- State Support Shipbuilding in Ukraine

Содержание

- 2. 1. Prerequisites for the development of shipbuilding in Ukraine 3 2. A Brief Overview Of The

- 3. 1. Prerequisites for the development of shipbuilding in Ukraine

- 4. Access to the largest navigable rivers in Eastern Europe (Dnieper and Danube), as well as access

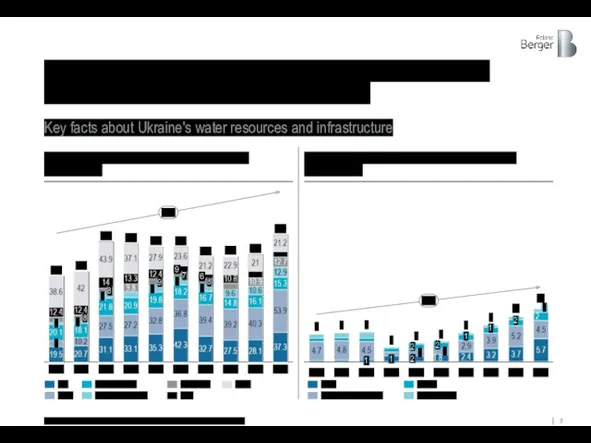

- 5. Ukraine has rich water resources, developed sea and river port infrastructure Key facts about Ukraine's water

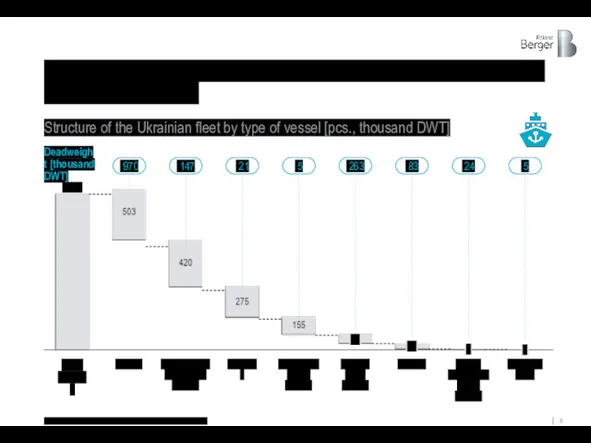

- 6. Modern Ukrainian companies have a developed fleet of commercial and auxiliary vessels Source: Register Book of

- 7. The country has 10 large and medium-sized shipyards capable of building and repairing a wide range

- 8. The country is increasing export cargo turnover through port infrastructure and waterborne transportation Key facts about

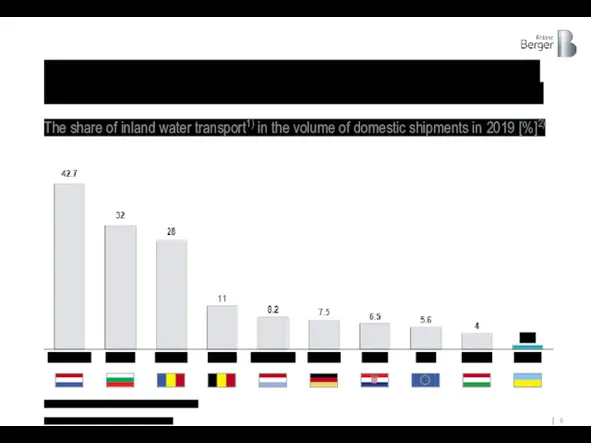

- 9. And in comparison in freight transport with other countries, Ukraine has a great potential for the

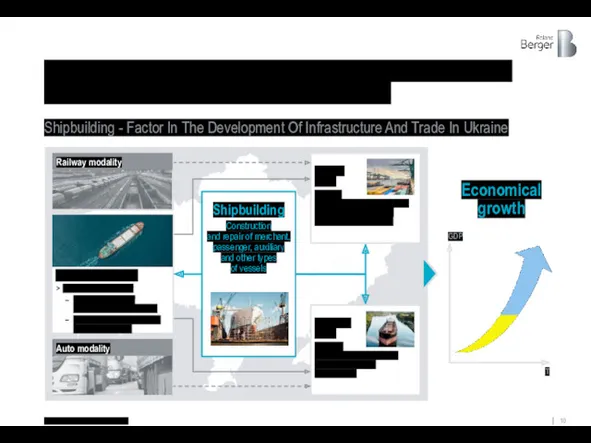

- 10. Further development of shipbuilding can be one of the pillars of support for sustainable economic development

- 11. 2. A Brief Overview Of The Reasons For The Development And Support Of The Shipbuilding Industry

- 12. Reason groups Description, examples Applicability to Ukraine Strategic Ensuring the independence of transport, food, energy and

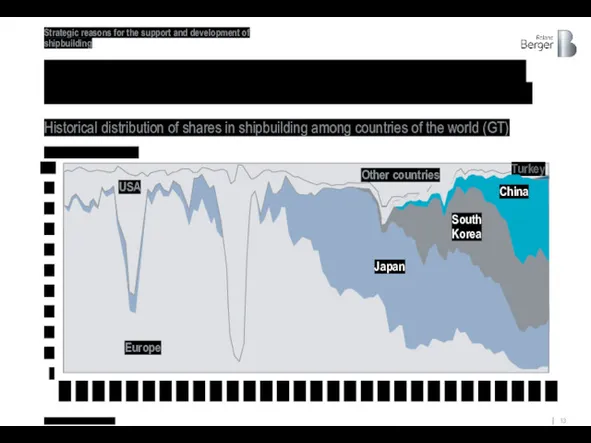

- 13. For example, despite the fact that in recent years Asian countries have begun to play a

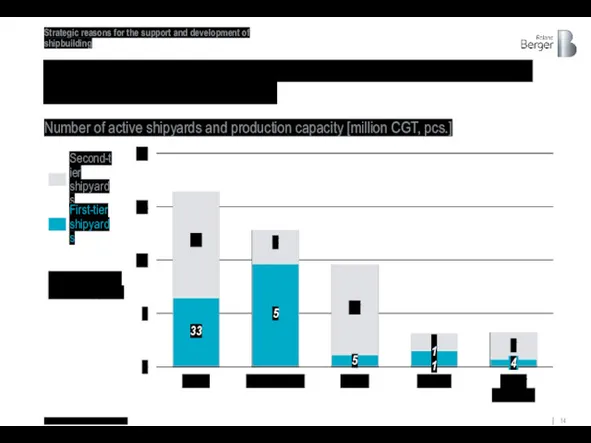

- 14. ХХ – number of active shipyards ... European countries retain production capacity in shipbuilding to ensure

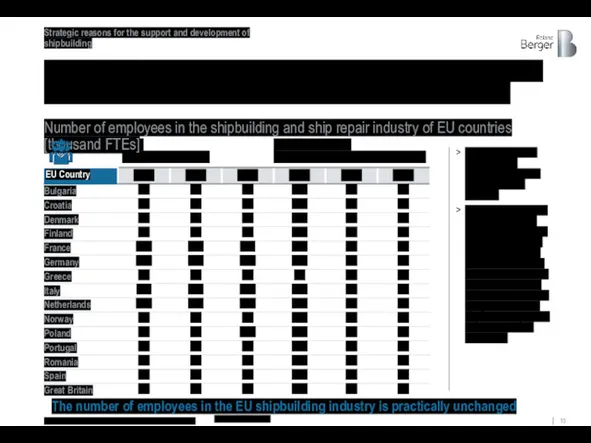

- 15. The number of employees in the shipbuilding industry of the largest EU countries remains practically unchanged

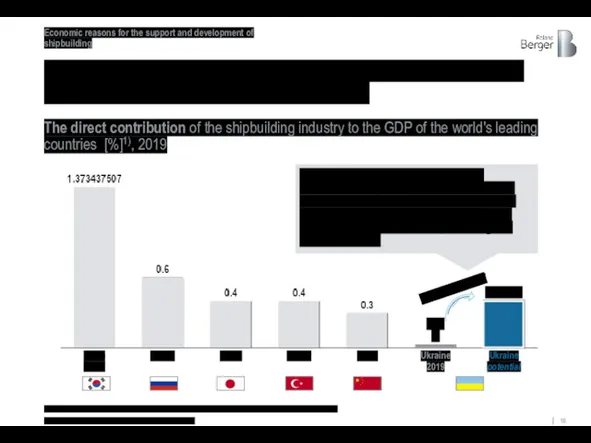

- 16. Turkey Russia South Korea Japan China Ukraine 2019 Ukraine potential 0.03% 0.3-0.6% The potential direct contribution

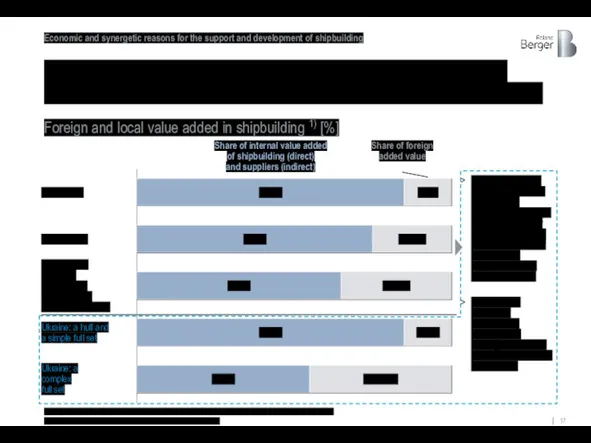

- 17. With a systematic approach to the development of the supplier industry, more than 85% of the

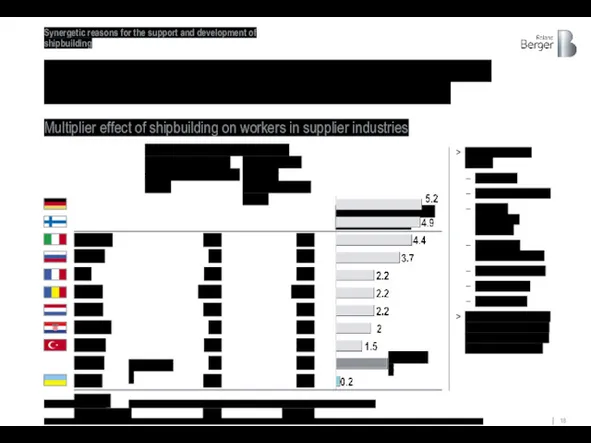

- 18. from 2 to 5 And the multiplicative effect of shipbuilding on the number of employees in

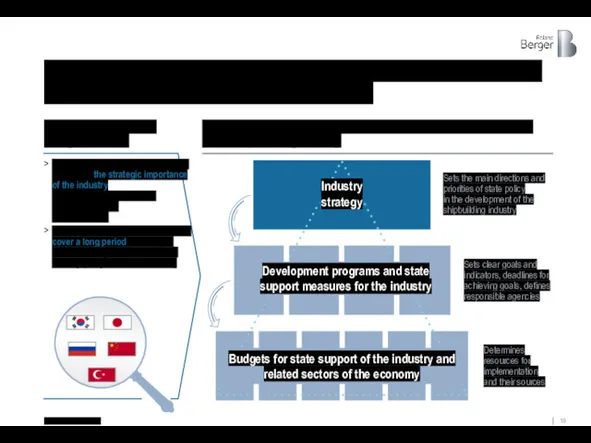

- 19. Sets clear goals and indicators, deadlines for achieving goals, defines responsible agencies Leading countries in shipbuilding

- 20. And the existence of long-term national support programs is a key factor in the development of

- 21. Reference Materials On Leading Countries In Shipbuilding

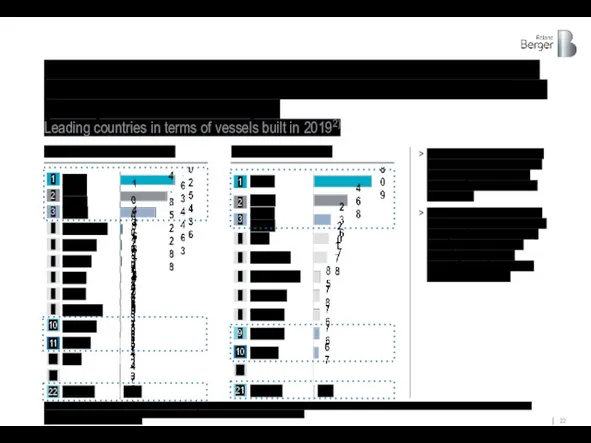

- 22. China, South Korea and Japan are in the world's top three in terms of total DWT

- 23. All leading countries have shipbuilding strategies to improve the competitiveness of shipyards Source: Roland Berger, OECD,

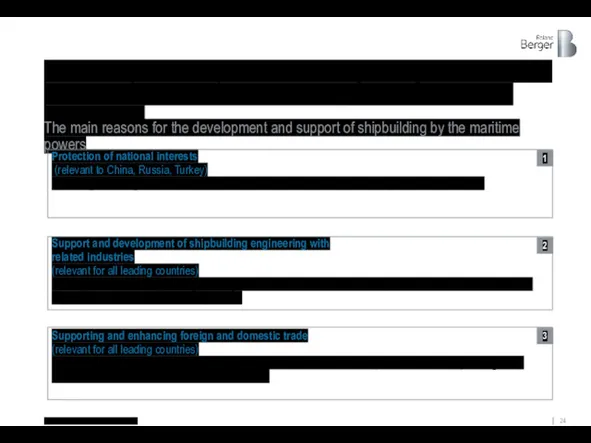

- 24. This industry is a priority for all shipbuilding leading countries since it protects national interests and

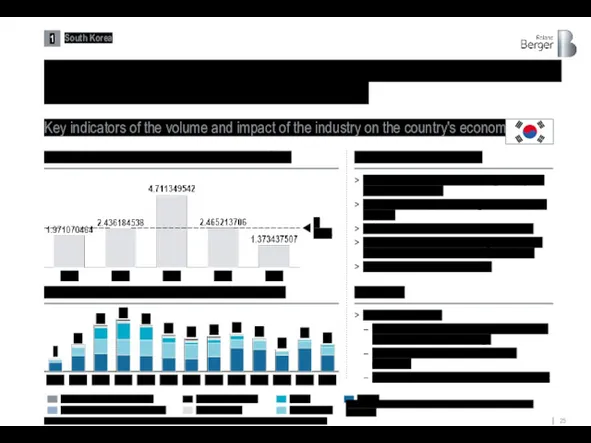

- 25. In South Korea, for example, shipbuilding is a strategic industry with a significant contribution to the

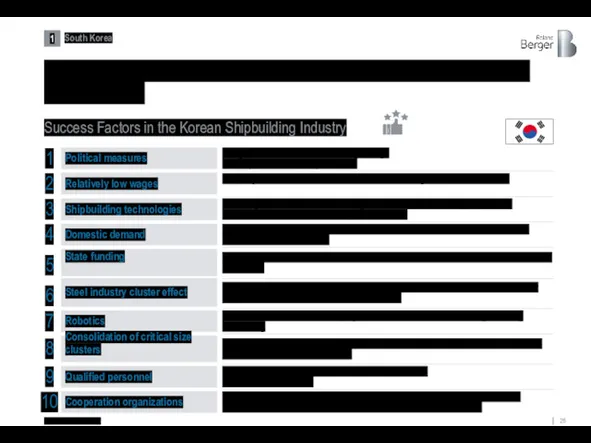

- 26. Many factors contribute to the success of Korean shipyards in the global market Success Factors in

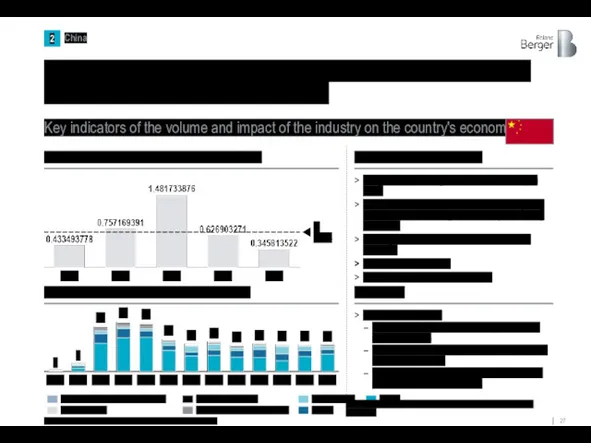

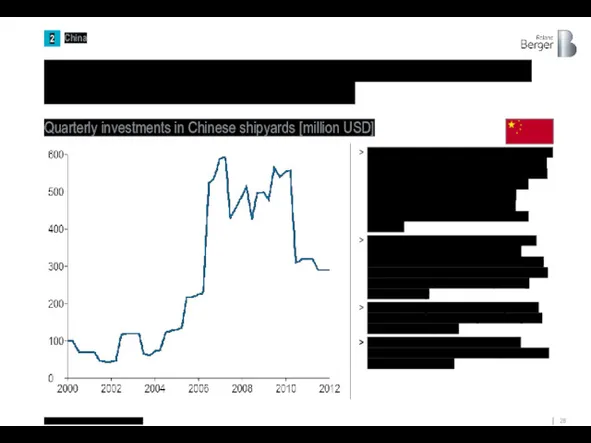

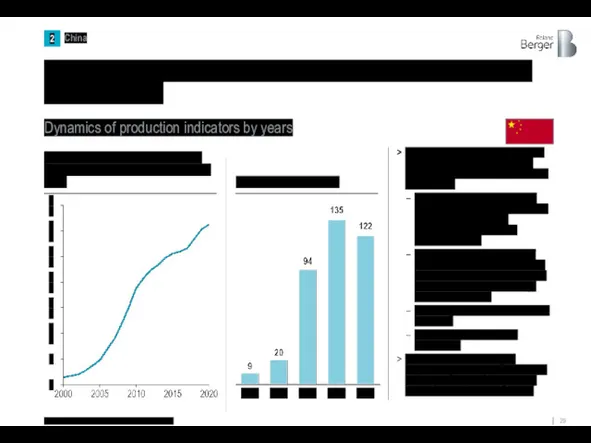

- 27. Since 2010, China, along with South Korea, has secured its place among the world's largest shipbuilders

- 28. Source: NBS, Total quarterly investment Quarterly investments in Chinese shipyards [million USD] The growth of entry

- 29. Rapid growth in production capacity has in turn supported China's trade expansion 30 0 20 15

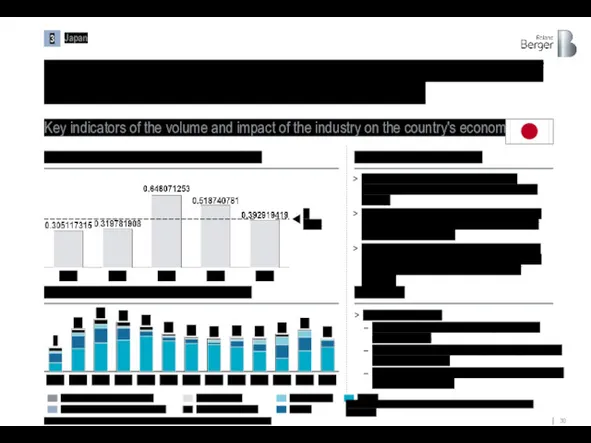

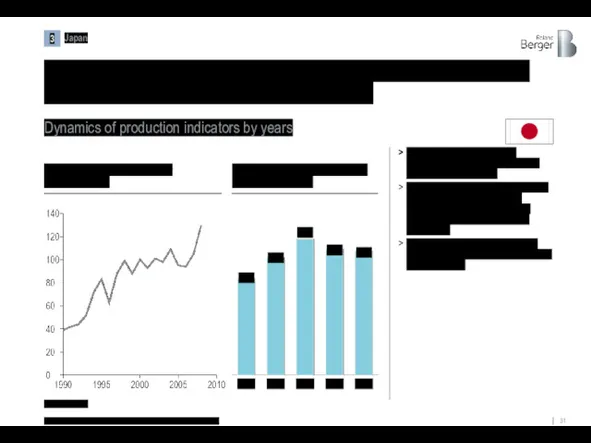

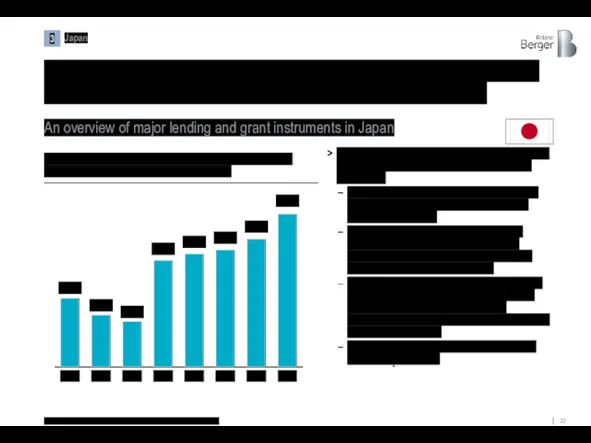

- 30. Thanks to the industry's stable support, Japan has remained one of the most powerful shipbuilding powers

- 31. By supporting R&D in the industry, the Japanese government has ensured a significant increase in productivity

- 32. The Japanese government has introduced a set of credit and grant instruments for the development of

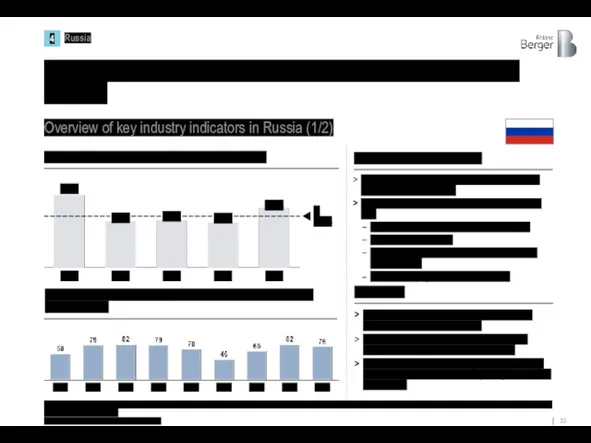

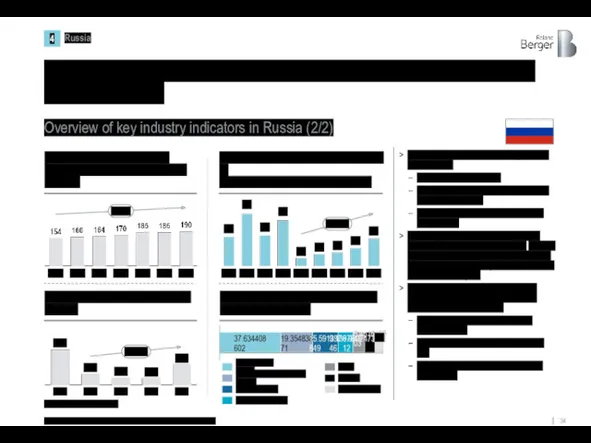

- 33. Shipbuilding is one of the strategic industries of Russia in recent decades Key measures and initiatives

- 34. Today, the industry includes 180 active shipyards employing about 190,000 people. Overview of key industry indicators

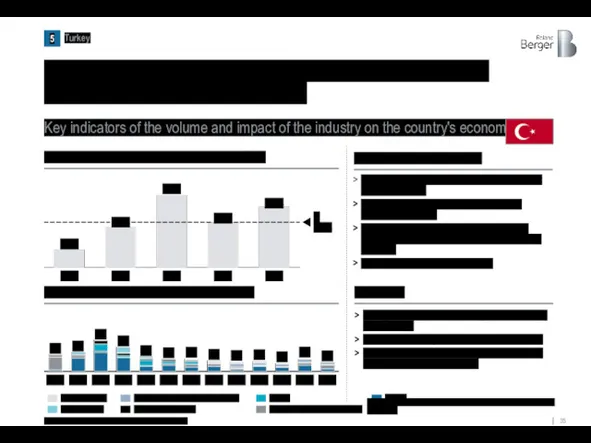

- 35. Since 2000, Turkey has been systematically developing and supporting the shipbuilding industry Key results Turkey was

- 36. Turkey's shipbuilding capacity has almost quadrupled during this period 400 1,600 1,200 200 1,400 600 800

- 37. Also, Turkey was among the leading countries in ship repairs Source: Republic of Turkey - Ministry

- 38. 3. The region market, the potential for Ukraine

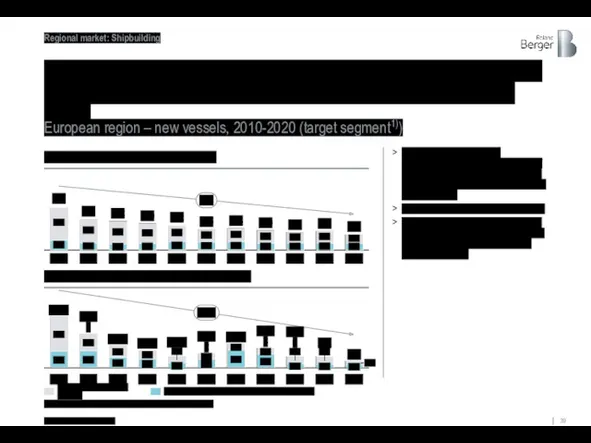

- 39. As the market for new shipbuilding declines, the Black Sea region's contribution to European shipbuilding has

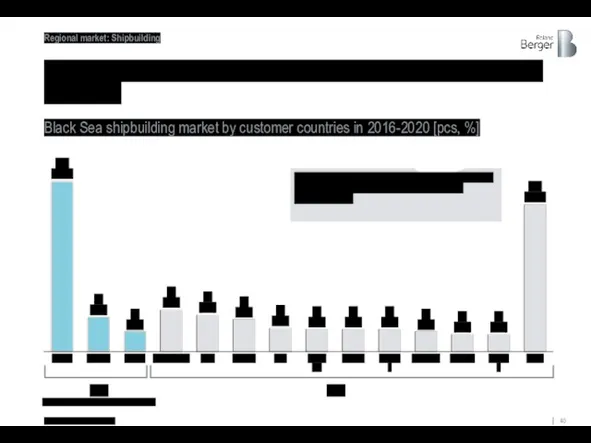

- 40. Most of the orders of the Black Sea region today come from foreign customers Black Sea

- 41. 67 48 Bulk carriers1) Tankers Container ships Other/Special (non-cargo) vessels2) Turkey and Romania have produced significantly

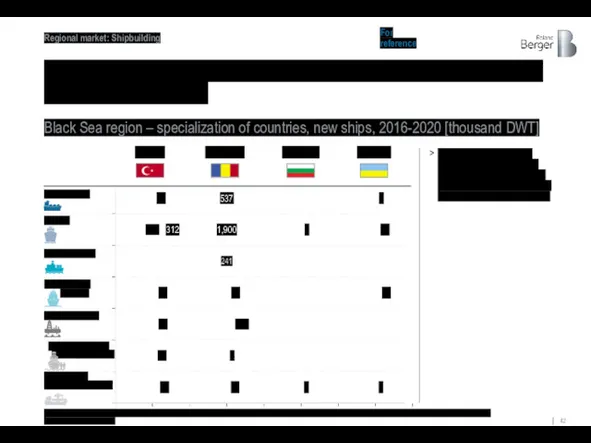

- 42. 3 24 77 11 2 3 6 39 105 37 13 45 241 312 312 1,900

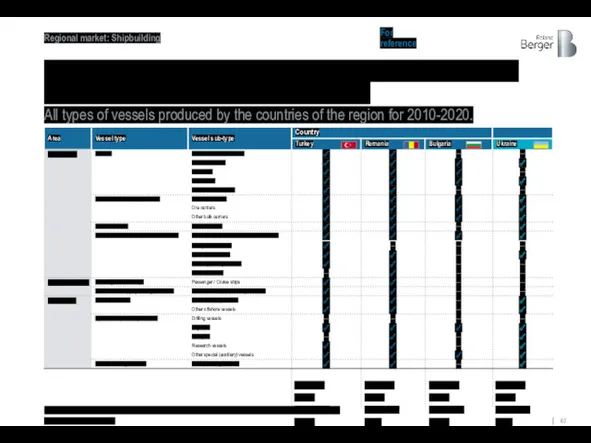

- 43. And all countries in the region, including Ukraine, are capable of producing a very wide range

- 44. The production capacity of Ukrainian shipyards today is ~196 thousand CGT, and the maximum deadweight up

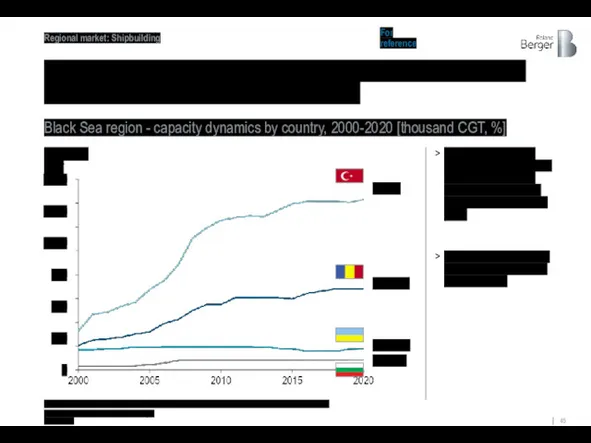

- 45. Since 2000, Turkey has tripled its shipbuilding capacity, Romania and Bulgaria have doubled their capacities Black

- 46. Despite such significant capacity, the Black Sea region is significantly underutilized 13% 19% 1,429 1,429 Romania

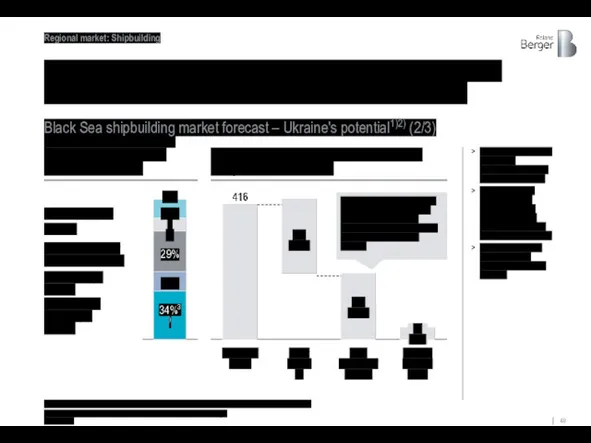

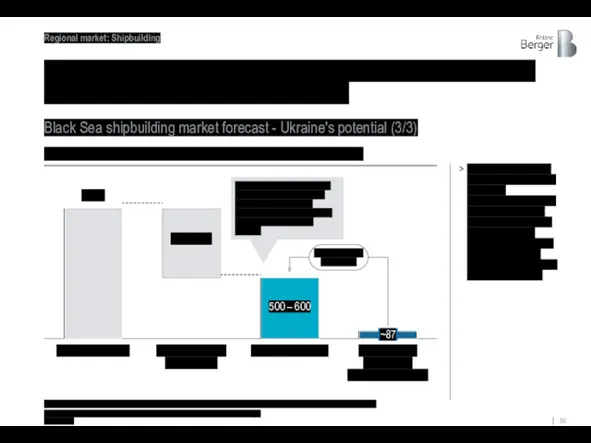

- 47. The forecast volume of construction of new ships in the Black Sea region in terms of

- 48. Ukrainian shipyards are technically able to produce the entire range of vessels under the planned Orderbook

- 49. The production capacity of Ukrainian shipyards approximately corresponds to half of the market of the Black

- 50. Given the available capacity, Ukraine's maximum potential for new construction is $500-600 million per year. 800

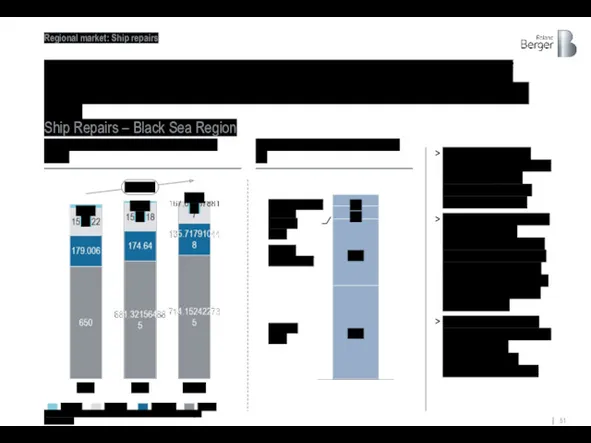

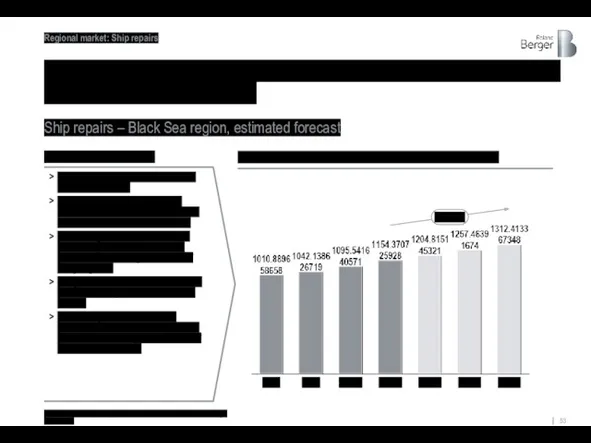

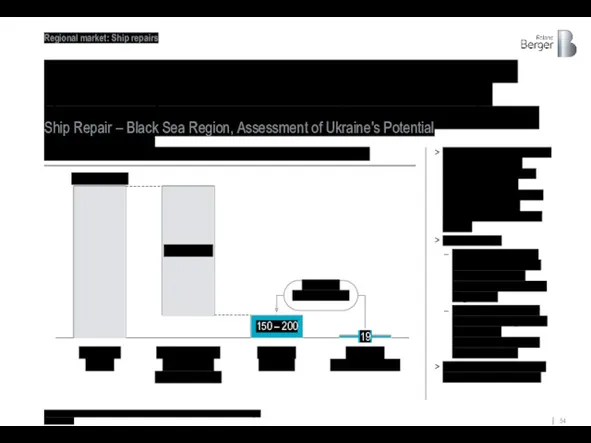

- 51. Ship repair market of the Black Sea region shows the growth of approx. 5% per year,

- 52. Two-thirds of ship repairs in Ukraine are carried out on the facilities of Ilyichevsk Shipyard and

- 53. The ship repair market in the Black Sea region is expected to grow by an average

- 54. Due to the factor of remoteness, as well as the fact that only the Ilyichevsk Shipyard

- 56. Скачать презентацию

1. Prerequisites for the development of shipbuilding in Ukraine 3

2. A Brief Overview Of

1. Prerequisites for the development of shipbuilding in Ukraine 3

2. A Brief Overview Of

1. Prerequisites for the development of shipbuilding in Ukraine

1. Prerequisites for the development of shipbuilding in Ukraine

Access to the largest navigable rivers in Eastern Europe

(Dnieper and

Access to the largest navigable rivers in Eastern Europe (Dnieper and

Ukraine has rich water resources, developed sea and river port infrastructure

Key

Ukraine has rich water resources, developed sea and river port infrastructure

Key

Modern Ukrainian companies have a developed fleet of commercial and auxiliary

Modern Ukrainian companies have a developed fleet of commercial and auxiliary

The country has 10 large and medium-sized shipyards capable of building

The country has 10 large and medium-sized shipyards capable of building

The country is increasing export cargo turnover through port infrastructure and

The country is increasing export cargo turnover through port infrastructure and

And in comparison in freight transport with other countries, Ukraine has

And in comparison in freight transport with other countries, Ukraine has

Further development of shipbuilding can be one of the pillars of

Further development of shipbuilding can be one of the pillars of

2. A Brief Overview Of The Reasons For The Development And Support

2. A Brief Overview Of The Reasons For The Development And Support

Reason groups

Description, examples

Applicability

to Ukraine

Strategic

Ensuring the independence of transport, food, energy

Reason groups

Description, examples

Applicability

to Ukraine

Strategic

Ensuring the independence of transport, food, energy

For example, despite the fact that in recent years Asian countries

For example, despite the fact that in recent years Asian countries

ХХ – number of active shipyards

... European countries retain production capacity

ХХ – number of active shipyards

... European countries retain production capacity

The number of employees in the shipbuilding industry of the largest

The number of employees in the shipbuilding industry of the largest

Turkey

Russia

South Korea

Japan

China

Ukraine

2019

Ukraine

potential

0.03%

0.3-0.6%

The potential direct contribution of shipbuilding to the GDP

Turkey

Russia

South Korea

Japan

China

Ukraine

2019

Ukraine

potential

0.03%

0.3-0.6%

The potential direct contribution of shipbuilding to the GDP

With a systematic approach to the development of the supplier industry,

With a systematic approach to the development of the supplier industry,

from 2 to 5

And the multiplicative effect of shipbuilding on the

from 2 to 5

And the multiplicative effect of shipbuilding on the

Sets clear goals and indicators, deadlines for achieving goals, defines responsible

Sets clear goals and indicators, deadlines for achieving goals, defines responsible

And the existence of long-term national support programs is a key

And the existence of long-term national support programs is a key

Reference Materials On Leading Countries In Shipbuilding

Reference Materials On Leading Countries In Shipbuilding

China, South Korea and Japan are in the world's top three

China, South Korea and Japan are in the world's top three

All leading countries have shipbuilding strategies to improve the competitiveness of

All leading countries have shipbuilding strategies to improve the competitiveness of

This industry is a priority for all shipbuilding leading countries since

This industry is a priority for all shipbuilding leading countries since

In South Korea, for example, shipbuilding is a strategic industry with

In South Korea, for example, shipbuilding is a strategic industry with

Many factors contribute to the success of Korean shipyards in the

Many factors contribute to the success of Korean shipyards in the

Since 2010, China, along with South Korea, has secured its place

Since 2010, China, along with South Korea, has secured its place

Source: NBS, Total quarterly investment

Quarterly investments in Chinese shipyards [million USD]

The

Source: NBS, Total quarterly investment

Quarterly investments in Chinese shipyards [million USD]

The

Rapid growth in production capacity has in turn supported China's trade

Rapid growth in production capacity has in turn supported China's trade

Thanks to the industry's stable support, Japan has remained one of

Thanks to the industry's stable support, Japan has remained one of

By supporting R&D in the industry, the Japanese government has ensured

By supporting R&D in the industry, the Japanese government has ensured

The Japanese government has introduced a set of credit and grant

The Japanese government has introduced a set of credit and grant

Shipbuilding is one of the strategic industries of Russia in recent

Shipbuilding is one of the strategic industries of Russia in recent

Today, the industry includes 180 active shipyards employing about 190,000 people.

Overview

Today, the industry includes 180 active shipyards employing about 190,000 people.

Overview

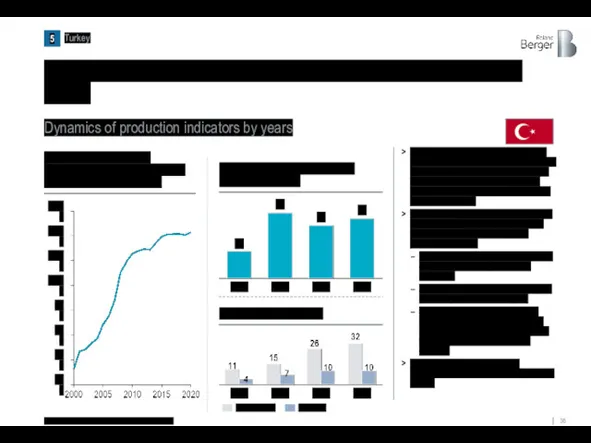

Since 2000, Turkey has been systematically developing and supporting the shipbuilding

Since 2000, Turkey has been systematically developing and supporting the shipbuilding

Turkey's shipbuilding capacity has almost quadrupled during this period

400

1,600

1,200

200

1,400

600

800

1,000

2003

2008

34

2019

2017

28

14

31

Dynamics of production

Turkey's shipbuilding capacity has almost quadrupled during this period

400

1,600

1,200

200

1,400

600

800

1,000

2003

2008

34

2019

2017

28

14

31

Dynamics of production

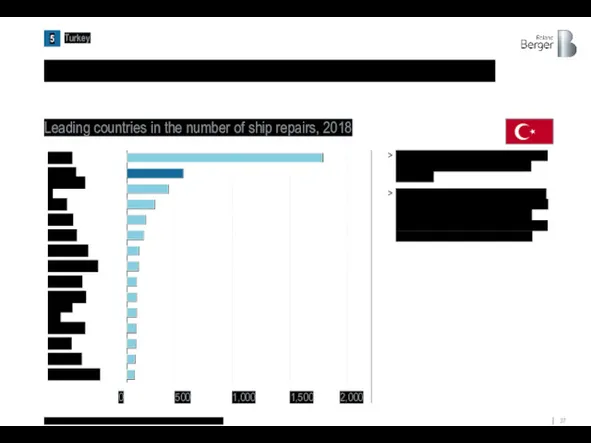

Also, Turkey was among the leading countries in ship repairs

Source: Republic

Also, Turkey was among the leading countries in ship repairs

Source: Republic

3. The region market, the potential for

Ukraine

3. The region market, the potential for

Ukraine

As the market for new shipbuilding declines, the Black Sea region's

As the market for new shipbuilding declines, the Black Sea region's

Most of the orders of the Black Sea region today come

Most of the orders of the Black Sea region today come

67

48

Bulk carriers1)

Tankers

Container ships

Other/Special (non-cargo) vessels2)

Turkey and Romania have produced significantly larger

67

48

Bulk carriers1)

Tankers

Container ships

Other/Special (non-cargo) vessels2)

Turkey and Romania have produced significantly larger

3

24

77

11

2

3

6

39

105

37

13

45

241

312

312

1,900

5

22

12

537

Turkey and Romania have produced significantly larger volumes over the past

3

24

77

11

2

3

6

39

105

37

13

45

241

312

312

1,900

5

22

12

537

Turkey and Romania have produced significantly larger volumes over the past

And all countries in the region, including Ukraine, are capable of

And all countries in the region, including Ukraine, are capable of

The production capacity of Ukrainian shipyards today is ~196 thousand CGT,

The production capacity of Ukrainian shipyards today is ~196 thousand CGT,

Since 2000, Turkey has tripled its shipbuilding capacity, Romania and Bulgaria

Since 2000, Turkey has tripled its shipbuilding capacity, Romania and Bulgaria

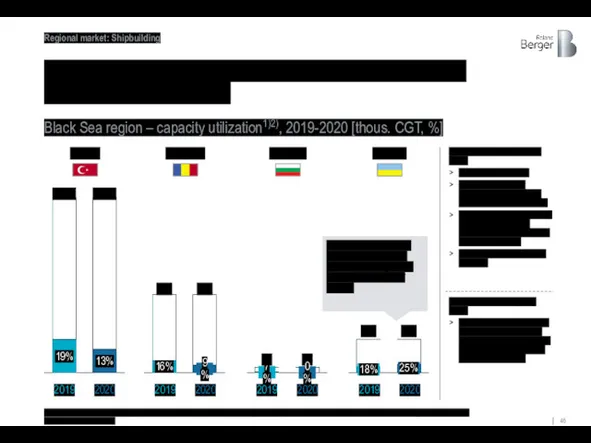

Despite such significant capacity, the Black Sea region is significantly underutilized

13%

19%

1,429

1,429

Romania

Turkey

Bulgaria

Ukraine

18%

25%

196

196

16%

9%

717

717

85

7%

0%

85

Approach

Despite such significant capacity, the Black Sea region is significantly underutilized

13%

19%

1,429

1,429

Romania

Turkey

Bulgaria

Ukraine

18%

25%

196

196

16%

9%

717

717

85

7%

0%

85

Approach

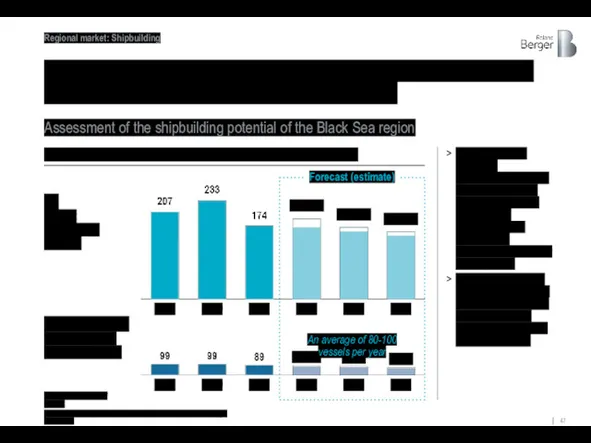

The forecast volume of construction of new ships in the Black

The forecast volume of construction of new ships in the Black

Ukrainian shipyards are technically able to produce the entire range of

Ukrainian shipyards are technically able to produce the entire range of

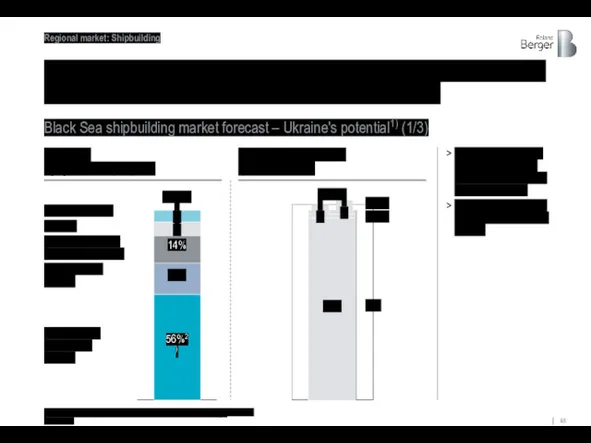

The production capacity of Ukrainian shipyards approximately corresponds to half of

The production capacity of Ukrainian shipyards approximately corresponds to half of

Given the available capacity, Ukraine's maximum potential for new construction is

Given the available capacity, Ukraine's maximum potential for new construction is

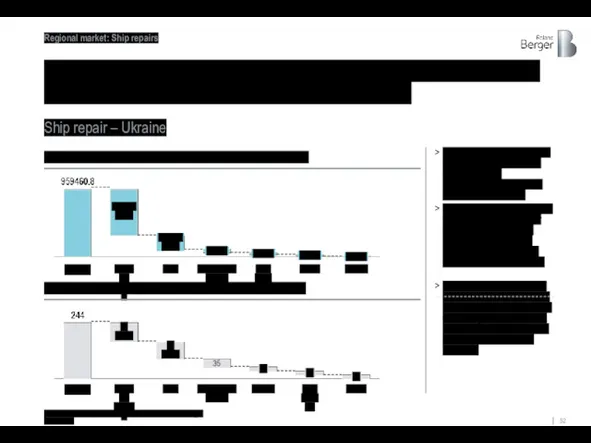

Ship repair market of the Black Sea region shows the growth

Ship repair market of the Black Sea region shows the growth

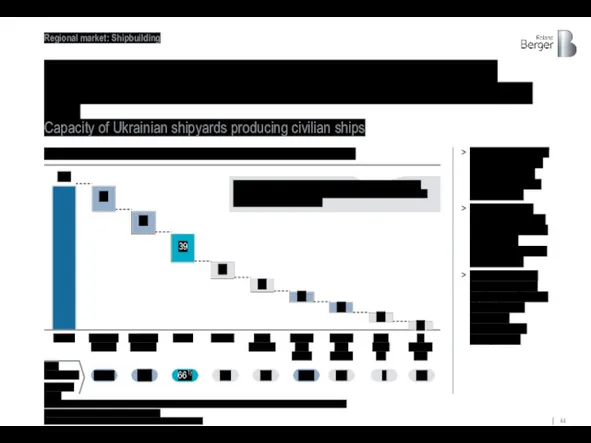

Two-thirds of ship repairs in Ukraine are carried out on the

Two-thirds of ship repairs in Ukraine are carried out on the

The ship repair market in the Black Sea region is expected

The ship repair market in the Black Sea region is expected

Due to the factor of remoteness, as well as the fact

Due to the factor of remoteness, as well as the fact

Сущность портфеля ценных бумаг и портфельного инвестирования. (Тема 1)

Сущность портфеля ценных бумаг и портфельного инвестирования. (Тема 1) Основы системы ОМС

Основы системы ОМС Ссудный капитал и кредит

Ссудный капитал и кредит Особенности сдачи отчетности за 9 месяцев 2023 года в бюджетной сфере

Особенности сдачи отчетности за 9 месяцев 2023 года в бюджетной сфере Видаткова частина бюджету України

Видаткова частина бюджету України Финансово-правовые нормы, их особенности, виды и структура

Финансово-правовые нормы, их особенности, виды и структура FEEL THE TASTE. Общество с ограниченной ответственностью

FEEL THE TASTE. Общество с ограниченной ответственностью УСН

УСН Изменения в бухгалтерской (финансовой) отчетности за 2018 год

Изменения в бухгалтерской (финансовой) отчетности за 2018 год Школа ЖКХ. Начисление платы за коммунальные ресурсы, расходуемые на общедомовые нужды. Лекция 5

Школа ЖКХ. Начисление платы за коммунальные ресурсы, расходуемые на общедомовые нужды. Лекция 5 Управление личными финансами

Управление личными финансами Специальные режимы налогообложения

Специальные режимы налогообложения Инвестиционная политика предприятия

Инвестиционная политика предприятия Концептуальные основы бухгалтерского учета и отчетности организаций сектора государственного управления

Концептуальные основы бухгалтерского учета и отчетности организаций сектора государственного управления Федеральный фонды обязательного медицинского страхования

Федеральный фонды обязательного медицинского страхования Финансовые меры поддержки для СМСП по муниципальной программе Развитие и поддержка малого и среднего предпринимательства

Финансовые меры поддержки для СМСП по муниципальной программе Развитие и поддержка малого и среднего предпринимательства Учет в строительстве. Понятие строительства, его особенности

Учет в строительстве. Понятие строительства, его особенности Методы учета (калькулирования) затрат

Методы учета (калькулирования) затрат Ко-бренды. Кобрендовые кредитные карты. Банк Тинькофф

Ко-бренды. Кобрендовые кредитные карты. Банк Тинькофф Состав и содержание финансовых ресурсов страховой компании

Состав и содержание финансовых ресурсов страховой компании Ценообразование. Тема 7

Ценообразование. Тема 7 Международные стандарты и нормативы регулирования аудиторской деятельности

Международные стандарты и нормативы регулирования аудиторской деятельности Материнский капитал как социальная защита населения

Материнский капитал как социальная защита населения Медицинское страхование

Медицинское страхование Неделя финансовой грамотности для детей и молодежи. 5-7 класс

Неделя финансовой грамотности для детей и молодежи. 5-7 класс Теория о минимумах и максимумах рынка (дополнение к теории Доу)

Теория о минимумах и максимумах рынка (дополнение к теории Доу) Форма №1. Бухгалтерский баланс

Форма №1. Бухгалтерский баланс РГС Защита здоровья

РГС Защита здоровья