- Financial derivatives market and financial engineering

Содержание

- 2. Lesson objectives Introduce the essence of financial engineering. Introduce main aspects of financial derivatives markets. Describe

- 3. Financial engineering Financial engineering involves application of mathematical methods to solve financial problems. It uses methods

- 4. Financial engineering 2 Securities pricing: Financial engineering is aimed at pricing derivative securities based on arbitrage

- 5. Financial derivatives market structure

- 6. Financial Derivatives Market Financial derivatives market demonstrated very impressive growth starting from 1990s up to global

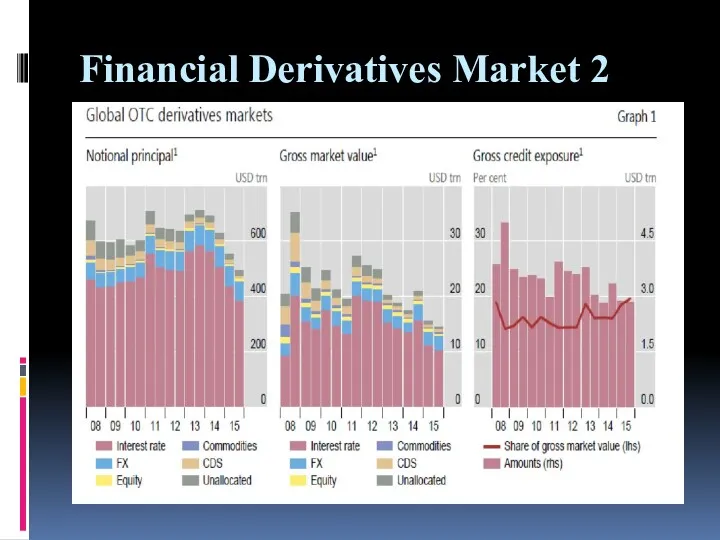

- 7. Financial Derivatives Market 2

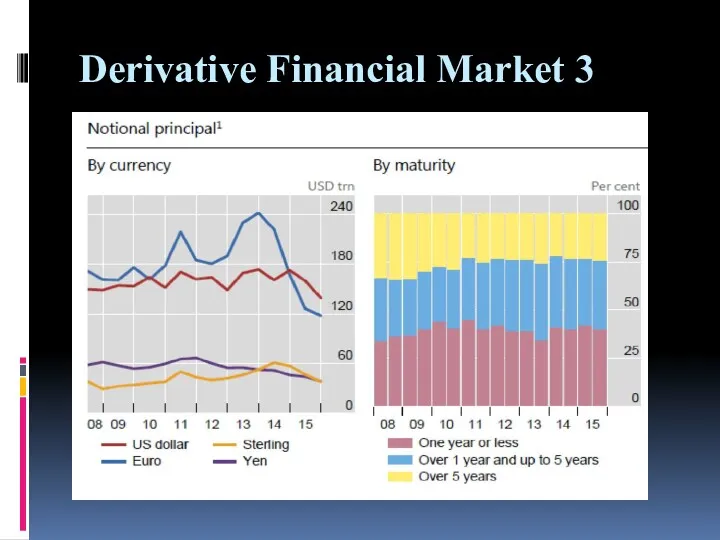

- 8. Derivative Financial Market 3

- 9. Derivative financial markets 3 In the derivative financial markets derivatives whose prices are derived from underlying

- 10. Onshore markets; Exchanges vs OTC Over-the-counter (OTC) markets evolved due to spontaneous trading activity. No formal

- 11. Onshore markets; Exchanges vs OTC 2 Organized exchanges are formal entities . Traded instruments and trading

- 12. Major players on derivatives markets Market makers: Market makers provide liquidity and must buy and sell

- 13. Major players on derivatives markets 2 Dealers: They quote two-way prices and hold large inventories of

- 14. Types of quoted prices Bid price The price at which the market maker is willing to

- 15. Major instrument classes Fixed income instruments – certificates of deposits, deposits , treasury bills . Bond

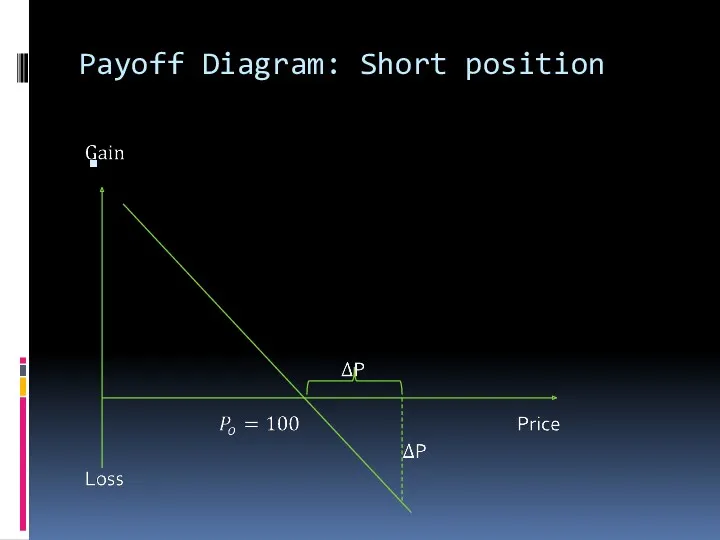

- 16. Long vs Short position Long position - buy an item for cash and hold it or

- 17. Payoff Diagram: Long position

- 18. Payoff Diagram: Funding long position

- 19. Payoff Diagram: Short position

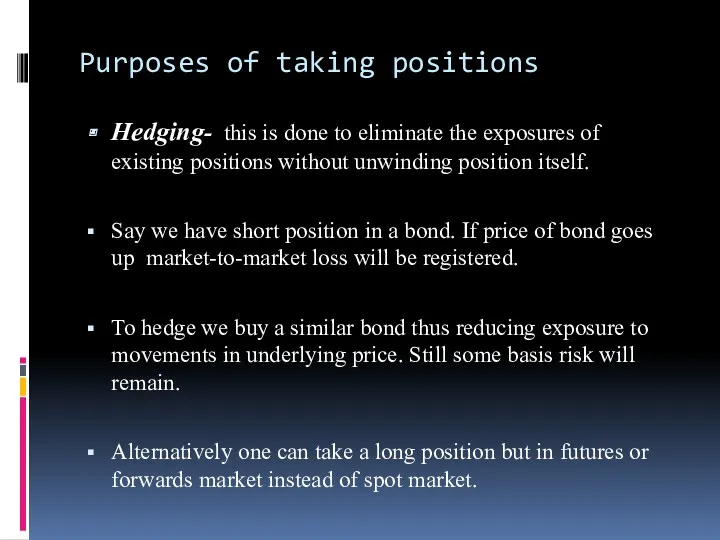

- 20. Purposes of taking positions Hedging- this is done to eliminate the exposures of existing positions without

- 21. Hedging with futures contract

- 22. Purposes of taking positions 2 Arbitrage Prices of financial instruments are arbitrage –free (no opportunity for

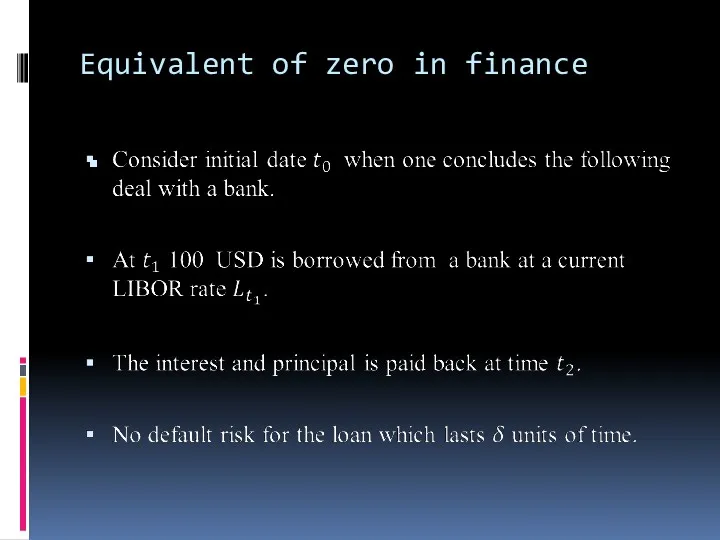

- 23. Equivalent of zero in finance

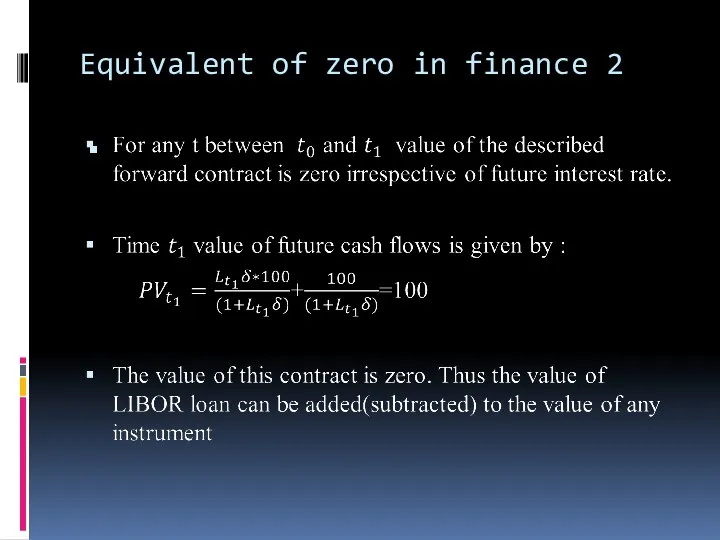

- 24. Equivalent of zero in finance 2

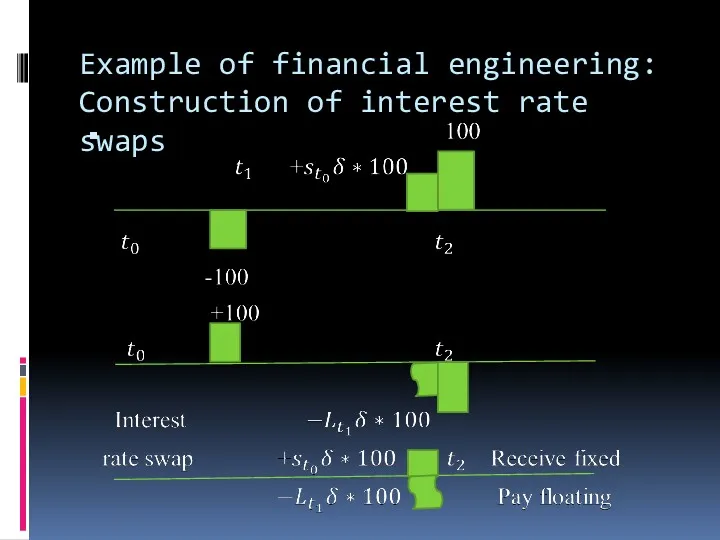

- 25. Example of financial engineering: Construction of interest rate swaps

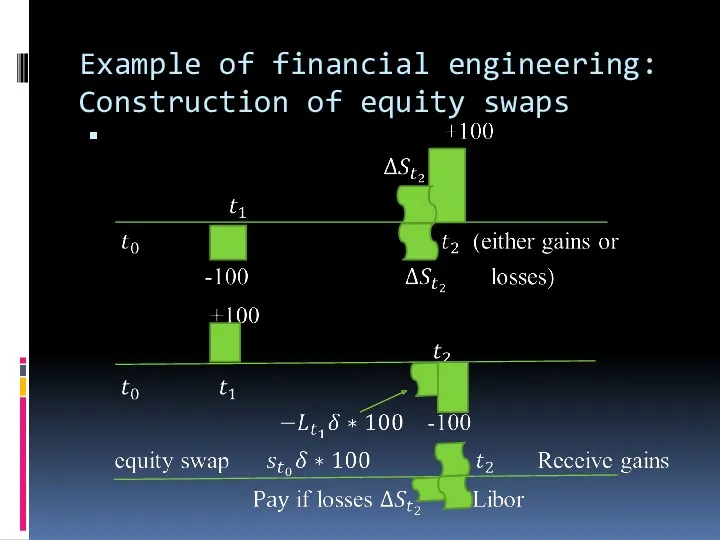

- 26. Example of financial engineering: Construction of equity swaps

- 27. Conclusion Financial engineering involves application of mathematical methods to solve such financial issues as securities valuation

- 29. Скачать презентацию

Lesson objectives

Introduce the essence of financial engineering.

Introduce main aspects of

Lesson objectives

Introduce the essence of financial engineering.

Introduce main aspects of

Financial engineering

Financial engineering involves application of mathematical methods to solve financial

Financial engineering

Financial engineering involves application of mathematical methods to solve financial

Financial engineering 2

Securities pricing: Financial engineering is aimed at pricing derivative

Financial engineering 2

Securities pricing: Financial engineering is aimed at pricing derivative

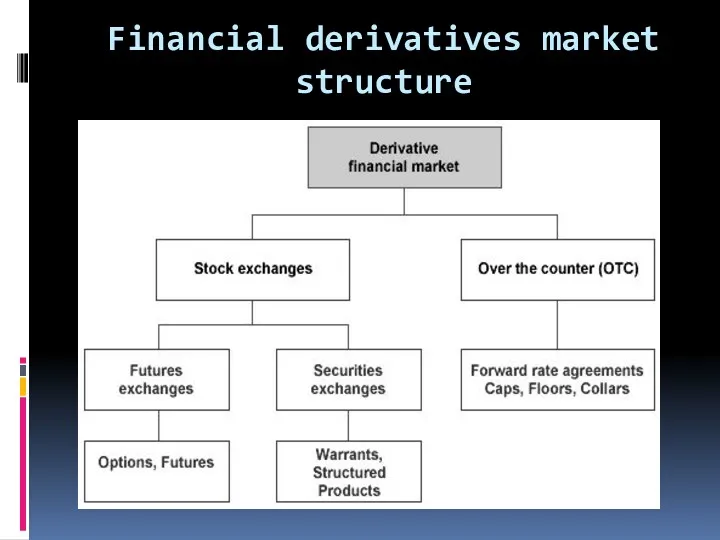

Financial derivatives market structure

Financial derivatives market structure

Financial Derivatives Market

Financial derivatives market demonstrated very impressive growth starting

Financial Derivatives Market

Financial derivatives market demonstrated very impressive growth starting

Financial Derivatives Market 2

Financial Derivatives Market 2

Derivative Financial Market 3

Derivative Financial Market 3

Derivative financial markets 3

In the derivative financial markets derivatives whose prices

Derivative financial markets 3

In the derivative financial markets derivatives whose prices

Onshore markets; Exchanges vs OTC

Over-the-counter (OTC) markets evolved due to spontaneous

Onshore markets; Exchanges vs OTC

Over-the-counter (OTC) markets evolved due to spontaneous

Onshore markets; Exchanges vs OTC 2

Organized exchanges are formal entities .

Onshore markets; Exchanges vs OTC 2

Organized exchanges are formal entities .

Major players on derivatives markets

Market makers: Market makers provide liquidity

Major players on derivatives markets

Market makers: Market makers provide liquidity

Major players on derivatives markets 2

Dealers: They quote two-way prices and

Major players on derivatives markets 2

Dealers: They quote two-way prices and

Types of quoted prices

Bid price

The price at which

Types of quoted prices

Bid price

The price at which

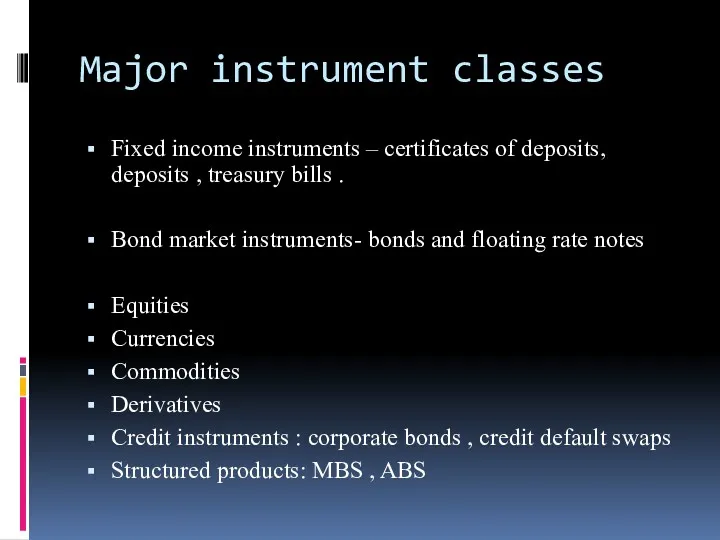

Major instrument classes

Fixed income instruments – certificates of deposits, deposits ,

Major instrument classes

Fixed income instruments – certificates of deposits, deposits ,

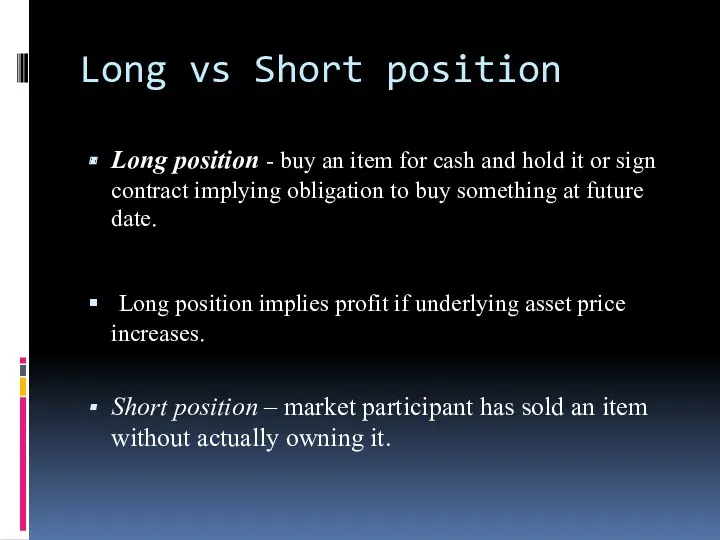

Long vs Short position

Long position - buy an item for cash

Long vs Short position

Long position - buy an item for cash

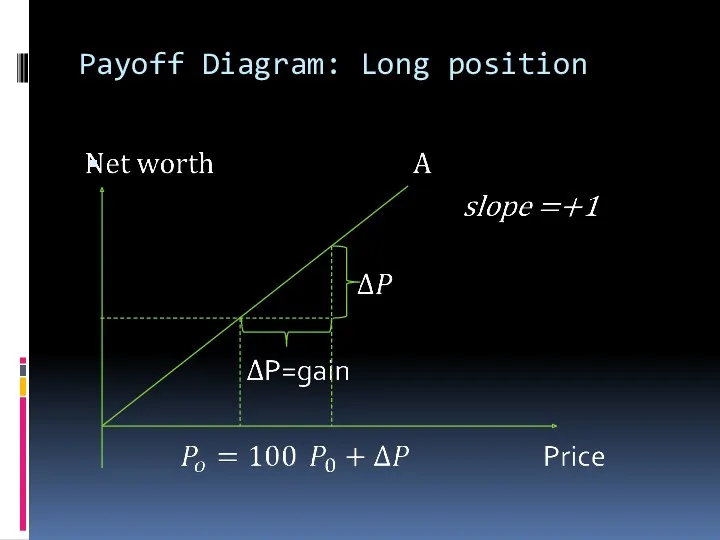

Payoff Diagram: Long position

Payoff Diagram: Long position

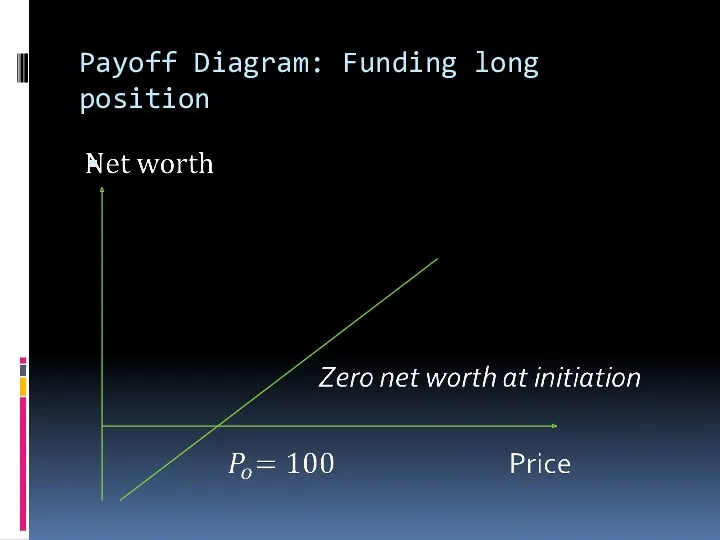

Payoff Diagram: Funding long position

Payoff Diagram: Funding long position

Payoff Diagram: Short position

Payoff Diagram: Short position

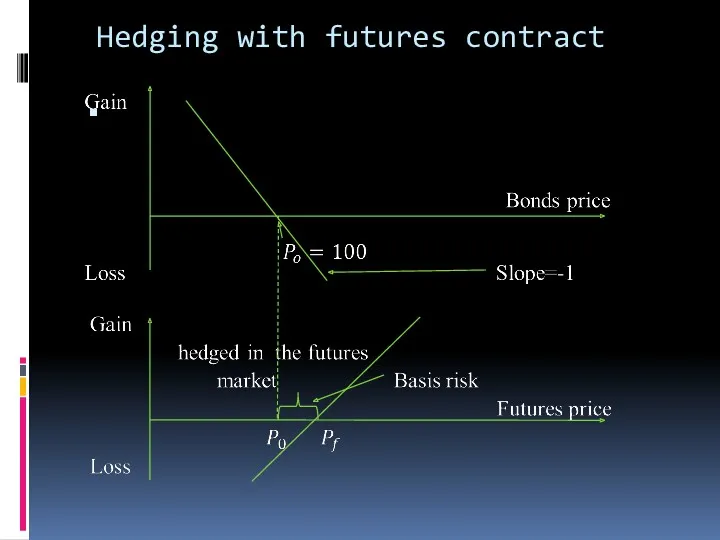

Purposes of taking positions

Hedging- this is done to eliminate the

Purposes of taking positions

Hedging- this is done to eliminate the

Hedging with futures contract

Hedging with futures contract

Purposes of taking positions 2

Arbitrage

Prices of financial instruments are arbitrage

Purposes of taking positions 2

Arbitrage

Prices of financial instruments are arbitrage

Equivalent of zero in finance

Equivalent of zero in finance

Equivalent of zero in finance 2

Equivalent of zero in finance 2

Example of financial engineering: Construction of interest rate swaps

Example of financial engineering: Construction of interest rate swaps

Example of financial engineering: Construction of equity swaps

Example of financial engineering: Construction of equity swaps

Conclusion

Financial engineering involves application of mathematical methods to solve such financial

Conclusion

Financial engineering involves application of mathematical methods to solve such financial

Биржа как институт рыночной экономики

Биржа как институт рыночной экономики Учет основных средств. Способы оценки основных средств

Учет основных средств. Способы оценки основных средств Информационные системы в банковском деле

Информационные системы в банковском деле Программа добровольного индивидуального страхования Стоп.коронавирус

Программа добровольного индивидуального страхования Стоп.коронавирус The history of the Euro

The history of the Euro Методы снижения рисков

Методы снижения рисков Налог на добавленную стоимость (НДС) при ввозе товара, порядок его установления и применения

Налог на добавленную стоимость (НДС) при ввозе товара, порядок его установления и применения Финансы публичных компаний. Прирост акционерной стоимости и инвестиционные решения корпорации

Финансы публичных компаний. Прирост акционерной стоимости и инвестиционные решения корпорации Організація та загальні принципи ведення обліку валютних операцій у прикладному рішенні 1С:Бухгалтерія 8

Організація та загальні принципи ведення обліку валютних операцій у прикладному рішенні 1С:Бухгалтерія 8 Межбанковское кредитование

Межбанковское кредитование Методы анализа и оценки рисков

Методы анализа и оценки рисков Администрация муниципального района Бабынинский район. Бюджет для граждан 2022

Администрация муниципального района Бабынинский район. Бюджет для граждан 2022 НДФЛ-2016. Внесение изменения в статью 218 части второй Налогового кодекса РФ

НДФЛ-2016. Внесение изменения в статью 218 части второй Налогового кодекса РФ Управление оборотным капиталом в период финансового оздоровления предприятия. Тема № 7

Управление оборотным капиталом в период финансового оздоровления предприятия. Тема № 7 Аудиторлық тәуекелділік және оның маңызы

Аудиторлық тәуекелділік және оның маңызы Общая характеристика корпоративных облигаций

Общая характеристика корпоративных облигаций Налог на прибыль организаций

Налог на прибыль организаций Финансовые аспекты в принятии управленческих решений

Финансовые аспекты в принятии управленческих решений НДФЛ. Эксперимент Единый налоговый платеж

НДФЛ. Эксперимент Единый налоговый платеж Затраты производства

Затраты производства Законодательная основа и организация таможенного дела в РФ

Законодательная основа и организация таможенного дела в РФ Сутність та види податків

Сутність та види податків Центр молодых специалистов 1С – от стажера до сотрудника фирмы

Центр молодых специалистов 1С – от стажера до сотрудника фирмы Выдача ЕТК льготной тарификации в МФЦ

Выдача ЕТК льготной тарификации в МФЦ Functions of Insurers

Functions of Insurers Ценные бумаги. Рынок ценных бумаг

Ценные бумаги. Рынок ценных бумаг Банк қызметінің құқықтық негіздері

Банк қызметінің құқықтық негіздері Валютная и финансово-кредитная система мировой экономики

Валютная и финансово-кредитная система мировой экономики