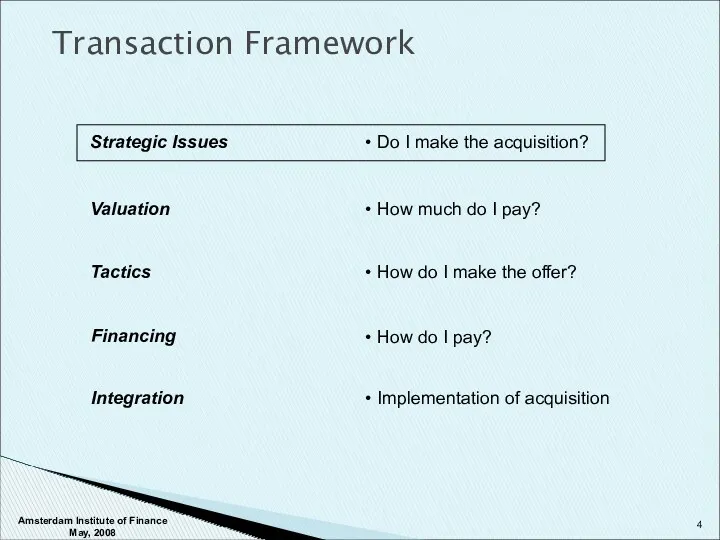

- Structuring. Transaction Framework

Содержание

- 2. Agenda Overview Perspective Creating the structure Covenants Amsterdam Institute of Finance May, 2008

- 3. Overview Amsterdam Institute of Finance May, 2008

- 4. Transaction Framework Strategic Issues Do I make the acquisition? Valuation How much do I pay? Financing

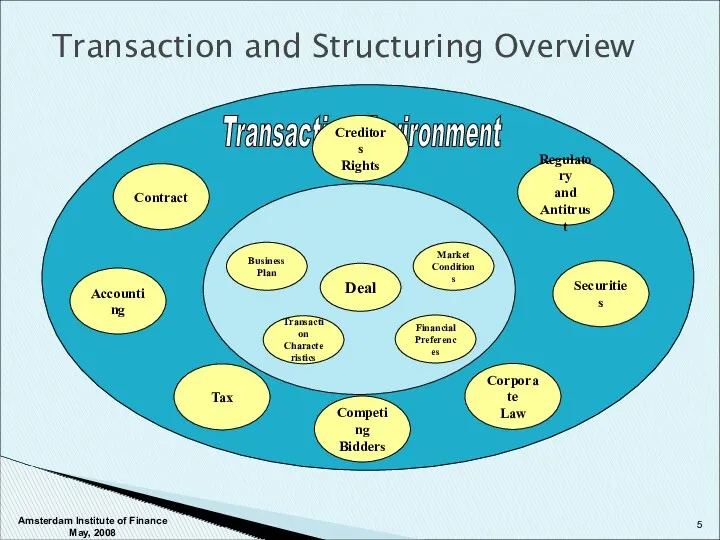

- 5. Transaction and Structuring Overview Accounting Tax Corporate Law Securities Regulatory and Antitrust Transaction Environment Contract Structuring

- 6. Structuring Environment Financial Preferences: Dilution Control Risk Tolerance Flexibility Exit Needs Market Conditions: Depth Pricing Requirements

- 7. Different Menus Bull Market Menu Bear Market Menu As the credit curve shifts, the menu that

- 8. Financing Approaches Left Hand Side Financing Right Hand Side Financing Based on the cash flow of

- 9. Perspective Amsterdam Institute of Finance May, 2008

- 10. Capital Market Specific Factors Credit Specific Factors Customer Objectives Valuation Structuring Perspective Amsterdam Institute of Finance

- 11. Acceptable leverage levels Interest Rate Amortization Acceptable tenor of senior debt Asset coverage Size of issue

- 12. Public Debt vs. Private Debt Relative Value Analysis Domestic vs. International Issuance Fixed vs. Floating Rate

- 13. Amount of available cash flow Reliability of cash flow Credibility of projections Credit Specific Factors Amsterdam

- 14. Issuer Objectives / Impact (1) Amsterdam Institute of Finance May, 2008

- 15. Issuer Objectives / Impact (2) Amsterdam Institute of Finance May, 2008

- 16. Critical Path & Decision Framework Financial Flexibility Target Credit Rating Determine Capital Structure Hedge No Action

- 17. Creating the Structure Amsterdam Institute of Finance May, 2008

- 18. Rule of Thumb Measures Balance Sheet Model Cash Flow Model Detailed Model Matching markets to the

- 19. Deal Financial Arithmetic Amsterdam Institute of Finance May, 2008

- 20. Netherlands LBO Volume by Industry Source: April 2008 EuroStats; www.lcdcomps.com

- 21. Purchase Price Minimum/Maximum Recapitalization Dividend Debt Refinancing Callability Premiums Tax Issues Expenses Other Uses Financing Need

- 22. Revolver Tied to advance against current assets Crossing liens Term Loan A Macro: Ratio of 3-4x

- 23. Current Asset approach Use standard advance rates Accounts Receivable 80% Inventory 60% PP&E 40% Consider the

- 24. Term Loans = Maximum Senior Debt - Revolver Focus is on Free Operating Cash Flow Market

- 25. Typical bank financings as structured as follows: Revolving Credit Term Loan A (amortising) Term Loans B

- 26. Long Term Debt = Max Total Debt - Max Senior Secured Debt Senior unsecured Sub Debt

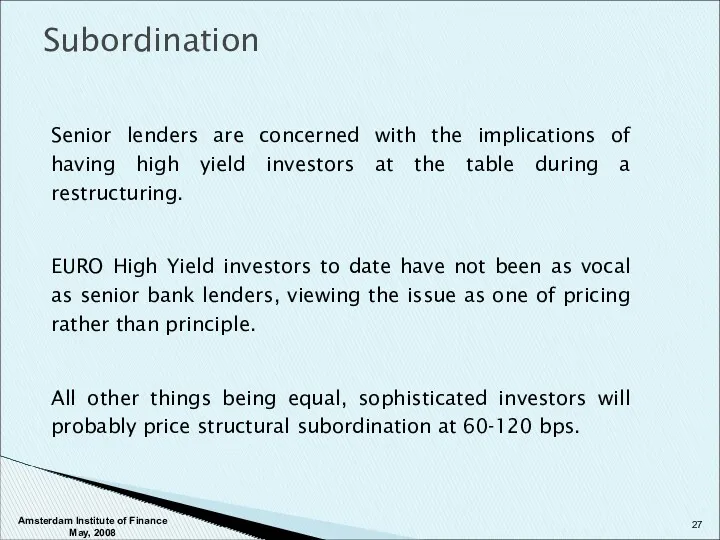

- 27. Subordination Senior lenders are concerned with the implications of having high yield investors at the table

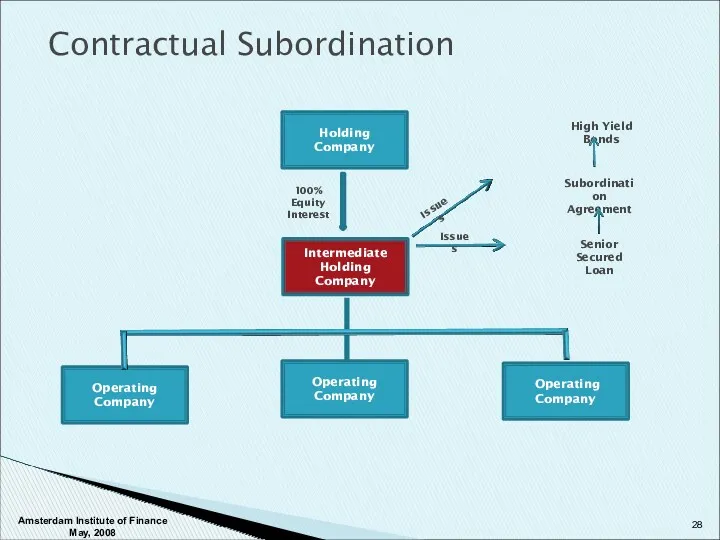

- 28. Contractual Subordination Holding Company Intermediate Holding Company Operating Company Operating Company Operating Company 100% Equity Interest

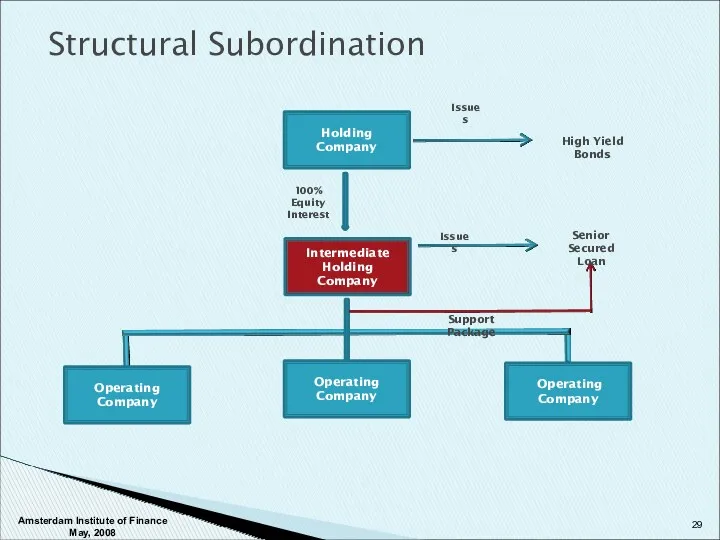

- 29. Structural Subordination Holding Company Intermediate Holding Company Operating Company Operating Company Operating Company 100% Equity Interest

- 30. Retranche Increase Pricing Lower Leverage Lower Purchase Price Seller Paper Increase Equity Senior Notes to cover

- 31. Covenants Amsterdam Institute of Finance May, 2008

- 32. PURPOSE: maintain the original deal WHY Agency problem due to asymmetric information Adverse Selection Moral Hazard

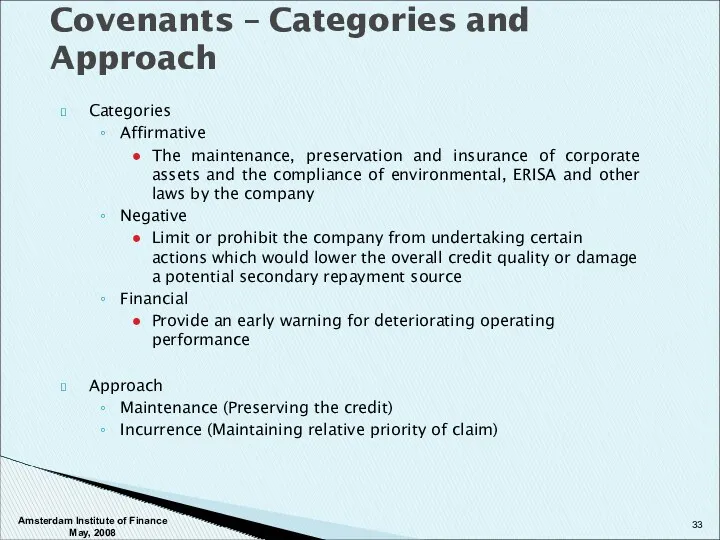

- 33. Categories Affirmative The maintenance, preservation and insurance of corporate assets and the compliance of environmental, ERISA

- 34. There are no standard covenants. They must be tailor fit for each deal and loan structure.

- 35. First-lien leveraged loans covenant statistics: Average number and distribution Excludes covenant-lite deals Amsterdam Institute of Finance

- 36. Amsterdam Institute of Finance May, 2008 Incidence of key covenants in first-lien leveraged loans Excludes covenant-lite

- 37. Amsterdam Institute of Finance May, 2008 Year One Debt/EBITDA Headroom as a Percentage of Covenant Level

- 38. Amsterdam Institute of Finance May, 2008 Percent of First-lien leveraged loans with one maintenance finance covenant

- 39. Average Debt/EBITDA Covenant Level and Projected Ratio for LBOs 1999 – 1Q08 Amsterdam Institute of Finance

- 40. Covenant Levels and Issues Covenants are negotiated between the lender and borrower. Covenant levels will affect

- 41. Translating Capital Structure and Debt Capacity into a Detailed Financing Structure. Conclusion Amsterdam Institute of Finance

- 42. Project Gear Amsterdam Institute of Finance May, 2008

- 43. Project Gear - Facts Potential deal for a company in auction. Private automotive parts company based

- 44. Project Gear - Facts Amsterdam Institute of Finance May, 2008

- 45. Project Gear - Facts Amsterdam Institute of Finance May, 2008

- 46. PMD Stats Amsterdam Institute of Finance May, 2008

- 47. Project Gear - Quick Analysis Amsterdam Institute of Finance May, 2008

- 48. Project Gear - Quick Analysis Amsterdam Institute of Finance May, 2008

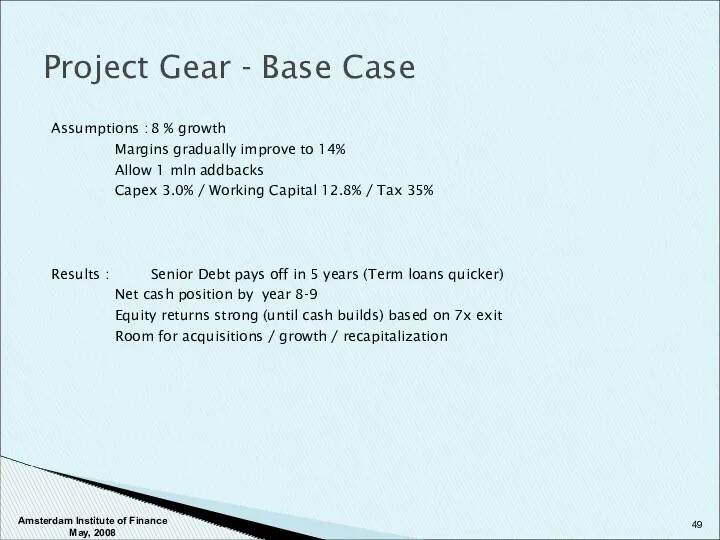

- 49. Project Gear - Base Case Assumptions : 8 % growth Margins gradually improve to 14% Allow

- 50. Project Gear - Base Case Amsterdam Institute of Finance May, 2008

- 51. Project Gear - Downside Assumptions : 0% growth Margins flat (slight decline) to 11% Do not

- 52. Project Gear - Downside Amsterdam Institute of Finance May, 2008

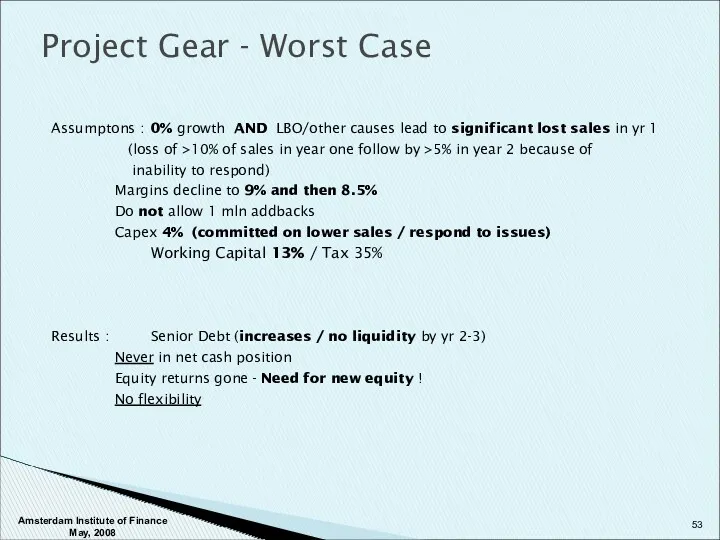

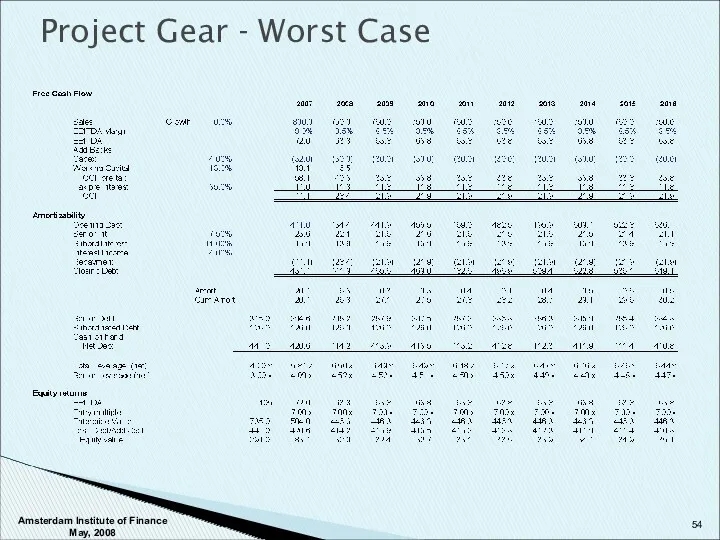

- 53. Project Gear - Worst Case Assumptons : 0% growth AND LBO/other causes lead to significant lost

- 54. Project Gear - Worst Case Amsterdam Institute of Finance May, 2008

- 55. Project Gear - Responses (How & When) Year 2007 - Probably waive with revised management plans

- 57. Скачать презентацию

Agenda

Overview

Perspective

Creating the structure

Covenants

Amsterdam Institute of Finance May, 2008

Agenda

Overview

Perspective

Creating the structure

Covenants

Amsterdam Institute of Finance May, 2008

Overview

Amsterdam Institute of Finance May, 2008

Overview

Amsterdam Institute of Finance May, 2008

Transaction Framework

Strategic Issues

Do I make the acquisition?

Valuation

How much do

Transaction Framework

Strategic Issues

Do I make the acquisition?

Valuation

How much do

Transaction and Structuring Overview

Accounting

Tax

Corporate

Law

Securities

Regulatory

and Antitrust

Transaction Environment

Contract

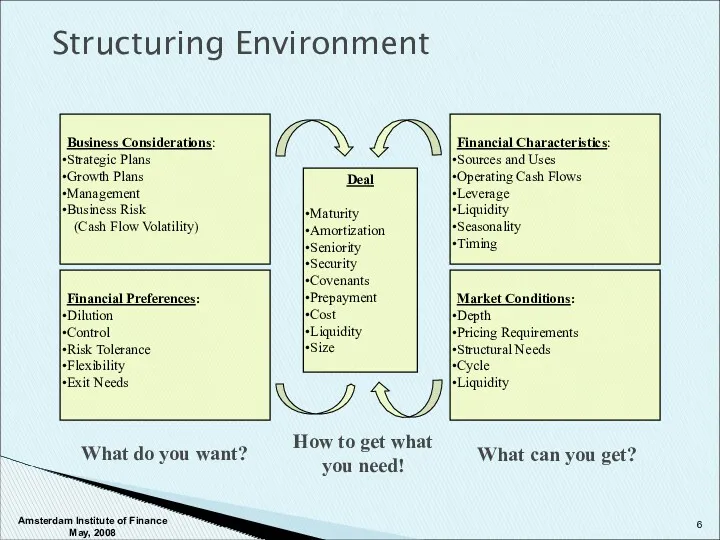

Structuring Environment

Business

Plan

Transaction

Characteristics

Financial

Preferences

Market

Conditions

Deal

Competing

Bidders

Creditors

Rights

Amsterdam Institute

Transaction and Structuring Overview

Accounting

Tax

Corporate

Law

Securities

Regulatory

and Antitrust

Transaction Environment

Contract

Structuring Environment

Business

Plan

Transaction

Characteristics

Financial

Preferences

Market

Conditions

Deal

Competing

Bidders

Creditors

Rights

Amsterdam Institute

Structuring Environment

Financial Preferences:

Dilution

Control

Risk Tolerance

Flexibility

Exit Needs

Market Conditions:

Depth

Pricing Requirements

Structural Needs

Cycle

Liquidity

Business Considerations:

Strategic Plans

Growth Plans

Management

Business

Structuring Environment

Financial Preferences:

Dilution

Control

Risk Tolerance

Flexibility

Exit Needs

Market Conditions:

Depth

Pricing Requirements

Structural Needs

Cycle

Liquidity

Business Considerations:

Strategic Plans

Growth Plans

Management

Business

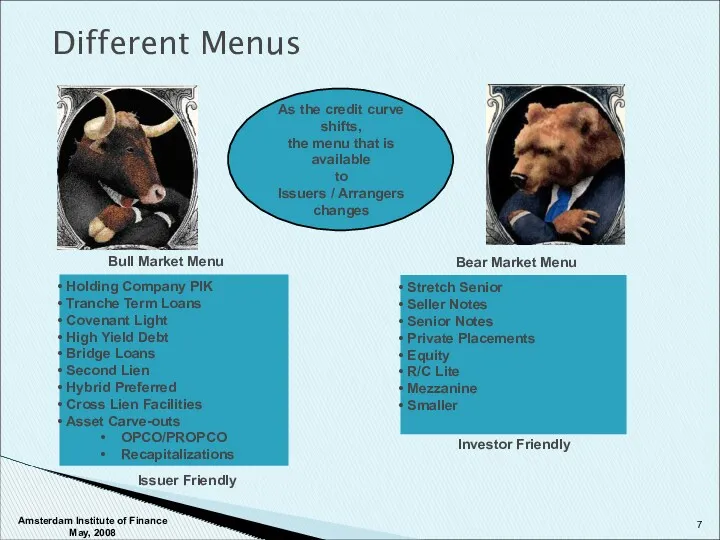

Different Menus

Bull Market Menu

Bear Market Menu

As the credit curve shifts,

the

Different Menus

Bull Market Menu

Bear Market Menu

As the credit curve shifts,

the

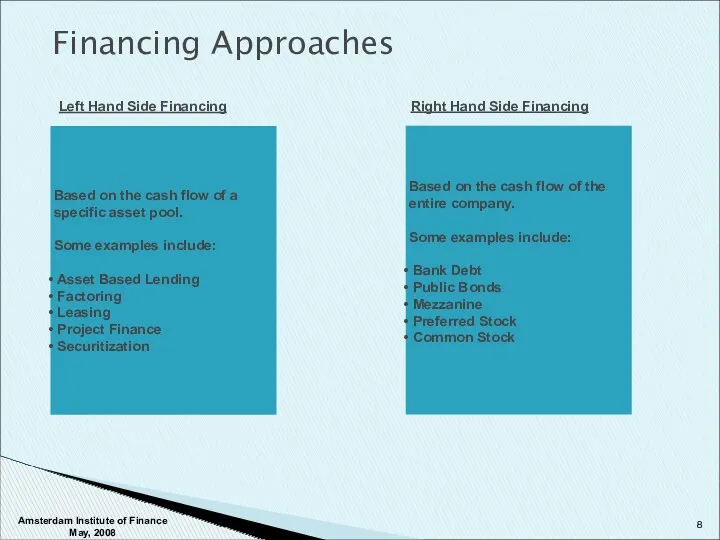

Financing Approaches

Left Hand Side Financing

Right Hand Side Financing

Based on the cash

Financing Approaches

Left Hand Side Financing

Right Hand Side Financing

Based on the cash

Perspective

Amsterdam Institute of Finance May, 2008

Perspective

Amsterdam Institute of Finance May, 2008

Capital Market Specific Factors

Credit Specific Factors

Customer Objectives

Valuation

Structuring Perspective

Amsterdam Institute of Finance

Capital Market Specific Factors

Credit Specific Factors

Customer Objectives

Valuation

Structuring Perspective

Amsterdam Institute of Finance

Acceptable leverage levels

Interest Rate

Amortization

Acceptable tenor of senior debt

Asset coverage

Size of issue

Market

Acceptable leverage levels

Interest Rate

Amortization

Acceptable tenor of senior debt

Asset coverage

Size of issue

Market

Public Debt vs. Private Debt

Relative Value Analysis

Domestic vs. International Issuance

Fixed vs.

Public Debt vs. Private Debt

Relative Value Analysis

Domestic vs. International Issuance

Fixed vs.

Amount of available cash flow

Reliability of cash flow

Credibility of projections

Credit Specific

Amount of available cash flow

Reliability of cash flow

Credibility of projections

Credit Specific

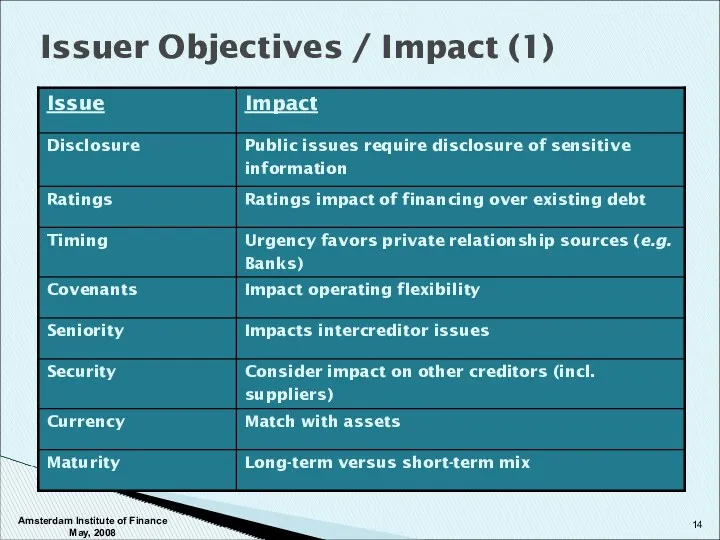

Issuer Objectives / Impact (1)

Amsterdam Institute of Finance May, 2008

Issuer Objectives / Impact (1)

Amsterdam Institute of Finance May, 2008

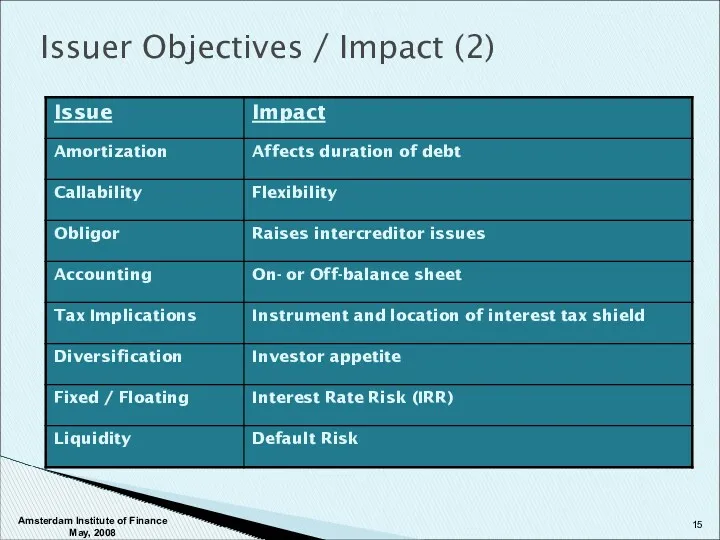

Issuer Objectives / Impact (2)

Amsterdam Institute of Finance May, 2008

Issuer Objectives / Impact (2)

Amsterdam Institute of Finance May, 2008

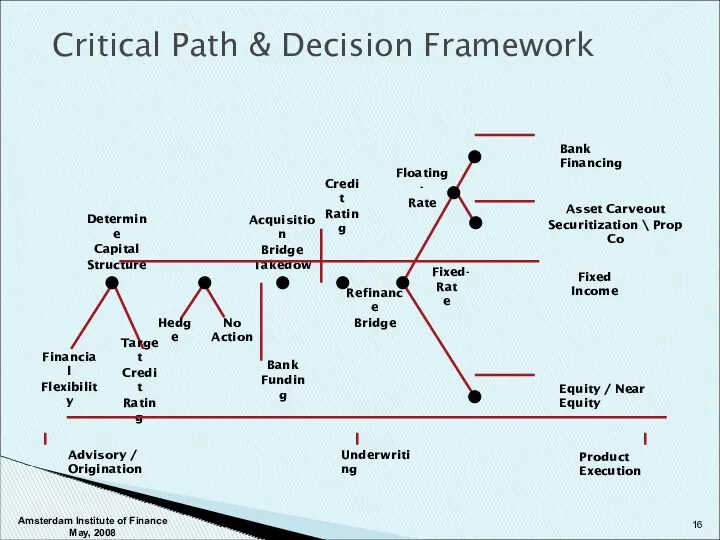

Critical Path & Decision Framework

Financial

Flexibility

Target

Credit

Rating

Determine

Capital

Structure

Hedge

No Action

Bank

Funding

Acquisition

Bridge

Takedown

Credit

Rating

Fixed Income

Asset Carveout

Securitization \

Critical Path & Decision Framework

Financial

Flexibility

Target

Credit

Rating

Determine

Capital

Structure

Hedge

No Action

Bank

Funding

Acquisition

Bridge

Takedown

Credit

Rating

Fixed Income

Asset Carveout

Securitization \

Creating the Structure

Amsterdam Institute of Finance May, 2008

Creating the Structure

Amsterdam Institute of Finance May, 2008

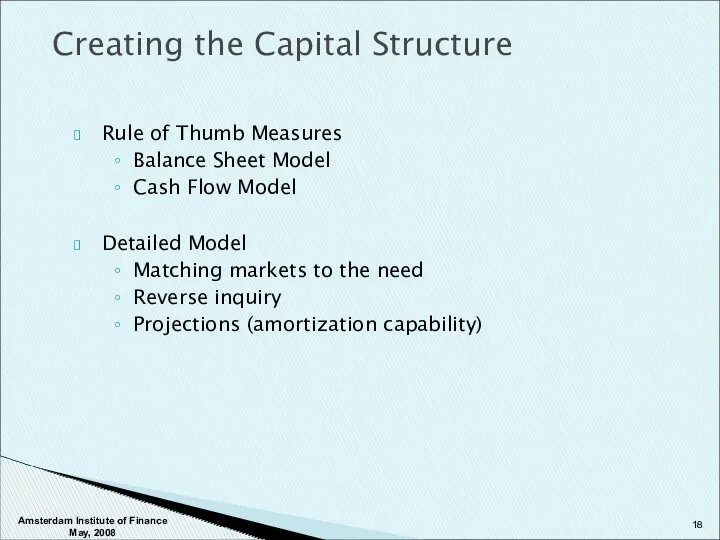

Rule of Thumb Measures

Balance Sheet Model

Cash Flow Model

Detailed Model

Matching markets to

Rule of Thumb Measures

Balance Sheet Model

Cash Flow Model

Detailed Model

Matching markets to

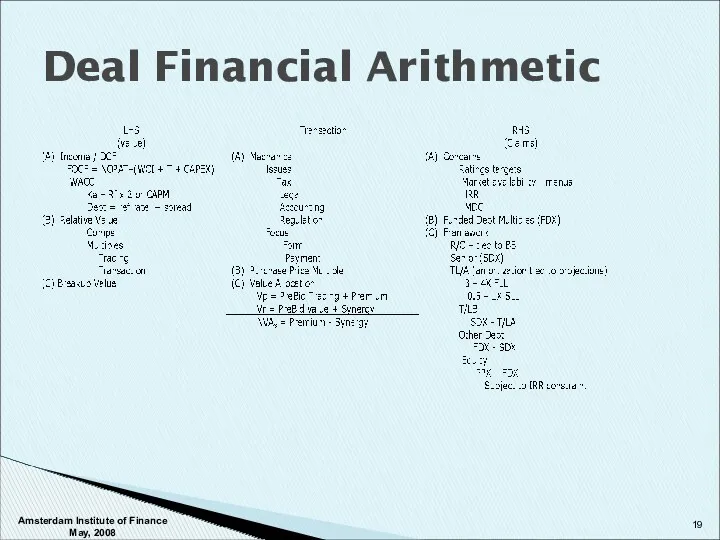

Deal Financial Arithmetic

Amsterdam Institute of Finance May, 2008

Deal Financial Arithmetic

Amsterdam Institute of Finance May, 2008

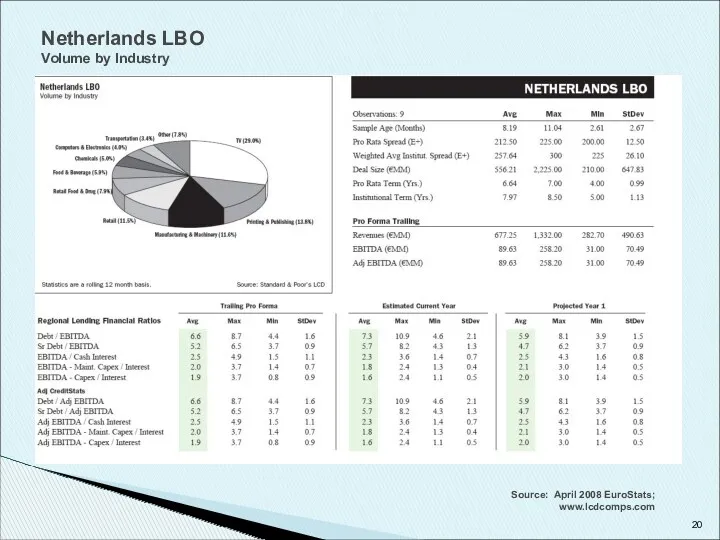

Netherlands LBO

Volume by Industry

Source: April 2008 EuroStats; www.lcdcomps.com

Netherlands LBO

Volume by Industry

Source: April 2008 EuroStats; www.lcdcomps.com

Purchase Price

Minimum/Maximum

Recapitalization Dividend

Debt Refinancing

Callability

Premiums

Tax Issues

Expenses

Other Uses

Financing Need As a Starting Point

Amsterdam

Purchase Price

Minimum/Maximum

Recapitalization Dividend

Debt Refinancing

Callability

Premiums

Tax Issues

Expenses

Other Uses

Financing Need As a Starting Point

Amsterdam

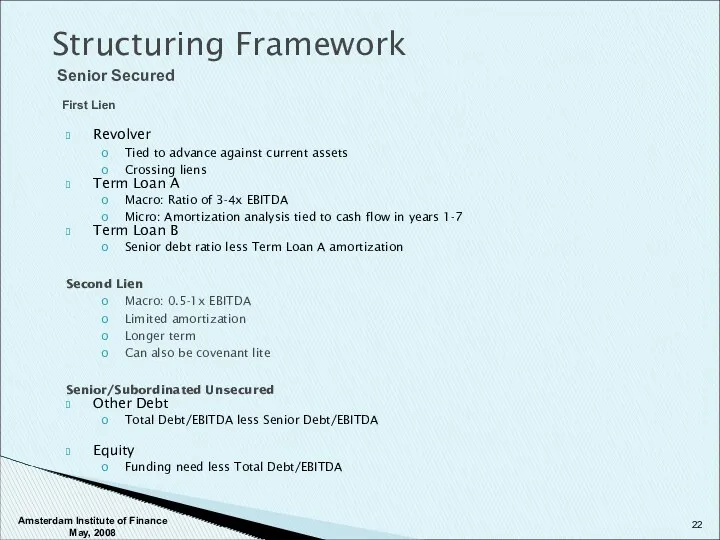

Revolver

Tied to advance against current assets

Crossing liens

Term Loan A

Macro: Ratio of

Revolver

Tied to advance against current assets

Crossing liens

Term Loan A

Macro: Ratio of

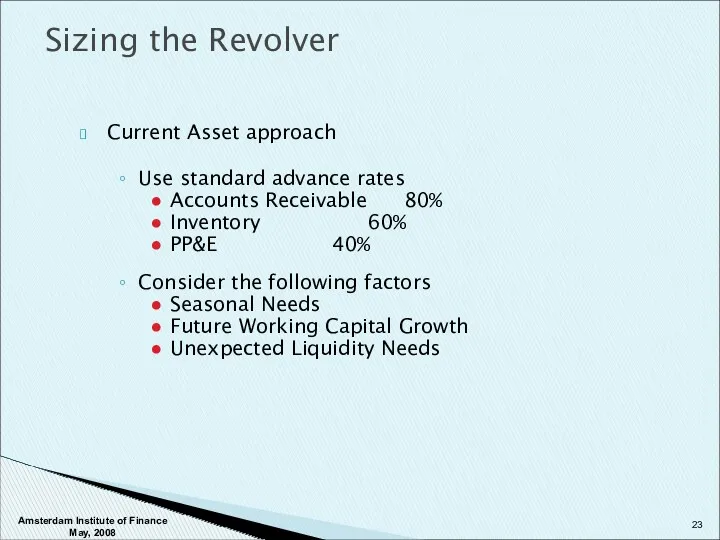

Current Asset approach

Use standard advance rates

Accounts Receivable 80%

Inventory 60%

PP&E 40%

Consider the

Use standard advance rates

Accounts Receivable 80%

Inventory 60%

PP&E 40%

Consider the

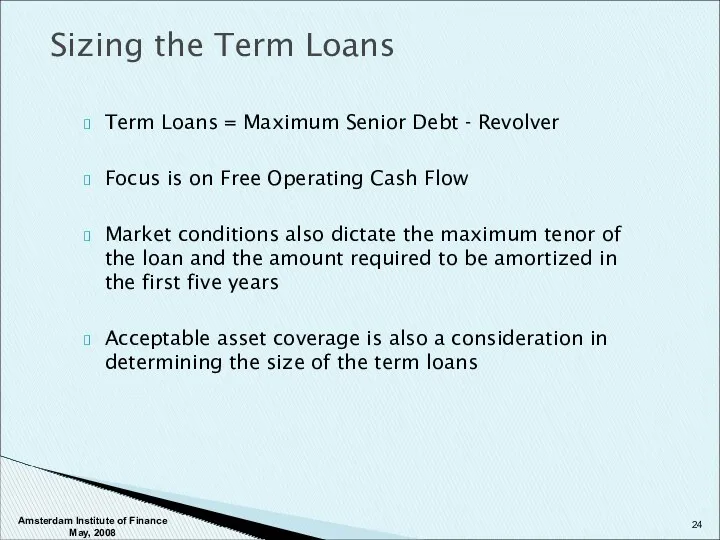

Term Loans = Maximum Senior Debt - Revolver

Focus is on Free

Term Loans = Maximum Senior Debt - Revolver

Focus is on Free

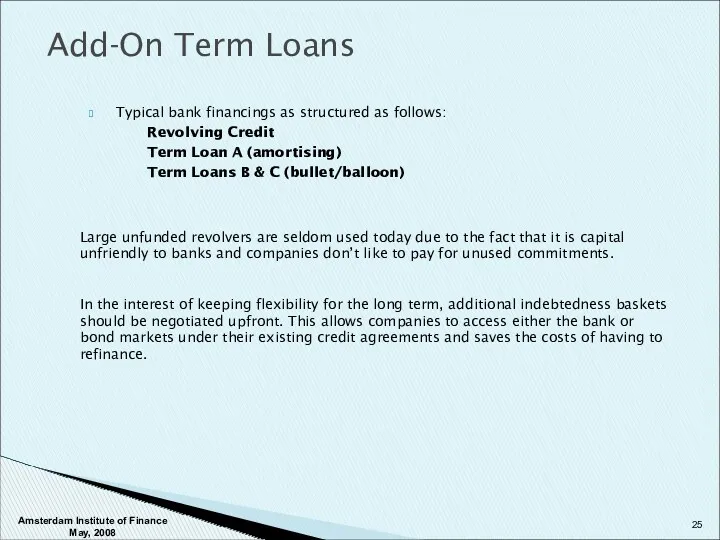

Typical bank financings as structured as follows:

Revolving Credit

Term Loan A (amortising)

Term

Typical bank financings as structured as follows:

Revolving Credit

Term Loan A (amortising)

Term

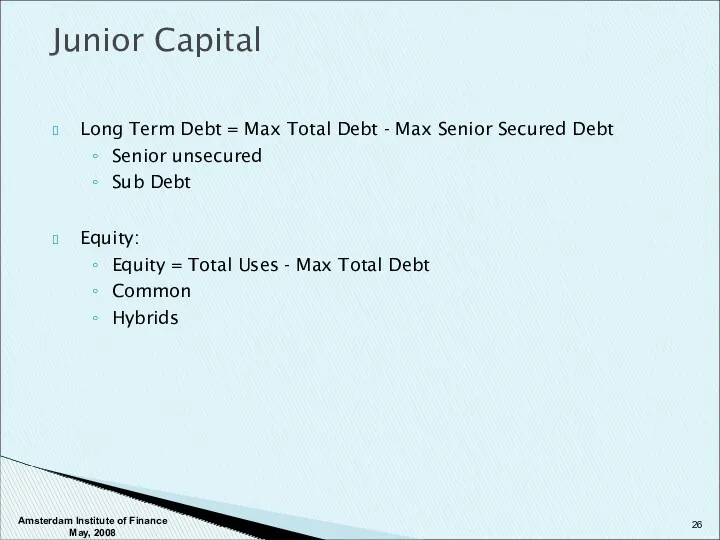

Long Term Debt = Max Total Debt - Max Senior Secured

Long Term Debt = Max Total Debt - Max Senior Secured

Subordination

Senior lenders are concerned with the implications of having high

Subordination

Senior lenders are concerned with the implications of having high

Contractual Subordination

Holding Company

Intermediate Holding Company

Operating Company

Operating Company

Operating

Company

100% Equity

Interest

Issues

Issues

High Yield Bonds

Subordination

Agreement

Senior

Contractual Subordination

Holding Company

Intermediate Holding Company

Operating Company

Operating Company

Operating

Company

100% Equity

Interest

Issues

Issues

High Yield Bonds

Subordination

Agreement

Senior

Structural Subordination

Holding Company

Intermediate Holding Company

Operating Company

Operating Company

Operating

Company

100% Equity

Interest

Issues

Issues

High Yield Bonds

Support

Structural Subordination

Holding Company

Intermediate Holding Company

Operating Company

Operating Company

Operating

Company

100% Equity

Interest

Issues

Issues

High Yield Bonds

Support

Retranche

Increase Pricing

Lower Leverage

Lower Purchase Price

Seller Paper

Increase Equity

Senior Notes to cover Amortizing

Retranche

Increase Pricing

Lower Leverage

Lower Purchase Price

Seller Paper

Increase Equity

Senior Notes to cover Amortizing

Covenants

Amsterdam Institute of Finance May, 2008

Covenants

Amsterdam Institute of Finance May, 2008

PURPOSE: maintain the original deal

WHY

Agency problem due to asymmetric information

Adverse Selection

Moral

PURPOSE: maintain the original deal

WHY

Agency problem due to asymmetric information

Adverse Selection

Moral

Categories

Affirmative

The maintenance, preservation and insurance of corporate assets and the compliance

Categories

Affirmative

The maintenance, preservation and insurance of corporate assets and the compliance

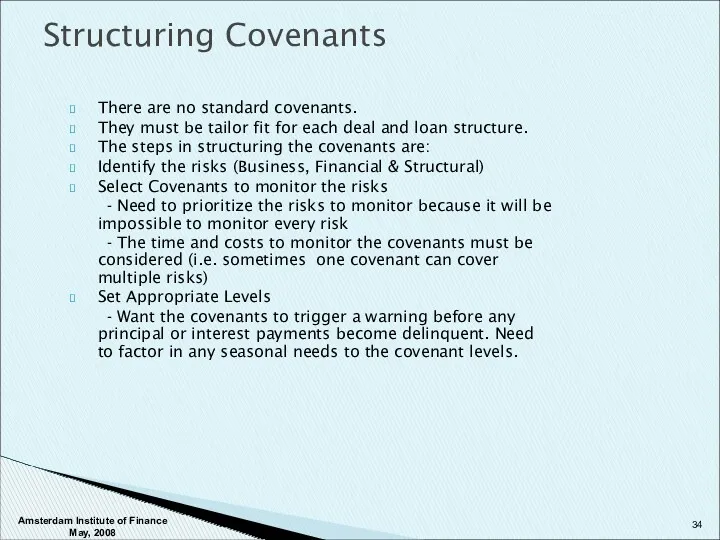

There are no standard covenants.

They must be tailor fit for

There are no standard covenants.

They must be tailor fit for

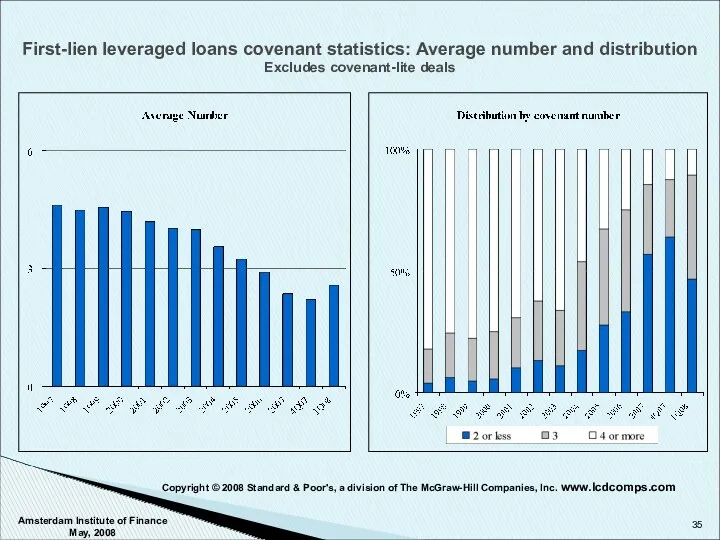

First-lien leveraged loans covenant statistics: Average number and distribution

Excludes covenant-lite

First-lien leveraged loans covenant statistics: Average number and distribution Excludes covenant-lite

Amsterdam Institute of Finance May, 2008

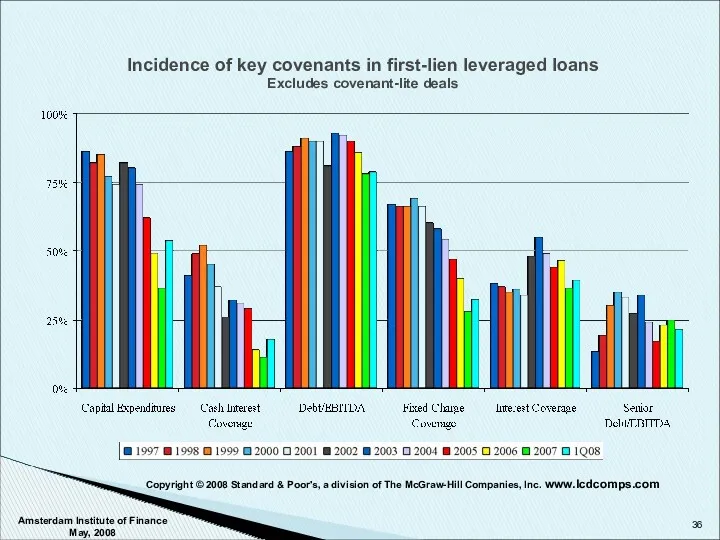

Incidence of key covenants in first-lien

Amsterdam Institute of Finance May, 2008

Incidence of key covenants in first-lien

Amsterdam Institute of Finance May, 2008

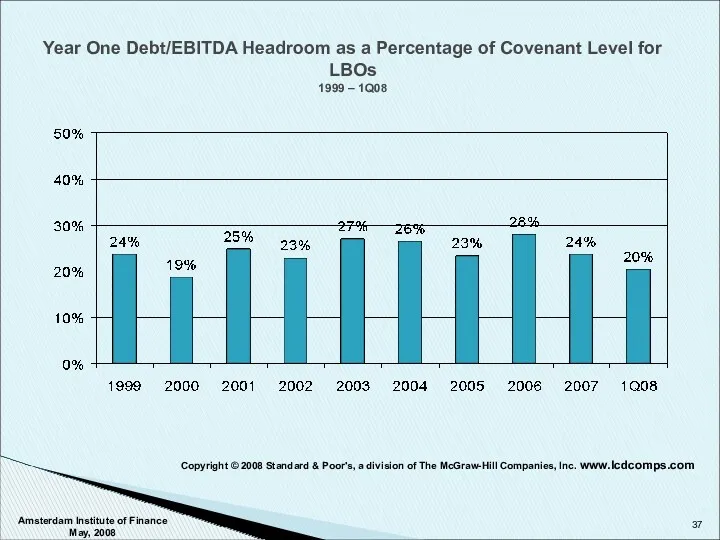

Year One Debt/EBITDA Headroom as a

Amsterdam Institute of Finance May, 2008

Year One Debt/EBITDA Headroom as a

Amsterdam Institute of Finance May, 2008

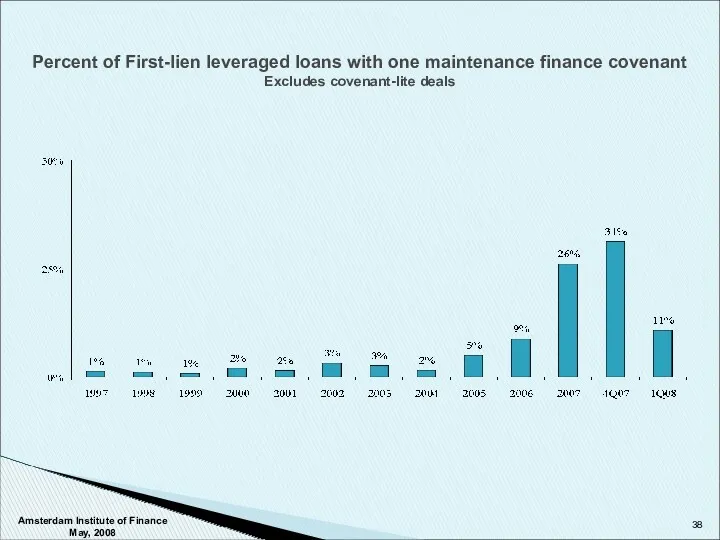

Percent of First-lien leveraged loans with

Amsterdam Institute of Finance May, 2008

Percent of First-lien leveraged loans with

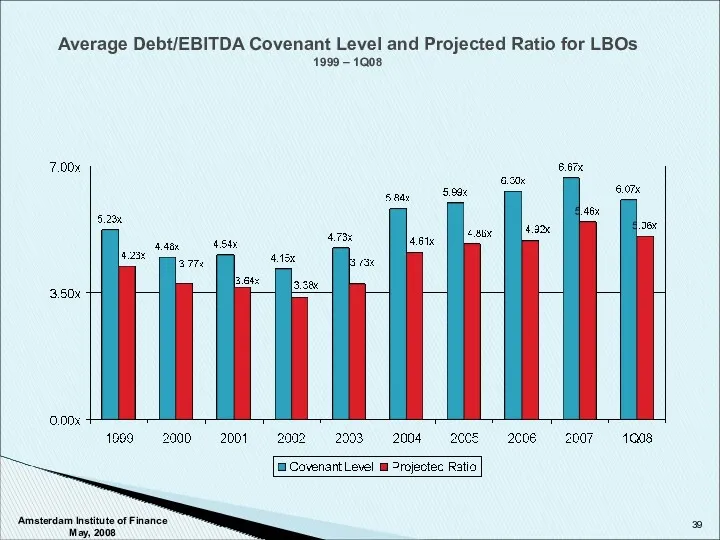

Average Debt/EBITDA Covenant Level and Projected Ratio for LBOs

1999 – 1Q08

Amsterdam

Average Debt/EBITDA Covenant Level and Projected Ratio for LBOs

1999 – 1Q08

Amsterdam

Covenant Levels and Issues

Covenants are negotiated between the lender and borrower.

Covenant

Covenant Levels and Issues

Covenants are negotiated between the lender and borrower.

Covenant

Translating Capital Structure and Debt Capacity into a Detailed Financing Structure.

Conclusion

Amsterdam

Translating Capital Structure and Debt Capacity into a Detailed Financing Structure.

Conclusion

Amsterdam

Project Gear

Amsterdam Institute of Finance May, 2008

Project Gear

Amsterdam Institute of Finance May, 2008

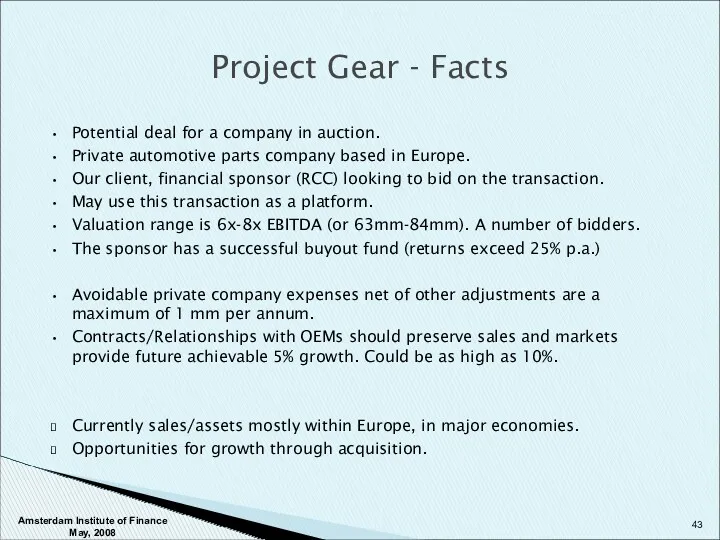

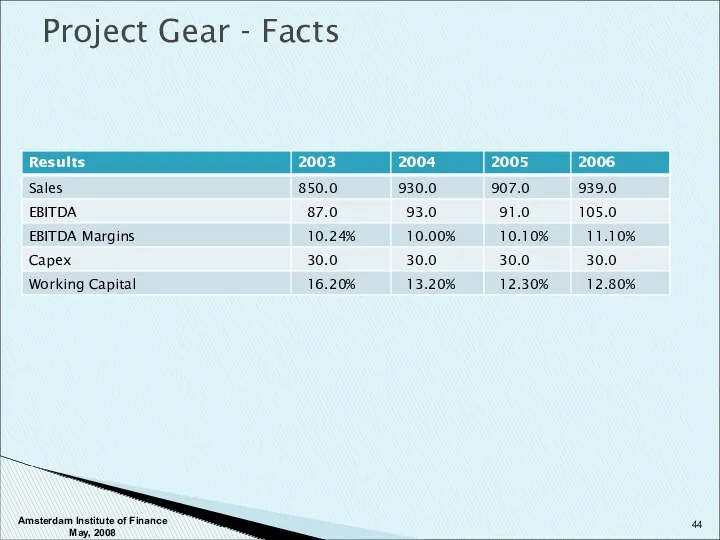

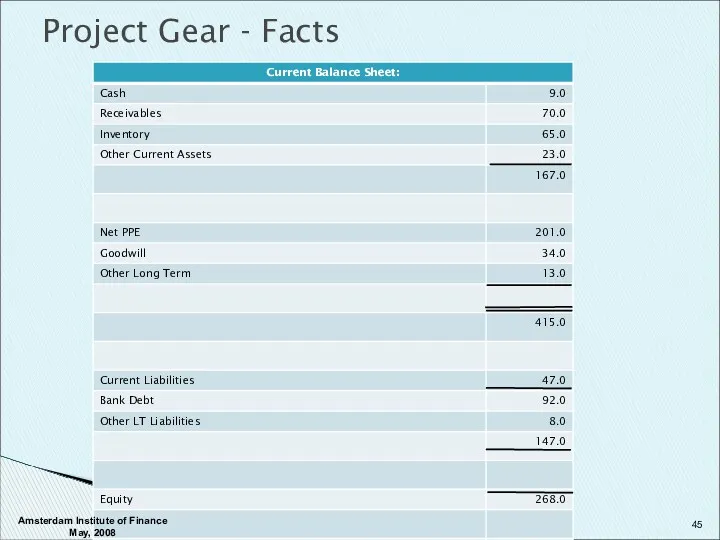

Project Gear - Facts

Potential deal for a company in auction.

Private automotive

Project Gear - Facts

Potential deal for a company in auction.

Private automotive

Project Gear - Facts

Amsterdam Institute of Finance May, 2008

Project Gear - Facts

Amsterdam Institute of Finance May, 2008

Project Gear - Facts

Amsterdam Institute of Finance May, 2008

Project Gear - Facts

Amsterdam Institute of Finance May, 2008

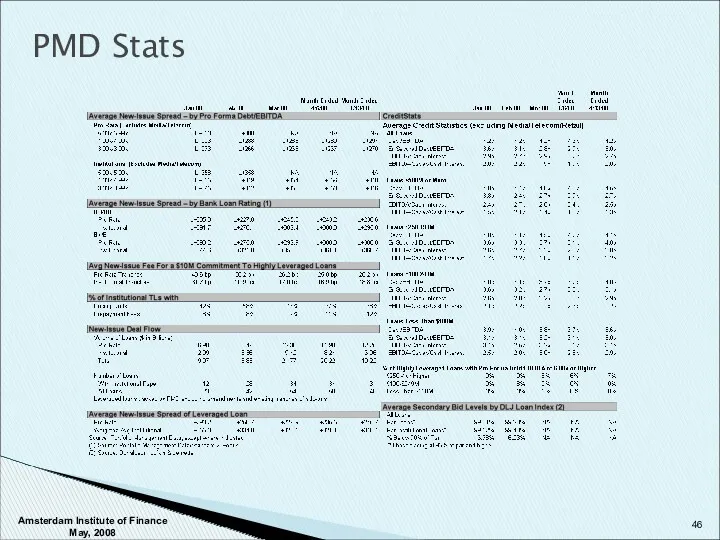

PMD Stats

Amsterdam Institute of Finance May, 2008

PMD Stats

Amsterdam Institute of Finance May, 2008

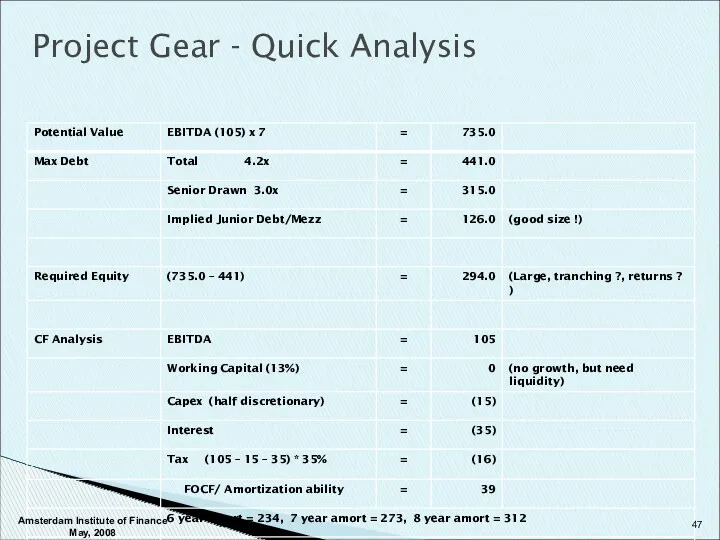

Project Gear - Quick Analysis

Amsterdam Institute of Finance May, 2008

Project Gear - Quick Analysis

Amsterdam Institute of Finance May, 2008

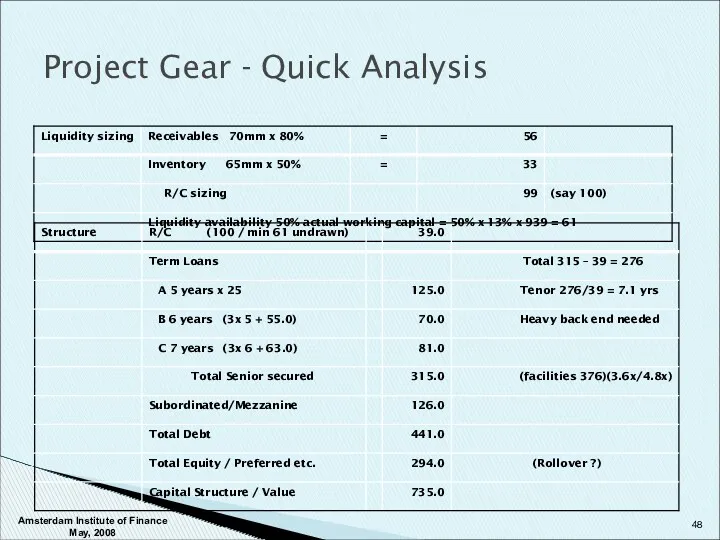

Project Gear - Quick Analysis

Amsterdam Institute of Finance May, 2008

Project Gear - Quick Analysis

Amsterdam Institute of Finance May, 2008

Project Gear - Base Case

Assumptions : 8 % growth

Margins gradually improve to

Project Gear - Base Case

Assumptions : 8 % growth

Margins gradually improve to

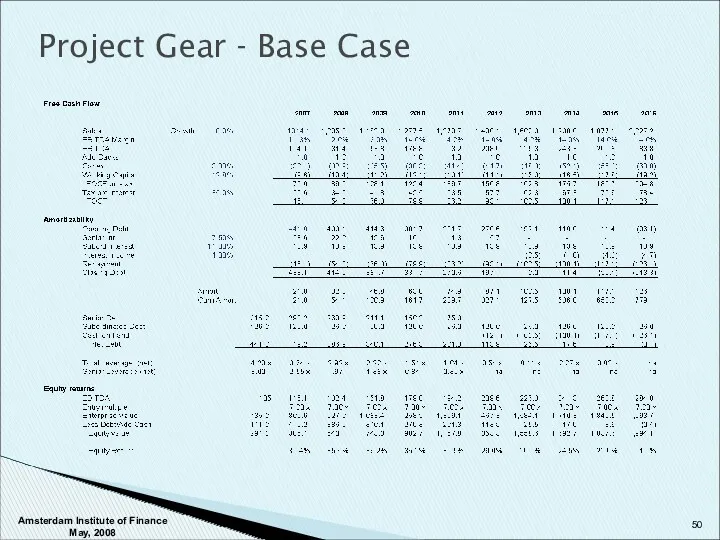

Project Gear - Base Case

Amsterdam Institute of Finance May, 2008

Project Gear - Base Case

Amsterdam Institute of Finance May, 2008

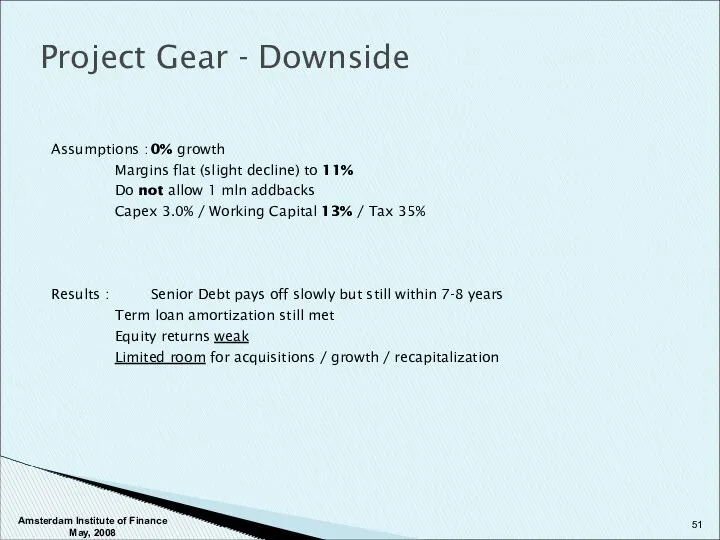

Project Gear - Downside

Assumptions : 0% growth

Margins flat (slight decline) to 11%

Do

Project Gear - Downside

Assumptions : 0% growth

Margins flat (slight decline) to 11%

Do

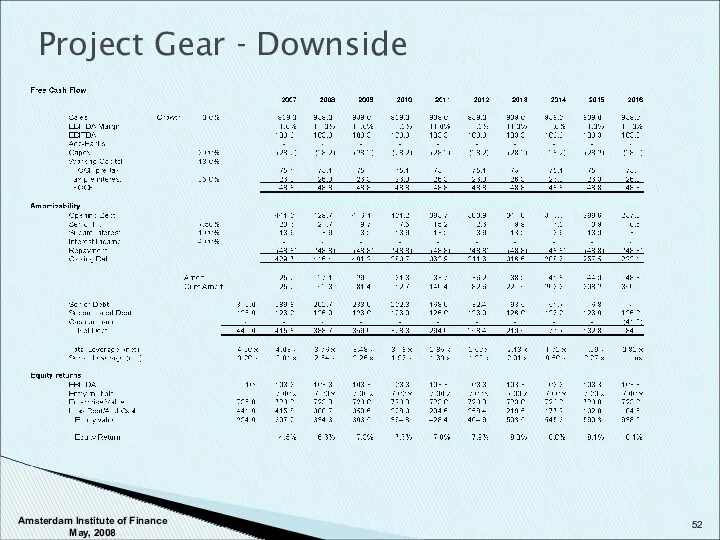

Project Gear - Downside

Amsterdam Institute of Finance May, 2008

Project Gear - Downside

Amsterdam Institute of Finance May, 2008

Project Gear - Worst Case

Assumptons : 0% growth AND LBO/other causes lead

Project Gear - Worst Case

Assumptons : 0% growth AND LBO/other causes lead

Project Gear - Worst Case

Amsterdam Institute of Finance May, 2008

Project Gear - Worst Case

Amsterdam Institute of Finance May, 2008

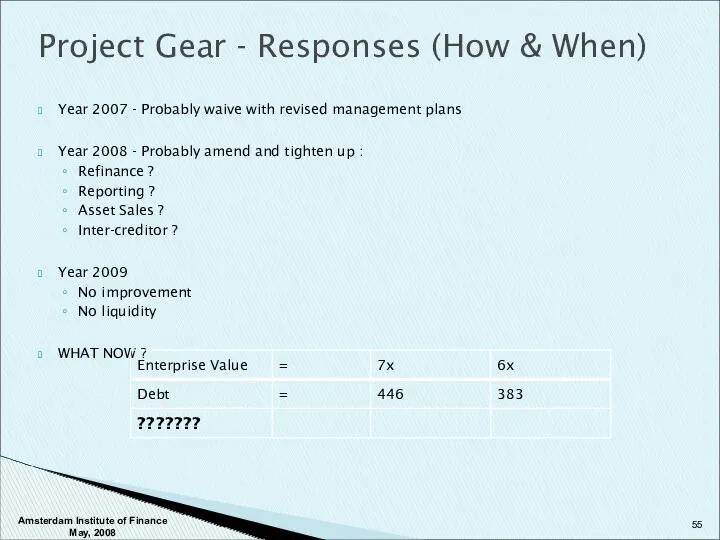

Project Gear - Responses (How & When)

Year 2007 - Probably waive

Project Gear - Responses (How & When)

Year 2007 - Probably waive

Сутність грошей та їх функції. Теорії грошей. (Тема 1)

Сутність грошей та їх функції. Теорії грошей. (Тема 1) Финансовые ресурсы предприятия и их источники, направления и использование

Финансовые ресурсы предприятия и их источники, направления и использование Мошенничество на рынке ценных бумаг

Мошенничество на рынке ценных бумаг Платежные сервисы. Применение ККТ в сфере ЖКХ

Платежные сервисы. Применение ККТ в сфере ЖКХ Контрольно-счетная палата Москвы

Контрольно-счетная палата Москвы Методы продаж банковских продуктов и услуг

Методы продаж банковских продуктов и услуг Жалақы қорынан міндетті ақша ұстап қалу. Жалақыны есептеу тәртібі

Жалақы қорынан міндетті ақша ұстап қалу. Жалақыны есептеу тәртібі Что такое деньги. 3 класс

Что такое деньги. 3 класс Сущность и формы кредита. Тема 4

Сущность и формы кредита. Тема 4 Личные финансы: от экономии к инвестициям. Непостоянные доходы

Личные финансы: от экономии к инвестициям. Непостоянные доходы Заполнение налоговой декларации

Заполнение налоговой декларации Трейдинг как привилегия

Трейдинг как привилегия Оценка эффективности коммерческой деятельности предприятия

Оценка эффективности коммерческой деятельности предприятия The finances of the company. Financial statements of the company

The finances of the company. Financial statements of the company ТАС Family - финансовая защита бюджета семьи

ТАС Family - финансовая защита бюджета семьи Лекция 2. Классификация инвестиций

Лекция 2. Классификация инвестиций Анализ тенденций развития валютного рынка

Анализ тенденций развития валютного рынка Халықаралық валюта жүйесі

Халықаралық валюта жүйесі Деньги, инфляция, процентные ставки, валютный курс

Деньги, инфляция, процентные ставки, валютный курс Налог на добавленную стоимость

Налог на добавленную стоимость Налоги и вычеты

Налоги и вычеты Финансовые коэффициенты

Финансовые коэффициенты Оценка финансового состояния организации (на примере ООО Агромашснаб г. Черкесска)

Оценка финансового состояния организации (на примере ООО Агромашснаб г. Черкесска) Инвестиционная безопасность коммерческой организации

Инвестиционная безопасность коммерческой организации Финансовое планирование и методы прогнозирования

Финансовое планирование и методы прогнозирования Фундаментальный анализ ценных бумаг

Фундаментальный анализ ценных бумаг Что поменять в учете из-за новых стандартов: ФСБУ Аренда

Что поменять в учете из-за новых стандартов: ФСБУ Аренда Монетарная политика

Монетарная политика