- Functions of Insurers

Содержание

- 2. Lecture Outline 1. Product Design and Ratemaking: - Basic Concepts and Types of Rate 2. Production

- 3. Introductory Notes The unique nature of the insurance product requires certain specialized functions that do not

- 4. Product Design The insurance process starts with creating products (i.e., policies or contracts) that specify the

- 5. Product Design Insurance contracts typically include: Provisions for covered perils; Coverage amounts and limits; Deductibles/retentions; Co-insurance

- 6. Product Design Insurance contract represents a bundle of services provided to insureds that includes but is

- 7. Ratemaking An insurance rate is the price per unit of insurance. Like any other price, it

- 8. Ratemaking One fundamental difference between insurance pricing and the pricing function in other industries is that

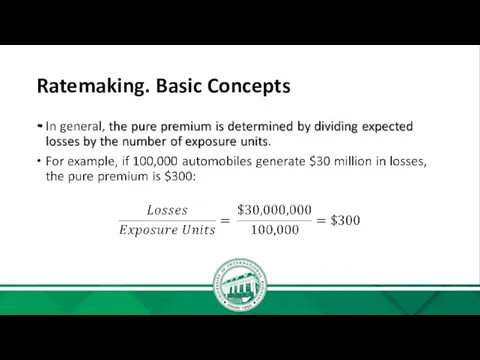

- 9. Ratemaking. Basic Concepts A rate is the price charged for each unit of protection or exposure

- 10. Ratemaking. Basic Concepts Regardless of the type of insurance, the premium income of the insurer must

- 11. Ratemaking. Basic Concepts

- 12. Ratemaking. Basic Concepts The process of converting the pure premium into a gross rate requires adding

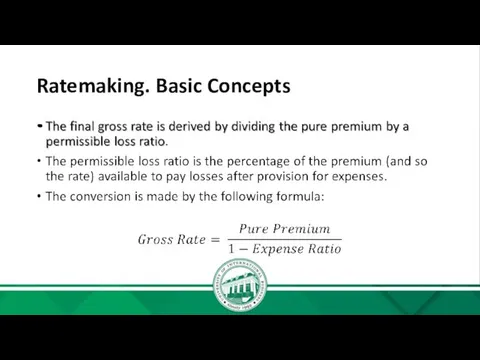

- 13. Ratemaking. Basic Concepts

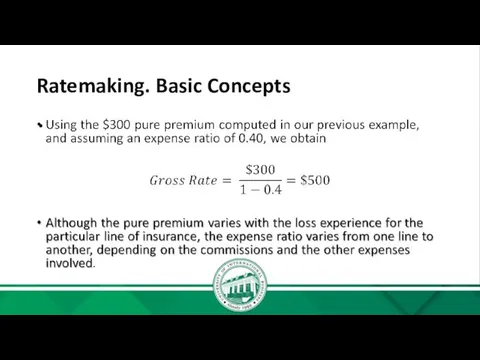

- 14. Ratemaking. Basic Concepts

- 15. Production and Distribution Production and distribution involve the marketing and sale of insurance contracts and related

- 16. Production and Distribution Classification of agents Independent agents can represent more than one insurer and “own”

- 17. Production and Distribution Other production/distribution services performed by insurers include activities related to: Marketing and advertising;

- 18. Underwriting The underwriting function entails the risk assessment, classification and selection of insureds to achieve an

- 19. Underwriting Several principles guide proper underwriting: selection according to standards; proper balance within classifications; and equity

- 20. Underwriting The balancing of risks within classifications is aimed at avoiding adverse selection causing an excessive

- 21. Underwriting It is important that insureds are treated fairly from the pricing perspective. In other words,

- 22. Loss Settlement The objective of loss settlement is to pay claims or benefit obligations arising out

- 23. Loss Settlement There are several steps in the settlement process. First, the insurer must determine that

- 24. Investment The reserves that insurers hold for unearned premiums, unpaid losses or benefits to be paid

- 25. Investment Because of their fiduciary responsibilities and the market’s valuation of their financial strength, insurers tend

- 26. The Essence of Reinsurance Reinsurance refers to the shifting of part or all of the insurance

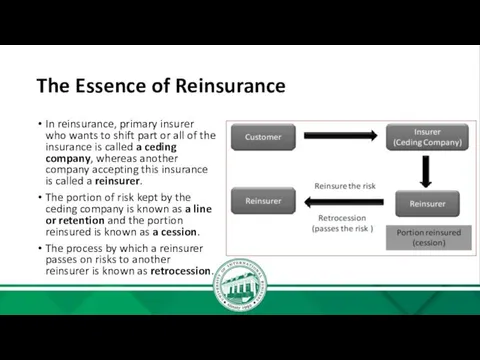

- 27. The Essence of Reinsurance In reinsurance, primary insurer who wants to shift part or all of

- 29. Скачать презентацию

Lecture Outline

1. Product Design and Ratemaking:

- Basic Concepts and Types

Lecture Outline

1. Product Design and Ratemaking:

- Basic Concepts and Types

Introductory Notes

The unique nature of the insurance product requires certain specialized

Introductory Notes

The unique nature of the insurance product requires certain specialized

Product Design

The insurance process starts with creating products (i.e., policies or

Product Design

The insurance process starts with creating products (i.e., policies or

Product Design

Insurance contracts typically include:

Provisions for covered perils;

Coverage amounts and

Product Design

Insurance contracts typically include:

Provisions for covered perils;

Coverage amounts and

Product Design

Insurance contract represents a bundle of services provided to insureds

Product Design

Insurance contract represents a bundle of services provided to insureds

Ratemaking

An insurance rate is the price per unit of insurance.

Like

Ratemaking

An insurance rate is the price per unit of insurance.

Like

Ratemaking

One fundamental difference between insurance pricing and the pricing function in

Ratemaking

One fundamental difference between insurance pricing and the pricing function in

Ratemaking. Basic Concepts

A rate is the price charged for each unit

Ratemaking. Basic Concepts

A rate is the price charged for each unit

Ratemaking. Basic Concepts

Regardless of the type of insurance, the premium income

Ratemaking. Basic Concepts

Regardless of the type of insurance, the premium income

Ratemaking. Basic Concepts

Ratemaking. Basic Concepts

Ratemaking. Basic Concepts

The process of converting the pure premium into a

Ratemaking. Basic Concepts

The process of converting the pure premium into a

Ratemaking. Basic Concepts

Ratemaking. Basic Concepts

Ratemaking. Basic Concepts

Ratemaking. Basic Concepts

Production and Distribution

Production and distribution involve the marketing and sale of

Production and Distribution

Production and distribution involve the marketing and sale of

Production and Distribution

Classification of agents

Independent agents can represent more than one

Production and Distribution

Classification of agents

Independent agents can represent more than one

Production and Distribution

Other production/distribution services performed by insurers include activities related

Production and Distribution

Other production/distribution services performed by insurers include activities related

Underwriting

The underwriting function entails the risk assessment, classification and selection of

Underwriting

The underwriting function entails the risk assessment, classification and selection of

Underwriting

Several principles guide proper underwriting:

selection according to standards;

proper balance

Underwriting

Several principles guide proper underwriting:

selection according to standards;

proper balance

Underwriting

The balancing of risks within classifications is aimed at avoiding adverse

Underwriting

The balancing of risks within classifications is aimed at avoiding adverse

Underwriting

It is important that insureds are treated fairly from the pricing

Underwriting

It is important that insureds are treated fairly from the pricing

Loss Settlement

The objective of loss settlement is to pay claims or

Loss Settlement

The objective of loss settlement is to pay claims or

Loss Settlement

There are several steps in the settlement process.

First, the

Loss Settlement

There are several steps in the settlement process.

First, the

Investment

The reserves that insurers hold for unearned premiums, unpaid losses or

Investment

The reserves that insurers hold for unearned premiums, unpaid losses or

Investment

Because of their fiduciary responsibilities and the market’s valuation of their

Investment

Because of their fiduciary responsibilities and the market’s valuation of their

The Essence of Reinsurance

Reinsurance refers to the shifting of part or

The Essence of Reinsurance

Reinsurance refers to the shifting of part or

The Essence of Reinsurance

In reinsurance, primary insurer who wants to shift

The Essence of Reinsurance

In reinsurance, primary insurer who wants to shift

Концептуальні основи комп'ютерних інформаційних систем в аудиті

Концептуальні основи комп'ютерних інформаційних систем в аудиті Облигации. История возникновения облигации

Облигации. История возникновения облигации Валютный контроль

Валютный контроль Қазіргі коммерциялық банктер

Қазіргі коммерциялық банктер Основы экономики. Задачи государства. Государственный бюджет

Основы экономики. Задачи государства. Государственный бюджет Банкротство предприятия: основные определения и порядок оценки вероятности. (тема 15)

Банкротство предприятия: основные определения и порядок оценки вероятности. (тема 15) Финансовая безопасность. (Тема 3)

Финансовая безопасность. (Тема 3) Финансовые ресурсы компании, их состав и содержание

Финансовые ресурсы компании, их состав и содержание Методы оценки коммерческой эффективности инвестиционных проектов

Методы оценки коммерческой эффективности инвестиционных проектов Страховий ринок США

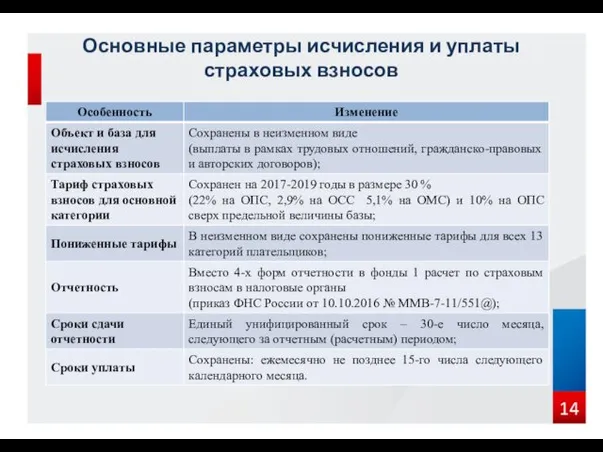

Страховий ринок США Страховые взносы

Страховые взносы Исламдық бағалы қағаздар нарығы

Исламдық бағалы қағаздар нарығы Государственные финансы. Государственные внебюджетные фонды

Государственные финансы. Государственные внебюджетные фонды История бухгалтерского учета

История бухгалтерского учета Финансирование инновационного предпринимательства

Финансирование инновационного предпринимательства State Support Shipbuilding in Ukraine

State Support Shipbuilding in Ukraine Структура и содержание внешнеторгового контракта

Структура и содержание внешнеторгового контракта Споживче кредитування

Споживче кредитування Карта вместо денег

Карта вместо денег Бухгалтерская (финансовая) отчетность

Бухгалтерская (финансовая) отчетность Общая характеристика хозяйственного учета

Общая характеристика хозяйственного учета Зарубіжний досвід забезпечення безпеки банківської діяльності

Зарубіжний досвід забезпечення безпеки банківської діяльності Личное финансовое планирование

Личное финансовое планирование Состав и характеристика источников финансирования

Состав и характеристика источников финансирования Суды о необоснованной налоговой выгоде

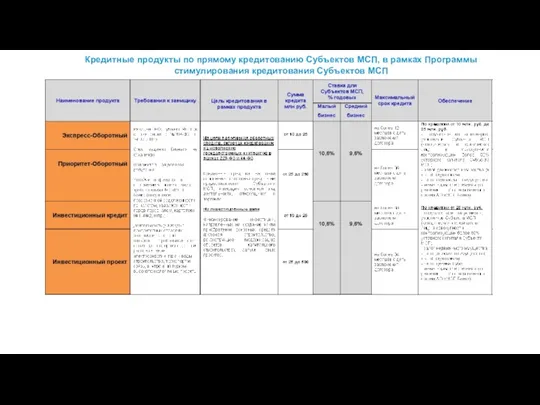

Суды о необоснованной налоговой выгоде Таблицы по продуктам МСП Банка

Таблицы по продуктам МСП Банка Анализ безубыточности

Анализ безубыточности Прогноз бюджета муниципального района Стерлитамакский район Республики Башкортостан на 2017 год и на период 2018 и 2019 годов

Прогноз бюджета муниципального района Стерлитамакский район Республики Башкортостан на 2017 год и на период 2018 и 2019 годов