- Ch1-2. Overview of the financial system. Financial Institutions and Markets

Содержание

- 2. OVERVIEW OF THE FINANCIAL SYSTEM FUNCTION OF FINANCIAL MARKETS STRUCTURE OF FINANCIAL MARKETS FUNCTIONS OF FINANCIAL

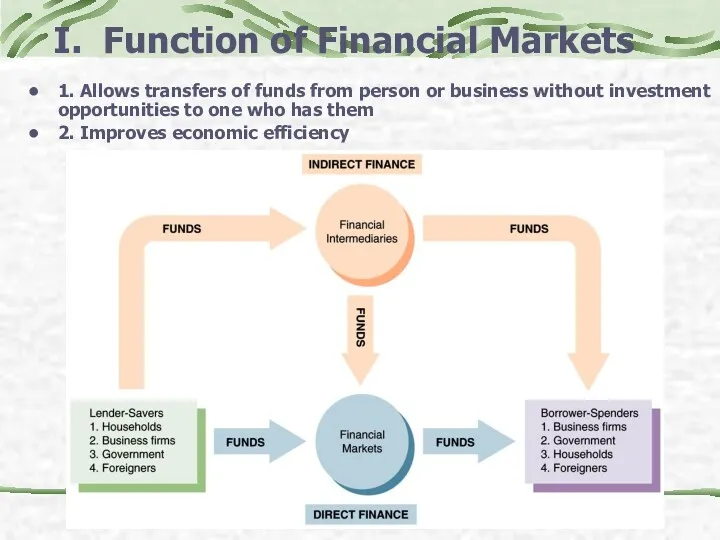

- 3. I. Function of Financial Markets 1. Allows transfers of funds from person or business without investment

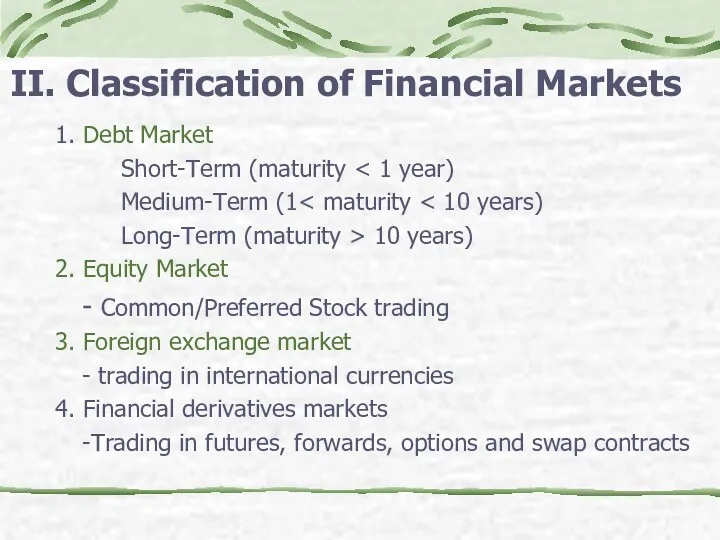

- 4. II. Classification of Financial Markets 1. Debt Market Short-Term (maturity Medium-Term (1 Long-Term (maturity > 10

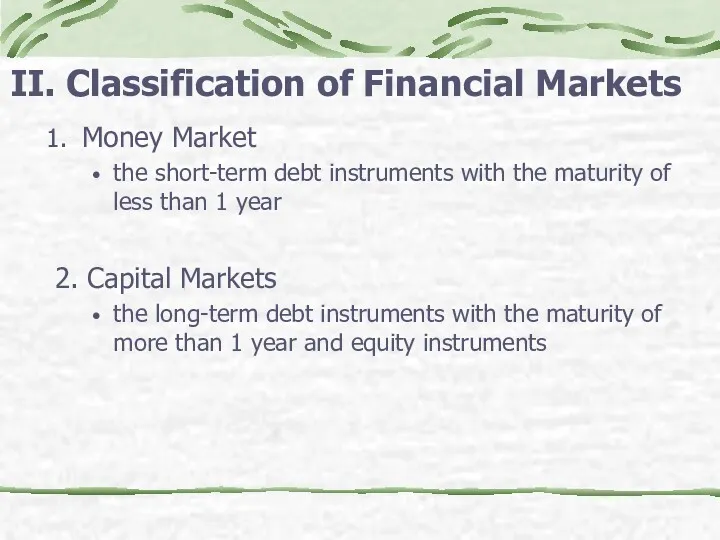

- 5. II. Classification of Financial Markets Money Market the short-term debt instruments with the maturity of less

- 6. Classification of Financial Markets 1. Primary Market New security issues sold to initial buyers Investment Banks

- 7. Classifications of Financial Markets 1. Exchanges Trades conducted in central locations (e.g., New York Stock Exchange,

- 8. Globalization of Financial Markets International Bond Market Foreign bonds sold in a foreign country and denominated

- 9. III. Functions of Financial Intermediaries Financial Intermediaries 1. Engage in process of indirect finance 2. More

- 10. Transactions Costs 1. Financial intermediaries make profits by reducing transactions costs 2. Reduce transactions costs by

- 11. Function of Financial Intermediaries A financial intermediary’s low transaction costs mean that it can provide its

- 12. Function of Financial Intermediaries Another benefit made possible by the FI’s low transaction costs is that

- 13. Asymmetric Information: Adverse Selection and Moral Hazard Adverse Selection 1. Before the transaction occurs 2. Potential

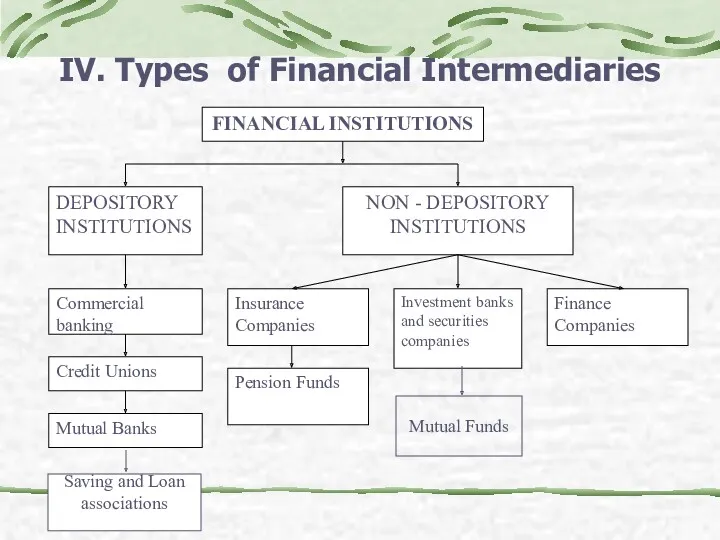

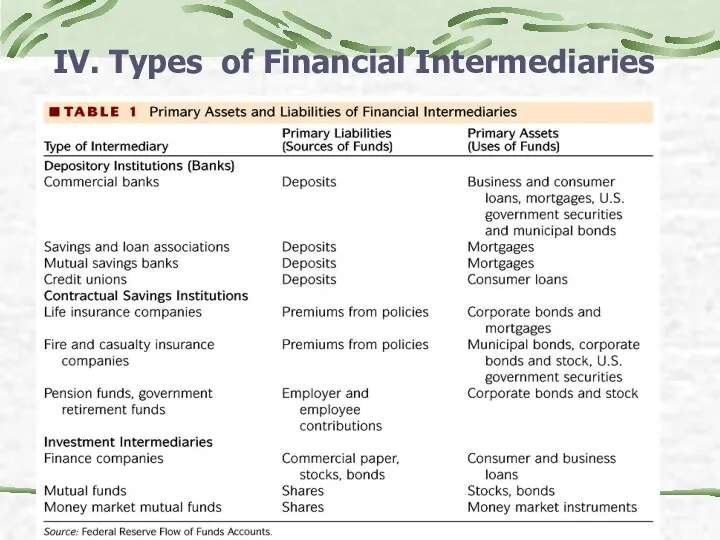

- 14. IV. Types of Financial Intermediaries Saving and Loan associations Mutual Funds

- 15. IV. Types of Financial Intermediaries

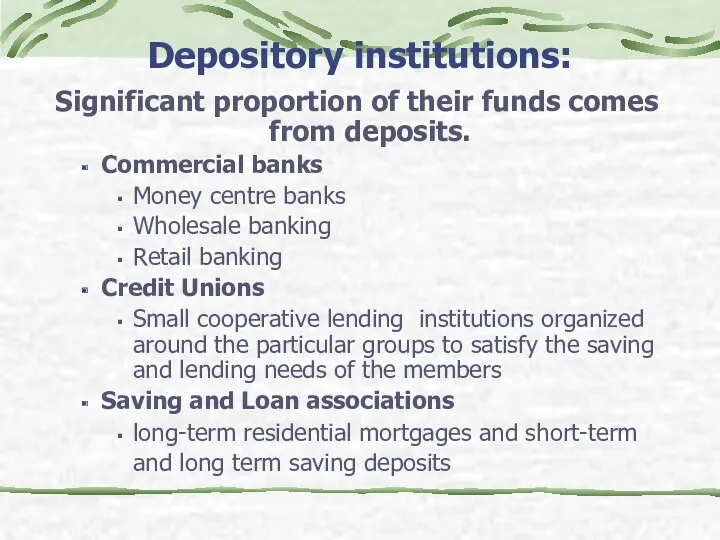

- 16. Depository institutions: Significant proportion of their funds comes from deposits. Commercial banks Money centre banks Wholesale

- 17. The Largest Banks in the World (by assets size)

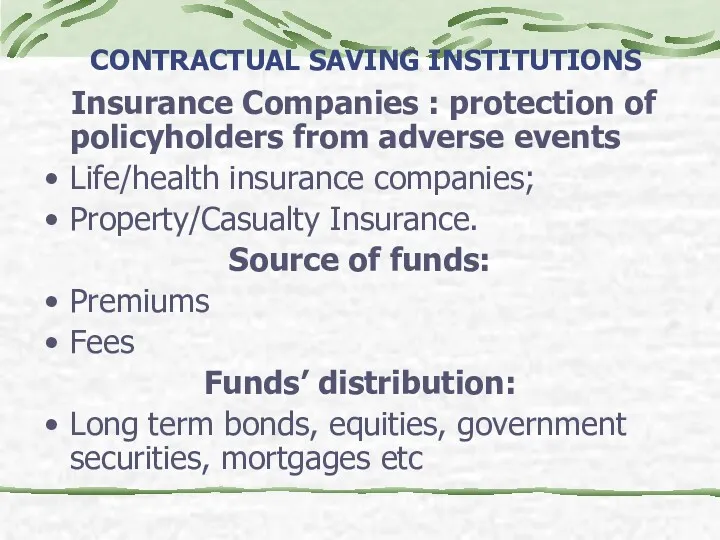

- 18. CONTRACTUAL SAVING INSTITUTIONS Insurance Companies : protection of policyholders from adverse events Life/health insurance companies; Property/Casualty

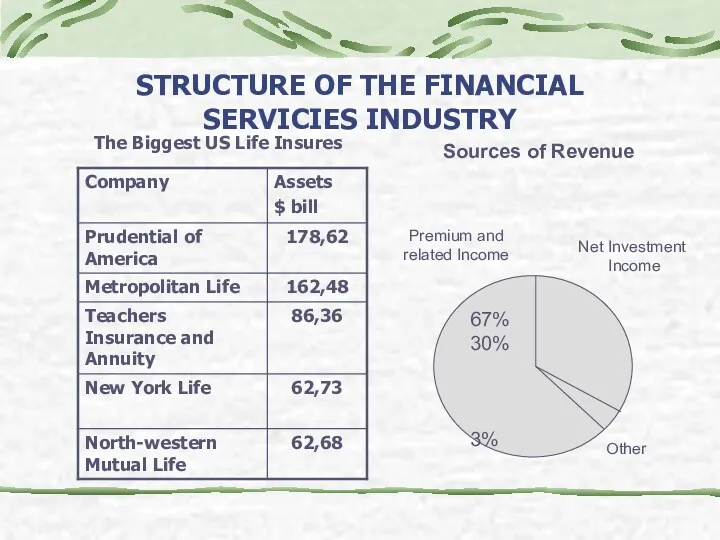

- 19. STRUCTURE OF THE FINANCIAL SERVICIES INDUSTRY The Biggest US Life Insures Sources of Revenue 67% 30%

- 20. CONTRACTUAL SAVING INSTITUTIONS Pension Funds: Private and Government organizations that provide financial services for retirement or

- 21. INVESTMENT INTERMEDIARIES Investment Banks engage in originating, underwriting and distribution of securities’ issue, investing and speculation,

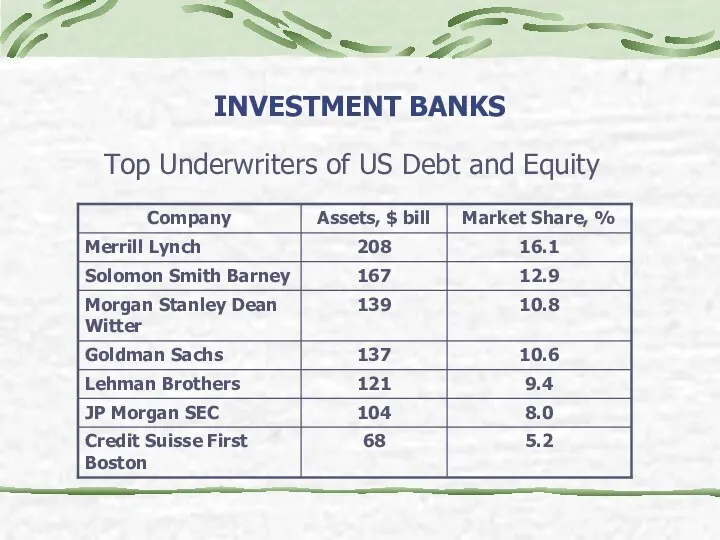

- 22. INVESTMENT BANKS Top Underwriters of US Debt and Equity

- 23. INVESTMENT INTERMEDIARIES Mutual Funds Pool the financial resources of individuals and companies and invest in diversified

- 24. INVESTMENT INTERMEDIARIES Types of Mutual Funds: Short - term Funds: Money Market Mutual Funds (MMMFs) Long

- 25. INVESTMENT INTERMEDIARIES Finance Companies Do not accept deposits but rely on short and long-term debt; Make

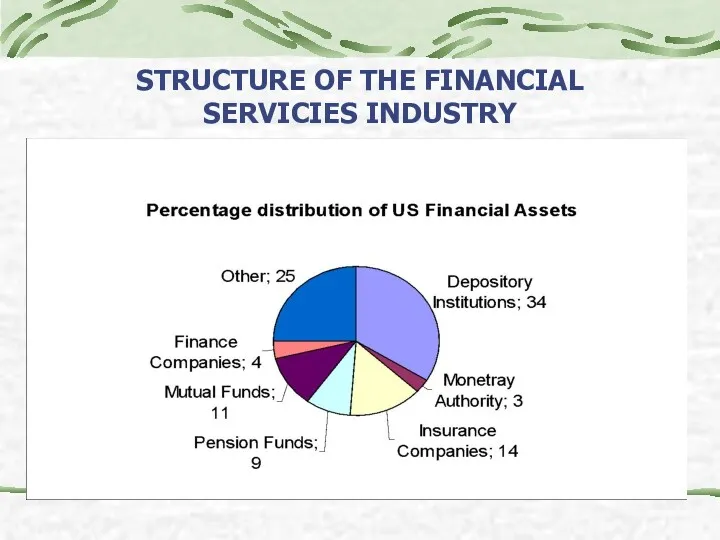

- 26. STRUCTURE OF THE FINANCIAL SERVICIES INDUSTRY

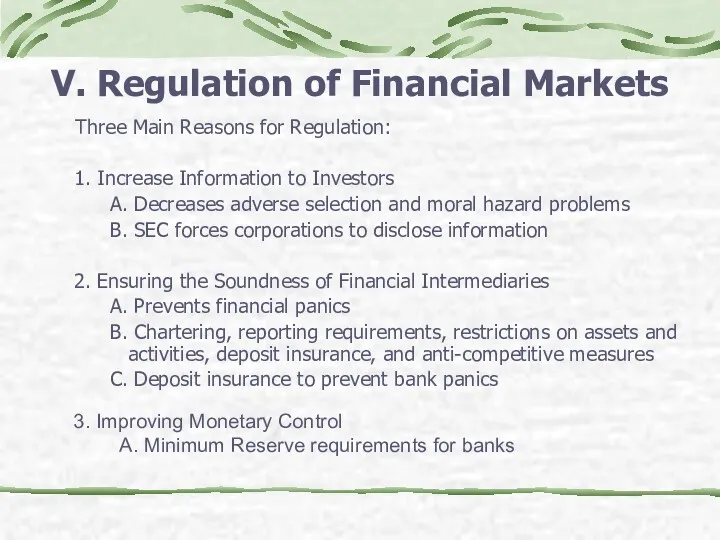

- 27. V. Regulation of Financial Markets Three Main Reasons for Regulation: 1. Increase Information to Investors A.

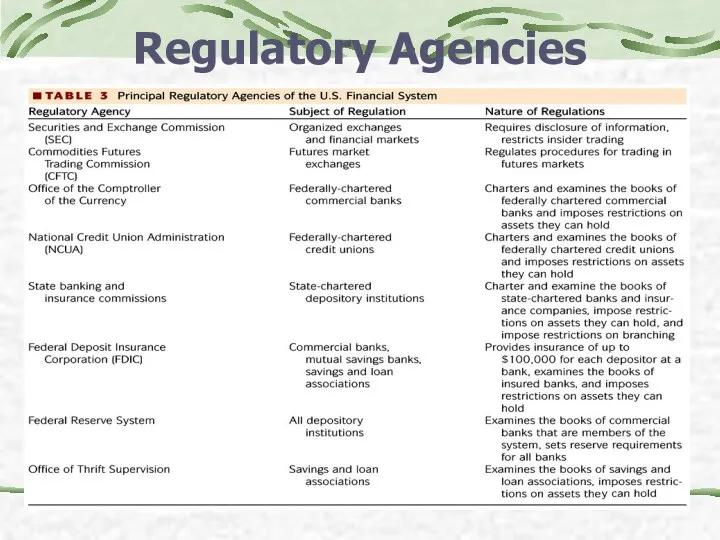

- 28. Regulatory Agencies

- 30. Скачать презентацию

OVERVIEW OF THE FINANCIAL SYSTEM

FUNCTION OF FINANCIAL MARKETS

STRUCTURE OF FINANCIAL MARKETS

FUNCTIONS

OVERVIEW OF THE FINANCIAL SYSTEM

FUNCTION OF FINANCIAL MARKETS

STRUCTURE OF FINANCIAL MARKETS

FUNCTIONS

I. Function of Financial Markets

1. Allows transfers of funds

I. Function of Financial Markets

1. Allows transfers of funds

II. Classification of Financial Markets

1. Debt Market

Short-Term (maturity < 1

II. Classification of Financial Markets

1. Debt Market

Short-Term (maturity < 1

II. Classification of Financial Markets

Money Market

the short-term debt instruments with the

II. Classification of Financial Markets

Money Market

the short-term debt instruments with the

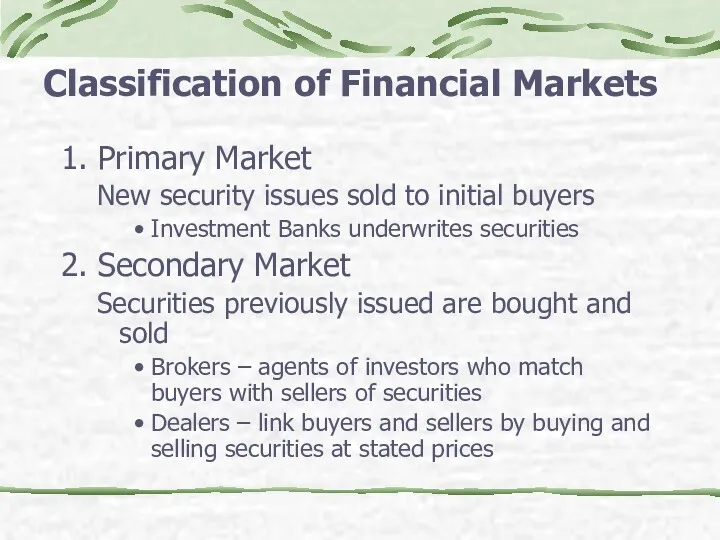

Classification of Financial Markets

1. Primary Market

New security issues sold to initial

Classification of Financial Markets

1. Primary Market

New security issues sold to initial

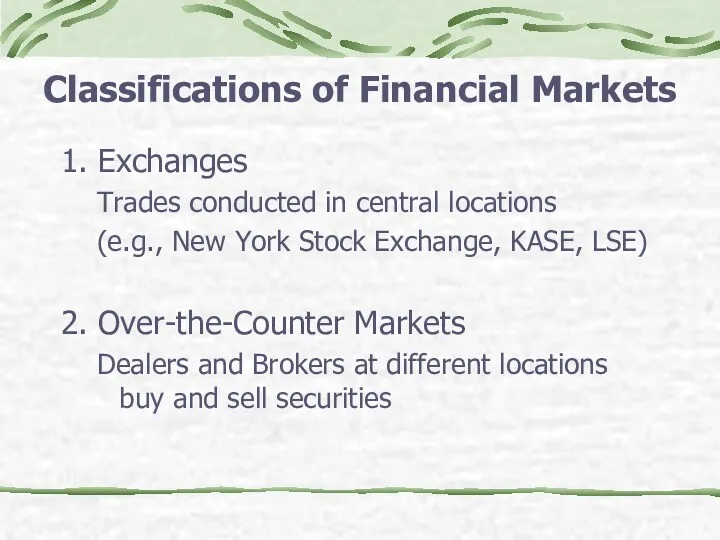

Classifications of Financial Markets

1. Exchanges

Trades conducted in central locations

(e.g., New

Classifications of Financial Markets

1. Exchanges

Trades conducted in central locations

(e.g., New

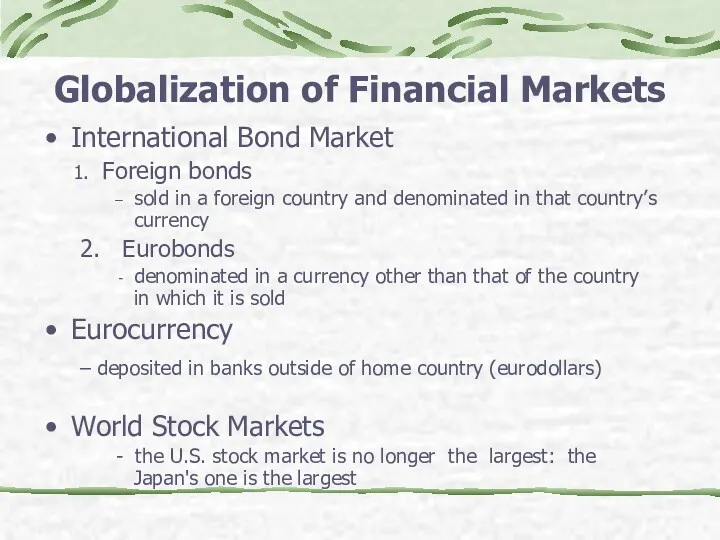

Globalization of Financial Markets

International Bond Market

Foreign bonds

sold in a foreign

Globalization of Financial Markets

International Bond Market

Foreign bonds

sold in a foreign

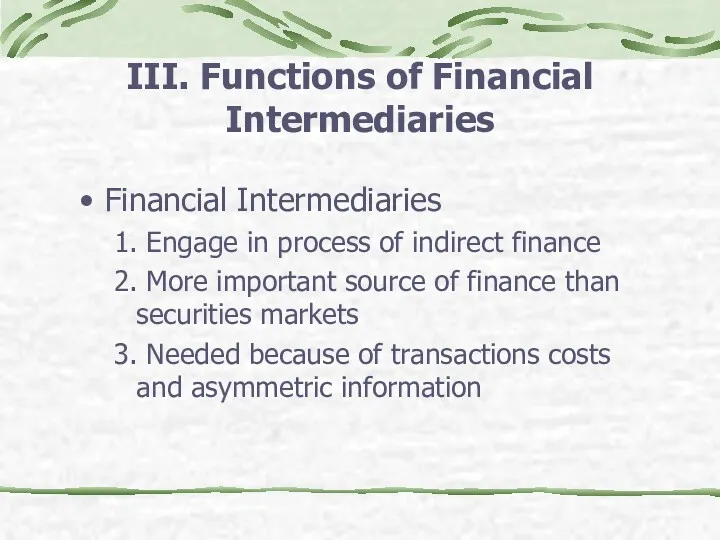

III. Functions of Financial Intermediaries

Financial Intermediaries

1. Engage in process of indirect

III. Functions of Financial Intermediaries

Financial Intermediaries

1. Engage in process of indirect

Transactions Costs

1. Financial intermediaries make profits by reducing transactions costs

Transactions Costs

1. Financial intermediaries make profits by reducing transactions costs

Function of Financial Intermediaries

A financial intermediary’s low transaction costs mean that

Function of Financial Intermediaries

A financial intermediary’s low transaction costs mean that

Function of Financial Intermediaries

Another benefit made possible by the FI’s low

Function of Financial Intermediaries

Another benefit made possible by the FI’s low

Asymmetric Information: Adverse Selection and Moral Hazard

Adverse Selection

1. Before the transaction

Asymmetric Information: Adverse Selection and Moral Hazard

Adverse Selection

1. Before the transaction

IV. Types of Financial Intermediaries

Saving and Loan

associations

Mutual Funds

IV. Types of Financial Intermediaries

Saving and Loan

associations

Mutual Funds

IV. Types of Financial Intermediaries

IV. Types of Financial Intermediaries

Depository institutions:

Significant proportion of their funds comes from deposits.

Commercial banks

Depository institutions:

Significant proportion of their funds comes from deposits.

Commercial banks

The Largest Banks in the World

(by assets size)

The Largest Banks in the World

(by assets size)

CONTRACTUAL SAVING INSTITUTIONS

Insurance Companies : protection of policyholders from adverse

CONTRACTUAL SAVING INSTITUTIONS

Insurance Companies : protection of policyholders from adverse

STRUCTURE OF THE FINANCIAL SERVICIES INDUSTRY

The Biggest US Life Insures

Sources of

STRUCTURE OF THE FINANCIAL SERVICIES INDUSTRY

The Biggest US Life Insures

Sources of

CONTRACTUAL SAVING INSTITUTIONS

Pension Funds:

Private and Government organizations that provide financial

CONTRACTUAL SAVING INSTITUTIONS

Pension Funds:

Private and Government organizations that provide financial

INVESTMENT INTERMEDIARIES

Investment Banks engage in originating, underwriting and distribution of securities’

INVESTMENT INTERMEDIARIES

Investment Banks engage in originating, underwriting and distribution of securities’

INVESTMENT BANKS

Top Underwriters of US Debt and Equity

INVESTMENT BANKS

Top Underwriters of US Debt and Equity

INVESTMENT INTERMEDIARIES

Mutual Funds

Pool the financial resources of individuals and companies and

INVESTMENT INTERMEDIARIES

Mutual Funds

Pool the financial resources of individuals and companies and

INVESTMENT INTERMEDIARIES

Types of Mutual Funds:

Short - term Funds:

Money Market Mutual

INVESTMENT INTERMEDIARIES

Types of Mutual Funds:

Short - term Funds:

Money Market Mutual

INVESTMENT INTERMEDIARIES

Finance Companies

Do not accept deposits but rely on short

INVESTMENT INTERMEDIARIES

Finance Companies

Do not accept deposits but rely on short

STRUCTURE OF THE FINANCIAL SERVICIES INDUSTRY

STRUCTURE OF THE FINANCIAL SERVICIES INDUSTRY

V. Regulation of Financial Markets

Three Main Reasons for Regulation:

1. Increase

V. Regulation of Financial Markets

Three Main Reasons for Regulation:

1. Increase

Regulatory Agencies

Regulatory Agencies

Закон волн Эллиотта. Идентификация волн в режиме реального времени

Закон волн Эллиотта. Идентификация волн в режиме реального времени Отчет об исполнении бюджета Бардымского муниципального района за 2019 год

Отчет об исполнении бюджета Бардымского муниципального района за 2019 год Возможности программ Фонда содействия инновациям

Возможности программ Фонда содействия инновациям Индивидуальные инвестиционные cчета. Казначейство РНКБ Банк (ПАО) 2018

Индивидуальные инвестиционные cчета. Казначейство РНКБ Банк (ПАО) 2018 Банк Авангард. Программа Школьное питание

Банк Авангард. Программа Школьное питание Актуальные вопросы учета поступлений в бюджетную систему Российской Федерации в 2021 г. и администрирование

Актуальные вопросы учета поступлений в бюджетную систему Российской Федерации в 2021 г. и администрирование Деньги. История денег

Деньги. История денег Профессия бухгалтер

Профессия бухгалтер Налоги. Структура налога

Налоги. Структура налога ВТБ24. Лизинг оборудования

ВТБ24. Лизинг оборудования Депозитная программа. Депозитный модуль АБС

Депозитная программа. Депозитный модуль АБС Анализ финансовой устойчивости предприятия

Анализ финансовой устойчивости предприятия Проектирование бизнеса. Практика 5. Денежные потоки инвестиционного проекта

Проектирование бизнеса. Практика 5. Денежные потоки инвестиционного проекта Бухгалтерский учет и налогообложение в субъектах малого предпринимательства

Бухгалтерский учет и налогообложение в субъектах малого предпринимательства Учёт, анализ состояния и оценка динамики дебиторской задолженности

Учёт, анализ состояния и оценка динамики дебиторской задолженности Инициативное предложение члена бюджетной комиссии Андреевой Натальи Евгеньевны в рамках проекта Народный бюджет

Инициативное предложение члена бюджетной комиссии Андреевой Натальи Евгеньевны в рамках проекта Народный бюджет Бюджет для граждан

Бюджет для граждан Субсидии администрации Краснодарского края для реализации программ социально ориентированных некоммерческих организаций

Субсидии администрации Краснодарского края для реализации программ социально ориентированных некоммерческих организаций Оценка состояния бухгалтерского учета и внутреннего контроля основных средств в ООО Электротехническая компания

Оценка состояния бухгалтерского учета и внутреннего контроля основных средств в ООО Электротехническая компания Управление капиталом организации

Управление капиталом организации Мастер-класс Финансовые ресурсы предприятия и Эффективность и риски предпринимательской деятельности

Мастер-класс Финансовые ресурсы предприятия и Эффективность и риски предпринимательской деятельности Финансовая политика государства

Финансовая политика государства План-график закупок для обеспечения государственных и муниципальных нужд на финансовый год

План-график закупок для обеспечения государственных и муниципальных нужд на финансовый год Ипотечное кредитование. ПАО Банк ЗЕНИТ

Ипотечное кредитование. ПАО Банк ЗЕНИТ Виды ценных бумаг

Виды ценных бумаг Вопросы по продуктам РКО Tinkoff

Вопросы по продуктам РКО Tinkoff Цели и задачи управления государственным долгом

Цели и задачи управления государственным долгом Ночной аудитор отеля

Ночной аудитор отеля