет для граждан Старооскольского городского округа на 2015 год и на плановый период 2016 и 2017 годов Вклады. Цифровой турнир по финансовой грамотности

Вклады. Цифровой турнир по финансовой грамотности Операции банка с драгоценными металлами. Управление золото-валютными резервами

Операции банка с драгоценными металлами. Управление золото-валютными резервами Підвищення пенсійних виплат з 1 травня 2017 року

Підвищення пенсійних виплат з 1 травня 2017 року Финансовые ресурсы, резервы, связь с кредитными ресурсами

Финансовые ресурсы, резервы, связь с кредитными ресурсами Проект YourKarma

Проект YourKarma Оборотные средства предприятия

Оборотные средства предприятия Термин лизинг

Термин лизинг Краткий обзор контура Эльба - сервис онлайн-бухгалтерии

Краткий обзор контура Эльба - сервис онлайн-бухгалтерии ТС Центральный парк-9. Итоги работы (II квартал 2023 год)

ТС Центральный парк-9. Итоги работы (II квартал 2023 год) Монетарная политика

Монетарная политика Доходный подход в оценке бизнеса

Доходный подход в оценке бизнеса