- International financial reporting standards. The structure of IFRS

Содержание

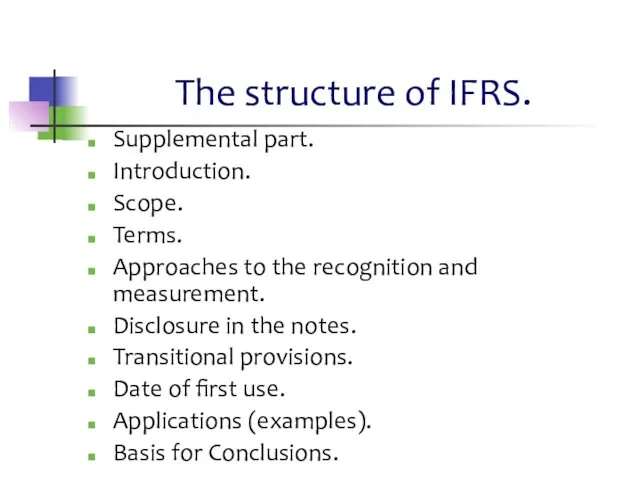

- 2. The structure of IFRS. Supplemental part. Introduction. Scope. Terms. Approaches to the recognition and measurement. Disclosure

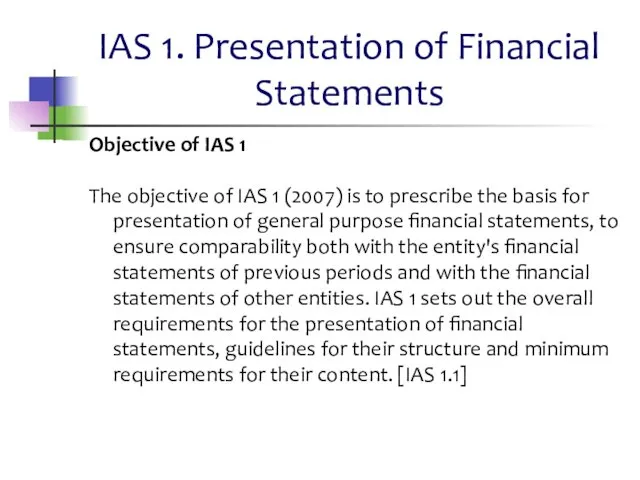

- 3. IAS 1. Presentation of Financial Statements Objective of IAS 1 The objective of IAS 1 (2007)

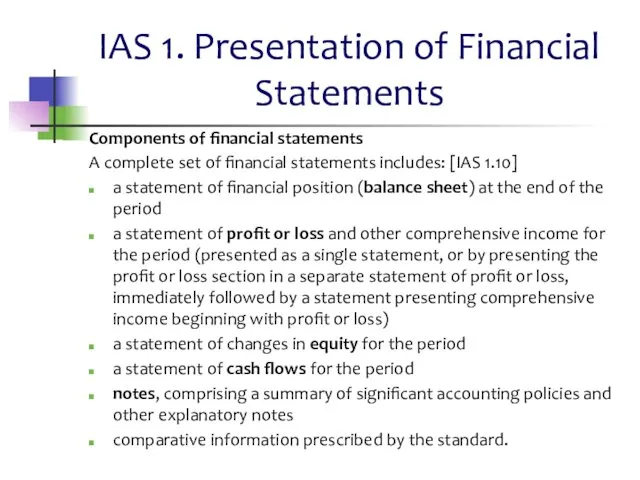

- 4. IAS 1. Presentation of Financial Statements Components of financial statements A complete set of financial statements

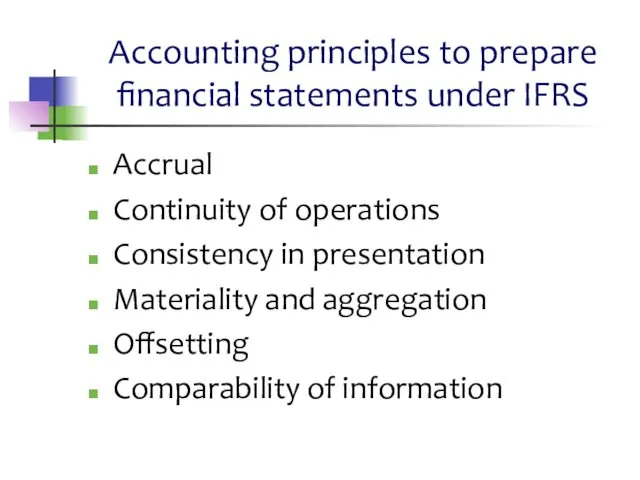

- 5. Accounting principles to prepare financial statements under IFRS Accrual Continuity of operations Consistency in presentation Materiality

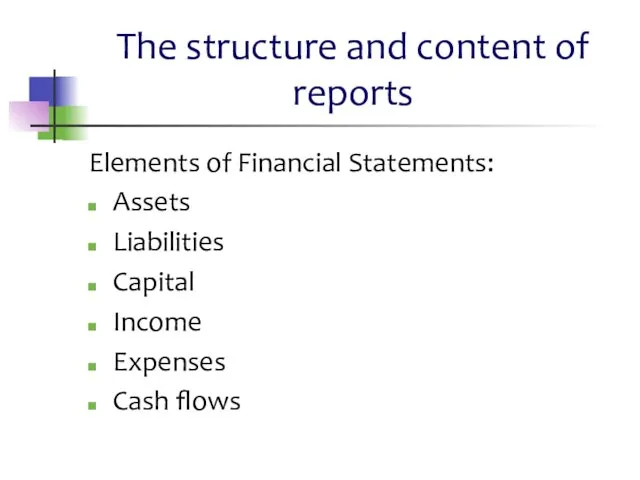

- 6. The structure and content of reports Elements of Financial Statements: Assets Liabilities Capital Income Expenses Cash

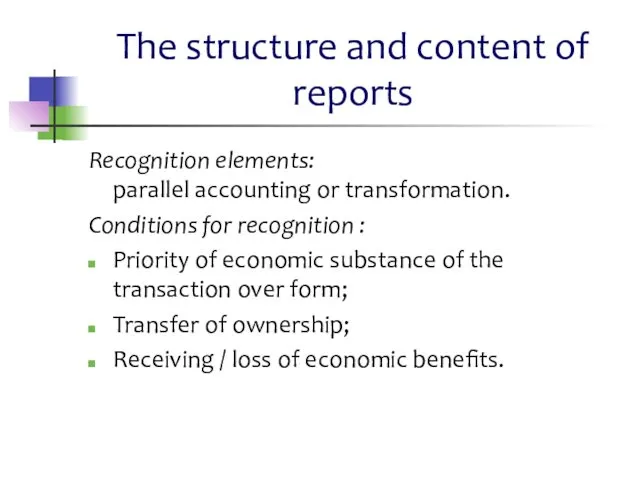

- 7. The structure and content of reports Recognition elements: parallel accounting or transformation. Conditions for recognition :

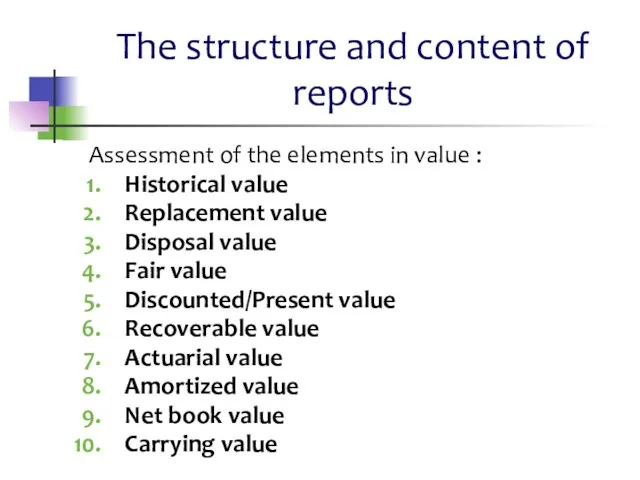

- 8. The structure and content of reports Assessment of the elements in value : Historical value Replacement

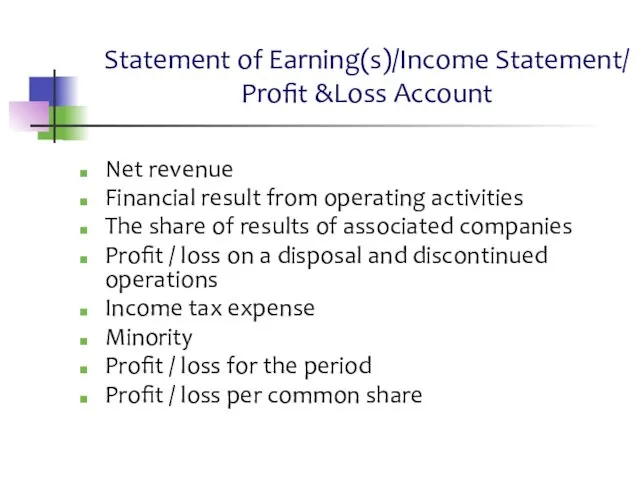

- 9. Statement of Earning(s)/Income Statement/ Profit &Loss Account Net revenue Financial result from operating activities The share

- 11. Скачать презентацию

The structure of IFRS.

Supplemental part.

Introduction.

Scope.

Terms.

Approaches to the

The structure of IFRS.

Supplemental part.

Introduction.

Scope.

Terms.

Approaches to the

IAS 1. Presentation of Financial Statements

Objective of IAS 1

The objective

IAS 1. Presentation of Financial Statements

Objective of IAS 1

The objective

IAS 1. Presentation of Financial Statements

Components of financial statements

A complete

IAS 1. Presentation of Financial Statements

Components of financial statements

A complete

Accounting principles to prepare financial statements under IFRS

Accrual

Continuity of operations

Consistency in

Accounting principles to prepare financial statements under IFRS

Accrual

Continuity of operations

Consistency in

The structure and content of reports

Elements of Financial Statements:

Assets

Liabilities

Capital

Income

Expenses

Cash flows

The structure and content of reports

Elements of Financial Statements:

Assets

Liabilities

Capital

Income

Expenses

Cash flows

The structure and content of reports

Recognition elements:

parallel accounting or transformation.

Conditions

The structure and content of reports

Recognition elements:

parallel accounting or transformation.

Conditions

The structure and content of reports

Assessment of the elements in value

The structure and content of reports

Assessment of the elements in value

Statement of Earning(s)/Income Statement/ Profit &Loss Account

Net revenue

Financial result from operating

Statement of Earning(s)/Income Statement/ Profit &Loss Account

Net revenue

Financial result from operating

1С:Розница 8. Магазин автозапчастей

1С:Розница 8. Магазин автозапчастей Стипендія

Стипендія Сущность прибыли организации

Сущность прибыли организации Экономическая оценка инвестиций в логистических системах. Часть 1

Экономическая оценка инвестиций в логистических системах. Часть 1 Налог на доходы физических лиц

Налог на доходы физических лиц Страхование имущества физических лиц. Страховые риски

Страхование имущества физических лиц. Страховые риски Понятие бюджетной системы

Понятие бюджетной системы Єдиний внесок на загальнообов'язкове державне соціальне страхування

Єдиний внесок на загальнообов'язкове державне соціальне страхування Денежный оборот. Налично-денежные и безналичные расчеты

Денежный оборот. Налично-денежные и безналичные расчеты Изменения в рабочем плане счетов

Изменения в рабочем плане счетов Рухани байлық па? Материалдық байлық па?

Рухани байлық па? Материалдық байлық па? Налоги на прибыль

Налоги на прибыль Upload Ex Business

Upload Ex Business Налоговая система в Японии

Налоговая система в Японии Налоги и налогообложение (ФВМ)

Налоги и налогообложение (ФВМ) Публічний звіт голови державного космічного агентства України

Публічний звіт голови державного космічного агентства України Связь риска с основными финансовыми показателями деятельности предприятия

Связь риска с основными финансовыми показателями деятельности предприятия Ипотека. Партнерские программы

Ипотека. Партнерские программы Финансовый план

Финансовый план Правила оформления авансовых отчетов по командировкам в пределах РФ

Правила оформления авансовых отчетов по командировкам в пределах РФ Домашняя бухгалтерия. Как экономить

Домашняя бухгалтерия. Как экономить Налоговая отчетность за 1 квартал 2020 года

Налоговая отчетность за 1 квартал 2020 года Юридические вопросы, налоги и финансы. Субъекты малого предпринимательства: кто к ним относится в 2018 году

Юридические вопросы, налоги и финансы. Субъекты малого предпринимательства: кто к ним относится в 2018 году Понятие инвестиций. Инвестиции

Понятие инвестиций. Инвестиции Анализ бухгалтерского баланса

Анализ бухгалтерского баланса Государственная поддержка малого бизнеса в России

Государственная поддержка малого бизнеса в России Методика анализа себестоимости продукции

Методика анализа себестоимости продукции Профессия бухгалтер

Профессия бухгалтер