- Role of financial intermediaries Types of financial intermediaries Lecture 2

Содержание

- 2. ©Ella Khromova Market imperfections In order to overcome market imperfections: Differences in preferences of lenders and

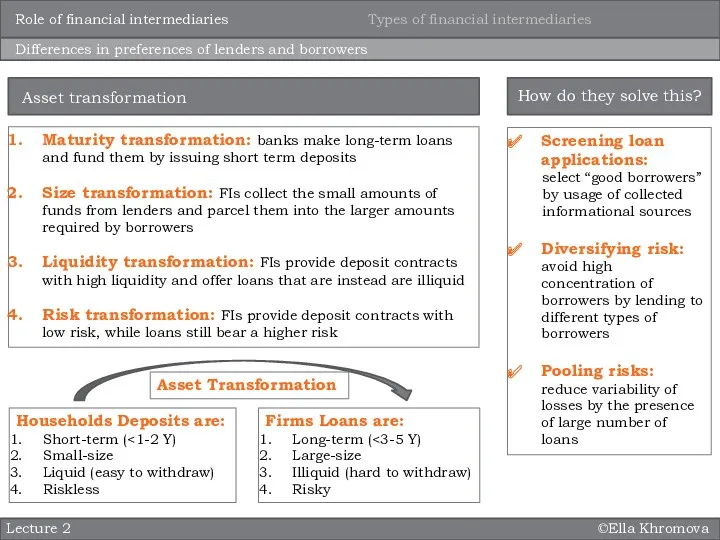

- 3. ©Ella Khromova Lecture 2 Differences in preferences of lenders and borrowers Maturity transformation: banks make long-term

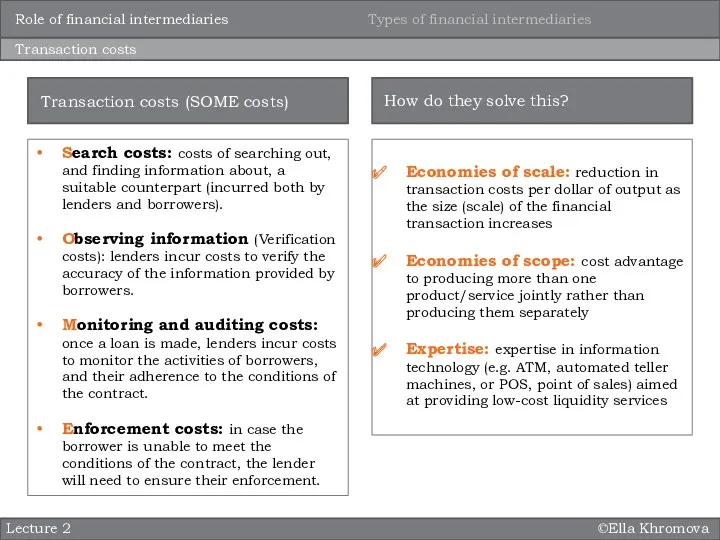

- 4. ©Ella Khromova Lecture 2 Transaction costs Search costs: costs of searching out, and finding information about,

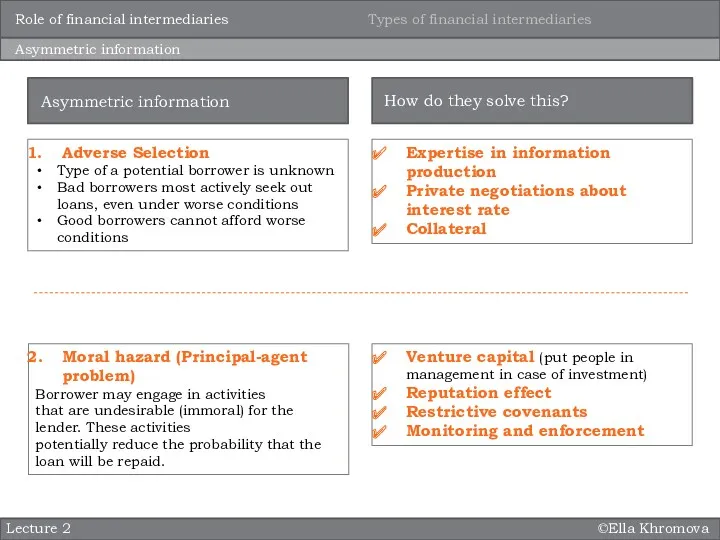

- 5. ©Ella Khromova Lecture 2 Asymmetric information Adverse Selection Type of a potential borrower is unknown Bad

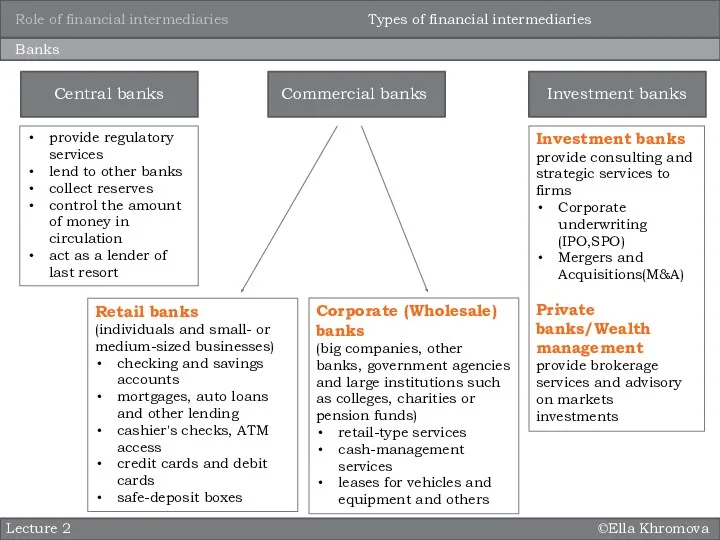

- 6. ©Ella Khromova Lecture 2 Banks Retail banks (individuals and small- or medium-sized businesses) checking and savings

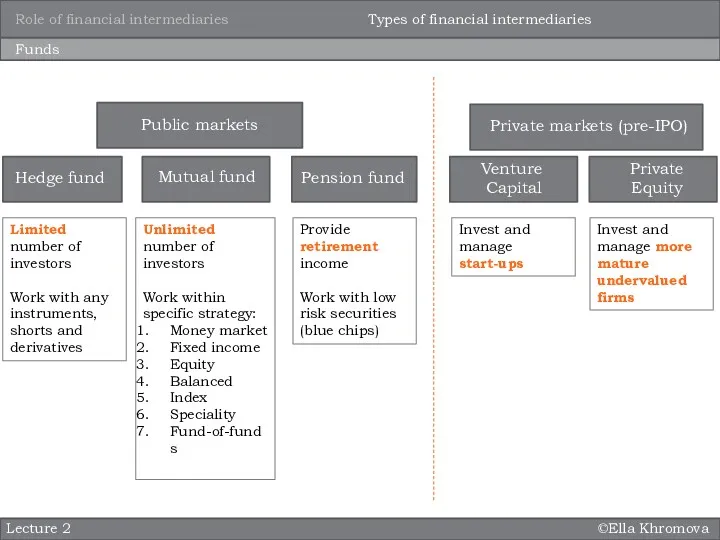

- 7. ©Ella Khromova Lecture 2 Funds Mutual fund Mutual fund Hedge fund Public markets Private markets (pre-IPO)

- 9. Скачать презентацию

©Ella Khromova

Market imperfections

In order to overcome market imperfections:

Differences in preferences of

©Ella Khromova

Market imperfections

In order to overcome market imperfections:

Differences in preferences of

©Ella Khromova

Lecture 2

Differences in preferences of lenders and borrowers

Maturity transformation: banks

©Ella Khromova

Lecture 2

Differences in preferences of lenders and borrowers

Maturity transformation: banks

©Ella Khromova

Lecture 2

Transaction costs

Search costs: costs of searching out, and

©Ella Khromova

Lecture 2

Transaction costs

Search costs: costs of searching out, and

©Ella Khromova

Lecture 2

Asymmetric information

Adverse Selection

Type of a potential borrower is unknown

Bad

©Ella Khromova

Lecture 2

Asymmetric information

Adverse Selection

Type of a potential borrower is unknown

Bad

©Ella Khromova

Lecture 2

Banks

Retail banks

(individuals and small- or medium-sized businesses)

checking and savings

©Ella Khromova

Lecture 2

Banks

Retail banks

(individuals and small- or medium-sized businesses)

checking and savings

©Ella Khromova

Lecture 2

Funds

Mutual fund

Mutual fund

Hedge fund

Public markets

Private markets (pre-IPO)

Pension fund

Pension fund

Role

©Ella Khromova

Lecture 2

Funds

Mutual fund

Mutual fund

Hedge fund

Public markets

Private markets (pre-IPO)

Pension fund

Pension fund

Role

Особливості та механізми оподаткування страхової діяльності в Україні та за кордоном

Особливості та механізми оподаткування страхової діяльності в Україні та за кордоном Финансовые рынки и инструменты

Финансовые рынки и инструменты Этапы бюджетного процесса

Этапы бюджетного процесса Финансовая система Нидерландов

Финансовая система Нидерландов Конкурс рисунка Финансовый мир глазами детей

Конкурс рисунка Финансовый мир глазами детей Регулювання фінансового ринку

Регулювання фінансового ринку Финансовое планирование

Финансовое планирование Счета эскроу

Счета эскроу Қазақстанның зейнетақы

Қазақстанның зейнетақы Выпускная квалификационная работа: Организация безналичных расчетов с использованием пластиковых карт

Выпускная квалификационная работа: Организация безналичных расчетов с использованием пластиковых карт Операції банків в іноземній валюті

Операції банків в іноземній валюті Различие между оценкой бизнеса в России и за рубежом

Различие между оценкой бизнеса в России и за рубежом Функции Центрального хранилища и Межрегиональных хранилищ Банка России

Функции Центрального хранилища и Межрегиональных хранилищ Банка России 1С:Предприятие 8. Использование конфигурации: Бухгалтерия предприятия (пользовательские режимы)

1С:Предприятие 8. Использование конфигурации: Бухгалтерия предприятия (пользовательские режимы) Ежемесячный отчет август 2016

Ежемесячный отчет август 2016 Моніторинг соціально-трудової сфери як інструмент регулювання й удосконалення соціально-трудових відносин

Моніторинг соціально-трудової сфери як інструмент регулювання й удосконалення соціально-трудових відносин Ақшалай талапты беріп қаржыландыру

Ақшалай талапты беріп қаржыландыру Методические основы оценки стоимости производственных объектов предприятия. (Тема 3)

Методические основы оценки стоимости производственных объектов предприятия. (Тема 3) Акцизы при ввозе товара, порядок его установления и применения

Акцизы при ввозе товара, порядок его установления и применения МСП БАНК. Продукты банка

МСП БАНК. Продукты банка Государственный кредит и государственный долг. (Тема 13)

Государственный кредит и государственный долг. (Тема 13) Акцизний податок

Акцизний податок Сутність та види податків

Сутність та види податків Страхование финансовых рисков

Страхование финансовых рисков Управление оборотным капиталом

Управление оборотным капиталом Роль НБУ у регулюванні грошової маси

Роль НБУ у регулюванні грошової маси Финансовая деятельность государства и муниципальных образований

Финансовая деятельность государства и муниципальных образований Коммерческое предложение кредит Бизнес-контракт

Коммерческое предложение кредит Бизнес-контракт