International Banking & Wealth Management. AML Quality & Control. Effective Anti – Money Laundering презентация

- International Banking & Wealth Management. AML Quality & Control. Effective Anti – Money Laundering

Содержание

- 2. Schedule: Money Laundering Defined Effective Due Diligence – Know your Client Trusts – Foundations - Complex

- 3. Money Laundering Defined When committed intentionally, Money Laundering, is defined as: the conversion or transfer of

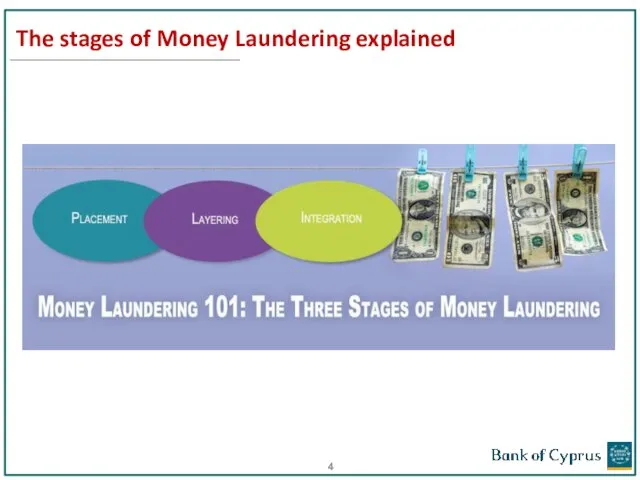

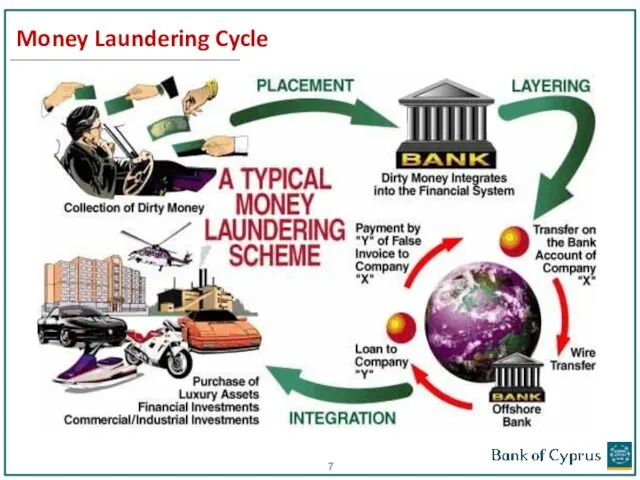

- 4. The stages of Money Laundering explained Layering Integration

- 5. The stages of Money Laundering explained Placement is the introduction of unlawful proceeds into the financial

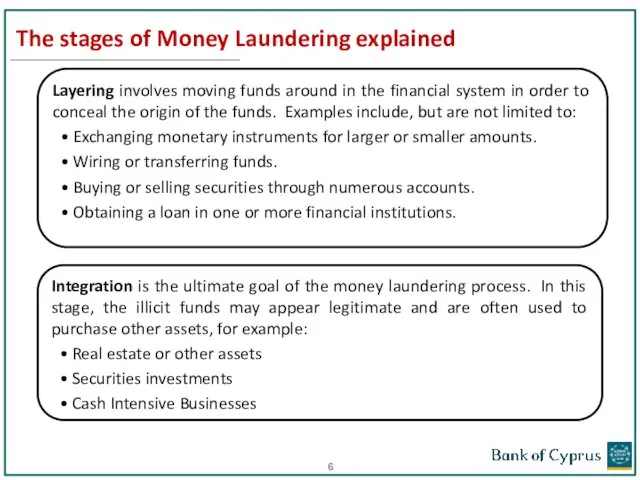

- 6. The stages of Money Laundering explained Layering involves moving funds around in the financial system in

- 7. Money Laundering Cycle

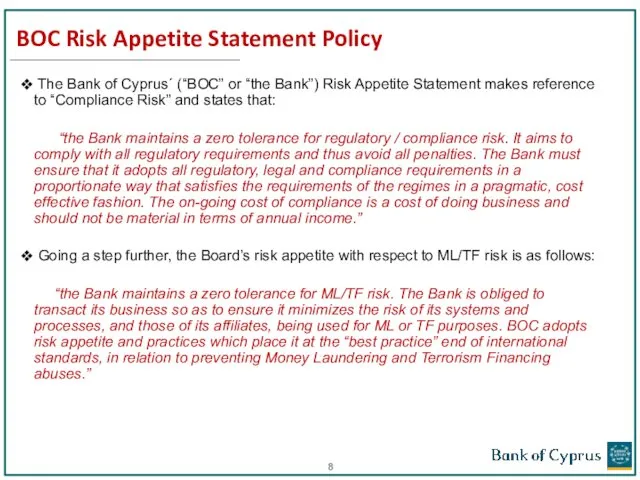

- 8. BOC Risk Appetite Statement Policy The Bank of Cyprus´ (“BOC” or “the Bank”) Risk Appetite Statement

- 9. It all comes down to: KNOW YOUR CLIENT Know your client (KYC) is the process of

- 10. KNOW YOUR CLIENT – the client profile Customer Due Diligence(CDD) – one of the measures to

- 11. Who is the customer – the UBO / physical person exercising management and control (all related

- 12. WHO IS THE ULTIMATE BENEFICIAL OWNER? The natural person(s) who ultimately owns or controls a customer

- 13. Client take-on – On-boarding Good practice examples Files contain a customer overview Establishing and documenting PEP

- 14. How far should you extend your CDD? SOURCE OF WEALTH How a customer became wealthy Was

- 15. Source of Wealth: Generic source of wealth descriptions are not acceptable e.g. “savings”, “from family”, “from

- 16. Source of Wealth: There is a wide array of sound practices to answer these questions until

- 17. Enhanced Due Diligence (EDD) EDD: A greater level of CDD undertaken for high risk entities. It

- 18. Enhanced Due Diligence (EDD) Before a client is opened in the system check: Legal & commercial

- 19. Customer Profile - Enhanced CDD measures - examples Obtaining additional information on the customer (e.g. occupation,

- 20. Politically Exposed Persons (PEPs) FATF Definition PEPs are individuals who are or have been entrusted with

- 21. Identifying PEPs (i) Natural persons who have, or had a prominent public function in the Republic

- 22. Identifying PEPs (cont’d) (ii) “Immediate family members” of PEPs include the following persons: 1. the spouse;

- 23. PEPs Informal, undocumented processes for identifying, classifying and declassifying customers as PEPs. People cease to be

- 24. Definition of Private Banking client for AML purposes Private Banking clients are considered to be high

- 25. Legal Structures and Corporate Vehicles There are numerous types of entities, which Legally make businesses Own

- 26. TRUST A trust is an arrangement where a person (the settlor) gives money or property to

- 27. TRUST

- 28. Beneficial Owners of a Trust Any individual, who has vested interest in at least 10% of

- 29. FOUNDATION The Foundation is a legal entity comparable to that of a company. The Foundation has

- 30. Chart of a PRIVATE FOUNDATION

- 31. Beneficial Owners of Private Foundations Where the individuals that benefit, have been determined: Anyone who benefits

- 32. RISKS OF TRUSTS, FOUNDATIONS Defraud authorities, creditors, commercial disputes Tax evasion vehicle (declaring as charitable) Service

- 33. RED FLAGS: Unexplained relationship between settlor, beneficiaries, controllers, property and 3rd parties Change of beneficiaries without

- 34. Sophisticated, Complex Legal Structures * Refer to OE151 for the definition of a complex structure (BOC

- 35. Why are legal structures complicated? Multiple layers of ownership with one or more entities (in each

- 36. Why are legal structures complicated and Risky?

- 37. Money laundering through Real Estate sector Classic method of laundering dirty money, particularly in countries with

- 38. RED FLAGS: Cash deposits Renovation and reselling as high-end property 3rd party payment Using a Loan

- 39. Trade-Based Money laundering One of the most sophisticated methods of cleaning dirty money Among the hardest

- 40. RED FLAGS: Significant discrepancies ? bill of lading-invoice (authenticity) Significant discrepancies ? value on invoice-market Type

- 41. Reliance on third parties for customer identification and due diligence purposes - Introduction Article 67 of

- 42. Definition of ‘third party’ A credit or financial institution or auditors or accountants or tax consultants

- 43. Business Associates Independent Professionals, natural or legal persons, who recommend customers to open accounts with the

- 44. Definition of Terrorist Financing By any means, directly or indirectly, Unlawfully and willfully, provides or collects

- 45. The Terrorist Financing Process Funds used to finance terrorism are considered an 'instrument of crime' (which

- 46. Differences between ML and TF

- 47. Terrorist Financing Red Flags The stated occupation of the customer is not in line with the

- 48. Terrorist Financing Red Flags Regarding nonprofit or charitable organizations, financial transactions occur for which there appears

- 49. Direct operational cost of Terrorist Attacks (Estimates)

- 50. Real – Life Case: The 9/11 Terrorist Attacks Funding for the 9/11 terrorist attacks has been

- 51. What are Sanctions? Sanctions are unilateral or multilateral economic actions taken against a target to influence

- 52. Who issues Sanctions? United Nations (UN) Resolutions can result in sanctions. If you live in a

- 53. EU Sanctions General The European Commission proposes restrictive measures and adopts a Common Position. Sanctions are

- 54. OFAC Sanctions General The US Treasury Department’s Office of Foreign Assets Control (OFAC) administers and enforces

- 55. OFAC Sanctions (cont.) OFAC Sanctions apply to: Everyone in the US, including foreign entities or individuals

- 56. Sanctions Type & Scope Sanctions can be: Specific ? Relate to specific lists of named individuals,

- 57. Sanctions Vs AML

- 58. Sanctions Evasions Forgery of documents Nested accounts Stripping wires Restructuring of corporate entities Re-routing of transactions

- 59. Sanctions & Embargoes Regulators are very serious – fines can be huge:

- 60. Effective Transaction Monitoring Article 58(e) of the Law What is required is a “detailed examination of

- 61. Effective Transaction Monitoring In practice, where a client’s instruction or transaction or behavior is not consistent

- 62. CUSTOMER REVIEW PROCESS Financial regulators require banks and non-banking financial institutions to perform AML KYC due

- 63. CUSTOMER REVIEW PROCESS A review should be performed when an unusual and/or significant transaction takes place,

- 64. CUSTOMER REVIEW PROCESS Review each customer's information: name, address, ID number, certificate of good standing (if

- 65. CUSTOMER REVIEW PROCESS The number of enquiries received from Correspondent Banks The number of filtering alerts

- 66. CUSTOMER REVIEW PROCESS Transaction Monitoring during the review: Need to check that the transactions processed in

- 67. A SAR is born! All should be aware of when and how to submit a suspicion

- 68. The “Suspicion Spectrum” It is important to understand the above so that there is comfort when

- 70. Скачать презентацию

Schedule:

Money Laundering Defined

Effective Due Diligence – Know your Client

Trusts –

Schedule:

Money Laundering Defined

Effective Due Diligence – Know your Client

Trusts –

Money Laundering Defined

When committed intentionally, Money Laundering, is defined as:

the conversion

Money Laundering Defined

When committed intentionally, Money Laundering, is defined as:

the conversion

The stages of Money Laundering explained

Layering

Integration

The stages of Money Laundering explained

Layering

Integration

The stages of Money Laundering explained

Placement is the introduction of unlawful

The stages of Money Laundering explained

Placement is the introduction of unlawful

The stages of Money Laundering explained

Layering involves moving funds around in

The stages of Money Laundering explained

Layering involves moving funds around in

Money Laundering Cycle

Money Laundering Cycle

BOC Risk Appetite Statement Policy

The Bank of Cyprus´ (“BOC” or

BOC Risk Appetite Statement Policy

The Bank of Cyprus´ (“BOC” or

It all comes down to: KNOW YOUR CLIENT

Know your client (KYC) is

It all comes down to: KNOW YOUR CLIENT

Know your client (KYC) is

KNOW YOUR CLIENT – the client profile

Customer Due Diligence(CDD) –

KNOW YOUR CLIENT – the client profile

Customer Due Diligence(CDD) –

Who is the customer – the UBO / physical person

Who is the customer – the UBO / physical person

WHO IS THE ULTIMATE BENEFICIAL OWNER?

The natural person(s) who ultimately owns

WHO IS THE ULTIMATE BENEFICIAL OWNER?

The natural person(s) who ultimately owns

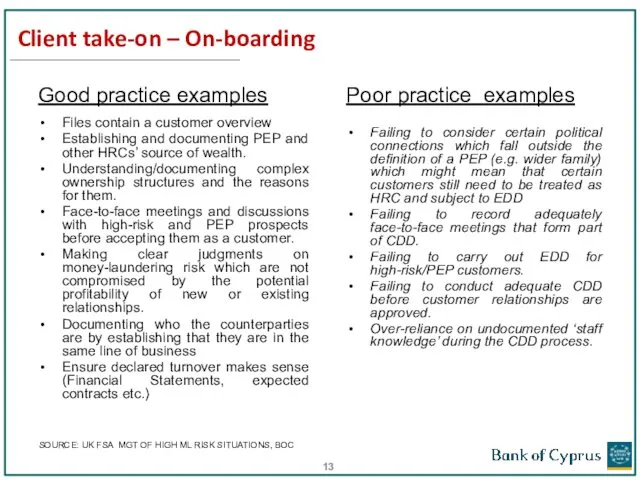

Client take-on – On-boarding

Good practice examples

Files contain a customer

Client take-on – On-boarding

Good practice examples

Files contain a customer

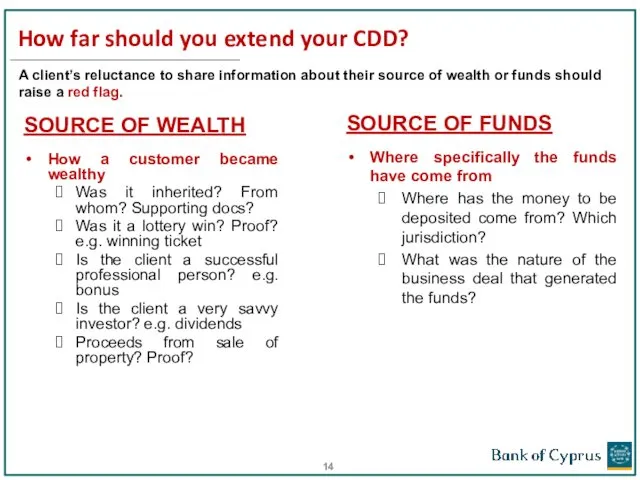

How far should you extend your CDD?

SOURCE OF WEALTH

How

How far should you extend your CDD?

SOURCE OF WEALTH

How

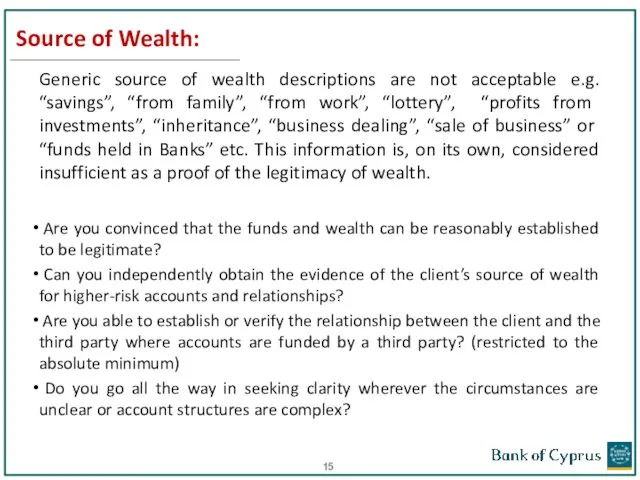

Source of Wealth:

Generic source of wealth descriptions are not acceptable e.g.

Source of Wealth:

Generic source of wealth descriptions are not acceptable e.g.

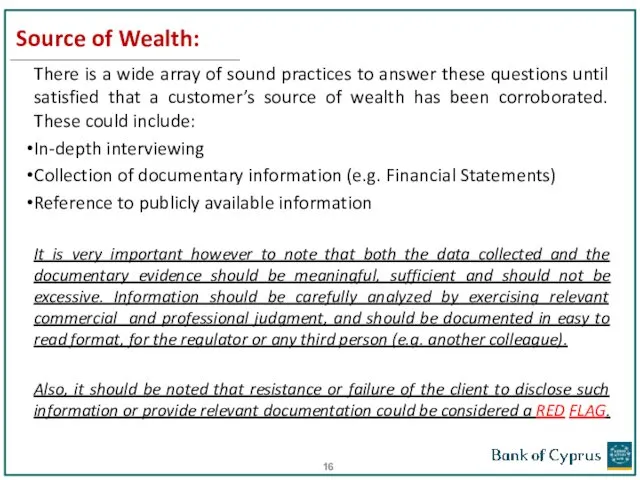

Source of Wealth:

There is a wide array of sound practices to

Source of Wealth:

There is a wide array of sound practices to

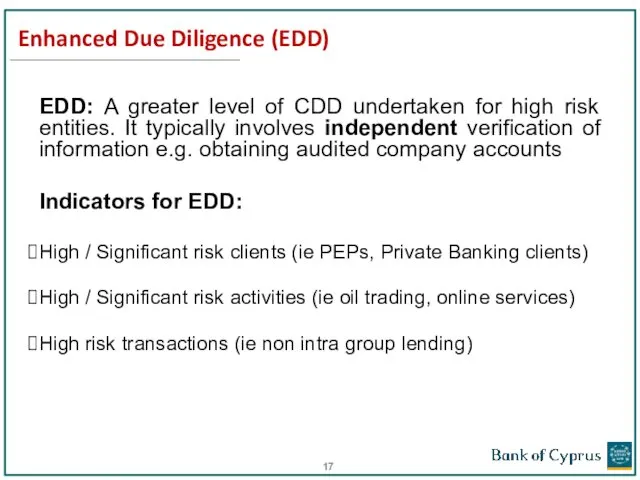

Enhanced Due Diligence (EDD)

EDD: A greater level of CDD undertaken

Enhanced Due Diligence (EDD)

EDD: A greater level of CDD undertaken

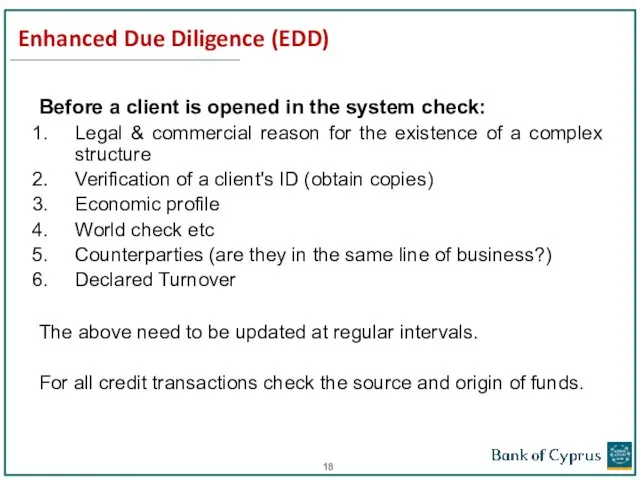

Enhanced Due Diligence (EDD)

Before a client is opened in the

Enhanced Due Diligence (EDD)

Before a client is opened in the

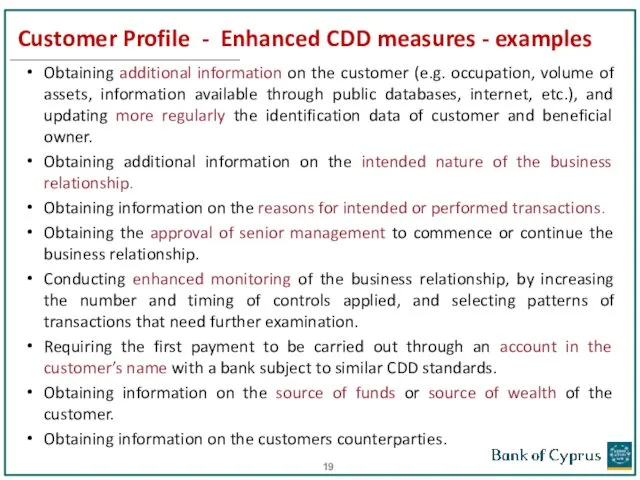

Customer Profile - Enhanced CDD measures - examples

Obtaining additional information

Customer Profile - Enhanced CDD measures - examples

Obtaining additional information

Politically Exposed Persons (PEPs)

FATF Definition

PEPs are individuals who are

Politically Exposed Persons (PEPs)

FATF Definition

PEPs are individuals who are

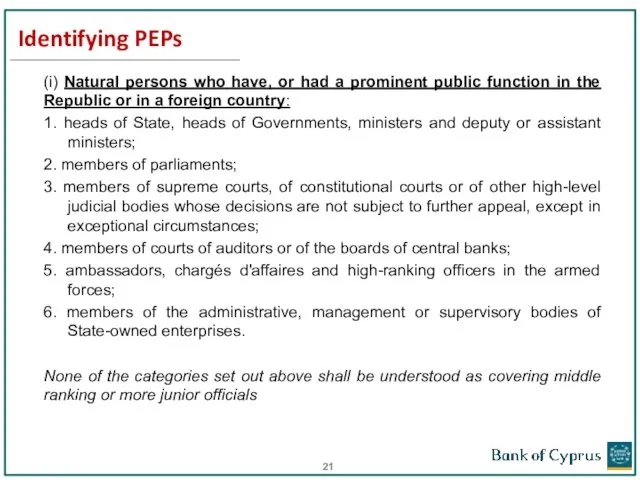

Identifying PEPs

(i) Natural persons who have, or had a prominent

Identifying PEPs

(i) Natural persons who have, or had a prominent

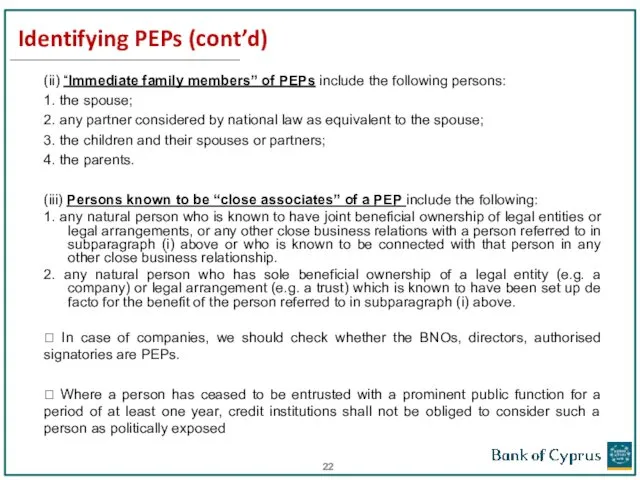

Identifying PEPs (cont’d)

(ii) “Immediate family members” of PEPs include the

Identifying PEPs (cont’d)

(ii) “Immediate family members” of PEPs include the

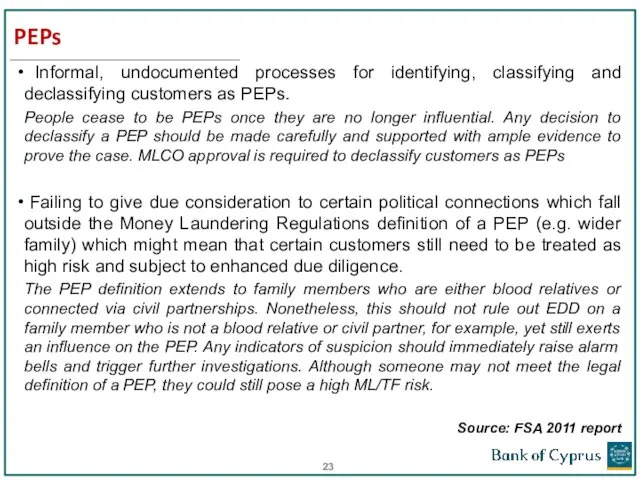

PEPs

Informal, undocumented processes for identifying, classifying and declassifying customers as

PEPs

Informal, undocumented processes for identifying, classifying and declassifying customers as

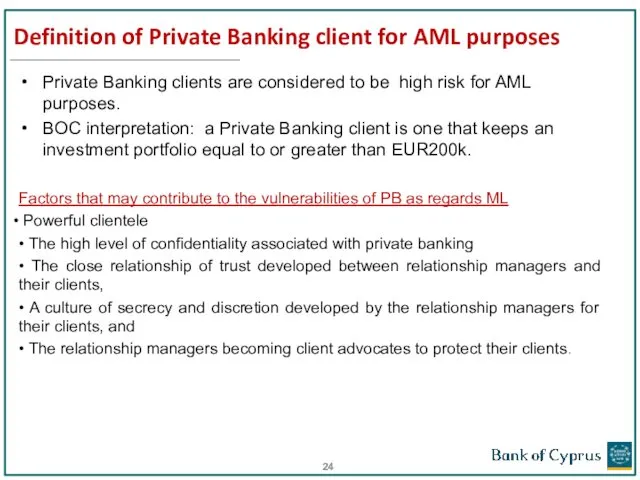

Definition of Private Banking client for AML purposes

Private Banking clients

Definition of Private Banking client for AML purposes

Private Banking clients

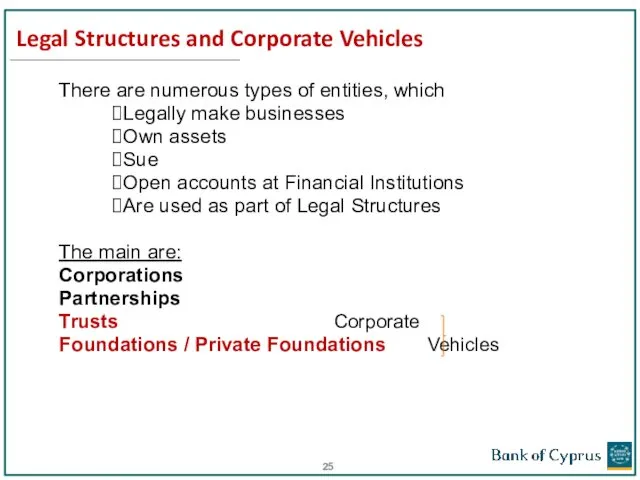

Legal Structures and Corporate Vehicles

There are numerous types of entities, which

Legal Structures and Corporate Vehicles

There are numerous types of entities, which

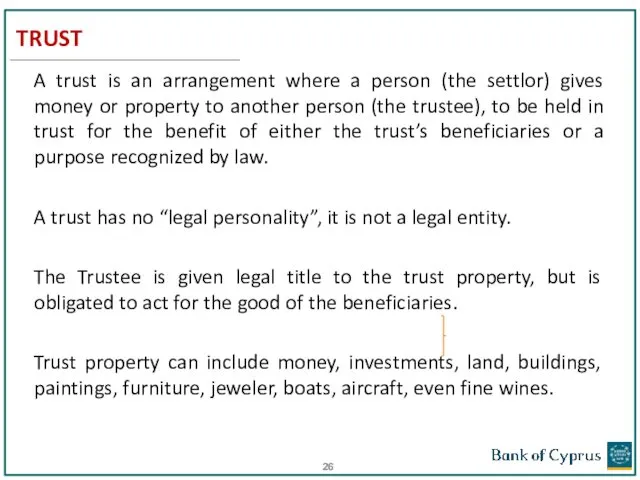

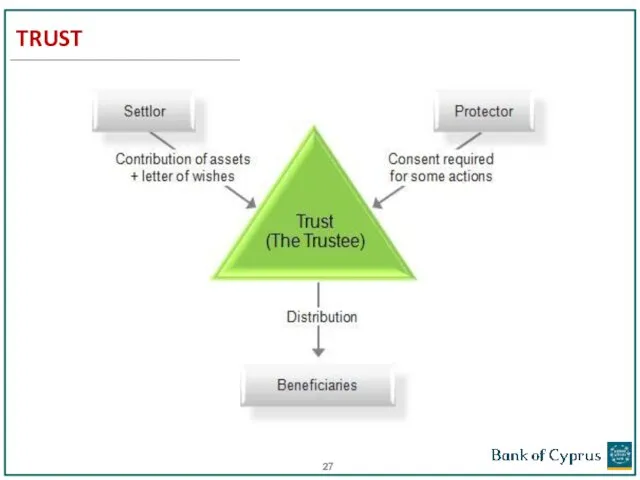

TRUST

A trust is an arrangement where a person (the settlor) gives

TRUST

A trust is an arrangement where a person (the settlor) gives

TRUST

TRUST

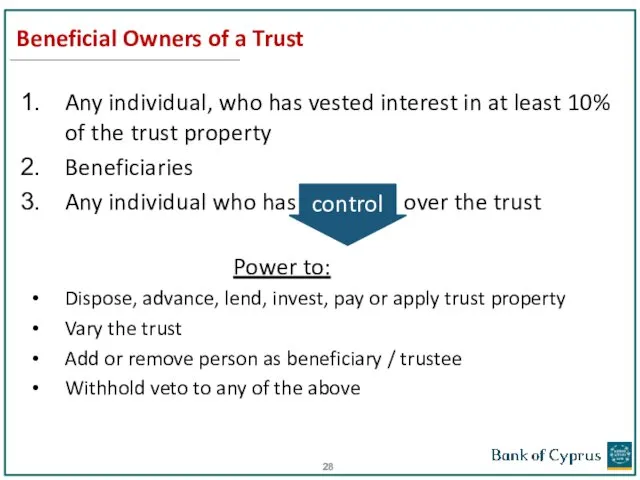

Beneficial Owners of a Trust

Any individual, who has vested interest in

Beneficial Owners of a Trust

Any individual, who has vested interest in

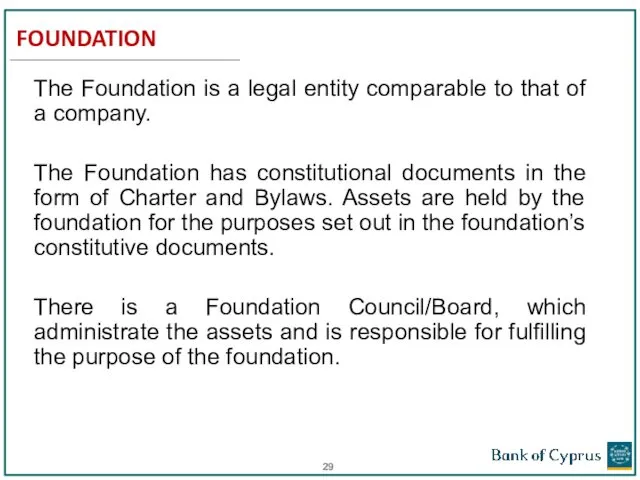

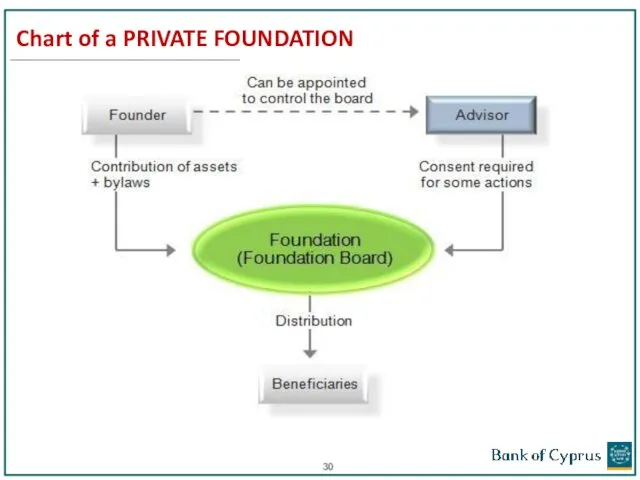

FOUNDATION

The Foundation is a legal entity comparable to that of a

FOUNDATION

The Foundation is a legal entity comparable to that of a

Chart of a PRIVATE FOUNDATION

Chart of a PRIVATE FOUNDATION

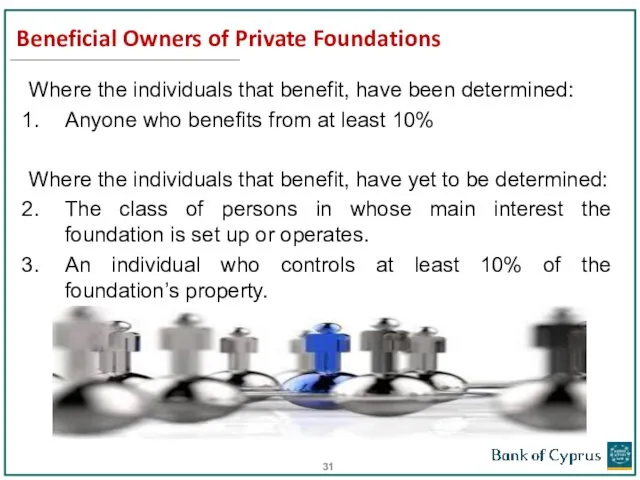

Beneficial Owners of Private Foundations

Where the individuals that benefit, have been

Beneficial Owners of Private Foundations

Where the individuals that benefit, have been

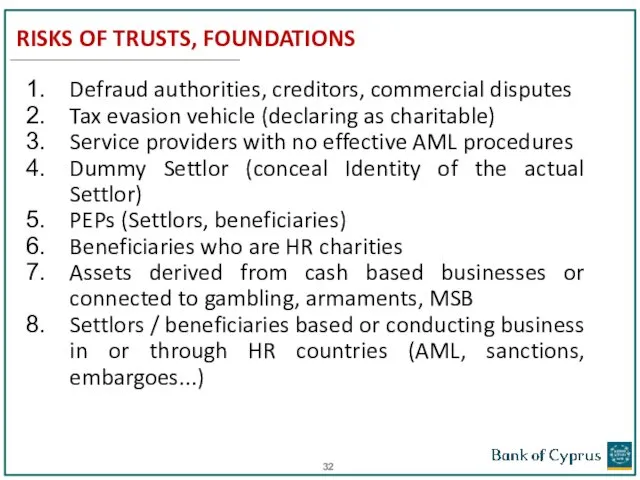

RISKS OF TRUSTS, FOUNDATIONS

Defraud authorities, creditors, commercial disputes

Tax evasion vehicle (declaring

RISKS OF TRUSTS, FOUNDATIONS

Defraud authorities, creditors, commercial disputes

Tax evasion vehicle (declaring

RED FLAGS:

Unexplained relationship between settlor, beneficiaries, controllers, property and 3rd

RED FLAGS:

Unexplained relationship between settlor, beneficiaries, controllers, property and 3rd

Sophisticated, Complex Legal Structures

* Refer to OE151 for the definition of

Sophisticated, Complex Legal Structures

* Refer to OE151 for the definition of

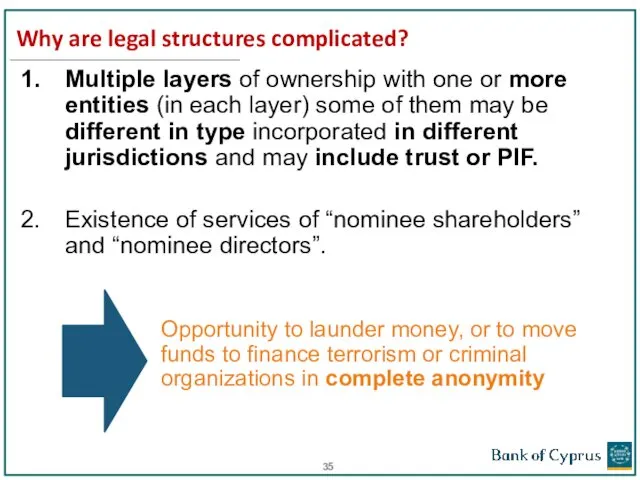

Why are legal structures complicated?

Multiple layers of ownership with one or

Why are legal structures complicated?

Multiple layers of ownership with one or

Why are legal structures complicated and Risky?

Why are legal structures complicated and Risky?

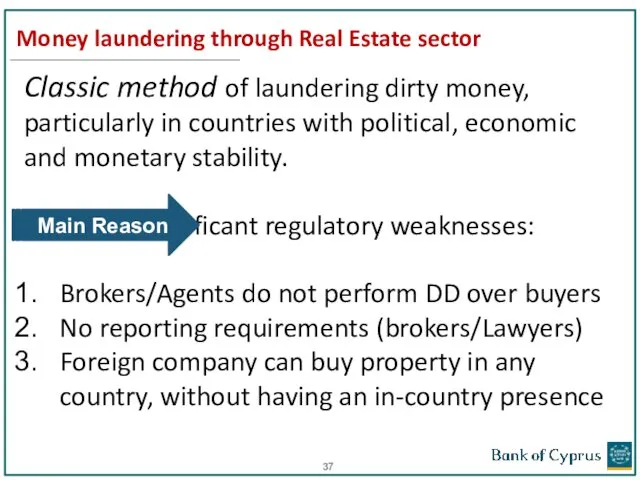

Money laundering through Real Estate sector

Classic method of laundering dirty money,

Money laundering through Real Estate sector

Classic method of laundering dirty money,

RED FLAGS:

Cash deposits

Renovation and reselling as high-end property

3rd party payment

Using a

RED FLAGS:

Cash deposits

Renovation and reselling as high-end property

3rd party payment

Using a

Trade-Based Money laundering

One of the most sophisticated methods of

Trade-Based Money laundering

One of the most sophisticated methods of

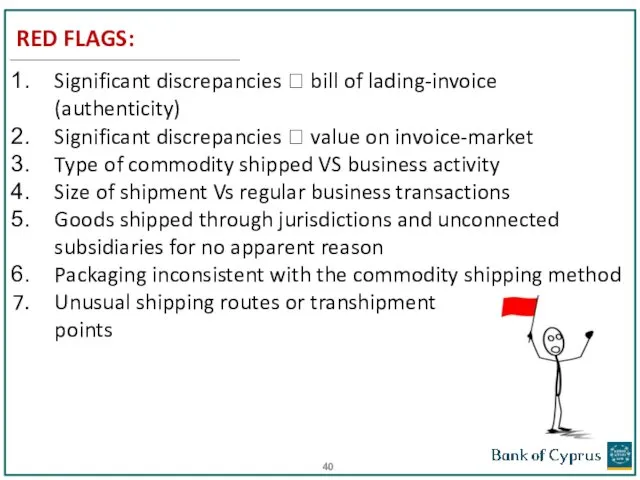

RED FLAGS:

Significant discrepancies ? bill of lading-invoice (authenticity)

Significant discrepancies ? value

RED FLAGS:

Significant discrepancies ? bill of lading-invoice (authenticity)

Significant discrepancies ? value

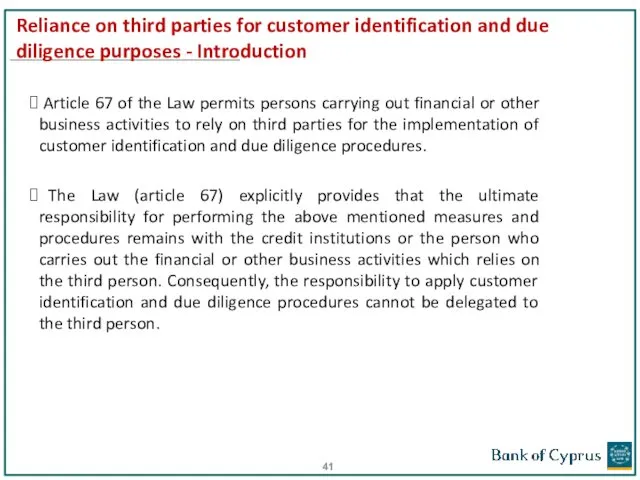

Reliance on third parties for customer identification and due diligence purposes

Reliance on third parties for customer identification and due diligence purposes

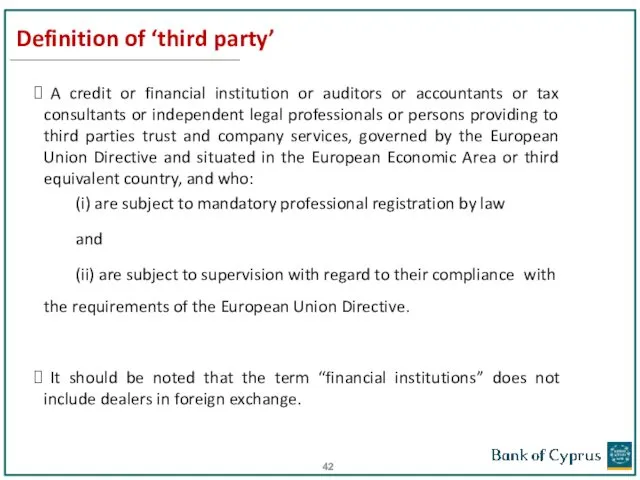

Definition of ‘third party’

A credit or financial institution or auditors

Definition of ‘third party’

A credit or financial institution or auditors

Business Associates

Independent Professionals, natural or legal persons, who recommend

Business Associates

Independent Professionals, natural or legal persons, who recommend

Definition of Terrorist Financing

By any means, directly or indirectly,

Unlawfully and willfully,

Definition of Terrorist Financing

By any means, directly or indirectly,

Unlawfully and willfully,

The Terrorist Financing Process

Funds used to finance terrorism are considered an

The Terrorist Financing Process

Funds used to finance terrorism are considered an

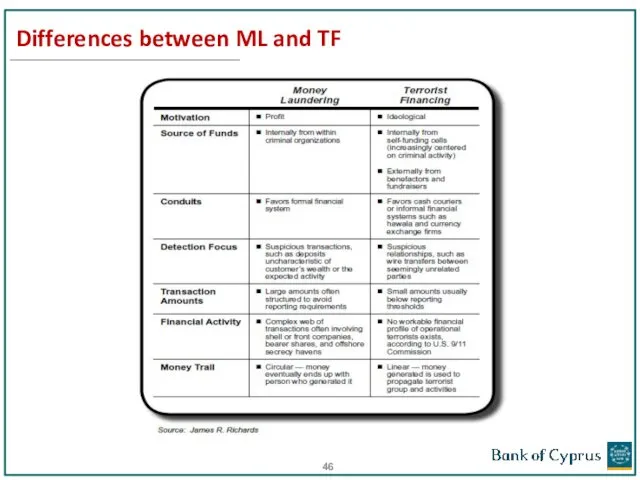

Differences between ML and TF

Differences between ML and TF

Terrorist Financing Red Flags

The stated occupation of the customer is

Terrorist Financing Red Flags

The stated occupation of the customer is

Terrorist Financing Red Flags

Regarding nonprofit or charitable organizations, financial transactions

Terrorist Financing Red Flags

Regarding nonprofit or charitable organizations, financial transactions

Direct operational cost of Terrorist Attacks (Estimates)

Direct operational cost of Terrorist Attacks (Estimates)

Real – Life Case: The 9/11 Terrorist Attacks

Funding for the 9/11

Real – Life Case: The 9/11 Terrorist Attacks

Funding for the 9/11

What are Sanctions?

Sanctions are

unilateral or multilateral

economic actions

taken against

What are Sanctions?

Sanctions are

unilateral or multilateral

economic actions

taken against

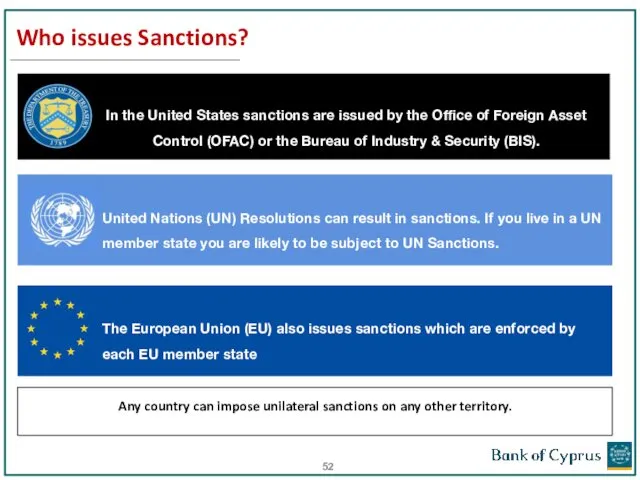

Who issues Sanctions?

United Nations (UN) Resolutions can result in sanctions. If

Who issues Sanctions?

United Nations (UN) Resolutions can result in sanctions. If

EU Sanctions

General

The European Commission proposes restrictive measures and adopts

EU Sanctions

General

The European Commission proposes restrictive measures and adopts

OFAC Sanctions

General

The US Treasury Department’s Office of Foreign Assets

OFAC Sanctions

General

The US Treasury Department’s Office of Foreign Assets

OFAC Sanctions (cont.)

OFAC Sanctions apply to:

Everyone in the US, including

OFAC Sanctions (cont.)

OFAC Sanctions apply to:

Everyone in the US, including

Sanctions Type & Scope

Sanctions can be:

Specific ? Relate to specific lists

Sanctions Type & Scope

Sanctions can be:

Specific ? Relate to specific lists

Sanctions Vs AML

Sanctions Vs AML

Sanctions Evasions

Forgery of documents

Nested accounts

Stripping wires

Restructuring of corporate entities

Re-routing of transactions

Withholding

Sanctions Evasions

Forgery of documents

Nested accounts

Stripping wires

Restructuring of corporate entities

Re-routing of transactions

Withholding

Sanctions & Embargoes

Regulators are very serious – fines can be huge:

Sanctions & Embargoes

Regulators are very serious – fines can be huge:

Effective Transaction Monitoring

Article 58(e) of the Law

What is required is

Effective Transaction Monitoring

Article 58(e) of the Law

What is required is

Effective Transaction Monitoring

In practice, where a client’s instruction or transaction

Effective Transaction Monitoring

In practice, where a client’s instruction or transaction

CUSTOMER REVIEW PROCESS

Financial regulators require banks and non-banking financial institutions to

CUSTOMER REVIEW PROCESS

Financial regulators require banks and non-banking financial institutions to

CUSTOMER REVIEW PROCESS

A review should be performed when an unusual and/or

CUSTOMER REVIEW PROCESS

A review should be performed when an unusual and/or

CUSTOMER REVIEW PROCESS

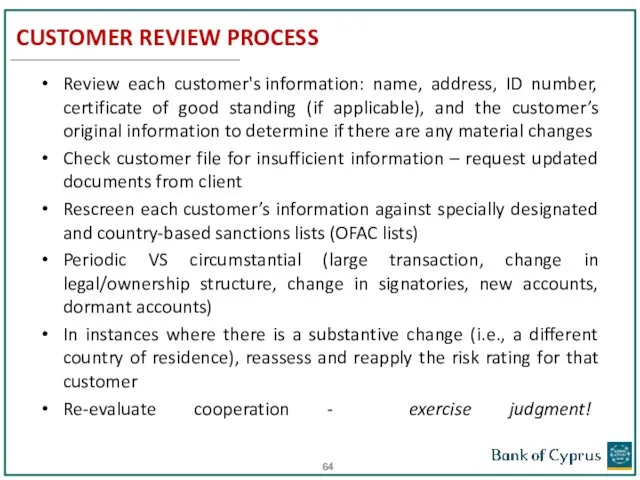

Review each customer's information: name, address, ID number, certificate of

CUSTOMER REVIEW PROCESS

Review each customer's information: name, address, ID number, certificate of

CUSTOMER REVIEW PROCESS

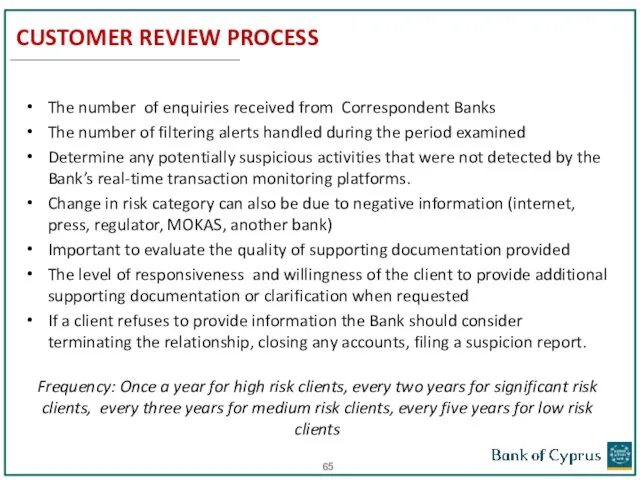

The number of enquiries received from Correspondent Banks

The number

CUSTOMER REVIEW PROCESS

The number of enquiries received from Correspondent Banks

The number

CUSTOMER REVIEW PROCESS

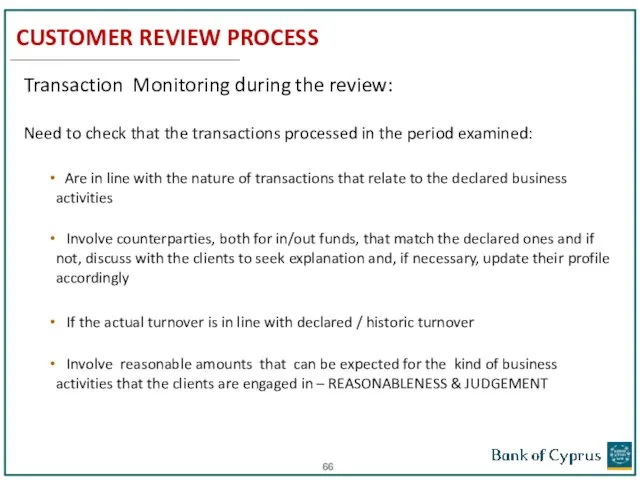

Transaction Monitoring during the review:

Need to check that the

CUSTOMER REVIEW PROCESS

Transaction Monitoring during the review:

Need to check that the

A SAR is born!

All should be aware of when and how

A SAR is born!

All should be aware of when and how

The “Suspicion Spectrum”

It is important to understand the above so that

The “Suspicion Spectrum”

It is important to understand the above so that

Похожие презентации

Халықаралық қаржылық есеп стандарттары

Халықаралық қаржылық есеп стандарттары Инвентаризация товарно-материальных ценностей

Инвентаризация товарно-материальных ценностей Проект поддержки местных инициатив Яжелбицкого сельского поселения

Проект поддержки местных инициатив Яжелбицкого сельского поселения Народный банк Казахстана

Народный банк Казахстана Біржовий та позабіржовий ринки цінних паперів

Біржовий та позабіржовий ринки цінних паперів Ипотечное кредитование

Ипотечное кредитование Державне інвестиційне кредитування. (Тема 5)

Державне інвестиційне кредитування. (Тема 5) Положения действующего законодательства о кредитных отношениях с участием юридических лиц и физических лиц

Положения действующего законодательства о кредитных отношениях с участием юридических лиц и физических лиц Классификация источников финансирования инвестиций. Формы и методы финансирования. Тема 3

Классификация источников финансирования инвестиций. Формы и методы финансирования. Тема 3 Факторинговые операции

Факторинговые операции Управленческий учет на предприятии

Управленческий учет на предприятии Проектное финансирование

Проектное финансирование Нормативное регулирование и организация бухгалтерского учета

Нормативное регулирование и организация бухгалтерского учета Оптимизация структуры капитала малого предприятия

Оптимизация структуры капитала малого предприятия Основы управления оборотными активами организации

Основы управления оборотными активами организации Анализ страховой фирмы Адонис

Анализ страховой фирмы Адонис Вопросник по внутреннему контролю цикла затрат

Вопросник по внутреннему контролю цикла затрат HV - podle našich účetních systémů

HV - podle našich účetních systémů Кәсіпкерлік қызметтің түрлері бойынша Өндірістік Коммерциялық Қаржылық

Кәсіпкерлік қызметтің түрлері бойынша Өндірістік Коммерциялық Қаржылық Финансы хозяйствующих субъектов

Финансы хозяйствующих субъектов Аналіз релевантностi інформації для прийняття управлінських рішень

Аналіз релевантностi інформації для прийняття управлінських рішень Рабочий отчет департамента аналитики компании IPO)

Рабочий отчет департамента аналитики компании IPO) Аудит

Аудит План счетов

План счетов Организация и стимулирование труда персонала в системе менеджмента предприятия ЗАО Сервисный центр ремонта медицинской техники

Организация и стимулирование труда персонала в системе менеджмента предприятия ЗАО Сервисный центр ремонта медицинской техники Банковская система

Банковская система

МФСО. Отчет о движении денежных средств

МФСО. Отчет о движении денежных средств