- Currency forwards and swaps

Содержание

- 2. Lesson objectives Introduce the concept of currency forwards and FX swaps and currency swaps Review the

- 3. Introduction Financial instruments can be denominated in different currencies. Financial markets offer wide variety of liquid

- 4. Currency forwards definition Foreign currency forwards are used as a foreign currency hedge when an investor

- 5. Currency forward contracts

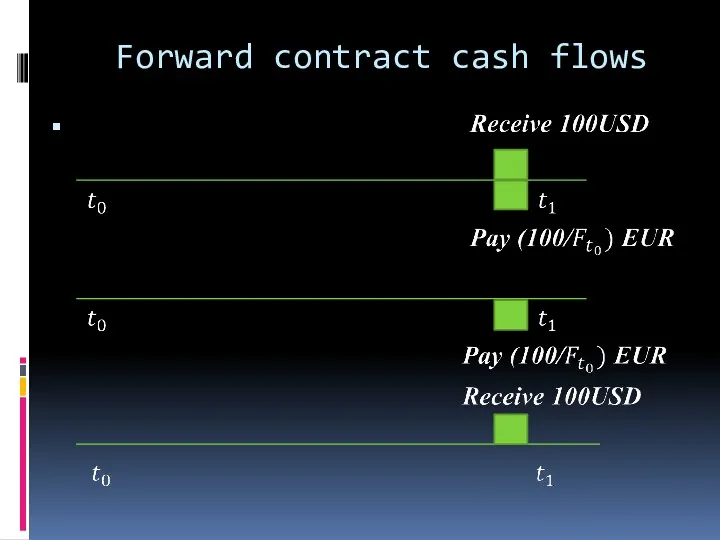

- 6. Forward contract cash flows

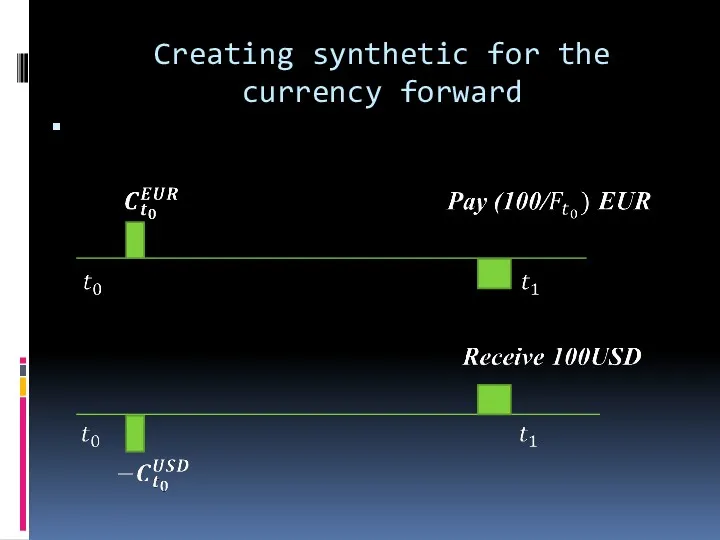

- 7. Creating synthetic for the currency forward

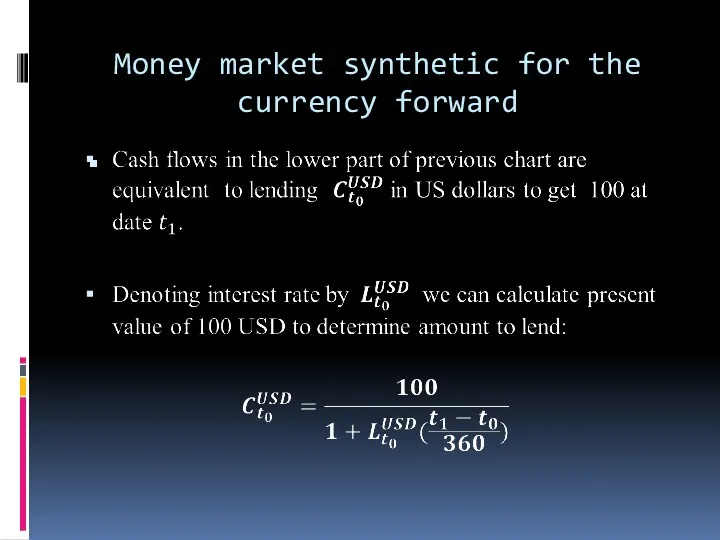

- 8. Money market synthetic for the currency forward

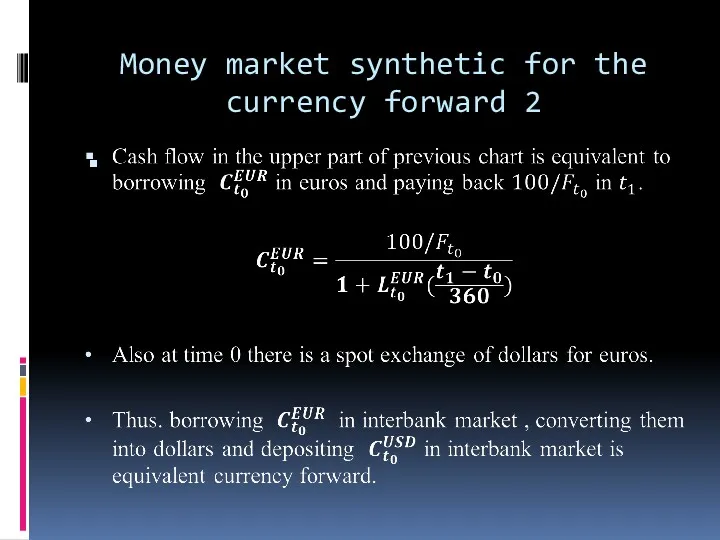

- 9. Money market synthetic for the currency forward 2

- 10. Bonds synthetic for the currency forward

- 11. Pricing of forward contracts

- 12. Pricing of forward contracts 2 FX forward USD against EUR Using proceeds buy USD against EUR

- 13. Quoting conventions for FX forwards Markets quote forward points rather than outright forward rates. For instance

- 14. Quoting conventions for FX forwards 2

- 15. Foreign exchange swaps Foreign exchange swap is a contract in which one party borrows one currency

- 16. Foreign exchange swaps 2

- 17. Foreign exchange swaps advantages FX swaps are interbank instruments , not available to clients . Counterparty

- 18. Currency swaps

- 19. Currency swaps 2

- 21. Скачать презентацию

Lesson objectives

Introduce the concept of currency forwards and FX swaps and

Lesson objectives

Introduce the concept of currency forwards and FX swaps and

Introduction

Financial instruments can be denominated in different currencies.

Financial markets offer

Introduction

Financial instruments can be denominated in different currencies.

Financial markets offer

Currency forwards definition

Foreign currency forwards are used as a foreign currency

Currency forwards definition

Foreign currency forwards are used as a foreign currency

Currency forward contracts

Currency forward contracts

Forward contract cash flows

Forward contract cash flows

Creating synthetic for the currency forward

Creating synthetic for the currency forward

Money market synthetic for the currency forward

Money market synthetic for the currency forward

Money market synthetic for the currency forward 2

Money market synthetic for the currency forward 2

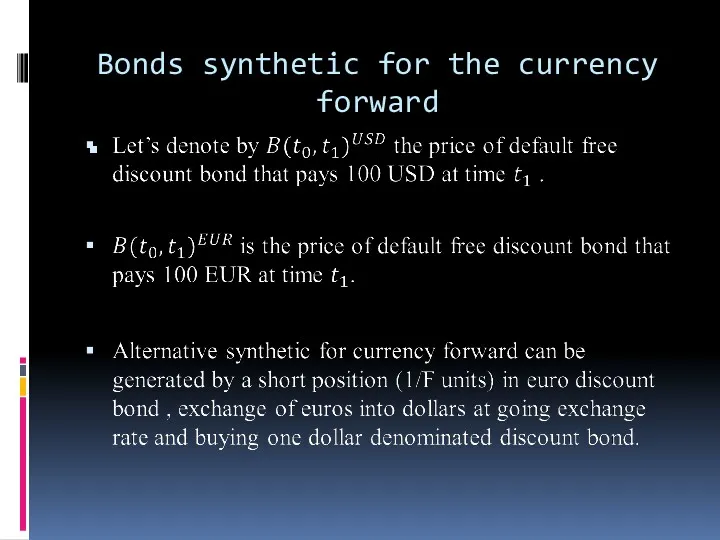

Bonds synthetic for the currency forward

Bonds synthetic for the currency forward

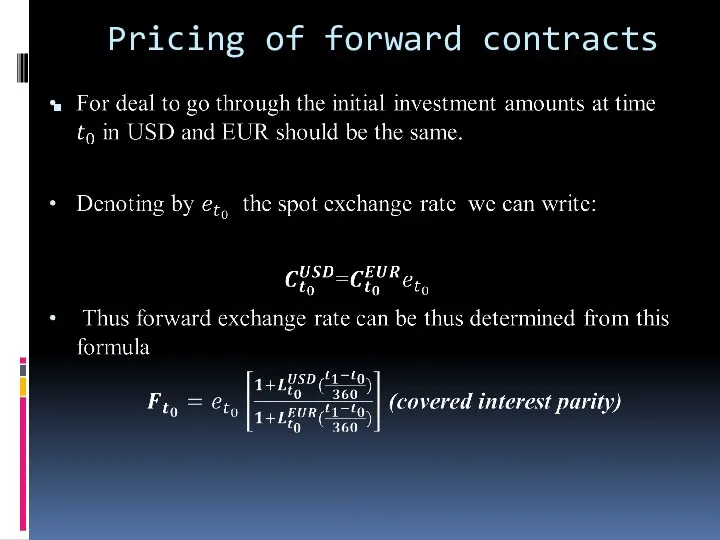

Pricing of forward contracts

Pricing of forward contracts

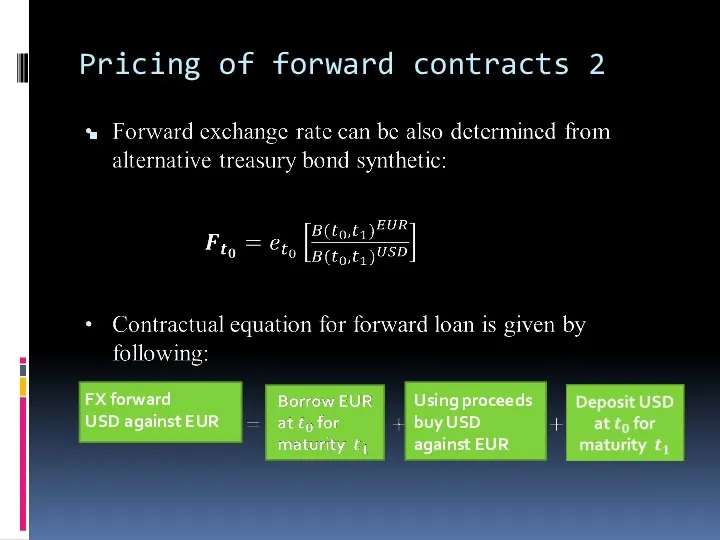

Pricing of forward contracts 2

FX forward

USD against EUR

Using proceeds

Pricing of forward contracts 2

FX forward

USD against EUR

Using proceeds

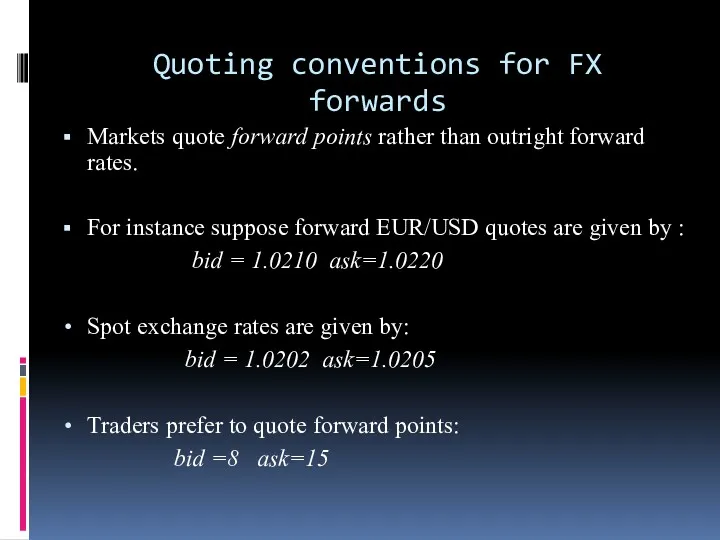

Quoting conventions for FX forwards

Markets quote forward points rather than outright

Quoting conventions for FX forwards

Markets quote forward points rather than outright

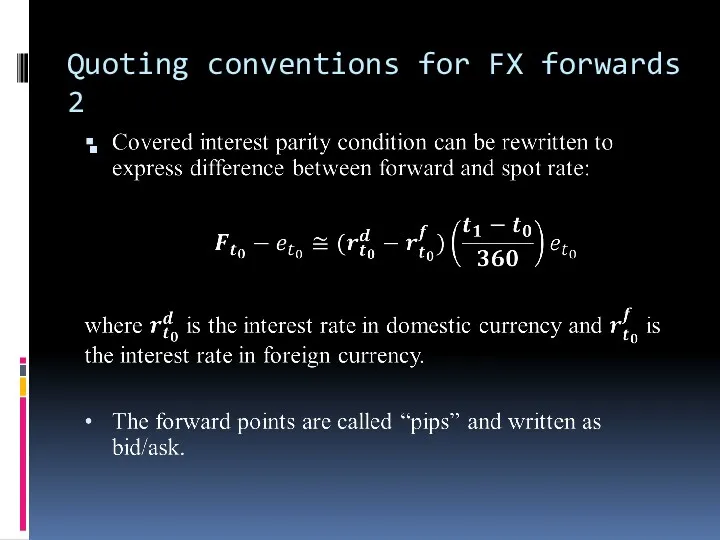

Quoting conventions for FX forwards 2

Quoting conventions for FX forwards 2

Foreign exchange swaps

Foreign exchange swap is a contract in which

Foreign exchange swaps

Foreign exchange swap is a contract in which

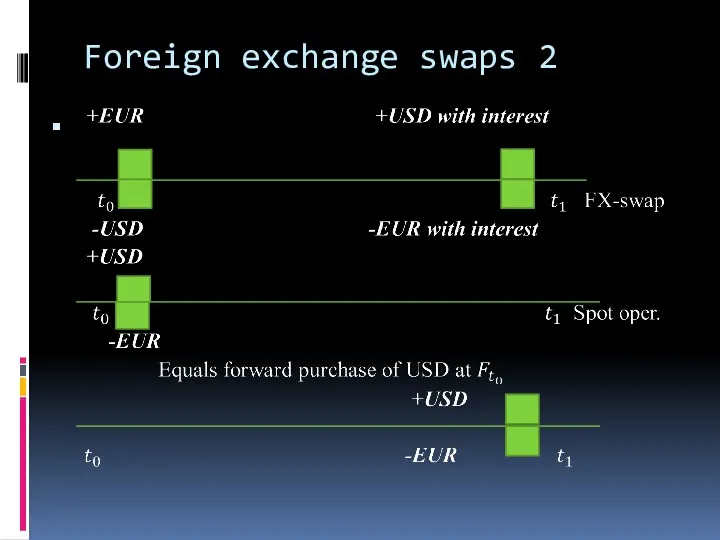

Foreign exchange swaps 2

Foreign exchange swaps 2

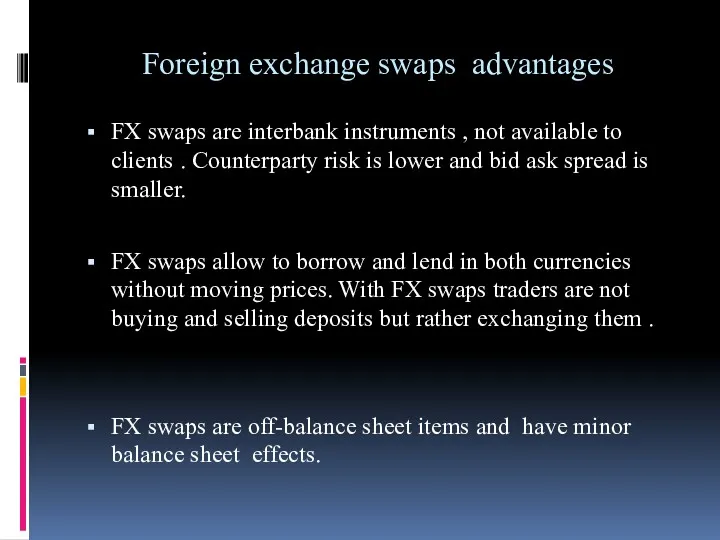

Foreign exchange swaps advantages

FX swaps are interbank instruments , not available

Foreign exchange swaps advantages

FX swaps are interbank instruments , not available

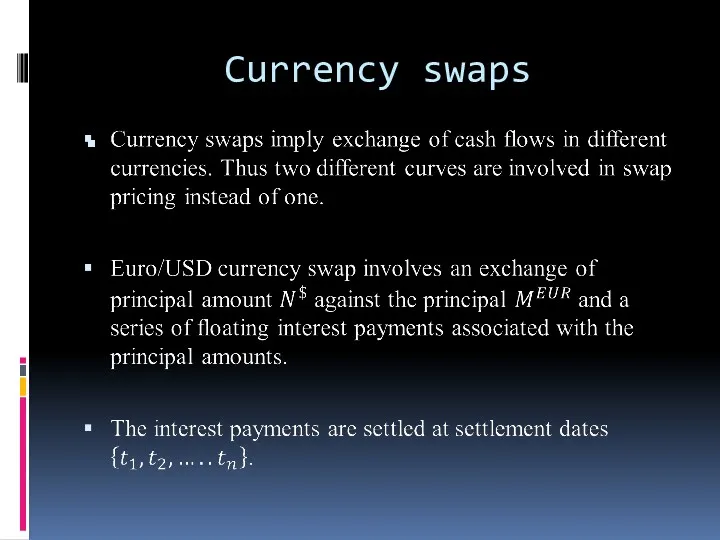

Currency swaps

Currency swaps

Currency swaps 2

Currency swaps 2

Финансовые инструменты АО Банк Развития Казахстана

Финансовые инструменты АО Банк Развития Казахстана Дебетовая карта

Дебетовая карта Отчетность страхователей для ведения индивидуального (персонифицированного) учета

Отчетность страхователей для ведения индивидуального (персонифицированного) учета Как работать с единым налоговым платежом

Как работать с единым налоговым платежом Основи побудови фінансово обліку

Основи побудови фінансово обліку Государственное регулирование кризисных ситуаций. Тема № 2

Государственное регулирование кризисных ситуаций. Тема № 2 Корректировка плана МТО ООО Таргин

Корректировка плана МТО ООО Таргин Бухгалтерлік есеп және аудит

Бухгалтерлік есеп және аудит Как проявить должную осмотрительность. Мнение ФНС

Как проявить должную осмотрительность. Мнение ФНС Сущность и функции денег. Денежное обращение

Сущность и функции денег. Денежное обращение Виды кредитов

Виды кредитов Навчальна дисципліна Фінанси для спеціальності Правознавство

Навчальна дисципліна Фінанси для спеціальності Правознавство Основы кредитно-денежной политики

Основы кредитно-денежной политики Положение по ведению бухгалтерского учета и бухгалтерской отчетности в РФ

Положение по ведению бухгалтерского учета и бухгалтерской отчетности в РФ Коммерческое предложение. Проект POS-credit

Коммерческое предложение. Проект POS-credit Недержавне пенсійне страхування: стан та перспективи розвитку

Недержавне пенсійне страхування: стан та перспективи розвитку Корпорация EG

Корпорация EG Налог на прибыль организаций

Налог на прибыль организаций Инвестиции и источники финансирования инвестиционной деятельности

Инвестиции и источники финансирования инвестиционной деятельности Анализ финансово-хозяйственной деятельности предприятия на примере ООО Фурла Рус

Анализ финансово-хозяйственной деятельности предприятия на примере ООО Фурла Рус Счета-фактуры по корректировкам отгрузок и возвратам, сводные справки. 1С:ERP Управление предприятием 2

Счета-фактуры по корректировкам отгрузок и возвратам, сводные справки. 1С:ERP Управление предприятием 2 Перевод работников АО Красная звезда на новые условия оплаты труда

Перевод работников АО Красная звезда на новые условия оплаты труда Управление пассивами банка

Управление пассивами банка Налог на доходы физических лиц

Налог на доходы физических лиц Рабочий отчет департамента аналитики компании IPO

Рабочий отчет департамента аналитики компании IPO Валютные системы. Валютные риски. Валютные кризисы

Валютные системы. Валютные риски. Валютные кризисы Банковские услуги. Виды банковских услуг для физических лиц

Банковские услуги. Виды банковских услуг для физических лиц Бюджет процесі

Бюджет процесі