- Accounting Principles

Содержание

- 2. 1 Learning Objectives After studying this chapter, you should be able to: [1] Explain what accounting

- 3. Preview of Chapter 1 Accounting Principles Eleventh Edition Weygandt Kimmel Kieso

- 4. LO 1 Explain what accounting is. Purpose of accounting is to: identify, record, and communicate the

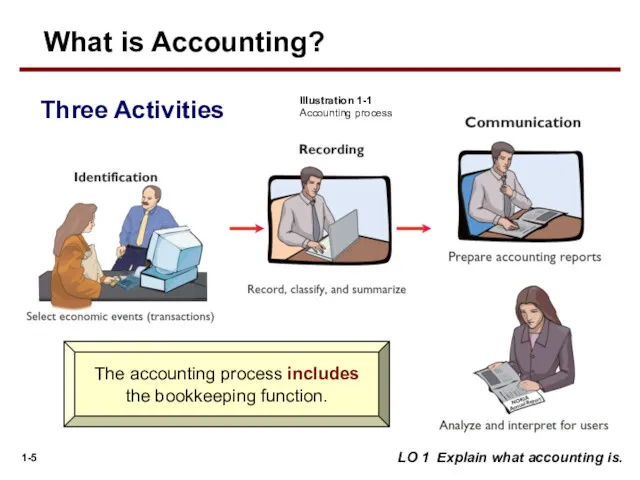

- 5. Three Activities LO 1 Explain what accounting is. Illustration 1-1 Accounting process The accounting process includes

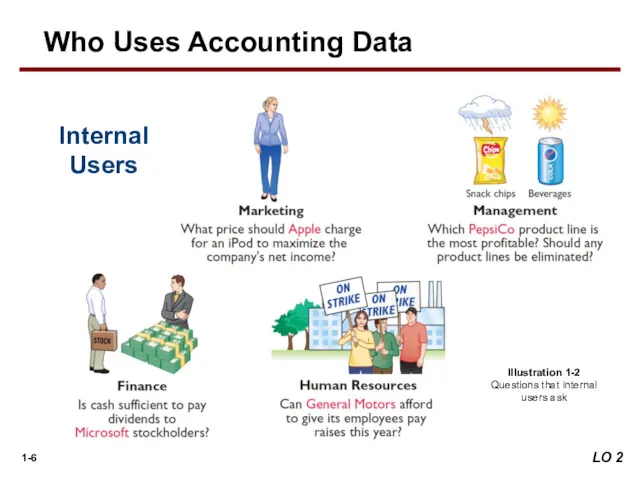

- 6. LO 2 Internal Users Illustration 1-2 Questions that internal users ask Who Uses Accounting Data

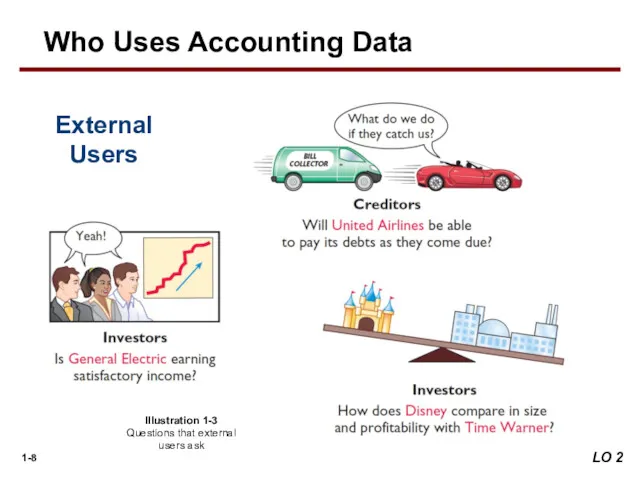

- 8. LO 2 External Users Illustration 1-3 Questions that external users ask Who Uses Accounting Data

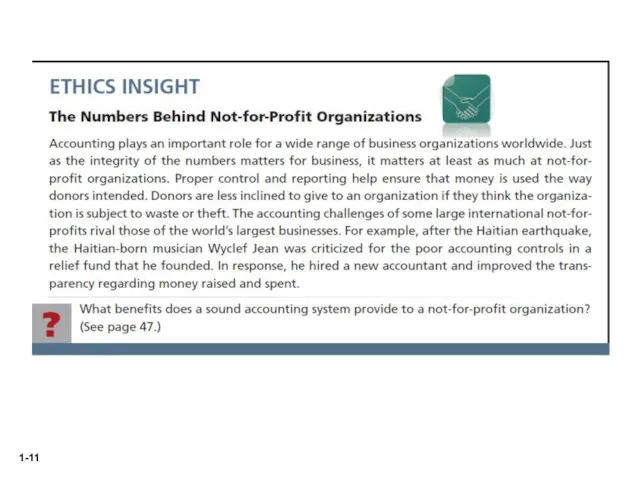

- 9. Ethics In Financial Reporting United States regulators and lawmakers were very concerned that the economy would

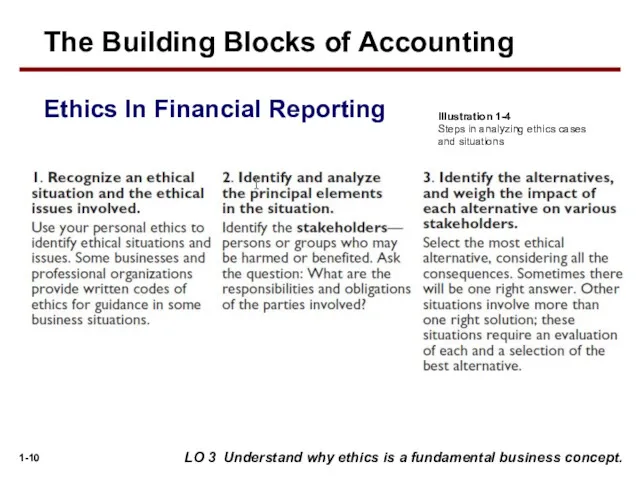

- 10. Illustration 1-4 Steps in analyzing ethics cases and situations LO 3 Understand why ethics is a

- 12. Ethics are the standards of conduct by which one's actions are judged as: right or wrong.

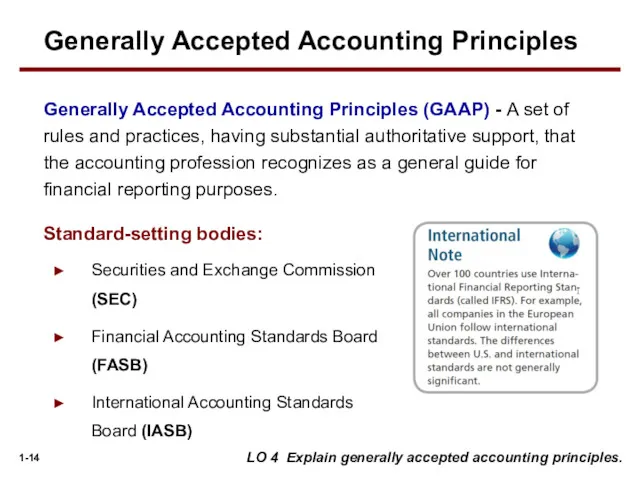

- 13. Various users need financial information The accounting profession has attempted to develop a set of standards

- 14. Generally Accepted Accounting Principles (GAAP) - A set of rules and practices, having substantial authoritative support,

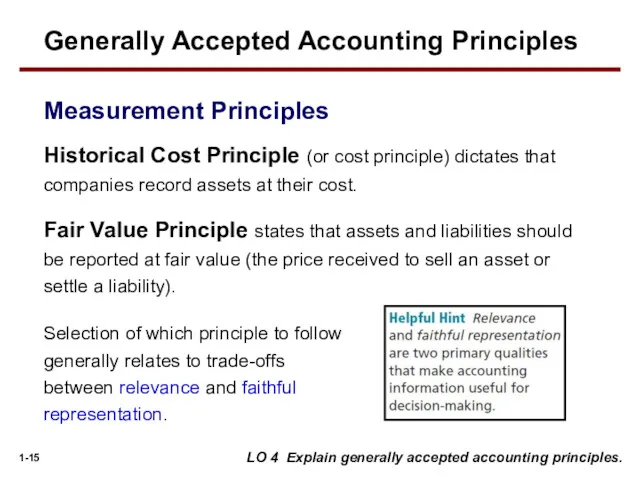

- 15. Historical Cost Principle (or cost principle) dictates that companies record assets at their cost. Fair Value

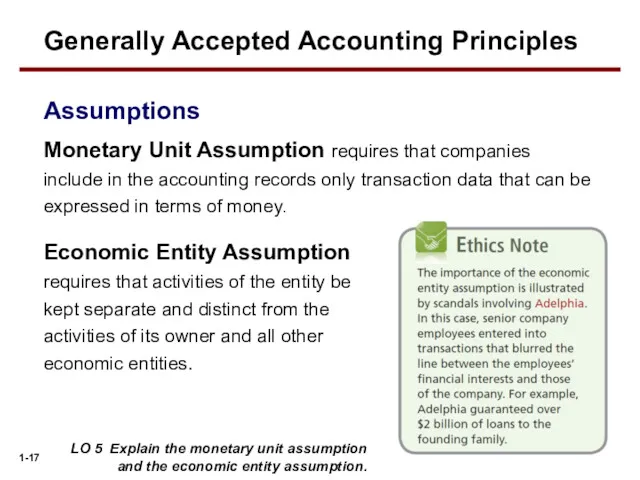

- 17. Monetary Unit Assumption requires that companies include in the accounting records only transaction data that can

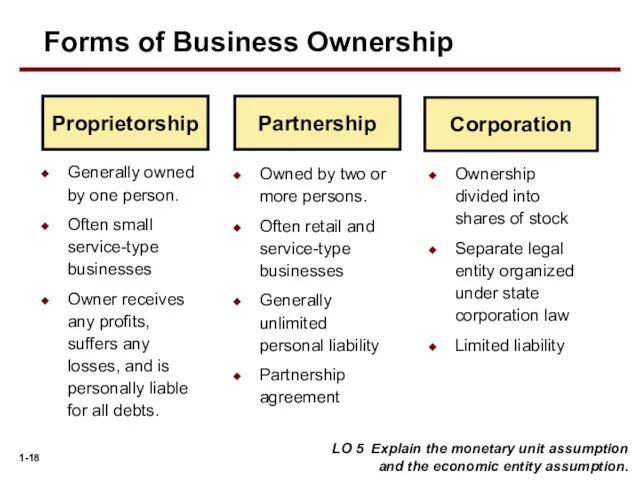

- 18. Proprietorship Partnership Corporation Owned by two or more persons. Often retail and service-type businesses Generally unlimited

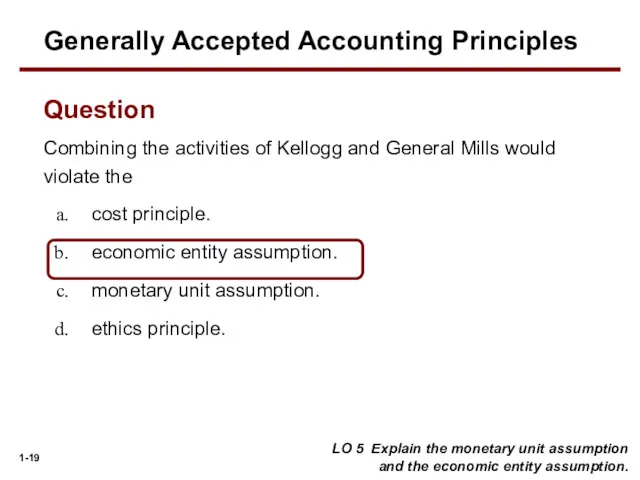

- 19. Question Combining the activities of Kellogg and General Mills would violate the cost principle. economic entity

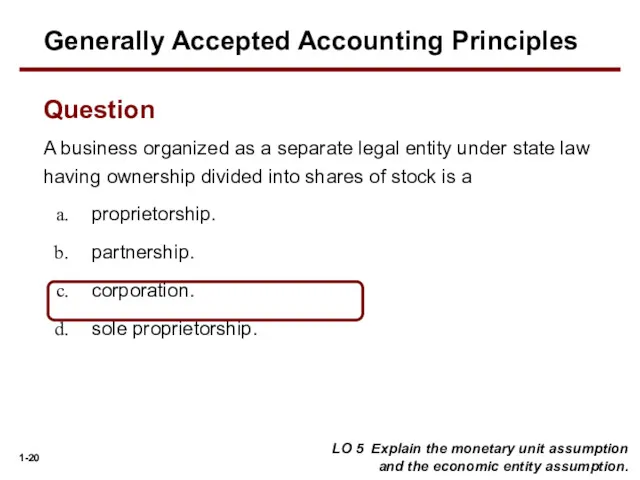

- 20. A business organized as a separate legal entity under state law having ownership divided into shares

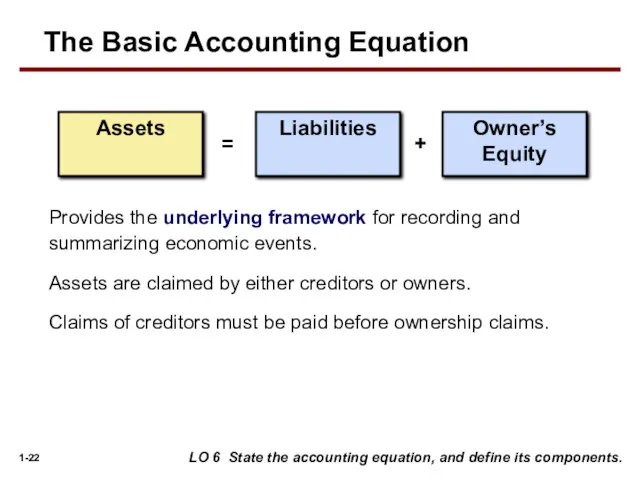

- 22. Provides the underlying framework for recording and summarizing economic events. Assets are claimed by either creditors

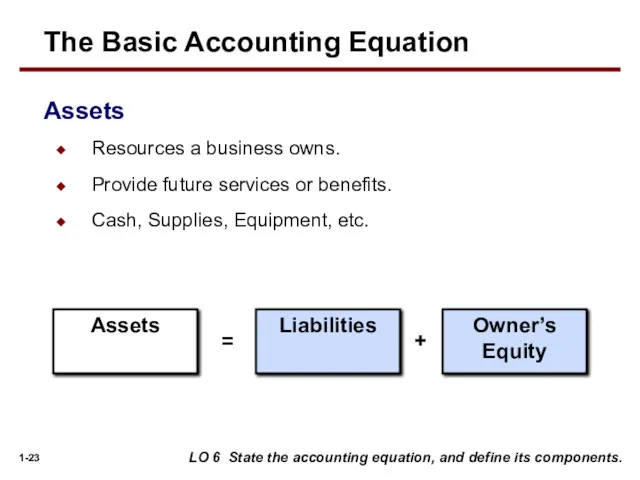

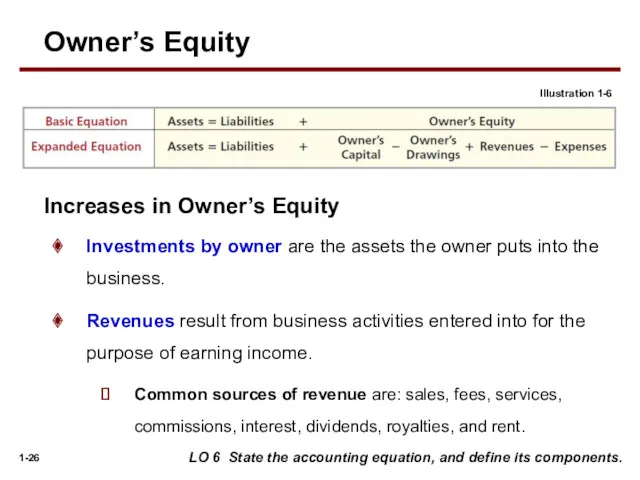

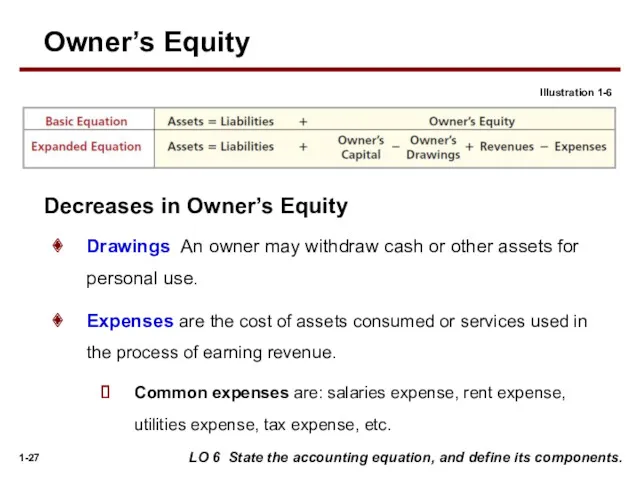

- 23. Assets Liabilities Owner’s Equity = + Resources a business owns. Provide future services or benefits. Cash,

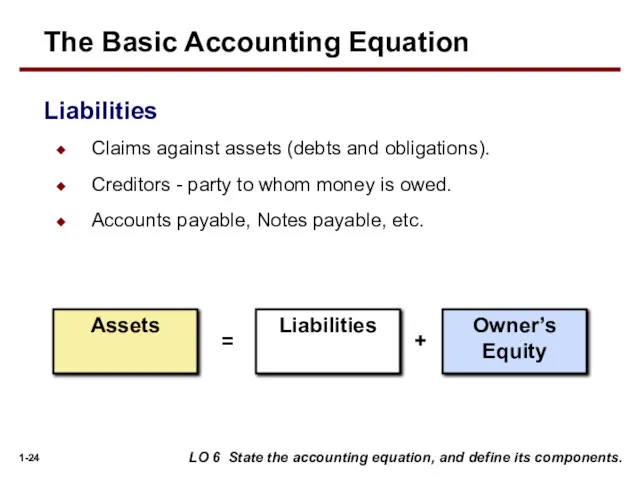

- 24. Claims against assets (debts and obligations). Creditors - party to whom money is owed. Accounts payable,

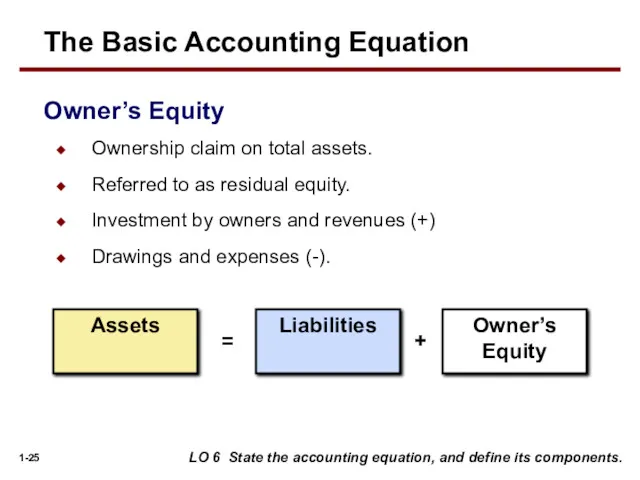

- 25. Ownership claim on total assets. Referred to as residual equity. Investment by owners and revenues (+)

- 26. Investments by owner are the assets the owner puts into the business. Revenues result from business

- 27. Drawings An owner may withdraw cash or other assets for personal use. Expenses are the cost

- 28. Transactions are a business’s economic events recorded by accountants. May be external or internal. Not all

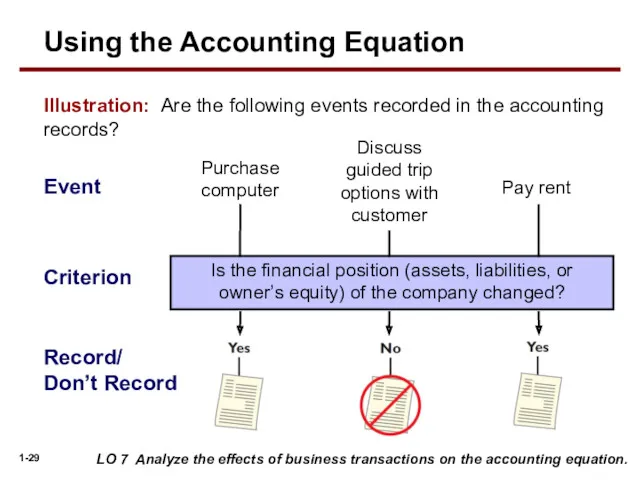

- 29. Illustration: Are the following events recorded in the accounting records? Event Purchase computer Criterion Is the

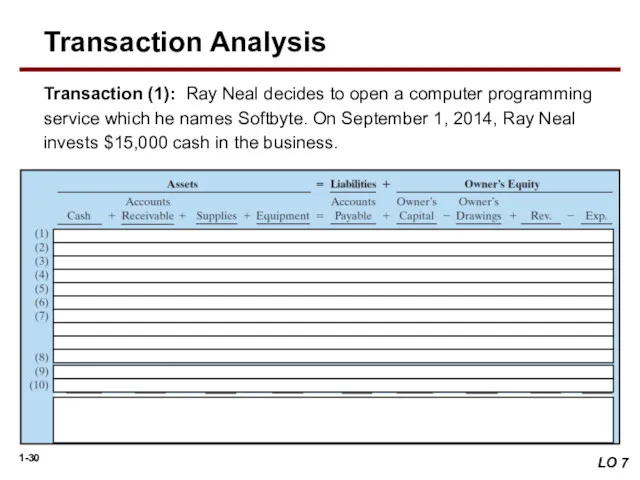

- 30. Transaction (1): Ray Neal decides to open a computer programming service which he names Softbyte. On

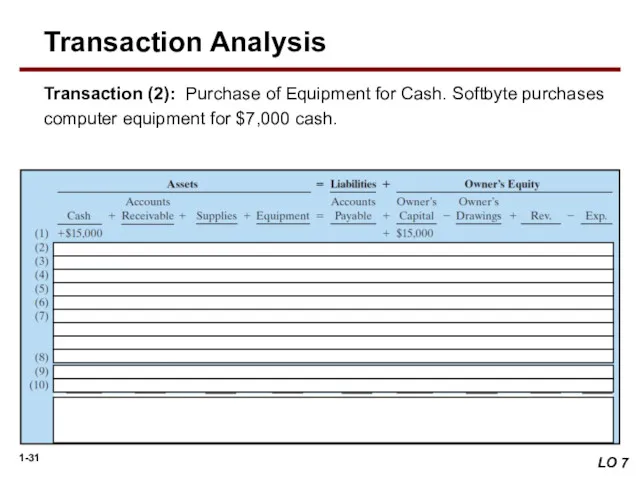

- 31. Transaction (2): Purchase of Equipment for Cash. Softbyte purchases computer equipment for $7,000 cash. LO 7

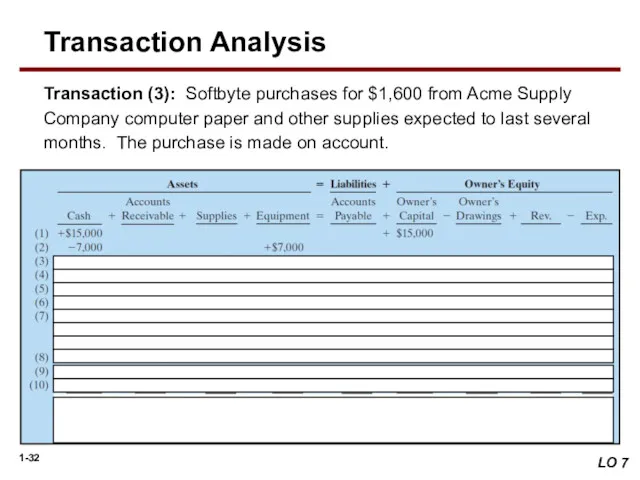

- 32. Transaction (3): Softbyte purchases for $1,600 from Acme Supply Company computer paper and other supplies expected

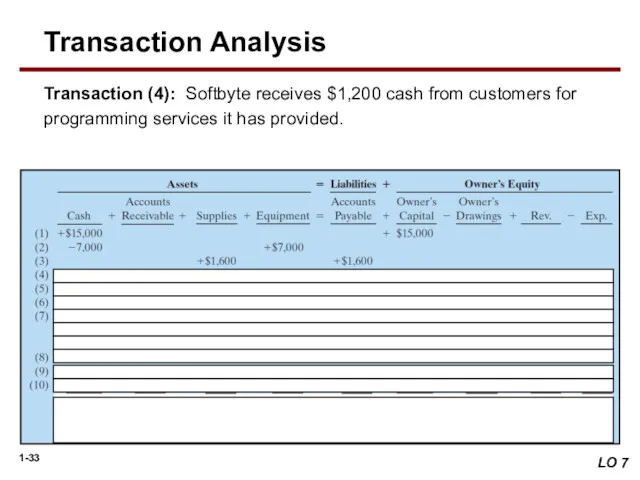

- 33. Transaction (4): Softbyte receives $1,200 cash from customers for programming services it has provided. LO 7

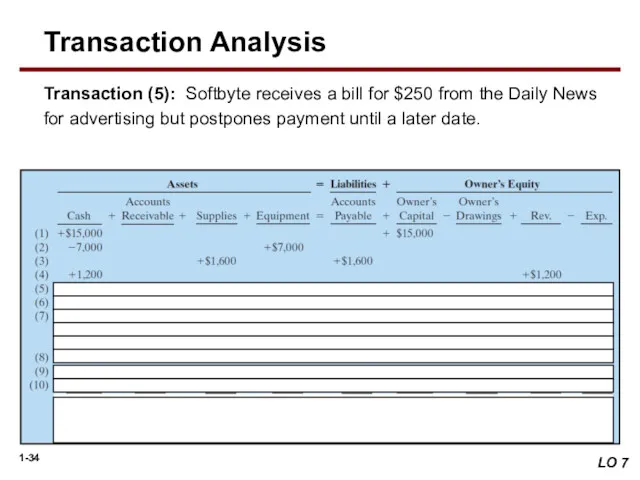

- 34. Transaction (5): Softbyte receives a bill for $250 from the Daily News for advertising but postpones

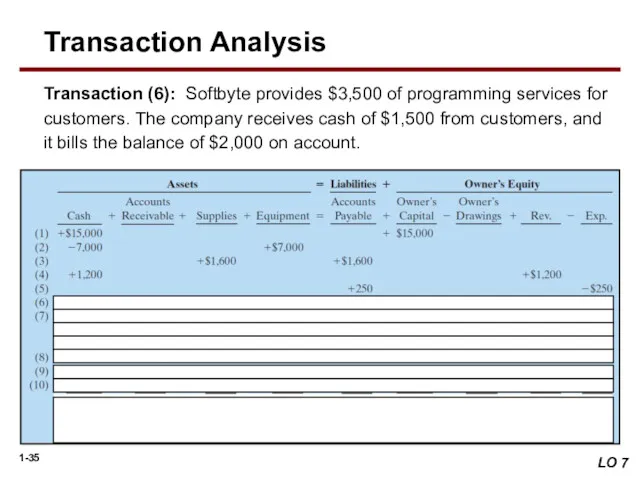

- 35. Transaction (6): Softbyte provides $3,500 of programming services for customers. The company receives cash of $1,500

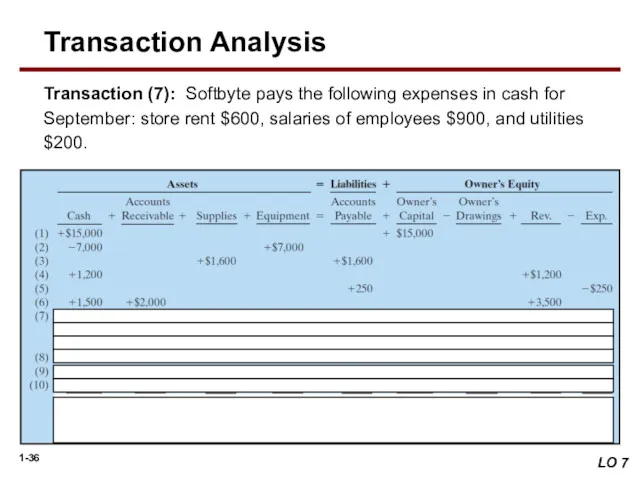

- 36. Transaction (7): Softbyte pays the following expenses in cash for September: store rent $600, salaries of

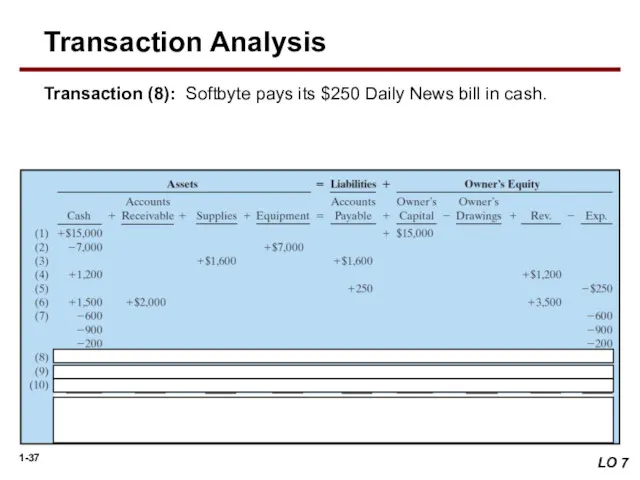

- 37. Transaction (8): Softbyte pays its $250 Daily News bill in cash. LO 7 Transaction Analysis

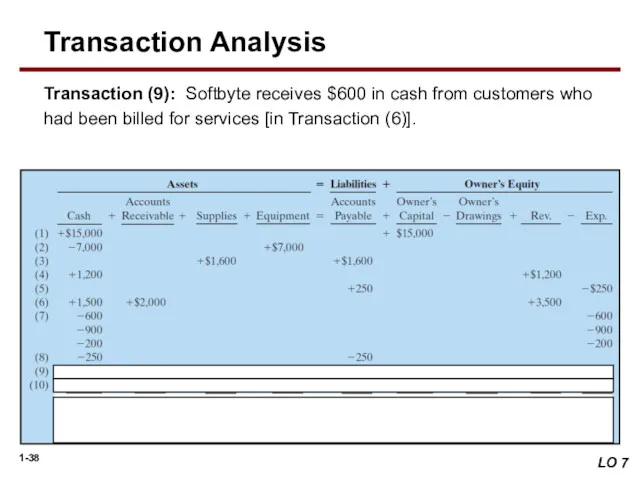

- 38. Transaction (9): Softbyte receives $600 in cash from customers who had been billed for services [in

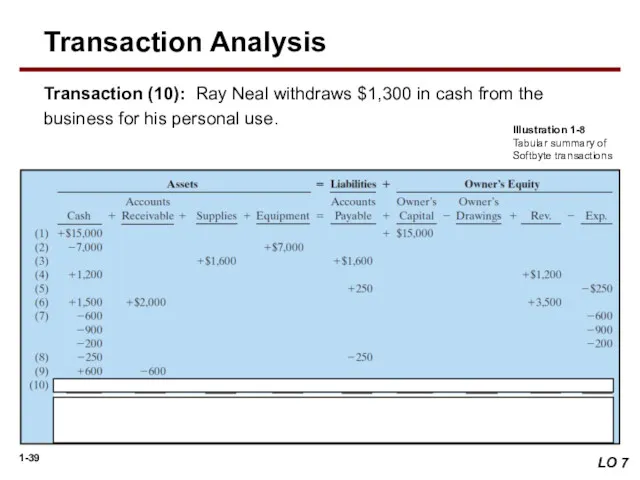

- 39. Transaction (10): Ray Neal withdraws $1,300 in cash from the business for his personal use. LO

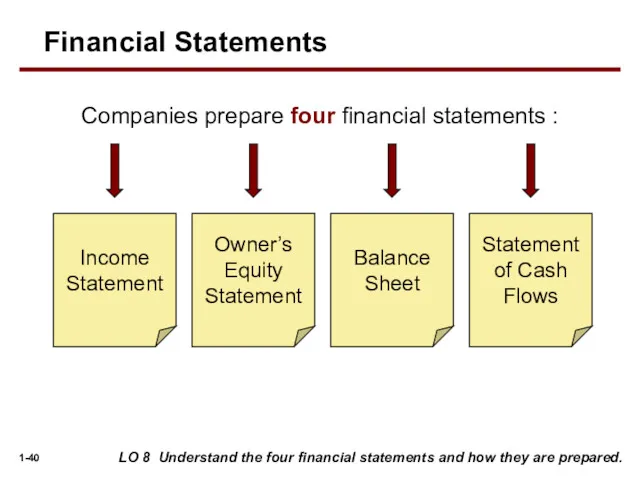

- 40. Companies prepare four financial statements : Balance Sheet Income Statement Statement of Cash Flows Owner’s Equity

- 41. Net income will result during a time period when: assets exceed liabilities. assets exceed revenues. expenses

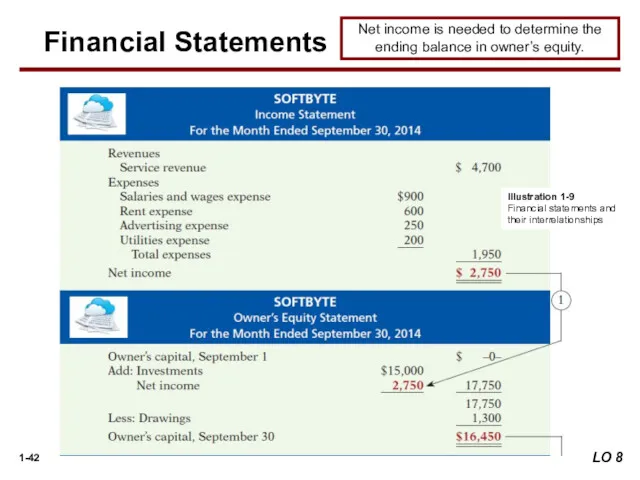

- 42. Net income is needed to determine the ending balance in owner’s equity. Illustration 1-9 Financial statements

- 43. The ending balance in owner’s equity is needed in preparing the balance sheet Financial Statements Illustration

- 44. The balance sheet and income statement are needed to prepare statement of cash flows. Financial Statements

- 45. LO 8 Understand the four financial statements and how they are prepared. Reports the revenues and

- 46. LO 8 Understand the four financial statements and how they are prepared. Reports the changes in

- 47. LO 8 Understand the four financial statements and how they are prepared. Reports the assets, liabilities,

- 48. LO 8 Understand the four financial statements and how they are prepared. Information for a specific

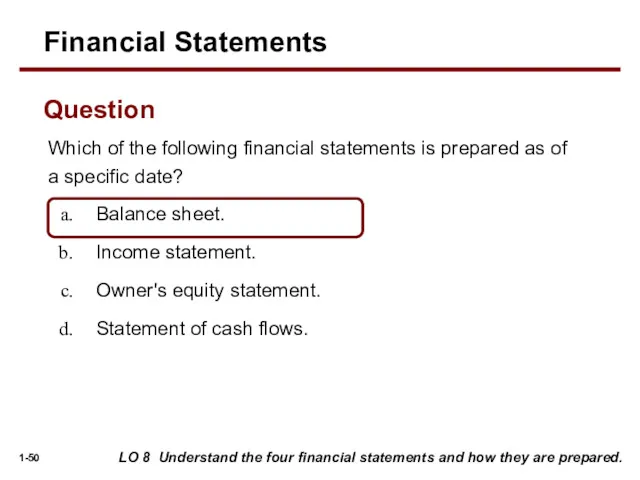

- 50. Which of the following financial statements is prepared as of a specific date? Balance sheet. Income

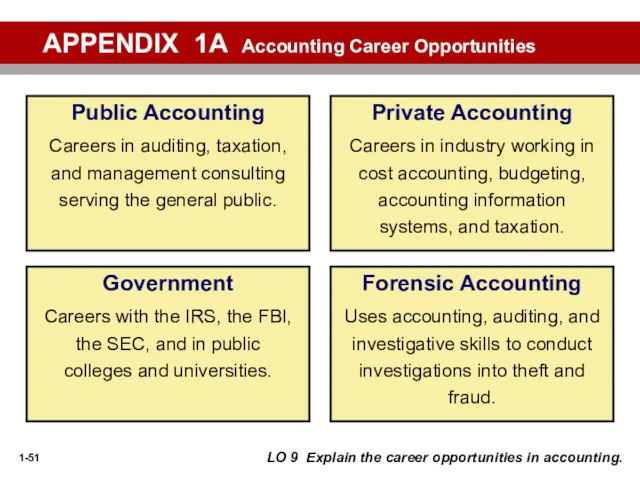

- 51. APPENDIX 1A Accounting Career Opportunities Forensic Accounting Uses accounting, auditing, and investigative skills to conduct investigations

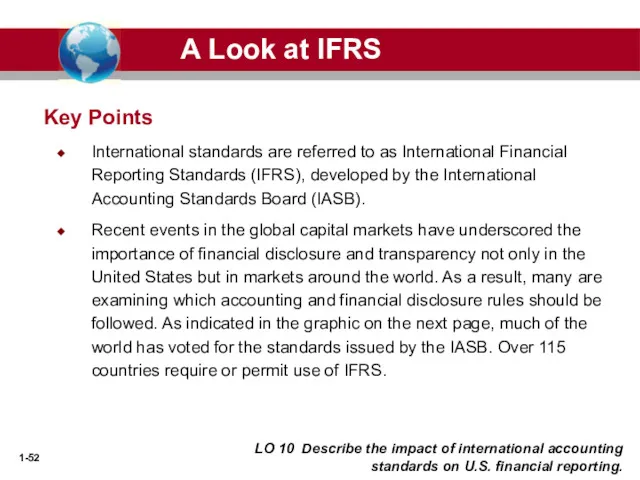

- 52. LO 10 Describe the impact of international accounting standards on U.S. financial reporting. Key Points International

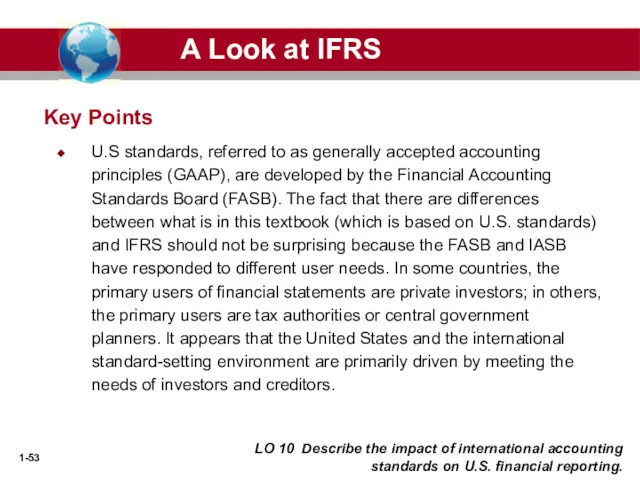

- 53. LO 10 Describe the impact of international accounting standards on U.S. financial reporting. Key Points U.S

- 54. LO 10 Describe the impact of international accounting standards on U.S. financial reporting. Key Points The

- 55. LO 10 Describe the impact of international accounting standards on U.S. financial reporting. Key Points IFRS

- 56. LO 10 Describe the impact of international accounting standards on U.S. financial reporting. Key Points The

- 57. Both the IASB and the FASB are hard at work developing standards that will lead to

- 58. Which of the following is not a reason why a single set of high-quality international accounting

- 59. The Sarbanes-Oxley Act determines: international tax regulations. internal control standards as enforced by the IASB. internal

- 60. IFRS is considered to be more: principles-based and less rules-based than GAAP. rules-based and less principles-based

- 62. Скачать презентацию

1

Learning Objectives

After studying this chapter, you should be able to:

[1] Explain

1

Learning Objectives

After studying this chapter, you should be able to:

[1] Explain

Preview of Chapter 1

Accounting Principles

Eleventh Edition

Weygandt Kimmel Kieso

Preview of Chapter 1

Accounting Principles

Eleventh Edition

Weygandt Kimmel Kieso

LO 1 Explain what accounting is.

Purpose of accounting is to:

identify,

record,

LO 1 Explain what accounting is.

Purpose of accounting is to:

identify,

record,

Three Activities

LO 1 Explain what accounting is.

Illustration 1-1

Accounting process

The accounting process

Three Activities

LO 1 Explain what accounting is.

Illustration 1-1

Accounting process

The accounting process

LO 2

Internal Users

Illustration 1-2

Questions that internal users ask

Who Uses

LO 2

Internal Users

Illustration 1-2

Questions that internal users ask

Who Uses

LO 2

External Users

Illustration 1-3

Questions that external users ask

Who Uses Accounting

LO 2

External Users

Illustration 1-3

Questions that external users ask

Who Uses Accounting

Ethics In Financial Reporting

United States regulators and lawmakers were very concerned

Ethics In Financial Reporting

United States regulators and lawmakers were very concerned

Illustration 1-4

Steps in analyzing ethics cases and situations

LO 3 Understand why

Illustration 1-4

Steps in analyzing ethics cases and situations

LO 3 Understand why

Ethics are the standards of conduct by which one's actions are

Ethics are the standards of conduct by which one's actions are

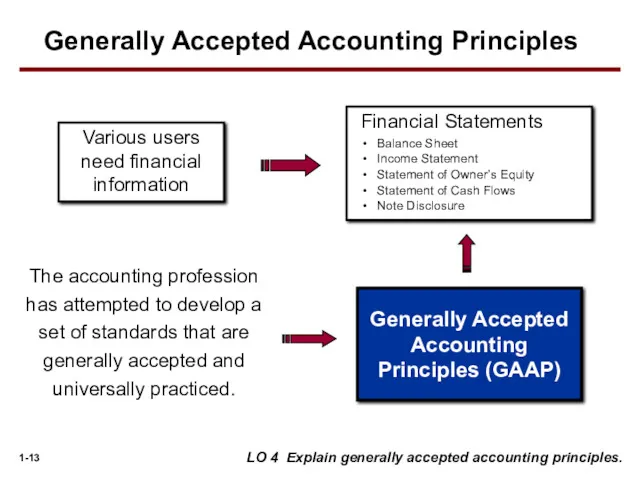

Various users need financial information

The accounting profession has attempted to develop

Various users need financial information

The accounting profession has attempted to develop

Generally Accepted Accounting Principles (GAAP) - A set of rules and

Generally Accepted Accounting Principles (GAAP) - A set of rules and

Historical Cost Principle (or cost principle) dictates that companies record assets

Historical Cost Principle (or cost principle) dictates that companies record assets

Monetary Unit Assumption requires that companies include in the accounting records

Monetary Unit Assumption requires that companies include in the accounting records

Proprietorship

Partnership

Corporation

Owned by two or more persons.

Often retail and service-type businesses

Generally unlimited

Proprietorship

Partnership

Corporation

Owned by two or more persons.

Often retail and service-type businesses

Generally unlimited

Question

Combining the activities of Kellogg and General Mills would violate the

Question

Combining the activities of Kellogg and General Mills would violate the

A business organized as a separate legal entity under state law

A business organized as a separate legal entity under state law

Provides the underlying framework for recording and summarizing economic events.

Assets are

Provides the underlying framework for recording and summarizing economic events.

Assets are

Assets

Liabilities

Owner’s Equity

=

+

Resources a business owns.

Provide future services or benefits.

Cash, Supplies, Equipment,

Assets

Liabilities

Owner’s Equity

=

+

Resources a business owns.

Provide future services or benefits.

Cash, Supplies, Equipment,

Claims against assets (debts and obligations).

Creditors - party to whom money

Claims against assets (debts and obligations).

Creditors - party to whom money

Ownership claim on total assets.

Referred to as residual equity.

Investment by owners

Ownership claim on total assets.

Referred to as residual equity.

Investment by owners

Investments by owner are the assets the owner puts into the

Investments by owner are the assets the owner puts into the

Drawings An owner may withdraw cash or other assets for personal

Drawings An owner may withdraw cash or other assets for personal

Transactions are a business’s economic events recorded by accountants.

May be external

Transactions are a business’s economic events recorded by accountants.

May be external

Illustration: Are the following events recorded in the accounting records?

Event

Purchase computer

Criterion

Is

Illustration: Are the following events recorded in the accounting records?

Event

Purchase computer

Criterion

Is

Transaction (1): Ray Neal decides to open a computer programming service

Transaction (1): Ray Neal decides to open a computer programming service

Transaction (2): Purchase of Equipment for Cash. Softbyte purchases computer equipment

Transaction (2): Purchase of Equipment for Cash. Softbyte purchases computer equipment

Transaction (3): Softbyte purchases for $1,600 from Acme Supply Company computer

Transaction (3): Softbyte purchases for $1,600 from Acme Supply Company computer

Transaction (4): Softbyte receives $1,200 cash from customers for programming services

Transaction (4): Softbyte receives $1,200 cash from customers for programming services

Transaction (5): Softbyte receives a bill for $250 from the Daily

Transaction (5): Softbyte receives a bill for $250 from the Daily

Transaction (6): Softbyte provides $3,500 of programming services for customers. The

Transaction (6): Softbyte provides $3,500 of programming services for customers. The

Transaction (7): Softbyte pays the following expenses in cash for September:

Transaction (7): Softbyte pays the following expenses in cash for September:

Transaction (8): Softbyte pays its $250 Daily News bill in cash.

LO

Transaction (8): Softbyte pays its $250 Daily News bill in cash.

LO

Transaction (9): Softbyte receives $600 in cash from customers who had

Transaction (9): Softbyte receives $600 in cash from customers who had

Transaction (10): Ray Neal withdraws $1,300 in cash from the business

Transaction (10): Ray Neal withdraws $1,300 in cash from the business

Companies prepare four financial statements :

Balance Sheet

Income Statement

Statement of Cash Flows

Owner’s

Companies prepare four financial statements :

Balance Sheet

Income Statement

Statement of Cash Flows

Owner’s

Net income will result during a time period when:

assets exceed liabilities.

assets

Net income will result during a time period when:

assets exceed liabilities.

assets

Net income is needed to determine the ending balance in owner’s

Net income is needed to determine the ending balance in owner’s

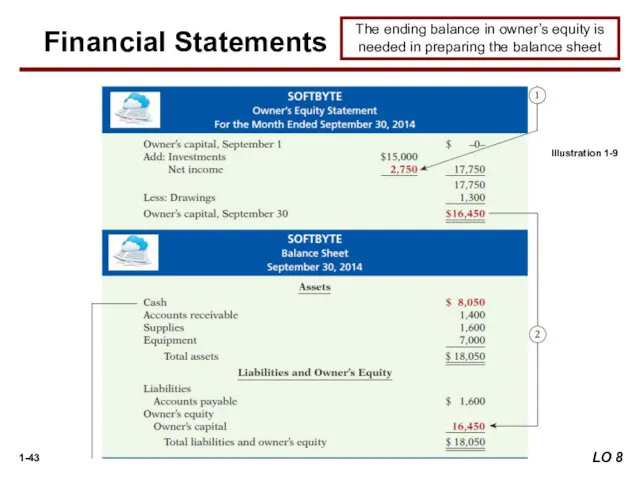

The ending balance in owner’s equity is needed in preparing the

The ending balance in owner’s equity is needed in preparing the

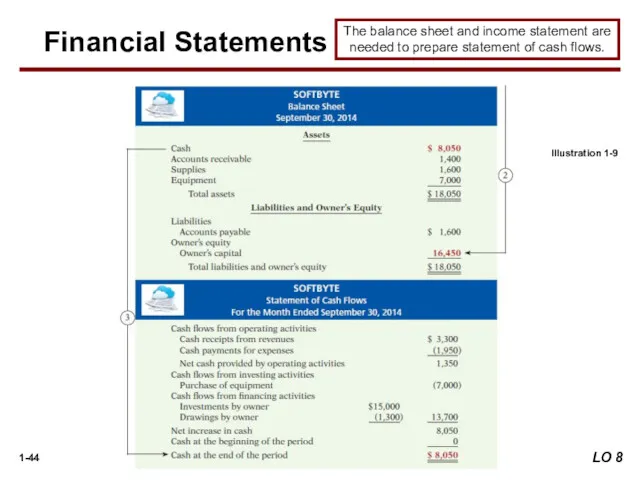

The balance sheet and income statement are needed to prepare statement

The balance sheet and income statement are needed to prepare statement

LO 8 Understand the four financial statements and how they are

LO 8 Understand the four financial statements and how they are

LO 8 Understand the four financial statements and how they are

LO 8 Understand the four financial statements and how they are

LO 8 Understand the four financial statements and how they are

LO 8 Understand the four financial statements and how they are

LO 8 Understand the four financial statements and how they are

LO 8 Understand the four financial statements and how they are

Which of the following financial statements is prepared as of a

Which of the following financial statements is prepared as of a

APPENDIX 1A Accounting Career Opportunities

Forensic Accounting

Uses accounting, auditing, and investigative skills

APPENDIX 1A Accounting Career Opportunities

Forensic Accounting

Uses accounting, auditing, and investigative skills

LO 10 Describe the impact of international accounting standards on U.S.

LO 10 Describe the impact of international accounting standards on U.S.

LO 10 Describe the impact of international accounting standards on U.S.

LO 10 Describe the impact of international accounting standards on U.S.

LO 10 Describe the impact of international accounting standards on U.S.

LO 10 Describe the impact of international accounting standards on U.S.

LO 10 Describe the impact of international accounting standards on U.S.

LO 10 Describe the impact of international accounting standards on U.S.

LO 10 Describe the impact of international accounting standards on U.S.

LO 10 Describe the impact of international accounting standards on U.S.

Both the IASB and the FASB are hard at work developing

Both the IASB and the FASB are hard at work developing

Which of the following is not a reason why a single

Which of the following is not a reason why a single

The Sarbanes-Oxley Act determines:

international tax regulations.

internal control standards as enforced by

The Sarbanes-Oxley Act determines:

international tax regulations.

internal control standards as enforced by

IFRS is considered to be more:

principles-based and less rules-based than GAAP.

rules-based

IFRS is considered to be more:

principles-based and less rules-based than GAAP.

rules-based

Учет расчетов

Учет расчетов General Risk Assessment

General Risk Assessment Состав и содержание сметной документации

Состав и содержание сметной документации Бухгалтерский баланс

Бухгалтерский баланс ДКБ. Этапы развития денег

ДКБ. Этапы развития денег Обязательное медицинское страхование

Обязательное медицинское страхование Локальний кшторис

Локальний кшторис Облікова політика підприємства

Облікова політика підприємства Документация и инвентаризация

Документация и инвентаризация Доходы и расходы семьи

Доходы и расходы семьи Финансовые инструменты рынка капитала

Финансовые инструменты рынка капитала Страхование

Страхование Методика расчета и уплаты налогов НДС: порядок исчисления и уплаты, налоговые вычеты

Методика расчета и уплаты налогов НДС: порядок исчисления и уплаты, налоговые вычеты Фонд обязательного медицинского страхования

Фонд обязательного медицинского страхования Державний фінансовий контроль

Державний фінансовий контроль День банка в Альфа-Банк

День банка в Альфа-Банк Есепті кезеңнің және өткен кезеңдердің бөлінбеген кірісі (пайдасы) жабылмаған зияны

Есепті кезеңнің және өткен кезеңдердің бөлінбеген кірісі (пайдасы) жабылмаған зияны артем

артем Права, обязанности, ответственность органов, осуществляющих финансовый контроль. (Лекция 5)

Права, обязанности, ответственность органов, осуществляющих финансовый контроль. (Лекция 5) ООО Лайф Иншуренс

ООО Лайф Иншуренс О государственном аудите

О государственном аудите Подготовка 6-НДФЛ с учетом последних изменений

Подготовка 6-НДФЛ с учетом последних изменений Деньги и инфляция. Занятие 7

Деньги и инфляция. Занятие 7 Как заработать на фондовом и валютном рынке

Как заработать на фондовом и валютном рынке Учет финансовых вложений

Учет финансовых вложений Международный валютный фонд

Международный валютный фонд Заполнение налоговой декларации

Заполнение налоговой декларации Моя будущая профессия - бухгалтер

Моя будущая профессия - бухгалтер